Jim Ovia steps down as Zenith Bank chairman after 36 years, passing the torch to CEO Adaora Umeoji.

When Jim Ovia founded Zenith Bank in July 1990 at age 38, with NGN 20 million (then about $2.5 million) in capital, Nigeria already had a rich history of indigenous banking institutions. National Bank of Nigeria (1933), African Continental Bank (1937), and Agbonmagbe Bank (1945), later renamed Wema Bank, were among the major banks.

In May, nearly 36 years after Zenith’s founding, Ovia retired as chairman after completing the maximum 12-year tenure permitted under the Central Bank of Nigeria’s (CBN) corporate governance code. Known as the godfather of Nigerian banking, Ovia leaves Zenith as Nigeria’s most valuable listed bank, with more than NGN 30 trillion (about $19.5 billion) in assets and NGN 1 trillion in after-tax profit in 2025.

Zenith was among the institutions that emerged stronger from Nigeria’s landmark 2004–05 banking consolidation, during which the CBN raised minimum capital requirements from NGN 2 billion to NGN 25 billion, reducing the number of the nation’s commercial banks from 89 to 25.

Building an African Banking Empire

The lender has since expanded beyond Nigeria, with subsidiaries in Ghana, Sierra Leone, and Gambia; branches in London, Paris, and Dubai; a representative office in China; and a growing East African presence following the acquisition of Paramount Bank Kenya. Last year, Zenith became the first Nigerian lender to exceed NGN 5 trillion in market capitalization.

Nigerian banking industry leader retiring, symbolizing leadership transition in finance sector.

The leadership transition follows years of internal succession planning. Adaora Umeoji, who joined Zenith in 1998, became the bank’s first female group managing director and CEO in 2024, after a 28-year career at the institution. Under her leadership, Zenith completed an NGN 350.46 billion capital raise, 160% subscribed, comfortably exceeding Nigeria’s new regulatory capital requirements while maintaining record profitability.

Ovia strengthened his financial commitment before stepping down as chairman. In December, five months before retiring, he acquired an additional NGN 14.8 billion in Zenith Bank shares, increasing his holding to 16.2% and cementing his position as the bank’s largest individual shareholder.

Ovia’s leadership laid “the foundation for what has become one of Africa’s most respected and globally recognized financial institutions,” according to the Nigerian Education Loan Fund. Shareholder advocate Boniface Okezie, national coordinator of the Progressive Shareholders Association of Nigeria, terms Zenith “one of the strongest banks in the country because of the solid foundation [Ovia] laid,” and expresses confidence that the lender’s governance framework will remain strong without its founder.

Charles Wachira is a contributing writer based in Kenya.

The Bermuda bank agrees to buy a 91.7% stake in CIBC Caribbean Bank for $1.8 billion, creating a regional giant.

This article appears in the July/August issue of Global Finance Magazine.

Butterfield Group has agreed to acquire a 91.7% stake in CIBC Caribbean Bank Limited for $1.8 billion — $1.09 billion in cash and the remainder in shares — in a deal that would create one of the region’s largest banking groups.

“This deal combines two storied, complementary banks with significant local scale advantages and time-honored customer relationships in their respective core jurisdictions,” said Michael Collins, Butterfield’s chairman and chief executive, in a statement.

The new banking group will hold an estimated $29 billion in assets. The Bermuda-based Butterfield Group—formerly The Bank of N.T. Butterfield & Son Limited—also operates in The Bahamas, the Cayman Islands, the Channel Islands, Singapore, Switzerland, and the U.K. CIBC has a presence in 10 countries and is based in Barbados.

CIBC will hold about 22% of the enlarged Butterfield Group and will have the right to appoint two directors to the board.

The bank’s top brass says the deal underscores a shift in the Caribbean financial sector.

“This is really a change in Butterfield’s positioning because it now picks up both a retail and a business portfolio that spans the entire gamut of the region, and it probably could make it the biggest bank in the region,” former Butterfield CEO Mariano Browne told the Trinidad and Tobago Guardian.

Butterfield has promised to maintain CIBC’s Barbados office. Customers should expect no immediate changes. Existing branches will remain open, and clients can expect improved cross-border payments and expanded consumer, digital, and merchant banking.

The deal, pending regulatory approval, should close in the first half of 2027.

In 2018, CIBC attempted to list FirstCaribbean on U.S. stock markets to raise up to $240 million but withdrew the application less than a month later after failing to drum up sufficient investor interest. A 2019 deal to sell 66.7% of CIBC to GNB Financial Group for $797 million fell through after the deal failed to secure regulatory approval.

Nic Wirtz is a contributing writer based in Guatemala.

Earnings Call Insights: Great Southern Bancorp (GSBC) Q2 2026

Management View

CEO Joseph Turner said results showed “the strength and resilience of our core banking franchise,” while noting Q2 net income of $15.8 million, or $1.43 per diluted share, “was negatively impacted by several one-time expenses

Seeking Alpha’s Disclaimer:This article was automatically generated by an AI tool based on content available on the Seeking Alpha website, and has not been curated or reviewed by humans. Due to inherent limitations in using AI-based tools, the accuracy, completeness, or timeliness of such articles cannot be guaranteed. This article is intended for informational purposes only. Seeking Alpha does not take account of your objectives or your financial situation and does not offer any personalized investment advice. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank.

The Ethiopia-Djibouti corridor sits at the centre of this transformation, serving as the primary gateway for Ethiopia’s import and export flows.

For financial institutions such as iibGroup, the role of banking extends well beyond liquidity provision. It is about deploying capital to support economic resilience, strengthen trade ecosystems, and deliver measurable social and environmental impact.

Embedding Sustainability at Scale

Unlike traditional ESG approaches that operate as standalone initiatives, iib East Africa integrates sustainability directly into its core financing model. As of 2025, over 80% of the bank’s loan portfolio was aligned with ESG-related financing, reflecting a deliberate shift towards impact-driven banking.

This represents a 20% increase in ESG-aligned financing since January 2025, driven by growth in renewable energy, infrastructure financing and trade finance solutions for ESG-compliant businesses. This scale of integration positions iib as the leading ESG-focused financial institution in Djibouti.

Supporting Trade Through ESG-Aligned Finance

Trade finance remains central to East Africa’s economy, yet many SMEs in essential sectors continue to face limited access to structured financing.

iib East Africa has expanded its dedicated trade finance facilities for ESG-compliant SMEs, particularly those involved in food import/export and essential goods. These facilities support regional food security, responsible supply chains and cross-border trade resilience.

By aligning trade finance with ESG principles, the bank ensures capital supports not only commercial growth, but also broader economic stability and sustainability.

H.E. Darren Welch, UK Ambassador to Ethiopia & Permanent Representative to the African Union, and Sohail Sultan, Chairman of iibGroup at the signing ceremony for the Chevening Scholarship partnership in Addis Ababa.

Mobilising Capital for High-Impact Projects

Beyond trade finance, iib is mobilising capital at scale through structured sustainable finance initiatives.

A significant development is a pipeline of approximately US$72.5 million, comprising a planned US$30 million social bond programme, a US$25 million Green Bond, and a US$17.5 million Blue Carbon programme.

The social bond programme is designed to finance high-impact projects including affordable housing, regional food security, essential infrastructure for telecommunications, education and healthcare, and capital for ESG-aligned SMEs.

The Green Bond will improve the energy efficiency of industrial and logistics SMEs.

Meanwhile, the Blue Carbon programme will restore 1,675 hectares of mangroves, preserve a further 780 hectares, establish a 400-hectare protective green barrier and target the sequestration of 2 million tonnes of CO₂. And with a projected investment of US$17.5 million and an expected IRR exceeding 20%, it demonstrates how sustainable finance can generate both commercial returns and measurable environmental outcomes.

Expanding into Ethiopia

By establishing a Representative Office in Addis Ababa, iibGroup has taken an important step in extending this model into one of Africa’s largest and most promising markets.

This expansion supports iib’s strategy of operating as a regional financial intermediary, facilitating cross-border trade, investment and capital flows between East Africa and international markets.

Backed by a robust correspondent banking network of more than 30 relationships across Ethiopia and the wider region, the bank provides trade finance, structured trade, cross-border payments, foreign exchange settlement, liquidity management and risk participation solutions.

Through its presence in Djibouti and Ethiopia, iib is positioned to connect local businesses with international capital while supporting trade, infrastructure and private-sector growth across the corridor, reinforcing its role as a regional connector.

Driving Social Impact Beyond Financing

In frontier markets, sustainable finance extends beyond balance sheet activity. iib East Africa complements its financing activities with direct community engagement that promote inclusive growth.

In 2025, this included:

Food distribution initiatives targeting vulnerable communities.

Literacy programmes and education support.

Environmental campaigns including beach clean-ups and tree planting.

Health awareness initiatives, including breast cancer awareness programmes.

Additionally, the bank is financing a housing project in partnership with Qatar Charity, involving the construction of 79 houses, plus a mosque and Islamic academic centre, representing a total investment of approximately US$500,000.

These initiatives reinforce the principle that sustainable finance should create both institutional and community impact.

A Model for Sustainable Banking in Frontier Markets

As East Africa’s financial systems continue to evolve, banks are becoming active enablers of economic development rather than just financial intermediaries.

iibGroup’s approach – anchored in ESG integration, trade facilitation and capital mobilisation – demonstrates how sustainable banking can be implemented effectively in frontier markets. By aligning financial performance with measurable impact, the bank is contributing to the development of a more resilient, inclusive and interconnected regional economy. Along the Ethiopia–Djibouti corridor, this model is not only relevant; it is essential.

Seventeen major institutions sign on to test around-the-clock liquidity and instant global value transfer.

Swift announced that its blockchain ledger is ready for initial use, enabling early adopter financial institutions to support cross-border payments around the clock using tokenized deposits.

The global cooperative, known for its vast messaging network used by banks to move money, called it a decisive step in scaling the benefits of digital value.

Cross-Border Velocity and Efficiency

So far, 17 banks from six continents are preparing to pilot live transactions on the ledger. They include ANZ, BNP Paribas, BNY, Citi, DBS, First Abu Dhabi Bank, FirstRand Bank Limited, HSBC, Itaú Unibanco, Lloyds Bank, Mashreq, MUFG Bank, OCBC, Standard Chartered, UBS, UOB and Wells Fargo. The shared ledger gives these participating banks a more secure layer for bank-issued tokenized deposits on their own ledgers, Swift argues.

Swift said banks stand to gain an improved client experience and greater global liquidity efficiency—even overnight and on weekends—without compromising existing compliance, credit, risk, and control standards.

It is the first use case for the ledger, which Swift announced last year and said it designed and built with feedback from international financial institutions in nine months. Swift said the development sets the stage for further innovation and interoperability on infrastructure, which it said is trusted to move the equivalent of world GDP every two to three days between more than 200 markets.

“With our new ledger capability, we’re extending the trust and stability of established finance into the frontiers of digital money. It allows tokenised value to move across borders with the velocity and flexibility modern commerce expects, while maintaining the same high levels of resiliency, security, and compliance global finance requires,” Thierry Chilosi, chief business officer at Swift, said in a prepared statement. “The strong support from banks shows the practical value of this approach — one that will help scale benefits globally while creating a foundation for future innovation in areas like programmable money and agentic commerce.”

Meeting G20 Targets

Following its initial go-live phase, Swift plans to expand the ledger’s functionality and availability. This builds on its existing infrastructure, where 75% of network payments already reach beneficiary banks within 10 minutes, or even seconds. The upgrades aim to help the industry meet Group of 20 international transaction targets.

Swift said it is also implementing a retail payments framework with its community aimed at ensuring upfront transparency on fees, full value delivery, and a faster, more consistent experience for consumers. Together with the ledger, Swift said, those upgrades lay the groundwork for value to move in any regulated form, anywhere, with high levels of security and resilience.

Anthony Noto covers corporate finance and private credit. Contact him at anoto@gfmag.com

Major US banks proved resilient under the Fed’s severe 2026 stress test scenario.

This year’s Federal Reserve Stress Test, which involved 32 U.S. banks, simulated a hypothetical real estate Armageddon in which commercial real estate prices fell 39%, housing prices declined 30%, unemployment spiked to 10%, and economic output dropped commensurately.

The results were encouraging.

Capital declined only 1.6 percentage points in aggregate, according to a Federal Reserve Board statement. All of the banks remained at their minimum common equity Tier 1 capital requirements despite having $708 billion in total hypothetical loan losses.

Of the projected losses, the Fed identified approximately $200 billion in credit card losses, $160 billion in commercial and industrial loan losses, and $75 billion in commercial real estate losses.

“Today’s results underscore the strength of the banking system,” Vice Chair for Supervision Michelle W. Bowman said in a prepared statement. “As we work to increase the transparency and accountability of the stress test, public feedback will help us continue to improve and instill greater confidence in the stress test and its results.”

Compared to last year’s stress test, this one saw a larger decline in aggregate capital due to higher loan losses stemming from increased loan balances and the greater severity of certain test variables, and lower projected unrealized gains in bank securities resulting from smaller hypothetical interest rate declines in the scenario.

The results, however, showed a projected increase in capital from higher interest income driven by recent bank financial performance, offset by the same hypothetical interest rate declines.

Regardless of their results, participating banks will not need to adjust their stress capital buffers since the Fed voted to maintain the current requirements until 2027.

Test Format Change

“This year marks the transition between the Federal Reserve’s existing stress test framework and an updated one that aims to enhance transparency, reduce volatility, and provide opportunities for public comment on the models and scenarios,” said Greg Baer, president and CEO of the Bank Policy Institute, in a statement. “We hope that the revised framework will shed more light on the inputs and provide more certainty. We have also recommended that the most recent Basel proposal be updated to eliminate overlaps with the stress test. These combined changes will allow banks to plan capital more efficiently and support more lending and capital markets financing.”

The Fed opened the 2026 test scenario for comments in October 2025 to improve transparency while avoiding litigation it faced in previous years over opacity and defects in the test itself.

“Capital requirements should not be set in a way that is shielded from meaningful public scrutiny,” the Fed’s Bowman said. “As vice chair for supervision, I am committed to providing transparency and accountability for both the Board and our supervised firms. This is essential for maintaining the value of our stress testing program, and for supervision and regulation more broadly.”

Banks are testing products on fake customers. It’s faster, cheaper, and ethically murky.

Financial institutions are quietly substituting real customers with algorithmic clones to bypass stringent data privacy laws and speed up time-to-market.

Testing a new credit card or AI investment app traditionally takes months of vetting. For bank product developers, the synthetic consumer, who never sleeps or complains to regulators, and costs fractions of a penny to interview, represents a faster, highly attractive alternative, prompting adoption across the industry.

U.S. Bank deploys synthetic audiences to model consumer segments, such as high-net-worth households, and test messaging and refine campaigns before launch. Regulatory sandboxes encourage this practice to keep pace with AI-driven fintech. Barclays, Lloyds Banking Group, and UBS are part of the UK FCA’s AI Live Testing initiative, utilizing advanced AI systems to test products and simulate market stressors.

NatWest, Monzo, and Santander, meanwhile, explore synthetic data ecosystems to train AI models, while JPMorgan Chase generates synthetic financial data to simulate market behaviors for risk management and product design.

Adoption Accelerates, Zero Governance

Industry experts warn that the true challenge is balancing the speed of agentic AI with the need for strong governance.

“Most banking leaders believe agentic AI can move faster if governance weren’t perceived as a constraint. But in practice, governance is what makes these systems deployable at scale. A critical part of that is robust testing against representative ground truth, and synthetic data provides a powerful proxy that enables banks to stress-test products against rare scenarios and edge cases,” said Mudit Gupta, EY Americas Financial Services Consulting AI Practice Leader.

“The trade-off,” he added, “is privacy: synthetic data is often treated as inherently safe when it can still leak sensitive signals through inference and linkage risks. It can also replicate and scale historical biases, embedding them behind a layer of abstraction that makes them harder to detect, audit, and challenge—turning a governance shortcut into a long-term ethical exposure.”

Ultimately, the rush to deploy synthetic consumers offers undeniable speed, but the industry must quickly confront whether these powerful proxies—if not rigorously governed—will fulfill their purpose as a testing shortcut or simply institutionalize Wall Street’s next major ethical crisis.

This article appears in the June 2026 issue of Global Finance Magazine.

A veteran dealmaker takes the helm as large-cap M&A shows signs of a selective recovery.

JPMorgan Chase, the global leader in investment banking revenue, has named Anu Aiyengar global chair of Investment Banking and M&A, signaling a renewed emphasis on dealmaking as a pillar of its investment banking strategy.

As part of a broader divisional shift, the bank also named Dorothee Blessing, Kevin Foley, and Jared Kaye as co-heads of Global Investment Banking, while Charles Bouckaert succeeds Aiyengar as global head of M&A.

The changes come as deal activity shows signs of recovery after nearly two years of sluggish momentum. Dealogic estimates that global deal announcements reached nearly $2 trillion by May 11. That’s a 33% increase from the same period last year.

Still, observers note that the current cycle is far from a repeat of the free-flowing deal market of 2021. Higher financing costs have made boards more disciplined about price and timing, while closer regulatory scrutiny from antitrust watchdogs in both the U.S. and Europe has raised the financial and reputational cost of getting large transactions wrong.

A Selective, Large-Cap Rally

“This has not been a full-spectrum, feel-good rally. It has been a highly selective one, skewed toward strategic, large-cap deals,” said Marc Cooper, CEO of Solomon Partners. “Deals valued at $5 billion and up accounted for more than half of all volumes. That distinction matters.”

Against this backdrop, Aiyengar’s appointment suggests JPMorgan sees senior dealmaking expertise as a defining advantage in the current market. The firm expects the dealmaking veteran to work closely with senior clients as boards decide whether to move forward with transactions or wait for better conditions.

Since joining JPMorgan in 1999, Aiyengar has advised on more than $1 trillion in transactions. She became sole head of the bank’s global M&A franchise in 2023, making her the only woman leading M&A at a major Wall Street house at the time.

Her move also carries symbolic weight in an industry where senior dealmaking roles remain dominated by men. In 2025, Business Insider named her the top U.S. M&A banker on its Rainmakers list, making her the first woman to hold the No. 1 position.

Labs are rethinking banking, as AI remains king, but human insight directs banking improvements.

So, the robot banker remains a long way off. But S&P Global estimates that up to 59% of financial institutions worldwide were actively using artificial intelligence in 2025. Beyond simply relying on technology for research (“Summarize new anti-money laundering mandates for me”), financial institutions have begun operationalizing AI processes.

This is a significant advancement. Instead of using AI like an intelligent chatbot, banks now direct systems to perform complex, multi-step tasks—saving untold human hours while both speeding up and improving operations.

How does this newer type of AI (called “agentic AI”) work?

Consider loan processing as an example. Someone applies for a loan. AI agents retrieve credit reports, verify income, calculate debt-to-income ratios, apply underwriting rules, approve or reject applications (or forward them to a human underwriter for approval), and generate documentation. In compliance monitoring, agents can read regulatory texts, map new mandates to internal policies and processes, identify where the financial institution (FI) falls short, generate remediation tasks, and track progress.

For proof of the increased operationalization of AI, look at some of the innovations germinated in the world’s best fintech labs, incubators, and accelerators.

At inovabra, a lab hosted by Banco Bradesco, innovators have developed an AI product that can generate initial drafts of legal pleadings. The Bank of Georgia’s AI Research Lab has launched Software Developer: Powered by Code2Doc.

This software can write other software. And Garanti BBVA Partners has nurtured Skymod, an AI-orchestration platform that enables financial institutions to securely delegate operational workflows to intelligent AI agents.

Knowing When AI Isn’t The Answer

Then there’s TD Lab. TD Lab is now experimenting with Physical AI, or AI-embedded machines (think robots, drones, and smart devices) capable of interacting with the physical world.

“Physical AI is about convergence,” said Chris Halabecki, senior manager and lab leader. “It’s about combining AI with objects that can sense or maneuver through the real world. As a lab team, we’re exploring how we can use physical AI to integrate more intelligence into everyday scenarios to better serve our colleagues and clients today and in the future.”

The lab has already developed proprietary software for a quadruped (robotic dog) device. Using LiDAR (Light Detection and Ranging), which is a sensing technology that uses pulsed laser light to measure distances, and AI together, the quadruped can detect and learn about objects in the surrounding area, then follow commands linked to those objects. Halabecki provided examples such as “Walk to the white couch” and “Go find Evan.”

Future use cases for these technologies may include robots that can count, sort, and verify cash.

One day, robotic relationship managers may recognize when a customer walks into a branch and guide them in making investment decisions. In the field, physical AI may be able to conduct home appraisals and complete other tasks.

With the much-ballyhooed capabilities of artificial intelligence, it’s a little surprising to hear Kadry Boutaina, chief of innovation for the digital transformation lab of Morocco’s Attijariwafa bank, say, “Sometimes, the answer is not AI.”

That doesn’t mean the lab, called Wenov, isn’t driving technological advancements. It works with external startups to offer “more and more digital services for our customers — both retail and business.” Boutaina notes that Attijariwafa faces significant competition in this field, from both established banks and newcomers — notably neobanks entering the Moroccan and broader West African markets.

But providing digital services does not always entail a wholesale AI revolution.

When Banks Let Employees Innovate

The Moroccan Ministry of Economy and Finance recently formalized laws governing crowdfunding in the country. The first regulated platform of this kind is being provided by Kiwi Collecte, a fintech company. Under Moroccan law, Kiwi Collecte may not directly hold or move funds. It must partner with a licensed Moroccan bank for those tasks. A partnership with Attijariwafa empowers the bank to hold and safeguard funds, process payments, and disburse money to beneficiaries.

Fraud prevention is ever important. Sandbox CAIXA has found an old-school way to fight it. Sandbox CAIXA is the innovation lab of Caixa Econômica Federal, a major state-owned bank in Brazil. Lucas Zaccaro, Sandbox CAIXA manager, said that in his country, technologically unsophisticated people are often victimized by scammers. When the bank is closed, thieves stand near ATMs. They then offer to help patrons who are unsure how to use the machines. These criminals “help” by tricking users into revealing their PINs, then stealing their cards.

A “really great idea” from a rank-and-file Caixa employee led the bank to broadcast recorded messages at 10 of these ATMs, warning patrons about the scam. Theft at those banks has stopped.

Zaccaro says that this fraud-prevention idea was submitted through an established process designed to encourage rank-and-file employees to submit innovative ideas. Employees use Microsoft Copilot to refine their concepts and submit them to Sandbox CAIXA for review and potential testing. The lab will now assess the feasibility of rolling out its scam warning across the ATM network—potentially using cameras to detect when people are at the ATM and triggering automated messages.

At the Banking and Financial Institutions Association of Colombia (Asobancaria), the focus is less on rapidly advancing technologies and more on meeting existing societal needs. One development from the Asobancaria Social Innovation Lab is a reference framework for identifying, classifying, and reporting on the banking sector’s social portfolios. This proposal—the second of its kind in Latin America after Guatemala’s Social Taxonomy—was developed through multiple sessions of analysis, technical feedback, and sector-wide validation with member institutions. To create this framework, Asobancaria worked closely with the Global Green Growth Institute (GGGI), which develops social-portfolio standards aligned with the United Nations Sustainable Development Goals.

Andrea Guzmán, GGGI’s sustainable finance officer, said the problem with sustainability reporting among Asobancaria member banks was a lack of alignment on standards, with each bank setting its own measures of success for its social portfolios.

The framework addresses issues such as financial inclusion, social infrastructure, affordable housing, and services for small and medium-size businesses. A single framework to which all member banks agree “improves transparency,” Guzmán says. “It supports better decision-making by investors and helps mobilize more resources for our social sector. It’s a framework we can base bonds on. It’s a framework that helps banks avoid accusations of greenwashing.”

Consider the framework for sustainable and affordable housing. Guzmán notes that in rural Columbia, many houses lack access to water and may have only dirt floors. Therefore, a bank could claim success in affordable housing if it funded units with wood floors, fully plumbed and connected to the electrical grid. But what if those apartments are so far from public transportation that no one can get to work or school? Guzmán said that under the framework, banks agree that any affordable housing projects they fund would have access to the nation’s external infrastructure and social services.

Here’s a closer look at some of the world’s best fintech labs and the innovations they’re nurturing.

The EU has proposed a new package of sanctions against Russia, aimed primarily at its banks, cryptocurrency networks, and drone production in response to the ongoing war in Ukraine. This 21st package targets 170 individuals and entities, including close to 90 banks, which would raise the total number of Russian banks under EU sanctions to over 100, or more than half of the country’s internationally connected lenders. These banks will face asset freezes and bans on travel and transactions. The proposal will be presented to EU ambassadors for discussion, requiring unanimous approval to be enacted.

Existing Western sanctions already restrict Russia’s banking system heavily. Many major banks were disconnected from the SWIFT payment system in 2022. Nevertheless, Russian companies have turned to smaller lenders to evade these sanctions. The goal of the new sanctions is to significantly harm Russia’s financial sector and push it toward negotiating peace with Ukraine.

As Russia’s economic growth has sharply slowed, warnings of a potential banking crisis have surfaced, though the central bank claims no crisis is present. The proposed sanctions package includes transaction bans on 35 banks, including some outside Russia, and 11 cryptocurrency platforms that aid in circumventing sanctions. EU leaders indicated plans for even stricter crypto measures in the future.

Additionally, the EU wants to freeze the oil price cap to prevent Moscow from gaining increased revenue amidst geopolitical tensions. Other measures include tighter restrictions on Russian liquefied natural gas, listings of vessels associated with sanctioned activities, and new import restrictions on fish and high-performance metal alloys vital for defense and aerospace sectors.

Western Europe’s banks were well capitalized, digitally evolving, and strategically acquisitive—despite rate headwinds.

After the exceptional windfall years of 2022 and 2023, when aggressive rate hikes fattened net interest margins, most Western European banks had a strong 2024, particularly the larger players with extensive branch networks and franchises. Fast forward to 2025, and a more sobering reality dawned. The European Central Bank’s (ECB’s) easing cycle was well underway, and with it came the question that had been quietly forming in the minds of analysts and investors alike: Could Western Europe’s banks sustain their profitability once the rate tailwind turned to a headwind? The evidence now clearly answers that question in the affirmative—though not without adaptation, and not without some pointed lessons along the way.

The headline story is one of structural resilience, corroborated at the highest levels: In the ECB’s Annual Report on Supervisory Activities published in March 2026, the bank confirms that banks under its direct supervision “remained resilient in 2025,” with the aggregate Common Equity Tier 1 capital ratio (CET1 ratio) of “significant institutions” climbing to 16.1% in the third quarter of 2025, driven by strong profitability and retained earnings. Return on equity (ROE) stabilized at around 10% across the sector—modest by the standards of the best performers in our latest Best Banks ranking.

Separately, the European Banking Authority’s (EBA’s) Autumn 2025 Risk Assessment Report affirms that European banks “remain strong in capital, liquidity, profitability and asset quality,” even as the report urges “continued vigilance” in the face of geopolitical uncertainty and rising operational risks. This picture is richly illustrated by the individual performers in this year’s awards, where CET1 ratios frequently exceed the European average by a wide margin.

Yet the year was not without its disappointments. Margin pressure was real, and pockets of weakness were visible. The EBA itself warns that declining net interest income has been a systemic challenge, offset only where banks had successfully diversified into fee and commission income.

That diversification imperative made M&A one of the defining strategic trends of the period—and it shows no sign of abating. DNB’s acquisition of Nordic asset manager Carnegie Holding and Bank of Cyprus’ purchase of Ethniki Insurance, for example, reflect a sector in active pursuit of scale, complementary revenue streams, and fintech capability.

KPMG 2025 Banking and Capital Markets CEO Outlook, published January 2026, adds important context here, however: “The vast majority of CEOs surveyed expect to be active in the deal market over the coming three years, although fewer envisage ‘high-impact’ deals (down from 48% to 41%). Instead, 46% favor ‘moderate-impact’ acquisitions, primarily targeting fintechs, digital lending platforms, and RegTech [regulatory technology] firms to accelerate innovation without overextending capital.” Overall, European banks recognize a strategic need for scale, with momentum toward both domestic consolidation and cross-border deals and are hoping that a more favorable regulatory environment may emerge to support this.

In Western Europe, technology and ESG have become structural pillars rather than peripheral initiatives. Danske Bank has leaned into generative AI (Gen AI) to support retail investment growth, while UBS CEO Sergio Ermotti highlights the role of transformational AI projects in bolstering operational resilience as the Credit Suisse integration approaches completion. Swedbank’s 99.9% digital uptime across Swedish and Baltic operations is now as commercially significant as any lending figure. On sustainability, Eurobank leads its Greek peers with over €6.9 billion ($8.1 billion) in sustainable financing; UniCredit has issued €6.5 billion in green bonds since 2021; and CaixaBank has become the first Spanish bank to receive a Sustainable Finances certification from AENOR, the Spanish Association for Standardization and Certification.

But the technological evolution carries a shadow. According to the KPMG CEO Outlook, cyber risk is now the number-one factor that could slow growth—cited by 86% of banking CEOs, up from 81% in 2024—and cybersecurity ranks as the top challenge facing banks globally, ahead of every other sector in KPMG’s survey. This reflects the uniquely exposed position of banks, whose large customer bases and access to highly confidential data make them prime targets. As digital-banking platforms, open-banking APIs, and AI tools expand attack surfaces, hackers are increasingly deploying AI to pursue payment fraud and install ransomware. It is little surprise, then, that 57% of banking CEOs are “prioritizing cybersecurity above all other investments.” The EBA echoes this concern, warning that elevated geopolitical risks are amplifying operational and cyber threats, and that banks must invest continuously in resilience infrastructure.

As we publish our annual Best Banks award winners, the outlook is cautiously optimistic. Rate normalization will continue to test income generation; geopolitical friction shows no sign of resolution. But the weight of evidence—from individual bank results, from the EBA, and from the ECB itself—points consistently in the same direction: Western Europe’s leading banks have diversified their revenues, fortified their capital, and earned ratings improvements to match. Resilience, it turns out, is not merely a buzzword for these banks—it’s a strategy.

Gonzalo Gortázar, CEO, CaixaBank

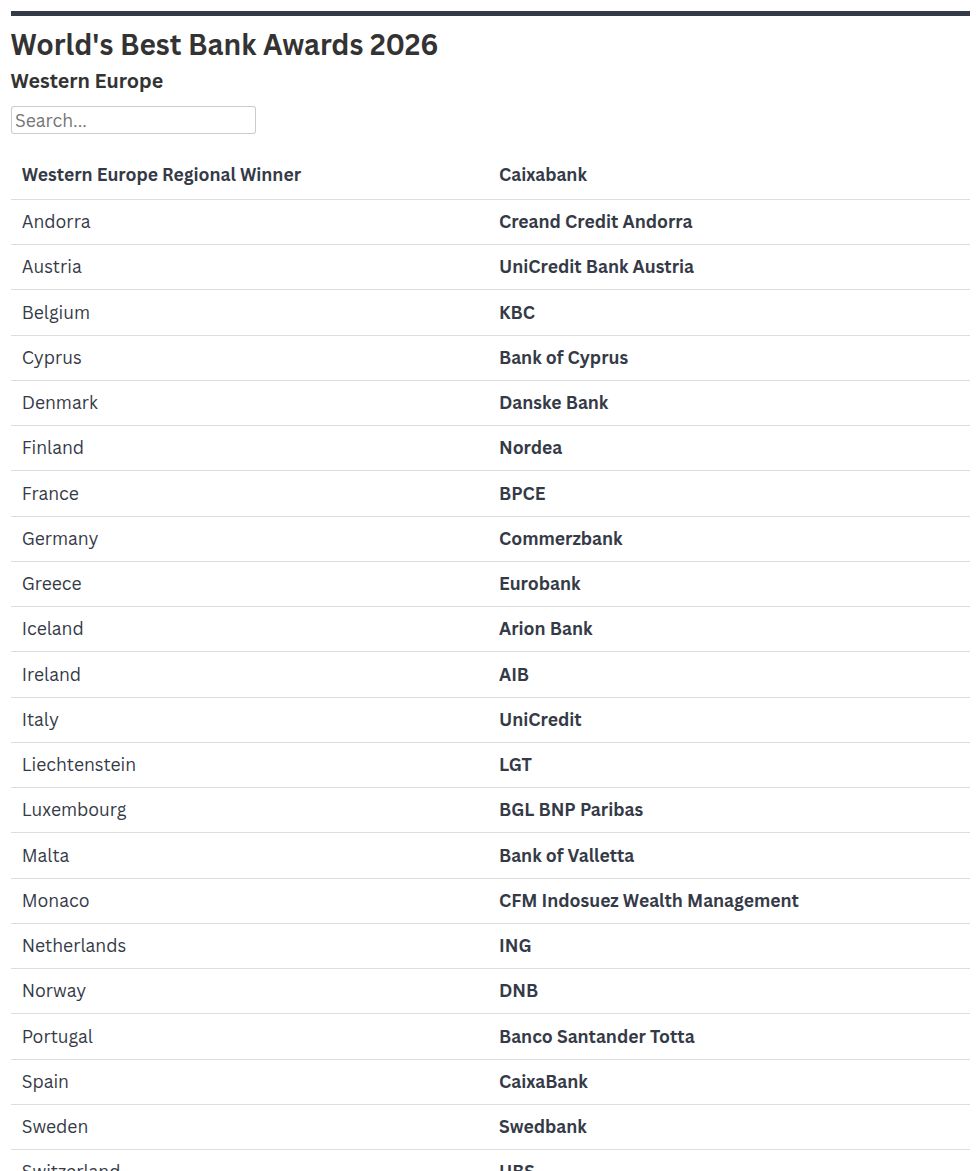

Western Europe

CaixaBank

Once again, CaixaBank has secured a dual victory as the Best Bank in Western Europe and the premier financial institution in its home country, Spain—a distinction the bank has now achieved for a remarkable eight consecutive years.

A domestic market leader, CaixaBank operates a “socially responsible universal banking model with a long-term vision, based on quality, proximity, omnichanneling, and specialization.”

The bank reports a net attributable profit of nearly €5.9 billion for 2025, net interest income of almost €10.7 billion, and an ROE of 14.9%. Revenues from services—including wealth management, protection insurance, and banking fees—were up 5.4% to nearly €5.3 billion. New loan origination to individuals grew 12.4% to almost €2.6 billion. New mortgage lending rose 6.5% to reach nearly €8.5 billion, while lending to businesses increased 7.6% to reach about €12.4 billion.

Exceeding both targets and expectations, CaixaBank has raised the growth and profitability targets set out in its 2025-2027 Strategic Plan.

CaixaBank’s commitment to the communities it serves was evident once again last year, with initiatives encompassing financial-inclusion solutions with a social impact, regional social projects, and a steadfast commitment to the environment. The bank is an Iberian and European leader in sustainable and socially responsible investment.

Reflecting the strength of the bank’s performance, Fitch Ratings revised CaixaBank’s Outlook to Positive from Stable in October while affirming both its Long-Term Issuer Default Rating and its Viability Rating at A-. Fitch also upgraded the bank’s Short-Term IDR to F1 from F2.

The agency says its outlook reflects its “expectation that CaixaBank’s leading domestic position and diversified business profile will enable it to capture additional growth opportunities stemming from Spain’s economy, rising credit demand and favorable business trends,” adding that these factors will “gradually strengthen CaixaBank’s earnings resilience through the interest rate and economic cycles.”

Andorra

Creand Credit Andorra

The winner for the eighth consecutive year, Creand Credit Andorra (formerly Credit Andorra) boasts over 75 years of experience in the principality, offering a comprehensive suite of global private banking, asset management, and insurance services. The bank posted a robust 2024 profit of €70.9 million, representing a solid performance following its exceptional 60% profit surge in 2023. Business volume reached €30.7 billion, an 11.1% year-on-year (YoY) increase. Beyond the group’s financial strength, it remains a key local employer with 508 staff in Andorra, where women make up 48% of the workforce.

Austria

UniCredit Bank Austria

One of the largest retail banks and best-capitalized major financial institutions in Austria, UniCredit Bank Austriais a leader in corporate banking, wealth, and private banking. As of September 2025, the bank’s key performance indicators included a return on allocated capital of 23% and a cost-income ratio of 39%—demonstrating best-in-class cost efficiency compared to its peers. The bank’s CET1 ratio of 18.6% reflects a prudent capital base. Revenues came in at €2 billion, while gross operating profit stood at €1.2 billion. UniCredit serves around 15 million clients through its corporate, individual, and payment solutions groups in Austria, Germany, Italy, and Central and Eastern Europe. Reporting its 20th consecutive quarter of profitable growth in the fourth quarter, the group says its vision is to be “the bank for Europe’s future.”

Belgium

KBC

In the beating heart of Europe, KBC wins the laurels as our Best Bank in Belgium. Net income at the end of June 2025 was €1.6 billion, up 9% YoY. Total assets were €390.7 billion. The group reported a strong capital base with a 14.6% CET1 ratio and an ROE of 15% for the period. A FTSE4Good Index Series constituent, the bank continues its sustainability journey, receiving recognition annually in the S&P Sustainability Yearbook of top performers.

Cyprus

Bank of Cyprus

It was another year of robust performance for Bank of Cyprus, which saw total assets rise 8% to €28.6 billion in 2025. While profit after tax moderated slightly to €481 million (down 5% YoY), the bank’s 37% cost-income ratio and strengthened 21% CET1 ratio underscore its market-leading efficiency and capital discipline. The bank’s €29.3 million acquisition of Ethniki Insurance Cyprus marked a significant step in diversifying its business model and bolstering noninterest income streams.

Denmark

Danske Bank

Offering a full range of retail, corporate, and institutional services, Danske Bank returns as our Best Bank in Denmark for the third time in a row. In 2025, a resilient Danish economy contributed to a 5% growth in business lending and a surge in retail investment activity that pushed assets under management (AUM) across the group to over 1 trillion Danish kroner (more than $157.3 billion). The bank’s Danish operations served as the primary engine for a group ROE of 13.3%. Growth was also supported by new partnerships and digital rollouts, including platform enhancements and the use of Gen AI. The bank maintained a robust CET1 ratio of 17.3% and a CAR of 20.9%, reflecting highly disciplined capital management by both European and Nordic banking standards.

Finland

Nordea

Returning to the top spot as our Best Bank in Finland, Nordea reports a record €478 billion in AUM in 2025, up 13% YoY. With an ROE of 15.5% and a CET1 ratio of 15.7%, this profitable, efficient universal bank drew its 2022-2025 strategy to a successful close. That included receipt of approval from the Finnish Competition and Consumer Authority for a partnership with domestic rival OP Financial Group to combine efforts in solving consumer and business payments challenges.

France

Groupe BPCE

Groupe BPCE’s net banking income was up an impressive 10% YoY to €25.7 billion in 2025; while gross operating income rose some 22% to reach some €8.4 billion. Bolstered by a CET1 ratio of 16.5%, the banking group employs 100,000 staff, serving 35 million customers worldwide, including consumers, professionals, companies, investors, and local authorities. The banking group says it plans to recruit 16,000 employees in 2026, including 10,000 in the Banques Populaires and Caisses d’Epargne networks. Nearly half of these recruitments will target young people, as part of the bank’s partnership with state-run agency France Travail.

Germany

Commerzbank

Another year, another record net income, and another win for Commerzbank—our Best Bank in Germany for the fourth year running. Net income for the first half of 2025 was up 0.9% to €1.3 billion; while total assets reached €582 billion, and total revenues rose 12.5% to €6.1 billion. Despite a dip in the bank’s CET1 ratio to 14.6% and its ROE to a low 8.1%, Commerzbank improved its cost-income ratio to 56% while absorbing €534 million in restructuring expenses. The Frankfurt-based financial institution continues to fend off a UniCredit takeover, a move the Italian giant has pursued since 2024. With almost 40,000 employees, Commerzbank’s ESG goals include net-zero operations by 2040 and portfolio neutrality by 2050.

Greece

Eurobank

Our winner continued its run in Greece; Eurobank achieved remarkable growth across loans, deposits and AUM in the first half of 2025—rising YoY by €5.3 billion, €4 billion, and 30%, respectively. Domestic assets reached €62.8 billion, supported by €37.3 billion in gross loans and €45.2 billion in deposits. Beyond the balance sheet, the group leveraged its performance to drive social impact, strengthening its startup incubator and funding significant public-school renovations. Notably, Eurobank leads its peers with over €6.9 billion in sustainable financing and an upward trend in Article 8 AUM, now exceeding €230 million. Article 8 funds are predominantly ESG compliant. The bank’s market-leading position was further solidified in 2025 through its acquisition of Eurolife’s life insurance business.

Iceland

Arion Bank

Arion Bank may be on the smaller side of the three major Icelandic banks, but what it lacks in size it made up for in efficiency and performance in 2025. The bank reports group AUM of 2 trillion Icelandic kronur ($15.9 billion), net earnings of 30.6 billion kronur, an ROE of 14.9%, a cost-income ratio of 42.3% and a CET1 ratio of 18.4%. Arion Bank’s service offering creates a broad revenue base, with a loan portfolio that is well diversified between retail and corporate customers. The bank is in merger discussions with Kvika Bank, currently the country’s fourth-largest bank, under which terms Arion Bank’s existing shareholders would hold 74% of the combined entity. The merger, which is expected to complete in late 2026, would be one of Iceland’s largest.

Ireland

AIB

AIB returns for a third year running as our Best Bank in Ireland. Serving a customer base of over 3.3 million, the Emerald Isle’s biggest bank posted a solid first half, with a €927 million profit after tax and a 21.4% return on tangible equity (ROTE), bolstered by a robust 16.4% CET1 ratio. 2025 saw the bank return to full private ownership, as well as the launch of its new slogan, “For the life you’re after,” encapsulating its commitments to customers, community, and sustainability.

Italy

UniCredit

Our Best Bank in Italy for the third consecutive year is UniCredit. While gross revenue moderated 3.1% to €11 billion, Italy remains the undisputed earnings powerhouse of the UniCredit group, contributing 41% of the total €10.6 billion net profit. With a unique Pan-European footprint and group assets reaching €870 billion at year-end 2025, UniCredit leverages its stability and low risk exposure to lead the continent’s green transition. The bank is making significant strides toward its 2050 net-zero target, notably through its €11.3 billion in environmental lending and the issuance of €6.5 billion in green bonds since 2021. In 2025, UniCredit deepened its domestic ESG impact through initiatives like Salotti Energia to build ESG awareness among Italian corporates and the One4Planet, Water Management loan. Furthermore, its Banking Academy Italy continues to drive social value, launching the Conta per Me primary school program and advanced fraud prevention training to protect the domestic retail base.

Lichtenstein

LGT

Liechtenstein’s largest player, LGT, continues its six-year unbroken winning streak. Total operating income increased 10% YoY to over 1.4 billion Swiss francs (more than $1.7 billion) in the first half of the year, group profits surged 38% to 240.6 million francs, and AUM reached 359.6 billion francs. While the bank trimmed its cost-income ratio to 75.7%, the figure remains high. Offsetting this is an impressive 18.5% CET1 ratio, reflecting the superior capital strength of this bank owned by the country’s royal family.

Luxembourg

BGL BNP Paribas

Our winner in Luxembourg, BGL BNP Paribas, reported first-half 2025 revenues of €315 million, up from €300 million for the same period in the previous year. With almost 2,100 employees in the Grand Duchy of Luxembourg, the bank provides universal services with a strategic emphasis on corporate and institutional clients. With deep regional roots dating back over a century, BGL BNP Paribas remains a cornerstone of Luxembourg’s economic landscape. Looking ahead, the bank is set to be a key driver of the group’s transition strategy, targeting 90% low-carbon energy financing by 2030.

Malta

Bank of Valletta

Malta’s banking sector remains highly concentrated; and with a 41% market share and total assets of €15.6 billion as of first-half 2025, Bank of Valletta is the most dominant domestic and commercial player in the sector—as well as our 2026 Best Bank in Malta. While the group registered a first-half profit before tax of €135.1 million (slightly down from €148.2 million in first-half 2024), return on average equity stood at 18.9% and CET1 ratio at 21.3%—a breakwater typical of the Mediterranean island.

Monaco

CFM Indosuez Wealth Management

Although its net income for 2024 fell slightly to €59.4 million, a 2.4% decrease from 2023, CFM Indosuez Wealth Management remains the leading player in Monaco. Despite lower interest rates and an unstable geopolitical context, wealth under custody grew 8.4%. “Customer business grew significantly, underpinned by strong new business momentum, a satisfactory performance in market activities and continued robust loan production.” Revenue increased 1.1% to €199.4 million driven by dynamic transactional business, though performance was impacted by a 2.1% rise in operating expenses due to inflation.

Netherlands

ING Group

Amid ongoing geopolitical uncertainty, the CEO of ING Group, Steven van Rijswijk hailed 2025 as a year in which the major global bank consistently executed its “strategy of accelerating growth, increasing impact and further diversifying income by doing more business with more customers and clients.” And so, returning for a third consecutive year, ING is once again our winner in the Netherlands, delivering strong commercial growth in its European base while achieving €23 billion in total income across the group. This was supported by an uptick in the bank’s customer base and a 15% rise in fee income to €4.6 billion. Commercial net interest income meanwhile came in at €15.3 billion. Achieving €56.9 billion in lending growth—more than double that of the previous year—ING’s net result for the year was broadly stable at €6.3 billion. The bank reports a 13.2% ROE and a 13.1% CET1 ratio. Of all its major markets, the Netherlands was a key driver and contributor to the bank’s growth in 2025.

Norway

DNB

Keeping its crown as the Best Bank in Norway for the fourth year in a row, DNB remains the dominant player in its home market, balancing massive scale with high profitability. Offering a full suite of retail, corporate, and investment banking, DNB maintained a strong reputation over the year, reporting an annualized ROE of 15.6%. Profits rose by 1.5% in the first half of 2025 to 21.3 billion Norwegian kroner ($2.1 billion), driven by solid performance across the group, and supported by a Norwegian economy that held up well in an unpredictable global environment. In 2025, the bank completed its 12 billion Swedish kronor ($1.2 billion) acquisition of Carnegie, a Nordic asset manager with 850 employees, strengthening DNB’s position in investment banking and wealth management.

Portugal

Banco Santander Totta

In Portugal, it is another consecutive win for Banco Santander Totta, which continued its growth strategy in 2025 via rigorous commercial and operational optimization. In a year defined by falling interest rates, it remained the most profitable bank and a benchmark for efficiency, posting a 31.8% ROTE and a 28% efficiency ratio while achieving a net profit of €963.8 million.

During this time, the bank continued to grow its customer base, particularly in high-value segments. Active customers increased by 40,000 to more than 1.9 million; while digital customers rose 5.1% to over 1.3 million, now representing 68% of the total base. This growth translated into a growth in commercial activity, with over 100,000 new accounts opened, 1.3 million daily transactions (up by 9.7%), and more than 327,000 new cardholders added.

Sweden

Swedbank

Swedbank had another successful year, with an ROE higher than the bank’s target of 15%—and according to president and CEO Jens Henriksson, “proof that our business model works.” The bank’s Swedish operations account for 71% of the group’s customer base; overall it serves a total of 7.3 million private customers and 545,000 corporate customers across Sweden, Estonia, Latvia, and Lithuania—offering loans, savings, payments, insurance, and daily banking services. In 2025, digital investments contributed to uptime of 99.9% for Swedbank’s app and internet bank for Sweden and the Baltic countries. This is a key focus for the bank as it sets out to improve its customer experience, with the aim “to make it easy to manage everyday matters digitally.”

Switzerland

UBS

For the sixth consecutive year, UBShas earned our Best Bank in Switzerland distinction. Throughout 2025, the bank remained laser focused on the Credit Suisse integration, which is slated for substantial completion by the end of 2026. A disciplined approach yielded a $7.8 billion net profit, supported by a solid 14.4% CET1 ratio, despite an 81.1% cost-income ratio.

CEO Sergio Ermotti attributed this performance to a “global, diversified franchise” that helped clients navigate market volatility. He further highlighted the bank’s digital evolution, noting that transformational AI projects are successfully bolstering operational resilience and improving client experience. As the Credit Suisse integration enters its final stages, industry attention is shifting toward the leadership transition following Ermotti’s planned 2027 departure.

United Kingdom

HSBC

HSBC is our Best Bank in the UK for the second consecutive year. HSBC UK employs 18,000 full-time staff across the country, serving over 15.3 million customers. For the year ending December 31, 2025, it posted a profit before tax of £5.6 billion ($7.5 billion). Revenue increased by £489 million, or 5%, to £10.5 billion, driven by higher net interest income. The bank’s ROTE of 19.2% was one percentage point lower than 2024, driven by growth in commercial lending. Supported by a 13.2% CET1 ratio and an 175% liquidity-coverage ratio, the its balance sheet remained resilient against a challenging economic backdrop.

Tan Su Shan, CEO and director of DBS Group—winner of this year’s Best Bank in Asia-Pacific—discusses the benefit of AI investments.

As global banks navigate trade fragmentation, AI disruption and volatile markets, DBS continues to distinguish itself through strong profitability and an aggressive technology strategy.

In this conversation with Deputy CEO Tan Su Shan, the bank’s leadership discusses how DBS surpassed $100 billion in market capitalization, scaled AI across hundreds of use cases and positioned itself to benefit from shifting intra-Asia trade flows.

Tan also outlines the challenges posed by tariffs, foreign-exchange swings and the accelerating evolution of generative and agentic AI as DBS looks toward 2026.

Global Finance: What factors shaped your bank’s performance in 2025?

Tan Su Shan: We delivered a solid financial performance in 2025, reflecting the resilience of our diversified franchise. Our total income and profit before tax hit new highs of S$22.9 billion ($18 billion) and S$13.1 billion, respectively. Return on equity (ROE) was 16.2%, within our medium-term target and several percentage points above our local and global peers.

A big part of our success was being well-positioned to capture structural growth opportunities arising from the shifting macro landscape, including rising intra-Asia trade and investment flows, as well as new trade and supply corridors between Asia and other regions such as Europe.

GF: What role did Al play in that performance?

Tan: We aim to sustain our leadership as an AI-enabled bank with a heart, using technology to deliver a competitive advantage while creating tangible impact for customers.

We have industrialized AI at scale, deploying more than 430 use cases—four times 2021 levels—powered by over 2,000 sophisticated models. These have delivered measurable outcomes, including stronger risk management, improved controls, and productivity gains. In 2025, our data analytics and AI/ML initiatives generated approximately S$1 billion in economic value.

Building on this foundation, we are embedding Gen AI and Agentic AI into customer journeys and internal workflows. Horizontal capabilities such as our DBS-GPT proprietary generative AI platform provide role-based access to millions of internal documents, accelerating decision-making and problem-solving. Vertical solutions such as DBS Joy, our Gen AI-enabled chatbot, deliver always-on, high-quality customer support at scale, improving customer satisfaction by 23% while handling more than 235,000 AI-powered interactions. Together, these capabilities lift productivity, decision quality, and customer experience by combining machine intelligence with human judgment.

GF: Which milestones did DBS reach in 2025?

Tan: It was a landmark year for DBS, notwithstanding global volatility, and the market’s confidence in our franchise has never been clearer. We surpassed the $100 billion market capitalization milestone in June and closed the year at $124 billion, cementing our position among the top 25 banks globally.

Moving ahead, we remain focused on building a resilient, growth-oriented, and future-ready market leader, anchored by our three strategic moats of trust, data, and culture.

GF: What was 2025’s greatest challenge for DBS?

Tan: Undoubtedly, our greatest challenge was the onset of tariffs following Liberation Day and the market volatility that followed. When you layer on headwinds from interest rates and significant FX fluctuations, you create a perfect storm we had to navigate. Despite these pressures, DBS delivered a solid financial performance. We achieved this by being proactive with our balance sheet hedging, securing record deposit inflows, and maintaining a sharp, strategic focus on high-ROE businesses such as wealth management.

At the same time, technology continued to move at a breathtaking pace, especially with the rapid shift toward Gen AI and Agentic AI. Fortunately, we weren’t starting from scratch, as we have been working with AI for more than a decade. Our early and sustained investments in data and technology gave us the robust foundation needed to industrialize AI across hundreds of meaningful use cases, positioning us to move quickly as the techno-logy evolves.

GF: Does 2026 present new challenges?

Tan: Our strategic priorities remain intact, and in 2026, we will continue leveraging our core strengths—what we term the “4 Ds”: Dependable, Diversifier, Digital, and Disruptor—to be a beacon of stability for our customers amid heightened volatility.

We have embarked on our vision to become an AI-enabled bank with a heart, transforming our operating models, leveraging machine intelligence, and preserving human empathy to reinforce the trust customers place in us. We will continue scaling our structural growth engines, which remain relevant even in a more bifurcated world.

This includes prioritizing growth in high-ROE businesses such as wealth management, transaction services, financial institutions group, and treasury customer sales. We also remain focused on our six core markets in Asia (Singapore, Hong Kong, India, Taiwan, China, and Indonesia) and on building connectivity between our Western and Asian clients. Strengthening resilience across every organizational layer remains a key, ongoing priority.

The White House’s long-anticipated cannabis regulatory shake-up may ease rules on paper, but for banks, processors, and payment networks, little changes in practice.

While the rescheduling of cannabis from Schedule I to Schedule III has sparked hope for industry reform, the reclassification doesn’t change the ongoing banking hurdles for smaller cannabis businesses in the U.S.

As large, publicly traded multi-state operators (MSOs) secure banking access, the majority of smaller cannabis companies still operate in a cash-only environment, with federal illegality, strict anti-money laundering rules, and a stalled bill blocking wider access to financial services. Alan Brochstein, an Austin, Texas-based analyst and founder of marketing firm New Cannabis Ventures, told Global Finance that meaningful reform still hinges on the passage of the SAFER Banking Act.

“Just because you’re Schedule III instead of Schedule I, you’re still federally illegal,” he said, referring to an April 23 order signed by Todd Blanche, President Donald Trump’s acting attorney general.

The reclassification formally recognizes cannabis for medical use. But the shift stops short of legalization and serves as a sobering reminder of the legal ambiguity that has kept major financial players wary.

“So, I don’t think that’s going to change,” Brochstein said. “Visa and Mastercard won’t allow processing, [and] rescheduling doesn’t change that.”

The bipartisan SAFER Banking Act, proposed in 2023, would provide a safe harbor for financial institutions serving state-sanctioned cannabis businesses, Brochstein explained. Lawmakers designed the bill to shield banks and credit unions from federal penalties and asset forfeiture when working with legal operators in compliant states. It remains stalled in Congress.

The reclassification has its benefits—expanding research, reducing tax burdens, and further legitimizing state medical programs across 40 states. Cannabis operators, however, remain boxed out of mainstream banking. Lenders, card networks, and cross-border investors are unlikely to change their stance substantially.

Regulatory Change, Financial Stagnation

For now, rescheduling grants medical cannabis some legitimacy, but the financial plumbing that underpins the industry remains frozen. As a result, operators rely on cash-heavy systems and state-by-state workarounds, especially in markets where recreational sales dominate revenue.

“I don’t think the banking landscape will change that much at this time,” said Richard Ormond, a partner at Los Angeles-based law firm Buchalter, capturing the industry’s central tension as financial institutions stay on the sidelines.

“Things will remain cautious as the majority of businesses, particularly in California, really focus on recreational use rather than just medical use,” Ormond predicted.

A broader review is coming, with Congressional hearings on the SAFER Act scheduled for June. Until then, cannabis suppliers are left with incremental progress on regulation—and persistent uncertainty in the banking system.

April 29 (UPI) — The United States has sanctioned 35 entities and individuals accused of overseeing a shadow-banking network that moved tens of billions of dollars for Iran, as the Trump administration flexes Washington’s financial might amid a stalemate in peace negotiations with Tehran.

The sanctions announced Tuesday come as U.S.-Iran peace negotiations came to a halt last week after Tehran said it would not participate in talks until the United States lifted its blockade of sea-based trade to the Middle Eastern nation.

Those blacklisted by the Treasury include several private companies known as rahbars, which manage thousands of overseas companies used by Iranian banks cut off from the international financial system to execute payments for Iranian trade.

According to the Treasury, these rahbar companies coordinate with Iranian exchange houses and front companies to conduct international trade on behalf of the Islamic Revolutionary Guard Corps, Iran’s Armed Forces General Staff, the National Iranian Oil Company and other sanctioned entities.

“By dismantling these financial channels, we advance the administration’s policy in the conflict with Iran and underscore our commitment to imposing maximum pressure on Iran,” State Department spokesman Thomas Pigott said in a statement.

The punitive action was part of what the Treasury calls Operation Economic Fury, a branded escalation of President Donald Trump‘s broader maximum-pressure campaign against Iran.

Coinciding with the sanctions on Tuesday, the Treasury’s Office of Foreign Assets Control issued an alert to financial institutions over the risks they face for doing business with so-called teapot oil refineries in China, primarily in Shandong Province, that import and refine Iranian crude oil.

According to the alert, China is the largest purchaser of Iranian oil, and the Treasury has designated multiple small China-based refineries since March of last year.

“The United States will further disrupt illicit funding streams that finance Iran’s malign activities,” Pigott said.

“We will not relent in our efforts to deny Iran and its proxies the resources they use to threaten U.S. interests and regional stability.”

Trump first employed the maximum-pressure campaign strategy to coerce Iran into negotiations over its nuclear program in 2018 after unilaterally withdrawing the United States from a landmark multinational accord that sought to prevent Tehran from obtaining a nuclear weapon.

Iran then breached its commitments under the deal, enriching uranium up to 60%, far exceeding the accord’s 3.67% but below weapons-grade levels.

Trump restored the maximum-pressure campaign after returning to office in 2025, and the United States bombed three major Iranian nuclear facilities that June.

The United States and Israel have since escalated their pressure campaign, attacking Iran in strikes that triggered a war now halted by a fragile cease-fire to permit peace talks.

Iran has imposed restrictions on energy trade through the Strait of Hormuz, prompting the United States to impose a blockade of Iran’s ports in response to what it describes as Tehran holding a major share of the world’s energy supplies hostage.