Western Europe’s banks were well capitalized, digitally evolving, and strategically acquisitive—despite rate headwinds.

After the exceptional windfall years of 2022 and 2023, when aggressive rate hikes fattened net interest margins, most Western European banks had a strong 2024, particularly the larger players with extensive branch networks and franchises. Fast forward to 2025, and a more sobering reality dawned. The European Central Bank’s (ECB’s) easing cycle was well underway, and with it came the question that had been quietly forming in the minds of analysts and investors alike: Could Western Europe’s banks sustain their profitability once the rate tailwind turned to a headwind? The evidence now clearly answers that question in the affirmative—though not without adaptation, and not without some pointed lessons along the way.

The headline story is one of structural resilience, corroborated at the highest levels: In the ECB’s Annual Report on Supervisory Activities published in March 2026, the bank confirms that banks under its direct supervision “remained resilient in 2025,” with the aggregate Common Equity Tier 1 capital ratio (CET1 ratio) of “significant institutions” climbing to 16.1% in the third quarter of 2025, driven by strong profitability and retained earnings. Return on equity (ROE) stabilized at around 10% across the sector—modest by the standards of the best performers in our latest Best Banks ranking.

Separately, the European Banking Authority’s (EBA’s) Autumn 2025 Risk Assessment Report affirms that European banks “remain strong in capital, liquidity, profitability and asset quality,” even as the report urges “continued vigilance” in the face of geopolitical uncertainty and rising operational risks. This picture is richly illustrated by the individual performers in this year’s awards, where CET1 ratios frequently exceed the European average by a wide margin.

Yet the year was not without its disappointments. Margin pressure was real, and pockets of weakness were visible. The EBA itself warns that declining net interest income has been a systemic challenge, offset only where banks had successfully diversified into fee and commission income.

That diversification imperative made M&A one of the defining strategic trends of the period—and it shows no sign of abating. DNB’s acquisition of Nordic asset manager Carnegie Holding and Bank of Cyprus’ purchase of Ethniki Insurance, for example, reflect a sector in active pursuit of scale, complementary revenue streams, and fintech capability.

KPMG 2025 Banking and Capital Markets CEO Outlook, published January 2026, adds important context here, however: “The vast majority of CEOs surveyed expect to be active in the deal market over the coming three years, although fewer envisage ‘high-impact’ deals (down from 48% to 41%). Instead, 46% favor ‘moderate-impact’ acquisitions, primarily targeting fintechs, digital lending platforms, and RegTech [regulatory technology] firms to accelerate innovation without overextending capital.” Overall, European banks recognize a strategic need for scale, with momentum toward both domestic consolidation and cross-border deals and are hoping that a more favorable regulatory environment may emerge to support this.

In Western Europe, technology and ESG have become structural pillars rather than peripheral initiatives. Danske Bank has leaned into generative AI (Gen AI) to support retail investment growth, while UBS CEO Sergio Ermotti highlights the role of transformational AI projects in bolstering operational resilience as the Credit Suisse integration approaches completion. Swedbank’s 99.9% digital uptime across Swedish and Baltic operations is now as commercially significant as any lending figure. On sustainability, Eurobank leads its Greek peers with over €6.9 billion ($8.1 billion) in sustainable financing; UniCredit has issued €6.5 billion in green bonds since 2021; and CaixaBank has become the first Spanish bank to receive a Sustainable Finances certification from AENOR, the Spanish Association for Standardization and Certification.

But the technological evolution carries a shadow. According to the KPMG CEO Outlook, cyber risk is now the number-one factor that could slow growth—cited by 86% of banking CEOs, up from 81% in 2024—and cybersecurity ranks as the top challenge facing banks globally, ahead of every other sector in KPMG’s survey. This reflects the uniquely exposed position of banks, whose large customer bases and access to highly confidential data make them prime targets. As digital-banking platforms, open-banking APIs, and AI tools expand attack surfaces, hackers are increasingly deploying AI to pursue payment fraud and install ransomware. It is little surprise, then, that 57% of banking CEOs are “prioritizing cybersecurity above all other investments.” The EBA echoes this concern, warning that elevated geopolitical risks are amplifying operational and cyber threats, and that banks must invest continuously in resilience infrastructure.

As we publish our annual Best Banks award winners, the outlook is cautiously optimistic. Rate normalization will continue to test income generation; geopolitical friction shows no sign of resolution. But the weight of evidence—from individual bank results, from the EBA, and from the ECB itself—points consistently in the same direction: Western Europe’s leading banks have diversified their revenues, fortified their capital, and earned ratings improvements to match. Resilience, it turns out, is not merely a buzzword for these banks—it’s a strategy.

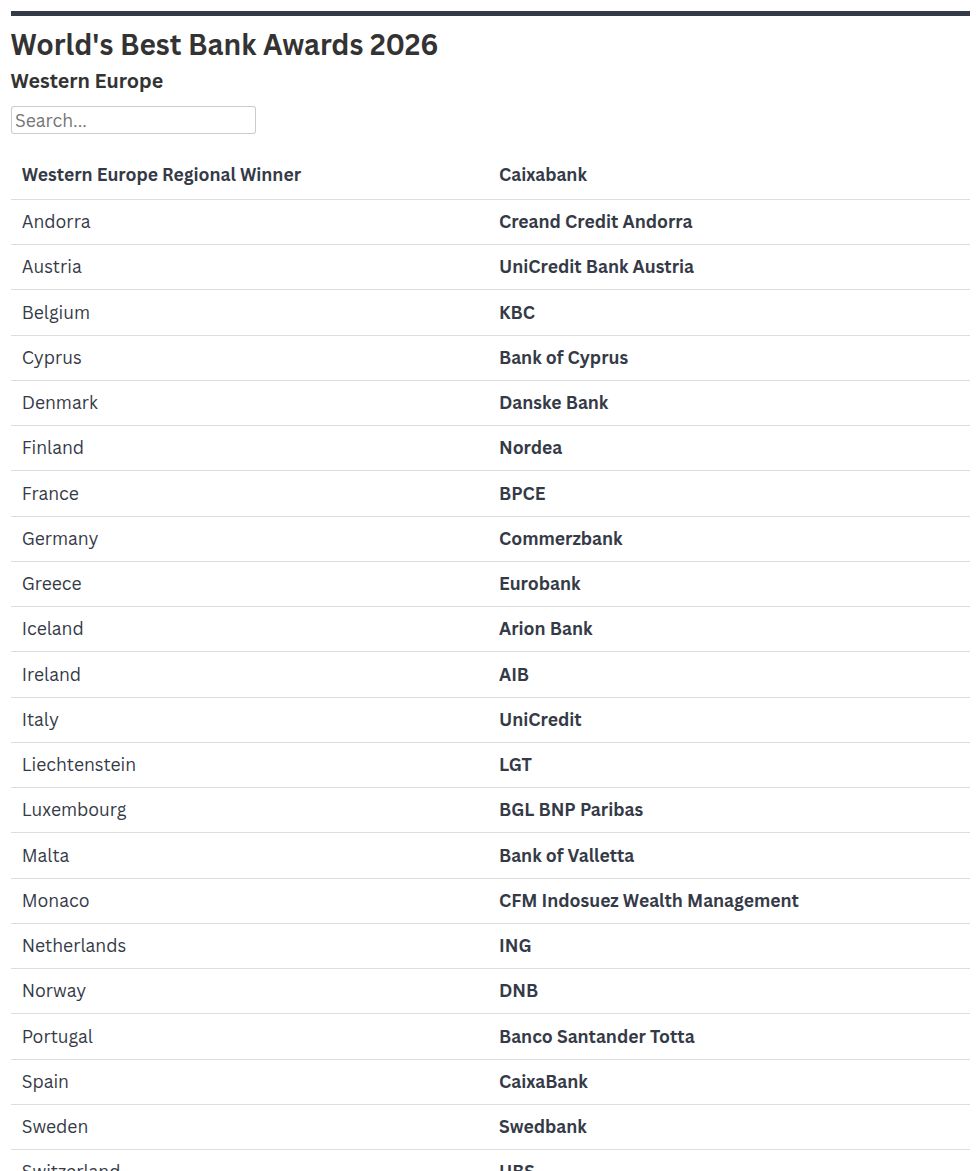

Western Europe

CaixaBank

Once again, CaixaBank has secured a dual victory as the Best Bank in Western Europe and the premier financial institution in its home country, Spain—a distinction the bank has now achieved for a remarkable eight consecutive years.

A domestic market leader, CaixaBank operates a “socially responsible universal banking model with a long-term vision, based on quality, proximity, omnichanneling, and specialization.”

The bank reports a net attributable profit of nearly €5.9 billion for 2025, net interest income of almost €10.7 billion, and an ROE of 14.9%. Revenues from services—including wealth management, protection insurance, and banking fees—were up 5.4% to nearly €5.3 billion. New loan origination to individuals grew 12.4% to almost €2.6 billion. New mortgage lending rose 6.5% to reach nearly €8.5 billion, while lending to businesses increased 7.6% to reach about €12.4 billion.

Exceeding both targets and expectations, CaixaBank has raised the growth and profitability targets set out in its 2025-2027 Strategic Plan.

CaixaBank’s commitment to the communities it serves was evident once again last year, with initiatives encompassing financial-inclusion solutions with a social impact, regional social projects, and a steadfast commitment to the environment. The bank is an Iberian and European leader in sustainable and socially responsible investment.

Reflecting the strength of the bank’s performance, Fitch Ratings revised CaixaBank’s Outlook to Positive from Stable in October while affirming both its Long-Term Issuer Default Rating and its Viability Rating at A-. Fitch also upgraded the bank’s Short-Term IDR to F1 from F2.

The agency says its outlook reflects its “expectation that CaixaBank’s leading domestic position and diversified business profile will enable it to capture additional growth opportunities stemming from Spain’s economy, rising credit demand and favorable business trends,” adding that these factors will “gradually strengthen CaixaBank’s earnings resilience through the interest rate and economic cycles.”

Andorra

Creand Credit Andorra

The winner for the eighth consecutive year, Creand Credit Andorra (formerly Credit Andorra) boasts over 75 years of experience in the principality, offering a comprehensive suite of global private banking, asset management, and insurance services. The bank posted a robust 2024 profit of €70.9 million, representing a solid performance following its exceptional 60% profit surge in 2023. Business volume reached €30.7 billion, an 11.1% year-on-year (YoY) increase. Beyond the group’s financial strength, it remains a key local employer with 508 staff in Andorra, where women make up 48% of the workforce.

Austria

UniCredit Bank Austria

One of the largest retail banks and best-capitalized major financial institutions in Austria, UniCredit Bank Austria is a leader in corporate banking, wealth, and private banking. As of September 2025, the bank’s key performance indicators included a return on allocated capital of 23% and a cost-income ratio of 39%—demonstrating best-in-class cost efficiency compared to its peers. The bank’s CET1 ratio of 18.6% reflects a prudent capital base. Revenues came in at €2 billion, while gross operating profit stood at €1.2 billion. UniCredit serves around 15 million clients through its corporate, individual, and payment solutions groups in Austria, Germany, Italy, and Central and Eastern Europe. Reporting its 20th consecutive quarter of profitable growth in the fourth quarter, the group says its vision is to be “the bank for Europe’s future.”

Belgium

KBC

In the beating heart of Europe, KBC wins the laurels as our Best Bank in Belgium. Net income at the end of June 2025 was €1.6 billion, up 9% YoY. Total assets were €390.7 billion. The group reported a strong capital base with a 14.6% CET1 ratio and an ROE of 15% for the period. A FTSE4Good Index Series constituent, the bank continues its sustainability journey, receiving recognition annually in the S&P Sustainability Yearbook of top performers.

Cyprus

Bank of Cyprus

It was another year of robust performance for Bank of Cyprus, which saw total assets rise 8% to €28.6 billion in 2025. While profit after tax moderated slightly to €481 million (down 5% YoY), the bank’s 37% cost-income ratio and strengthened 21% CET1 ratio underscore its market-leading efficiency and capital discipline. The bank’s €29.3 million acquisition of Ethniki Insurance Cyprus marked a significant step in diversifying its business model and bolstering noninterest income streams.

Denmark

Danske Bank

Offering a full range of retail, corporate, and institutional services, Danske Bank returns as our Best Bank in Denmark for the third time in a row. In 2025, a resilient Danish economy contributed to a 5% growth in business lending and a surge in retail investment activity that pushed assets under management (AUM) across the group to over 1 trillion Danish kroner (more than $157.3 billion). The bank’s Danish operations served as the primary engine for a group ROE of 13.3%. Growth was also supported by new partnerships and digital rollouts, including platform enhancements and the use of Gen AI. The bank maintained a robust CET1 ratio of 17.3% and a CAR of 20.9%, reflecting highly disciplined capital management by both European and Nordic banking standards.

Finland

Nordea

Returning to the top spot as our Best Bank in Finland, Nordea reports a record €478 billion in AUM in 2025, up 13% YoY. With an ROE of 15.5% and a CET1 ratio of 15.7%, this profitable, efficient universal bank drew its 2022-2025 strategy to a successful close. That included receipt of approval from the Finnish Competition and Consumer Authority for a partnership with domestic rival OP Financial Group to combine efforts in solving consumer and business payments challenges.

France

Groupe BPCE

Groupe BPCE’s net banking income was up an impressive 10% YoY to €25.7 billion in 2025; while gross operating income rose some 22% to reach some €8.4 billion. Bolstered by a CET1 ratio of 16.5%, the banking group employs 100,000 staff, serving 35 million customers worldwide, including consumers, professionals, companies, investors, and local authorities. The banking group says it plans to recruit 16,000 employees in 2026, including 10,000 in the Banques Populaires and Caisses d’Epargne networks. Nearly half of these recruitments will target young people, as part of the bank’s partnership with state-run agency France Travail.

Germany

Commerzbank

Another year, another record net income, and another win for Commerzbank—our Best Bank in Germany for the fourth year running. Net income for the first half of 2025 was up 0.9% to €1.3 billion; while total assets reached €582 billion, and total revenues rose 12.5% to €6.1 billion. Despite a dip in the bank’s CET1 ratio to 14.6% and its ROE to a low 8.1%, Commerzbank improved its cost-income ratio to 56% while absorbing €534 million in restructuring expenses. The Frankfurt-based financial institution continues to fend off a UniCredit takeover, a move the Italian giant has pursued since 2024. With almost 40,000 employees, Commerzbank’s ESG goals include net-zero operations by 2040 and portfolio neutrality by 2050.

Greece

Eurobank

Our winner continued its run in Greece; Eurobank achieved remarkable growth across loans, deposits and AUM in the first half of 2025—rising YoY by €5.3 billion, €4 billion, and 30%, respectively. Domestic assets reached €62.8 billion, supported by €37.3 billion in gross loans and €45.2 billion in deposits. Beyond the balance sheet, the group leveraged its performance to drive social impact, strengthening its startup incubator and funding significant public-school renovations. Notably, Eurobank leads its peers with over €6.9 billion in sustainable financing and an upward trend in Article 8 AUM, now exceeding €230 million. Article 8 funds are predominantly ESG compliant. The bank’s market-leading position was further solidified in 2025 through its acquisition of Eurolife’s life insurance business.

Iceland

Arion Bank

Arion Bank may be on the smaller side of the three major Icelandic banks, but what it lacks in size it made up for in efficiency and performance in 2025. The bank reports group AUM of 2 trillion Icelandic kronur ($15.9 billion), net earnings of 30.6 billion kronur, an ROE of 14.9%, a cost-income ratio of 42.3% and a CET1 ratio of 18.4%. Arion Bank’s service offering creates a broad revenue base, with a loan portfolio that is well diversified between retail and corporate customers. The bank is in merger discussions with Kvika Bank, currently the country’s fourth-largest bank, under which terms Arion Bank’s existing shareholders would hold 74% of the combined entity. The merger, which is expected to complete in late 2026, would be one of Iceland’s largest.

Ireland

AIB

AIB returns for a third year running as our Best Bank in Ireland. Serving a customer base of over 3.3 million, the Emerald Isle’s biggest bank posted a solid first half, with a €927 million profit after tax and a 21.4% return on tangible equity (ROTE), bolstered by a robust 16.4% CET1 ratio. 2025 saw the bank return to full private ownership, as well as the launch of its new slogan, “For the life you’re after,” encapsulating its commitments to customers, community, and sustainability.

Italy

UniCredit

Our Best Bank in Italy for the third consecutive year is UniCredit. While gross revenue moderated 3.1% to €11 billion, Italy remains the undisputed earnings powerhouse of the UniCredit group, contributing 41% of the total €10.6 billion net profit. With a unique Pan-European footprint and group assets reaching €870 billion at year-end 2025, UniCredit leverages its stability and low risk exposure to lead the continent’s green transition. The bank is making significant strides toward its 2050 net-zero target, notably through its €11.3 billion in environmental lending and the issuance of €6.5 billion in green bonds since 2021. In 2025, UniCredit deepened its domestic ESG impact through initiatives like Salotti Energia to build ESG awareness among Italian corporates and the One4Planet, Water Management loan. Furthermore, its Banking Academy Italy continues to drive social value, launching the Conta per Me primary school program and advanced fraud prevention training to protect the domestic retail base.

Lichtenstein

LGT

Liechtenstein’s largest player, LGT, continues its six-year unbroken winning streak. Total operating income increased 10% YoY to over 1.4 billion Swiss francs (more than $1.7 billion) in the first half of the year, group profits surged 38% to 240.6 million francs, and AUM reached 359.6 billion francs. While the bank trimmed its cost-income ratio to 75.7%, the figure remains high. Offsetting this is an impressive 18.5% CET1 ratio, reflecting the superior capital strength of this bank owned by the country’s royal family.

Luxembourg

BGL BNP Paribas

Our winner in Luxembourg, BGL BNP Paribas, reported first-half 2025 revenues of €315 million, up from €300 million for the same period in the previous year. With almost 2,100 employees in the Grand Duchy of Luxembourg, the bank provides universal services with a strategic emphasis on corporate and institutional clients. With deep regional roots dating back over a century, BGL BNP Paribas remains a cornerstone of Luxembourg’s economic landscape. Looking ahead, the bank is set to be a key driver of the group’s transition strategy, targeting 90% low-carbon energy financing by 2030.

Malta

Bank of Valletta

Malta’s banking sector remains highly concentrated; and with a 41% market share and total assets of €15.6 billion as of first-half 2025, Bank of Valletta is the most dominant domestic and commercial player in the sector—as well as our 2026 Best Bank in Malta. While the group registered a first-half profit before tax of €135.1 million (slightly down from €148.2 million in first-half 2024), return on average equity stood at 18.9% and CET1 ratio at 21.3%—a breakwater typical of the Mediterranean island.

Monaco

CFM Indosuez Wealth Management

Although its net income for 2024 fell slightly to €59.4 million, a 2.4% decrease from 2023, CFM Indosuez Wealth Management remains the leading player in Monaco. Despite lower interest rates and an unstable geopolitical context, wealth under custody grew 8.4%. “Customer business grew significantly, underpinned by strong new business momentum, a satisfactory performance in market activities and continued robust loan production.” Revenue increased 1.1% to €199.4 million driven by dynamic transactional business, though performance was impacted by a 2.1% rise in operating expenses due to inflation.

Netherlands

ING Group

Amid ongoing geopolitical uncertainty, the CEO of ING Group, Steven van Rijswijk hailed 2025 as a year in which the major global bank consistently executed its “strategy of accelerating growth, increasing impact and further diversifying income by doing more business with more customers and clients.” And so, returning for a third consecutive year, ING is once again our winner in the Netherlands, delivering strong commercial growth in its European base while achieving €23 billion in total income across the group. This was supported by an uptick in the bank’s customer base and a 15% rise in fee income to €4.6 billion. Commercial net interest income meanwhile came in at €15.3 billion. Achieving €56.9 billion in lending growth—more than double that of the previous year—ING’s net result for the year was broadly stable at €6.3 billion. The bank reports a 13.2% ROE and a 13.1% CET1 ratio. Of all its major markets, the Netherlands was a key driver and contributor to the bank’s growth in 2025.

Norway

DNB

Keeping its crown as the Best Bank in Norway for the fourth year in a row, DNB remains the dominant player in its home market, balancing massive scale with high profitability. Offering a full suite of retail, corporate, and investment banking, DNB maintained a strong reputation over the year, reporting an annualized ROE of 15.6%. Profits rose by 1.5% in the first half of 2025 to 21.3 billion Norwegian kroner ($2.1 billion), driven by solid performance across the group, and supported by a Norwegian economy that held up well in an unpredictable global environment. In 2025, the bank completed its 12 billion Swedish kronor ($1.2 billion) acquisition of Carnegie, a Nordic asset manager with 850 employees, strengthening DNB’s position in investment banking and wealth management.

Portugal

Banco Santander Totta

In Portugal, it is another consecutive win for Banco Santander Totta, which continued its growth strategy in 2025 via rigorous commercial and operational optimization. In a year defined by falling interest rates, it remained the most profitable bank and a benchmark for efficiency, posting a 31.8% ROTE and a 28% efficiency ratio while achieving a net profit of €963.8 million.

During this time, the bank continued to grow its customer base, particularly in high-value segments. Active customers increased by 40,000 to more than 1.9 million; while digital customers rose 5.1% to over 1.3 million, now representing 68% of the total base. This growth translated into a growth in commercial activity, with over 100,000 new accounts opened, 1.3 million daily transactions (up by 9.7%), and more than 327,000 new cardholders added.

Sweden

Swedbank

Swedbank had another successful year, with an ROE higher than the bank’s target of 15%—and according to president and CEO Jens Henriksson, “proof that our business model works.” The bank’s Swedish operations account for 71% of the group’s customer base; overall it serves a total of 7.3 million private customers and 545,000 corporate customers across Sweden, Estonia, Latvia, and Lithuania—offering loans, savings, payments, insurance, and daily banking services. In 2025, digital investments contributed to uptime of 99.9% for Swedbank’s app and internet bank for Sweden and the Baltic countries. This is a key focus for the bank as it sets out to improve its customer experience, with the aim “to make it easy to manage everyday matters digitally.”

Switzerland

UBS

For the sixth consecutive year, UBS has earned our Best Bank in Switzerland distinction. Throughout 2025, the bank remained laser focused on the Credit Suisse integration, which is slated for substantial completion by the end of 2026. A disciplined approach yielded a $7.8 billion net profit, supported by a solid 14.4% CET1 ratio, despite an 81.1% cost-income ratio.

CEO Sergio Ermotti attributed this performance to a “global, diversified franchise” that helped clients navigate market volatility. He further highlighted the bank’s digital evolution, noting that transformational AI projects are successfully bolstering operational resilience and improving client experience. As the Credit Suisse integration enters its final stages, industry attention is shifting toward the leadership transition following Ermotti’s planned 2027 departure.

United Kingdom

HSBC

HSBC is our Best Bank in the UK for the second consecutive year. HSBC UK employs 18,000 full-time staff across the country, serving over 15.3 million customers. For the year ending December 31, 2025, it posted a profit before tax of £5.6 billion ($7.5 billion). Revenue increased by £489 million, or 5%, to £10.5 billion, driven by higher net interest income. The bank’s ROTE of 19.2% was one percentage point lower than 2024, driven by growth in commercial lending. Supported by a 13.2% CET1 ratio and an 175% liquidity-coverage ratio, the its balance sheet remained resilient against a challenging economic backdrop.