The USD-bolívar exchange rate has nearly doubled in 2026. (EFE)

Caracas, June 9, 2026 (venezuelanalysis.com) – Venezuela has registered the lowest month-to-month inflation figure since October 2024.

According to the Venezuelan Central Bank (BCV), consumer prices went up by 6.3 percent in May. Inflation has fallen for four consecutive months after hitting 32.6 percent in January, following the US military attack and kidnapping of President Nicolás Maduro.

Overall, prices have more than doubled in the first five months of 2026, and accumulated 12-month inflation currently stands at 525 percent.

Despite the widespread use of the US dollar in cost structures, prices have likewise gone up by 12.5 percent over the last year when measured in USD, meaning a loss of purchasing power even for those with incomes pegged to the official exchange rate.

Venezuela’s inflation remains heavily correlated with currency instability. Despite the Central Bank devaluing the USD-bolívar exchange rate by more than 30 percent since March and providing significantly increased volumes offoreign currency to the private sector, a 30-40 percent gap remains between the official and parallel market rates.

Since January, the BCV has directed over US $5.5 billion in foreign currency via bank-run exchange tables, at more than double the rate of 2025, according to figures from Banca y Negocios. However, the chasmbetween official and parallel rates has persisted.

Many economists have identified the stabilization of the foreign exchange market as a necessary step for macroeconomic recovery, but critics have pointed to a lack of regulation and accountability in forex allocation as fueling currency speculation.

Caracas’ monetary and fiscal policy is presently subject to US control. Since January, the Trump administration has mandated that Venezuelan export revenues, principally oil sales, be deposited in US Treasury accounts. Washington returns an undisclosed portion of the proceeds at a time of its choosing.

The White House has likewise imposed that disbursed funds be channeled directly to the private sector via foreign exchange auctions, as well as outside auditing of Central Bank accounts by consulting giant Deloitte. Secretary of State Marco Rubio indicated in January that the Venezuelan government headed by Acting President Delcy Rodríguez would need to submit a “budget request” before accessing its own resources.

For its part, the Rodríguez administration has fast-tracked a series of pro-business reforms tailored to attract foreign investment, including in the oil, mining, and electricity sectors.

As part of efforts to court US investors, Economic Vice President Calixto Ortega reportedly took part in a closed-door meeting with US officials and corporate representatives hosted by the Atlantic Council, a hawkish Washington-based think tank funded by the US government, its allies, and major corporations.

The opening to foreign investment has seen Western business executives flock to Caracas in recent weeks, often escorted by White House officials, to explore opportunities. Pro-Trump tech billionaires such as Fred Ehrsam have made repeated visits, while Peter Thiel’s Erebor Bank struck a corresponding banking agreement with Venezuela’s largest public bank.

Javier Kulesz, a strategist from investment bank Jefferies, relayed optimism after a visit to the South American country and forecast an imminent “stream of announcements” related to the country’s debt restructuring and investments in key economic sectors.

Tehran, Iran – Iran is facing more energy constraints as its summer season begins, with the widespread use of air conditioning and other needs during hotter months contributing to an imbalance between supply and consumption.

For decades, successive Iranian governments have kept utility bills well below supply costs for households and offices through a mix of implicit oil-and-gas subsidies, administered tariffs, state-controlled pricing, and sometimes direct financial support.

The negative impacts of the war with Israel and the United States on the economy mean the government has fewer tools at its disposal to deal with an energy crisis this summer.

Despite having the world’s third-largest proven crude oil reserves, Iran will have to import fuel again as demand outpaces refinery output.

President Masoud Pezeshkian has repeatedly urged households and offices to take practical steps to limit energy consumption. Last week, he removed his jacket during a government meeting to demonstrate how Iranians can avoid turning down their air conditioning thermostats in their offices.

Even though energy costs for households are much lower than in other parts of the world, corruption, mismanagement, sanctions, chronic inflation and currency devaluation have eroded the benefits Iranians usually feel from subsidised energy prices.

In November 2019, the government announced a tiered gasoline price scheme that would see huge increases for some consumers. This sparked nationwide protests, and since then, the government has been wary about similar price hikes.

While inflation has galloped on, continued subsidies have kept fuel artificially low.

The administration’s attempts to tackle the subsidies burden due to a mounting budget crunch have resulted in only limited increases in petrol through a complex three-tiered pricing system.

This is applied via a government-issued fuel card, giving most users of Iranian-made vehicles access to 60 litres (15.85 US gallons) per month of subsidised petrol at 15,000 rials (0.8 cents) and another 100 litres (26.42 gallons) at 1.6 cents.

Iranians going over this amount then must use an “emergency card” issued at petrol stations, permitting them to an additional 30 litres (7.9 gallons) of fuel a day at 50,000 rials (about 2.9 cents) per litre.

After a new cap was imposed during the war to limit fuel consumption, each card allows only 30 litres of fuel a day. Petrol stations are issued their own “emergency card” for uses beyond this limit.

Due to supply constraints, staff at petrol stations have now reportedly been instructed to limit the use of these cards to 10 to 15 litres (up to 4 gallons) or asked not to issue any new cards at all to customers.

The Iranian government is running similar schemes for natural gas, electricity and urban water, with fears of social unrest making them averse to any sudden price hikes.

There appears to be little the government can do to bridge the divide between lower energy production and growing demand for subsidised fuel, illustrated by the perpetual queues at petrol stations since the start of the war.

“Reforming and increasing the price of energy is currently not feasible and logical due to the current economic conditions and social concerns,” Esmail Saghab Esfahani, a vice president of the state-linked Organization for Energy Optimization and Strategic Management, said earlier this week.

There have been some changes to pricing structures, but this is impacting small businesses that are already struggling with the dire economic conditions in Iran.

One 35-year-old owner of a welding workshop near Tehran, who asked to remain anonymous, told Al Jazeera that a surge in his monthly energy bill from 40 million rials ($23) per month in the previous Persian calendar year to three times that today.

“I went to the electricity company, and they only kept saying the tariffs have gone up,” he said.

“I had a similar message from a friend who is paying much more now for roughly the same usage as before, so it looks like we’re to pay for the cost of war.”

Authorities say that any complaints about escalating bills will be reviewed. They also have a system where normal household energy consumption is kept artificially low, but excessive users can be billed as much as 45 times the normal prices.

Despite having the second-largest proven natural gas reserves in the world, Iran still suffers from perpetual supply shortages during its winter and summer, when consumption is at its highest.

The situation has worsened during the war, with strikes on Iranian energy facilities seeing Iran’s gasoline production capacity drop marginally from 115 million litres (30.37 million gallons) per day to 110 million litres (29.06 million gallons). Meanwhile, consumption has jumped from 10 million litres (2.64 million litres) in 2025 to 140 million litres this year (36.98 million litres).

US President Donald Trump’s threats of more strikes on power plants have heightened fears of further blackouts and gas shortages this summer, meaning the energy crisis is likely to continue in the coming months.

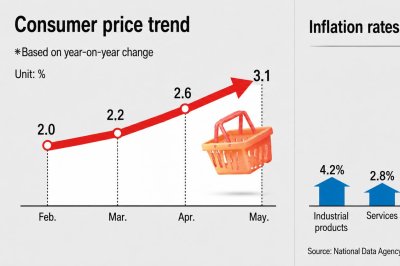

Consumer prices in South Korea rose 3.1% in May from a year earlier, driven by sharp increases in petroleum products, international airfares and overseas group tour fees. Data from National Data Agency. Graphic by Asia Today and translated by UPI

June 2 (Asia Today) — South Korea’s consumer price growth topped 3% in May for the first time in 26 months as a prolonged Middle East war drove up global oil prices, raising concerns that high inflation could continue through the second half of the year.

The consumer price index stood at 119.92 in May, with 2020 set as the base year of 100, up 3.1% from a year earlier, according to consumer price data released Tuesday by the National Data Agency. It was the first increase of 3% or more since March 2024.

Industrial products rose 4.2% from a year earlier, while service prices increased 2.8%. Petroleum prices showed the sharpest increase, jumping 24.2%, the largest gain in three years and 10 months since July 2022, when the Russia-Ukraine war was at its height.

Gasoline prices rose 23.1%, diesel prices climbed 33.3% and kerosene prices increased 21.7%.

Among services, international airfares, which are directly affected by fuel costs, rose 33.5%, while overseas group tour fees increased 26.3%.

The living price index, which tracks frequently purchased items with a high share of household spending, rose 3.3% from a year earlier, showing a worsening burden felt by consumers.

Lee Doo-won, an official in charge of economic trend statistics at the data agency, said petroleum prices rose more sharply because of higher international oil prices caused by the Middle East war.

“International airfares and prices for travel and lodging-related items rose sharply as fuel surcharges linked to global oil prices increased and the number of peak-season days, including holidays, grew,” Lee said.

The government said it will work to reduce price uncertainty by stabilizing petroleum prices.

A Finance Ministry official said the government’s petroleum price cap and fuel tax cut reduced the May consumer price increase by 0.6 percentage point.

“We will make every effort to stabilize prices felt by households through petroleum price stabilization measures and a task force on livelihood prices,” the official said.

Experts said inflation led by higher global oil prices is likely to continue in the second half.

“Although the United States and Iran have announced plans to discuss reopening the Strait of Hormuz, the high oil price trend is likely to continue in the second half even if the war ends, given the destruction of local oil facilities,” said Jeong Se-eun, an economics professor at Chungnam National University.

“For South Korea, which imports all of its oil, oil prices affect overall inflation. There is also concern that abnormal weather forecast for this summer could raise agricultural prices,” Jeong said.

“With no notable downward factor in the second half, inflation is expected to stay around 3%,” she added.

Park Jin, a professor at the Korea Development Institute School of Public Policy and Management, said prices are determined by market supply and demand.

“On the supply side, there are inflation concerns caused by unstable oil prices. On the demand side, there are price-increase factors such as a strong domestic stock market,” Park said. “Preemptive steps, including consideration of an interest rate hike, are needed.”

Now, the fee change is being criticised, with passengers and drivers calling it “disgusting” and “mad”.

Meanwhile, taxi operators are being forced to warn customers that the charge will be part of their cab bill when rides are booked.

Mark Streeter, boss of Norwich’s Courtesy Taxis, told Norwich Evening News: “The main annoyance from our side is that we tell customers it’s an extra £5 or so, and now it’s gone up with no warning. So either the customer or the driver has to pay more than expected.”

Norwich Airport has responded to explain that the drop-off fee increase is a result of growing business costs and worsening energy prices.

A spokesperson for Norwich Airport told The Sun: “We understand that no one welcomes increased charges. But our airport group is facing sharp rises in costs, including a tripling of business rates, higher employment costs such as National Insurance and rising energy costs.”

Admitting that there is no choice but to rely on the public to absorb some of the growing costs, the spokesperson added: “At the same time, we continue to invest millions of pounds in maintaining the airport infrastructure needed to provide an essential public service in our regions.

“We cannot keep absorbing these increased costs without passing some of the additional burden on to our customers.”

Norwich’s change in drop-off policy comes alongside Stansted Airport‘s similar changes.

The London airport took its 15-minute express drop-off charge from £7 to £10 in March, with stays of up to 30 minutes now costing £28 instead of £25.

Meanwhile, London Gatwick‘s fee for a 10-minute drop-off now costs £10, up £5 from when it was first introduced in 2021.

Wall Street closed the week higher as easing Middle East tensions, softer-than-expected inflation data, and strong corporate earnings boosted investor sentiment.

Investor sentiment improved after President Donald Trump said a framework to end the conflict with Iran and restore shipping

Eid al-Adha, one of the most important dates in the Islamic calendar, comes at a critical time for Iranians this year.

Meat from sacrificed animals is often eaten at Iranian tables, but a blockade on Iranian ports and sanctions by the US has led to escalating costs across the country.

Unlike Nowruz, the Persian New Year, Eid al-Adha is not as widely celebrated in Iran, but mosques and other institutions still observe the ritual of animal sacrifice, known as qurbani, through authorised livestock and slaughter centres.

Here, animals are sacrificed according to Islamic law in a hygienic environment. But another goal of the network is to control runaway inflation by offering meat at lower prices than market rates.

Meat substitutes

A Tehran municipality body announced on Tuesday that each kilogramme of sacrificial meat would be sold at 7.4 million rials ($4.30) at designated shops.

The price for a similar cut on the market can be more than three times that, depending on its quality and the location of the butchers. The minimum wage is currently less than $100 per month in Iran.

“I usually buy meat for a stew or a few dishes around every three weeks; for some families in the neighbourhood, it has become a sort of luxury,” said a middle-aged woman, who lives with her husband and son in Tehran.

She told Al Jazeera that chicken, eggs and legumes have become replacements for red meat, but the costs of these staples have significantly increased, too.

Masoud Rasouli, a meat-packing industry representative, told the state-linked Mehr news agency earlier this week that demand for red meat has decreased by 50 percent compared with last year.

He said some meat was imported to counter any effects of the US blockade, but local demand is currently so low that “existing livestock population is enough for all the needs of the market”.

Data released by the state-linked Iranian Labour News Agency this week showed that the current cheapest government-announced price for one kilogramme of meat during Eid is equal to the price of a 50kg live sheep 10 years ago.

According to the Statistical Center of Iran, year-on-year inflation stood at more than 73 percent in the first month of the Persian calendar year that ended in late April.

Iranian rice was up by 173 percent and chicken by 191 percent in that month compared with a year before, while liquid cooking oil more than quadrupled. Figures for the next month are expected to be worse.

Controlling inflation

Price-control measures – which have been implemented by authorities to fight a decade of rampant inflation – have been unable to adequately compensate for the ever-decreasing purchasing power of Iranian households living under local mismanagement and US sanctions – and now war and a blockade.

A young man working at a butcher shop in southwestern Tehran said they have had to increase prices several times over recent months after suppliers announced hikes.

“Our sales were a bit higher today because of the Eid, but we see even our most frequent customers far less these days. Most of the conversations with the customers are about the prices,” he told Al Jazeera.

Iran and the US have been holding negotiations through regional mediators to potentially end the war. But amid exchanges of fire and inflexibility over demands, no breakthrough has emerged even as both sides say a memorandum of understanding has mostly been negotiated.

Religious messaging

Beyond greetings and congratulatory phone calls with regional peers, Iranian authorities also used the Muslim festival this year to issue political messages.

On Wednesday morning in the capital, the authorities organised a large prayer to mark Eid at the University of Tehran, which was led by ultraconservative Ayatollah Ahmad Khatami.

He said that “submitting to humiliation” is an example of “evil” and the height of vice, at a time when he believes the other side, the US, seeks a surrender from Iran.

“Your enemies, the Iranian nation’s enemies, and this mad enemy sitting in the Black House – which is wrongly referred to as the White House – want your humiliation. But this madman will take that wish to his grave,” he said about US President Donald Trump.

Khatami, a member of the powerful Guardian Council and the clerical Assembly of Experts, also praised the supporters of the government who have taken to the streets every night for almost three months and said this “unprecedented” phenomenon would be repeated on the nights of Eid al-Adha.

President Masoud Pezeshkian had a relatively softer approach, but his comments were still laden with religious symbolism.

“In today’s turbulent world, where the fire of tyranny, occupation, and the arrogance of the hegemonic powers burns bright, Eid al-Adha conveys the message of dignity, liberty, and fearlessness in the face of the pharaohs of our time,” he said.

Foreign Minister Abbas Araghchi said in a message on Wednesday that he hoped for harmony in the Muslim world, amid this difficult time for the region.

“We pray that, by the auspiciousness and blessing of this great Eid, we will witness the deepening and strengthening of Islamic solidarity for cooperation and mutual assistance in confronting war, discrimination and occupation, especially in the West Asia region, and that our world will return to the path of reviving peace and justice,” he said.

Australia’s annual consumer price inflation slowed more sharply than anticipated in April, cooling to 4.2% from March’s 4.6% print and beating market expectations for a milder drop to 4.4%.

According to data released by the Australian Bureau of Statistics, the headline

MILLIONS of families will be able to enjoy discount meals and days out this summer, the Chancellor announced today.

From June 25 to September 1 the Government is temporarily cutting the VAT on attractions and children’s meals in restaurants from 20% to just 5%.

Sign up for the Travel newsletter

Thank you!

The cut will apply to theme parks, zoos, museums, soft play, fairs and even cinema tickets.

The full list of businesses participating has not yet been announced but several major firms including Merlin Entertainments and Odeon Cinema have confirmed they will be taking part.

If a business chooses to pass on the full benefit then the total saving for a family of two adults and two children could be:

The Government said it expects qualifying businesses to pass these savings on to families by lowering the prices people pay on eligible children’s meals and tickets.

As a result, the VAT cut will be directly reflected at the till.

It added that passing on the full saving should help businesses attract more customers over the summer, which could increase footfall and support local economies.

The plans are part of a package to help households with the cost of living.

Meanwhile, throughout August all children aged between five and 15 in England will be able to travel for free on any local bus service.

Among the attractions taking part are Alton Towers, Legoland Windsor, Warwick Castle and Cadbury World.

Fiona Eastwood, chief executive officer of Merlin Entertainments, said: “Merlin will be applying this VAT cut to both admission tickets and children’s meals, adding more value to days out and short breaks at our 20 UK attractions.”

Meanwhile, Mark Way, president AMC Europe & managing director at Odeon Cinema Groups, said: “We’re excited that our guests will be able to enjoy the big screen for less over this blockbuster summer.”

Which activities will be included?

The following activities and meals will benefit from the VAT cut:

Children’s meals for consumption on the premises are eligible where served from a dedicated children’s menu and marketed, presented and priced as such.

For cinemas, theatres, exhibitions, concerts and shows, the reduced rate applies to children’s and family tickets only.

The reduced rate applies to admission tickets, including adults, for:

Amusement parks and fairs, including water parks and theme parks (excluding pay-per-ride attractions)

Circuses

Adventure parks, including outdoor adventure centres

Museums and similar cultural facilities, including planetariums, heritage sites, nature reserves and botanical gardens.

Zoos, aquariums, wildlife parks and farm visitor attractions.

Soft play centres, indoor bounce parks and indoor play facilities

Observation attractions, including viewing platforms, towers and observation wheels

Season tickets that allow you repeat entry solely within the relief period.

But there are several attractions and popular activities that will not be included in the scheme. They include:

Sports facilities, such as when they are provided by non-profit bodies e.g. swimming at a community swimming pool.

Season or advance purchase tickets that allow repeat entries outside of the 25 June to 1 September dates, unless it is priced the same as a standard single-entry ticket.

For sales that have been made before the legislation is in place, including before the announcement, businesses may opt to apply the reduced rate or refund the VAT saving.

The European Commission on Thursday cut its 2026 growth forecast for the European economy, as the ongoing conflict in the Middle East drives energy prices sharply higher.

ADVERTISEMENT

ADVERTISEMENT

The EU economy is now expected to grow by just 1.1% in 2026, down from the 1.4% projected in the Commission’s autumn forecast. The eurozone outlook was revised down further to 0.9%.

In its report, the Commission warned that disruption to global energy markets — caused by escalating tensions around the Strait of Hormuz, one of the world’s key oil and gas shipping routes — has significantly worsened Europe’s economic outlook.

“Before the end of February 2026, the EU economy was expected to continue expanding at a moderate pace, alongside a further decline in inflation,” the report said. “However, the outlook has changed substantially since the outbreak of the conflict.”

Inflation is also expected to rise sharply due to the disruption around Hormuz.

EU inflation is forecast to reach 3.1% this year — a full percentage point higher than previously expected — driven mainly by soaring energy costs after oil and gas prices surged amid fears of supply disruptions in the Gulf.

For EU officials, the shock recalls 2022, when Russia’s invasion of Ukraine triggered Europe’s worst energy crisis in decades.

The Commission described the latest turmoil as “the second such shock in less than five years”, warning that Europe’s dependence on imported fossil fuels leaves it highly vulnerable whenever geopolitical tensions threaten global energy supplies.

Consumer confidence has already fallen to a 40-month low, according to the forecast, as households prepare for higher heating and fuel bills while businesses face rising operating costs and weaker demand.

Investment is also expected to slow as companies confront tighter financing conditions and growing uncertainty. Export growth is weakening as global demand softens.

Despite the deteriorating outlook, Brussels said the bloc is better prepared than during the Ukraine-related energy crisis, thanks to years of investment in renewable energy, lower gas consumption and efforts to diversify away from Russian supplies.

“The push towards supply diversification, decarbonisation and lower energy consumption has left the EU economy better placed to absorb today’s shock,” the Commission said.

However, EU officials acknowledged that risks remain heavily skewed to the downside.

The report warned that prolonged disruption in the Strait of Hormuz or across wider Middle Eastern supply chains could drive energy prices even higher, derail the expected easing of inflation in 2027 and potentially stall Europe’s recovery altogether.

The Commission also cautioned that shortages of refined oil products, fertilisers and other industrial inputs could spread through global supply chains, increasing food and manufacturing costs across Europe.

Meanwhile, European governments are preparing for growing fiscal pressure. Public deficits across the EU are expected to widen as governments increase spending to protect households from rising energy bills while also boosting defence expenditure amid mounting geopolitical instability.

Italian Prime Minister Giorgia Meloni has recently urged the European Commission to relax fiscal rules for households and industries struggling with soaring energy costs, arguing that energy security should be treated with the same urgency as defence spending.

At the centre of Rome’s request is the EU’s national escape clause, adopted on 8 July, which allows member states temporary fiscal flexibility to increase defence spending under exceptional circumstances.

Meloni said Brussels had already shown a willingness to loosen budget rules in response to Russia’s war in Ukraine and growing concerns about Europe’s military preparedness. Italy is now seeking similar flexibility for emergency energy measures.

Drop off fees at Edinburgh Airport have increased from todayCredit: Andrew Barr – The Sun GlasgowThe fees were blamed on surging business ratesCredit: Andrew Barr – The Sun Glasgow

It will now cost £8.50 for a ten-minute slot to either drop-off or pick someone up near the main terminal.

The fees have been hiked by £2.50 and were rolled out today.

Bosses have also scrapped a 50 per cent discount for people driving electric vehicles to the airport.

Instead, more spaces have been added to the free drop-off area – where motorists can park for free for 30 minutes.

The price hike has been blamed on a surge in business rates.

Airport chiefs claim they have been hit by a hit by a 142 per cent rise – an £8million increase – which was branded “simply unacceptable”.

Edinburgh Airport’s chief executive Gordon Dewar said: “This decision to impose an unplanned and wholly disproportionate £8million rates increase has an immediate and negative impact on our business.

“We made this clear in correspondence with the Lothians Assessor, who set the increase, and in discussions with the Scottish Government, which has endorsed it.

“A 142% increase reduces our ability to invest, grow and compete. In practical terms, it equates to funding around 200 jobs, two aircraft stands, or five new security lanes. It is not a cost that can be absorbed; it must be covered, and trade-offs like this are unfortunately unavoidable.

“Like many across the hospitality and tourism sectors who have seen business rates soar, we have no choice but to pass part of this cost on to passengers.

“We had not planned to raise fees this year, but the absence of a transitional relief scheme – equivalent to that available in England and Wales – leaves us with no alternative.

“We have always accepted that, given our size, we should pay more, but the scale of this increase is simply unacceptable.”

Bosses previously wrote to the Convenor of the Lothian Valuation Joint Board, which sets non-domestic rates, as well as the First Minister and the Public Finance Minister, to outline their concerns.

Mr Dewar added: “We have made clear to both the Assessor and the Scottish Government that a system which produces such markedly different outcomes for comparable assets operating within the same national economy cannot credibly be described as fair, proportionate or fit for a modern Scotland. This systemic inconsistency lies at the heart of our concern.”

It comes just months after Glasgow and Aberdeen airports – both owned by AGS – increased their drop off fees.

It costs £7 for people to park for up to 15 minutes at both of the sites.

A Scottish Government spokesperson said: “The valuation of all non-domestic property is a matter for the Scottish Assessors who are independent of central and local government.

“The Scottish Government estimates Edinburgh Airport will, with Transitional Relief, have a net non-domestic rates bill of around £8.1 million for 2026-27, compared to £5.4 million before revaluation.

“The Scottish Government’s Revaluation Transitional Relief protects those most affected at revaluation – including airports – and will cap increases in gross liabilities up to the next revaluation in 2029.”

Long-term US borrowing costs climbed to levels not seen since before the global financial crisis after the Treasury auctioned $25bn (€21.3bn) in 30-year bonds at a high yield of 5.058% on Wednesday, according to the department’s own data.

ADVERTISEMENT

ADVERTISEMENT

The sale came only hours after the US Senate voted to confirm former Federal Reserve governor Kevin Warsh as the next chairman, succeeding Jerome Powell.

The auction result immediately complicated the backdrop for Warsh’s arrival at the central bank, underlining the pressure facing policymakers as inflation is rising.

At the time of writing on Thursday, US 30-year bonds are trading at 5.02% while 10-year notes are selling with a yield of 4.44%.

US inflation figures released earlier this week showed consumer prices rose 3.8% from April 2025 as the 10-week Iran war pushed energy costs higher and distanced inflation from the Federal Reserve’s 2% target.

Producer price data also pointed to persistent underlying cost pressures across the economy, reinforcing expectations that the central bank may struggle to ease monetary policy quickly.

Rising Treasury yields have broad implications for the economy because they influence borrowing costs on mortgages, corporate debt and other forms of credit.

Higher long-term yields can also increase financing costs for the US government at a time when public debt is nearing $40 trillion (€34.1tn).

Investors are increasingly concerned that a combination of resilient economic growth, elevated energy prices and sustained government borrowing could keep inflationary pressures alive despite two years of restrictive monetary policy.

The yield on the benchmark 30-year Treasury bond being auctioned above 5% is a symbolic threshold last reached in 2007 before the onset of the global financial crisis.

While market conditions today differ substantially from that period, the move nonetheless underscores the sharp repricing that has taken place in global bond markets over the past two years.

Kevin Warsh inherits a difficult policy environment

Kevin Warsh takes over the Federal Reserve at a delicate moment for the US economy.

The former Morgan Stanley banker and Fed governor has previously argued in favour of maintaining the central bank’s credibility on inflation, while also signalling support for reforms to the institution’s communication strategy and balance sheet policies.

Warsh’s confirmation comes as financial markets remain divided over how aggressively the Federal Reserve should respond to persistent inflation pressures.

Some investors believe rates may need to stay higher for an extended period, while others warn that maintaining tight monetary conditions for too long could weigh heavily on economic growth and employment.

The main driver of the rise in inflation is the current disruption to global energy markets caused by the Iran war which also leaves the central bank at the mercy of geopolitics and not able to effectively control the situation.

Analysts stated that Wednesday’s Treasury auction illustrated the immediate challenge confronting the incoming Fed chair.

Elevated bond yields can help tighten financial conditions without additional rate increases from the central bank, but they can also amplify risks for heavily indebted households, businesses and the federal government itself.

For Warsh, the market reaction served as an early reminder that restoring confidence on inflation may prove more complicated than simply holding interest rates at restrictive levels.

WASHINGTON — The Senate confirmed President Trump’s nominee to lead the Federal Reserve, Kevin Warsh, bringing new leadership to the world’s most powerful central bank at a fraught moment for the global economy.

Warsh was confirmed Wednesday in a largely party-line vote. His nomination had been thrown into doubt in recent months after Republican Sen. Thom Tillis of North Carolina said he would block the nomination while the Justice Department investigated Fed Chair Jerome H. Powell. The Powell inquiry was dropped in April, clearing the way for the Senate to confirm Warsh.

Senate Majority Leader John Thune (R-S.D.) urged colleagues to support Warsh during a floor speech Wednesday morning, saying it’s crucial that a Fed chair “understand not only the macro” but also “appreciate the microeconomy: and that’s the hardworking Americans, their jobs and their livelihoods.”

“Kevin Warsh is just such a person,” Thune said.

Warsh, 56, a former top Fed official, will become chair at an unusually difficult time for the independent agency.

Inflation has topped the Fed’s 2% target for five years and is now rising faster because of surging gas prices. The Fed’s interest rate-setting committee is divided and saw the most dissenting votes in more than three decades last month. And Powell, after years of personal attacks from the Republican president and an unprecedented legal investigation by the Justice Department, plans to stay on the Fed’s board even after his term as chair ends, potentially creating a competing power center.

Trump has demanded change at the Federal Reserve

The Fed has faced numerous threats to its independence from Trump, who has repeatedly attacked Powell for not cutting interest rates. Trump also sought to fire Fed Gov. Lisa Cook and launched an investigation into brief Senate testimony by Powell on a building renovation.

Kevin Hassett, director of the White House’s National Economic Council, said in a Fox News interview on Sunday that he believes the markets are relieved that Warsh “is going to help lower interest rates over time.”

“Obviously, data driven,” said Hassett. “I’m not putting any pressure on Kevin Warsh.”

In December, Trump said on his social media platform that he wanted a Fed chair who would cut interest rates when the stock market rose — the opposite of what traditional economics would prescribe — and added, “Anyone that disagrees with me will never be the Fed chairman!”

Trump’s comments have fueled concerns over whether Warsh will set rates based on economic conditions or seek to cut rates to appease Trump, even if doing so could worsen inflation. At Warsh’s confirmation hearing last month, Sen. Elizabeth Warren, a Democrat from Massachusetts, derided him as a “sock puppet” for Trump. Warsh declined to say that Democrat Joe Biden had won the 2020 election against Trump, who has falsely claimed that voter fraud cost him reelection.

Still, Warsh denied at the hearing that Trump had pressured him to reduce the Fed’s key rate.

“The president never once asked me to commit to any particular interest rate decision, period,” Warsh said then. “Nor would I ever agree to do so if he had. … I will be an independent actor if confirmed as chair of the Federal Reserve.”

A critic of the Fed’s leadership in the past

Warsh has been highly critical of the Fed’s recent track record, particularly the inflation spike in 2021-22, the worst in four decades, and has called for “regime change.” Yet he has provided only broad outlines of what that change would involve.

He has called for limiting the Fed’s communications, which would be a sharp shift after decades of increasing transparency. He has argued that some of its communications tools, such as quarterly forecasts of where its key rate may head, have made it harder for officials to switch gears.

Senate Democrats also have condemned Warsh for not fully divulging the details of his extensive wealth, which disclosures show amounts to at least $100 million. His investments include stakes in Polymarket and SpaceX, but he hasn’t revealed how large those holdings are. He promised to sell all such assets within 90 days of being sworn in.

“He will be the wealthiest Fed chair in history, but he refuses to provide transparency to the American people about who he is entangled with,” Warren said.

Warsh faces difficult economic conditions

The Fed is still grappling with how to respond to the 50% jump in gas prices from the Iran war. The increase has boosted inflation, which reached 3.8% in April.

The Fed is tasked by Congress with keeping prices stable, which it seeks to do by raising its short-term rate to make borrowing and spending more expensive, cooling growth and inflation.

The Fed typically looks past temporary price increases that stem from supply disruptions, such as the war’s cutoff of oil through the Strait of Hormuz, because those prices typically level off — or even fall back down — once the supply is restored.

But the Fed also followed that approach after the COVID-19 pandemic snarled global supply chains for goods, lifting prices for things such as cars, furniture and electronics. Inflation turned out to last longer than expected, and Powell and other Fed officials have acknowledged they waited too long to raise rates. Inflation surged to 9.1% by June 2022.

The Fed’s rate-setting committee has kept rates unchanged for three straight meetings as it evaluates the effect of the gas price spike. At its most recent meeting last month, three members of the committee objected to language that suggested its next move would be a rate cut. They preferred more neutral language that would allow for a hike. Many Fed watchers saw those dissents as a warning shot to Warsh that he won’t be able to easily engineer rate reductions.

A fourth member of the 12-member committee, Stephen Miran, dissented in favor of a rate cut, as he has at every meeting since Trump appointed him to the Fed’s board last September. Miran is serving until a replacement is named, and Warsh will take his spot.

Powell, meanwhile, said at a news conference April 29 that he would remain as a Fed governor until the Justice Department closes its investigation into the Fed’s building project, the first time a chair may stay on the board for an extended period since 1948. His term as a governor lasts until January 2028.

U.S. Atty. Jeanine Pirro has dropped the government’s investigation, but she has said it could be reopened if the Fed’s inspector general office, which has looked into the renovation project since last July, finds evidence of criminal activity.

Rugaber and Cappelletti write for the Associated Press.

Final demand inflation rose by 6% on an annual basis in April, marking the largest increase since 2022, the U.S. Bureau of Labor Statistics reported Wednesday. More than three-quarters of the 2% increase in final demand goods in April was attributed to a 7.8% increase in energy prices. File Photo by John Angelillo/UPI | License Photo

May 13 (UPI) — Final demand wholesale inflation rose by 6% on an annual basis in April, marking the largest increase since 2022, the U.S. Bureau of Labor Statistics reported Wednesday.

More than three-quarters of the 2% increase in final demand goods in April was attributed to a 7.8% increase in energy prices. Final demand services moved up 1.2%, pushed along largely by a 2.7% increase in trade services.

The producer price index increased by a seasonally adjusted 1.4% in April, double the rate increase in March. The increase outpaced the Dow Jones consensus estimate of 0.5%. It is the largest monthly increase since March 2022.

The annual 6% wholesale inflation increase is the largest since December 2022.

Machinery and equipment wholesaling was another big factor in rising inflation. Final demand service prices for machinery and equipment rose by 3.5%.

Final demand excluding volatile food and energy rose 0.6%, the largest bump since October. For the year ending in April, final demand excluding food and energy was up 4.4%, the largest increase since February 2023.

By commodity type, the index for unprocessed goods went up 4.1%. Intermediate demand goods increased 2.7% for the month, the sixth consecutive monthly increase.

About 80% of the index increase for unprocessed goods for intermediate demand can be attributed to unprocessed energy materials which increased 9.2%. Crude petroleum rose by 11.3%.

Unprocessed non-food materials and excluding energy fell by 1%.

President Donald Trump gives remarks during a law enforcement leaders dinner, celebrating the start of National Police Week, in the Rose Garden at the White House on Monday. Photo by Aaron Schwartz/UPI | License Photo

Tehran, Iran – Skyrocketing inflation is jeopardising food security among households in conflict-hit Iran, new figures show, as diplomatic efforts to end the war launched by the United States and Israel intensify.

“The people must realistically understand the conditions and restrictions of the country,” President Masoud Pezeshkian told a group of officials who gathered on Sunday to discuss rebuilding structures damaged or destroyed in US and Israeli attacks.

“It is natural that there are difficulties and problems in this path, but through people’s cooperation and reliance on national cohesion, problems can be solved,” he was quoted as saying by state media.

Pezeshkian’s comments came a day after the Statistical Center of Iran (SCI) said Farvardin, the first month of the Persian calendar year that ended on April 20, had an inflation rate of 73.5 percent compared to the same month of the previous year. The SCI also noted that inflation was five percent higher in Farvardin compared to the previous month.

The Central Bank of Iran, which reports figures based on a different method and with different data sets, reported a slightly lower inflation rate of 67 percent for Farvardin compared to a year earlier, and a seven percent monthly increase.

Although not matched, both figures indicate a considerably accelerating pace for general inflation, which has been among the highest in the world over recent years, and is continuously making Iranians poorer.

A Tehran resident told Al Jazeera she could no longer afford some of the items she could just last month.

“And it’s not just me – I think most people in society right now can’t afford many of the things they want,” she said.

Figures from the institutions also showed that food inflation is much higher than headline inflation, meaning that people are increasingly forced to pay an expanding share of their shrinking salaries on basic items.

The SCI reported a staggering 115 percent food inflation rate for the first month of the year, compared to the same period the year before, with several staple items more than tripling in price.

Solid vegetable oil had the highest increase at 375 percent, followed by liquid cooking oil at 308 percent; imported rice at 209 percent; Iranian rice at 173 percent; and chicken at 191 percent. The lowest price hikes were for butter, at 48 percent, followed by infant formula at 71 percent and pasta at 75 percent.

Majid, a young man who works at a liver kebab shop in the capital, said the eatery has increased prices three times in recent months.

“The price of liver has doubled. When we ask suppliers why, they either say there’s a shortage or that sheep are being exported. Honestly, there’s no real oversight,” he said.

The state-run Consumers and Producers Protection Organization said in a directive sent to 31 governors across Iran on Sunday that new price hikes for cooking oil are “illegal” and “must be returned to previous levels”, without saying how officials expected that to happen amid deteriorating economic conditions.

The country’s embattled currency, the rial, has also been registering new all-time lows over the past two weeks. On Sunday afternoon, it stood at about 1.77 million against the US dollar in Tehran’s open market after marginally recovering. The rate was about 830,000 per US dollar a year ago.

Subsidies and ‘enemy plots’

The response from the government has included offering subsidies and coupons, while trying to crack down on acts such as hoarding that are perceived to be contributing to price hikes.

But this has not been accompanied by a clear macroeconomic stabilisation package as the US presses on with a naval blockade of Iranian ports.

As Iranian media reported on Sunday that Tehran had sent an official response to the text for an agreement earlier proposed by the US through mediator Pakistan, Pezeshkian said, “If there is talk of negotiations, it does not mean surrender.”

People walk through a local market in Tehran [File: Majid Asgaripour/WANA via Reuters]

The government hands out monthly cash subsidies and electronic vouchers to buy essential goods at select stores, which together amount to less than $10 each month per person. Authorities are considering raising the amount, but a hefty budget crunch has made that more difficult.

Pezeshkian and Central Bank chief Abdolnasser Hemmati have said they are aware of the price increases, but have blamed the war that began in late February while coordinating with the judiciary to act against price gauging and hoarding.

A number of lawmakers in Iran’s hardline-dominated parliament, as well as state television hosts and outlets linked to the Islamic Revolutionary Guard Corps (IRGC), have said the price surges are suspicious. They have described the runaway prices as being part of an “economic revenge” campaign by enemies who suffered failures in the military arena.

“I want the people of Iran not to be fooled by the enemy-made price hikes,” a guest on state television’s Ofogh network said on Saturday. “Great things have happened, and great things are ahead. The economic achievements of the war are unrivalled by any other period.”

But some of the economic pain continues to be inflicted as a direct result of a near-total internet shutdown now being imposed by Iranian authorities for a 72nd day.

Numerous officials in the government, internet infrastructure firms, telecommunication companies and other state-linked organisations have emphasised that they are against a tiered internet system that is now being implemented. But they have said they bear no responsibility, since the blackout, which is expected to remain in place until the war ends, is ordered by the Supreme National Security Council.

In the meantime, the combined impact of local mismanagement, Western sanctions, blockade, war and the internet shutdown is squeezing people and businesses hard.

“The startup ecosystem of the country is dead, we are searching for a tombstone for it,” the Guild Association of Internet-based Businesses said in a statement on Saturday.

San Francisco, United States – Greer Dove’s days are packed with studying business and finance, as well as doing administrative work at college, along with caring for her eight-year-old daughter with special needs. But once a week, Dove, a single mother, makes sure to drop in at the food bank in California’s Marin County to pick up vegetables, fruit and other food. Along with the federal government’s food benefits, they keep her housing running.

“We need this so we can keep functioning at a high level,” she says. “She loves fruit, so I make sure to get it,” she says of her daughter.

Recommended Stories

list of 4 itemsend of list

Dove, who is also looking for a full-time job, has worked in restaurants, event management, retail, television shows, office administration and payroll over the years. But she has been on the federal government’s Supplemental Nutritional Assistance Program (SNAP) for six years, and with the food bank, for more than three years. Before she got food benefits, Dove fed her daughter all she had and skipped meals or looked around for snacks in the offices she worked at to get her through the day.

United States President Donald Trump’s One Big Beautiful Bill Act (OBBBA), passed in June, cut SNAP benefits by more than $186bn over the next 10 years to make up for extending cuts to income tax. This could lead to more than 3 million people nationwide, and 665,000 recipients in California, losing such food benefits, according to estimates.

“This will bring a series of cuts that collectively present an existential threat to food benefits,” says Andrew Cheyne, managing director of government relations and public affairs at the County Welfare Directors Association of California.

California’s proposed billionaire tax, which seeks to impose a one-time 5 percent tax on the assets of the state’s more than 200 billionaires to make up for the funding gap created by the OBBBA, got more than 1.5 million signatures in April. It is likely to be on the ballot for the November midterm election.

While most of the nearly $100bn expected to be raised through the tax will go towards filling the gap in health insurance created by the OBBBA, 10 percent will be used to make up for the retrenchment in food benefits.

In California, where more than 5.3 million people, more than any other state, receive food benefits, the impacts of the cuts began to be felt in April when 72,000 immigrants started losing benefits. June onwards, nearly 600,000 recipients will be screened for work eligibility. Recipients, including those who are homeless, seniors, foster youth and veterans, will have to work, study or volunteer to receive food benefits. Failing the screening to meet work requirements for three months will lead to their food benefits being cut.

Brian Galle, professor of law at the University of California at Berkeley and one of the tax measure’s authors, says that in California, the state that introduced gig work, “jobs are increasingly precarious. You may find enough work or not. You may get tips or not. But nutrition needs are steady.”

Making impossible choices

On a recent Friday morning, new members lined up to enrol at a whitewashed, bunting-festooned La Ofrenda food bank in San Francisco’s Mission district. The food bank doles out fresh vegetables, fruit and bread that have been donated by large grocery stores once those products neared expiration date.

Gladys Lee had taken a 45-minute train ride after a friend told her about it. Lee worked at downtown San Francisco’s Hyatt hotel as a room cleaner for three decades until a back injury meant she could not push the heavy cleaning carts any more and had to leave. After seven years of struggling to find work, food was getting scarce, and Lee found her way to La Ofrenda. She packed what she could into a carton and held it in her arms for the train ride back.

Volunteers gathered at the La Ofrenda food bank in San Francisco’s Mission District [Saumya Roy/Al Jazeera]

Food benefit rolls have shrunk by more than 3.3 million nationally in the six months from July 2025, when the OBBBA was enacted, to January 2026.

In California, the rolls of Calfresh, as food benefits are known in the state, shrank by 288,000 or 6 percent from July 2025 to February 2026, according to analysis by the Center for Budget and Policy Priorities, a Washington, DC-based think tank. This reduction in rolls happened even before the OBBBA cuts began.

Brooke Rollins, the agriculture secretary, wrote in a recent essay that the shrinking of SNAP rolls reflected an ebullient economy and buoyant job growth.

“The drop in SNAP recipients affirms that many Americans are moving from welfare to work,” she wrote. “It is no secret that Trump’s massive tax cuts and deregulation efforts are unleashing robust, private sector-led economic growth, which are fueling trillions in investments, booming wage growth”.

But unemployment remained stable at about 4.4 percent since July 2025, according to the Bureau of Labor Statistics data, while SNAP rolls shrank.

“This last time we saw such a steep, quick decline, other than during natural disasters, is three decades ago when welfare reform was enacted,” says Dottie Rosenbaum, senior fellow and director of Federal SNAP Policy at the Center for Budget and Policy Priorities.

Nationally, SNAP rolls shrank by 8 percent, while in California, they shrank by 5.5 percent, in part because the work eligibility requirements were delayed until June, while some other states have already implemented them.

At La Ofrenda, Roberto Alfaro, executive director of the nonprofit Homey, says he started the food bank when food costs went up during the pandemic. They have stayed high, he says. Now he sees people doing day jobs and night jobs and coming for food when they have paid rent.

“People are making impossible choices,” says Keely O’Brien, a policy advocate at the Western Center for Law and Poverty.

While California is the world’s fourth-largest economy, growth has come with a soaring cost-of-living crisis.

“With rising housing and utility costs, few households can dedicate that much of their income towards food,” O’Brien says.

The OBBA has also shifted the administrative cost of meeting work eligibility requirements to states, and beginning next year, part of the cost of SNAP will also fall on states.

“To make requirements more stringent, you are creating more government, more bureaucratic logjam,” says Jaren Sorkow, state director for the Children’s Defence Fund.

This has already led to a 51 percent drop in SNAP rolls in Arizona, which has begun implementing the OBBBA cuts, according to data by the Center for Budget and Policy Priorities.

Food being given out at the La Ofrenda food bank in San Francisco’s Mission District [Saumya Roy/Al Jazeera[

Making something from nothing

Several measures to counter the $100bn gap in funding for health insurance and food benefits created by the OBBBA have been floated in California. The biggest of these is the one-time 5 percent tax on those with assets of more than a billion dollars. The tax will raise $100bn, its authors estimate.

As it seems set to be voted on in the November election, it faces mounting opposition from the state’s tech entrepreneurs who have funded measures to undercut the tax.

Tech entrepreneurs have called it an economic 9/11, saying taxing their assets, including shareholding in startups, will lead to a flight of capital and innovation from the state. Sergey Brin, a cofounder of Google Inc, now spends a week in Nevada and a week in his Bay Area offices and has spent more than $57m on opposing the billionaire tax. He has backed two measures that undercut the billion tax, which have also received 1.4 million and 1.5 million signatures and are also set to be on the ballot for the November election.

One of these measures prohibits future taxes on personal property, including financial assets, savings and retirement accounts, as well as intellectual property. The other would increase audits of taxpayer-funded programmes, and includes language that would essentially invalidate the billionaire tax.

In a recent statement to The New York Times, Brin said, “I fled socialism with my family in 1979 and know the devastating, oppressive society it created in the Soviet Union. I don’t want California to end up in the same place.”

The coalition of unions backing the billionaire tax is bracing for the fight ahead. “We expect to be outspent,” says Kris Cuaresma-Primm, director of partnerships for the coalition that is backing the billionaire tax. “We will keep communicating to people that there is a tidal wave of pain coming from the cuts, and we want to reclaim the losses from the OBBBA.”

Giulia Varaschin, senior tax policy adviser at the International Tax Observatory, who recently coauthored a study on wealth taxes, says there is little academic evidence that such taxes cause the wealthy to leave at a notable scale. “There is only a marginal flight with very little, if any, economic impact,” she says.

The study, coauthored with the economist Gabriel Zucman, who supports the California billionaire tax, did find that wealth taxes had not raised as much revenue as estimated in several European countries and became less popular as a result.

Varaschin says this was because these taxes were levied on a larger set of the wealthy, which included homeowners or small businesses, rather than the ultra-rich or billionaires. The taxpayers could hardly afford to pay it, and the government made exemptions instead. These taxes also did not touch assets, where much of the wealth of the ultra-rich lies, Varaschin says.

The California tax remedies this by taxing only billionaires and taxing assets, including shares in companies.

Daniel Shaviro, Wayne Perry professor of taxation at New York University, says, “Traditionally, these taxes can be hard to enforce because tax administration don’t want to go after these people.”

Even if it passes, “The governor could just say this is not a high priority for him and not enforce it,” Shaviro says, referring to Governor Gavin Newsom, who has opposed the tax.

But Primm says, “The governor is out of touch with Californians on this”.

Newsom is in the last year of his last term as governor. However, nearly all the candidates running for the June 2 primary for governor, except billionaire Tom Steyer, who is running as a progressive Democrat, also oppose this measure. While some have said this will lead to a flight of capital, others say the spending plan does not include expenses for education, which was not cut in the OBBBA.

Greer Dove, who gets food through Calfresh and the San Francisco Marin Food Bank for herself and her daughter, says the looming food benefit cuts are worrying. “The anxiety of it all is adding up. I could be next.”

Central banks hold rates steady as energy shock tests inflation fight.

Caught between rising inflation and slowing growth, the United States Federal Reserve, the European Central Bank and the Bank of England are keeping interest rates and borrowing costs steady.

That’s despite rising energy bills, fuel and food costs squeezing businesses and households worldwide.

The International Monetary Fund is warning of a global slowdown, and no one knows how long the energy shock set off by the US-Israel war on Iran will last.

The impact will be felt hardest in emerging markets and developing nations. Central banks face a tough choice: fight rising prices or support a weakening economy.

epa11846878 British Airways aircraft at Gatwick Airport in London, Britain, 23 January 2025. The British government is considering airport expansions in London. Plans for a third runway at Heathrow and a second runway at Gatwick are under review by the Treasury in an effort to boost growth. Transport Secretary Heidi Alexander has a deadline of 27 February to decide whether to permit Gatwick to bring its existing emergency northern runway into routine use. EPA/ANDY RAINCredit: EPA

BRITISH Airways passengers face higher fares after its parent company warned rising oil prices will add about £1.72billion to its fuel bill this year.

International Airlines Group (IAG), which also owns Iberia and Aer Lingus, said it expects to pass on part of the extra cost through ticket prices, with business class and other premium long-haul passengers among those most likely to be affected.

Sign up for the Travel newsletter

Thank you!

IAG warned the crisis could deepen if the strait remains blocked, with global jet fuel supplies potentially restrictedCredit: Getty

Chief executive Luis Gallego said airlines need to increase fares to help offset fuel costs, which make up about a quarter of their spending.

The rise follows disruption linked to the Middle East conflict and the closure of the Strait of Hormuz, which normally carries about a fifth of the world’s oil and gas shipments.

IAG warned the crisis could deepen if the strait remains blocked, with global jet fuel supplies potentially restricted.

However, the group said it does not expect any disruption to summer fuel supplies.

Mr Gallego said there is less jet fuel coming from the Middle East, but there are “other places with record supply” such as the US.

He said IAG has been “planning for situations like this for many years”, and has invested in its own jet fuel supply at its “main hubs”.

The company recorded a pre-tax profit of £365million during the three months to the end of March.

That was a 76.6% increase from £207million a year earlier.

The group now expects its annual fuel bill to reach £7.78billion.

Mr Gallego attributed the firm’s “strong first quarter” to “continued strong demand for our networks and airline brands”.

He added: “IAG is uniquely positioned to navigate the current headwinds created by the Middle East conflict thanks to our leading positions across diverse markets, strong brands, structurally high margins and strong balance sheet, as well as a strong track record of execution.”

IAG said about 3% of its capacity was “exposed to the Gulf region” at the start of the war on February 28, mostly with British Airways flights.

A large part of this has been redeployed, including boosting capacity at destinations where there are now fewer flights by Middle East carriers such as Bangkok, Singapore and the Maldives.

British Airways has also announced additional flights this summer on routes with higher demand for direct flights, such as India and Nairobi.

The UK bond market is currently experiencing a period of intense volatility, with the yield on 30-year government bonds, known as gilts, climbing to its highest point since 1998.

ADVERTISEMENT

ADVERTISEMENT

On Tuesday, 30-year gilt yields rose as much as 0.14% to 5.79%, their highest level this century, before dipping slightly to around 5.6% at the time of writing.

The yield on the 10-year gilt also climbed as much as 0.15% to 5.11%, very close to the 18-year high of 5.12% hit earlier in the Iran war. It has since lowered somewhat to roughly 4.93% on Thursday.

Bond prices and yields have an inverse relationship. Bond yields rise when prices fall in order to increase investment attractiveness as demand for the debt weakens.

The surge in gilt yields indicates that investors currently perceive UK debt as a riskier prospect than other lending options, requiring a larger premium to commit their capital over the long term.

Presently, there are several reasons for this evident but abnormal lack of confidence.

The primary catalyst is the fear that the Bank of England may be forced to keep interest rates higher for longer to mitigate the chance that inflation will remain “sticky” and not return to the 2% target as quickly as previously hoped.

This estimation has been fuelled by surging energy prices due to the disruption caused by the Iran war. Gilts have continuously sold off during the conflict.

Speaking to Euronews, Richard Carter, head of fixed interest research at Quilter Cheviot, added that “the UK is expected to be the worst hit developed economy by events in the Middle East due to its reliance on energy imports, so the longer energy prices remain elevated, the deeper the pain the country is likely to experience.”

Beyond geopolitics and global energy markets, there are many domestic factors currently contributing to the exceptional distrust in UK debt.

Keir Starmer, fiscal policy and local elections

Political uncertainty and fiscal policy are also playing a central role in the recent and severe gilts sell-off.

In 2024, after Keir Starmer’s election, the Labour party pledged “fiscal discipline” and established a long-term framework in the Autumn Budget to distinguish the new government’s approach from the former.

The plan introduced the “Stability Rule” mandating that the current budget, which covers day-to-day costs such as public sector salaries and welfare, must be in surplus by the end of 2029/30. This effectively prohibits borrowing to fund the ongoing operations of the British state.

Additionally, the “Investment Rule” was also put forward to target the national balance sheet. This norm requires Public Sector Net Financial Liabilities (PSNFL) to be falling as a percentage of GDP within the same timeframe as the “Stability Rule”.

By using PSNFL rather than the traditional measure of net debt, the UK Treasury has more room to borrow for long-term capital projects like infrastructure and green energy, which are technically classified as “investments” rather than “spending”.

Finally, the Budget Responsibility Act 2024established a “fiscal lock”, legally preventing any significant tax or spending changes from being introduced without an independent assessment from the Office for Budget Responsibility (OBR).

Despite all these rigid guardrails, bond markets are now sceptical because investors fear political necessity will eventually override fiscal prudence.

Recent scrutiny of Starmer has intensified as he faces a mounting challenge from the left of his party, where dissenting voices are calling for a shift away from “fiscal conservatism” to address funding crises in the NHS and local government.

On top of that, the disastrous appointment of Peter Mandelson as Britain’s ambassador to Washington, and the revelations of his past friendship with Jeffrey Epstein, have severely damaged Starmer’s administration over the last few months.

The problems have culminated in the local elections taking place in 136 authorities for more than 5,000 council seats on Thursday. More than half of the seats up for grabs this week are being defended by Starmer’s party.

Analysts project that Labour will suffer a massive loss and potentially end up over 1,000 councillors down. Any major setback will certainly increase internal pressure to oust Keir Starmer as the leader in which case snap elections could be triggered.

The head of markets at AJ Bell, Dan Coatsworth, explained to Euronews that “investors will be watching bond markets like a hawk over the coming days as the results of the UK local elections are released. Any major setback to Labour will fuel calls for Keir Starmer to be replaced as prime minister and if that happens, bond markets will want to know who is taking over.”

“The obvious challengers, Angela Rayner and Andy Burnham, are seen as candidates who might push for greater government borrowing and spending, which could take gilt yields even higher. Fundamentally, there is a real risk of gilt yields soaring if Labour experiences a wipeout in the local elections,” Coatsworth added.

Speaking to Euronews, the head of fixed interest research at Quilter Cheviot, Richard Carter, conveyed the same sentiment.

“The uncertain UK political backdrop has played a role ahead of the local elections with gilt investors concerned about a Labour Party lurch to the left should Keir Starmer either be replaced or have little choice but to appease his backbenchers in the wake of challenging results.”

Effectively, these local results are no longer just a measure of regional popularity, but a high-stakes verdict of political viability that could determine the long-term stability of British borrowing costs.

The cost to the UK Treasury, businesses and households

For the British government, the consequences of the ongoing bond market shift are measured in billions of pounds as the UK’s debt-interest bill is highly sensitive to fluctuations in gilt yields.

According to estimates from fiscal watchdogs, every 0.25% rise in government borrowing costs adds approximately £2.5 billion (€2.9bn) to the annual debt-servicing cost. A 0.5% increase, which has already been observed this spring, therefore requires the UK Treasury to find an extra £5 billion (€5.8bn) every year just to pay interest.

The rise in gilt yields also has a direct and immediate impact on the real economy as they serve as the benchmark for pricing a vast array of financial products, most notably fixed-rate mortgages.

As yields climb, lenders adjust their swap rates, which inevitably leads to higher monthly repayments for millions of homeowners looking to refinance.

Businesses also feel the squeeze. The cost of corporate loans and commercial credit is often tied to the yield curve. When the state has to pay more to borrow, the private sector follows suit, potentially stifling investment and slowing economic growth.

“A gilt yield shock might be called a stealth tax, but it is not an intentional one. It would be the knock-on effects of bond prices falling and yields going up, which can negatively affect asset prices and tighten financial conditions,” Coatsworth told Euronews.

“Consumers would experience higher mortgage costs and potentially spend less money, particularly if companies scale back hiring if their borrowing costs rise from higher gilt yields, as the two are intertwined. It could also lead to lower public spending and pave the way for tax rises,” Coatsworth added.

Every increase in the cost of debt limits the amount of capital available for private innovation and reduces the disposable income of households already struggling with the cost of living.

A fragile ceasefire may have paused the US-Israeli war on Iran, but the economic cost is crippling the daily lives of Iranians. The US is blockading Iranian ports, while the price of goods skyrockets and businesses struggle to keep employees.

Workers are gathering in cities around the world to mark International Labour Day, with some demonstrations, such as those in Istanbul, Turkiye, turning to scuffles with police.

Trade Unions are calling for solidarity and the protection of workers’ rights as the United States-Israeli war on Iran and rising energy costs raise concerns about the global economy.

“Working people refuse to pay the price for Donald Trump’s war in the Middle East,” the European Trade Union Confederation, which represents 93 trade union organisations in 41 European countries, told the media. “Today’s rallies show working people will not stand by and see their jobs and living standards destroyed.”

Josua Mata, leader of the SENTRO umbrella group of workers’ groups in the Philippines, said: “Every Filipino worker now is aware that the situation here is deeply connected to the global crisis.”

Renato Reyes, a leader of the left-wing political group Bayan in the Philippines, told The Associated Press: “There will be a louder call for higher wages and economic relief because of the unprecedented spikes in fuel prices.”

In Indonesia, Said Iqbal, president of the Indonesian Trade Union Confederation, told reporters: “Workers are already living pay cheque to pay cheque.”

Some of the largest demonstrations are being held in South America, including in Chile, Bolivia and Venezuela. In Argentina, angry workers protested on Thursday in the capital of Buenos Aires over President Javier Milei’s recent overhaul of long-held labour protections.

In Cuba, the foreign ministry held a gathering on Thursday in defiance of what it called the US’s “aggressions, threats, intensified blockade, and energy siege”.

On Friday, Cubans are expected to mark International Labour Day with a mass rally and a march in Havana.

In many countries, Labour Day rallies attract large crowds because May 1 is a public holiday. In the Turkish city of Istanbul, roads around Taksim Square were closed to make way for marches during the day. Later on Friday, demonstrators clashed with police, international media reported.

In France, where most people have the day off for May Day, workers’ unions using the slogan “bread, peace and freedom” called for protests in Paris and other cities.

Global recession fears

Fears of a global recession are looming over Labour Day rallies at a time when income inequality is growing.

In Gaza, Palestinian workers have cancelled May Day events because of the economic crisis caused by Israel’s genocidal war on Gaza and poor conditions on the ground.

The Palestinian General Federation of Trade Unions said that about 550,000 workers across Gaza and the West Bank have no income and that the situation is unprecedented.

The International Trade Union Confederation has reported that at least four CEOs of major corporations each pocketed more than $100m in pay and bonuses last year, while many workers are facing potential job cuts.

Workers’ rights coalitions are calling for urgent action to curb extreme wealth. They want governments to impose higher, fairer taxes on the wealthiest and limit excessive executive pay.

While Labour Day began in the US, when workers protested for an eight-hour workday in the 1880s, the US does not count May Day as a public holiday.

However, an umbrella group of activist and workers’ groups known as May Day Strong has called for protests under the slogan, “workers over billionaires”. Hundreds of demonstrations and marches have been planned across the US.