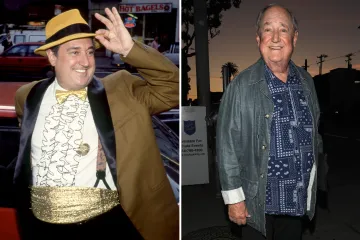

Lizzie McGuire star Robert Carradine tragically ‘found hanged’ aged 71 as tributes pour in for actor

BELOVED actor Robert Carradine’s death has been ruled a suicide, as tear-jerking tributes pour in for the late star.

The Lizzie McGuire lead tragically died on Tuesday following a decades-long battle with bipolar disorder.

Citing the Los Angeles County Medical Examiner’s Office, Page-Six reported the cause of Carradine’s death was sequelae of an anoxic brain injury resulting from hanging.

Sequelae are conditions resulting from a prior disease, injury, or attack.

Robert’s body has been released to his family.

“It is with profound sadness that we must share that our beloved father, grandfather, uncle, and brother Robert Carradine has passed away,” the family said in statement announcing the heartbreaking news.

“In a world that can feel so dark, Bobby was always a beacon of light to everyone around him.

“We are bereft at the loss of this beautiful soul and want to acknowledge Bobby’s valiant struggle against his nearly two-decade battle with Bipolar Disorder.

“We hope his journey can shine a light and encourage addressing the stigma that attaches to mental illness.”

Older brother and fellow actor Keith Carradine added that the family wished to shed light on Robert’s condition and bring awareness to mental health.

Most read in Entertainment

Robert was first diagnosed with the illness after his brother David died by asphyxiation in 2009.

“We want people to know it, and there is no shame in it,” Keith said.

“It is an illness that got the best of him, and I want to celebrate him for his struggle with it, and celebrate his beautiful soul.

“He was profoundly gifted, and we will miss him every day.

“We will take solace in how funny he could be, how wise and utterly accepting and tolerant he was. That’s who my baby brother was.”

Robert got his big break with a role in Revenge of The Nerds in 1984, starring as head nerd, Lewis Skolnick.

He went on to find a new generation of fans starring in Disney Channel’s Lizzie McGuire, as Sam McGuire, dad of the title character.

His co-star Hilary Duff released a heartbreaking tribute to the actor, writing that she “always felt so cared for by my on-screen parents”.

She wrote in a tearjerking Instagram post: “This one hurts. It’s really hard to face this reality about an old friend.

“There was so much warmth in the McGuire family and I always felt so cared for by my on-screen parents.

How to get help

EVERY 90 minutes in the UK a life is lost to suicide

It doesn’t discriminate, touching the lives of people in every corner of society – from the homeless and unemployed to builders and doctors, reality stars and footballers.

It’s the biggest killer of people under the age of 35, more deadly than cancer and car crashes.

And men are three times more likely to take their own life than women.

Yet it’s rarely spoken of, a taboo that threatens to continue its deadly rampage unless we all stop and take notice, now.

If you, or anyone you know, needs help dealing with mental health problems, the following organisations provide support:

“I’ll be forever grateful for that. I’m deeply sad to learn Bobby was suffering.

“My heart aches for him, his family, and everyone who loved him.”

Robert’s daughter, Ever Carradine, shared an emotional statement on Instagram, writing that the late actor “was all heart”.

She wrote: “My sweet, funny dad, who’s only 20 years older than I am, who never missed an opportunity to drive me to the airport or tell me how much he loved my homemade salad dressing, is gone.

“Whenever anyone asks me how I turned out so normal, I always tell them it’s because of my dad.

“I knew my dad loved me, I knew it deep in my bones, and I always knew he had my back.”

Ever added: “My dad was a lover, not a fighter. He was all heart, and in a world so full of conflict and division, I think we can all take a page out of his book today, open our hearts and feel and share the love.”

Robert was born in Los Angeles to actress and artist Sonia Sorel and actor John Carradine.

He began acting as a child star, appearing in The Cowboys with John Wayne in 1972.

The late actor is survived by three children and his brother Keith, who is known for playing Tom Frank in the 1975 film Nashville.

If you or someone you know is affected by any of the issues raised in this story, call or text the 988 Suicide & Crisis Lifeline at 988, chat on 988lifeline.org, or text Crisis Text Line at 741741.

Column: Fall of Kabul may not mean end of U.S. global power

WASHINGTON — Amid the chaos in Kabul, politicians and pundits have declared the Taliban’s victory in Afghanistan a defeat from which U.S. influence may never recover.

“Biden’s credibility is now shot,” wrote Gideon Rachman, chief oracle of Britain’s Financial Times.

“A grave blow to America’s standing,” warned the Economist.

But take a deep breath and remember some history.

When South Vietnam collapsed after a war that involved four times as many U.S. troops, many drew the same conclusion: The age of U.S. global power was over.

Less than 15 years later, the Berlin Wall came down, the Cold War began to end, and the United States soon stood as the world’s only superpower.

The lesson: A debacle like the defeat in Kabul — or the one in Saigon two generations earlier — doesn’t always prevent a powerful country from marshaling its resources and succeeding.

I’m not dismissing the tragedy that has befallen the Afghans or the damage that U.S. credibility has suffered. When President Biden told a news conference that he had “seen no questioning of our credibility from allies,” he sounded as if he was in denial — or, perhaps worse, out of touch.

No questioning? How about the question from Tobias Ellwood, chairman of the British Parliament’s defense committee: “Whatever happened to ‘America is back’?”

Or the complaint from Armin Laschet, the German conservative who could be his country’s leader after elections next month: “The greatest debacle NATO has experienced since its founding.”

Whether he likes it or not, Biden has repair work to do.

The first step, already underway, is making sure the endgame in Kabul doesn’t get any worse.

That means keeping U.S. troops on the ground until every American is out, as Biden has promised. It also requires an energetic effort to evacuate Afghans who worked with the U.S. government and other institutions, even if that requires risking the lives of some American troops. Those Afghans trusted us; if we abandon them, it will be a long time before we can credibly ask the same of anyone else.

And, of course, the administration needs to prevent Al Qaeda and other terrorist groups from replanting themselves in Taliban-ruled Afghanistan. If the United States fails at that — the original reason we invaded the country almost 20 years ago — Biden’s decision to withdraw will justly be judged a fiasco.

There’s repair work to do beyond Afghanistan, too.

“We’ve got to show that it would be wrong to see American foreign policy through the lens of Afghanistan,” Richard N. Haass, president of the nonpartisan Council on Foreign Relations and a former top State Department official, told me.

The United States has more important interests that need attention and allies that need reassurance, he said.

“The most important thing is to deter our major foes,” he said, referring to China, Russia and Iran.

“This is a moment to strengthen forces in Europe, mount more freedom of navigation operations [by the U.S. Navy] in the South China Sea,” he said. “This is a good time to say we’re serious about our commitment to Taiwan,” which China periodically threatens.

Biden took a step in that direction in his recent interview with ABC’s George Stephanopoulos, listing Taiwan along with South Korea and Japan as places where the U.S. “would respond” to an attack.

If anything, Haass and other foreign policy veterans say, the questions about American credibility are likely to make Biden react more strongly to the next few challenges overseas.

“The most intriguing question is what effect this episode has on Biden’s thinking,” suggested Aaron David Miller of the Carnegie Endowment for International Peace. “Will he think: ‘I’ve got to be tougher with the Iranians now? Do I have to signal to a country like Taiwan that I’m prepared to protect American interests there?’”

But the notion that American influence has been fatally damaged is overblown, he argued.

“There have been many other instances in which U.S. credibility has been diminished, but our phone continues to ring,” Miller said.

Biden and his aides already know most of this. The premises of his foreign policy — reviving U.S. domestic strength, revitalizing U.S. alliances, and focusing on vital interests like China and Russia — provide a foundation for recovery.

“My dad used to have an expression: If everything is equally important to you, nothing is important to you,” the president said last week. “We should be focusing on where the threat is the greatest.”

The test Biden faces now is whether he can execute that strategy — and show that he’s credible where it matters most — more successfully than in his botched withdrawal from an unwinnable war.

Merida Open: Katie Boulter loses to Jasmine Paolini in last eight

Britain’s Katie Boulter was unable to build on a superb start as she lost to Italian top seed Jasmine Paolini in the last eight of the Merida Open.

Against the world number seven in Mexico, Boulter won the first set in 28 minutes without dropping a game.

But errors started to creep in as Paolini went on to win 0-6 6-3 6-3.

Having won only three points on her serve in the opening set, Paolini started the second set strongly, holding for the first time and then breaking to go 3-1 up.

Boulter, who came into the contest on the back of a seven-match winning run, including claiming the Ostrava Open title, broke straight back to love but neither player could hold serve in the next three games.

It was Paolini who held her nerve to take the second set and level the contest.

The 2024 Wimbledon and French Open finalist raced into a 2-0 lead in the decider and, although Boulter broke back and held serve to lead 3-2, the Italian’s confidence grew as she won four games in a row to claim a semi-final spot.

“It was a really tough one – Katie, the first set she was smashing every ball and hitting a winner everywhere,” Paolini told Sky Sports.

“I was telling myself to play more deep in the court and hit the ball harder because I had to raise the level to try and win the match and in the end it worked out.

“I was trying to be calm, to think what I had to do. I think when you’re nervous you can’t find the solutions.”

Spain’s very own sakura: cherry blossom season in the Jerte valley | Spain holidays

It’s late March and the villagers of the Jerte valley in Extremadura, Spain’s wild west, are twitchy – as if they’re hosting a party and wondering if all the guests will show up. The event they’re waiting for is the flowering of the valley’s cherry trees, which number about two million. So far, only a handful – a variety called Royal Tioga – have dared to don their frilly spring frocks. The rest are still clutching their drab grey winter garb.

Predicting the arrival of blossom is always tricky, but thanks to an unseasonably wet March the trees are three weeks late when I visit. With snow still cloaking the surrounding sierras, the tourist office in Cabezuela del Valle, halfway up the valley, is hastily finding alternative activities for the coachloads of blossom-seekers from Madrid. As with any nature-reliant activity, such as whale watching or aurora hunting, timing is challenging. But unlike hit-and-miss spectacles involving wild animals, at least I know the blossoming will happen eventually. (Sadly wildfires later affected parts of the Jerte valley last summer, but thankfully few cherry trees were affected.)

The nation most associated with cherry blossom is, of course, Japan. There, the sakura, or ornamental cherry blossom tree, has for centuries symbolised the transient nature of life, and for a few weeks in springtime, its delicate pink confetti blossom sprinkles streets and temple gardens. Millions join hanami, or flower viewings across the country.

Spain’s display is different. This is a rural spectacle rather than a mostly urban one – and has the big advantage, for me at least, of being a lot closer to the UK. I’ve travelled by train from my Devon village and I’m also hoping the journey might be as fun as the destination.

It is. There’s the sunrise over a milky River Teign as we glide through Teignmouth, and by teatime I’m in Paris, eating a glossy coffee religieuse – doubledecker eclairs that look like nuns in habits – on a sunlit boulevard. A dawn start the next day takes me, via TGV, along the French Riviera, past palm-fringed resorts, onwards to Barcelona and finally to Plasencia, in Extremadura. It’s 11pm, yet the Plaza Mayor in its historic walled heart still echoes to the chatter of animated locals digging into raciones of Iberian ham and paprika-flecked grilled octopus.

Next morning, I ascend the valley to the peaceful village of Jerte and its hospedería – one of Extremadura’s network of hotels which, like the national paradores network, are all housed in restored historic buildings. The squat white-washed building was once a leather-tanning factory, but later became an oil press. My room looks out on the vocal River Jerte, and beyond to hillsides crisscrossed with terraces planted with cherry trees. At least I have a ringside seat as their buds strain to unfurl.

I join the collective waiting game, passing the hours by roaming Jerte’s cobbled streets beneath the geranium-draped balconies of its half-timbered houses. One afternoon I tackle the rugged mountain trail taken by Holy Roman emperor and King of Spain Carlos V to reach the monastery he chose for his retirement in 1556. The poor emperor was so riddled with gout he had to be carried on a sedan chair over the mountains and across a vigorous river at a point now marked by a stone bridge known as the Puente Nuevo. My circuit culminates in the high drama of Los Pilones, a jumble of granite boulders that have been eroded and bleached by the river to form crystalline bowl-shaped pools.

Back in Jerte there are cherry products to sample – from liqueurs to jams and bottled fruit. In the hospedería, a knockout cherry and pistachio dessert rounds off the regional tasting menu – remarkable value at €45. In summer, local people marry cherries with tomatoes to make a variation on gazpacho. Edible cherries, of course, are the big difference between the Jerte and Japan: Japan’s trees are ornamental, whereas the Jerte’s are fruiters, and the main source of income for the valley’s inhabitants. Had I time to linger another couple of months, I could witness the area’s second annual spectacle – trees laden with the lipstick-red fruit. That calls for more festivities so, from a tourism point of view, Jerte has two bites at the cherry.

At the processing factory down the valley towards Plasencia, I see white-coated workers cleaning the machinery, ready to wash, grade and pack Jerte’s cherries from late May to late July. “This is family agriculture,” says Mónica Tierno Díaz, who directs a collective of 15 local cherry farming cooperatives. “Cherries are our way of life. Picking them is how I learned to count as a kid. Most growers in the valley have just a few hectares and pick the cherries by hand into chestnut wooden baskets. But marketing and selling their fruit is difficult. So we do that for them, our key markets being Britain and Germany.”

Alongside commercial varieties, such as Lapins and Van, Jerte produces a small stalkless one called Picota, which is unique to the region and has protected designation of origin certification. Pop into your local supermarket in June and you may well spot these tiny, slightly crunchy jewels. “Many people got used to black gobstopper cherries, so getting them to buy these smaller, paler cherries was a challenge,” says Mónica. “But once people taste them and realise how sweet they are, they’re hooked.”

Next morning, I drive down the valley to the hillside village of El Torno and witness a Jerte transformed; it’s as if snow has silently fallen during the night. The trees have finally put on their floral finery, the party has begun. I explore the orchards on foot – the best way to experience them – following one of the valley’s many well-marked footpaths, and settle beneath the blossom-laden trees for a hanami picnic, Spanish-style. I’m grateful for my early start, for I’m soon joined by a boisterous crowd of blossom-baggers who have followed one of the tourist office’s cherry-viewing driving routes and are now posing for the ultimate floral selfie. As well as El Torno, the 50km motoring circuit takes in neighbouring Rebollar and villages such as Valdastillas, Piornal and Cabrero on the other side of the valley, while the equally spectacular 30km linear route traces the main road down the valley.

With each passing day, the blossom edges up the valley like a frothy white wave, finally reaching the village of Tornavacas at the top. Donning my walking boots again, I head there from Jerte along the Ruta Cerezo en Flor (the cherry blossom trail), and from its mirador (viewpoint), I gaze at the sea of blossom below. (Incidentally, if you tire of blossom-gaping, the tourist office runs a two-week Cherry Blossom festival – part of a six-week spring festival – with an ambitious lineup of events across the valley’s villages, from folk dancing to concerts and exhibitions; 27 March-11 April.) Returning to my hotel in Jerte, I notice the streets and bars are buzzing. Time, I think, for a celebratory tot of the local cherry liqueur.

I’m sad to leave this magical valley. But as I journey home, I console myself that in a few months I’ll hopefully be savouring Jerte’s Picotas at home, a sweet, equally fleeting reminder of Spain’s very own sakura.

The trip was provided by the Extremadura tourist board and the Spanish tourist office in London. The Hospedería Valle del Jerte has doubles from around €135 B&B. Travel was provided by Rail Europe; an Interrail Global pass starts from €318 for five days travel over a month for adults

Korean film revenue, admissions fall 40% in 2025

Moviegoers buy tickets at a CGV theater in Seoul. File. Photo by Yonhap News Agency

Feb. 27 (Asia Today) — Revenue and admissions for South Korean films plunged about 40% in 2025 from a year earlier, according to industry data released Thursday, underscoring ongoing challenges for the domestic box office.

The Korean Film Council said in its annual industry report that total theater revenue reached 1.047 trillion won ($785 million) last year, while total admissions stood at 106.09 million, down 12.4% and 13.8% respectively from 2024.

The industry narrowly maintained the 1 trillion won and 100 million admissions thresholds, helped by a string of late-year hits including “Zombie Daughter,” “F1: The Movie,” “Demon Slayer: Kimetsu no Yaiba – Infinity Castle,” “Zootopia 2” and “Avatar: Fire and Ash.”

However, Korean films alone saw a much steeper decline.

Domestic titles generated 419.1 billion won ($314 million) in revenue and drew 43.58 million viewers, down 39.4% and 39.0% from a year earlier. Their market share fell to around 40%, and no Korean film surpassed 10 million admissions in 2025.

In contrast, foreign films posted revenue of 627.9 billion won ($471 million) and 62.51 million admissions, up 24.7% and 21.0% year-on-year.

Special format screenings such as IMAX and 4D recorded 110 billion won ($82 million) in revenue, up 46.3% from 75.9 billion won the previous year. The average number of cinema visits per person declined to 2.08 from 2.40.

The export value of completed Korean films rose 19.9% to $50.28 million, driven largely by demand in Asian markets including Japan, Taiwan, Indonesia and Vietnam.

The council said overall theater visits declined, but audiences showed a stronger tendency toward selective viewing of major titles, suggesting a more concentrated box office environment.

— Reported by Asia Today; translated by UPI

© Asia Today. Unauthorized reproduction or redistribution prohibited.

Original Korean report: https://www.asiatoday.co.kr/kn/view.php?key=20260227010008420

Bolivian military plane carrying banknotes crashes near capital, killing 20 | Aviation News

Air force plane transporting cash veers off runway and into busy road; crowds scramble for scattered banknotes in the wreckage.

Published On 28 Feb 2026

At least 20 people have been killed and more than 30 injured after a Bolivian Air Force Hercules transport plane, carrying a cargo of newly printed banknotes, crashed onto a busy highway while attempting to land in bad weather near the capital, La Paz.

The military plane was attempting to land on Friday evening at El Alto International Airport when it skidded off the runway and ploughed into a nearby road, local authorities said.

Recommended Stories

list of 4 itemsend of list

“There are about 20, maybe a few more,” Police Colonel Rene Tambo, head of the police homicide division in El Alto, said of the number of people killed.

Defence Minister Marcelo Salinas said the Hercules C-130 “landed and veered off the runway” and came to a stop in a field.

Firefighters responding to the crash successfully extinguished a fire that broke out, the minister said, noting that the cause of the crash remains under investigation.

“A heavy hailstorm” was falling and “there was lightning” when the plane went down, Cristina Choque, a 60-year-old vendor whose car was struck by plane wreckage, told the AFP news agency.

Footage shared on social media showed chaotic scenes as crowds gathered at the crash site.

Some people appeared to collect banknotes scattered among debris from the aircraft, the wrecked vehicles and the bodies of victims.

Authorities used water hoses and tear gas to push back onlookers and looters.

The Ministry of Defence, in a statement, said later that “the money transported in the crashed aircraft has no official serial number… therefore it has no legal or purchasing power”.

The ministry also warned that the “collection, possession, or use” of the money “constitutes a crime”.

Bolivian Air Force General Sergio Lora said that two of the six crew members of the aircraft were still unaccounted for.

The central bank was expected to brief reporters later on Friday regarding the stricken plane’s cargo.

Bolivia’s La Paz, situated at an altitude of 3,650 metres (11,975 feet) and surrounded by Andean mountain peaks, is the highest administrative capital in the world.

Robbie Williams ends feud with Gary Barlow as he emotionally reveals he apologised for his ‘smug’ behaviour

ROBBIE Williams has finally put his feud with Take That bandmate Gary Barlow to bed with a public apology at his War Child gig tonight.

During the intimate concert at Manchester‘s Aviva Studios, Robbie took a moment to reflect on the recent Take That Netflix documentary.

He famously quit the band at the height of their fame in 1995 to pursue a solo career, fed-up of playing second fiddle to the pop group’s leader, Gary.

Years of mud-slinging followed, predominantly from Robbie towards his boyband rival which had a severe impact on Gary’s self-esteem.

Though they quashed their feud for a 2010 reunion tour and album, questions still lingered at just how friendly the pair were.

Today, Robbie did his best to make amends for past behaviours and admitted he was out of order at times to Gary (and Howard Donald and Mark Owen).

READ MORE ON ROBBIE WILLIAMS

“Did anybody see the Take That documentary?,” he asked the audience. “I have to say I was a bit of a ‘c***’ in the second episode. I don’t think anybody has seen a man smugger than Robbie Williams in the second episode.

“And you know what, I felt really bad. I felt f***ing horrible about it. I’d been horrible to Gary, horrible to Mark, horrible to Howard and I was genuinely thinking about it for days and days and days and I’d go to bed at night and I was thinking I’ve gotta apologise again.

“But just to clarify, I f**king love Gary Barlow now. And he loved me. There’s only so many times I can apologise now.”

He then segued into his 90s track Ego A Go Go, written about Gary, calling it a “horrible song”.

Its chorus goes: “Ego a go go now you’ve gone solo/Living on a memory/Now you’ve gone stately/And yes you do hate me/Could you offer an apology.”

Listening to his band rehearse the track on a previous date, Robbie said he had a revelation.

“I was sat there thinking hang on no one has ever left a boyband and gone ‘they’re a c, they’re a c except me’. But I’m a c***,” he said.

In the three-part Netflix docuseries, Gary talks about his struggle with bulimia, which started following Take That’s split in 1996 and his rivalry with Robbie.

Taunts from Robbie are replayed during, with footage showing him saying: “My problem always was with Gary, I wanted to crush him.

“I wanted to crush the memory of the band and I didn’t let go. Even when he was down I didn’t let go.”

Speaking at the premiere at Battersea Power Station, Gary admitted it was tough to watch.

He said: “It’s a narrative I haven’t thought about for years and years.

“When we had our reunion we spent a lot of time talking about it and I remember leaving on one particular day and we’d discussed everything. And I remember leaving and my shoulders were light.

“And I’d not thought about it since because I’d not needed to. And it brought it all back. Tricky times, they were.”

As well as the tough times, Take That fans get a front seat to the inner workings of the group’s comeback with Robbie in 2011.

Opening up about healing their old wounds, Robbie said: “I needed Gary to listen to my truth.”

Gary continued: “There were things around people not being supportive of his songwriting and his weight.

“I’d called him Blobby rather than Robbie one day, which I shouldn’t have done.

“Then I hit him with things he had done to me that I didn’t like.

“In about 25 minutes we’d put things to bed that had haunted us for years.”

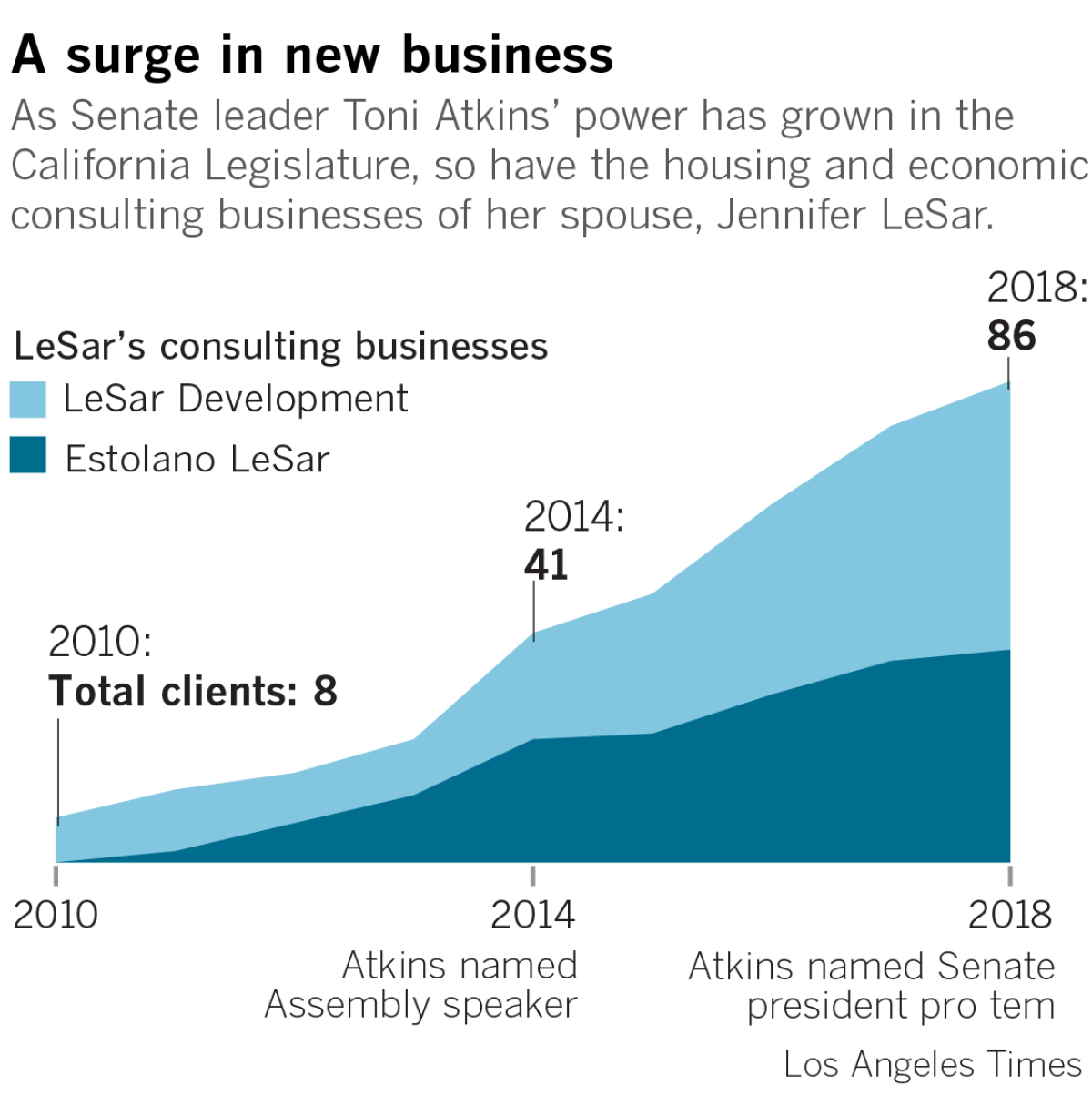

As power of California Senate leader grows, so does her spouse’s consulting business

Reporting from Sacramento — Toni Atkins is one of California’s most powerful lawmakers, ascending to leadership roles in the Assembly and Senate the last five years.

As Atkins’ clout has soared, so too has the consulting businesses of her spouse, Jennifer LeSar.

The clientele for LeSar’s two affordable housing and economic development firms has grown nearly fourfold since 2013, the year before Atkins became Assembly speaker, according to Atkins’ economic disclosure forms.

In 2018, the year that Atkins’ colleagues elevated her to Senate president pro tem, her spouse’s firms had contracts with 86 public agencies, developers, nonprofits and other clients, the forms indicate, which was more than in any previous year. The year before, LeSar had received a lucrative contract from a Bay Area agency without going through a competitive bidding process — a rare step allowed in emergencies, when a company offers a unique service or when the agency can justify a compelling reason to do so.

LeSar is now in a position to potentially garner even more business as Gov. Gavin Newsom and legislative leaders, including her spouse, propose increasingly bold responses to the state’s housing affordability crisis.

In the last three years, LeSar’s firms have received $1.3 million from state agencies alone, including contracts to implement one of the state’s largest low-income housing programs, which Atkins, a Democrat from San Diego, supports. Additionally, over the last 18 months, LeSar worked on a plan that calls for a package of state legislation that would rewrite major California housing policies. The Metropolitan Transportation Commission, a Bay Area public agency, is paying LeSar’s firm more than half a million dollars for the effort, through the no-bid contract.

Agency executives said LeSar’s relationship with Atkins had no bearing on their decision to hire her, and the Senate leader said she wouldn’t treat the bills any differently than any other proposals from her colleagues.

Atkins and LeSar, who has worked in affordable housing for nearly three decades, both said they are concerned about a perception of conflicts of interest and, as a result, consult with attorneys about possible intersections in their work.

“We spend a lot of time trying to make sure in our very busy days that we’re following the letter of the law,” Atkins said.

“These questions have been asked and answered before by the press and have largely been accepted as a nonissue,” LeSar said in an email response to The Times. She declined an interview request.

Rey Lopez-Calderon, executive director of the government ethics group California Common Cause, said the dramatic increase in LeSar’s clientele could raise concerns from the public that outside groups are trying to curry favor with a powerful politician by hiring her spouse.

“That’s really obviously a number that’s eyebrow raising,” Lopez-Calderon said. “It definitely runs the risk of the public thinking something shady is going on.”

Still, he said, absent evidence LeSar or Atkins used their relationship to leverage new business, there wasn’t anything illegal or unethical about LeSar’s consulting work.

Source: State Sen. Toni Atkins’ Annual Statements of Economic Interest

(Kyle Kim / Los Angeles Times)

Lawmakers have faced questions about potential conflicts involving a spouse and development issues before. In 2011, opponents of redevelopment agencies, which provided significant funding for low-income housing, criticized then-state Sen. Bob Huff about his efforts to save the program, noting that Huff’s wife was a paid consultant for a developer with a financial stake in the issue.

Political rivals have alleged Atkins’ relationship with LeSar is also a conflict, given Atkins’ outsized role in housing debates. In 2015, Atkins, then in the Assembly, proposed legislation to impose a fee on real estate transactions, such as mortgage refinancing, to fund low-income housing development. A version of the bill passed in 2017. When she first introduced the measure, Atkins requested an opinion from the Office of Legislative Counsel, which assured her that the bill presented no conflict of interest because the funding was not tied to any specific company or project. LeSar has vowed not to bid on funding directly tied to the bill.

Assembly leader Toni Atkins denies conflict of interest in funds proposal »

The couple married in 2008 after meeting while running in housing, LGBT advocacy and political circles in San Diego, where Atkins once served as a city councilwoman. Just before her election to the Legislature, Atkins worked for LeSar Development for about 18 months. While there, she wrote a report on development near transit and handled other housing work across the state. As of last month, Atkins was pictured on the business’ website, listed as an alumna of the firm. She no longer appears on a redesign of the site that became public Wednesday.

In 2011, after Atkins had been elected to the Legislature, LeSar opened a second firm, Estolano LeSar Advisors, with Cecilia Estolano, an attorney who worked in housing and economic development for the city of Los Angeles. Last year, Atkins abstained from voting on Estolano’s appointment to the powerful UC Board of Regents, which governs the state’s flagship university system.

Recent clients for the two firms, according to Atkins’ economic disclosures, have included the city and county of Los Angeles, UC Berkeley, USC, the California Endowment, the Metropolitan Water District of Southern California, for-profit and nonprofit developers and the Open Society Foundations, the organization founded by billionaire George Soros.

Rick Gentry, president of the San Diego Housing Commission, praised LeSar. Among other work, he said, she guided his public housing agency in 2014 into expanding its portfolio to provide homelessness services.

“She knows as much about the industry as anyone I’ve ever met,” Gentry said.

Officials with the Metropolitan Transportation Commission cited LeSar’s experience as their reason for hiring her.

The agency was finishing an effort to plan for growth in the Bay Area through 2040 and realized that project was futile without a comprehensive attempt to deal with the nation’s worst housing affordability challenges.

“Jennifer LeSar is extremely qualified and well-positioned to take on multiple roles for this project,” wrote Vikrant Sood, a senior planner with the Metropolitan Transportation Commission, in a June 2017 memo justifying her hiring.

LeSar’s firm researched prior studies on the region’s housing problems and planned and attended the group’s meetings. The result of the effort was a proposal, known as the CASA Compact, which said the Bay Area could fix its housing problems only through a suite of state legislation.

The CASA Compact calls for new state laws to boost protections for tenants, increase apartment construction near transit and help raise more than $1 billion to build low-income housing, among other things. Bay Area legislators have introduced more than a dozen bills that align with the plan, nearly all of it affecting the entire state.

Metropolitan Transportation Commission officials said LeSar did not recommend any of the policies the region decided to pursue but, rather, packaged together the conclusions into a final report. LeSar also said she declined additional work with MTC once it became clear that the CASA Compact was going to advance state bills.

She said she sought a legal opinion in January after the agency discussed offering her a new contract to help implement the plan.

LeSar initially told The Times that her attorney had advised her that the second contract would be a potential conflict so she declined the work. But in later correspondence with The Times, she said that she had been mistaken. The attorney’s advice, LeSar said, was that the new contract wouldn’t pose a conflict, but she decided to forgo the work to avoid any appearance of a problem.

Commission officials anticipated the CASA Compact process would lead to state legislation from the beginning. Sood said in the June 2017 memo that originally justified LeSar’s hiring that CASA “will yield a package of legislative and funding solutions at the state and regional level.”

Despite that, agency officials decided to pursue LeSar directly rather than putting the initial contract out to a competitive bid, a process designed to ensure an agency receives the best services for the lowest cost and without bias. The agency said it could do so because it had a compelling reason — LeSar’s background and the ambitious nature of the project — to hire her without first seeking out other firms.

No MTC officers publicly opposed hiring LeSar. Following agency rules, then-Executive Director Steve Heminger signed off on the first $200,000 of the contract himself. The agency’s administrative committee, which is made up of Bay Area elected officials, voted unanimously and without comment in December 2017 to increase the amount to $450,000. (The contract value rose to $511,000 when it was extended again at the beginning of this year.)

Some local government officials in the Bay Area’s smaller cities oppose the CASA Compact because they believe it takes away their power. Michael Barnes, a councilman in the city of Albany — a community that borders Berkeley — said LeSar’s extensive work with the MTC over the last 18 months adds to fears that lawmakers, out of deference to Atkins, will overlook local leaders’ concerns when evaluating the legislation.

“We have very strict guidelines for our ethical behavior,” Barnes said. “For me, as someone who has lived under these guidelines as an elected official, this doesn’t seem ethical.”

LeSar’s businesses also have seen an increase in contracts with state agencies, per Atkins’ economic disclosures. Since February 2016, the two firms have received at least nine contracts from four state departments. All but one — a $5,000 contract to advise housing department employees on evaluating loan documents — were awarded through competitive bidding processes.

Much of the contract work has come from the Governor’s Office of Planning and Research, which is responsible for administering housing and planning efforts funded by the state’s cap-and-trade program, which taxes polluters. The state has provided roughly $400 million annually through Affordable Housing and Sustainable Communities program, one of the largest budget allocations for low-income development and one that Atkins has said she “led the effort” in the Legislature to fund. Estolano LeSar was hired to help applicants from disadvantaged communities write grants and provide other support for their projects.

Newsom’s office declined to comment, but Ken Alex, who was OPR director under former Gov. Jerry Brown, said he was unaware of Atkins and LeSar’s relationship.

“I have heard from staff that the work was good and would have been advised if it was not,” Alex said.

Atkins said she has sometimes voted in ways that have hurt her spouse’s business. In 2011, she supported ending the state’s redevelopment program, the property tax set aside for local governments that funded local affordable housing and economic development.

“I was part of a vote that actually almost killed her business for a period of time,” Atkins said.

Atkins said she doesn’t plan to write any of the bills recommended in the CASA Compact proposal. She said she wouldn’t abstain from voting on them or otherwise handle them differently than any other piece of legislation because the bills address broad policy matters and therefore don’t present a conflict.

But if CASA Compact measures pass, it could be a signal to outside groups that hiring LeSar could be beneficial to getting similar efforts through the Legislature, given Atkins’ substantial influence over the fate of legislation at the Capitol, said Lopez-Calderon of Common Cause.

“I definitely think that some businesses will imagine that exact scenario and act accordingly,” he said.

'Everybody knew what they were part of' – Williamson on Euro 2022

Leah Williamson speaks to Kelly Somers on The Football Interview.

Source link

7Pines Resort Sardinia review: The perfect getaway on this Italian island where residents live beyond 100 years old

Writer Becky Ward followed the Blue Zone principles for living a healthy life on a trip to the northern region of the Italian island of Sardinia

This island is one of the world’s five Blue Zones(Image: Getty)

If you’re not familiar with the world’s Blue Zones, they are regions where life expectancy is higher due to the diet and lifestyle habits of the locals. Exercise, stress management and social connections are all thought to play a part, with many residents living beyond 100 years.

One such region is in Sardinia, the Italian island often referred to as the Jewel of the Mediterranean thanks to its glorious beaches and lush landscape. The Nuoro province in the mountainous centre of the island is known for its high concentration of centenarians and was at one point home to the oldest women in the world, who lived to 113. While that record has since been surpassed, Sardinia is still a place where you can embrace a healthy lifestyle, and we headed to the 7Pines Resort in the north of the island to do exactly that.

The five-star resort has that laid-back vibe that makes you relax from the moment you arrive and are handed a welcome glass of prosecco. At its centre is a double layered pool with ambient house music playing softly in the background. There are floor-to-ceiling windows in the two restaurants and the gym to give the impression of the outside flowing in.

The rooms blend seamlessly into the landscape and are decorated with natural wood and textured stone tiles, and the little extras in our deluxe room, such as complimentary flip flops and a mini freezer filled with ice to chill our drinks, made our stay here feel even more special.

Get active

We started our days with an early morning swim. As well as the main pool, there’s an adults-only pool and a sandy beach with calm waters where you can go for a dip. The resort offers an activity such as a stretch class or Pilates each morning. We were initially wary of using the gym owing to the fact that everyone can see you through the glass walls, but we quickly realised what this actually means is you have a wonderful view to accompany your workout.

Keen to stretch our legs some more, we headed out of the resort for a two-hour walk around neighbouring Baja Sardinia. Along the way – which is part roadside path and part trail – we stopped off at five beaches, ranging from small sandy coves that we had all to ourselves to the large stretch of golden sand in the heart of the resort town. Here the water is crystal clear and not too deep, and when you’re ready for refreshments there are restaurants and bars on the concourse where you can enjoy a cool drink and a snack in the sunshine.

Further afield, the Pevero Health trail is a network of paths through aromatic scrubland with viewpoints to climb to and accessible beaches. It’s a 20-minute drive from the resort and it’s worth considering car hire as taxis here are expensive.

Eat well

The breakfast buffet at 7Pines will set you up for the day. As well as the usual fresh fruit and pastries, you’ll find cooked meats, grilled vegetables and a choice of egg dishes, including Uova Frattau, a typical Sardinian dish combining traditional bread, tomato purée, pecorino cheese and a poached egg.

The poolside Spazio by Franco Pepe restaurant boldly claims to serve the world’s best pizza and you’ll find unique offerings such as the delicious Spazio Mare, a fried pizza with buffalo mozzarella, red prawn, green salad and lime. We also tried the trattoria menu here, which includes catch of the day, pasta dishes and Italy’s best (in our opinion) dessert: tiramisu.

At the fine dining restaurant Capogiro, we enjoyed the Le Nostre Storie (our stories) tasting menu, a delightful mix of theatre and flavour using fresh herbs from the resort’s kitchen garden. From the amuse bouche served on ceramic sea creatures to the delicate lobster ravioli in a crab broth, every dish was beautifully presented and made our taste buds dance.

Pamper yourself

The spa at 7Pines has five treatment rooms named after flowers and plants found on the island. They face into an open-air relaxation area from where you can also access the sauna, steam room, ice bath and experience showers. To maintain the intimate feel of the area the resort allows a maximum of five guests at a time, so you’re advised to book a time slot.

Our personalised body massage somehow managed to be both relaxing and invigorating. While we almost dozed off during the treatment as our therapist worked the tension out of our back and shoulders, we felt full of renewed energy afterwards. Other pampering treats on offer include body scrubs, facials, manicures and reflexology.

Have fun

Being social and having fun are key components of living well. The resort’s beachside bar Cone Club was closed during our visit, but has DJs and party vibes throughout the summer. It’s the perfect spot to watch the sunset too. Over in Baja Sardinia, Phi Club is another popular beach club during the summer months.

The swim-up bar at 7Pines attracts a crowd towards the end of the afternoons. Our favourite tipple was the Bellavista sparkling wine – a crisp and fresh Italian fizz that became our daily sundowner.

If you’re a wine lover, the hotel can organise for you to go wine tasting at a local vineyard. Capichera Vineyard is a 20-minute drive from 7Pines and offers a golf buggy tour of the estate followed by a tasting of five wines. Watersports and boat trips (half and full day) are also bookable at the concierge desk. Of course if all you want to do is lounge around on the uber comfy sunbeds, that’s perfectly okay too!

How much does it cost?

Rooms at 7Pines Resort Sardinia start from €350 per night based on two people sharing. See BA or Ryanair for flights from the UK to Olbia, which is a 30-minute drive from the resort.

Fish and chip shop with a difference crowned UK’s best takeaway

Brothers Aman and Gavin Dhesi’s fish and chip shop has been crowned the UK’s best takeaway at the National Fish & Chip Awards 2026, beating hundreds of chippies across the country

A number of Yorkshire spots made the shortlist(Image: coldsnowstorm via Getty Images)

When the two brothers first opened their fish and chip shop, their ambition was to become ‘everyone’s local’ — and now they’re celebrated not just in their hometown, but across the entire country as the very best.

In what the industry hails as the ‘Oscars’ of the seafood world, this modest chip shop in York claimed top honours at The National Fish & Chip Awards 2026. The Scrap Box was crowned the best fish and chip takeaway in the UK — a title the owners are taking in their stride.

To even be considered for the prestigious awards, those shortlisted must demonstrate ‘extensive product knowledge, sustainable business practices, employer integrity, first-rate customer service’ and, naturally, an exceptional talent for cooking mouth-watering fish and chips.

What’s impossible to overlook is that both winners, including The Scrap Box, along with four out of six commended establishments, are all rooted in Yorkshire — cementing the county’s status as the undisputed home of the great British chippy.

The takeaway’s owners, brothers Aman and Gavin Dhesi, stumbled upon the site — formerly a toilet block beside a layby — and immediately saw its potential.

Their vision was to create a chippy that would serve the villages surrounding York and Pocklington, as well as hungry travellers passing through on their way to the seaside.

The two co-owners of the establishment, who are also siblings, are absolutely thrilled with their accomplishment. Gavin said: “There are so many outstanding fish and chip shops across the UK and countless awards, but this is the one every chippy dreams of, the ‘Oscars’ of our industry!”.

Save on the best holiday cottages in Yorkshire

This article contains affiliate links, we will receive a commission on any sales we generate from it. Learn more

Famous for its dramatic landscapes, historic cities, hearty food, and rich cultural heritage Yorkshire is just waiting to be explored. Sykes Cottages has a large number of properties to choose from with prices from £31 per night.

“With the most rigorous judging and the highest calibre of past winners, it’s a true honour to be recognised at this level. To represent the very best of fish and chips for the year ahead is both humbling and hugely meaningful to our team and a testament to the craft, care, and consistency we put into every portion of fish and chips.”

The chippy, located at Trunk Road Services on Hull Road in Dunnington, maintains a strong commitment to sustainability regarding the fish they serve.

Their website reveals the brothers made the business Marine Stewardship Council (MSC) certified back in 2024, enabling them to trace every piece of cod and haddock they serve right back to where it came from.

The roadside eatery has accumulated more than 200 glowing TripAdvisor reviews, with numerous satisfied customers sharing their experiences.

One recent visitor said: “I’m always wary of places that say ‘award-winning’ and never say what award they won!” However, here the accolades are prominently showcased for everyone to see.

“Attracted by the great exterior mural as we passed by, we promised ourselves to come back later. A lovely, fresh-looking interior, clean. The young chap who served us was extremely pleasant. Top-notch haddock and chips – freshly cooked and not greasy at all. We eat loads of fish and chips and could tell these were excellent.”

Their eye-catching mural is impossible to miss for people driving past, featuring a striking image of a fish gliding through water, set against the city’s distinctive skyline. While it certainly entices people through the door, it’s the delicious food that ensures customers return again and again.

Other contenders in the category included The Fish Works in Largs, Scotland, which secured second spot. Rounding out the top three was another Yorkshire chippy, Shaw’s Fish & Chips of Dodworth, situated in Barnsley.

Ensure our latest headlines always appear at the top of your Google Search by making us a Preferred Source. Click here to activate or add us as your Preferred Source in your Google search settings.

Italian-style UK village with palm trees and plazas is a Mediterranean paradise

This village resort has been captivating visitors for 100 years with Italian-inspired architecture and palm trees that make you feel like you’re on a Mediterranean holiday

The village was inspired by the Mediterranean way of life (Image: ChrisHepburn via Getty Images)

If you’re dreaming of an Italian escape, it turns out you needn’t venture beyond British shores, as this private village resort nestled in Wales delivers that authentic ‘la dolce vita’ experience without the eye-watering cost of flights.

Deliberately designed to evoke a slice of paradise along the Welsh coastline, Portmeirion provides the perfect retreat, boasting a wealth of dining, drinking, shopping and breathtaking natural scenery to soak up.

Every carefully considered detail within the village is crafted to conjure the feeling of a Mediterranean haven, and it has continued to draw visitors in droves ever since its establishment in the 1920s.

Guests can stay for however long suits them, whether that’s simply popping in for a leisurely day-long stroll through its immaculately designed streets, or settling in for a longer break spanning several days. Indeed, many devoted visitors opt for an annual pass, granting them unlimited access throughout the year, weather permitting.

Best holiday cottage deals in Wales

This article contains affiliate links, we will receive a commission on any sales we generate from it. Learn more

Wales is renowned for its stunning mountains, picturesque coastline and rich Celtic history. Sykes has a wide and varied collection of holiday cottages, houses and apartments across the country. Prices start from £35 per night with current deals.

When did it all begin?

The stunning Portmeirion sprang from the imagination of Welsh architect Clough Williams-Ellis, whose vision was to create a development that would complement and preserve the natural splendour of its surroundings.

His creation was constructed across two distinct phases — the first running from 1926 to 1939, and the second from 1954 to 1976.

By the time the project was complete, Clough was well into his 90s, and the vast majority of the buildings had been designed and constructed by him personally, with only a handful being relocated from elsewhere.

One such feature was the Town Hall, which was transported from the Bristol Colonnade.

Throughout his work, Clough showed a distinct fondness for Italian architectural styles, leading many to speculate that the Italian coastal town of Portofino served as his inspiration.

He firmly rejected these claims, however, insisting that he merely wished to ‘capture’ the atmosphere of the Mediterranean — and it’s safe to say he delivered on that ambition.

Despite its compact size, the village boasts an impressive array of styles and hidden gems, from its Riviera-inspired townhouses to the ornamental gardens and Italian-style piazzas scattered throughout.

Central to all of this is the grand Hotel Portmeirion and its accompanying village rooms, which provide private accommodation for the approximately 200,000 visitors who flock to the village each year.

One recent guest wrote on TripAdvisor: “As if straight out of cinque terre Italy! Buildings of unusual shapes sizes and colour everywhere you looked. Magnificent it really made you feel as if you’d stepped into another world.”

Where to stay

The Hotel Portmeirion was opened by Clough in 1926 as the centrepiece of the village, serving as the catalyst for his grand vision for the surrounding development.

Within its walls lies a complete world of its own, featuring 14 elegant bedrooms alongside a fine-dining restaurant and an impressive terrace and bar space.

The four-star hotel also features an open-air swimming pool situated on the estuary lawn. Rates for a double room for one night start at approximately £328 and can incorporate breakfast and dinner packages.

The village rooms are scattered throughout Portmeirion and cater for all types of groups, with family rooms on offer and ground-floor alternatives for accessibility requirements.

Every village room is individually crafted to be distinctive whilst maintaining that Mediterranean ambience, and all benefit from the picturesque views across the Dwyryd Estuary and beyond.

With magnificence at its heart, the village is also home to its own castle, Castell Deudraeth, which serves as a four-star residence that Clough described as “the largest and most imposing single building on the Portmeirion estate”.

Those opting not to stay but still wanting to sample the glitz and glamour of the castle can choose to dine at its own brasserie. There are also self-catering cottages on offer to rent in the village, alongside a motorhome park for caravans and campers.

Eating Out

Offering breakfast, lunch, afternoon tea and dinner, the Castell Deudraeth Brasserie serves excellent food in a relaxed setting with stunning surroundings. One visitor wrote on TripAdvisor: “A lovely traditional conservatory-style restaurant, with prompt, friendly and efficient service, a good choice on the menu, reasonable prices and very tasty food.”

They added: “We enjoyed lamb shank, plaice, and pork T-bone main courses after fine starters, with good wine choice. The Castell is an impressive Victorian-built place, with an impressive fireplace and surround in the lounge area.”

The Hotel Portmeirion’s restaurant similarly features prominently amongst favourites, boasting over 500 excellent TripAdvisor reviews. Elsewhere, Caffi Glas proves a popular dining destination, with guests particularly taken by its alfresco seating arrangement, designed to evoke an Italian piazza complete with central fountain.

The open-air dining experience proves a hit with visitors seeking that holiday atmosphere, who relish the establishment’s freshly made pizzas, pasta dishes and salads. Complementing the food are delicious wines available by the glass alongside locally sourced, traditional Welsh beers – a fitting tribute to its Welsh location.

Ensure our latest headlines always appear at the top of your Google Search by making us a Preferred Source. Click here to activate or add us as your Preferred Source in your Google search settings.

Pakistan-Afghanistan live: Iran, EU urge dialogue amid deadly clashes | Pakistan Taliban News

Live updatesLive updates,

Pakistan says it has targeted Taliban forces in Afghanistan’s Kabul and border regions; UN chief says civilians also impacted.

Published On 28 Feb 2026

Russia-Ukraine war: List of key events, day 1,465 | Russia-Ukraine war News

These are the key developments from day 1,465 of Russia’s war on Ukraine.

Published On 28 Feb 2026

Here is where things stand on Saturday, February 28:

Fighting

- Russia struck port infrastructure overnight in Ukraine’s southern Odesa region, igniting fires and damaging equipment, warehouses and food containers, Deputy Prime Minister Oleksii Kuleba said.

- A localised truce has been established near the Russian-controlled Zaporizhzhia nuclear power plant to allow repairs to power lines, Russian news agencies report, citing the head of Russia’s state nuclear corporation.

- Ukraine shot down a drone near the border with Romania during a Russian attack on port infrastructure on the Danube River, Romania’s Ministry of National Defence said.

- Romania said it scrambled fighter jets and that the drone was brought down 100 metres (110 yards) from the Romanian village of Chilia Veche, on the opposite side of the Danube River to Ukraine.

- Russian forces have taken control of the village of Biliakivka in the Dnipropetrovsk region of eastern Ukraine, the Russian RIA Novosti state news agency reported, citing the Ministry of Defence.

- Ukraine’s military said it struck an oil depot in the Russian-occupied Luhansk region overnight, causing a large fire at the facility.

- Firefighters were trying to bring a fire at an oil refinery in Russia’s southern Krasnodar region under control, local officials said early Saturday.

- Ukraine is considering forming partnerships with allies to build air defences capable of intercepting ballistic missiles and to address a critical shortage of munitions for United States-made Patriot systems, the country’s defence minister said.

- Ghana’s Foreign Minister Samuel Okudzeto Ablakwa said 55 Ghanaians had been killed fighting in Ukraine, and that some 272 citizens of the African country are believed to have been lured to fight for Russia in Ukraine since 2022.

Regional security

- The Swedish military intercepted a suspected Russian drone off the country’s south coast while a French aircraft carrier was docked in Malmo, officials said.

- Kremlin spokesman Dmitry Peskov said it was “absurd” to suggest the drone that was electronically disabled near a French aircraft carrier in Sweden earlier this week was Russian.

- The European Commission said Croatia is assessing whether it can legally import seaborne Russian crude to supply Hungary and Slovakia through its Adria pipeline.

- The move by Croatia follows after oil supplies via the Ukrainian section of the Druzhba pipeline to Hungary and Slovakia – the only European Union countries still importing Russian oil – were halted last month due to damage Ukraine blamed on a Russian drone strike.

- In a video posted on Facebook, Hungarian Prime Minister Viktor Orban urged Ukraine’s President Volodymyr Zelenskyy to grant Hungarian and Slovak inspectors access to repair and restart the Druzhba pipeline.

- President Zelenskyy said he had not been offered nuclear weapons by the United Kingdom or France, but added he would accept such an offer “with pleasure”, after Russia’s Foreign Intelligence Service accused both countries of working to provide Kyiv with a nuclear bomb.

- Poland’s parliament approved a law to implement the EU’s Security Action for Europe (SAFE) defence procurement programme aimed at boosting member states’ military readiness.

Economy

- The International Monetary Fund said its executive board had approved an $8.1bn, four-year loan for Ukraine, anchoring a broader $136.5bn international support package. The World Bank estimates Ukraine will need $588bn for post-war reconstruction.

- Economists say Russia is grappling with heavy state defence spending alongside deepening structural challenges, including labour shortages and high inflation.

- Ukraine’s major steelmaker ArcelorMittal Kryvyi Rih said it is closing another division due to a worsening energy crisis caused by continued Russian attacks on Ukraine’s power system.

Peace talks

- Bilateral talks between US and Ukrainian officials in Geneva concluded on Thursday, with Kyiv saying preparations are under way for the next round of negotiations aimed at ending the war.

- Ukraine’s chief negotiator, Rustem Umerov, said on X that discussions were held in two formats: separate meetings with the United States and a trilateral session involving the US and Switzerland.

- Umerov said participants spoke with President Zelenskyy and were working to ensure the next three-sided meeting with Russia on a settlement is “as substantive as possible”.

Politics and diplomacy

- Former British Prime Minister Rishi Sunak has begun advising the Ukrainian government on economic renewal as Kyiv works to rebuild its energy sector before next winter.

- Finland, Ukraine and the Czech Republic will skip the opening ceremony of the Milano Cortina Paralympics in protest against the inclusion of Russian athletes competing under their own flag while the war in Ukraine is ongoing.

- German Chancellor Friedrich Merz said “diplomacy cannot succeed at the moment” with Russia, and that greater emphasis should be placed on defending Ukraine from Moscow’s aggression.

BBC Death in Paradise’s Mervin Wilson announces exit as detective is kidnapped

Death in Paradise detective Mervin Wilson was kidnapped in a cliffhanger after travelling to Antigua to visit his brother Solomon

Has Mervin Wilson been kidnapped?(Image: BBC)

In the latest episode of Death in Paradise, Detective Mervin Wilson (portrayed by Don Gilet) revealed he was taking a temporary leave from Saint Marie.

After cracking another case with his team, Mervin decided to take his colleague Naomi Thomas’s (played by Shantol Jackson) advice and travel to Antigua to visit his brother, Solomon (Daniel Ward).

Mervin’s relationship with his brother got off on the wrong foot when Solomon raided his shack and nicked his belongings. Following this incident, Solomon returned to Antigua, leaving Mervin uncertain if they would ever cross paths again.

However, towards the end of Friday’s episode, Mervin informed Naomi that he wouldn’t be at work the next day as he was heading for Antigua.

“DS Thomas, I am just letting you know I won’t be coming in tomorrow,” Mervin announced over the phone, reports the Express.

For the latest showbiz, TV, movie and streaming news, go to the new **Everything Gossip** website.

“I am actually taking your advice as it goes, I am going to see Sol. Yeah, well, I mean, I don’t even know if he wants to see me, but hey, what is the worst that could happen?”

Immediately after, Naomi rushed to inform her colleagues, expressing worry about the detective.

“Sir,” Naomi said urgently, to which the Commissioner (Don Warrington) responded, “DS Thomas, what is it?”

“I think something has happened to the inspector,” she added.

The episode ended on a cliffhanger, with Mervin bound and kidnapped by an unknown assailant – but who could be responsible?

“What the hell is going on?” The detective demanded as he attempted to escape.

As he glanced up, it seemed Mervin recognised who his abductor was as he raged, “You!”

Death in Paradise is available to stream on BBC iPlayer.

Ensure our latest headlines always appear at the top of your Google Search by making us a Preferred Source.** Click here to activate**** or add us as your Preferred Source in your Google search settings.**

Judge extends order protecting Minnesota refugees from arrest, deportation

MINNEAPOLIS — A federal judge Friday extended an order protecting refugees in Minnesota who are lawfully in the U.S. from being arrested and deported, saying a Trump administration policy turns the “American Dream into a dystopian nightmare.”

U.S. District Judge John Tunheim granted a motion by advocates for refugees to convert a temporary restraining order that he issued in January into a more permanent preliminary injunction while the case develops.

The order applies only in Minnesota. But the implications of a new national policy on refugees that the Department of Homeland Security announced Feb. 18 were a major part of the discussion at a hearing held by the judge the next day.

“Minnesota refugees can now live their lives without fear that their own government will snatch them off the street and imprison them far from loved ones,” Kimberly Grano, an attorney with the International Refugee Assistance Project, told the Associated Press.

The Trump administration asserts that it has the right to arrest potentially tens of thousands of refugees across the U.S. who entered the country legally but don’t yet have green cards. A new Homeland Security memo interprets immigration law to say that refugees applying for green cards must return to federal custody one year after they were admitted to the U.S. so that their applications can be reviewed.

The judge expressed disbelief in a 66-page opinion.

“This Court will not allow federal authorities to use a new and erroneous statutory interpretation to terrorize refugees who immigrated to this country under the promise that they would be welcomed and allowed to live in peace, far from the persecution they fled,” Tunheim said.

He said the U.S. decades ago promised refugees fleeing persecution that they could build a new life after rigorous background checks.

“We promised them the hope that one day they could achieve the American Dream,” Tunheim wrote. “The Government’s new policy breaks that promise — without congressional authorization — and raises serious constitutional concerns. The new policy turns the refugees’ American Dream into a dystopian nightmare.”

Homeland Security and U.S. Citizenship and Immigration Services said in a statement Friday night that the ruling was “yet another lawless and activist order from a federal judge” and that the Trump administration expected to be “vindicated in court.”

“USCIS is committed to rooting out fraud and protecting the public safety and national security interests of the American people by screening and vetting aliens,” the statement said.

Justice Department attorney Brantley Mayers said during a court hearing last week that the government should have the right to arrest refugees one year after entering the U.S., but he also indicated that would not always happen.

The judge noted that one refugee in the case, identified as D. Doe, was arrested in January after being told that someone had struck his car.

“He was immediately flown to Texas, where he was interrogated about his refugee status. He was kept in ‘shackles and handcuffs’ for sixteen hours. D. Doe was ultimately released on the streets of Texas, left to find his way back to Minnesota,” Tunheim said.

Karnowski and White write for the Associated Press and reported from Minneapolis and Detroit, respectively. AP writer Rebecca Boone in Boise, Idaho, contributed to this report.

Wolverhampton Wanderers 2-0 Aston Villa: Derby points record was ‘hanging over our heads’ – Rob Edwards

Wolves head coach Rob Edwards says the prospect of ending the season with fewer points than record-holders Derby County was “hanging over their heads”, and believes his side will have more confidence going forward after their 2-0 win over local rivals Aston Villa.

MATCH REPORT: Wolverhampton Wanderers 2-0 Aston Villa

Available to UK users only.

Ramadan in Yemen’s Aden: Optimism dimmed by tensions and shortages | Politics News

Aden, Yemen – Abu Amjad was shopping with his two children last week, finally able to take them out and buy them new clothes – a cherished Ramadan tradition in Yemen.

The 35-year-old is a teacher, and he had just received his salary. That payment was a sign things are improving in Aden – the salaries are funded by Saudi Arabia as a way of backing the Yemeni government, which has recently arrived to take control of Aden after the defeat of secessionist forces.

Recommended Stories

list of 3 itemsend of list

But problems and instability are never far away in Yemen.

Just as soon as the children, Amjad, 10, and Mona, 7, began trying on their outfits, the sound of gunfire erupted. Shoppers froze. Amjad and Mona clutched their father, asking to leave.

About 3km (2 miles) away, security forces had opened fire on protesters who attempted to breach the gates of al-Maashiq Palace, where members of the Yemeni government have been based since they arrived from Riyadh a week ago.

The gunfire shattered the family’s moment of joy.

“It ruins your joy when you see a person bleed and robs you of peace when you hear prolonged gunfire,” Abu Amjad told Al Jazeera.

After years of operating from exile, Yemen’s Saudi-backed, UN-recognised cabinet is spending Ramadan in Aden, a move that has coincided with improvements in basic services and a renewed sense of relief. Yet that relief was overshadowed by the deadly confrontation between security forces and antigovernment protesters, in which at least one person was killed.

“That was the first clash after the return of the government to Aden. Our concern is that it may not be the last,” said Abu Amjad.

Government wins

Yemen’s new Prime Minister Shaya al-Zindani has said that stabilising Aden and other areas under government control was among the new government’s main priorities.

The Yemeni government is currently in its strongest position for years. An advance by the separatist Southern Transitional Council (STC) at the end of last year in eastern Yemen ultimately was a step too far for the United Arab Emirates-backed group.

Saudi Arabia considered the STC advance the crossing of a red line, and lent its full military backing to the Yemeni government, allowing it to take territory it had not controlled for years.

Now, the Yemeni government and Saudi Arabia are focused on attempting to improve conditions in the southern and eastern areas of Yemen under government control, to attract more public support. That would in turn weaken support for both the STC and the Houthi rebels, who have controlled northwestern Yemen, including the capital, Sanaa, since the country’s war began in 2014.

Lit city and busy markets

Abdulrahman Mansour, a bus driver and resident of Khormaksar in Aden, said Ramadan this year feels different.

“When I see the lights on and the markets busy on Ramadan nights in Aden, it feels like a different city. The improvement is undeniable,” Mansour, 42, told Al Jazeera.

He noted that one distinct difference this Ramadan is the stable provision of electricity. “This reminds me of the pre-war time. We used to take that service for granted,” said Mansour.

“When the city is dark at night, it appears gloomy, and families prefer to stay home. The movement of people brings life to the city and helps small businesses keep afloat, especially in Ramadan,” Mansour added.

Yemeni Electricity Minister Adnan al-Kaf said last week that efforts to improve electricity services in Aden and other provinces continue, noting that Saudi support had contributed to improved service over the past two months.

Wafiq Saleh, a Yemeni economic researcher, said the improvement in the living standards of citizens in Aden and southern Yemen, in general, was obvious, particularly after Saudi Arabia’s payment of public sector salaries and the supply of basic services such as water and electricity.

Saleh told Al Jazeera, “The recent Saudi financial support has been very generous, and it can help the government during this period by enabling it to work on reactivating dormant resources, resuming oil exports, combating corruption, and improving the efficiency of revenue collection with transparency and good governance.”

But Saleh emphasised that the progress achieved so far is not the result of economic reforms by the Yemeni government, but rather because of Saudi support.

Therefore, according to the economist, the improvement in the living situation and the currency’s value may not be sustainable, even if it is a positive indicator and may be the first step towards promised economic reforms in the country.

“There must be a comprehensive vision for developing revenue collection so that the government can implement sustainable economic reforms,” Saleh said.

Search for cooking gas

While the distribution of electricity has improved in Aden, other essential services remain strained. Cooking gas shortages remain a major concern. The search for it remains a daily struggle for families in the port city, and the crisis has intensified in Ramadan.

Lines of vehicles queue at stations, while residents wait with cylinders for a few litres (quarts) of gas.

“Going from one station to another in search of cooking gas while fasting is exhausting,” said Fawaz Ahmed, a 42-year resident of Khormaksar district.

Fawaz describes the shortage of cooking gas as a cause of hunger in the city. “If I stay in [my home] village, I would resort to firewood. But in the city, that option is not available, and if we find firewood in the market, it is expensive.”

Gas distributors say the quantity of cooking gas supplied to them is not adequate, citing this as the root cause of the crisis. Supplies are transported from Marib province in northern Yemen.

Tensions to continue

The cooking gas shortage is a sign that it will not be plain sailing for the Yemeni government in Aden.

And opponents will likely seize on any ongoing problems to foment more unrest.

Majed al-Daari, editor-in-chief of the independent Yemeni news site Maraqiboun Press, described the situation in Aden as “very worrying”.

“What happened to the demonstrators at the start of Ramadan underscores the fragility of the political and security situation. Tensions are set to continue,” al-Daari said.

“The STC will continue mobilising its supporters against the government. This is its last card that it will use to restore lost political interests,” al-Daari added.

The STC said in a statement last week that raids and arbitrary arrests had targeted people who had participated in the recent protests. These attacks, the statement emphasised, would only increase the determination of the southerner secessionists.

For Abu Amjad, demonstrations in Aden give space to chaos, which he resents.

“At least, Ramadan should pass without protests. Political actors should spare us this month so we can fast and share some joy with our children,” he said.

Peace ‘within reach’ as Iran agrees no nuclear material stockpile: Oman FM | Military News

Oman’s Foreign Minister says most recent indirect talks between US, Iran ‘really advanced, substantially’ and diplomacy must be allowed do its work.

Iran agreed during indirect talks with the United States never to stockpile enriched uranium, said Oman’s top diplomat, who described the development as a major breakthrough.

Oman’s Foreign Minister Badr bin Hamad Al Busaidi also said on Friday that he believed all issues in a deal between Iran and the US could be resolved “amicably and comprehensively” within a few months.

Recommended Stories

list of 4 itemsend of list

“A peace deal is within our reach … if we just allow diplomacy the space it needs to get there,” Al Busaidi said in an interview with CBS News in Washington, DC, after Oman brokered the third round of indirect talks between the US and Iran in Geneva on Thursday.

“If the ultimate objective is to ensure forever that Iran cannot have a nuclear bomb, I think we have cracked that problem through these negotiations by agreeing [on] a very important breakthrough that has never been achieved any time before,” Al Busaidi said.

“The single most important achievement, I believe, is the agreement that Iran will never ever have nuclear material that will create a bomb,” he said.

“Now we are talking about zero stockpiling, and that is very, very important because if you cannot stockpile material that is enriched, then there is no way that you can actually create a bomb,” he added.

There would also be “full and comprehensive verification by the IAEA [International Atomic Energy Agency]”, he said, referring to the UN’s nuclear watchdog.

Oman’s top diplomat also said Iran would degrade its current stockpiles of nuclear material to “the lowest level possible” so that it is “converted into fuel, and that fuel will be irreversible”.

“This is something completely new. It really makes the enrichment argument less relevant, because now we are talking about zero stockpiling,” Al Busaidi said.

Regarding recent US demands regarding Iran’s missile programme, Al Busaidi said: “I believe Iran is open to discuss everything”.

Asked if he thought enough ground was covered in the most recent talks in Geneva to hold off a US attack on Iran, the minister said, “I hope so.”

“We have really advanced substantially, and I think, obviously, there remains various details to be ironed out, and this is why we need a little bit more time to really try and accomplish the ultimate goal of having a comprehensive package of the deal,” he said.

“But the big picture is that a deal is in our hands,” he added.

The foreign minister’s comment followed after he met earlier on Friday with US Vice President JD Vance and as US President Donald Trump continued to sabre-rattle while at the same time declaring he favoured a diplomatic solution with Tehran.

Trump said on Friday that he was not happy with the recent talks that concluded in Geneva.

“We’re not exactly happy with the way they’re negotiating,” Trump told reporters in Washington, adding that Iran “should make a deal”.

“They’d be smart if they made a deal,” he said.

Trump later said that he would prefer it if the US did not have to use military force, “but sometimes you have to do it”.

The US and Iranian sides are expected to meet again on Monday in Vienna, Austria, for more indirect negotiations.

Emmerdale fans ‘devastated’ as fan favourite Bear Wolf endures sad twist

Emmerdale viewers were left “devastated” after things got worse for Bear Wolf on Friday night’s episode of the ITV soap after everything the fan favourite has already been through

Things got worse for Bear Wolf on Friday’s edition of Emmerdael