Outsourcing credit lets the Chinese EV maker scale fast while leaving asset risks to lenders.

This article appears in the July/August issue of Global Finance Magazine.

Walk the streets of cities like Valencia or Paris, and you don’t need the data to see BYD everywhere, especially in ride-hailing fleets and private transportation. These days, the sleek logo you notice isn’t always Tesla’s or Kia’s; it’s often BYD’s.

Sales of BYD’s electric vehicles surged across Europe last year, up roughly 270% year over year. In the first quarter of 2026, sales increased by another 156%.

While most coverage frames this as a product story, the bigger story is financing: BYD’s rise has less to do with design or price than with how the cars are financed.

BYD hasn’t expanded in Europe by building a traditional captive-finance arm. Instead, it has plugged directly into the region’s existing banking and leasing infrastructure, achieving captive-finance reach without the balance-sheet burden. In doing so, it has turned Europe’s financial system into a distribution engine that moves vehicles by turning them into financeable assets.

At first glance, BYD’s success seems straightforward: strong demand, rapid adoption, and a new entrant quickly gaining share. But in a market where vehicles are often financed, leased, and cycled through multiple channels before reaching long-term ownership, the headline numbers don’t always tell the whole story. The surge in European BYD registrations may signal demand and financing strength, or it may reflect window dressing shaped by the way the system works.

Turning Cars Into Collateral

Stefan Bratzel, Center of Automotive Management

BYD relies on a familiar but strategically deployed set of financing and leasing arrangements. Vehicles are sold in bulk to leasing companies, fleet operators, and dealer networks, which then finance or lease them to end users, including corporate clients, ride-hailing drivers, and private buyers. European banks and auto-finance platforms provide the underlying credit, while leasing firms structure contracts and manage residual-value assumptions.

What stands out in BYD’s case is the speed and scale of the operation.

“European OEMs [original equipment manufacturers] built their captive finance arms over 30 to 40 years, and those businesses now function as profit centers,” says Stefan Bratzel, founder and executive director of the Center of Automotive Management (CAM) in Bergisch Gladbach, Germany. “BYD cannot replicate this overnight, nor does it try to.”

Instead, he notes, the company is partnering with established asset finance providers to accelerate market entry. BYD gains “speed to market at the cost of margin while it accumulates the balance sheet and regulatory standing to eventually internalize these functions.”

In effect, BYD is compressing a decades-long buildout of captive finance into a partner-led model, trading margin and control for faster access to Europe’s credit and leasing channels.

It’s easy to see the appeal for lenders: Vehicles placed into leasing or fleet programs become financeable units, bundled into loan or lease portfolios that generate predictable cash flow. In a market where electrification is both a policy priority and an investment theme, high-volume EV programs provide a steady pipeline of assets.

Window Dressing?

The speed of BYD’s expansion raises questions about the numbers.

“BYD’s channel mix is improving,” says Matthias Schmidt, an independent analyst tracking the European auto market. Retail share in Germany rose to 32.5% of volume in the first four months of 2026, compared with 12.4% for all of last year, suggesting a shift toward a more balanced sales mix. But the relationship between registrations and vehicles actually on the road is less straightforward.

“Out of more than 30,472 BYD models registered in Germany since it entered the market in December 2022, only 18,536 are currently on the road,” says Schmidt, suggesting that “after models have been registered, they are then being exported to other European markets as used-car inventory or are going back into used-car inventory in Germany. This could be a strategy to demonstrate to market observers that they are performing better in Europe’s largest market than they actually are. We call it window-dressing the data.”

In a system driven by leasing, fleet placement, and dealer networks, that gap is not necessarily unusual. Vehicles can be registered into the channel before reaching long-term ownership, then repositioned through resale, export, or short-term use across markets. For financial stakeholders, the distinction matters: registrations may signal momentum, but they do not necessarily show sustained demand.

What Banks Are Really Underwriting

For the institutions partnering with BYD and helping fund its expansion, the focus is less on BYD’s near-term concern — speed to market — and more on how those assets perform over time.

Residual value assumptions underpin the economics of leasing. If vehicles retain value, the system works: Monthly payments remain competitive, credit risk remains contained, and lenders and leasing firms can recycle assets efficiently through secondary markets. When they don’t, the economics tighten quickly.

“The EV residual value question is the single biggest structural challenge in automotive finance right now,” Bratzel says. “Whoever solves that problem credibly — either through data, scale, or balance sheet — will have a significant structural advantage.”

Bratzel points to one potential factor that could shape how banks ultimately price that risk: “Vertical integration around the battery — especially battery cells — can have a positive impact on risk assessments, as this is based on a lot of their own data.”

BYD’s advantage stems in part from how much of that data it controls. Unlike many automakers that rely on third-party suppliers for critical components, the company produces its own battery cells and key parts of the EV supply chain. That level of vertical integration gives BYD clearer visibility into battery performance over time, arguably the most important variable in determining how an electric vehicle depreciates.

The geographic distribution of BYD’s growth in Europe adds another layer.

According to Schmidt, roughly 70% of Chinese EV registrations in Western Europe in the first quarter of this year were concentrated in Spain, Italy, and the U.K.: markets that tend to be more price-sensitive and open to new entrants.

While this doesn’t invalidate BYD’s growth, it suggests that location-dependent finance dynamics are driving expansion as much as consumer demand.

Traditional OEM Captive Finance

BYD Partner-Led Model

Builds and operates own finance arm

Uses banks and leasing partners

Significant capital commitment

Lower capital burden

Controls lending and leasing directly

Outsources financing functions

Often takes decades to build

Can scale immediately

Retains finance profits

Trades margin for speed

Higher control

Faster market entry

Source: Center of Automotive Management (CAM)

What Happens Next

BYD’s approach is working. It has outsourced the slowest component of automotive expansion — credit formation — while maintaining control of product supply and commercial momentum.

As Bratzel suggests, this is not a permanent structure: It’s transitional. It’s designed to gain scale first, then possibly internalize financing over time. Meanwhile, European banks and leasing platforms are providing balance-sheet support to enable growth.

Schmidt’s analysis leaves little ambiguity: Not all growth is created equal. Registration data may reflect momentum, but it can also reflect channel dynamics — fleet placements, dealer inventory, cross-border repositioning — that cloud actual on-the-ground demand.

For lenders, the distinction is not academic. They are not underwriting registrations. They are underwriting residual values, which is where the rubber meets the road.

Over the next two to three years, vehicles deployed and financed today will begin to cycle back through the system via lease returns, resale markets, and secondary channels. At that point, the assumptions that anchor today’s financial models will be tested against real-world market conditions.

But the next phase will be less about volume. It will instead focus on testing the model that facilitated BYD’s rapid entry into Europe. If BYD’s vehicles hold their value, the company’s partner-led model will look less like a workaround and more like a fast-track version of what legacy automakers spent decades building. If residual values weaken, or if too much of the growth proves channel-driven rather than demand-driven, the financing engine that built BYD’s presence could become a constraint.

That’s the real question for banks: Can the vehicles BYD has placed in Europe retain their value once they return to the market? Because in a financing-driven system, growth can be engineered, but asset performance determines whether it lasts.

Rocco Pendola is a contributing writer based in Spain.

The United States Federal Reserve is set to hold interest rates steady as inflationary pressures mount, driven by heightened fuel prices as tensions between the US and Iran continue.

The central bank said on Wednesday that it will maintain rates at 350-375 basis points during the second monetary policy decision under new Chairman Kevin Warsh.

Recommended Stories

list of 4 itemsend of list

“Inflation remains elevated relative to the Committee’s 2 percent goal, in part reflecting supply shocks that have driven price increases in certain sectors, including energy. The Committee will deliver price stability,” the central bank said in a statement upon the release of its decision.

CME FedWatch, which tracks the likelihood of monetary policy decisions, forecast a 66.3 percent chance of maintaining rates, while there was a 33.7 percent chance that rates would increase to 375-400 basis points.

Of the 12, three members, Beth M Hammack, Neel Kashkari, and Lorie K Logan, voted to raise rates by 25 basis points.

“My colleagues and I considered the economic shocks of recent years, strained supply chains arising from the pandemic, military conflicts, energy supply disruptions, substantial increases in tariff rates, and yes, the surge in AI-related investment,” Warsh told reporters.

“We are not relying on any one individual piece of data as cover or as an excuse, or as validation. What I care about and what I think the Committee cares about is trends on the data.”

Monetary policy decisions have become more uncertain as Warsh has scrapped forward guidance, which typically helps financial institutions and journalists better understand upcoming policy choices.

Flying blind

That is putting pressure on analysts.

“With little guidance on the reaction function under the new chairman, markets are filling the void with speculation that Warsh may be eyeing a surprise hike to reinforce anti-inflation credibility,” Barclays economists said in a note.

Citadel Securities earlier this week forecast a rate hike. Meanwhile, analysts at S&P Global forecast that rates would hold steady.

At the last meeting, the central bank’s governors were evenly split on whether to raise interest rates this year, as the central bank maintained rates during its first meeting under Warsh.

Warsh had previously said that there was “no tolerance” for inflation as the central bank pushes to reach the Fed’s 2 percent target.

Market shifts

Financial pressures on the broader market eased last month, with consumer inflation moderating. The Consumer Price Index report released in July for the month of June by the US Labor Department’s Bureau of Labor Statistics showed a 0.4 percent decline in consumer inflation, marking the first monthly decline since April 2020 in the early days of the COVID-19 pandemic. However, that was a correction from the previous month, when the CPI rose by 0.5 percent.

The CPI remains elevated at 3.5 percent on an annual basis, according to the report, though that is still a slowdown from 4.2 percent in May. However, consumers are still feeling the pinch, especially at the petrol pump.

Prices are on the upswing. The average price for a gallon of petrol is $4.09 ($1.08 per litre), up 3 cents from this time last week, and up from $3.86 ($1.02 per litre) this time last month, according to the American Automobile Association (AAA), which tracks daily petrol prices. By comparison, daily petrol prices were $2.98 ($0.78 per litre) when the US and Israel first struck Iran on February 28.

Those pressures are echoed by a slump in consumer confidence for the third straight month, according to The Conference Board, which released its report on Tuesday.

“Consumers anticipate little improvement in business conditions over the next six months,” Dana M Peterson, chief economist at The Conference Board, said upon the report’s release.

Political flashpoint

The decision is overshadowed by pressure from the White House. Interest rates have been a point of contention between Trump and the central bank. Trump has long pushed the Fed to cut rates, putting former Chair Jerome Powell in the crosshairs and making him the subject of investigations by the US Department of Justice.

But Warsh has yet to become a target of Trump’s scorn. “Kevin is fantastic,” he told reporters on Monday on board Air Force One. “He’s got a board, and the board members are very political.”

Trump made those claims despite the central bank’s longstanding commitment to maintaining its independence from political pressure.

Major central banks are confronting an increasingly difficult inflation landscape as multiple price pressures converge, raising questions over whether policymakers can continue treating inflation shocks as temporary.

The U.S. Federal Reserve, the Bank of Japan and the Bank of England all meet this week against a backdrop of elevated inflation driven by rising energy costs, geopolitical tensions, supply chain disruptions, fiscal stimulus, labor market tightness and climate related risks.

While central banks have traditionally argued that isolated price shocks eventually fade without requiring aggressive monetary tightening, economists warn that today’s inflation environment is no longer defined by a single disruption but by several overlapping forces reinforcing one another.

Inflation remains well above target

The Federal Reserve’s preferred inflation measure, the Personal Consumption Expenditures (PCE) Price Index, is expected to remain significantly above the central bank’s 2 percent target.

Stay ahead of the geopolitical week.

MD Briefing delivers expert analysis across five global fronts — the Indo-Pacific, energy, geoeconomics, European security, and the Middle East — every Monday morning. Free.

Economists expect headline PCE inflation to stand at 3.7 percent and core inflation, which excludes food and energy, at 3.3 percent.

Inflation has remained above the Fed’s target for more than five consecutive years, complicating expectations that price growth will naturally return to normal levels.

Energy prices return as a major concern

Renewed military tensions in the Middle East have pushed crude oil prices sharply higher, adding fresh uncertainty to the global inflation outlook.

Brent crude briefly climbed above $100 per barrel before easing, while volatility in oil markets has increased as conflict around the Gulf and Red Sea threatens global energy supplies.

Higher crude prices have translated into rising fuel costs, with average U.S. gasoline prices now more than 30 percent above levels recorded a year earlier.

For central banks, energy inflation remains particularly difficult because monetary policy cannot directly resolve geopolitical conflicts or supply disruptions.

Food inflation adds further pressure

Food prices are emerging as another source of concern.

Annual U.S. food inflation already stands near 3 percent, while forecasts suggest stronger El Niño weather conditions could reduce agricultural production and lift global food prices over the coming months.

Some projections indicate food inflation could approach 5 percent next year, adding further upward pressure to overall consumer prices worldwide.

Unlike financial market volatility, rising food and fuel costs directly affect households and often shape public perceptions of inflation more than broader economic indicators.

Core inflation refuses to ease

Although policymakers often focus on core inflation because it removes volatile food and energy prices, underlying price pressures remain stubbornly elevated.

Persistent wage growth, continued strength in consumer spending and resilient labor markets have prevented meaningful progress toward the Fed’s inflation target.

Economists also warn that prolonged increases in food and energy prices eventually feed into broader consumer prices, making it increasingly difficult to separate temporary inflation from structural trends.

Tariffs and artificial intelligence create new price risks

Additional inflationary risks are emerging from trade policy and technological investment.

President Donald Trump’s renewed tariffs on imported goods could increase costs across multiple industries, while continued demand for artificial intelligence infrastructure has intensified shortages in advanced semiconductor markets.

Higher chip prices are expected to affect consumer electronics and industrial production, creating another potential source of inflation in manufactured goods.

Meanwhile, expansionary fiscal policies and strong financial conditions continue to support consumer demand, limiting the slowdown in prices that central banks have been seeking.

Strong labor markets complicate policy

Employment conditions remain exceptionally resilient across advanced economies.

In the United States, unemployment has remained near historically low levels, while wage growth above 3 percent continues to support household spending.

Although robust labor markets are generally viewed as positive for economic growth, they also contribute to persistent service sector inflation by increasing business labor costs.

This has made it harder for central banks to achieve price stability without risking slower economic growth.

Analysis: Inflation risks are becoming structural

The challenge facing central banks is no longer whether one inflation shock will fade but whether multiple overlapping shocks are creating a new inflation environment.

Energy markets remain vulnerable to geopolitical conflict. Climate related disruptions continue to threaten food production. Trade barriers are increasing production costs, while the rapid expansion of artificial intelligence is reshaping industrial demand and supply chains. At the same time, strong labor markets and expansionary fiscal policies continue to support consumer spending.

Individually, policymakers can argue that each of these factors is temporary or outside the influence of interest rates. Collectively, however, they reinforce one another and increase the likelihood that inflation remains above target for longer than anticipated.

For the Federal Reserve and other major central banks, the risk is no longer simply misjudging one temporary shock. The greater challenge is determining whether today’s inflation reflects a lasting structural shift in the global economy. If these pressures persist simultaneously, policymakers may be forced to maintain higher interest rates for longer, even at the cost of slower growth, making the path back to price stability significantly more difficult than markets currently expect.

This important question can easily cost holidaymakers extra cash

Tourists need to pick this option when paying for items abroad to avoid ‘hidden fees’(Image: Getty)

People going on holiday this summer should know this simple money mistake to avoid as it could needlessly cost you more without realising. The ‘rule’ to remember is very simple, according to money and travel experts.

Travel specialist Kate Donnelly (@Thedonelleyedit) claims that all British people heading abroad this summer should remember one important thing that could result in hidden fees when on holiday. She said that we all have the option to avoid these, even if the choice seems clear and convenient.

She said: “When you are abroad, you should always pay in the local currency. Whether that’s euros or dollars, depending on where you are, and you should never select the option of paying in Great British Pound (GBP).”

Why does it matter what you choose?

Whether you’re buying a meal or using a cash machine, you should always have the option to pay in local currency instead of DCC. Nobody should choose on your behalf.

Content cannot be displayed without consent

Kate confirmed: “When you’re abroad, and you choose to pay in pounds, you are allowing the ATM or the shop to do the exchange. Within this, there will also be a conversion charge, which is notoriously a really poor rate, meaning you will end up paying significantly more if you pay in the local currency.

“It’s your bank or the card provider that does the exchange. Even if they add on a transaction fee, you are still going to be getting a better rate if you choose to pay in pounds.”

Choosing dynamic currency conversion (DCC) means the amount is converted from the local currency to pounds at the point of sale. But, “DCC usually costs you more”, according to HSBC.

The bank said: “You might choose DCC and pay in pounds because it’s a currency you’re more familiar with. It could give you a better understanding of how much you’re spending. But there are extra fees, and the exchange rate is usually higher.”

Kate added: “The best thing to do when going on holiday is to invest in a fee-free card, such as a Monzo or a Starling. They add no transaction fees, and they also offer the best exchange rate.”

Martin Lewis previously appeared on ITV’s This Morning to talk about this exact issue. He said that the best thing to do, wherever you are in the world, is to pay in local currency to avoid inflated fees.

HEADING abroad can be stressful, from packing all the essentials to leaving for the airport at the crack of dawn.

To make it as easy as possible, take a look at all of the new rules for a smooth-sailing holiday this summer.

Heading on your summer holiday soon? Make sure you read all these new rules firstCredit: Alamy

EES

The Entry/Exit System (EES) is a new system that has been implemented across 29 European countries in the Schengen Area.

These include holiday hotspots like Spain, France, Italy, Greece, Portugal and Germany.

Sign up for the Travel newsletter

Thank you!

EES tracks when you enter and leave European countries by using biometrics and eventually it will replace passport stamping.

Essentially Brits will have to register at a machine and scan their passport – the good news is that you then you don’t have to do it again for another three years.

If you want to find out more on the step-by-step process – head here.

Something else to be aware of about EES is that it has resulted in long queues, so it’s wise to leave extra time when heading abroad.

There have been reports of up to six- hour delays outside of peak travel time at border control at multiple airports.

During the summer, you might experience queues in the arrivals hall, but there have also been travellers who have missed flights on their way home too.

Brits now have to register with EES before heading to the Schengen AreaCredit: AFPThere have been reports of incredibly long queues at border controlCredit: Getty

eGates

There are new rules at UK airports for children which is actually good news for families.

Now, children aged eight and over can now use eGates when accompanied by an adult – they also need to be at least 120cm tall.

The height restriction is in place as kids need to be able to see and be captured by the biometric screens at the eGates.

The rule change impacts 13 airports across the UK that currently use eGates, including:

London Heathrow

London Gatwick

London City

London Luton

London Stansted

Manchester

Birmingham

Bristol

East Midlands

Newcastle

Cardiff

Edinburgh

Glasgow

Passports

Brits heading on holiday are STILL being caught out by passport rules, so it’s worth reminding yourself beforehand.

Passports must be only be valid for 10 years, with any months rolled over from previous passports no longer allowed.

Figures have shown up to 100,000 holidaymakers a year face being turned away atairportsif their passport is more than a decade old.

Make sure your passport is in date before you travelIf you have a burgundy passport – this is likely to run out of date soonCredit: Alamy

For example, if a passport has June 2016 start date but a November 2026 expiry, it has technically expired.

Alongside the requirement to have between three to six months left on it, enforced by a number of countries, it is still causing confusion for travellers.

Most places in Europe only want three months left on a passport, but places like the UAE, Egypt, and Chile require six months in total.

Another passport rule to be aware of only affects those with dual nationality.

A rule that came into effect at the beginning of 2026 means that you can no longer use your foreign passport to enter the UK.

Instead, you have to use a valid British passport.

If you don’t have this, you can apply for a certificate of entitlement, which costs £589.

Visas and travel requirements

Luckily for Brits, citizens can visit more than 170 countries in the world without a visa.

When heading on holiday, families can enter with just their passport to the Schengen Area and most European countries.

In most destinations, you can travel for up to 90 days within any 180-day period – so if you’re going to the likes of Spain for a two-week break, you’re covered.

But there are certain countries where an additional entry requirement is needed.

Most countries in Europe don’t require an ESTA for British citizensCredit: GettyAnyone heading to the USA for a holiday will need a valid ESTACredit: Alamy

Be sure to check the entry requirements in advance as some take a few weeks to come through – although most holiday visas are approved quicker.

For example, if you’re headed to Florida for a theme park getaway to Orlando, then you’ll need to apply for an ESTA.

It costs around £30 per application and can be approved in as little as 72 hours.

Countries where you’ll need a visa or other travel requirement include India, Australia and parts of Egypt.

Until December 31, 2026, UK passport holders can visit China for up to 30 days without a visa.

Holidaymakers are being caught out as surprise charges like currency exchange fees and data roaming and pushing them over their budget

Holidaymakers are spending an extra £100 on hidden fees(Image: Getty Images)

The average holidaymaker overspends their travel budget by more than £100 per trip, with surprise charges identified as the primary culprit. A survey of 2,000 adults who holiday abroad found that currency exchange fees and data roaming are among the most frequent unexpected charges encountered.

Despite 53% claiming they set a firm spending limit before heading off, more than four in ten (43%) say then end up over budget due to unforeseen hidden charges.

To tackle these sneaky fees, seven in ten (70%) said they rely mainly on cash while abroad, while 44% choose to use their debit card instead.

Kat Robinson, head of everyday banking at The Co-operative Bank, which conducted the research as part of its announcement to scrap foreign exchange fees on debit card spending overseas, said: “Spending abroad should be straightforward, but extra card fees can quickly catch people out.

The research also revealed that 34% of people struggle to get to grips with exchange fees. On average, 48% opt to pay in the local currency when using their card abroad which is reported to be the most cost-effective way to pay.

Kat said: “Given the option when spending abroad, always pay in the local currency. Paying in pounds might feel more familiar, but it could mean being hit with extra currency conversion charges from the retailer – a hidden cost that often only becomes clear on returning home.”

Despite the OnePoll.com study finding that the majority of holidaymakers (91%) check exchange rates, one in three admitted they were unsure or unaware that paying in pounds, rather than the local currency, would actually cost them more.

To help holidaymakers dodge unnecessary charges this summer, The Co-operative Bank is scrapping its 2.75% foreign transaction fee on debit card purchases abroad across all its personal current accounts, enabling customers to spend overseas as they would at home without fretting about additional costs.

With millions of Britons jetting off abroad each year, the move is intended to help reduce unexpected charges and better control holiday spending.

Kat added: “By removing foreign transaction fees, we’re making it more affordable for customers to use their debit card overseas and make the most of their money, whether they’re on a family holiday, a city break or exploring somewhere new.

JACKSON, Miss. — The former mayor of Mississippi’s capital city and the former City Council president have pleaded guilty in a bribery scheme one week before they were set to face trial.

Former Jackson Mayor Chokwe Antar Lumumba and former Jackson City Council President Aaron Banks pleaded guilty Monday to one count of conspiracy. Their pleas came after Hinds County District Attorney Jody Owens pleaded guilty last week and resigned. All three are Democrats.

Two other people — Angelique Lee, the Democratic former vice president of the Jackson City Council, and Sherik Marve Smith, a businessman and relative of Owens — had already pleaded guilty to bribery charges.

A November 2024 indictment accused Owens of taking at least $115,000 from two FBI agents posing as real estate developers and facilitating more than $80,000 in bribe payments to Banks, Lumumba and Lee in exchange for their help greenlighting a development project.

Lumumba, Banks and Owens could be sentenced to up to five years in prison. Their sentencing hearings are set for Oct. 15.

Lumumba, who previously called the charges a political prosecution, lost his reelection bid last year. His lawyers did not immediately respond to The Associated Press’ requests for comment.

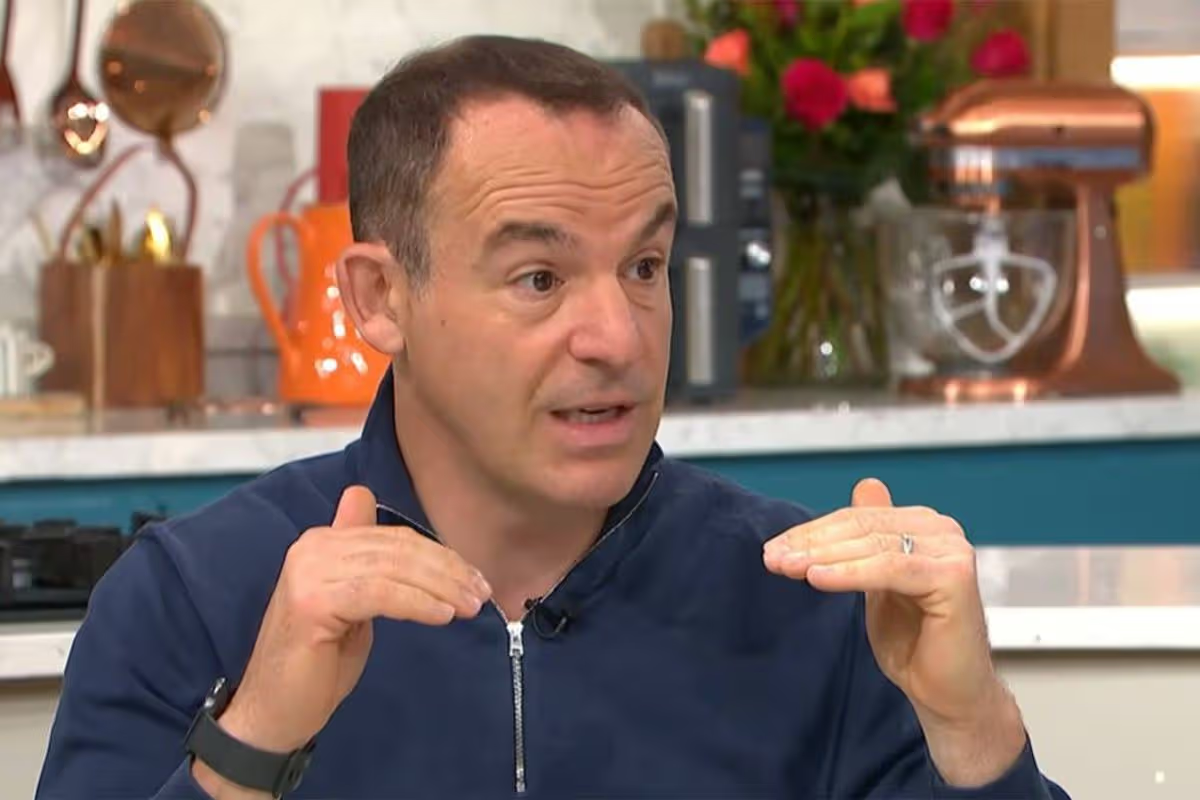

Martin Lewis has shared his top holiday money saving tip, explaining whether you should pay in local currency or pounds on your card abroad – and how it could save you money on extra charges

09:31, 01 Jul 2026Updated 09:31, 01 Jul 2026

Martin Lewis has shared his holiday advice (file image)(Image: ITV)

Martin Lewis has finally settled the age-old holiday debate, revealing whether it’s better to pay in pounds or local currency when using your bank card overseas. Sharing his expert insight with BBC viewers, he cut through the confusion, offering clear guidance on the smartest way to spend abroad without losing out.

Martin advised: “When you go abroad and you pay on plastic [card] and the overseas cash machine or shop asks you: ‘Do you want to pay in Pounds or Euros?’ What do you do?

“Well, the correct answer is you should always pay in euros or whatever the local currency is. That means it’s your plastic that’s doing the exchange rate conversion, not the overseas shop or ATM.”

He stressed that this rule applies no matter where in the world you are. Social media users were quick to chip in with their own tips and experiences. One user suggested: “Just get Revolut or Monzo.”

Another declared: “I use Starling Bank it has no fees abroad and recommends paying in the local currency instead of Pounds. Something I saw online about dynamic exchange rate and it can cost you more otherwise.”

A third added: “Revolut has always been the best on doing this, can exchange right in the app as well, and when withdrawing it’ll just take it straight from that, half the time the only fee is the cash fee by the machine you use.”

Meanwhile, a recent holidaymaker shared their own experience: “Just back from Spain and not a single ATM did free cash withdrawals either, thankfully that’s all I was charged with my Chase account.”

One shrewd traveller commented: “I just get Euros before I go anywhere save all the hassle, and if I’m really stuck for cash go into an actual bank on holiday and withdraw money on my card.”

This handy tip comes on the heels of advice from a money-saving guru who stressed the importance of securing travel insurance ‘ASAB’.

During an appearance on This Morning, the financial whizz revealed: “My travel insurance rule is get it ASAB (as soon as you book). People do get a little confused about this, so let’s break it down.”

He continued to explain: “If you’re getting a single trip policy, so that is a policy to cover just one holiday, then what you do is as soon as you book, you go on one of the travel insurer’s website, you tell it your holiday dates and you buy the policy then.”

Martin Lewis made clear that if your holiday falls in August but you booked back in January, getting your insurance sorted in January is equally crucial.

“That means you have the travel insurance in place to covers that holiday,” he said, adding: “You don’t need to [cover yourself] for extra dates [in case there’s a delay at the airport] because you have your return date.

“If something delays you, so you weren’t back, that would still be covered because that delay is all part of the travel insurance.”

In its Annual Economic Report, published on Sunday, the Bank for International Settlements (BIS), known as the central bank for central banks, warned that the enormous spending on AI is accumulating financial vulnerabilities that could amplify any future shock and spread from markets into the wider economy.

ADVERTISEMENT

ADVERTISEMENT

Presenting the findings, BIS general manager Pablo Hernández de Cos said the message was one of “urgency”, with policymakers urged to act before any reversal makes the eventual adjustment more painful.

At the core of the warning is the scale of the spending, despite massive investment having supported global growth over the past year.

The five largest “hyperscalers”, the technology giants racing to build AI infrastructure, are on track to commit more than $1 trillion (€878bn) to AI-related investment across 2025 and 2026, a pace that is outstripping their earnings and free cash flow and pushing some to borrow heavily to keep up.

The BIS suggests this race is fuelled by a belief that only a handful of dominant players will ultimately prevail, encouraging firms to pour money into projects whose returns remain deeply uncertain.

Echoes of past manias

The report sets today’s AI boom against a long historical lineage, from the canal mania of the 1830s and Britain’s railway mania of the 1840s to the electrification of the 1920s and the dotcom bubble.

Each began with a genuine technological breakthrough that attracted more capital than commercial returns could justify, the BIS notes, with each episode ending “with an eventual reversal in investment, inducing economy-wide recessions”.

Compounding the danger are stretched share prices and opaque financing.

The BIS highlights the spread of “circular financing”, in which chipmakers and cloud giants take equity stakes in AI labs that then commit to buying their chips and computing power, effectively recycling money back to the original investors as revenue.

Much of the funding now flows through hedge funds and private credit vehicles that face lighter scrutiny than banks.

According to Zhang Tao, the BIS chief representative for Asia and the Pacific, that reliance on non-bank channels means an AI downturn could unwind into a sharper, faster crash than a traditional banking crisis.

The hidden costs of data centres

Beyond financial markets, critics argue the true cost of the AI build-out is being obscured in plain sight.

A central concern, examined by the Wall Street Journal, is how the technology giants account for their data centres.

By assuming the expensive equipment inside them will stay useful for longer, firms can spread its cost over more years, lowering the depreciation charged against profits in any given period and making earnings look healthier than the underlying cash burn implies.

However, the specialist chips at the heart of these facilities may become obsolete far faster than those extended schedules assume, leaving a gap between reported profits and economic reality, as well as a balance sheet more exposed than it appears should demand disappoint or a sizable need to replace hardware arise.

The physical scale is staggering.

Columbia University economist Stijn Van Nieuwerburgh estimates the build-out could cost in the region of $8 trillion (€7tn) over the next six years, financed in part through the kind of off-balance-sheet arrangements the BIS flagged.

The costs are also no longer confined to corporate accounts.

Some economists now warn of a so-called “third wave” of inflation, after the pandemic and tariffs, driven this time by the AI build-out. As chip manufacturers prioritise high-margin parts for AI servers, the resulting squeeze on memory and storage has rippled out to consumer electronics.

For example, Apple raised prices on its MacBooks, iPads and other devices last week, citing an “extraordinary surge in demand for memory and storage” and saying it had “never seen a component price increase this much, this quickly”.

The company’s shares fell around 6%, their worst day in over a year, as Microsoft, Nintendo and Sony have also made similar moves.

Beyond hidden costs and inflationary pressures, where the strain may spread furthest is raw power.

Goldman Sachs expects data centres to account for nearly half of the growth in US electricity demand by 2030, with consumer power prices forecast to rise around 6% a year through 2026 and 2027.

The BIS itself notes that the build-out’s hunger for electricity is already pressuring prices and input costs, with potential spillovers to inflation, though it stresses, as do many economists, that AI could yet prove disinflationary if its promised productivity gains eventually arrive.

A view of the Bank of Korea headquarter building in Seoul, South Korea, 15 June 2026. Photo by JEON HEON-KYUN / EPA

June 26 (Asia Today) — South Korean banks are restricting mortgages and personal loans months earlier than usual as rapid household debt growth threatens to exhaust their annual lending quotas.

The country’s five largest commercial banks – KB Kookmin, Shinhan, Hana, Woori and NH NongHyup – recorded household loan growth through May that exceeded targets agreed upon with financial regulators, according to banking industry data released Friday.

Their combined household loan balance increased from 767.296 trillion won ($496.4 billion) at the end of April to 770.823 trillion won ($498.7 billion) at the end of May.

The one-month increase was 3.527 trillion won ($2.3 billion).

Mortgage growth slowed, but personal credit borrowing rose rapidly as a strengthening stock market encouraged more investors to borrow money to buy shares.

Outstanding personal credit loans at the five banks increased by 2.174 trillion won ($1.4 billion), from 104.341 trillion won ($67.5 billion) in April to 106.515 trillion won ($68.9 billion) in May.

Banks have responded by reducing loan limits, restricting online applications and suspending products that allow borrowers to receive larger mortgages.

Hana Bank will suspend enrollment Wednesday in mortgage insurance and guarantee programs that allow banks to lend without deducting an amount reserved to protect tenants’ small security deposits.

Without the programs, the maximum mortgage available for an apartment may fall by about 55 million won ($35,600) in Seoul and 48 million won ($31,100) in Gyeonggi Province.

KB Kookmin Bank suspended the programs Friday, while NH NongHyup Bank had already stopped offering them.

Industrial Bank of Korea also stopped accepting some individual loan applications submitted through outside loan consultants.

Banks have also reduced unsecured credit limits.

Hana Bank and Woori Bank lowered their personal credit loan limits to 100 million won ($64,700).

Shinhan Bank is reducing the limits on revolving credit lines by as much as 20% when customers renew them.

Online lenders KakaoBank, Kbank and Toss Bank have also reduced limits on personal loans and revolving credit accounts and restricted some new lending.

Banking officials said the restrictions began unusually early this year.

Banks ordinarily introduce stronger lending controls around October or November as they approach their annual household loan limits.

This year, however, regulators set substantially lower growth targets and banks are attempting to prevent a rush of applications late in the year.

One banking official said loan applications and inquiries increased after the government signaled that it would continue tightening household debt controls.

Some borrowers are seeking loans earlier because they fear financing will become more difficult later in the year, the official said.

Annual lending restrictions are not new in South Korea.

Banks sometimes receive permission to issue additional loans if their annual limits are exhausted earlier than expected. In other cases, borrowers must delay loans until the following year.

Lee Eun-hyung, a researcher at the Korea Research Institute for Construction Policy, said banks have repeatedly adjusted lending levels to comply with annual debt-management targets.

“Whether additional lending capacity is provided at the end of the year depends on the government’s policy direction and market conditions at that time,” Lee said.

Banking officials said additional lending allocations appear unlikely this year because the government remains focused on controlling household debt and stabilizing the real estate market.

Easing restrictions while housing prices remain elevated could further stimulate demand, they said.

The possibility that banks could exhaust their quotas early has prompted some prospective borrowers to accelerate home purchases or seek loan approval before further restrictions are introduced.

The Civil Aviation Authority (CAA) has issued a warning to passengers about the dangers of packing power banks in hold luggage after a surge in lithium battery incidents on UK flights

13:34, 26 Jun 2026Updated 14:16, 26 Jun 2026

BBC News showed footage of the power bank fire breaking out in the overhead locker of a flight(Image: Getty Images)

UK-based airlines have prohibited a common electrical device labelled the ‘number one safety risk to aircraft’ after footage emerged showing it erupting into flames inside a cabin. Passengers on flights are being urged not to place power banks or vapes in their checked luggage as the busy summer holiday travel season gets underway across parts of the UK.

Several carriers have begun implementing outright bans on power banks that travellers use to charge their phones and tablets amid mounting safety concerns. Generally, power banks are permitted only in hand luggage, not checked baggage, because of worries they could explode and catch fire mid-flight.

Power banks house rechargeable lithium batteries, which pack a considerable amount of energy into a compact space, and when defective can trigger fierce fires that spread rapidly.

Content cannot be displayed without consent

On BBC Breakfast today, correspondent Katy Austin described it as a ‘terrifying situation’ on a recent flight. She said: “Flames broke out in the overhead baggage compartment of an Air China plane last October. The cause is thought to have been a lithium battery. They’re in loads of commonly used devices like laptops, vapes, phones, and power banks. They can store a lot of energy in a small space, but if they overheat or are defective, this video of a test in a lab shows just how quickly a fire can start.

“Last year, UK authorities were informed of 643 incidents where lithium batteries were detected packed in hold bags. That’s nearly twice the number the year before. Reports of devices overheating or malfunctioning also nearly doubled to more than 200. Most were in the cabin where crew could deal with the situation. The fear is that incidents in the hold could not be discovered until it’s too late to control.”

“It contains a lot of energy in a very small space, which is fantastic for, you know, our devices. It means we can use them for longer. But the problem with that is when things go wrong, the fires can be quite ferocious and you can’t put these fires out in the way you can with a normal fire that you might have because these fires are like self fueling.

“The advice for plane passengers is to take items like mobile phones, vapes, and power banks on board with you. Never charge power bank on a flight and turn off laptops completely if they’re going to be put in check-in bags.”

The CAA revealed that reports of passenger devices overheating or malfunctioning last year were almost double the figure from 2024. Instances of lithium battery-powered gadgets being wrongly packed in hold baggage surged by 91% during the same timeframe.

CAA director of aviation safety Giancarlo Buono said: “Pack right for a safe flight, and that means don’t put your batteries in your checked bag. Take them into the cabin with you. This simple tip will make your flight safer for you, and the other passengers you’re flying with.”

Research involving airline passengers revealed that 36% have no idea about the risks associated with packing batteries in hold luggage.

easyJet

EasyJet enforces stringent rules stipulating that all lithium-ion batteries, spare batteries and power banks must be carried in cabin hand luggage only, with a blanket ban on hold luggage due to the risk of fire. Power banks below 100Wh (approximately 27,000mAh) are permitted without prior approval; those between 100-160Wh require authorisation from the airline.

Portable electronic devices containing batteries must be transported exclusively as carry-on baggage.

Should any of these items find their way into checked baggage, steps must be taken to prevent accidental activation and to safeguard the devices from harm; all devices must be completely powered down (not left in sleep or hibernation mode). EasyJet imposes a limit of 15 portable electronic devices per passenger.

Portable electronic devices housing non-spillable batteries must not exceed 12V or 100Wh, and passengers are permitted to carry a maximum of 2 spare batteries. When bringing smart baggage into the cabin, travellers must be able to quickly and easily detach and remove the lithium battery/power bank, although it may remain inside the bag.

Smart baggage will not be accepted for travel if the lithium battery/power bank cannot be readily detached and removed by the passenger. If smart luggage is to be checked into the hold, the lithium battery/power bank must be removed from the smart luggage at Bag Drop and taken into the cabin.

Any exposed terminals must be protected against short circuits. The lithium battery/power bank must be detachable, so if it cannot be removed from your luggage, the bag will not be permitted on board.

Passengers may carry up to 15 personal electronic devices (this includes but is not limited to: smartphones, tablets, laptops, cameras, handheld game consoles, headphones, power banks). Spare lithium batteries (including power banks) must be individually protected to prevent short circuits by placing them in their original retail packaging, or by otherwise securing terminals by taping over any exposed terminals or putting each battery in a separate plastic bag or protective pouch, and must only be transported in carry-on baggage.

Passengers are also permitted to bring up to 20 spare lithium batteries, as long as they don’t surpass 100Wh each. Spare lithium batteries, including power banks taken into the cabin, must not go beyond 100Wh and mustn’t be used to charge or power other portable electronic devices during taxi, take-off or landing.

They must not be placed in cabin baggage stored in the overhead locker. Rather, they ought to be kept in cabin baggage under the seat in front of you, or carried on your person.

Devices or batteries exceeding 100Wh are banned in both the cabin and hold, apart from electric wheelchair batteries. Spare batteries, including power banks, are not allowed in checked baggage.

TUI’s regulations forbid passengers from packing loose lithium batteries, power banks, or spare batteries in checked-in luggage. These items must only be carried in hand luggage.

Power banks must generally not exceed 100Wh, and terminals must be safeguarded against short circuits. Devices shouldn’t be recharged while on board.

Dry AA(A) batteries (type Alkaline, NiMh, NiC) for small personal items such as a pocket torch or a radio are permitted, provided they’re inside the device or contained in sturdy packaging. When devices are placed in hold baggage, measures must be taken to protect the device from damage and prevent accidental activation; the device must be completely switched off (not in sleep or hibernation mode).

Spare batteries and power banks should be individually protected against short circuits by keeping them in their original packaging, with terminals covered in tape or placed in a plastic bag in hand luggage.

Airline approval is always required for medical devices. For further information, see section Baggage – Medical baggage.

TUI fly requires that all power banks must be carried in hand luggage, never in checked baggage. They must be packaged to prevent short circuits (original packaging or terminals covered with tape).

Generally, capacity is limited to 100 Watt-hours (Wh) per battery, with power banks not permitted to be used for charging devices or recharged while onboard.

Hand Luggage Only: Due to fire risk, all lithium-powered battery packs must be in the cabin. Capacity Limits: Power banks up to 100 Wh (roughly 27,000 mAh at 3.7V) are generally permitted.

Safety Requirements: Terminals must be protected against short circuits, such as by taping them or keeping them in individual plastic bags.

In-flight Usage: Power banks cannot be used to charge phones or laptops during flight, nor should they be recharged using aircraft power outlets.

Storage: Keep them in your seat pocket or under your seat, not in overhead bins

Major US banks proved resilient under the Fed’s severe 2026 stress test scenario.

This year’s Federal Reserve Stress Test, which involved 32 U.S. banks, simulated a hypothetical real estate Armageddon in which commercial real estate prices fell 39%, housing prices declined 30%, unemployment spiked to 10%, and economic output dropped commensurately.

The results were encouraging.

Capital declined only 1.6 percentage points in aggregate, according to a Federal Reserve Board statement. All of the banks remained at their minimum common equity Tier 1 capital requirements despite having $708 billion in total hypothetical loan losses.

Of the projected losses, the Fed identified approximately $200 billion in credit card losses, $160 billion in commercial and industrial loan losses, and $75 billion in commercial real estate losses.

“Today’s results underscore the strength of the banking system,” Vice Chair for Supervision Michelle W. Bowman said in a prepared statement. “As we work to increase the transparency and accountability of the stress test, public feedback will help us continue to improve and instill greater confidence in the stress test and its results.”

Compared to last year’s stress test, this one saw a larger decline in aggregate capital due to higher loan losses stemming from increased loan balances and the greater severity of certain test variables, and lower projected unrealized gains in bank securities resulting from smaller hypothetical interest rate declines in the scenario.

The results, however, showed a projected increase in capital from higher interest income driven by recent bank financial performance, offset by the same hypothetical interest rate declines.

Regardless of their results, participating banks will not need to adjust their stress capital buffers since the Fed voted to maintain the current requirements until 2027.

Test Format Change

“This year marks the transition between the Federal Reserve’s existing stress test framework and an updated one that aims to enhance transparency, reduce volatility, and provide opportunities for public comment on the models and scenarios,” said Greg Baer, president and CEO of the Bank Policy Institute, in a statement. “We hope that the revised framework will shed more light on the inputs and provide more certainty. We have also recommended that the most recent Basel proposal be updated to eliminate overlaps with the stress test. These combined changes will allow banks to plan capital more efficiently and support more lending and capital markets financing.”

The Fed opened the 2026 test scenario for comments in October 2025 to improve transparency while avoiding litigation it faced in previous years over opacity and defects in the test itself.

“Capital requirements should not be set in a way that is shielded from meaningful public scrutiny,” the Fed’s Bowman said. “As vice chair for supervision, I am committed to providing transparency and accountability for both the Board and our supervised firms. This is essential for maintaining the value of our stress testing program, and for supervision and regulation more broadly.”

Banks are testing products on fake customers. It’s faster, cheaper, and ethically murky.

Financial institutions are quietly substituting real customers with algorithmic clones to bypass stringent data privacy laws and speed up time-to-market.

Testing a new credit card or AI investment app traditionally takes months of vetting. For bank product developers, the synthetic consumer, who never sleeps or complains to regulators, and costs fractions of a penny to interview, represents a faster, highly attractive alternative, prompting adoption across the industry.

U.S. Bank deploys synthetic audiences to model consumer segments, such as high-net-worth households, and test messaging and refine campaigns before launch. Regulatory sandboxes encourage this practice to keep pace with AI-driven fintech. Barclays, Lloyds Banking Group, and UBS are part of the UK FCA’s AI Live Testing initiative, utilizing advanced AI systems to test products and simulate market stressors.

NatWest, Monzo, and Santander, meanwhile, explore synthetic data ecosystems to train AI models, while JPMorgan Chase generates synthetic financial data to simulate market behaviors for risk management and product design.

Adoption Accelerates, Zero Governance

Industry experts warn that the true challenge is balancing the speed of agentic AI with the need for strong governance.

“Most banking leaders believe agentic AI can move faster if governance weren’t perceived as a constraint. But in practice, governance is what makes these systems deployable at scale. A critical part of that is robust testing against representative ground truth, and synthetic data provides a powerful proxy that enables banks to stress-test products against rare scenarios and edge cases,” said Mudit Gupta, EY Americas Financial Services Consulting AI Practice Leader.

“The trade-off,” he added, “is privacy: synthetic data is often treated as inherently safe when it can still leak sensitive signals through inference and linkage risks. It can also replicate and scale historical biases, embedding them behind a layer of abstraction that makes them harder to detect, audit, and challenge—turning a governance shortcut into a long-term ethical exposure.”

Ultimately, the rush to deploy synthetic consumers offers undeniable speed, but the industry must quickly confront whether these powerful proxies—if not rigorously governed—will fulfill their purpose as a testing shortcut or simply institutionalize Wall Street’s next major ethical crisis.

This article appears in the June 2026 issue of Global Finance Magazine.

Tyra Banks has filed a defamation lawsuit against Netflix and the directors of “Reality Check: Inside America’s Next Top Model” claiming that she was manipulated and misrepresented in the series.

The three-part documentary, directed by married duo Mor Loushy and Daniel Sivan, revisited the reality show’s rise and many controversies, including former contestant Shandi Sullivan discussing what she described as a blackout sexual encounter that took place during Cycle 2 of the series and was a major plot point because Sullivan was in a relationship.

Sullivan said in “Reality Check” that she felt like producers should have stepped in considering she was heavily intoxicated, but instead they followed her into the bathroom and bedroom to record a sexual encounter with a male model. In a following scene, Banks lectures Sullivan about cheating and “carnal” temptation.

“Tyra Banks participated in the Netflix documentary series about ‘America’s Next Top Model’ because she believed viewers deserved a candid conversation about the show’s legacy — its successes and its shortcomings,” reads the lawsuit. “There are aspects of the show for which Ms. Banks takes accountability and she wanted ANTM viewers to hear that from her directly.”

The lawsuit, filed on Saturday in the Central District of California, claims that the supermodel turned media personality participated in a 3½-hour interview, of which about 16 minutes was used.

“The producers used what could be stripped of context and reassembled to support a false and defamatory narrative unrelated to what she actually expressed,” reads the suit. “The accountability Banks took ended up on the cutting room floor.”

The suit alleges that producers used “selective editing, deliberate omission and surgical manipulation of continuous footage” to create a false narrative that Banks “knowingly allowed a contestant to be sexually assaulted on her show, exploited that contestant’s trauma for ratings, and then could not even remember it when asked.”

Banks claims that she asked Netflix and the producers of the docuseries for access to the unedited footage of her 3½-hour interview, and proposed they work together to “correct the record.”

“Had they agreed, Ms. Banks could have made the truth public and this litigation would likely have been unnecessary,” reads the suit.

According to the suit, Banks was pitched the docuseries as a “definitive three-hour Netflix docuseries exploring America’s Next Top Model as a groundbreaking popculture phenomenon.” The pitch had a Netflix logo on its cover, and Banks had “long trusted and admired Netflix.” The streamer’s involvement was the reason Banks claims she considered the project.

Banks claims the pitch included promises that the documentary would unpack the show’s legacy “not as a takedown, but as a thoughtful in-depth reflection on its influence, evolution, and impact on fashion, television, and culture.”

The suit claims Banks was prepared for a fair comeuppance, but ultimately the former supermodel felt hoodwinked. “Nothing suggested that the project would falsely accuse Ms. Banks of covering up a sexual assault, or being indifferent to what a contestant characterizes as a traumatic experience.”

In February, directors for “Reality Check” revealed that Banks wasn’t invited to participate in the docuseries until well after production began

“It was like, ‘Hey, this can be a great addition, but definitely not a necessity,’” Sivan said. “People talking trash about her is very easy to find. … But having her passion, bringing this program to life, is something that only she could tell.”

Sivan and Loushy, who also helmed the acclaimed 2025 docuseries “American Manhunt: Osama bin Laden,” said they treated “Reality Check” with the same level of care as previous heavyweight projects.

“There were things that were sensitive and important for me,” Loushy said, from the harassment that she said “ANTM” contestants endured to the insecurities that “to us as women, are sitting tight and hard every day on our heart.”

The directing duo hoped to examine the good intentions Banks and producers had, of turning the fashion industry on its head, empowering women and championing diversity, and the way those intentions evolved as the show moved through cycles.

“At the end of the day, was it a force of good, or was it a force of evil? I hope people keep debating that,” Sivan said.

Former Times staff writer Malia Mendez contributed to this report.

The EU has proposed a new package of sanctions against Russia, aimed primarily at its banks, cryptocurrency networks, and drone production in response to the ongoing war in Ukraine. This 21st package targets 170 individuals and entities, including close to 90 banks, which would raise the total number of Russian banks under EU sanctions to over 100, or more than half of the country’s internationally connected lenders. These banks will face asset freezes and bans on travel and transactions. The proposal will be presented to EU ambassadors for discussion, requiring unanimous approval to be enacted.

Existing Western sanctions already restrict Russia’s banking system heavily. Many major banks were disconnected from the SWIFT payment system in 2022. Nevertheless, Russian companies have turned to smaller lenders to evade these sanctions. The goal of the new sanctions is to significantly harm Russia’s financial sector and push it toward negotiating peace with Ukraine.

As Russia’s economic growth has sharply slowed, warnings of a potential banking crisis have surfaced, though the central bank claims no crisis is present. The proposed sanctions package includes transaction bans on 35 banks, including some outside Russia, and 11 cryptocurrency platforms that aid in circumventing sanctions. EU leaders indicated plans for even stricter crypto measures in the future.

Additionally, the EU wants to freeze the oil price cap to prevent Moscow from gaining increased revenue amidst geopolitical tensions. Other measures include tighter restrictions on Russian liquefied natural gas, listings of vessels associated with sanctioned activities, and new import restrictions on fish and high-performance metal alloys vital for defense and aerospace sectors.

Avios points are on offer(Image: imageBROKER/Chris Putnam via Getty Images)

A bank is tempting new customers with 10,000 Avios Points.

J.P Morgan Personal Investing confirmed the deal was running until July 31, 2026. The bank revealed customers could put their points towards flights at a time when concerns are mounting over potential fare increases.

The offer is open to new customers who invest £500 or more in a single payment before the end of July.

To qualify for the points, new clients must keep at least £500 invested from August 1, 2026, until February 1, 2027, after which the Avios will be awarded within 55 days of this holding period concluding. New clients can open a Stocks and Shares ISA, Junior ISA, Lifetime ISA, Personal Pension or General Investment Account.

New investors will need to complete the sign-up form, accessible via the promotional page. J.P Morgan reminded customers that their capital was at risk and that transfers in were excluded from the offer.

Claire Exley, head of advice and guidance at J.P. Morgan Personal Investing, said: “Many UK savers are curious about investing for the first time but unsure when to get started. Over the long term, it’s often more important to stay invested over several years than to try to time the market and pick the ‘perfect’ moment.

“For those thinking about starting to invest, our Avios offer is designed to help make that first step in investing feel a little more rewarding. With the cost of travel on many people’s minds, those Avios points could help towards a future holiday or bring a dream trip a bit closer.

“Whether you’re using a Stocks and Shares ISA for the first time, investing for your children, or topping up your pension, what often matters most is choosing an approach you’re comfortable with and staying invested for the long term.”

June 5 (UPI) — The Treasury Department on Friday issued an advisory that financial institutions, including banks and casinos, to “be vigilant” against signs of unlawful employment of illegal immigrants.

The Department’s Financial Crimes Enforcement Network, called FinCEN, in the advisory calls on the institutions employ methods to detect schemes covering up the employment of people who are not authorized to work in the United States.

Treasury Secretary Scott Bessent said in a FinCEN press release that part of the Trump administration’s crackdown on illegal immigration includes “securing our financial system.”

“This administration will not allow illegal aliens to abuse financial institutions to steal billions of dollars from hardworking American taxpayers,” Bessent said.

In order for non-immigrants to work in the United States, employers are required to petition with U.S. Citizenship and Immigration Services for eligibility, before a prospective employee either applies to the State Department for a visa or enters the country through a port of entry, according to USCIS.

FinCEN said in the release that the hiring, concealing and exploiting of workers without visas can give employers advantages over other businesses, depress wages, facilitate identity theft and steal tax revenue from the United States.

The agencies additionally said that the hiring of these workers can also help fund and assist criminal enterprises that include drug trafficking and human trafficking.

The financial institutions are being asked to watch out for red flags of shell companies, identity theft, fraudulently used social security and worker identification numbers, shell companies and a raft of other detectable signs of fraud.

In addition to depository institutions such as banks, credit unions, money services businesses and securities and futures firms, FinCEN has aimed the advisory at casinos, the insurance industry, mortgage companies and brokers, and the precious metals and jewelry industries.

The Treasury Department said that more than $2.5 billion in suspicious activity reported by financial institutions was linked to payroll fraud schemes in 2025 alone, noting one multi-year scheme that cost the United States more than $38 million in tax revenue.

President Donald Trump discusses renovations to the Lincoln Reflecting Pool and makes an announcement on coal in the Oval Office at the White House on Thursday. Photo by Samuel Corum/UPI | License Photo

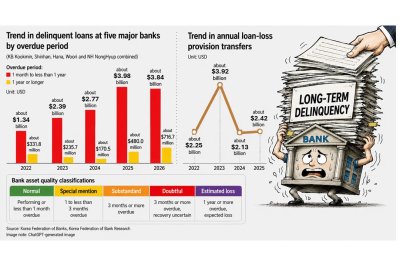

South Korea’s five major banks saw long-term delinquent loans rise to about $716.7 million in 2026, while loans overdue for one month to less than one year remained elevated at about $3.84 billion. Data from Korea Federation of Banks and Korea Federation of Bank Research. Graphic by Asia Today and translated by UPI

June 3 (Asia Today) — South Korea’s major commercial banks are facing growing pressure from a sharp rise in long-overdue loans, with the amount of loans unpaid for more than one year exceeding 1 trillion won, or about $716 million, in the first quarter.

Loans overdue for less than one year, which could later worsen into long-term delinquencies, also approached 6 trillion won, or about $3.84 billion. The increase suggests that borrower distress is deepening, especially among corporate borrowers, despite banks’ efforts to dispose of nonperforming loans.

The sequential expiration of COVID-19 loan maturity extensions also appears to be adding pressure on delinquent borrowers.

Banks, which have continued to post strong earnings, are concerned that rising long-term delinquencies could increase loan-loss provision burdens. The longer a loan remains overdue and the lower its chance of recovery becomes, the more banks must set aside in provisions.

If the Bank of Korea raises its base rate in the second half, borrowers’ repayment burdens could grow further, increasing the risk of additional long-term delinquencies. Analysts say asset quality management could become a key factor determining banks’ earnings performance.

According to financial industry data released Wednesday, the combined balance of loans overdue for at least one year at KB Kookmin Bank, Shinhan Bank, Hana Bank, Woori Bank and NH NongHyup Bank reached 1.0972 trillion won, or about $716 million, in the first quarter.

That was up 49.3% from 734.9 billion won, or about $480 million, a year earlier. Compared with 261 billion won, or about $170 million, in 2024, the figure has more than quadrupled. It was also more than double the 508 billion won, or about $332 million, recorded in 2022 during the COVID-19 pandemic.

The increase appeared across all five banks. By bank, NH NongHyup had the largest balance of long-term overdue loans at 474.8 billion won, or about $310 million, followed by KB Kookmin at 166.9 billion won, or about $109 million, Hana at 155.2 billion won, or about $101 million, Shinhan at 151.5 billion won, or about $99 million, and Woori at 148.8 billion won, or about $97 million.

Loans overdue for at least one month but less than one year totaled 5.8851 trillion won, or about $3.84 billion, approaching the 6 trillion won mark. The figure was slightly lower than 6.1002 trillion won, or about $3.98 billion, a year earlier, but remained high by historical standards.

By category, loans overdue for at least one month but less than three months rose from a year earlier to 2.8225 trillion won, or about $1.84 billion. Loans overdue for at least six months but less than one year, which are considered more likely to become long-term delinquencies, reached 1.1111 trillion won, or about $726 million. Both were record highs since the banks began disclosing the relevant data.

The surge in long-term delinquencies is widely attributed to a sharp increase in new overdue loans in 2024 and 2025. Higher interest rates and weak domestic demand weakened borrowers’ repayment capacity, with some distressed borrowers slipping into long-term delinquency.

The increase appears particularly concentrated among corporate borrowers, whose loans are relatively large and harder to recover. At the end of March, the banking sector’s corporate loan delinquency rate stood at 0.68%, up 0.06 percentage point from 0.62% a year earlier.

“Distress pressure has continued for a long period in sectors such as construction and real estate leasing because of the weak housing market,” an official at a commercial bank said.

A renewed period of rate increases could add to the problem. The Bank of Korea left open the possibility of at least one base rate increase in the second half during last month’s monetary policy meeting, raising concerns that banks could face greater asset quality pressure.

Higher base rates can push up market rates, including bank bond yields, increasing borrowers’ interest burdens. That could deepen distress among loans already in arrears and increase new delinquencies, potentially expanding the volume of long-term overdue loans later.

That would likely translate into higher loan-loss provisions for banks. Banks classify loans into five asset-quality categories: normal, precautionary, substandard, doubtful and estimated loss.

When a loan is classified as substandard, banks must set aside provisions equal to 20% of the loan amount. As the overdue period grows longer and repayment capacity worsens, the required provision ratio rises. Doubtful loans, which are overdue for more than three months and have low recovery prospects, require 50% provisioning. Loans classified as estimated losses after more than one year overdue require 100% provisioning.

That means if a doubtful loan deteriorates into an estimated loss, the provisioning burden doubles.

A rise in provision expenses would directly weigh on bank earnings. In 2022, the five major banks set aside 3.5422 trillion won, or about $2.31 billion, in annual loan-loss provisions, while their combined net profit rose 18.6% from a year earlier to 13.7472 trillion won, or about $8.98 billion.

But in 2023, when banks set aside more than 6 trillion won, or about $3.92 billion, in provisions because of real estate project financing distress and other factors, their net profit growth slowed to 2.6%.

Provision expenses fell sharply the following year, but as delinquencies continue to rise, the possibility of renewed growth in provisions has increased. Analysts say careful risk management has become more important.

“As the delinquency period lengthens, the sale price of nonperforming loans tends to fall, so if long-term delinquencies increase, banks disposing of bad loans will also face greater loss burdens,” a financial industry official said.

“The key will be whether banks can prevent new distress from expanding while effectively clearing existing bad loans,” the official said.

Rescue workers have pulled stranded farmers from flood waters in eastern Syria after the Euphrates burst its banks. Among the worst-affected areas was Deir Az Zor, where the flooding caused a bridge collapse and cut-off communities.

The Civil Aviation Authority today said ‘more awareness’ was needed as travellers ‘not aware’

The Civil Aviation Authority said portable chargers carry ‘serious risks’ of overheating or catching fire in luggage(Image: Getty)

Airlines have banned very common electrical items from flights – as news emerged of a surge in problems on flights caused by the items. Some carriers have begun to completely ban power banks that people use to charge their phones and tablets due to safety concerns. Generally, power banks are only permitted in carry-on, not checked luggage, amid fears they could explode and catch fire mid-flight.

The Civil Aviation Authority (CAA) today said ‘more awareness’ was needed as portable chargers carry ‘serious risks’ of overheating or catching fire. Jonathan Nicholson from the CAA told BBC News that restrictions such as not putting the devices in checked luggage were not “somebody being pedantic” or “for the sake of it”, with passengers urged “to do the right thing”.

Concerns are rising that people are ignoring the bans and simply taking the devices on board. Power banks have become popular because they offer essential, portable, and fast-charging power for smartphones and other devices while on the move, easing battery anxiety. They are affordable, compact, and versatile, enabling users to remain connected without needing a wall outlet, making them perfect for travel.

It comes after a UK-bound easyJet flight was diverted to Rome last week because a passenger had packed a charging power bank in hold luggage. The airline said the captain had decided to divert “in line with safety regulations” after a passenger informed crew during the flight that the portable charger was in the hold of the aircraft. Many airlines have toughened rules on power banks, often requiring that they be stored in hand luggage because of the risk of lithium-ion batteries catching fire.

The flight touched down safely at Rome Fiumicino and was rescheduled to the next day. A survey by the CAA of 1,000 UK passengers in November 2025 suggested more than a third know what lithium batteries are and are aware rules exist, but are unsure what the rules involve. Over-55s typically knew the rules better.

Mr Nicholson said the “basic set of international rules” all passengers must follow on power banks are:

Take them with you on board the aircraft, not in checked luggage

A maximum of two power banks per passenger

When on board the aircraft, don’t use them and “absolutely do not charge the power bank itself because that’s when they become really hot and most susceptible to having an issue”

Mr Nicholson said incidents involving power banks were “certainly on the rise” as portable chargers grow in popularity, alongside vapes which are not allowed in checked luggage either.

Vietnam Airlines, Vietjet Air and now Emirates have banned the batteries. Emirates states, like many airlines, the devices cannot be used during flight. In certain circumstances, they will be permitted on planes provided they are switched off and stored under your seat – not in the overhead cabin – with these rules coming into effect in October.

According to UK Civil Aviation Authority (CAA) safety experts, lithium batteries pose a danger on planes primarily because of their potential to enter “thermal runaway,” a phenomenon where a battery undergoes a rapid, uncontrollable rise in temperature, leading to fire, explosion, and the release of toxic fumes. Ryanair, easyJet and TUI all have regulations in place concerning power banks, batteries and electrical devices.

Ryanair

You may carry up to 15 personal electronic devices (this includes but not limited to: smartphones, tablets, laptops, cameras, handheld game consoles, headphones, power banks). Spare lithium batteries (including power banks) must be individually protected to prevent short circuits by placement in the original retail packaging or by otherwise insulating terminals by taping over exposed terminals or placing each battery in a separate plastic bag or protective pouch and carried in carry-on luggage only.

You may also carry up to 20 spare lithium batteries, provided they do not exceed 100Wh each.