Venezuelan oil revenues are currently controlled by the US Treasury Department. (Archive)

Caracas, May 15, 2026 (venezuelanalysis.com) – Venezuelan oil production has moved past 1 million barrels per day (bpd) for the first time in over seven years.

The latest OPEC monthly report placed the Caribbean nation’s April output at 1.031 million bpd, as measured by secondary sources. The figure increased by 46,000 bpd compared to the previous month.

For its part, state oil company PDVSA reported April’s production at 1.136 million bpd, up from 1.095 million bpd in March. Direct and secondary measurements have differed over time due to disagreements over the inclusion of natural gas liquids and condensates.

With the oil industry under crushing US coercive measures, crude production plummeted from around 1.9 million bpd when the first sanctions were levied against PDVSA. Following the US imposition of an export embargo in January 2019, output fell under 1 million bpd, hitting decades-lows around 350,000 bpd in 2020 before a steady recovery in recent years.

Since the January 3 US military strikes against Venezuela and kidnapping of President Nicolás Maduro, the Trump administration has imposed control over the nation’s energy sector, with revenues deposited in US Treasury-run accounts before being partially returned to Caracas at US officials’ discretion.

US Secretary of State Marco Rubio stated on Thursday that “for the first time in over a decade the wealth of Venezuela is benefitting the people of Venezuela,” though he did not mention the impact of US sanctions first imposed in late 2014.

While US coercive measures remain in place, the White House has issued a series of licenses allowing Western corporations to return to the Venezuelan energy sector.

BP, Chevron, Eni, Repsol, and Shell are among the companies to have struck oil and natural gas contracts with the Venezuelan government led by Acting President Delcy Rodríguez in past weeks, taking advantage of a recent pro-business legislative overhaul that slashed royalties and taxes, granted private partners increased control over operations and sales, and opened the way for disputes to be settled in international arbitration bodies.

Lesser-known companies Overseas Oil and Crossover Energy have likewise inked agreements for energy projects in the South American country.

ExxonMobil and ConocoPhillips are also evaluating prospects for a return to Venezuela, according to the Wall Street Journal. The two oil giants saw their assets nationalized by the former Hugo Chávez government in the 2000s after refusing to accept the country’s reforms asserting sovereignty over the industry. Both corporations would go on to secure compensation via international arbitration, with an award of over US $10 billion to ConocoPhillips still outstanding.

The recent rebound in oil production coincided with an increase in US-sourced diluent imports. Exports also surged in April to 1.23 million bpd, the highest figure in over seven years. Apart from a growing number of cargoes to US refineries, Indian refiner Reliance is receiving increased shipments after securing US Treasury approval.

In contrast, two tankers reportedly headed to China and Cuba, respectively, will return their cargoes to Venezuelan ports after being intercepted by US naval forces. Prior to the January 3 operation and US control over oil exports, China had been the primary destination for Venezuelan crude. Caracas had likewise been the main supplier of oil to Cuba in the last two decades.

Venezuelan and US authorities have offered no clarity on the return of export proceeds to the South American country, with US Secretary of State Marco Rubio stating that Caracas needs to submit a “budget request” before accessing its funds. The Venezuelan Central Bank’s handling of US-disbursed resources will be subjected to outside auditing, with Pentagon and CIA contractor Deloitte reportedly among the companies hired.

Despite the absence of official data on Venezuelan export revenues and the portion being returned to the country, the Rodríguez administration’s injection of foreign currency into exchange tables run by public and private banks increased in April and May. US authorities reportedly mandated that PDVSA revenues be funneled directly to private sector importers via forex auctions as opposed to having the Venezuelan Central Bank run foreign currency assignments.

The imposition of Venezuelan state sovereignty over the oil industry was one of the pillars of the Bolivarian Revolution from the get-go.

This edition of Tatuy Tv’s “Chávez the Radical” compiles several speeches by ComandanteChávez where he discusses the multiple policies that had subordinated the Venezuelan oil industry to transnational corporate interests and their nefarious consequences.

Issues like state ownership, royalties, taxes, and international arbitration are as relevant as ever today as the country undergoes major pro-business reforms in the oil sector.

US President Donald Trump has called Cuba ‘a failed nation’, as his administration expands its pressure campaign. Cuba has announced it’s getting rid of its fixed prices at the petrol pump as fuel shortages and power cuts worsen.

After successfully launching Nigeria’s only operational oil refinery in 2024, billionaire businessman Aliko Dangote has set his sights on East Africa as the next location for another mega refinery project, according to recent reports.

It comes as African countries are actively seeking ways to make energy more secure, following huge global disruptions amid the US and Israel’s war on Iran and Tehran’s subsequent closure of the Strait of Hormuz, through which about 20 percent of the world’s oil and natural gas is shipped.

Recommended Stories

list of 3 itemsend of list

Dangote, Africa’s richest man, appeared to be one of the winners from this fallout when his newly operational refinery, located in Nigeria’s commercial Lagos State, began selling large volumes of crude oil across the continent as the war on Iran escalated in March and global oil prices soared.

At present, West, South and East Africa rely primarily on importing refined petroleum products from the Middle East, meaning they are highly vulnerable to disruptions there.

Neighbours of Nigeria – Cameroon, Togo, Ghana and even Tanzania, further to the east – are among the countries that have turned to Nigeria as supplies from the Middle East dry up.

By the end of March, the refinery, which has the capacity to produce 650,000 barrels per day (bpd), reported it was also receiving orders from beyond the continent, especially for severely scarce jet fuel as hundreds of flights were cancelled across regions.

Supply from Dangote’s refinery has cushioned the impact of the war in terms of fuel supply for Nigeria and neighbouring countries, analysts say.

Nigeria is Africa’s largest oil producer, and the $19bn project in Lagos is currently the world’s largest single-train refinery, meaning it employs a single processing line rather than multiple units. But it hit full production capacity in February 2026, the same month the war with Iran started.

Nigeria has no functional state-owned refinery, so Dangote’s refinery is now positioning the country to be a net exporter of jet fuel and diesel.

Here’s why more refining capacity in Africa matters for the continent:

Petroleum trucks line up at the gantry inside the Dangote Industries oil refinery and fertiliser plant site in the Ibeju Lekki district of Lagos, Nigeria, March 2, 2026 [Sodiq Adelakun/Reuters]

What is Dangote’s plan for an East Africa refinery?

In April, Kenya’s President William Ruto announced that East African countries were in talks to build a joint oil refinery at Tanzania’s Tanga port, which would have a similar capacity to Dangote’s Lagos operation.

“We do not want to be held hostage any more by the Strait of Hormuz,” Ruto said at a Nairobi business event in April, which Dangote was present at.

“We do not want to be held hostage by wars that are started by other people. We have our resources here, and we are saying we are going to use our African resources to industrialise our region.”

In an interview with the Financial Times on Sunday, however, Dangote said he would prefer to build the new operation in Kenya rather than Tanzania.

“I’m leaning more towards Mombasa because Mombasa has a much larger, deeper port,” the billionaire told the UK newspaper.

“Kenyans consume more. It’s a bigger economy,” he said, adding that “the ball is in the hands of President Ruto … Whatever President Ruto says is what I’ll do.”

He has projected construction costs of between $15bn and $17bn.

But venturing into East Africa, which has a very different commercial landscape from West Africa, could prove a challenge, analyst Dumebi Oluwole of Lagos-based intelligence firm Stears told Al Jazeera.

“Dangote has proven it [his operation] can build at scale,” she said. “The East African test will be whether it can also navigate the political and logistical landscape of a fragmented, multi-country market.”

Why aren’t African countries already producing more oil?

Despite having sizeable crude reserves, African countries only refine about 44 percent of the total oil consumed themselves, with imports making up the rest, according to a 2022 African Union report.

The top producers of refined oil are Algeria, Egypt and South Africa. There are about 21 refineries in North Africa.

Southern Africa has another seven, while West Africa has 14. However, most refineries in the two regions are either not operating or are producing below the capacity they are equipped to.

East Africa’s only existing refinery is in Mombasa, but it stopped operating in 2013 due to a combination of slow government policies and exiting investors, who deemed it commercially unviable as a result.

There is currently no refining capacity at all in East Africa, despite the region having about 4.7 billion barrels of crude reserves, according to the African Union, mainly in Uganda, South Sudan, Kenya and the Democratic Republic of the Congo.

Kenya imported 40 million barrels of petroleum in 2025. It regularly buys oil from the UAE, Saudi Arabia, India and Oman, all of which have been hampered by Iran’s closure of the Strait of Hormuz.

Nigeria itself is Africa’s biggest net crude producer with a 1.5 million to 1.6 million bpd capacity. The country has not refined meaningfully since 2019.

What difference will local refineries make for African countries?

Exporting most of its crude to then import refined products is expensive and puts Africa on the back foot, analyst Oluwole said.

More oil refined on the continent would mean lower petrol pump prices, lower transport costs, and more energy available for people and businesses, in theory. It would also mean greater access to by-products like fertilisers for farmers, for example, or petrochemicals for manufacturers.

“Dangote has demonstrated that a viable, scalable, intra-African energy supply option is possible – that proof of concept matters enormously,” said Oluwole.

“It reflects a growing continental conviction that Africa can provide for itself, and that this is no longer wishful thinking,” she added.

In Nigeria’s case, Dangote’s refinery is yet to ease pressures, though. Local airlines, for example, have complained about having to pay high prices for jet fuel even with improved local supplies. Analysts say that could be because Nigeria’s government removed fuel subsidies in 2023. Bureaucracy within the state oil company also forced Dangote’s refinery to import crude.

Still, the refinery is contributing to “a more transparent and competitive market”, Oluwole said, adding that results should eventually show.

Other countries are stepping up. Last week, Angola’s $470m Cabinda refinery began supplying domestic as well as foreign markets. The project is owned primarily by the United Kingdom’s Gemcorp Capital and has a capacity of 30,000bpd, with plans to double by the end of 2026.

Dangote’s planned refinery in Kenya, if completed, could also help to reduce East Africa’s reliance on the Middle East.

A separate, government-funded refinery project in Uganda’s Hoima region is also in the works. Authorities expect the project to be able to refine 60,000bpd when it starts operations in 2029. It will be fed by the joint Uganda-Tanzania East African Crude Oil Pipeline (EACOP), an ongoing project which will transport crude from Uganda’s Lake Albert to Tanzania’s Tanga Port.

Uganda also plans to produce diesel, jet fuel, kerosene and Liquefied Petroleum Gas (LPG).

With big plans in place, Oluwole says it’s now left to African governments to create enabling business environments for the private sector.

“Dangote has opened the door,” she said. “The question now is whether African institutions and governments will walk through it.”

US Department of Energy moves to transfer 53.3 million barrels amid rising oil prices.

Published On 12 May 202612 May 2026

The United States has announced its latest release of emergency oil stockpiles in coordination with the International Energy Agency (IEA).

The US Department of Energy said on Monday that it had begun transferring 53.3 million barrels from the strategic petroleum reserve after awarding contracts to nine companies under its emergency exchange programme.

Recommended Stories

list of 4 itemsend of list

Trafigura Trading LLC, a Texas-based commodities trading company, was granted the biggest haul of nearly 13 million barrels, with Marathon Petroleum Corporation and ExxonMobil set to receive 12.4 million barrels and 11.4 million barrels, respectively.

Macquarie Commodities Trading US, Atlantic Trading & Marketing, BP Products North America, Energy Transfer Crude Marketing, Mercuria Energy America and Phillips 66 will receive between 1.05 million and 6.55 million barrels each, according to the Energy Department.

Under the department’s exchange scheme, participating firms are required to replenish the stockpile with new barrels at a later date.

“These actions continue to move oil swiftly into the market, address near-term supply needs, and ensure that the Strategic Petroleum Reserve remains strong through the return of premium barrels,” Kyle Haustveit, the head of the department’s Hydrocarbons and Geothermal Energy Office, said in a statement.

The transfer comes after US President Donald Trump’s administration agreed in March to release 172 million barrels of crude as part of the IEA’s coordination of the largest unloading of global stockpiles in history.

Oil prices have surged since the US and Israel launched their war on Iran in late February, with Tehran’s retaliatory blockade of the Strait of Hormuz paralysing one of the world’s most important trade routes.

Maritime traffic in the strait has ground to a halt amid Iranian threats against commercial shipping, disrupting about one-fifth of the global oil trade.

Oil prices continued to edge higher on Monday after Trump dismissed Iran’s latest peace proposal and warned that the ceasefire between the sides was “on life support”, dampening hopes for a quick resolution to the conflict.

Facing growing public discontent over rising fuel prices, Trump on Monday also pledged to waive the 18.4 cents-per-gallon federal tax on petrol, though taxation is the purview of the US Congress.

Futures for Brent crude, the international benchmark, were up about 1 percent in Asia on Tuesday morning, topping $105 a barrel.

Oil prices surged in early trade as investors digested the latest developments in the Middle East, with both Brent and US crude climbing over 4%.

ADVERTISEMENT

ADVERTISEMENT

It comes after Trump’s rejection of Tehran’s response to the latest US proposition on bringing the conflict in Iran, and subsequent impact on trade passing through the Strait of Hormuz, to an end.

In other trading, US futures edged lower, while Tokyo’s Nikkei 225 fell 0.4% to 62,486.84 after briefly reaching another record high in intraday trading at above 63,300.

South Korea’s Kospi gained 4.1% to 7,804.71. It also hit an all-time intraday high, led by gains from tech-related stocks including Samsung Electronics and memory chip maker SK Hynix.

Technology-related stocks and growing artificial intelligence-related interest have supported markets in Japan and South Korea despite the Iran war, with the Nikkei 225 and Kospi rising more than 10% and 30%, respectively, over the past month.

Meanwhile, Donald Trump will head to China this week for talks with his counterpart, Xi Jinping. The two leaders are expected to discuss a wide range of topics, including trade concerns.

Crude oil futures gained Sunday after President Trump rejected Iran’s latest response to his proposal to end the Middle East as “totally unacceptable,” while the Strait of Hormuz remains mostly closed.

Iran’s proposal reportedly emphasizes Iranian sovereignty over the strait while calling

Satellite images have captured a suspected oil slick spanning dozens of square kilometres near Iran’s Kharg Island, the country’s main oil export hub. Despite fears of a disaster, environmental observers say the slick is shrinking.

Large-scale crude oil storage tanks are seen in the background at a Sodegaura Refinery in Sodegaura, Chiba Prefecture, Tokyo Bay, Japan, 06 April 2026. Photo by FRANCK ROBICHON / EPA

May 8 (Asia Today) — Japan is expanding imports of Russian Sakhalin-2 crude oil beyond a one-time emergency purchase, extending supply arrangements to multiple refiners and fuel networks around Tokyo Bay as concerns grow over instability in the Strait of Hormuz.

Japanese officials have reportedly asked Fuji Oil, an Idemitsu Kosan affiliate, to accept crude shipments from the Sakhalin-2 project after similar imports were arranged through Taiyo Oil.

The move comes as Japan seeks to reduce risks tied to Middle Eastern oil supplies while continuing to use sanction exemptions that remain in place for Sakhalin-2 energy resources.

The Sankei Shimbun reported Wednesday that the tanker Voyager, carrying crude oil from the Russian Far East project, was heading toward Fuji Oil facilities in Sodegaura, Chiba Prefecture.

Fuji Oil became a subsidiary of Idemitsu Kosan in November 2025 and operates a refinery that supplies petroleum products to the greater Tokyo metropolitan area.

According to ship tracking data cited by the newspaper, the Voyager departed Prigorodnoye Port in southern Sakhalin on April 24 and arrived near Imabari in western Japan on Sunday. The vessel later conducted unloading operations at Taiyo Oil facilities before departing for Tokyo Bay.

The tanker is expected to arrive in Sodegaura on Friday and leave Tokyo Bay on Saturday.

Idemitsu Kosan acknowledged the shipment was made at the request of Japan’s Ministry of Economy, Trade and Industry.

A company spokesperson told Sankei that the import did not violate sanctions and described it as part of efforts to diversify procurement sources and maintain stable fuel supplies.

Before halting most Russian crude purchases after Moscow’s invasion of Ukraine in 2022, Idemitsu sourced roughly 4% of its oil imports from Russia.

Analysts say the significance of the latest shipment lies not simply in Japan buying Russian oil again, but in Tokyo integrating Sakhalin-2 crude into a broader emergency procurement network involving multiple refiners.

Japan had already begun using the sanctions exemption amid rising Middle East tensions, but the latest deliveries suggest the mechanism is evolving into a more permanent contingency supply channel.

The development is also drawing attention in South Korea, which remains heavily dependent on Middle Eastern oil imports.

According to Korea National Oil Corp. data, South Korea imported about 1.03 billion barrels of crude oil in 2024, with 71.5% sourced from the Middle East. Saudi Arabia accounted for 32.2% of imports, followed by the United States at 16.4% and the United Arab Emirates at 13.7%.

Although South Korea has steadily increased imports of U.S. crude, its supply structure remains highly exposed to shipping disruptions through the Strait of Hormuz.

Energy analysts say South Korea may eventually need to move beyond reliance on strategic petroleum reserves alone and develop broader contingency planning that includes alternative suppliers, refinery compatibility and supply stability at major refining hubs such as Ulsan, Yeosu, Daesan and Incheon.

Japan’s latest actions suggest governments are increasingly seeking practical emergency supply options within existing sanctions frameworks rather than relying solely on traditional energy security measures.

Zawiya refinery shut down in ‘precautionary measure’ as emergency declared following explosions and gunfire nearby.

Published On 8 May 20268 May 2026

Libya’s largest operational oil refinery at Zawiya has been shut down and an emergency declared following fighting between armed groups nearby.

The National Oil Corporation (NOC) and Zawiya Refining Company announced a “precautionary halt” to operations and evacuated employees from the oil complex and port.

Recommended Stories

list of 3 itemsend of list

NOC confirmed the safety of all employees and added that fuel supplies would continue as normal.

A Facebook statement said alarm sirens were activated “following armed clashes involving heavy weapons that erupted around the oil complex in the early hours of Friday”.

“These clashes resulted in several heavy weapons projectiles landing in various locations within the oil complex,” adding that no significant damage had been reported.

“However, the clashes have intensified and reached the residential area adjacent to the refinery, making the area a direct target for heavy shelling and significantly increasing the risk of further damage,” it said.

Authorities in Zawiya, west of the capital Tripoli, said they had launched a “large-scale operation” against criminal groups, as fighting and explosions were heard, the AFP news agency reported.

The operation targeted “criminal hideouts and wanted individuals” who were “involved in serious acts”, the authorities said, citing “murder and attempted murder, kidnapping and extortion, drug, arms and human trafficking and illegal migration”.

Videos verified by Al Jazeera showed explosions and gunfire, as well as damage to several cars and facilities inside the refinery. The sound of sirens was audible after shells fell inside operational sites.

The Zawiya Refining Company called on all parties to cease fire immediately and for the Libyan authorities to intervene to protect lives and key facilities.

The refinery, around 40km (25 miles) west of Tripoli, has a capacity of 120,000 barrels per day. It is connected to the 300,000 bpd Sharara oilfield.

Since Muammar Gaddafi’s downfall in 2011, Libya has been plagued by violence between the Tripoli-based Government of National Unity (GNU), led by Prime Minister Abdul Hamid Dbeibah, and the eastern-based government, led by military leader Khalifa Haftar which is not internationally recognised.

It is unclear what caused the fighting, but local media said it started following a security operation against armed groups.

Footage released by the Pentagon shows US strikes on two Iranian oil tankers in the Strait of Hormuz. The US military says the vessels were disabled following overnight exchanges of fire with Iranian forces, preventing them from reaching ports in the Gulf of Oman.

This photo shows a South Korean oil carrier that arrived at a port in the southwestern city of Yeosu on Thursday. Photo by Yonhap

A South Korean vessel has successfully passed through the Red Sea and is currently en route home, marking the fourth oil shipment of its kind, the oceans ministry said Friday.

The arrival comes as Seoul has been scrambling to bring in oil through alternative routes amid the ongoing blockade of the Strait of Hormuz.

After loading oil shipments at Saudi Arabia’s Yanbu Port, the ship passed through the Red Sea at around 11:00 a.m., the Ministry of Oceans and Fisheries said. Details of the vessel’s movement were withheld due to safety reasons.

The ship is the fourth Korean oil carrier to transit the waterway that connects the Indian Ocean to the Mediterranean via and Suez Canal since the country began using the waterway to avoid the Strait of Hormuz.

That water lane has effectively been blocked by Iran for over a month.

The first Korean ship to take the alternate route since the war began arrived at a port in the southwestern city of Yeosu on Thursday, carrying some 2 million barrels of oil, according to sources familiar with the matter. The ship had left the Red Sea last month.

Two more Korean oil carriers successfully passed through the Red Sea earlier this week.

The ministry said it will continue efforts to stabilize oil shipments to the country and take steps to ensure the safety of Korean vessels and crew members navigating through the region.

Copyright (c) Yonhap News Agency prohibits its content from being redistributed or reprinted without consent, and forbids the content from being learned and used by artificial intelligence systems.

Brent crude rises amid clashes in critical waterway.

Published On 8 May 20268 May 2026

Oil prices have jumped after clashes between United States and Iran in the Strait of Hormuz pushed their tenuous ceasefire to the brink.

Futures for Brent crude rose as much as 7.5 percent during a volatile trading session on Thursday, before easing as Asia’s markets opened on Friday morning.

Recommended Stories

list of 4 itemsend of list

The international benchmark stood at $101.12 per barrel as of 03:00 GMT, down from the day’s high of $103.70.

The latest rise came after the US and Iran exchanged fire in the critical strait, a conduit for about one-fifth of global oil and natural gas supplies, despite the truce announced between the sides on April 7.

US Central Command (CENTCOM) said it launched strikes on Iran after three US Navy guided-missile destroyers came under attack from Iranian missiles, drones and small boats in the strait.

Iran’s Khatam al-Anbiya Central Headquarters earlier accused the US of violating the ceasefire by attacking an Iranian oil tanker and another vessel in the vicinity of the waterway.

The Iranian military headquarters also accused the US of targeting civilian areas, including Qeshm Island.

US President Donald Trump on Thursday appeared to downplay the clashes, saying the ceasefire remained in effect, while Iran’s state-run Press TV said the situation had gone “back to normal”.

Shipping in the strait has been at a near standstill since late February amid the threat of Iranian attacks on the massive oil tankers that usually transport much of the world’s energy supplies.

Brent prices are up about 40 percent compared with before the war amid an estimated shortfall in daily production of 14.5 million barrels.

Asian stock markets opened lower on Friday amid the heightened tensions, with Japan’s benchmark Nikkei 225, South Korea’s KOSPI and Hong Kong’s Hang Seng Index each falling more than 1 percent.

On Wall Street, the benchmark S&P 500 fell about 0.4 percent overnight after hitting an all-time high the previous day.

A gas station in South Africa displays the latest prices for petrol and diesel after they hit a record high on Wednesday despite global oil prices plunging back below $100 a barrel on hopes of a deal to end the war in Iran. Photo by Kim Ludbrook/EPA

May 6 (UPI) — Global oil prices fell sharply and financial markets rallied Wednesday after U.S. President Donald Trump paused a military operation to reopen the Hormuz Strait to commercial shipping to give advanced peace talks with Iran a chance to deliver “a complete and final deal.”

Falls in Brent crude of more than $10 a barrel to $99, American crude by $13 to $92 a barrel and rallies in Asian stock markets overnight that fed into Europe when bourses opened there failed to feed through to U.S. gas prices, which jumped 5 cents a gallon to their highest level of the war.

AAA motor club figures showed a national average of $4.54 for a gallon of petrol and $5.67 for diesel, meaning drivers were paying 53% and 51% more than before the war started on Feb. 28, with the caveat that fuel price adjustments normally lag crude oil price movements by several days.

The White House believes a draft one-page, 14-point memorandum of understanding to end the war and create a structure for more in-depth nuclear talks could succeed in breaking the deadlock, two U.S. officials and two other sources said.

An Iranian foreign ministry spokesman confirmed to CNBC that Iran was in receipt of the U.S. proposal and was “evaluating it.”

The Trump administration anticipates Iran will give its response with regard to the most critical elements of the plan in the next two days and although nothing has been finalized it was being seen as significant because it was the closest the sides had been to a deal since the beginning of the war.

However, Trump also appeared ambivalent, saying Wednesday it was “perhaps” too big of a stretch to believe Iran would take the deal and threatening to order the U.S. military to restart its airborne offensive against the country if it didn’t.

Analysts said investor confidence was boosted mainly by the fact the cease-fire was holding and signs that the economy was nowhere near as badly affected by the war as feared.

“This helped oil prices to come back down again and ease fears about a renewed escalation, with investors a bit more hopeful that an extended stagflationary shock would be avoided,” Deutsche Bank wrote in a note.

It added that investor confidence was also bolstered by new U.S. economic data showing among other positive indicators, that job vacancies declined less than anticipated in March, saying the numbers “cemented the case that the conflict’s wider economic impact was still fairly muted.”

“This helped oil prices to come back down again and ease fears about a renewed escalation, with investors a bit more hopeful that an extended stagflationary shock would be avoided,” they added.

Hopes were also riding on the possibility China would prevail on visiting Iranian foreign minister Abbas Araghchi to persuade Iran to uphold the current truce with the United States, so as not to throw a wrench into Trump’s visit to Beijing on May 14, the first by any U.S. president in almost a decade.

China is one of Iran’s largest customers for its oil exports.

President Donald Trump speaks before signing a proclamation inside the Oval Office at The White House on Tuesday. The memorandum is set to restore the Presidential Fitness Test Award, a competitive school-based fitness program last seen under the Obama administration. Photo by Tom Brenner/UPI | License Photo

Amid Spirit Airlines’ bankruptcy, airlines that were once confident in their financial resilience are now navigating a volatile geopolitical landscape.

The collapse of Spirit Airlines, the scrappy low-cost carrier, underscores the fragile economics of air travel amid $4-per-gallon jet fuel and high crude prices.

From Atlanta-based Delta Air Lines to Hong Kong-based Cathay Pacific, carriers are reassessing routes and fares as soaring fuel costs threaten profits, while the Iran war disrupts shipping through the Strait of Hormuz.

Airlines and investors had anticipated stable fuel costs in the second quarter, but analysts have had to adjust their outlooks. Forward-looking projections indicate fuel prices will remain above previous forecasts, a development that could continue to pressure airline profit margins and ticket pricing strategies.

“Fuel forward expectations for the second quarter haven’t changed, but what has changed are expectations for the rest of the year,” Matt Woodruff, head of aerospace and defense/transports at CreditSights, told Global Finance. “[Fuel prices] will be higher for longer than we were thinking a month or two ago.”

‘Good Aircraft’ Grounded

On April 23, former President Donald Trump publicly mused about rescuing Spirit Airlines, calling the carrier “virtually debt-free” and noting its “good aircraft, good assets.” He suggested buying the airline and potentially profiting when oil prices decline, adding, “I’d love to be able to save those jobs … I like having a lot of airlines, so it’s competitive.”

The plan never materialized, and Spirit shut down on May 3. Travelers remained stranded as jet fuel prices hit unprecedented highs amid the Iran war, now more than two months old.

“We regret to inform you that all Spirit Airlines flights have been canceled, effective immediately,” read a notice when opening the carrier’s app.

The ripple effects were felt beyond Dania Beach, Florida, where the airline is based. Spirit operated international flights throughout Latin America, the Caribbean, and Central America, including Colombia, Mexico, the Dominican Republic, Jamaica, Peru, Costa Rica, and Aruba. Its sudden closure left 17,000 direct and indirect employees without work.

The Trump administration and Treasury Secretary Scott Bessent quickly blamed Biden-era opposition to the much-debated Spirit/JetBlue Airways Corp. merger. The two carriers had a $3.8 billion deal in the works, which Bessent argued “would have given them much more resiliency.” Spirit filed for bankruptcy protection in November 2024, saddled with more than $2.5 billion in losses since 2020.

But no airline, not even one with low-cost appeal, is immune to the whims of the global oil market.

At the time of Spirit’s first bankruptcy under Biden, U.S. airlines were paying an average of $2.31 per gallon for jet fuel. Under Trump, that figure has nearly doubled, with the Argus US Jet Fuel Index reporting $4.26 per gallon as of May 4.

Consider the Warnings

Brent crude prices are hovering above $100 per barrel, while regional conflicts near the Strait of Hormuz—through which a significant share of the world’s oil passes—continue to heighten supply concerns.

Fuel is often the largest single operating expense for airlines. Delta Air Lines, for example, disclosed in a March filing that its 2025 fuel costs accounted for 31.3% of its operating expenses. The company noted that a one-cent increase in jet fuel adds about $40 million to its fuel tab for the year.

Delta paid $2.7 billion for fuel in the first quarter of 2026.

The airline produces some of its own jet fuel, which means it avoids paying full market prices for fuel conversion, shielding it from the worst of the “crack spread” costs, Woodruff said. “They’re getting a benefit relative to everyone else, but they’re still feeling it.”

Cuts are underway. Starting May 19, the company will no longer offer food or drinks on flights under 349 miles.

Other carriers are responding to the latest volatility by raising fares, canceling routes, rerouting aircraft to avoid restricted airspace, and reconsidering expansion plans. Airfares have increased five times since the war in Iran began, with a sixth hike underway late last month, according to the Wall Street Journal.

“The routes that aren’t doing well, those are going first,” Woodruff said. “Regional jets, for example, often don’t make much money — those are, for sure, a target.”

What’s Next

Spirit isn’t the only airline feeling the effects of this new norm. Its former suitor, JetBlue, is reevaluating routes that may no longer cover rising fuel, airport, and maintenance costs. Delta is canceling hundreds of flights, while international carriers — including Paris-based Air France, Cologne-based Lufthansa, and Cathay Pacific — are trimming routes to protect margins.

This shift stands in stark contrast to late 2024, when Delta CEO Ed Bastian welcomed the incoming Trump administration as a “breath of fresh air.” Through much of 2025, that optimism seemed justified, as major U.S. carriers forecast continued profitability into 2026.

And that might still be the case despite the war in Iran rattling global energy markets and upending long-held assumptions about fuel stability and travel demand.

Each airline is now telling a two-sided story about how robust demand is while also raising fares. United Airlines’ fare numbers, for example, will be 15% to 20% higher than last year.

Whether consumers will tolerate such a price hike remains to be seen. “Ultimately, consumers are going to decide what they are willing to pay and what they aren’t, not a formula,” Southwest CEO Bob Jordan told reporters in April.

Even the forward fuel curves today indicate that, even if the war ended today, costs wouldn’t normalize until well into next year, Woodruff said.

By 2027, airlines expect to offset most, if not all, of the recent fuel cost increases through higher fares, he added. But that outlook assumes forward fuel prices in the first quarter of 2027 will be lower than they are today. If they’re not, carriers could continue to face significant financial pressure.

Oil prices fell back in early trade but remained elevated as investors kept an eye on escalating tensions between the US and Iran and progress on ships passing through the Strait of Hormuz.

ADVERTISEMENT

ADVERTISEMENT

At the time of writing, Brent crude was trading 1.38% lower at $112.86 while US crude, or WTI, was down 2.27% at $104 per barrel. US futures edged 0.1% higher.

Elsewhere, regional trading was thin overnight with markets in Japan, South Korea and mainland China closed for holidays.

Hong Kong’s Hang Seng fell 1.1% to 25,805.98. Australia’s S&P/ASX 200 lost 0.5% to 8,649.80, while Taiwan’s Taiex traded 0.2% lower at 40,626.22.

The fragile ceasefire between the US and Iran was tested on Monday after the US military said it had sank six Iranian small boats targeting civilian ships, while two US-flagged ships successfully passed through the Strait of Hormuz.

The key waterway for oil and gas transport remains largely closed despite repeated demands from the US for Iran to reopen the strait and as the United States imposed a sea blockade on Iranian ports. US President Donald Trump’s “Project Freedom” plan under which the United States would help guide stranded ships through the Strait of Hormuz began on Monday.

Brent crude, the international standard, surged above $114 a barrel on Monday, gaining nearly 6%. Before the war began in late February, it was trading near $70.

Venezuela has gone through many stages in its assertion of ownership over natural resources and relationship with foreign corporations. (Venezuelanalysis / AI-generated image)

Venezuela’s recent Hydrocarbon Law reform has sparked fierce debates about its short- and long-term implications. In this essay, Blas Regnault, an energy policy analyst and researcher, offers an in-depth analysis of the new legislative framework, from the significant changes to the state’s governance over its natural resources to his perspective on a sovereign recovery of the oil industry.

The recent hydrocarbon reform: an overview

It is important to distinguish between two closely connected but analytically separate developments: first, US oversight of Venezuelan oil revenues after Maduro’s kidnapping; and secondly, the new Hydrocarbon Law itself. The first is an externally imposed mechanism that conditions oil sales, revenue collection, transport, and the distribution of oil proceeds to US interests. The second is a domestic legal reform whose constitutionality and political legitimacy have been widely questioned.

It remains unclear whether the new law is fully operative in practice, or whether it is only being applied selectively while its fiscal substance is displaced by the US revenue-control mechanism. But the outcome is largely the same: a loss of fiscal automaticity and a form of fiscal sovereignty under tutelage in relation to Venezuelan oil income.

In other words, the crisis of governance in the Venezuelan oil sector, together with its chronic lack of transparency since 2017, now culminates in a profound loss of sovereign control over all three dimensions of the business: its rentier dimension, belonging to the nation; its fiscal dimension, belonging to the state; and its shareholder dimension, linked to the role of the state oil company PDVSA as principal participant in extraction and commercialisation.

Therefore, the new law is not simply a technical reform. It is not merely about updating contracts, modernising procedures, or making the sector more attractive to investors. The deeper issue is that the reform changes the way the nation is compensated for the use of the subsoil and therefore alters the very governance of the sector. What is at stake is the relationship between sovereignty, ownership of the subsoil, and public income.

It is true that, on paper, the law formally preserves state ownership over the resource. But the business models it opens weaken the practical substance of that ownership. And that is the crucial point. Ownership is not a decorative legal formula. Ownership means that the state, acting on behalf of the nation, has the right to decide whether the resource remains underground or is extracted; and if it is extracted, under what conditions, with what public charge, and for whose benefit. The recent reform softens the link between ownership and the nation’s participation as owner of the subsoil, turning something that was once grounded in a general rule into something negotiable, adjustable, and highly discretionary.

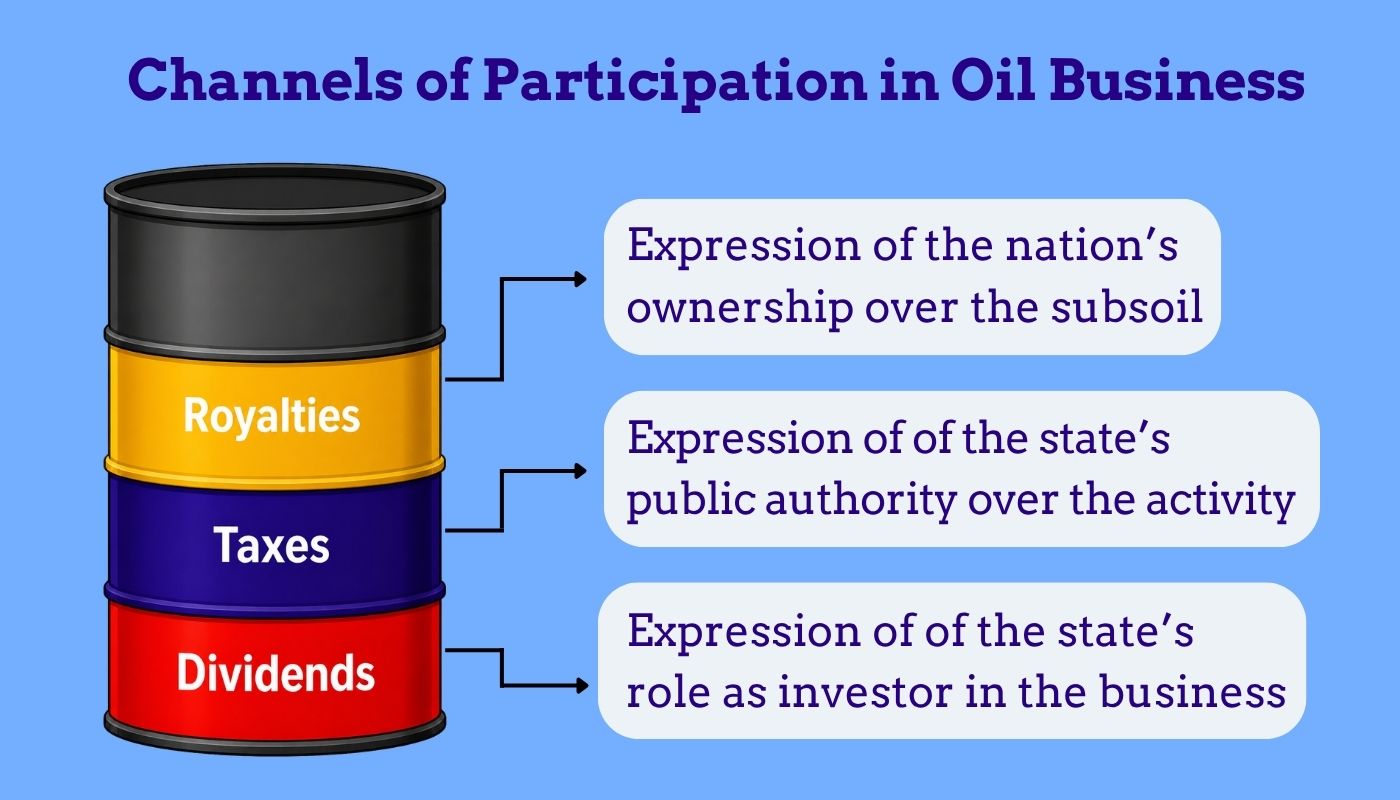

A useful way of understanding the economic and social significance of the reform is to distinguish the different streams of public income historically associated with oil in Venezuela. Under the former hydrocarbon law, the nation participated in the oil business through three distinct channels: as owner, as tax authority, and as shareholder. The first channel, corresponding to ownership, was royalty. The second was taxation, arising from the state’s fiscal authority over the activity. The third was dividends, arising when the state participated through PDVSA and therefore received income in its capacity as stakeholder rather than as landlord or tax authority.

This distinction matters because the oil business has historically involved different claimants competing over the fruits of extraction. In a sector marked by extraordinary profitability and strategic importance, the owner of the rent, the fiscal authority, and the capitalist operator all seek to maximize their share of the value generated. In the Venezuelan framework that prevailed before 2026, those three roles were clearly present: the nation as owner of the subsoil, the state as fiscal authority, and the operator as capitalist actor. The new law alters the balance between them.

Illustration of the different revenue streams in the Venezuelan oil industry. (Venezuelanalysis)

Royalty

The royalty is where the change is most revealing. As already noted, royalty is the clearest expression of ownership. It is paid upfront. It does not depend on profit. It is charged before taxes are assessed and before the remaining income covers the factors of production; that is, wages, interest, profits, and the other claimants on the project. In other words, royalty is not part of the production costs. If the oil price is 100 dollars per barrel and the agreed royalty rate is 30 per cent, the owner receives 30 dollars per barrel straight away. That is the proprietorial logic in its purest form.This has long been a battleground in the global oil industry. The dispute over rent has historically taken place between the operating companies, whether private national oil companies acting as operators, and the owner of the resource, that is, the landlord. Depending on the property-rights regime, that owner may be a private individual, as in parts of Texas, or the state, as in Venezuela and in most oil-exporting countries. Whether in Texas, Alaska, Saudi Arabia, Kuwait, Norway, the United Kingdom, Nigeria, or Venezuela, the property-rights regime has been the principal legal instrument through which the owner secures a share of the rent. It is a legitimate exercise of sovereignty, recognised by all parties involved in the global oil business.

Table 1: Effect of royalty rates on the nation’s per-barrel income using Merey 16 prices, Venezuela, January–March 2026

Month (oil price)

30% royalty

10% royalty

1% royalty

Jan 2026 ($43.21)

$12.96

$4.32

$0.43

Feb 2026 ($52.31)

$15.69

$5.23

$0.52

Mar 2026 ($86.00)

$25.80

$8.60

$0.86

Source: author’s calculations based on OPEC-MOMR January – March 2026 for Merey 16

And yet the new law, in practical terms, empties out that proprietorial logic by turning royalty into a negotiable variable within a range of zero to 30 per cent, something highly unusual in the global oil business. The potential scale of the loss becomes immediately clear once one thinks in terms of export volumes. At an oil price of 86 dollars per barrel, a 1 per cent royalty leaves the nation with less than one dollar per barrel, whereas a 30 per cent royalty yields 25.8 dollars. If Venezuela exports 800,000 barrels per day, that means roughly 688,000 dollars per day under a 1 per cent royalty, compared with 20.64 million dollars per day under a 30 per cent royalty. This is a dramatic compression of the owner’s income. It shows that a high oil price cannot compensate for the hollowing out of the royalty. Put simply, under the new law, higher oil prices will no longer automatically translate into greater income for the nation if royalties are arbitrarily lowered to the benefit of transnational capital. This is not a marginal fiscal concession; it is a radical compression of the nation’s proprietorial income.

Taxes

Turning to taxes, under the previous legal framework, the fiscal regime included not only taxes on profits, but also local and municipal taxes on oil activity, together with other parafiscal charges and special contributions linked to extraordinary profits. These different channels gave the public side several routes through which to capture value from extraction. Under the new law, much of that architecture is displaced and compressed into an integrated tax on gross income that will also be set in a discretionary fashion up to a fixed ceiling. According to supporters of the reform, this new framework is designed to ensure the project’s “economic equilibrium.” But the political significance of that shift is considerable. What was previously structured through several distinct legal claims can now be more easily absorbed into a flexible package, negotiated project by project. In that sense, this is not simply simplification; it is a substantial thinning of the fiscal claim. Once the fiscal architecture becomes thinner, the public claim over oil value becomes weaker, more flexible, and ultimately more negotiable.

Table 2 illustrates the magnitude of the change using the March 16, 2026, marker Merey 16 price. Under the previous regime, taxes and parafiscal charges alone could amount to about $31 per barrel, or 36 percent of the barrel price. Under the post-reform interim scenario, that could fall to about $17.6 per barrel, or 20.5 percent.

Table 2: Tax and parafiscal take per barrel before and after the reform

Fiscal Component

Former Law (reference model)

Post-reform scenario

Difference

Taxes and parafiscal charges per barrel (USD)

$31

$17.6

-$13.4

As share of barrel price (%)

36%

20.5%

-15.5%

Note: Figures are illustrative and based on the March 2026 Merey 16 price of US$86 per barrel, using the reference model for the former regime and the intermediate scenario for the post-reform regime. Source: Authors’ calculations based on the comparative fiscal scenarios and March 2026 Merey 16 price data.

Dividends

Finally, there are dividends arising from state equity participation, and these too must be distinguished from both royalty and taxation. Dividends are not paid because the nation owns the subsoil, nor are they collected because the state exercises fiscal authority over the activity. They arise because the state participates in the business as shareholder and therefore receives part of the profits in its capacity as investor. In other words, dividends represent the state’s participation in the profits of the business itself. But that income is not necessarily available for immediate public use in the same way as royalty or taxation. Part of it may be retained within the company, used for reinvestment, capital expenditure, debt service, or the wider financial needs of the enterprise. So, unlike royalty, which expresses ownership, or tax, which expresses fiscal authority, dividends are tied to the corporate logic of the business. Depending on the ownership structure, this channel of participation may range, illustratively, from zero to 60 per cent of distributable profits.

International jurisdiction of potential oil litigation

There is also an important jurisdictional dimension. By reducing the fiscal share captured by the state and by placing greater weight on contractual flexibility, the reform moves the sector towards a framework that is more exposed to international arbitration. At the same time, the sanctions and licensing regime has become part of a broader architecture of control over the oil business: control over access to the fields, control over marketing channels, and control over financial access to revenues. So, this is not merely a domestic fiscal reform. It is also part of a broader reordering of the legal and financial chain through which Venezuelan oil is governed.

Key takeaways

Supporters of the new law argue that it delivers increased flexibility, greater operability, improved investment prospects, and greater bankability. And that is not a trivial argument. In a country that has experienced production collapse, sanctions, institutional erosion, and a loss of market share, it is understandable that policymakers would seek a framework that appears more attractive to capital. In that sense, the reform may indeed reduce perceived risk and make projects easier to finance. It may also simplify part of the gross take and make negotiations easier. In that sense, the reform should not be caricatured. But it also entails the abandonment of each of the nation’s and the state’s historic roles in the sector, undermining the institutional fabric that once gave the oil economy a degree of stability and rationality.

For that reason, the disadvantages of the reform ultimately outweigh its potential benefits. What is lost is fiscal automaticity. That means the nation is no longer guaranteed a stable share by rule, but must now negotiate it, justify it, or recover it through more uncertain channels. Put differently, the reform replaces payment-by-rule with payment-by-negotiation on a case-by-case basis. In practical terms, each contract will generate its own conditions over each of the principal sources of public income arising from oil activity.

What is also lost is the clarity of a system in which the state charges because it owns the resource, not because the project happens to be commercially convenient. Once royalties become variable and fiscal terms are subordinated to the “economic equilibrium” of the project, the centre of gravity shifts. The guiding principle is no longer the nation as sovereign owner; it becomes the financial viability for the investor/operator. That is a profound political change presented as technical pragmatism.

In summary: the 2026 reform does not abolish formal ownership, but it hollows it out in practice. It replaces a more proprietorial fiscal logic with a more contractualized and discretionary one. That may attract investment, but it also weakens the automatic link between national ownership and national income. Whatever mechanism one chooses to emphasize, the result is much the same:

The nation no longer receives royalty by rule, but under externally conditioned arrangements. What is presented as flexibility is a retreat from ownership.

The state compresses its fiscal participation at every level.

The state oil company weakens its position as an investor.

Once that happens, the central question is no longer simply, “How much is the state collecting?” but rather “Who decides, under what rules, with what traceability, and with what accountability?”

Shell oil wells in Lake Maracaibo, Western Venezuela, in the 1950s. (Archivo Fotografía Urbana)

The historical context of Venezuela’s oil legislation

Venezuela’s oil history is not just a history of contracts or companies; it is a history of how the nation has tried to define its authority over the subsoil. Venezuela did not begin from the same position as many oil-exporting countries in West Asia or North Africa. It was already an independent republic when it developed its mining and hydrocarbons legislation. That matters, because it means Venezuela built a national jurisdictional framework around state ownership of mines and deposits, rather than inheriting a colonial concessionary order imposed from outside. That distinction is central.

From the early twentieth century onwards, successive legal frameworks progressively consolidated the republic’s sovereign claim over oil-bearing land. In other words, Venezuelan oil law was historically moving towards a more explicit assertion of the nation’s right to charge for the extraction of its natural wealth. This is one reason Venezuela mattered so much internationally: not only because it was a major producer, but because it became a reference point for fiscal regimes and sovereign oil governance, including later in the wider OPEC environment. In that sense, Venezuela’s experience was historically complete in a way that few other oil-producing countries were.

Nevertheless, there is a paradox surrounding the 1975-1976 nationalization of the oil industry. On paper, it ought to have marked the culmination of national control, but it did not deepen sovereignty. In practice, it helped produce a shift towards a more internationalized governance structure. The Ministry, as representative of the owner-nation, was gradually displaced by state oil company PDVSA, and PDVSA increasingly operated under a logic of global business rather than one of public sovereign rule. So instead of the owner-state speaking directly, the national oil company became the intermediary, and that had long-term consequences. Put differently, PDVSA, together with international oil capital, gained ground in the long struggle to reduce the landlord’s direct grip over rent.

This is where the historical relationship with Western transnational corporations becomes more nuanced than a simple story of foreign domination versus nationalist resistance. The issue is not merely the presence of Western companies, but the governance structures they operate under. Venezuela moved from a more classic proprietorial regime towards a more cessionary one, and later, especially in the late 1980s and 1990s, towards more liberal or non-proprietorial arrangements. The oil opening (“Apertura Petrolera”) of the 1990s is especially important here, because it reduced the fiscal burden and shifted the framework in a way that centralized the operator’s conditions. That was already a major break.

The Chávez years brought a partial reversal. The restoration of the property right was not merely ideological posturing; it was a restoration of a more classical fiscal logic, in which the sovereign character of the state take was reaffirmed. But that restoration took place amid other contradictions, including the politicization of PDVSA and the accumulation of debt. So even that phase did not resolve the deeper institutional tensions.

The 2026 reform, then, does not emerge from nowhere. It is a new chapter of a long historical movement: from national jurisdiction, to nationalization, to cessionary governance, to the oil opening, to partial reassertion, to crisis and collapse, and now to a new form of contractualization from a position of weakness. Venezuela’s oil history has been a struggle not simply over who owns the oil, but over who governs the terms on which ownership is exercised. The present reform is the latest chapter in that struggle, but it is a particularly radical one because it comes after institutional erosion and under a global order that is far more contractual, litigious, and externally structured than the one Venezuela faced in the mid-twentieth century.

Chevron, Eni, Repsol, and Shell are among the corporations to have struck contracts under the new and improved conditions. (Venezuelanalysis)

Oil in the present geopolitical battle

The current geopolitical context of the US-Israeli aggression against Iran should, in principle, strengthen Venezuela’s bargaining position. When West Asia becomes more unstable, supply security rises as a strategic concern, and oil regains immediate geopolitical urgency, countries with large reserves and an established production history become more valuable.

Venezuela has occupied that position before. Venezuelan oil played an important strategic role for the Allies during the Second World War, for example. Today, renewed disruption around Iran and the Strait of Hormuz has again tightened the market and raised the geopolitical value of accessible barrels.

That is precisely why the current outcome appears so paradoxical. If global conditions improve Venezuela’s leverage, one would expect the country to negotiate from a stronger position and to demand a larger participation. One would expect a legal framework that captures more rent, not less; that uses geopolitical scarcity to reinforce state take, not to dilute it. But the current reform, alongside the sequence of deals with foreign conglomerates, and combined with US control over revenues, seem to move in the opposite direction.

This leads to the second point: the geopolitical issue is not only price or supply. It is also about control. What is emerging is a form of sovereignty under tutelage. Venezuela may formally remain the owner of the resource, but effective control over commercialization, revenue channels, and external validation appears increasingly conditioned from outside. Whether one calls that tutelage, external supervision, or subordinated reintegration, the takeaway is the same: sovereignty over the resource is no longer identical to sovereignty over the business. Recent US licenses illustrate the point very clearly. Washington has opened the door to renewed oil transactions with PDVSA, but under Treasury oversight and with proceeds channelled into US-administered accounts. That is not normal sovereign control over national oil income.

This is where the distinction between the origin and the destination of rent becomes especially useful. Even before we ask what is done with oil income socially or politically, we first need to know how that income is generated: through what pricing, what discounts, what fiscal structure, and through which payment channels. If that first level is opaque, then both the origin and the destination of rent become politically indeterminate. In other words, the problem is not only that the country may receive less revenue. The problem is that the country may not even be able to clearly verify what it is owed, how, and why. That is a much deeper sovereignty problem.

As a result, a geopolitical context that would, in theory, favor Venezuela, sees the country re-entering global markets with weakened sovereignty, under a framework of greater flexibility for operators and less certainty for the nation. That is why the debate is no longer only about production volumes or export flows. The real debate is about the jurisdictional and political order that now governs Venezuelan oil: who authorizes, who commercializes, who arbitrates disputes, who tracks the proceeds, and who answers to the country.

Blas Regnault was a guest on the Venezuelanalysis Podcast.

What does a sovereign recovery look like?

Moving from critique to programme is difficult, and the first honest thing to say is that no one can predict the exact path ahead. Venezuela is emerging from collapse, sanctions, loss of market share, institutional erosion, and a deep social crisis. Any recovery scenario, therefore, is bound to be politically fraught. But one thing is clear: if the country does not rebuild the public intelligibility of oil income, then any so-called recovery may simply reproduce opacity, distrust, inequality, and social tension.

A sovereign recovery does not mean autarky. It does not mean excluding foreign firms, nor does it mean mechanically returning to an earlier model. It means something more precise: restoring the link between ownership, public rule, and accountable income capture. In other words, if the nation owns the resource, then the nation must be able to know, verify, and govern how value is extracted from it. That means transparency over net prices, discounts, taxes, royalties, exemptions, payment channels, and the destination of funds. Without that, there can be no recovery in any meaningful sovereign sense. It would simply be resumed extraction.

A sovereign recovery also requires stripping away some of the ideological confusion that usually surrounds debates on natural resources. As Bernard Mommer argued more than twenty years ago, the governance of natural resources is, in many ways, a more elementary question than the conventional left-right divide suggests. In the case of oil and minerals, the deeper divide is above versus below. It is the tension between those who live and work on the surface (the nation, society, the public realm) and those who make their living from the subsoil.

That is why the question of ownership comes before the question of distribution, that is, before the question of what is done with the income generated by oil activity. Only after establishing the governance over the resource and the rules over its extraction does the familiar left-right question properly arise: how that income is used, whether for social spending, public services, etc., or private accumulation.

The first step, then, is transparency. Not as a slogan, but as an institutional obligation. Who is selling? At what net price? Under what discounts? With what deductions? Paid where? Audited by whom? These are not minor administrative questions. They are the very mechanics of sovereignty in an extractive economy. If the country cannot answer them, then the state is no longer exercising full command over its principal source of income.

The second step is to move away from excessive discretion and back towards intelligible general rules. Contracts will always matter in oil. But there is a difference between contracts operating within a strong public framework and contracts effectively replacing public rule. Once everything becomes negotiable in the name of investment or “economic equilibrium,” the public realm shrinks and the executive realm expands. That is politically dangerous in any country, but especially in one where oil historically underpinned a broader social pact.

The third step is to reconnect oil income with social legitimacy. This is not an abstract issue. It is whether oil wealth translates to salaries, living standards, public services, social protection, and some minimum sense of collective benefit. If the country enters a new extractive cycle in which more oil is produced but public income remains narrow, opaque, or externally conditioned, then social tensions are likely to intensify rather than diminish. That is why a sovereign recovery cannot be measured by production figures alone. It must be judged by whether the nation regains an intelligible and legitimate claim over the income stream.

In simple terms, the average Venezuelan citizen is aware of fluctuations in crude prices because they know they affect the national budget. Oil income is widely and legitimately perceived as income belonging to the nation, and therefore as something that ought to support public services and collective welfare. Even when that income is later misused (through corruption, clientelism, or mismanagement) the underlying perception remains: oil revenue belongs to all Venezuelans.

That is also why the current situation can be described as one of sovereignty under tutelage. The country may still be sovereign in formal terms, yet it operates under external supervision in practical terms. Unless that gap is closed, the language of recovery will remain politically fragile.

Blas Regnault is an oil market analyst and researcher based in The Hague, whose work explores how oil prices move across time and what they tell us about the global economy. Drawing on years of experience in central banking, energy research, and international consulting, he brings together political economy, business cycles, production costs, and petroleum governance in a way that is both rigorous and accessible.

He has spent much of his career studying the deeper forces behind oil price trends and fluctuations, always with an eye on the institutional and geopolitical realities of the global petroleum market. Later this year, he will publish his book, Political Economy of Oil Prices: Trends and Business Cycles in the Global Petroleum Market, with Routledge.

The views expressed in this article are the author’s own and do not necessarily reflect those of the Venezuelanalysis editorial staff.

Crude prices were slightly lower ahead of European markets opening as traders digested comments from US President Donald Trump that Washington would help ships leave the Strait of Hormuz from today. Iran, however, has rejected the plan.

ADVERTISEMENT

ADVERTISEMENT

At the time of writing, the price of a barrel of US benchmark crude (WTI) was down 0.28% to $101.65 a barrel, while Brent crude, the international standard, edged down 0.06% to $108.10 a barrel.

Much hinges now on progress towards ending the war with Iran and unlocking the bottleneck through the Strait of Hormuz.

The oil market “remains the fulcrum, with hundreds of tankers, bulk carriers, and cargo ships still stranded across the Gulf, idling as storage constraints force producers to shut … production simply because there is nowhere left to store it,” Stephen Innes of SPI Asset Management said in a commentary note.

Trump said what he called “Project Freedom” would begin Monday morning in the Middle East. The US Central Command said it would involve guided-missile destroyers, more than 100 aircraft and 15,000 service members, but the Pentagon did not immediately answer questions about how they would be deployed.

Asia-Pacific and US markets

In Asian share trading overnight, Hong Kong’s Hang Seng jumped 1.4% to 26,135.47. Markets in mainland China and Japan were closed for “Golden Week” holidays. In Australia, the S&P/ASX 200 slipped 0.3% to 8,704.70.

Strong buying of tech stocks pushed shares in South Korea sharply higher, as the Kospi gained 3.8%. Taiwan’s Taiex surged 4.2%.

On Friday, the S&P 500 climbed 0.3% to another all-time high of 7,230.12, closing out a fifth straight winning week. The Dow Jones Industrial Average dipped 0.3% to 49,499.27, and the Nasdaq composite added 0.9% to a record close of 25,114.44.

Apple led the way after delivering better profit than expected. Because it’s one of Wall Street’s biggest stocks in terms of overall size, its rally of 3.3% was by far the strongest force lifting the S&P 500.

Stock prices generally follow the path of corporate profits over the long term, and US companies have been exceeding expectations for earnings in the first three months of 2026. That’s even with the war with Iran and high oil prices souring confidence for many US households.

Strong earnings boost S&P 500

A little more than a quarter of the companies in the S&P 500 have reported already, and 84% of them have topped analysts’ estimates, according to FactSet. The index is on track to deliver roughly 15% growth in profit from a year earlier.

The main uncertainty for the global economy is where oil prices are heading because of the Iran war. Oil prices moved higher last week on worries that the war might keep the Strait of Hormuz closed for a long time, trapping oil tankers pent up in the Persian Gulf instead of delivering crude to customers worldwide.

Brent was selling for a little more than $70 per barrel before the war began, and soaring prices helped the two biggest U.S. oil companies report stronger profit for the latest quarter than analysts expected. But stock prices nevertheless fell for both Exxon Mobil, 1%, and Chevron, 1.4%, as oil prices regressed Friday and each reported drops in net income from a year earlier.

In other dealings early Monday, the dollar rose to 157.18 Japanese yen from 156.80 yen. The euro fell to $1.1724 from $1.1746.

May 3 (UPI) — Oil exports from the United States have increased by more than 30% the U.S.-Israeli war in Iran started and the Strait of Hormuz was blockaded in response.

The Port of Corpus Christie has overtaken the ports in Saudi Arabia and Iraq in the last few weeks as the two Persian Gulf ports have been cut off from the rest of the world since the Strait has been blockaded.

Over the past two months, the United States has sold more than 250 million barrels of oil to foreign buyers as exports have increased by 30%, from 3.9 million barrels per day in February to 5.2 million barrels per day in April, Bloomberg and CNBC reported.

Experts have warned, however, that domestic oil inventories are depleting stockpiles and there is a question of how long the country will be able to continue replacing oil on the market that is stuck in the Strait.

Although selling oil is good for business, oil producers are struggling to keep up with the demand and it is possible that selling so much could have an add-on effect of pushing gas prices for American consumers even higher than they have gone since the war started.

“Ships are coming to take our oil, but once significant volumes of are leaving the United States, it can be expected that balances will tighten,” Clayton Seigle, senior fellow at the Center for Strategic and International Studies, told Bloomberg.

“We are digging ourselves a hole in terms of spending down inventories,” he said.

Roughly 20% of global oil supplies pass through the Strait of Hormuz and Iran’s shutting of it has caused gas and fuel prices to skyrocket over the last two months, including massive effects on the airline industry, which has seen seen the price of jet fuel double since before the war.

Oil from the United States, Latin America and West Africa could for a short time be a substitute for Middle Eastern oil for countries in Asia, which has been hurt the most, but it is not ideal, Matt Smith, director of commodity research at Kpler, told CNBC.

“Asian markets are buying whatever they can get their hands on, so they’re taking a lot of light sweet [American] crude [oil],” Smith said, but their refineries are optimized for the heavier oil produced in the Middle East.

“It’a hole that can’t be plugged,” Smith told CNBC. “The answer has to be ensuring secure supply from the Middle East.”