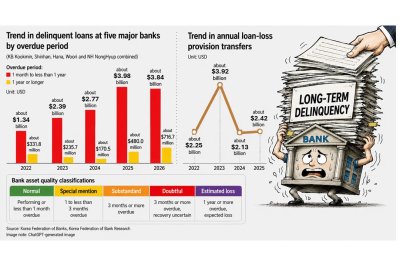

South Korea’s five major banks saw long-term delinquent loans rise to about $716.7 million in 2026, while loans overdue for one month to less than one year remained elevated at about $3.84 billion. Data from Korea Federation of Banks and Korea Federation of Bank Research. Graphic by Asia Today and translated by UPI

June 3 (Asia Today) — South Korea’s major commercial banks are facing growing pressure from a sharp rise in long-overdue loans, with the amount of loans unpaid for more than one year exceeding 1 trillion won, or about $716 million, in the first quarter.

Loans overdue for less than one year, which could later worsen into long-term delinquencies, also approached 6 trillion won, or about $3.84 billion. The increase suggests that borrower distress is deepening, especially among corporate borrowers, despite banks’ efforts to dispose of nonperforming loans.

The sequential expiration of COVID-19 loan maturity extensions also appears to be adding pressure on delinquent borrowers.

Banks, which have continued to post strong earnings, are concerned that rising long-term delinquencies could increase loan-loss provision burdens. The longer a loan remains overdue and the lower its chance of recovery becomes, the more banks must set aside in provisions.

If the Bank of Korea raises its base rate in the second half, borrowers’ repayment burdens could grow further, increasing the risk of additional long-term delinquencies. Analysts say asset quality management could become a key factor determining banks’ earnings performance.

According to financial industry data released Wednesday, the combined balance of loans overdue for at least one year at KB Kookmin Bank, Shinhan Bank, Hana Bank, Woori Bank and NH NongHyup Bank reached 1.0972 trillion won, or about $716 million, in the first quarter.

That was up 49.3% from 734.9 billion won, or about $480 million, a year earlier. Compared with 261 billion won, or about $170 million, in 2024, the figure has more than quadrupled. It was also more than double the 508 billion won, or about $332 million, recorded in 2022 during the COVID-19 pandemic.

The increase appeared across all five banks. By bank, NH NongHyup had the largest balance of long-term overdue loans at 474.8 billion won, or about $310 million, followed by KB Kookmin at 166.9 billion won, or about $109 million, Hana at 155.2 billion won, or about $101 million, Shinhan at 151.5 billion won, or about $99 million, and Woori at 148.8 billion won, or about $97 million.

Loans overdue for at least one month but less than one year totaled 5.8851 trillion won, or about $3.84 billion, approaching the 6 trillion won mark. The figure was slightly lower than 6.1002 trillion won, or about $3.98 billion, a year earlier, but remained high by historical standards.

By category, loans overdue for at least one month but less than three months rose from a year earlier to 2.8225 trillion won, or about $1.84 billion. Loans overdue for at least six months but less than one year, which are considered more likely to become long-term delinquencies, reached 1.1111 trillion won, or about $726 million. Both were record highs since the banks began disclosing the relevant data.

The surge in long-term delinquencies is widely attributed to a sharp increase in new overdue loans in 2024 and 2025. Higher interest rates and weak domestic demand weakened borrowers’ repayment capacity, with some distressed borrowers slipping into long-term delinquency.

The increase appears particularly concentrated among corporate borrowers, whose loans are relatively large and harder to recover. At the end of March, the banking sector’s corporate loan delinquency rate stood at 0.68%, up 0.06 percentage point from 0.62% a year earlier.

“Distress pressure has continued for a long period in sectors such as construction and real estate leasing because of the weak housing market,” an official at a commercial bank said.

A renewed period of rate increases could add to the problem. The Bank of Korea left open the possibility of at least one base rate increase in the second half during last month’s monetary policy meeting, raising concerns that banks could face greater asset quality pressure.

Higher base rates can push up market rates, including bank bond yields, increasing borrowers’ interest burdens. That could deepen distress among loans already in arrears and increase new delinquencies, potentially expanding the volume of long-term overdue loans later.

That would likely translate into higher loan-loss provisions for banks. Banks classify loans into five asset-quality categories: normal, precautionary, substandard, doubtful and estimated loss.

When a loan is classified as substandard, banks must set aside provisions equal to 20% of the loan amount. As the overdue period grows longer and repayment capacity worsens, the required provision ratio rises. Doubtful loans, which are overdue for more than three months and have low recovery prospects, require 50% provisioning. Loans classified as estimated losses after more than one year overdue require 100% provisioning.

That means if a doubtful loan deteriorates into an estimated loss, the provisioning burden doubles.

A rise in provision expenses would directly weigh on bank earnings. In 2022, the five major banks set aside 3.5422 trillion won, or about $2.31 billion, in annual loan-loss provisions, while their combined net profit rose 18.6% from a year earlier to 13.7472 trillion won, or about $8.98 billion.

But in 2023, when banks set aside more than 6 trillion won, or about $3.92 billion, in provisions because of real estate project financing distress and other factors, their net profit growth slowed to 2.6%.

Provision expenses fell sharply the following year, but as delinquencies continue to rise, the possibility of renewed growth in provisions has increased. Analysts say careful risk management has become more important.

“As the delinquency period lengthens, the sale price of nonperforming loans tends to fall, so if long-term delinquencies increase, banks disposing of bad loans will also face greater loss burdens,” a financial industry official said.

“The key will be whether banks can prevent new distress from expanding while effectively clearing existing bad loans,” the official said.

— Reported by Asia Today; translated by UPI

© Asia Today. Unauthorized reproduction or redistribution prohibited.

Original Korean report: https://www.asiatoday.co.kr/kn/view.php?key=20260604010001073