British oil giant BP announced plans Friday to sell off its North Sea business ending six decades of exploration and extraction on the U.K. Continental Shelf since the company first struck gas there in 1964. File photo by Neil Hall/EPA

July 31 (UPI) — British oil giant BP announced plans Friday to sell off its North Sea business, ending six decades of exploration and extraction in the U.K. Continental Shelf since the company first struck gas there in 1964.

The firm said that nothing would change for the time being while a buyer was found, vowing in a news release that it was fully committed to continuing to run its operations, prioritizing safety and dependability, while delivering for its customers, partners and investors.

The outcome of a review of its portfolio, BP said the goal was to enhance the value of the company by making it simpler and stronger through adhering to its approach of allocating capital in a rigorous fashion.

“The North Sea remains integral to the U.K.’s energy system. However, as we focus our portfolio and direct capital to our highest-value opportunities, we believe our North Sea business will be better positioned as part of another company. It has world-class people, resilient assets and a proud heritage, and it is precisely these qualities that can attract an owner ready to back its next chapter,” said BP.

“We are seeking an outcome that recognizes that value.”

CEO Meg O’Neill stressed that Britain would remain of key importance to the company going forward, saying BP was proud of the employment it generated, its input to the economy and its role in keeping energy flowing every day.

As recently as May, O’Neill described the North Sea basin as one of “untapped potential.”

The share price gained slightly on the news, rising a little more than 1% to $7.36 in mid afternoon trade on the London Stock Exchange on Friday.

BP has 24 fields across five main nodes in the North Sea, including its key Clair Ridge and Schielhallion fields of the Shetland Islands, with 1,100 workers pumping a little under 100,000 barrels of gas and oil daily.

Energy consultant Rystad, which estimates the North Sea business was worth $2.6 billion, told the Financial Times that it believed that the TotalEnergies-HitecVision-Repsol joint venture Neo Next +, Delek Group of Israel or Eni of Italy were in the running to buy it.

While the United States enjoys sufficient energy resources, thanks to shale oil, the European Union does not. To assure itself of the energy supplies in the Gulf that the European Union needs, the EU should consider assisting the Gulf States in the construction and operations of the pipeline.

Building a large-scale, completely underground oil pipeline system from the Persian/Arabian Gulf oil fields to the Mediterranean Sea is estimated to cost between $40 billion and $60 billion and would take 5 to 7 years to complete. The exact metrics depend heavily on the chosen route, political alignment across transit countries, and the required total throughput capacity.

Breakdown of Total Costs

Modern mega-pipeline engineering over long desert and mountain distances faces massive cost drivers:

Stay ahead of the geopolitical week.

MD Briefing delivers expert analysis across five global fronts — the Indo-Pacific, energy, geoeconomics, European security, and the Middle East — every Monday morning. Free.

· Construction & Trenching ($18B – $25B): Burying multiple large-diameter (e.g., 42 to 48-inch) pipelines entirely underground requires extensive trenching, rock blasting, and specialized anti-corrosion coatings. Global benchmarks show that large-scale overland pipelines average $8 million to $12 million per mile, but full underground burial heavily drives up labor and machinery costs.

· Pumping Stations & Terminals ($8B – $12B): Moving millions of barrels of crude daily across hundreds of miles requires heavily fortified pumping stations every 60–100 miles, alongside massive new storage and loading terminals on the Mediterranean coast.

· Geopolitical & Geotechnical Risk Premium ($7B – $10B): Multi-billion dollar contingencies are standard to absorb project snags, material inflation, and complex international legal/right-of-way frameworks.

· Security Infrastructure ($5B – $10B): Given the vulnerability of cross-border energy corridors, modern estimates for Gulf bypass networks integrate specialized defensive technologies (like automated drone surveillance or surface-to-air missile defenses) to protect critical facilities.

Construction Timeline and Stages

· Megaprojects of this length are restricted by a sequential project lifecycle that cannot easily be accelerated simultaneously:

· Diplomacy & Right-of-Way (Years 1–2): Securing cross-border transit legal treaties (e.g., routing through Saudi Arabia, Jordan, Israel, or Syria/Turkey) and finalizing environmental impact assessments.

· Material Procurement & Logistics (Years 2–3): Manufacturing and transporting millions of tons of high-grade steel line pipe and heavy industrial pumps.

· Civil Trenching & Laying (Years 3–6): Heavy execution phase. Crews can typically lay roughly 1 to 2 miles of pipe per day per construction spread.

Multiple spreads working simultaneously across different geographic zones are required to finish within a 3-to-4-year active construction window. · Testing & Commissioning (Year 7): Hydrostatic pressure testing of the lines to ensure underground integrity, followed by line fill and gradual commercial scale-up

Proposed Alternative Routes

Producers in the region actively advance or evaluate different variants of this corridor to bypass maritime chokepoints like the Strait of Hormuz:

· The Mesopotamian Corridor (Iraq/Syria route): A ~1,500 km route linking the southern oil fields of Basra to Mediterranean ports like Baniyas, Syria. While geographically direct, it remains vulnerable to high regional instability.

· The Trans-Arabian Upgrades: Adapting or running parallel lines to existing corridors (like the Saudi East-West Petroline, which travels 1,200 km to the Red Sea) and extending them northward to Mediterranean Sea terminals.

How Standard Micro-Tunneling Works for Utilities: When pipeline engineers hit a mountain or an environmental zone where they cannot dig an open trench, they use Micro-Tunnel Boring Machines (MTBMs) or Horizontal Directional Drilling (HDD). These systems are highly specialized to avoid the exact problems of passenger-sized tunnels:

· Sized to the Pipe: Unlike a 12-foot-wide transit tunnel, an MTBM is built to the exact outer diameter of the oil pipe (typically 4 to 5 feet for a 48-inch line). This means crews excavate 90% less rock and dirt.

· Pipe-Jacking Method: Instead of laying concrete tunnel walls and then trying to slide a heavy steel pipe inside later, MTBMs use a process called “pipe jacking.” Powerful hydraulic rams at the surface push the actual steel oil pipe directly behind the drilling head as it advances into the rock.

· No Open Voids: Because the pipeline fits perfectly into the drilled hole, there is no empty space left around it. The pipe is completely surrounded by solid rock or stabilizing grout, eliminating the risk of dangerous, explosive gas pockets building up in an open tunnel.

The Mountain Ranges the Route Must Clear

· To get from the Gulf fields (like Ghawar in Saudi Arabia or Basra in Iraq) to the Mediterranean, a pipeline must breach the Syrian Desert and cross a series of rugged, geologically active mountain walls running parallel to the Mediterranean coast:

· The Jordan Rift Valley & Dead Sea Fault: Before hitting the mountains, the pipeline must drop down into one of the lowest, most seismically active valleys on Earth (falling hundreds of feet below sea level) and then immediately climb back out.

· The Judean Hills & Golan Heights: Depending on the exact coastal terminal, the line must climb over rugged limestone ridges ranging from 3,000 to 4,000 feet high.

· The Anti-Lebanon & Mount Lebanon Ranges: If the route takes a more northern path toward Syria or Lebanon, it faces severe alpine conditions with peaks soaring between 9,000 and 10,000 feet.

The Geopolitical Treaties Required

Building a multi-billion dollar piece of energy infrastructure across national borders requires an intricate web of international legal frameworks. Historically, cross-border pipelines are governed by Host Government Agreements (HGAs) and Intergovernmental Agreements (IGAs).

To make a Gulf-to-Mediterranean pipeline a reality, several unprecedented breakthroughs would be needed:

· Transit Fees and Tariffs: The countries hosting the pipeline but not producing the oil (like Jordan or Syria) must negotiate “transit fees.” These are typically paid in cents per barrel of oil that passes through their territory, providing them with billions in long-term revenue.

To make a Gulf-to-Mediterranean pipeline a reality, several unprecedented breakthroughs would be needed:

· Transit Fees and Tariffs: The countries hosting the pipeline but not producing the oil (like Jordan or Syria) must negotiate “transit fees.” These are typically paid in cents per barrel of oil that passes through their territory, providing them with billions in long-term revenue.

· The “Right of Way” Guarantee: Sovereign nations must sign legally binding treaties promising that they will not shut off or seize the pipeline during diplomatic disputes. A famous historical warning is the original Trans-Arabian Pipeline (Tapline), which was repeatedly disrupted, sabotaged, and eventually shut down permanently due to border conflicts and transit fee arguments between Saudi Arabia, Jordan, Syria, and Lebanon.

· The Abraham Accords Framework: If the pipeline takes the most geologically direct southern route to terminals in Israel (like Ashkelon or Haifa), it relies heavily on the long-term stability and expansion of the Abraham Accords. Saudi Arabia and Israel would need formalized economic treaties to protect a joint energy corridor from regional political shifts.

· Joint Security Commands: Because a pipeline stretching thousands of miles across the Middle East is a prime target for non-state actors and drone strikes, treaties must establish a unified security framework. This allows military and intelligence sharing across borders to patrol the pipeline corridor with automated drone networks and satellite monitoring.

Environmental Safeguards for Freshwater Aquifers The Jordan Valley and the surrounding mountain ridges contain critical freshwater sources, such as the Mountain Aquifer, which supply drinking water to millions of people in Israel, Palestine, and Jordan. A single major crude oil leak could seep into the porous limestone and permanently poison these non-renewable water reserves. To mitigate this, engineers deploy an array of specialized defenses:

· Pipe-in-Pipe Technology (Double Containment): In high-consequence water zones, crews do not use a standard single-wall pipe. They build a “pipe-in-pipe” system where the main 48-inch crude oil line sits inside a larger, secondary outer steel casing. The vacuum gap between the two pipes is monitored 24/7 for pressure changes; if the inner pipe leaks, the outer pipe captures the oil before it touches the soil.

· Fiber-Optic Acoustic Leak Detection: Continuous fiber-optic cables are buried directly alongside the pipeline. These cables can “hear” the micro-acoustic vibrations and sudden temperature drops caused by a pinhole leak. This allows operators to pinpoint the exact location of a breach within meters in less than a minute.

· Emergency Remote Isolation Valves: The pipeline is segmented by heavy-duty, automated shut-off valves. In flat areas, these are placed every 20 miles. In critical aquifer zones or steep mountain drops, they are placed every 1 to 2 miles. If the control center detects a pressure drop, these valves slam shut automatically via satellite command to trap the oil inside a small, isolated section, preventing millions of gallons from draining into the environment.

Daily Revenue for Transit Countries

· Transit countries like Jordan or Syria do not own the oil, but they make massive profits simply by letting it cross their land. These fees are negotiated as a tariff—a fixed dollar amount charged per barrel of oil moved.

· Assuming a modern mega-pipeline with a capacity of 2 million barrels per day (bpd) and a standard international transit tariff of $0.60 to $1.20 per barrel, we can calculate the massive financial impact on a host country’s budget:

DAILY TRANSIT REVENUE ESTIMATE │

Pipeline Throughput Capacity │ 2,000,000 Barrels / Day

Average transit tariff rate: $0.90 USD per barrel

Daily Revenue Generated │ $1,800,000 USD / Day

Annual Revenue Generated │ $657,000,000 USD / Year

The Broader Economic Impact

· Direct Budget Injection: For a developing economy like Jordan, an extra $650M+ per year in pure cash represents a massive boost to their national budget, easily funding large-scale public infrastructure or health programs.

· In-Kind Energy Off-Takes: Rather than taking 100% of the payment in cash, transit treaties often allow host countries to take a portion of the payment in free crude oil. This allows them to supply their local refineries and secure cheap domestic gasoline without relying on volatile global energy imports.

· Long-Term Economic Leverage: Hosting the pipeline transforms these non-producing nations into critical gatekeepers for global energy markets, giving them significant diplomatic leverage when negotiating trade and security deals with major global superpowers.

Maritime Shipping Insurance & The Strait of Hormuz Bypass The Strait of Hormuz is the world’s most sensitive maritime energy chokepoint. During periods of regional conflict, Lloyd’s of London and global marine underwriters designate

the Persian Gulf as a listed area (high-risk zone), triggering drastic shifts in shipping economics.

· War Risk Premiums: When regional tensions spike, war risk insurance premiums for oil tankers navigating the Strait can surge from a baseline of 0.025% of the ship’s value to over 0.25% to 0.5% per voyage. For a modern $100 million Very Large Crude Carrier (VLCC), this adds an extra $250,000 to $500,000 in insurance costs for a single transit.

· Bypassing the Chokepoint: Moving oil via the underground pipeline directly to the Mediterranean entirely eliminates the need for tankers to enter the Persian Gulf. Tankers load at secure Mediterranean ports (like Ashkelon, Haifa, or Baniyas) within standard, lower-risk European maritime zones.

· Shipping Time Savings: Loading in the Mediterranean slashes the sailing distance to European and North American refineries by roughly 3,500 to 4,500 miles compared to sailing all the way around Africa or paying steep transit fees to use the Suez Canal. This reduces freight operating costs and completely erases the risk of a regional conflict stranding a fleet inside the Gulf.

Naval Defense Infrastructure at the Mediterranean Terminal

Because the new Mediterranean pipeline terminal would handle up to 2 million barrels of oil per day, it becomes a high-value strategic asset. Protecting it requires a multi-layered naval defense perimeter extending miles out to sea:

· Anti-Drone & Anti-Torpedo Netting: Heavy, underwater physical barriers and sensor nets are deployed around the loading buoys and piers to catch or detonate incoming unmanned underwater vehicles (UUVs) or loitering aquatic explosive drones.

· Phalanx CIWS & Missile Batteries: The onshore terminal facility integrates close-in weapon systems (CIWS) and surface-to-air missile batteries (like Iron Dome or Barak MX systems) to intercept incoming rocket, drone, or anti-ship missile strikes launched from sea or land.

· Active Naval Patrols: Host nations deploy continuous maritime security cordons using fast attack craft, sonar-equipped corvettes, and aerial reconnaissance drones to enforce a strict 5-to-10 mile exclusion zone around the offshore loading terminals, vetting every incoming commercial vessel.

Conclusions

With political tensions between the United States and the European Union increasing and confidence in the United States’ foreign policy falling, Europe needs to find and secure an energy source that is not dependent on either the United States or Russia. An agreement, both economic and political, would in the long run make Europe independent from energy sources from either country. The idea of an overland pipeline to the Mediterranean is both economically and engineeringly possible. What is needed is the political will to make it happen.

The Houthis recently declared a naval blockade on Saudi Arabia in the Red Sea, targeting several tankers.

Published On 28 Jul 202628 Jul 2026

Yemen’s Iran-aligned Houthi group says it has fired ballistic missiles at a Saudi oil tanker, more than a week after imposing a naval blockade on Saudi vessels in the Red Sea.

In a post on X, Yahya Saree, the Houthi military spokesman, said the group had “carried out a military operation targeting the Saudi oil tanker (NCC GHAZAL) for violating the maritime navigation ban” that the group had imposed on Saudi vessels.

He added that the group had used several ballistic missiles and forced the vessel to retreat.

The UK Maritime Trade Operations (UKMTO), a maritime security monitor, said a tanker reported an explosion while transiting the Red Sea, adding that the crew is safe and no environmental damage was reported.

The Houthis seized the capital Sanaa in 2014 and have fought the internationally recognised Yemeni government, which Saudi Arabia backs, for more than a decade.

On July 20, the Houthis announced their maritime blockade, accusing Saudi leaders of imposing “an unjust and oppressive siege” on Yemen for nearly 12 years, “plundering our resources and imposing a comprehensive blockade”.

It went on to affirm “the right of our great people to respond to the blockade with a blockade”.

“We targeted two Saudi oil tankers, named Encelia and Layla, for their violation of the blockade decision issued by the armed forces,” Houthi military spokesperson Yahya Saree said on July 22.

The Saudi Press Agency reported that the Encelia had been hit, citing an official source at Saudi Arabia’s Transport General Authority who said all crew members were safe.

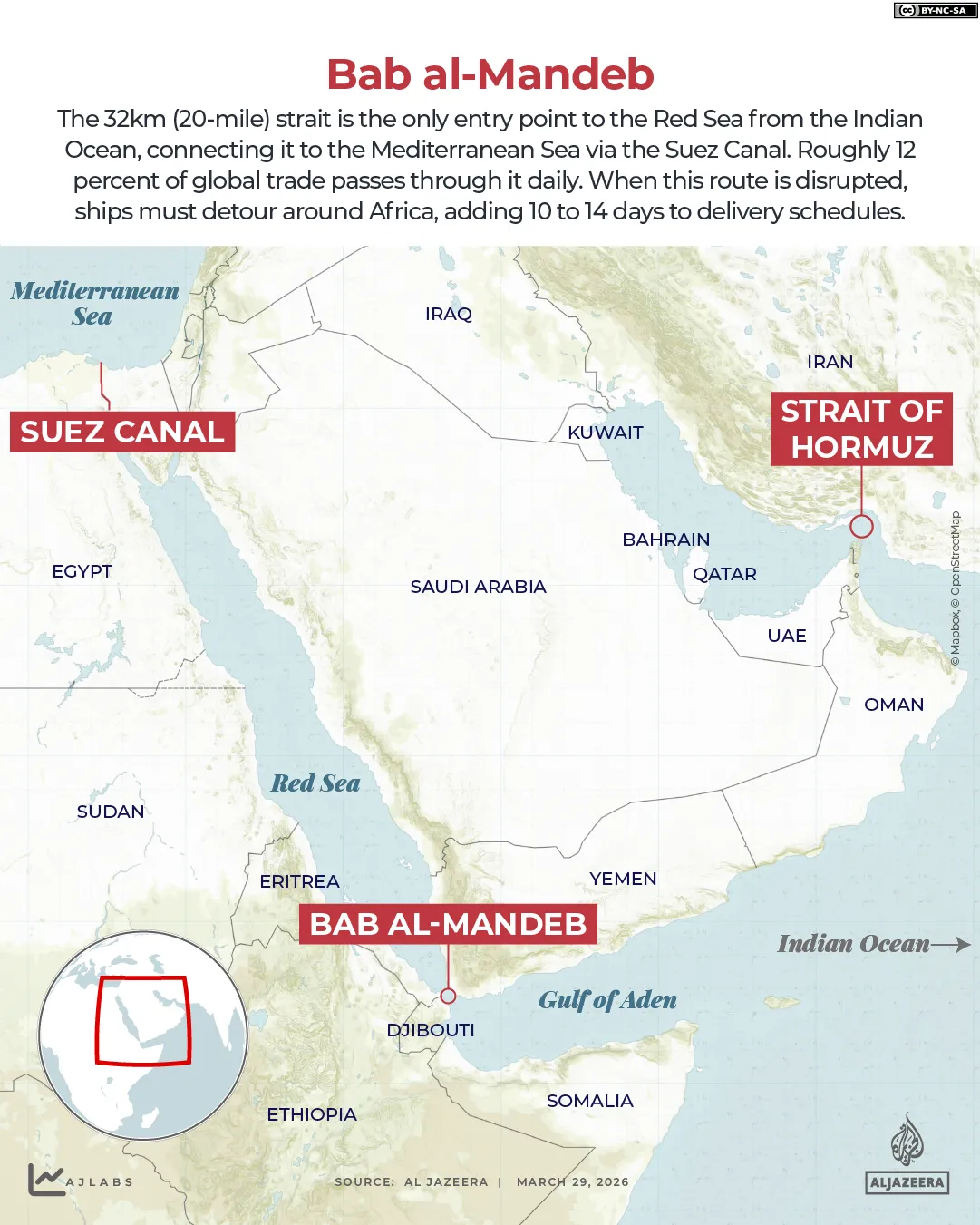

The Bab al-Mandeb chokepoint connecting the Red Sea to the Gulf of Aden is one of the world’s most important shipping routes, including for oil exports.

Between Yemen to the northeast and Djibouti and Eritrea in the Horn of Africa to the southwest, the strait is just 29km (18 miles) at its narrowest point, limiting traffic to two channels for inbound and outbound vessels heading to the Suez Canal.

In 2024, about 4.1 billion barrels of crude oil and refined petroleum products passed through the strait – about 5 percent of the global total.

Bond investors are increasingly betting that the Federal Reserve could raise interest rates this week after higher oil prices and renewed inflation concerns pushed Treasury yields to multi-month highs, Bloomberg News reported Sunday.

Tehran-backed Houthi forces in Yemen have fired missiles and drones at two of Saudi Arabia’s most strategically important oil facilities on the Red Sea, in a major escalation of the latest simmering regional conflict to be reignited by the war launched by the United States and Israel against Iran.

But the skies over the country at the epicentre of the widening war were quiet for a second successive night, with no new US attacks on Iran reported by Sunday morning.

Recommended Stories

list of 3 itemsend of list

Iran had been pounded by 13 consecutive waves of overnight US air strikes since July 11, after the Islamic Revolutionary Guard Corps (IRGC) attacked tankers trying to transit the Strait of Hormuz. As hostilities escalated, both sides declared that an interim peace agreement signed in June was dead, and a second phase of talks to finalise a comprehensive peace deal appeared doomed.

But there have been no US air strikes since Friday, and tentative signs are emerging that Washington and Tehran are still talking via mediators and might return to more meaningful discussions.

Even if another fragile truce is agreed, however, the cascade of consequences unleashed by the war is still stoking conflict and confrontation elsewhere.

Iran’s attacks on shipping in the Strait of Hormuz have put a stranglehold on exports of oil and raw materials for fertiliser, sending energy prices soaring and raising the risk of a food security crisis in some of the world’s most vulnerable countries.

In March, in response to attacks on Iran, the Tehran-backed Hezbollah movement in Lebanon resumed missile attacks on Israel, which then launched a devastating invasion of southern Lebanon that has displaced 1.2 million people.

Now, another smouldering regional conflict has erupted again, between US-allied Saudi Arabia and the Houthi movement which controls most of northern and western Yemen, including the capital, Sanaa. Saudi Arabia and its regional allies joined a brutal civil war against the Houthis in 2015, until a truce was agreed in 2022.

Risk of global crisis

The truce collapsed this month after an attack on Sanaa airport to stop an Iranian plane landing provoked the Houthis to fire ballistic missiles at Saudi Arabia. Last Monday, the Houthis declared a naval blockade of Saudi Arabia, and late on Friday the Saudis launched air strikes on the Houthi-held city of Hodeidah.

In retaliation, Houthi forces launched Sunday’s attacks on facilities belonging to Saudi state oil giant Aramco in the coastal cities of Jizan and Yanbu, Houthi military spokesman Yahya Saree said.

There has been no comment from Saudi Arabia on the extent of any damage to Aramco’s refinery in Jizan, but a large column of smoke was seen rising after the attack.

In Yanbu, Saudi Arabia’s principal west coast export gateway, two ballistic missiles aimed at oil installations were intercepted by a Patriot battery operated in Saudi Arabia by the Greek military under an agreement with Riyadh.

The escalating conflict has raised fears that the Houthis could block the Bab al-Mandeb Strait, which connects the Red Sea to the Gulf of Aden. If both the Bab al-Mandeb and Hormuz straits were blocked, the resulting supply chain crisis would cause major economic damage across the world.

Entangled wars

Besides spreading to the Red Sea, the US-Iran war has become entangled with the deadliest active conflict in the world – Russia’s attempted conquest of Ukraine.

A long-range strike on an Iranian vessel in the Caspian Sea on Saturday caused an explosion that killed one sailor and wounded another, according to Iran’s Ministry of Foreign Affairs, which blamed the attack on Ukraine and summoned Kyiv’s charge d’affaires in Tehran to convey its condemnation of the “hostile and criminal” act.

Ukrainian President Volodymyr Zelenskyy said in a post on X that Kyiv had achieved “very strong results” with long-range strikes in the Caspian Sea, hitting “vessels used in military cargo shipments involving Iran, as well as a warship”.

Zelenskyy claimed in further comments on X on Saturday that since the start of July, Kyiv had detected “active Russian satellite surveillance of the Gulf states and US military facilities located there”. He said the satellite images were passed to Tehran to help the IRGC identify targets for ballistic missile and drone attacks.

US President Donald Trump has not given a reason for the sudden cessation in air strikes on Iran, but a senior administration official told the Reuters news agency that Trump “has always been clear that his preference is diplomacy, but he has shown Iran what will happen if they fail to come to the table in a serious way”.

Trump said on Friday that there was still some communication with Iran.

“They are talking to us right now; they’d love to make a deal,” he said. “I don’t think they’re ready to … but I’m willing to listen.”

Al Jazeera’s Resul Serdar, reporting from Tehran, said Iranian officials had confirmed the two sides were exchanging messages.

“There have been proposals conveyed by the mediators, and Tehran is still reviewing them,” Serdar said, adding there was “not much progress yet” due to “fundamental differences” in their positions and deep mistrust.

Yemen’s Houthis say they have targeted oil facilities in Saudi Arabia owned by Aramco, in the latest escalation between the two sides. Saudi authorities say they intercepted the missile and drone attacks. Yousef Mowry has more details from Sanaa.

Houthis attacked two oil depots along the Red Sea on Saturday belonging to oil giant Saudi Aramco (ARMCO) as the US held off on bombing sites in Iran on Friday night, the first time in two weeks that has happened.

Houthi blockade for now is shaping who moves Saudi crude, not whether it moves, analysts say, even as oil prices soar.

As oil prices hit $100 a barrel on Thursday, experts say they are watching to see which vessels Yemen’s Houthis allow to pass through in the Red Sea as that will indicate how the crude market trends.

Brent futures rose $6.58 or 6.96 percent, to $100.65 a barrel, exceeding $100 for the first time since late May.

Recommended Stories

list of 4 itemsend of list

That was on the back of the Iran-aligned Houthis saying they were cutting off the passage Riyadh had been using to ship parts of its crude oil once Iran closed the Strait of Hormuz to retaliate against United States and Israel attacks.

On Monday, the Yemeni group declared a naval blockade on shipments from Saudi Arabia and said they would target Saudi, Israeli, and United States-linked tankers in the Bab el-Mandeb, which links the Red sea to the Indian Ocean.

On Thursday, the Houthis attacked two Saudi Arabian oil tankers, the group said, with a Saudi news agency later confirming that one of the two vessels was set ablaze.

It is not clear if the second one was also hit, according to marine analysis firm, Windward.

“The Houthis are quite mercurial and there is no complete clarity on what the blockade means,” said Michelle Bockmann, a senior maritime intelligence analyst at Windward.

“We’re watching now the ability of Chinese-owned tankers at [Saudi port] Yanbu if they are allowed to go through Bab el-Mandeb. Two have gone through but those had been loaded before the blockade was announced.”

The Houthis have previously relied on China for help, including for drone components, and “the Chinese have previously had a free pass”, said Bockmann, including between 2023 and 2025 when the Houthis attacked cargo ships aligned with Israel and the US in the Red Sea in the wake of the war on Gaza.

Windward tracking shows the cargo that moved through the Bab el-Mandeb chokepoint on July 20 was Saudi in origin but Chinese in crew and destination, and it drew no interdiction. The two vessels passed through the same corridor that Western- and Saudi-linked operators were being warned to avoid.

The enforcement is calibrated to affiliation rather than cargo and the blockade is shaping who moves Saudi crude, not whether it moves, Windward said.

“No one has ever been able to predict their actions… but they know you don’t have to do a lot to get the oil markets to react,” said Bockmann referring to the rise in benchmark oil prices on Thursday.

Rachel Ziemba, adjunct senior fellow at the Center for a New American Security, underscored that the standoff in Bab el-Mandeb is happening while crude buffers have nor been replenished after the peak of the Hormuz crisis earlier this year.

“The multiple chokepoints are new and an example of littoral states looking to use their leverage,” Ziemba said.

Diesel also impacted

For now, both the Houthi threats and the continued closure of the Strait of Hormuz through which nearly one-fifth of the world’s oil transited before the US-Israel war on Iran, has sent prices soaring, including at the pump in the US reaching the national average of $4.09 per gallon (3.4 liter).

“Today’s rise in oil prices could cause $0.10 to $0.20 rise over the next week or two per gallon average price in US,” said Patrick De Haan, head of petroleum analysis at GasBuddy.

But De Haan is looking beyond the two straits and says he’s watching the availability of diesel as price per gallon averages $5.34.

“Diesel prices are being impacted more significantly,” he told Al Jazeera.

One reason behind that is that Ukrainian drone attacks have taken offline some of Russia’s oil refineries. The shortages are being felt domestically leading to Russia banning diesel exports, De Haan said.

“Oil exports are one story, but supplies of diesel gasoline, jet fuel is another story,” he said.

Another unknown in the mix is the role of China which, historically has been a major importer but slashed those imports in the past few months, helping stabilise global prices as some pressure on demand eased.

“It’s been one of the reasons that oil prices haven’t gone up dramatically – that china slashed its imports, and no one predicted that,” De Haan said. “For now, we don’t know if china is using its own strategic reserves or if it will start import again.”

Between those geopolitical plays and the upcoming hurricane season in the US, there is “another wildcard ahead for global refining capacity” and prices, De Haan said.

The U.S. war with Iran escalated again Thursday as Iran-backed Houthis in Yemen attacked two Saudi Araian oil tankers in the Red Sea, causing global oil prices to surge amid fears of yet another vital energy corridor being choked off by the conflict.

The attacks came after the Trump administration threatened additional strikes on Iran’s nuclear infrastructure while pushing a new deal to help Saudi Arabia develop a nuclear energy program of its own. Also Thursday, four Republicans in the U.S. House joined Democrats in a vote to halt the American military campaign absent congressional approval. Senate Republicans blocked a similar measure.

The price of oil hit $100 a barrel for the first time since May, increasing the financial pressure on Americans at the gas pump and the political pressure on President Trump to end a war he promised would last weeks but has persisted for months. At least 18 U.S. service members have died in the war.

The Houthis, who control the populous northwest of Yemen, receive arms and training from Tehran but had remained largely on the sidelines since the U.S. and Israel launched the war. Their latest strikes complicate already fraught negotiations between the U.S. and Iran after the collapse of a ceasefire this month amid renewed hostilities in the Strait of Hormuz, the other major energy passageway choked by the conflict.

The Houthis had this week announced a naval blockade of Saudi ships in the Red Sea, which stretches along Saudi Arabia’s western flank. That blockade centered on the Bab al Mandeb strait, the only southbound route for Saudi tankers headed to Asian markets.

Tanker traffic has already been heavily diminished in the Persian Gulf along Saudi Arabia’s northeast flank and between it and Iran, because of Iran’s threats to vessels traveling through the Strait of Hormuz. Saudi Arabia had diverted its oil exports to its Red Sea ports and out the Bab al Mandeb, dispatching some 4.5 million barrels via that route per day.

In a social media post Thursday, Trump said that if the Houthis continue attacking ships in the Red Sea, the U.S. “will hold Iran responsible” because the Houthis are an Iranian proxy, and inflict “major military punishment” on the Houthis and Iran.

He said he was “very disappointed” in the Houthis, “in that they have, until now, acted very professionally and smart” amid the Iran war.

At a later event Thursday, Trump said the U.S. is “doing extremely well” against Iran, which he accused of having “evil intentions.”

Democrats in the House and Senate cited the war’s spread to the Red Sea as yet another reason that Congress should act to pass a war powers measure to halt the president’s military campaign. Sen. Chris Van Hollen (D-Md.), who led the unsuccessful effort in the Senate, cited the expansion while recalling how Trump had claimed victory in Iran as far back as March.

“If we won back in March, why are more Americans getting killed in July? If we won back in March, why is the Strait of Hormuz closed? If we won back in March, why is the war expanding as Houthis attack ships transiting the Bab al Mandeb strait in the Red Sea? If we won back in March, why are oil and gas prices and diesel prices shooting through the roof again, imposing costs on every American family?” Van Hollen said. “Is that their definition of winning?”

The Houthis’ military spokesman, Yahya al-Sarea, said the group’s forces conducted “a qualitative military operation” targeting two Saudi oil tankers with missiles and drones for what he said were violations of the Houthis’ blockade on the Red Sea.

The Houthis have accused Saudi Arabia of imposing a blockade on airports and seaports in northwestern Yemen, where most of the country’s population lives and which the Houthis otherwise control. They also blamed Saudi Arabia for an attack this month on Sanaa’s airport to prevent the landing of a plane carrying a Houthi delegation returning from the funeral of Iranian Supreme Leader Ali Khamenei, who was killed at the start of the war.

Al-Sarea said that in addition to striking the two tankers, the Houthis forced 10 other ships to turn back from their passage, will “continue their naval operations against the Saudi enemy” and will “continue imposing the equation of blockade against blockade.”

The escalation of the war — and the shock wave it sent through global energy markets — added to regional uncertainty already being stoked by the Trump administration’s announcement Wednesday that it had agreed to work with Saudi Arabia to develop a civilian nuclear program.

That announcement, after years of U.S. attempts to block nuclear proliferation in the Middle East, sparked widespread concern in Washington, where lawmakers will vote on the deal, and in Israel, which has long feared a nuclear arms race in the region.

Trump administration officials said the deal would “uphold the highest standards of nuclear safety and nonproliferation,” with American firms developing the program. But they provided few details, and questions immediately arose about the absence of clear inspection protocols or any requirement that Saudi Arabia first normalize diplomatic relations with Israel.

On Thursday, Trump said the deal would be conditioned on Saudi Arabia joining the Abraham Accords and establishing diplomatic ties with Israel. White House Press Secretary Karoline Leavitt later said that Trump had not talked to Saudi leaders since making that condition public, but that they would have to agree to it or “the deal is off.”

Leavitt said that Trump had raised the matter with Saudi leaders in the past, and that it is something Trump “feels very strongly about.”

Asked whether Israel pressured the president to impose the condition, Leavitt said, “Not to my knowledge.”

Earlier this week, Defense Secretary Pete Hegseth told Congress that the Iran war has already cost the U.S. $37.5 billion. House Republicans on Wednesday pushed through a $1.15-trillion defense policy bill to fund the war moving forward. Most Democrats voted against the measure in protest of the war, and it faces stiff opposition in the Senate.

Trump in recent days has tried to deny polls showing plummeting support for the war among Americans. On Wednesday, before attending the dignified transfer of the bodies of U.S. service members killed in the war to Dover Air Force Base in Delaware, Trump claimed Americans don’t want high gas prices but “aren’t against the war.”

On Tuesday, Trump posted statistics showing that more U.S. service members died in past wars, which Democrats denounced as disrespectful to those killed in the current conflict.

The Houthis seized control of the Yemeni capital in 2014, along with much of Yemen’s populous northwest. Their advance triggered a devastating Saudi-led campaign to dislodge them. Since 2022, the two sides have been in a stalemate, though tensions have been rising again in recent months.

Mohammed al-Basha, founder of the Basha Report, a U.S. risk advisory firm focused on the Middle East and Africa, said the Houthis’ latest escalation comes as their influence is growing because of the increased importance of Bab al Mandeb while the Strait of Hormuz is choked off by Iran.

“This is their moment, because with everything happening in the Strait of Hormuz, Bab al Mandeb quadrupled in importance. By exerting maximum pressure in this period, they can maximize the effect of any kinetic action they’re trying to do,” Al-Basha said.

“Their narrative is very aggressive. They want war. And they feel that because they want war and sense that the U.S. and Saudi Arabia don’t, that they will submit to their demands.”

The announcement by the head of Yemen’s Presidential Leadership Council, Rashad al-Alimi, to resume oil exports starting July 20 following a halt that began in late 2022 has revived hope that the Yemeni government’s most important source of foreign currency will be restored. The government, struggling economically and facing continued Houthi rebel control over Yemen’s northwest, needs the money – and has pledged to direct the revenues towards paying salaries, improving services, and supporting economic stability.

However, the flow of oil from Yemen’s fields to global markets does not depend solely on a decision made by politicians; it requires creating a security environment, after years of war, that allows for the protection of facilities, pipelines and ports, in addition to restoring the confidence of shipping and insurance companies, as well as international buyers.

Recommended Stories

list of 4 itemsend of list

With Yemen’s war threatening to escalate after a four-year period of calm, the stability the country needs to resume oil exports may be elusive.

The export test

Yemen has proven oil reserves estimated at about three billion barrels, primarily concentrated in the Masila, Marib and Shabwa basins. While the United States Energy Information Administration (EIA) indicates that the country still holds sufficient resources for production and export, the security environment hinders their extraction and transport to global markets.

Yemen’s oil production reached a historical peak of about 439,000 barrels per day (bpd) at the beginning of the millennium, but it has gradually declined due to the depletion of some old fields. This decline accelerated with the outbreak of the war in 2014 and the targeting of oil infrastructure, settling at a level of 19,000bpd in 2024, according to the International Monetary Fund (IMF).

A report published by S&P Global estimated actual production, following the halt in exports, at about 7,000bpd to 10,000bpd in 2023 and 2024, almost all of which was for domestic use.

Yemeni Minister of Oil and Minerals Mohammed Bamqaa said that export revenues would be deposited in the Central Bank as part of a government directive to bolster the state’s financial resources, pointing out that there are oil stockpiles exceeding 1.7 million barrels ready for export.

Bamqaa added that total production will initially reach about 60,000bpd. He explained that the ministry has directed oil companies to prepare timelines to increase production and develop the fields, in a way that raises production capacity by up to 25 percent during the first month after exports resume.

Professor of financial economics at Hadramout University, Mohammed al-Kasadi, told Al Jazeera that while he expected oil production to meet the 60,000bpd figure mentioned by Bamqaa, the figure does not reflect the actual volume of exports, as the local market consumes about 20,000bpd to operate refineries and power plants, which makes the quantities available for export likely to hover at about 40,000bpd.

Hassan Mohammed Moghalis, an expert in Yemeni affairs, told Al Jazeera that most of the fields located in government-controlled areas remain capable of production. At the forefront of these are the Masila fields in Hadramout and the al-Uqla fields in Shabwa, which represent the fundamental base for any anticipated resumption. Moghalis explained that crude oil can be transported via pipelines to Arabian Sea ports.

However, Moghalis pointed out that resuming exports does not simply mean opening the valves, as some fields require maintenance and restoration after a long period of suspension. Additionally, pipelines and pumping stations require technical reviews to ensure their readiness before resuming regular operations.

A view of the Safer oil refinery in Marib, Yemen, in September 2020 [File: Ali Owidha/Reuters]

Market confidence

Despite the importance of restarting production at the oilfields, experts believe bigger obstacles await after the oil reaches Yemen’s ports. Houthi attacks targeting export ports in Hadramout and Shabwa in late 2022 made shipping and insurance companies more wary of handling Yemeni crude, pushing up insurance costs and weakening buyers’ willingness to enter into contracts.

The Houthis have conditioned the resumption of exports on them receiving a share of the revenues to cover public sector salaries.

Al-Kasadi, of Hadramout University, says that the government’s success in pumping oil to the port does not automatically guarantee a successful export process. Maritime transport and insurance companies primarily assess the level of security risks and the likelihood of ports or tankers facing renewed attacks – currently a particular concern in light of Houthi attacks on shipments tied to Saudi Arabia, which supports the Yemeni government.

Al-Kasadi added that the oil market relies heavily on trust and stability. Therefore, any export operation requires buyers to be convinced that shipments will depart safely and that export activities will not suddenly halt again.

Moghalis, the expert, believes that providing military protection for ports and pipelines is the first step, but not the only condition. It is also imperative to restore the confidence of insurance companies and international buyers, as oil does not reach markets solely through production, but rather via an interconnected system of transport, financing and insurance.

He added that any new attack on the ports, even if it does not cause significant material damage, could be enough to send the sector back to square one, given shipping companies’ sensitivity to risks in conflict zones.

But, as al-Kasadi pointed out, a resumption in exports is vital. He argued that the halt in exports was not merely an oil sector crisis, but rather developed into a comprehensive financial crisis. The government lost its most crucial source of foreign currency, which negatively impacted the Yemeni rial’s exchange rate and the state’s ability to finance basic services.

Economic pressure

Despite the importance of resuming exports, Yemeni affairs expert Abdul Karim al-Ansi warned against overstating its immediate impact on the Yemeni economy.

He told Al Jazeera that the resumption of exports will undoubtedly provide a vital source of foreign currency and afford the Central Bank greater leeway to support monetary stability. However, it will not be enough on its own to end the economic crisis, as the Yemeni economy faces broader challenges related to the division between government- and Houthi-controlled areas, weak non-oil revenues and declining economic activity.

Al-Ansi added that the extent to which Yemenis benefit from oil revenues will ultimately depend on how these funds are managed and the government’s ability to channel them into salaries and basic services, rather than solely on the volume of exports.

And while successful initial shipments could send a positive signal to markets and investors, al-Ansi stressed that the real test would be whether exports can be sustained. Yemen’s economy needs a steady flow of foreign currency, rather than sporadic shipments that stop whenever security conditions deteriorate.

The suspension of oil exports has not only deprived the government of its most important source of revenue, but also intensified pressure on the foreign exchange market. As dollar inflows from oil sales have dried up, demand for foreign currency has remained high to finance imports of essential goods, particularly food, fuel and medicine. The resulting shortage has weakened the Yemeni rial and contributed to rising inflation.

These pressures have been compounded by the monetary division between the Central Bank in Aden and the Houthis in Sanaa, which has created two separate financial systems and exchange rates. The split complicates monetary policy and limits the authorities’ ability to use oil revenues in a coordinated way to stabilise the economy.

Al-Kasadi said that Saudi financial support for the government had recently helped contain currency volatility in government-held areas. However, he stressed that such support was no substitute for a steady and sustainable flow of oil revenues – which needs a period of stability, something that may be difficult if the conflict escalates in Yemen, as it is currently threatening to do.

An armed student rallies in support of the Houthi-imposed naval embargo against Saudi Arabia in Sanaa, Yemen, Wednesday. Hundreds of students gathered at Sanaa University to support the move. Photo by Yahya Arhab/EPA

July 23 (UPI) — The Houthis in Yemen claimed responsibility for two attacks on Saudi oil tankers in the Red Sea with missiles and drones.

The Iran-backed Houthis, who have been fighting for control of Yemen, claimed on Wednesday that they had hit the Encelia and the Layla oil tankers, which they said were violating their blockade of Saudi ships. They had announced the blockade on Monday.

Saudi Arabia’s transportation authority confirmed the attack on the Encelia in a statement. It said there was a fire on board but the crew were all safe. It didn’t mention the Layla.

Houthi military spokesperson Yahya Saree said the group promised to continue naval operations and would continue “enforcing the ‘siege for a siege’ equation,” the BBC reported.

The Houthis claimed they had also forced “10 ships to retreat and return.” That claim could not be independently verified, The Times said, but at least six vessels reversed course in the Red Sea on Monday and Tuesday after the Houthis warned shipping companies to avoid Saudi ports, according to Kpler, a maritime data company. It was not clear if those ships were part of the Houthis’ claims.

The Saudis and the Houthis have been in an effective cease-fire since 2022. But last week, tensions flared when the Houthis accused the Saudis of striking the airport in Yemen’s capital Sanaa. The spat came from a dispute when an Iranian plane had tried to land at the airport.

The Houthis then attacked the Abha airport in Saudi Arabia.

When the Houthis announced the “maritime embargo,” they didn’t give many details. But a media official said they would close the Bab al-Mandab Strait. That strait is on the other side of the Arabian Peninsula from the Strait of Hormuz. It’s the gateway between the Arabian Sea and the Red Sea, and blockades of both straits would cut off Saudi Arabia ships entirely.

The United States and Iran continued to trade attacks for the 12th consecutive night after the cease-fire between the two countries ended.

Astronaut Buzz Aldrin walks on the surface of the Moon during the Apollo 11 mission on July 20, 1969. Photo by NASA/UPI | License Photo

New data released on Thursday showed that UK petrol prices have risen by 5p a litre since the beginning of July, hitting reaching almost £1.56.

Diesel is at £1.72 a litre, on average, according to the RAC.

Average gasoline prices in the US have surpassed $4 a gallon once more, up from $3.92 a month ago, according to motorist advocacy group AAA.

“More expensive fuel and energy can ripple through the wider economy, increasing costs for businesses and ultimately feeding through into the price of food and other goods,” said Jonathan Raymond, investment manager at Quilter Cheviot.

“This creates another headache for central banks as they continue their battle against inflation.

“If energy prices remain elevated, policymakers may come under pressure to keep interest rates higher for longer or even raise them. This would come as a blow to mortgage holders and borrowers already feeling the strain.”

The Bank of England, which sets UK interest rates, has held them at 3.75% in its last four meetings.

Paul Dales, chief UK economist at Capital Economics, said he believed the Bank will “almost certainly” hold them again. But he said analysts still expected that interest rates could be cut next year if energy price rises ease.

Kevin Warsh, the newly-appointed chair of the US Federal Reserve, last week told Congress that the central bank had “no tolerance to persistently elevated inflation”.

US President Donald Trump had pushed Warsh’s predecessor, Jerome Powell, to cut interest rates.

Trump has made it clear he expects Warsh to fulfil his demand for reductions in borrowing costs for Americans.

But the Fed held US interest rates between 3.5% and 3.75% at Warsh’s first meeting last month. He also told Congress that he was committed to “restoring price stability” in the wake of the Middle East conflict impacting prices.

Before the war, roughly 15 million barrels of Gulf oil passed through the Strait of Hormuz every day, as roughly a fifth of the world’s traded oil moved through the maritime chokepoint in peacetime.

ADVERTISEMENT

ADVERTISEMENT

With the channel still largely closed and prices elevated, at least seven major pipeline projects are now under construction, in planning or under discussion to push supplies out through the Red Sea, the Suez Canal and the Gulf of Oman instead, according to Gulf officials, energy companies and market analysts.

With the Iran war reignited this month, Brent crude is trading again at around $93 a barrel at the time of writing, well above the roughly $72 it fetched after June’s short-lived truce, and the US benchmark WTI has also risen to roughly $90 a barrel.

Depending so heavily on the Strait of Hormuz “is no longer a prudent long-term strategy,” said Victoria Grabenwöger, a senior researcher at the data firm Kpler.

Two escape valves already exist, and both are close to their limits.

Saudi Arabia’s East-West pipeline, built in the 1980s when Tehran threatened shipping during the Iran-Iraq war, carries crude from the Abqaiq complex to Yanbu on the Red Sea, where tankers head south towards the Arabian Sea or north to the Suez Canal.

Meanwhile, the UAE has been channelling more oil to Fujairah, its port on the Gulf of Oman about 145 kilometres south of the Strait of Hormuz.

Together the two links had a spare capacity of some 3.5 to 5.5 million barrels a day before the war, according to the US Energy Information Administration, and both now run close to full representing around 6.5 million barrels a day.

Abu Dhabi’s state oil company is also racing to finish a project it began before the war.

Its $3 billion (€2.6bn), 300-kilometre pipeline to Fujairah, laid alongside an existing line, is designed to lift deliveries by over 1.2 million barrels a day and is roughly half built, according to Kpler, which expects the official early-2027 completion target to slip to mid-2027 because the port itself must be expanded.

Even that timetable, the firm argues, only became conceivable because of the blockade.

Red Sea relief, Red Sea risk

The Red Sea route has vulnerabilities of its own, and this week served as a reminder.

Yemen’s Iran-backed Houthi rebels, who declared a blockade on Saudi-linked shipping in retaliation for the kingdom’s blockade of Yemen and an attack on Sanaa’s airport, said on Thursday they had attacked two Saudi tankers, the Encelia and the Layla, setting both on fire.

Saudi state media reported a blaze at the bow of the Encelia with no casualties, while the UK Maritime Trade Operations centre reported a tanker struck by “an unknown projectile” southwest of Al Shuqaiq.

The Iran-backed group has disrupted the Bab el-Mandeb Strait before, a maritime chokepoint carrying about 12% of world trade, and a Houthi drone strike forced the East-West pipeline itself to shut back in 2019.

Iraq’s $60 billion bet on Washington

Nowhere is the scramble more urgent than in Iraq, which draws about 90% of state revenues from oil exports and has had to cut output because of its dependence on the Strait of Hormuz.

Prime Minister Ali al-Zaidi returned from Washington last week with 48 agreements signed with American firms, spanning energy, healthcare and technology and worth more than $60 billion, according to Reuters, including tie-ups involving ExxonMobil, Shell, Halliburton, KBR and GE Vernova.

The centrepiece is a deal with Syria to rebuild the long-dormant pipeline running from the Kirkuk fields to the Mediterranean port of Baniyas, a project Iraqi state media says Chevron will execute and which the US State Department, welcoming the plan, called “a critical energy corridor” with an initial capacity of 2 million barrels a day.

Baghdad is also weighing a line from Basra to Jordan’s Aqaba.

Washington’s ambassador to Turkey, Tom Barrack, predicted the agreements would render the Strait of Hormuz “an afterthought”.

“The Yemeni armed forces have carried out a significant military operation targeting two Saudi oil tankers that violated the ban imposed by the armed forces in the Red Sea,” the Houthis claimed on Telegram. “The operation involved a number of ballistic and cruise missiles, as well as drones. Thanks to God’s help, the strikes were accurate and caused a large fire on both vessels.”

بيان القوات المسلحة اليمنية بشأن استهداف سفينتين نفطيتين سعوديتين خالفتا قرار الحظر في البحر الأحمر ما أدى إلى نشوب حريق كبير فيهما، واجبار 10 سفن على التراجع والعودة – 22 يوليو 2026م pic.twitter.com/S5ijNZYaV7

TWZ cannot independently verify the Houthi claim. However, in a post on X, UKMTO stated that a master of an oil tanker “reports being struck by an unknown projectile which has caused a fire onboard that the crew are currently fighting.”

The incident took place 70NM southwest of Al Shuqaiq, Saudi Arabia, the organization added. “There are no reported casualties and no environmental impact. Authorities are investigating. Vessels are advised to transit with caution and report any suspicious activity to UKMTO.”

The increasing tensions on the BAM come as U.S. President Donald Trump threatened to destroy Iranian bridges and power plants each time Iran hits a ship transiting the Strait of Hormuz, which has been a major flashpoint of tit-for-tat exchanges of fire. Trump also threatened that he will retaliate for the deaths of three U.S. Army soldiers during a July 17 attack on Muwaffaq Salti Air Base (MSAB) in Jordan. He made those statements at a dignified transfer ceremony for the soldiers, plus one killed in Iraq, at Dover Air Force Base in Delaware today.

The incident in the Red Sea took place a day after the U.S. Navy warned that the Houthis had moved weapons near the BAM.

“Recent Houthi statements indicated a readiness to target shipping (specifically Saudi-affiliated) if directed,” the Navy’s Joint Maritime Information Center (JMIC) warned on Tuesday. “According to regional reporting, Iran has instructed the Houthis to stand ready to close the Red Sea oil route should the United States strike Iranian power infrastructure.”

“Sources close to the group stated that the Houthis have completed preparations to attack shipping, including the deployment of missiles and drones positioned near Bab al-Mandeb.”

The Houthis have also “told shipping companies not to load or discharge cargo at Saudi Arabian ports or they may be targeted, according to an email the group sent to companies,” Reuters reported.

The Houthis are gearing up for potential anti ship missile launches, releasing footage that appears to show their Asef anti-ship ballistic missile (ASBM) as they continue to threaten commercial shipping linked to Saudi Arabia.

As we have frequently detailed, a Houthi blockade of the BAM threatens to add further pressure on oil exports from the Middle East, already drastically affected by the Iranian closure of the Strait of Hormuz and the resumption of the U.S. blockade on Iranian ports. Saudi Arabia has diverted millions of barrels of oil per day through pipelines to its Yanbu port on the Red Sea in an effort to minimize the energy shortages due to the hostilities in the Persian Gulf. This also raised the specter of the U.S. having to get as involved as it did during the previous Houthi campaign against shipping that ended last September, which could pull resources away from Iranian-focused operations.

Before the attack claim, global trade intelligence firm Kpler pointed out on X that while traffic continues through both straits, “operational confidence remains under pressure.”

“Traffic declined sharply across both chokepoints on 21 July, with Strait of Hormuz crossings down 31% day-on-day to nine vessels and Bab al-Mandeb down 34% to 29 amid a worsening security backdrop,” Kpler added. “Four confirmed vessel U-turns near the Gulf of Aden suggest operators are becoming more cautious following Houthi threats against Saudi-linked shipping. At the same time, confirmed maritime attacks continue around the Strait of Hormuz, reinforcing concerns that uncertainty across both regional chokepoints could reshape routing decisions, increase freight costs and sustain higher geopolitical risk premiums for energy markets.”

Dual chokepoint risks deepen

Shipping continues through both the Strait of Hormuz and Bab el Mandeb, but operational confidence remains under pressure. Traffic declined sharply across both chokepoints on 21 July, with Strait of Hormuz crossings down 31% day-on-day to nine… pic.twitter.com/D7dmCRffcv

As noted earlier in this piece, Trump visited Dover Air Force Base to take part in the dignified transfer ceremony honoring Lt. Tyler James Feehan, 25, of Hawaii, Pvt. Isabella Gonzales, 19, of Texas, Sgt. Angel Rampersad, 28, of New York and Sgt. Michael Emmanuel Swinton, 30, of North Carolina.

Today, we honor four American heroes who made the ultimate sacrifice in service to our nation.

May God hold them in His eternal embrace and comfort their grieving families, and may God forever… pic.twitter.com/P5NA59ltAU

— Rapid Response 47 (@RapidResponse47) July 22, 2026

Feehan, Gonzales and Rampersad were killed during the July 17 Iranian barrage of MSAB. U.S. Central Command (CENTCOM) previously announced Rampersad as missing, but her status was updated to a Duty Status–Whereabouts Unknown and she is believed to be deceased.

Swinton was killed during a controlled detonation of a downed One-Way Unmanned Aerial System on July 19, 2026, at Erbil Air Base, Iraq.

— Rapid Response 47 (@RapidResponse47) July 22, 2026

Speaking to reporters, Trump said his administration would share the results of the investigation into the MSAB attack and vowed that Iran would “pay a big price.”

Those comments followed an earlier statement the president posted on Truth Social vowing to target key infrastructure sites each time Iran strikes a ship transiting the Strait of Hormuz.

“From this point forward, any time the Islamic Republic of Iran shoots at a ship in the Strait of Hormuz, whether it be by Missile, Rocket, Drone, or any other device or weapon, the United States will bomb and destroy ONE BRIDGE OR POWER PLANT, including those located next to, or in, the Capital City of Tehran,” Trump proclaimed.

Not surprisingly, Iranian officials reacted to Trump’s comments by issuing their own threats in response.

“Iran will retaliate against regional infrastructure and energy facilities with American interests if the United States strikes any Iranian bridge or power plant, responding directly to a new threat from US President Donald Trump,” the Islamic Revolutionary Guard Corps (IRGC)-connected Tasnim news agency stated on X.

A military source said Iran will retaliate against regional infrastructure and energy facilities with American interests if the United States struck any Iranian bridge or power plant, responding directly to a new threat from US President Donald Trump. pic.twitter.com/a8MIFqxktx

Earlier on Wednesday, Jordanian officials said the country was once again targeted by Iran.

“An official military source at the General Command of the Jordanian Armed Forces—Arab Army stated that air defense systems detected six missiles coming from Iranian territory targeting the Kingdom’s territory today, and engaged them immediately upon their entry into Jordanian airspace,” the Jordanian military stated on X. “Air defenses intercepted and shot down four missiles, while the other two fell in two remote, uninhabited areas, without causing any casualties or material damage.”

“The Kingdom’s airspace is under continuous operational monitoring, and the Armed Forces will deal with any aerial threat targeting Jordanian territory according to the applicable rules of engagement, in a manner that ensures the protection of the Kingdom’s sovereignty and the safety of its citizens,” officials added.

The situation in Jordan is so intense that the U.S. Embassy in Amman issued a security alert.

“President Trump, Secretary of State Rubio, and the Department of State have no higher priority than the safety and security of American citizens,” the embassy cautioned on X. “We remind U.S. citizens that Iran has attacked civilian and critical infrastructure across the Middle East, including hotels, airports, diplomatic facilities, and other civilian locations.”

Security Alert: U.S. Embassy Jordan July 22

President Trump, Secretary of State Rubio, and the Department of State have no higher priority than the safety and security of American citizens. We remind U.S. citizens that Iran has attacked civilian and critical infrastructure… pic.twitter.com/UOihlptEwp

— U.S. Embassy Amman (@USEmbassyJordan) July 22, 2026

Over the course of the past 12 days, Iran has lobbed missiles and drones at several Arab nations, taking particular aim at U.S. military installations.

Satellite imagery continues to emerge on social media purporting to show damage at these bases. The images below claim to show a 117-FPS radar at Al-Jaber Air Base in Kuwait destroyed by an Iranian barrage. While the image clearly shows what appears to be a radome destroyed, TWZ cannot independently verify the date, location or provenance of the imagery. CENTCOM, which does not talk about battle damage, declined comment.

Imagery has also emerged purporting to show that U.S. Air Force aerial refueling tankers and other aircraft have evacuated Al Udeid Air Base in Qatar, the largest American base in the region. Again, we cannot confirm the details and CENTCOM, which also does not typically talk about the movements of assets, declined comment.

However, Axios reported last week that the Trump administration “notified Israel it is sending dozens more refueling planes to the country ahead of a potential expansion of military operations against Iran.”

“Israeli officials say the U.S. wants to send several dozen more refueling planes in the coming days, bringing the number of planes to the same level it had at the beginning of the war,” Axios added. “Israeli officials say the U.S. military prefers operating the refueling planes from Ben Gurion Airport, because other air bases in the region are more exposed to Iranian attacks and less safe for U.S. planes. At the moment, the Iranians are still deterred from launching attacks on Israel, because it will likely trigger a massive retaliation.”

The U.S. still sits ready to conduct long-range bomber strikes from bases in the U.S. and the U.K.

There were recent unconfirmed claims by open-source trackers that B-1B Lancer bombers out of RAF Fairford in England took part in yesterday’s attacks on Iran. Again, we cannot verify that and CENTCOM declined comment.

Overnight, B-1B “Lancer” bombers flying from RAF Fairford (EGVA) conducted strikes in Iran as the US ramps up operations again. Although 2 bombers launched, it appears it was pre-planned that only 1 of them would… pic.twitter.com/Q7Ic3Ahqk3

However, Israel’s KAN news outlet claimed that “Israel has been informed by the United States that it intends to escalate attacks on Iran in the coming days and to carry out attacks using heavy bombers for the first time in the current escalation.”

In addition, other U.S. Air Force assets – including EA-37B Compass Call electronic warfare jets – appear headed to the region, according to online flight trackers. While we don’t know for sure these jets will actually head to the Middle East, it could be another sign of the U.S. bolstering assets ahead of an increase in intensity of attacks, which have been largely focused over the past 12 days on Iranian coastal targets.

Amid these rising tensions with Iran, the Houthis have now apparently raised the stakes and it will be absolutely critical to keep the BAM open as the world already sits on the razor’s edge of a full-on energy crisis.

UPDATE: 7:17 PM EDT –

CENTCOM announced a new round of attacks on Iran.

“At 5:30 p.m. ET today, U.S. forces began launching more strikes against Iranian military targets at the Commander in Chief’s direction,” the command stated on X. “The mission will continue to further degrade Iran’s ability to threaten civilian mariners and commercial vessels transiting regional waters.”

At 5:30 p.m. ET today, U.S. forces began launching more strikes against Iranian military targets at the Commander in Chief’s direction. The mission will continue to further degrade Iran’s ability to threaten civilian mariners and commercial vessels transiting regional waters.

Claimed attacks come days after Houthis announced naval embargo on Saudi vessels.

Yemen’s Iran-aligned Houthis have claimed an attack on two Saudi oil tankers transiting through the Red Sea.

“We targeted two Saudi oil tankers, named ENCELA and LAYLIA, for their violation of the blockade decision issued by the armed forces,” Houthi military spokesperson Yahya Saree said on Wednesday.

Recommended Stories

list of 3 itemsend of list

Saree added that the attacks were carried out, “using a number of ballistic and cruise missiles, as well as drones”, and led to fires on the ships.

The Houthis, officially known as Ansar Allah, had also forced “nearly ten ships… to abandon their routes, and turn back”, Saree said.

Saudi Arabia has not commented on the claims, but the United Kingdom Maritime Trade Operations (UKMTO) centre said it had received reports that a tanker has been struck.

“The master of a tanker reports being struck by an unknown projectile which has caused a fire onboard that the crew are currently fighting,” UKMTO, which monitors shipping in the region, said.

Yemen’s Houthi group, which has fought the Yemeni government and a Saudi-led coalition that backs it for more than a decade, imposed a maritime blockade on Saudi Arabia on July 20. That followed some of the worst violence Yemen has seen for four years, after the Yemeni government bombed the Houthi-controlled Sanaa airport to stop an Iranian plane from landing.

The Houthis said the declaration of the maritime embargo on Saudi Arabia was “based on the equation of ‘an eye for an eye’ and affirmed “the right of our great people to respond to the blockade with a blockade”.

The group, which seized Sanaa in 2014, accused Saudi leaders of imposing “an unjust and oppressive siege” for nearly 12 years, “plundering our resources and imposing a comprehensive blockade on our ports and airports by land, sea, and air”.

“The Saudis feel that they can instigate a popular uprising against the Houthis using these economic strangulation methods,” Hussain al-Bukhaiti, a journalist based in Sanaa told Al Jazeera.

Riyadh has rejected claims that it was imposing a siege on the Yemeni people, and the group’s critics point out that they have rejected a proposal from Jordan to resume flights between Amman and Sanaa.

“The ultimate goal for Ansar Allah’s naval blockade against the Saudis, is to force Riyadh to lift its embargo on the ports and airports controlled by the Houthis,” al-Bukhaiti said.

Amid the disruption in shipping through the Strait of Hormuz due to the US-Israel war on Iran, Saudi Arabia has been attempting to facilitate oil flow through alternative routes through the Red Sea and the Bab al-Mandeb Strait. But that route is now under threat from the Houthis.

The Houthis disrupted global commerce when they began attacking ships around the Bab al-Mandeb after the launch of Israel’s genocidal war on Gaza in October 2023. The attacks ended with the announcement of a “ceasefire” in Gaza in October 2025.

“The people who are questioning if the Houthis can successfully do a blockade against the Saudis should remember, how successfully the Houthis closed access to the Red Sea for the Israeli ports, which in fact resulted in the closure of Eilat port in southern Israel,” said al-Bukhaiti. “Eventually the Americans had to do a deal with the Houthis, with mediation from Oman,” he added, referring to a May 2025 agreement.

The Bab al-Mandeb chokepoint connecting the Red Sea to the Gulf of Aden is one of the world’s most important shipping routes, including for oil exports.

Between Yemen to the northeast and Djibouti and Eritrea in the Horn of Africa to the southwest, the strait is just 29km (18 miles) wide at its narrowest point, limiting traffic to two channels for inbound and outbound vessels using the Suez Canal.

In 2024, about 4.1 billion barrels of crude oil and refined petroleum products passed through the strait – about 5 percent of the global total.

With the Strait of Hormuz effectively closed since Israel and the US launched their war on Iran in late February, shutting down Bab al-Mandeb as well could block 25 percent of the world’s oil and gas supply.

Weekly insights and analysis on the latest developments in military technology, strategy, and foreign policy.

As renewed hostilities between Iran and the U.S. and its allies enter a 10th day, the Houthi rebels of Yemen say they are imposing an embargo on Saudi oil shipments passing through the Bab el-Mandeb (BAM) Strait. The move threatens to add further pressure on oil exports from the Middle East, already drastically affected by the Iranian closure of the Strait of Hormuz and the resumption of the U.S. blockade on Iranian ports. Saudi Arabia has diverted millions of barrels of oil per day through pipelines to its Yanbu port on the Red Sea in an effort to minimize the energy shortages due to the hostilities in the Persian Gulf. This also raises the specter of the U.S. having to get as involved as it did during the previous Houthi campaign against shipping that ended last September, which could pull resources away from Iranian-focused operations.

BREAKING: Houthis of Yemen announce a a “maritime embargo” against Saudi Arabia, “effective immediately.”

Saudi Arabia has until now exported ~4.5m b/d from Yanbu in the Red Sea, most of it heading South throughout the Bab al-Mandab Strait between Yemen and Djibouti-Eritrea pic.twitter.com/c96Apzh9As

On Monday, Kuwait said it came under Iranian fire again.

“Kuwaiti air defenses are currently engaging hostile missile and drone attacks following the heinous Iranian aggression,” the Kuwaiti Defense Ministry stated on X. “The General Staff of the Army notes that any sounds of explosions heard are a result of air defense systems intercepting hostile attacks. Everyone is urged to adhere to the security and safety instructions issued by the relevant authorities.”

Hours earlier, Bahrain said it too had come under a new wave of Iranian attacks.

“The General Command of the Bahrain Defense Force (BDF) announces that Iran is continuing its systematic hostility approach through its sinister attacks targeting civilians in the Kingdom of Bahrain,” BDF posted on X. “The General Command clarifies that, with strong will and high combat readiness, the air defense systems attacked, intercepted and destroyed a number of treacherous Iranian air strikes today, Monday, July 20, 2026.”

The extent of the damage in either Kuwait or Bahrain is unclear at the moment. These most recent attacks came after U.S. Central Command on Sunday night said it wrapped up a ninth straight day of strikes on Iranian assets, targeting “military command centers, air defense and coastal surveillance sites, maritime capabilities, missile and drone launch sites, and communications networks to further diminish Iran’s ability to attack commercial vessels and civilian mariners transiting the Strait of Hormuz,” the command stated on X.

Amid this kinetic activity, as we noted earlier in this story, the Iranian-backed Houthis say they will no longer permit Saudi Arabian ships passage through from the Red Sea into the Bab el-Mandeb Strait.

“The Yemeni Armed Forces declare a maritime embargo against the criminal Saudi enemy, based on the equation of an ‘eye for an eye,’ effective immediately upon the issuance of this statement,” the Houthis stated on Monday, according to the official Houthi SABA media outlet. The move follows increased tensions between the Houthis and Saudi Arabia as well as a request by Iran “to stand ready to close the Red Sea oil route if the United States strikes Iranian power infrastructure,” Reuters reported last week. “The idea has been discussed within the Islamic Republic’s leadership, and the message has been conveyed to Iran’s Houthi allies.”

⚡️BREAKING: Yemen’s Houthis have announced a Naval Blockade on Saudi Arabia from the Red Sea

This move essentially Cuts OFF Saudi oil exports through the Bab al-Mandeb Strait pic.twitter.com/gqV8E5hfq1

Houthi forces on Monday reportedly began issuing warnings on open maritime frequencies near Yemen that the BAM is closed to Saudi shipping and its vessels are subject to attack.

Houthi forces are reportedly issuing warnings on open maritime frequencies near Yemen that the Bab al-Mandab Strait is closed to Saudi shipping. pic.twitter.com/MD0KhmTmJ5

A Houthi shut down of the Bab el-Mandeb (BAM) Strait, a narrow stretch of water between Yemen and Djibouti, would choke off the flow of oil exports from Saudi Arabia, exacerbating the above-mentioned impingement on the flow of oil from the closed Strait of Hormuz.

Having both straits closed at once is something of a ‘sum of all fears’ scenario for the global energy marketplace.

“The full closure of the BAM would cut global oil supply by 7% as it would leave most Saudi oil exports unable to leave the region,” Reuters noted on Monday. “The disruption would add to the massive cut to global oil flows from the war in the Gulf, which has already reduced shipments by 10% of global supply.”

You can read more about the effects of both straits being closed at once in our story about that here.

The Bab el-Mandeb Strait is a strategic chokepoint where the Houthis declared they have imposed an embargo on Saudi shipping. (Google Earth) The Bab al-Mandab Strait between Yemen and Djibouti has become a dangerous chokepoint of Houthi attacks. (Google Earth image)

Beyond affecting the flow of oil, a Houthi blockade on the BAM threatens to open a new front in this conflict.

The Houthis carried out a campaign against shipping in November 2023 in solidarity with Palestinians over the latest war between Israel and Gaza. However, while it was ostensibly aimed at only Israeli connected ships, numerous commercial vessels with no clear Israeli ties were attacked as were several U.S. and allied warships. The campaign stretched into the summer of 2025, forcing some vessels to avoid the Suez Canal for a far longer route around Africa, boosting shipping costs by nearly $200 billion at the time.

The Houthi attacks also forced the U.S. and allies to deploy many warships, including the Eisenhower and Truman Carrier Strike Groups (CSG) to both defend against Houthi attacks and strike targets in Yemen. These operations resulted in a large expenditure of air defense and strike munitions.

You can see video of some of those encounters below.

WATCH: CENTCOM releases footage as US HAMMERS Iran

The possibility exists that a new wave of Houthi attacks — especially if non-Saudi ships are targeted — could drag in U.S. forces already in heavy use in the Persian Gulf region battling the Iranians. This sets up a major showdown as Saudi oil is a lifeline to Asian supplies hobbled by conflict in the Persian Gulf. We reached out to CENTCOM for comment and will update this story with any pertinent details shared.

Earlier on Monday, the head of the European-led task force providing maritime security in the Red Sea region told us the Houthis remain a threat to navigation despite not having attacked any merchant vessels since September 2025.

“The security situation in the Bab el-Mandeb remains fragile and is highly sensitive to regional escalation,” Rear Admiral Vasileios Gryparis, Commander of EUNAVFOR ASPIDES, told TWZ. “On the rhetorical level, the Houthis’ leadership reiterated several times their alignment with the broader Axis of Resistance.”

Gryparis’s comments, in response to a query from last week about Iran’s outreach to the Houthis, came before the Yemeni group’s embargo declaration.

“From an operational standpoint, we assess that the Houthis pose a threat and are capable of rapidly escalating,” the ASPIDES commander told us. “We maintain a frequent presence at sea, monitor the situation, and adjust our actions when needed. In the event of a resumption of Houthi attacks on merchant vessels, which remains a possibility, we are present and ready to implement our mandate, within our means and capabilities. ASPIDES remains ready, within its defensive mandate, to adapt to evolving operational requirements.”