Energy markets remain on tenterhooks as the prospect of prolonged war in the Middle East grows.

Published On 13 Mar 202613 Mar 2026

Share

Oil prices have again risen above $100 per barrel as energy markets see little relief amid the biggest disruption to global energy supplies in a generation.

Brent crude, the international benchmark, surged more than 9 percent on Thursday as traders weighed the prospect of weeks, or even months, of turmoil in energy markets as the United States and Israel wage war on Iran.

Recommended Stories

list of 4 itemsend of list

Brent futures, which are traded outside of regular market hours, were priced at $101.13 as of 03:00 GMT.

Asian stock markets, including exchanges in Tokyo, Seoul and Hong Kong, opened sharply lower on Friday, following steep losses on Wall Street overnight.

The latest surge in oil prices came after Iran’s Supreme Leader Mojtaba Khamenei pledged to maintain the effective closure of the Strait of Hormuz, which normally transports about one-fifth of global oil supplies.

In a statement read out on his behalf on Iranian state television, Khamenei described Tehran’s threats against shipping in the waterway as a “lever” that “must continue to be used”.

US President Donald Trump struck a similarly defiant tone on Thursday, posting on Truth Social that stopping Iran from getting nuclear weapons was of “far greater interest and importance” than rising oil prices.

‘Lack of tangible goals in this war’

Traffic through the strait has effectively ground to a halt due to Iranian threats, with only a handful of vessels passing through each day, many of them claiming links to China, Iran’s key economic partner.

According to the United Kingdom Maritime Trade Operations (UKMTO) centre, no more than five ships have passed through the waterway each day since the US and Israel launched joint strikes on Iran on February 28, compared with an average of 138 daily transits before the war. At least 16 commercial vessels have been attacked in the region since the start of the conflict, according to the UKMTO.

Tehran has claimed responsibility for several of the attacks, including a strike on Wednesday that crippled a Thai-flagged vessel off the coast of Oman.

Efforts to bring calm to the market have so far done little to tame prices, which are up nearly 40 percent compared with before the start of the war.

The International Energy Agency’s (IEA) announcement on Wednesday that member countries would release 400 million barrels of oil from emergency stockpiles drew a tepid response among traders eyeing a daily shortfall in global supplies estimated at 15-20 million barrels.

The US Department of the Treasury’s issuance on Thursday of a temporary licence authorising countries to purchase sanctioned Russian oil that has been stranded at sea also failed to move the market, with Brent crude staying above $100 a barrel after the Treasury announcement.

“The key problem is a lack of tangible goals in this war,” said Adi Imsirovic, an energy security expert at the University of Oxford.

“It makes it hard for oil traders to see the light at the end of the tunnel,” he said.

Trump has repeatedly floated the possibility of using the US Navy to escort commercial shipping through the strait, but the Pentagon has yet to conduct such operations amid concerns about the risks posed by Iranian attacks in the narrow waterway.

In an interview with CNBC on Thursday, US Energy Secretary Chris Wright said that Washington was “not ready” to provide navy escorts but that such operations could begin by the end of the month.

“It’ll happen relatively soon but it can’t happen now,” Wright said.

As oil prices rise, the US, Israel and Iran seem ready to keep fighting no matter the costs.

The price of oil has soared over $100 a barrel globally as a result of the US-Israeli war on Iran. Iran has effectively shut down shipping lanes in the Strait of Hormuz, while Israel has attacked critical Iranian oil depots. Despite public pressure and outrage, all parties seem prepared to continue the war. What will it mean for the global economy and the people caught in the crossfire?

Zein Basravi (@virtualzein), Al Jazeera Senior Correspondent

Episode credits:

This episode was produced by Chloe K. Li, with Sarí el-Khalili, Catherine Nouhan, Tuleen Barakat, Spencer Cline and our host, Malika Bilal. It was edited by Alexandra Locke.

Our sound designer is Alex Roldan. Our video editors are Hisham Abu Salah and Mohannad al-Melhem. Alexandra Locke is The Take’s executive producer.

The global energy landscape is facing its most volatile period in decades following the US-Israeli strikes against Iran on 28 February that triggered a wider and potentially prolonged conflict in the Middle East.

ADVERTISEMENT

ADVERTISEMENT

What began as a targeted military operation has rapidly escalated into a direct confrontation with global economic implications.

Based on claims by Iranian state media and regional reports, the Islamic Revolutionary Guard Corps (IRGC) has ostensibly adopted a strategy of “energy blackmail” to leverage the international community into pressuring the US and Israel to cease its attacks.

The $200 per oil barrel threat was first articulated shortly after the conflict began.

On Sunday 1 March, a senior IRGC spokesperson warned that if “cowardly anti-human actions” continued, the world should prepare for a massive price surge, even as high as $200 per oil barrel.

This rhetoric has since become a central pillar of Tehran’s messaging.

As recently as this Wednesday, Ebrahim Zolfaqari, the spokesperson for Iran’s Khatam al-Anbiya military command headquarters, told state media: “Get ready for the oil barrel to be at $200, because the oil price depends on the regional security which you have destabilised.”

Iran’s tactical disruption

The IRGC’s current strategy relies on “internationalising” the cost of the conflict.

By disrupting the flow of nearly 20% of the world’s oil and liquefied natural gas (LNG) through the Strait of Hormuz, Iran aims to drag the global economy into the fray.

This is why the IRGC has targeted vessels from neutral nations, including ships sailing under Thai, Japanese and Marshall Islands flags, among others.

According to energy analysts, this disruption is designed to create domestic political pressure within Western nations, to in turn force the US and Israel to pull back on military action in exchange for energy stability.

By striking countries that have not attacked them directly, Tehran is signaling that no maritime trade is safe as long as the strikes on its soil continue.

The main vector of this strategy is precisely the disruption of energy markets, an element Iran can influence directly through its geographical advantage.

A history of oil price shocks

While $200 per barrel sounds astronomical, oil has approached similar levels in the past when adjusted for inflation.

The highest nominal price ever recorded was around $147 in 2008, driven by peak oil fears and rampant speculation just before the global financial crisis. When adjusted for 2026 inflation, that 2008 peak represents roughly $211 per barrel.

Previous major shocks, such as the 1973-74 Arab Oil Embargo and the 1979 Iranian Revolution, saw prices quadruple and double respectively from pre-crisis levels.

In 1980, prices hit a nominal peak of about $39.50, which would be approximately $160 in today’s terms.

However, the current crisis involves a total physical blockade of one of the world’s most critical maritime chokepoint, increasing the risk of a price “moonshot”.

Market response and reserves

At the time of writing, Brent crude is trading just above $100 per barrel, a sharp increase from the $60 range seen in mid-February before the Iran war began.

The International Energy Agency has attempted to stabilise the market by orchestrating the largest-ever coordinated release of strategic reserves, but the continuation of Iranian strikes agaisnt oil infrastructure and tankers has largely neutralised the effort.

With insurance providers cancelling war-risk coverage and shipping companies redirecting fleets, the market remains in a state of high anxiety.

If the blockade on the Strait of Hormuz persists, the $200 figure may shift from a political threat to an increasingly likely scenario.

In a recent report, Oxford Economics identified $140 per barrel as the threshold at which the global economy tips into mild recession, reducing world GDP by 0.7% by year-end and pushing the UK, the Eurozone and Japan into contraction.

The United States military is “not ready” to accompany oil ships through the Strait of Hormuz, a top official in President Donald Trump’s administration says as Iran continues to block the strategic waterway.

US Energy Secretary Chris Wright told the CNBC business news channel on Thursday that the markets are experiencing a “short-term disruption”, predicting that the war would go on for “weeks, not months”.

Recommended Stories

list of 3 itemsend of list

Despite Trump’s repeated threats, Iran has largely succeeded in shutting down the strait, which links the Gulf to the Indian Ocean. The closure has sent oil prices soaring.

Wright described the effects of the crisis as “short-term pain for long-term gain”, arguing that the US is “destroying” Iran’s ability to threaten the energy market.

Last week, Trump suggested that the US Navy would escort ships through the Gulf, but Wright said on Thursday that the move “can’t happen now”.

“We’re simply not ready. All of our military assets right now are focused on destroying Iran’s offensive capabilities and the manufacturing industry that supplies their offensive capabilities,” the energy secretary said.

“We don’t want this to be a brush-off for a year or two. We want to permanently destroy their ability to build missiles, to build roads, to have a nuclear programme.”

His comments came as Iran’s new supreme leader, Mojtaba Khamenei, affirmed in his first public comment since being selected to succeed his assassinated father, Ali Khamenei, that the Strait of Hormuz should remain closed during the war.

“The will of the people is to continue effective and deterrent defence,” Khamenei said in a written statement. “The tactic of closing the Strait of Hormuz must also continue to be used.”

The Iranian military has said it would “welcome” the US Navy escorting oil ships, suggesting it is prepared to strike US forces in the narrow waterway.

On Wednesday, three commercial vessels were attacked near the strait.

Wright announced earlier this week on social media that the US Navy had escorted an oil ship through the strait, then quickly deleted the post. The White House subsequently confirmed that the claim was not true.

It is not clear why the statement was released and then retracted.

Assurances by US officials that Washington would open the strait have temporarily calmed markets, only for prices to spike again.

The price of a barrel of oil peaked at about $120 on Sunday, up from about $70 before the US and Israel launched the war on February 28. It has been yo-yoing between $80 and $100 for the past few days.

In addition to the marine blockade, Iran has targeted oil installations across the Gulf.

As one of the world’s largest oil producers, the US is largely self-sufficient. But possible shortages in Asia and Europe have put a strain on prices globally.

According to data from the American Automobile Association, the average price of one gallon (3.78 litres) of petrol in the US is now $3.60, up from $2.94 last month.

Rising energy prices could fuel inflation and affect the cost of basic goods, including food.

But Trump suggested on Thursday that the US is benefitting from skyrocketing oil prices.

“The United States is the largest Oil Producer in the World, by far, so when oil prices go up, we make a lot of money,” the US president wrote in a social media post.

“BUT, of far greater interest and importance to me, as President, is stopping an evil Empire, Iran, from having Nuclear Weapons, and destroying the Middle East and, indeed, the World.”

Iran denies seeking a nuclear weapon, and Trump reiterated for months before the current conflict that US strikes against Iranian facilities in June had “obliterated” the country’s nuclear programme.

Brent futures rose sharply on Thursday, spiking above $100 before easing slightly but remaining higher than levels seen earlier in the week as markets stay incredibly volatile.

ADVERTISEMENT

ADVERTISEMENT

This comes despite an unprecedented decision by the 32-member International Energy Agency (IEA) on Wednesday to release a record 400 million barrels to calm markets, more than double the volume released after Russia’s 2022 invasion of Ukraine.

Following the IEA decision, Iran stepped up its offensive campaign and launched strikes on Omani oil storage facilities at the Salalah port and multiple ships in and near the Strait of Hormuz, sending prices higher again.

Record coordinated release of reserves

The US alone is contributing 172 million barrels. Germany, France and Italy also confirmed they would tap their stocks, while Japan said it would begin releases next Monday.

IEA executive director Fatih Birol described the current Iran-related crisis as an “oil market challenge unprecedented in scale”, adding that the collective response reflected “strong solidarity” in defence of global energy security.

Exports of crude and refined products from the region have dropped to 10-15% of pre-war levels, with the Strait of Hormuz, which normally carries one-fifth of the world’s oil, effectively closed to the large majority of tankers.

Iran’s attacks blunt expected price relief

The new Iranian strikes came at lightning speed, directly after the IEA announcement.

Drones targeted fuel storage tanks and silos at Oman’s Salalah port, igniting fires that Omani authorities were still working to contain late on Wednesday.

British maritime security firm Ambrey confirmed damage to the facilities, while Danish shipping giant Maersk temporarily halted port operations.

Omani officials stressed there had been “no disruption to the continuity of oil supplies or petroleum derivatives” inside the country itself, while Iranian state media reported that President Pezeshkian had assured Oman’s sultan the incident would be investigated.

At the same time, six vessels were struck in the Gulf and Strait of Hormuz.

Among the reports, there was confirmation of a projectile hitting a container ship near the UAE and strikes on two tankers in Iraqi waters.

UK Maritime Trade Operations, and other monitoring groups, attributed the incidents to Iranian forces or proxies.

These developments, occurring the very day of the reserves release, appear to have smothered the anticipated calming effect on prices.

As of Thursday, the number of ships struck in the region since the beginning of the conflict rose to at least sixteen.

Record release may signal deeper market concerns

Some analysts note that the sheer volume of the release could itself be interpreted negatively. Previous coordinated actions never exceeded 183 million barrels.

The scale of the release suggests importing nations already view the disruption as the most severe and long-lasting in decades.

Even worse, a record release may not be enough.

Speaking to Euronews, Warren Patterson, Head of Commodities Strategy at ING, was blunt in his assessment.

“A record 400 million barrel release from emergency reserves is helpful, but it’s not going to go very far to offset the roughly 15 million daily supply currently disrupted.”

Patterson also added that “the only solution that will bring oil prices down on a sustained basis is getting oil flowing through the Strait of Hormuz again.”

Oxford Economics echoes this concern, warning that “the economic effect of higher energy costs rises as the oil price increases,” in a report that seemingly indicates the crisis is far from over and we have yet to feel the compounding effect of the initial shock.

Russian sanctions relief remains off the table

With the reserve release failing to calm prices, attention has turned to Russian oil as a potential source of additional supply.

The US Treasury last week granted Indian refiners a 30-day waiver to purchase Russian crude from vessels already stranded at sea, though the measure expires on 4 April and deliberately excludes new shipments.

Following the G7 emergency discussions on Wednesday, French President Emmanuel Macron stated that the group had agreed “the situation does not justify lifting any sanctions” on Russia, emphasising the need to increase global production instead.

The contrast between Washington’s narrow waiver and the G7’s firm collective position leaves little prospect of sanctions relief acting as a meaningful pressure valve, a view shared by analysts.

“Any sanction relief for Russia would see some marginal supply increases, but again not enough, with Russia’s oil output having held up well in recent years despite sanctions,” Warren Patterson of ING told Euronews.

$140-$150 oil barrel possible if conflict is prolonged

Should tensions persist, analysts warn prices could climb substantially higher.

Oxford Economics identifies $140 per barrel as the threshold at which the global economy tips into mild recession, reducing world GDP by 0.7% by year-end and pushing the UK, the Eurozone and Japan into contraction.

The managing director of the IMF, Kristalina Georgieva, also stated that every 10% increase in oil prices, provided they persist for most of the year, will push up global inflation by 0.4% and reduce worldwide economic output by as much as 0.2%.

“The risk is stark,” Patterson warned. “It’s only a matter of time before we see oil prices hitting fresh record highs if the conflict is not swiftly and decisively resolved.”

The IEA’s intervention has provided a temporary buffer, but with little visible impact on prices.

The surge in oil prices triggered by the war in Iran is increasingly becoming a major concern for global central banks, which are closely monitoring the potential economic and financial consequences of the shock.

More than a week of conflict in the Middle East has disrupted energy supply routes and pushed crude prices sharply higher, raising fresh fears about inflation. For policymakers already grappling with fragile economic conditions, the oil spike presents a complex policy dilemma.

Historically, oil shocks have posed a difficult challenge for central banks. Rising energy prices can drive inflation higher while simultaneously weakening consumer spending and business activity by raising costs. In such circumstances, policymakers face an uncomfortable choice: tighten policy to control inflation or ease financial conditions to support economic growth and employment.

The current situation could potentially produce both outcomes at once, creating a scenario where inflation rises even as economic demand weakens a combination that complicates monetary policy decisions.

Inflation Versus Economic Growth

Central banks traditionally respond to inflationary pressures by raising interest rates or maintaining tighter monetary policy. Some policymakers argue that responding quickly to inflation triggered by an oil shock can prevent inflation expectations from becoming entrenched and reduce longer-term economic damage.

Others, however, advocate “looking through” temporary energy-driven price spikes, arguing that aggressive tightening could unnecessarily damage economic growth. This approach gained prominence after the pandemic, when many central banks initially viewed inflation as temporary a judgment widely criticised in hindsight.

The decision facing policymakers now depends on several uncertainties, including how long the conflict lasts, how severely energy supplies are disrupted, and whether governments intervene with subsidies or price caps to protect consumers.

Given these unknowns, many central banks may prefer to adopt a cautious approach, waiting to see how markets and economic conditions evolve before making significant policy adjustments.

Financial Stability Risks Enter the Picture

Beyond inflation and growth concerns, central banks must also consider a third responsibility that has gained prominence since the global financial crisis: financial stability.

Senior policymakers worry that the oil shock could expose vulnerabilities that have been building in global financial markets for years. A large macroeconomic disturbance involving energy prices, inflation, interest rates and currency volatility could trigger a broader financial stress event.

Much of the concern centres on the growing role of “shadow banking” institutions, financial intermediaries operating outside traditional banking regulation. These entities have become increasingly important providers of credit to companies and governments.

One major area of focus is the rapid expansion of private credit funds, which now manage more than $3 trillion globally. These funds allow asset managers to lend directly to businesses, often outside the scrutiny of public markets or traditional banking standards.

Regulators worry that during a major shock, investors could rapidly withdraw funds from these vehicles, potentially creating liquidity problems for borrowers and spillover risks for banks that help finance or manage the funds.

Pressure in Bond and Repo Markets

Another major source of concern lies in government bond markets, where highly leveraged hedge funds have become increasingly active. Many of these funds use repurchase agreements, or “repo” markets, to borrow money and finance large trades involving government bonds.

These strategies often rely on exploiting small price differences between cash bonds and futures contracts, but they involve substantial leverage. While such activity can help smooth government financing, it can also create systemic vulnerabilities during periods of market stress.

The Financial Stability Board, which monitors risks to the global financial system for the G20, warned earlier this year that sudden deleveraging in repo markets could disrupt sovereign bond markets.

More than $16 trillion in repo transactions backed by government bonds were outstanding last year, with about 60% concentrated in the United States. A sudden withdrawal of leveraged investors could therefore have significant ripple effects across global financial markets.

New Fragilities: Stablecoins and Technology Stocks

Regulators are also monitoring emerging risks linked to digital finance. Stablecoins cryptocurrencies pegged to traditional currencies such as the U.S. dollar have grown rapidly and are increasingly investing reserves in government bonds.

With the stablecoin market now worth roughly $300 billion and expanding, any loss of confidence in these assets could trigger large-scale sales of the bonds that back them. Such an event could add stress to already volatile financial markets.

At the same time, some investors remain concerned about high valuations and heavy market concentration in the rapidly growing artificial intelligence sector, which could amplify market volatility during periods of economic uncertainty.

Analysis: Oil Shock Could Trigger Wider Financial Stress

The Iran war oil shock illustrates how geopolitical crises can interact with financial vulnerabilities to create broader economic risks.

Higher energy prices directly increase inflation and strain household finances. At the same time, they can force central banks to reconsider interest-rate policies, potentially leading to higher borrowing costs and greater volatility in financial markets.

Such conditions could expose weaknesses in highly leveraged sectors of the financial system, particularly in shadow banking, hedge funds and digital financial markets.

Although previous shocks including the economic turmoil following Russia’s invasion of Ukraine did not ultimately trigger a major financial crisis, policymakers remain cautious. The brief turmoil in the U.S. regional banking sector in 2023 demonstrated how quickly financial stress can emerge when economic conditions shift.

If oil prices remain elevated and central banks are forced to respond aggressively, the resulting tightening of financial conditions could amplify existing vulnerabilities across markets.

For now, the disturbances appear manageable. But the combination of geopolitical conflict, energy market disruption and financial fragility ensures that central banks will continue to watch the situation with increasing concern.

Two foreign tankers were seen ablaze in Iraqi territorial waters after a strike near the al-Faw port. Authorities say they evacuated 25 crew members but have confirmed at least one death and are battling to control the flames.

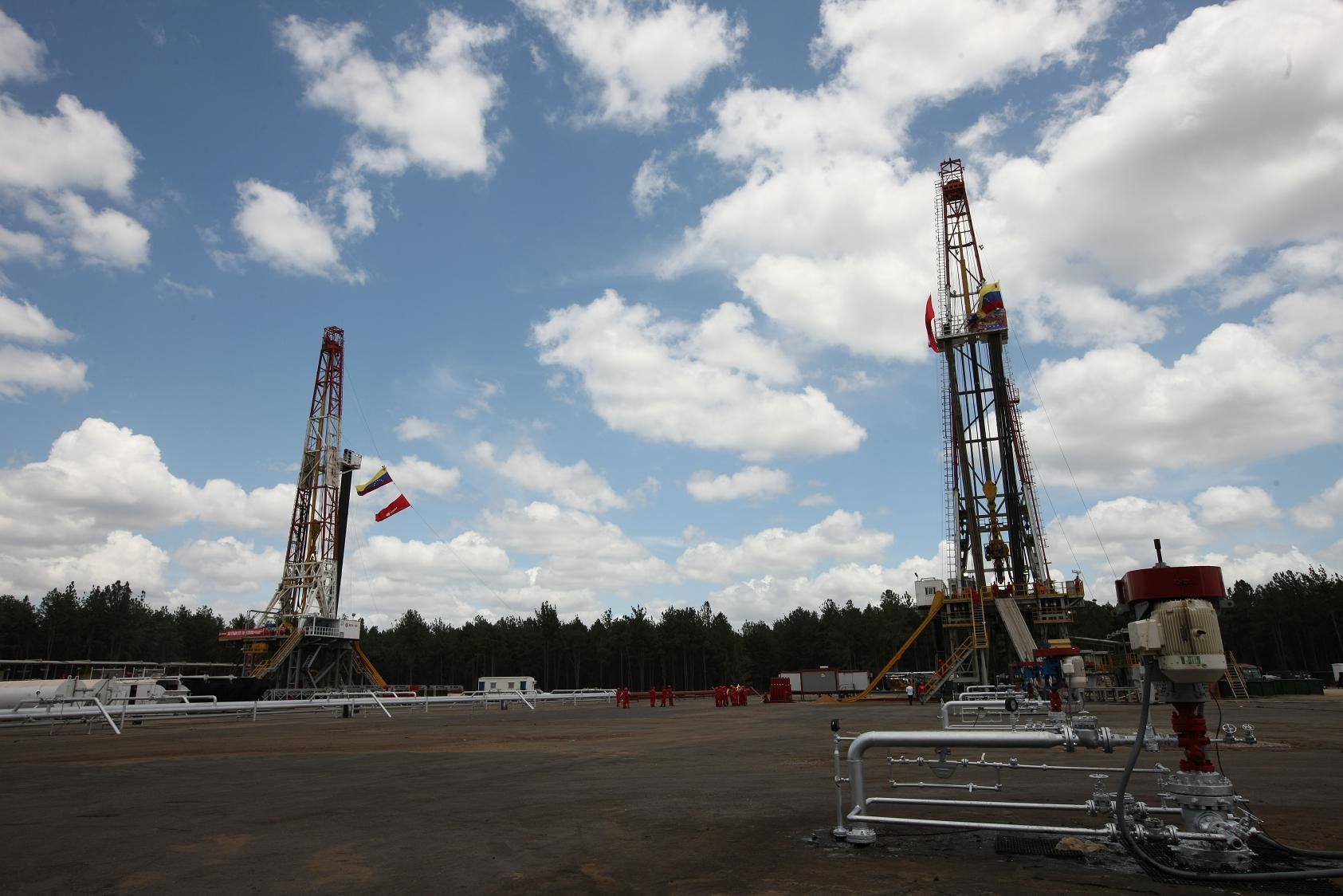

The Punta de Mata division produced over 400,000 bpd in the 2000s. (PDVSA)

Caracas, March 11, 2026 (venezuelanalysis.com) – Energy conglomerates Chevron and Shell are reportedly securing major oil deals in Venezuela following the recent pro-business reform of the country’s Hydrocarbon Law.

According to Reuters, joint venture Petropiar, where Chevron holds a minority stake, will expand its operations into the Ayacucho 8 bloc of Venezuela’s Orinoco Oil Belt.

Venezuelan state oil company PDVSA completed exploration and appraisal of the 510 square-kilometer area located south of Petropiar’s current operations, but its development has been limited. Under the agreement, Chevron looks to significantly expand its extra-heavy crude output from the Orinoco Oil Belt, which holds three-quarters of Venezuela’s oil reserves.

Chevron is reportedly looking to secure reduced royalties and taxes under the recently reformed Hydrocarbon Law in order to launch operations in the new area. Petropiar currently produces 90,000 barrels per day (bpd) of upgraded Hamaca crude. PDVSA’s joint ventures with Chevron have a total present output of around 250,000 bpd.

In January, Venezuela’s National Assembly approved a legislative overhaul that significantly improved conditions and benefits for private corporations in the oil and natural gas sector. Royalty and income tax levies, previously set at 30 and 50 percent, respectively, can now be slashed at the Venezuelan executive’s discretion.

In addition, joint venture minority partners can directly manage crude operations and sales, while legal disputes can be taken to international arbitration instances. Furthermore, PDVSA can also lease out projects to private operators in exchange for a percentage of the oil output.

Under the latter model, Shell is reportedly set to take over operations in PDVSA’s Punta de Mata division in eastern Monagas state, one of the most historically productive and profitable regions for Venezuela’s oil industry. The division produced over 400,000 bpd of light and medium crude grades in the 2000s but recent production was around 90,000 bpd.

The London-based multinational, which had a strong presence in the Venezuelan energy sector throughout the twentieth century, is likewise interested in capturing and processing natural gas that is currently flared in oil extraction processes.

Shell is additionally set to lead the Dragon offshore natural gas project alongside Trinidad and Tobago’s National Gas Corporation (NGC) in Venezuelan waters. The Nicolás Maduro government had suspended all joint initiatives with Trinidad due to its administration’s support for Washington’s Caribbean military buildup and threats against Venezuela last year.

Since the January 3 US military strikes and kidnapping of President Maduro, the acting Venezuelan authorities led by Delcy Rodríguez have fast-tracked a diplomatic rapprochement with the Trump administration while also vowing to “adapt” legislation to attract foreign investment. Following the hydrocarbon reform, a new mining law has also been preliminarily approved by the Venezuelan parliament.

US Energy Secretary Chris Wright and Interior Secretary Doug Burgum have visited Venezuela in recent weeks and hailed the investment opportunities in oil and minerals for US conglomerates.

Since January, the Trump administration has taken control of Venezuelan oil exports, with crude shipments handled by commodity traders Vitol and Trafigura and proceeds deposited in accounts run by the US Treasury. US authorities so far have only returned US $500 million, out of a reported $2 billion agreement, to the Caribbean nation.

The White House has also issued a number of licenses in an effort to boost US involvement in the Venezuelan energy sector, including limited waivers to export inputs and technology. In addition, Washington has allowed several corporations to negotiate agreements with Caracas while mandating that contracts be subject to US jurisdiction and that all royalty, tax and dividend payments be made to US Treasury-run accounts.

Alongside Chevron and Shell, the other companies with early access to the Venezuelan energy sector are BP, Eni, Maurel & Prom, and Repsol. The latter two held meetings with Rodríguez in February to discuss investment opportunities, while ExxonMobil has announced plans to send a delegation to the country in the coming weeks.

Venezuela’s oil production rebounded in February, with OPEC secondary sources registering an output of 903,000 bpd, up from 823,000 bpd in January. A US naval blockade since December had forced PDVSA to cut back production before exports began to flow again under Washington’s control. The oil sector remains under US financial sanctions.

For its part, PDVSA reported a February output of 1.02 million bpd, up from 924,000 bpd the prior month. The direct and secondary measurements have differed over time due to disagreements over the inclusion of natural gas liquids and condensates.

Global currency and commodity markets stabilised slightly on Tuesday after a volatile start to the week triggered by the war involving Iran, United States and Israel. The U.S. dollar steadied against major currencies after earlier declines, following remarks from U.S. President Donald Trump that the conflict could end “very soon.”

Financial markets had been thrown into turmoil a day earlier amid fears that a prolonged war could trigger a major global energy shock. The conflict has disrupted oil and gas exports through the critical Strait of Hormuz, a vital shipping route for global energy supplies.

Although markets calmed somewhat after Trump’s comments, the broader environment remains highly uncertain as investors continue to assess the potential economic fallout from the conflict.

Dollar Holds Ground as Oil Prices Ease

In Asian trading, the U.S. dollar was largely steady against other major currencies after retreating from the highs reached during Monday’s market turbulence.

The currency traded at around 157.73 yen against the Japanese yen and about $1.1632 against the euro, reflecting a stabilisation following the sharp movements seen earlier.

Meanwhile, oil prices remained elevated but declined from the dramatic peaks reached at the start of the week. Brent crude traded at roughly $93 per barrel, still significantly higher than levels before the outbreak of the war but well below Monday’s surge toward $120.

The pullback in oil prices helped ease immediate concerns about a severe energy shock, although analysts caution that volatility could continue if the conflict escalates again.

Investors Remain Cautious

Despite the relative calm in currency markets, analysts say investors are far from convinced that the crisis is nearing resolution.

Rodrigo Catril, a currency strategist at National Australia Bank, warned that markets could continue to experience sudden shifts in sentiment as geopolitical developments unfold.

According to Catril, it remains unclear whether the Iranian leadership would be willing to pursue de-escalation, suggesting that the risk of renewed market volatility remains high.

The Islamic Revolutionary Guard Corps in Iran dismissed Trump’s suggestion that the conflict could end quickly, describing the remarks as “nonsense.”

Risk-Sensitive Currencies Under Pressure

Currencies closely linked to global economic sentiment weakened as investors remained cautious.

The Australian dollar slipped to around $0.7063, while the New Zealand dollar fell to roughly $0.5912. These currencies often decline during periods of geopolitical uncertainty or when investors shift toward safer assets.

The dollar, by contrast, has benefited from its traditional role as a safe-haven currency during times of crisis. The escalation of the conflict and disruption to energy markets prompted investors to move funds into U.S. assets, supporting the currency.

The British pound recovered from losses earlier in the week to trade around $1.3434.

Energy Prices and Global Growth Concerns

Investors remain concerned that sustained high energy prices could slow global economic growth. Rising oil costs increase expenses for businesses and households, effectively acting as a tax on economic activity.

At the same time, higher energy prices could complicate monetary policy by pushing inflation upward and making it harder for central banks to lower interest rates.

Analysts at Deutsche Bank noted that a broader market sell-off in risk assets would likely require several conditions to occur simultaneously: persistently high oil prices, a shift in central bank policy expectations and clear evidence of a slowing global economy.

Strategist Henry Allen said markets are now significantly closer to those thresholds than they were just a week ago, though the full conditions for a major downturn have not yet materialised.

Analysis: Markets Brace for Prolonged Volatility

The market reaction to the Iran war underscores how closely global financial conditions are tied to geopolitical developments in the Middle East.

While Trump’s comments about a possible quick end to the conflict helped stabilise markets temporarily, the underlying risks remain substantial. The disruption of energy supplies through the Strait of Hormuz continues to threaten global oil flows and could trigger renewed price spikes if the conflict intensifies.

For investors, the situation presents a delicate balance. On one hand, hopes for de-escalation could stabilise energy prices and reduce pressure on financial markets. On the other, continued fighting or further disruptions to oil shipments could quickly reignite volatility across currencies, commodities and equities.

Until there is clearer evidence of either de-escalation or escalation, markets are likely to remain highly sensitive to political developments, with the dollar continuing to benefit from its role as a global safe haven.

Attacks on multiple commercial ships in the waters around Iran on Wednesday increased global energy concerns, pushed nations to unleash strategic oil reserves and sparked fresh critiques of the Trump administration’s readiness for a war it started.

As Trump administration and U.S. military officials continued to claim increasing success and advantage in the conflict — and authorities downplayed a reported threat of drone attacks on California — leaders around the world scrambled to respond to the latest attacks and the International Energy Agency’s call for the largest ever release of strategic oil reserves by its members to help stem energy price spikes.

President Trump also faced renewed questions about a deadly strike on an Iranian elementary school at the start of the war, after the New York Times reported Wednesday that a military investigation had determined the U.S. was responsible.

“I don’t know about it,” Trump said when asked about the report.

In an address Wednesday morning, IEA Executive Director Fatih Birol said energy shipments through the Strait of Hormuz had “all but stopped” amid the conflict, driving massive global competition for oil and gas in wealthier countries and fuel rationing in poorer nations.

He said the IEA’s 32 member nations have brought a “sense of urgency and solidarity” to recent discussions on the matter, and had unanimously agreed to “launch the largest ever release of emergency oil stocks in our agency’s history,” making 400 million barrels of oil available.

However, he said the most needed change is the “resumption of traffic through the Strait of Hormuz.”

A vendor pumps petrol from Iranian fuel oil tankers for resale near the Bashmakh border crossing between Iraq and Iran.

(Ozan Kose / AFP/Getty Images)

Several countries, including Germany, Austria and Japan, had already confirmed their plans to release reserves.

The White House did not immediately respond to a request for comment on any U.S. plans to release its strategic reserves, or how much would be released. The U.S. is an IEA member.

Trump told reporters Wednesday that the U.S. has hit Iran “harder than virtually any country in history has been hit,” including by wiping out its naval fleet and eliminating other vessels capable of laying mines, and that he believes oil companies should resume shipments through the strait despite the recent attacks.

U.S. Interior Secretary Doug Burgum backed the idea of releasing oil reserves in a Fox News interview.

“Certainly these are the kinds of moments that these reserves are used for, because what we have here is not a shortage of energy in the world; we’ve got a transit problem, which is temporary,” Burgum said. “When you have a temporary transit problem that we’re resolving militarily and diplomatically — which we can resolve and will resolve — this is the perfect time to think about releasing some of those, to take some pressure off of the global price.”

Burgum said that while Iran is “holding the entire world hostage economically by threatening to close the strait,” Trump has made the consequences of such actions “very clear,” and “there’s a lot of options between ourselves and our allies in the region, including our Arab friends in the region, to make sure that those straits keep open and that energy keeps flowing for the global economy.”

The IEA did not provide details as to the release of the 400 million barrels, part of a broader reserve of some 1.2 billion barrels held by its members. It said the reserves “will be made available to the market over a time frame that is appropriate to the national circumstances of each Member country and will be supplemented by additional emergency measures by some countries.”

The agency said an average of 20 million barrels of crude oil and oil products transited the strait per day in 2025, and that options for bypassing the strait are “limited.”

While some tankers believed linked to Iran were still getting through the Strait of Hormuz, which under normal circumstances carries about 20% of the world’s oil and natural gas, Iranian officials threatened attacks on other vessels — saying they would not allow “even a single liter of oil” tied to the U.S., Israel or their allies through the channel, which connects to the Persian Gulf.

Trump has repeatedly claimed that the U.S. and its powerful Navy would support commercial vessels and ensure the strait remains open to oil shipments, but that has not been the case.

Tankers wait off the Mediterranean coast of southern France on Wednesday.

(Thibaud Moritz / AFP/Getty Images)

The United Kingdom Maritime Trade Operations center, run by the British military, reported at least three ships struck in the region Wednesday — including ships off the United Arab Emirates and a cargo ship that was struck by a projectile in the strait just north of Oman, setting it ablaze.

The Trump administration and the U.S. military, meanwhile, have been pushing out messaging about wiping out Iran’s ability to plant mines in the strait — posting dramatic videos of major strikes on tiny boats on small docks.

Adm. Brad Cooper, the leader of U.S. Central Command, said in a video posted to X on Wednesday morning that “in short, U.S. forces continue delivering devastating combat power against the Iranian regime.”

“I’ve said this before, but it bears repeating: U.S. combat power is building, Iranian combat power is declining,” he said.

The U.S. has struck more than 60 Iranian ships, and just “took out the last of four Soleimani-class warships,” he said. “That’s an entire class of Iranian ships now out of the fight.”

Cooper said Iranian ballistic missile and drone attacks have “dropped drastically” since the start of the war, though “it’s worth pointing out that Iranian forces continue to target innocent civilians in gulf countries, while hiding behind their own people as they launch attacks from highly populated cities in Iran.”

He also addressed the attacks on commercial shipping in the region directly, saying that “for years, the Iranian regime has threatened commercial shipping and U.S. forces in international waters,” and that the U.S. military’s “mission is to end their ability to project power and harass shipping in the Strait of Hormuz.”

Other U.S. leaders called the U.S. war plan — and specifically its approach to protecting the Strait of Hormuz — into question.

In a series of posts to X late Tuesday, which he said followed a two-hour classified briefing on the war, Sen. Chris Murphy (D-Conn.) slammed the administration’s plans as “incoherent and incomplete.”

Murphy wrote that the administration’s goals for the war seemed to be focused primarily on “destroying lots of missiles and boats and drone factories,” and without a clear plan for what to do when Iran — still led by “a hardline regime” — begins rebuilding that infrastructure, other than to continue bombing them. “Which is, of course, endless war,” he wrote.

Murphy also specifically criticized the administration’s plan for the Strait of Hormuz — which he said simply doesn’t exist.

“And on the Strait of Hormuz, they had NO PLAN,” he wrote. “I can’t go into more detail about how Iran gums up the Strait, but suffice it [to] say, right now, they don’t know how to get it safely back open. Which is unforgiveable, because this part of the disaster was 100% foreseeable.”

Ships in the strait remained under threat of various forms of attack Wednesday, as did much of the region as the war raged on.

There was an attack on a U.S. Embassy operations center at Baghdad’s airport, which officials attributed to a drone launched by Iranian proxies based in Iraq. No casualties were reported.

Lebanon’s Health Ministry reported the death toll there — from fighting between Israel and Iranian-backed Hezbollah fighters — had risen to 634 since last week, including 91 children. Another 1,500 people had been wounded, the ministry said.

Iranian authorities have said U.S. and Israeli attacks have killed 1,255 people since Feb. 28. That includes many Iranian leaders, including then-Supreme Leader Ayatollah Ali Khamenei. U.S. officials have said Iranian attacks in the region have killed seven U.S. service members, with another 140 wounded.

CBS News reported Wednesday that dozens of those injuries were sustained by service members in the March 1 Iranian drone attack on a tactical operations center in Kuwait — which is also where six of the seven deaths occurred.

The outlet reported that the attack was more severe than the Trump administration has revealed, with more than 30 military members still in hospitals Tuesday with a range of battle injuries including “brain trauma, shrapnel wounds and burns.”

Threats extended beyond the Middle East, too — including to California, where law enforcement agencies were warned by federal authorities that Iran “allegedly aspired to conduct a surprise attack” on California using drones launched from a vessel off the U.S. coast.

However, sources told The Times that advisory was cautionary and not backed by credible intelligence.

Times staff writer Gavin J. Quinton, in Washington, D.C., contributed to this report.

The executive director of the International Energy Agency Fatih Birol said he is glad to see IEA’s 32 member countries unanimously agree to release 400 million barrels of oil from its emergency stockpile.. File Photo by Ole Berg-Rusten/EPA-EFE

March 11 (UPI) — The International Energy Agency agreed to take emergency action and release 400 million barrels of oil into the market, the coalition announced Wednesday.

The 32 members of the IEA unanimously agreed to tap into their emergency reserves in response to the strain on the oil market from the war in Iran.

“The oil market challenges we are facing are unprecedented in scale, therefore I am very glad that IEA member countries have responded with an emergency collective action of unprecedented size,” Fatih Birol, IEA executive director, said in a statement.

“Oil markets are global so the response to major disruptions needs to be global too. Energy security is the founding mandate of the IEA, and I am pleased that IEA members are showing strong solidarity in taking decisive action together.”

The IEA said oil will be released to the market “over a timeframe that is appropriate to the national circumstances of each member country.”

The release of emergency reserves is the sixth in the coalition’s history since being founded in 1974.

Japanese Prime Minister Sanae Takaichi said Wednesday that Japan plans to begin releasing oil from its stockpile possibly next week. Japan is an IEA member.

Oil prices soared after the United States and Israel launched military operations against Iran. Iran has threatened vessels traveling through the Strait of Hormuz, a critical route in the oil trade, in response.

About 25% of the world’s seaborne oil is transported through the Strait of Hormuz.

The IEA has an emergency stockpile of more than 1.2 billion barrels of oil, There are 600 million additional barrels obligated by member governments.

Sen. Markwayne Mullin, R-Okla., speaks to the press outside the U.S. Capitol on Thursday. Earlier today, President Donald Trump announced Mullin would replace Kristi Noem as Secretary of the Department of Homeland Security. Photo by Bonnie Cash/UPI | License Photo

HomeNewsOil Underinvestment Could Hinder US’ Iran-Crisis Response: Here’s Why

No matter how the Iran war gets resolved, the US and other countries will be forced to reckon with a global oil market in complete disarray.

Underinvestment in the oil industry makes the current supply shock much riskier worldwide, industry experts say, forcing the US, the EU, and various Gulf countries into a scramble over where and how to extract.

Prior to the US’ attack on Iran on February 28, the situation had already been precarious. Iran basically controls the Strait of Hormuz, the world’s busiest oil shipping channel. Transportation through this channel is currently closed, despite President Donald Trump’s promise to keep it open. Regardless of how this situation resolves, the broader implications of structural underinvestment across the oil and gas value chain have exposed just how unstable the global energy infrastructure is.

“This is not your father’s energy sector anymore,” Adam Turnquist, Chief Technical Strategist for LPL Financial, says.

Essentially, there was a shift from “drill drill drill” to returning cash to shareholders through dividends and free cash flow, he explained. This change led to better stock performance and improved financial metrics, such as credit spreads and default swaps. But, Turnquist adds, “there’s evidence of under-investment.”

‘A Multi-Million-Barrel Disruption’

Recall the 2011‑2014 time frame when oil prices were above $100 per barrel. Major oil companies like ExxonMobil, Chevron Corp, BP plc, Shell plc and TotalEnergies SE enjoyed strong cash flows, allowing them to generate substantial profits and reward shareholders.

When oil prices collapsed between 2014 and 2016, institutional shareholders pushed hard for capital discipline instead of growth. Corporations, rather than drilling aggressively, returned troves of cash to investors via buybacks and dividends.

In 2023, alone, Exxon, Chevron, Shell, TotalEnergies, and BP returned a record $114 billion to shareholders — 76% higher than their average payouts.

“That translated into lower reinvestment rates, fewer long‑cycle megaproject sanctions, and a bias toward short‑cycle barrels, even as global demand continued to grow,” Benny Wong, Senior Energy Analyst at PitchBook, told Global Finance.

There was also an energy transition, and companies prioritized ESG (environmental, social, and governance) over long-term oil projects, leading major funds to reduce fossil fuel investments.

“The result is a thinner spare capacity buffer and a smaller pipeline of readily deployable projects, which limits the industry’s ability to backfill a sudden, multi‑million‑barrel disruption like the one arising from the Iran conflict,” Wong added.

Oil Prices Spike

So far, the shock is reverberating across the globe. Brent crude, the international benchmark, entered 2026 oversupplied, with forward prices in the $50s, according to Chas Johnston, CreditSights senior analyst.

On Monday, the price of Brent crude spiked to $119.50 per barrel—the highest it has been since the summer of 2022, when Russia invaded Ukraine.

“It’s nearly the same cadence,” Turnquist says, citing Bloomberg data. See the chart below.

West Texas Intermediate (WTI), the U.S. benchmark, also saw similar price spikes, briefly reaching $119.48 per barrel. By late Monday, prices fell back below $90 per barrel, following mixed signals from US leadership, including contradictory statements from Trump and Defense Secretary Pete Hegseth about the conflict’s timeline.

And it could get worse, according to Wood Mackenzie, a consultancy firm for the energy sector. On Tuesday, the firm determined that $200 per barrel “is not outside the realms of possibility in 2026.”

To quell the panic, extreme measures are under consideration. The 32 member countries of the International Energy Agency (IEA) agreed on Wednesday to make 400 million barrels of oil from their emergency reserves available to the market to address the current disruption. That’s double the amount the IEA put into the market in 2022.

Over the weekend, Energy Secretary Chris Wright said the US could potentially release oil from its 400 million barrels of reserve to lower gas prices.

Trump subsequently confirmed that he would ease sanctions on certain countries to help reduce oil prices. This followed a recent 30-day waiver announced by US Treasury Secretary Scott Bessent on sanctions for Russian oil sales to India, due to global supply pressures.

Can Any Country Fill The Gap?

Further complicating matters, oil-producing countries like Bahrain and Kuwait declared “force majeure,” stopping production as storage nears capacity and exports falter. With Iran, Israel, and the U.S. each targeting energy infrastructure and the narrow Strait of Hormuz under threat, it remains unclear which alternative transport routes or supply sources could fill the gap.

Saudi Arabia and the United Arab Emirates remain two key options because they hold most of OPEC’s effective spare capacity. However, analysts still question how much cushion truly exists and how long they can sustain it. Reports already suggest Saudi Arabia and the UAE have begun reducing output by several million barrels per day.

“In other words,” Wong says, “the buffer is meaningful but not unlimited, particularly if the disruption is prolonged or widens regionally.”

West African and Guyanese deepwater projects won’t quickly replace lost supply, either. However, they could strengthen global production over the medium to long term, Wong says. Guyana’s rapidly developing offshore sector, for example, could add more output in the coming years, though expansion will still take time.

Then there’s Namibia, which has had significant offshore discoveries in recent years. BP, Shell and TotalEnergies are among the companies that have set up shop there, but as Wong puts it: “Commercial production is still a few years away.”

US Shale Is Another Issue

As for the US, a rapid ramp now requires more than just a strong price signal.

“Producers are operating with much tighter capital discipline, and scaling quickly requires having available rigs, completion crews, frac sand and pipeline takeaway capacity, all of which can act as bottlenecks,” Wong says.

CreditSights’ Johnston agrees.

“The ability for US producers to respond is also quite limited, because it still takes six to nine months to bring new production online, even from the short-cycle shale industry,” he says.

Until then, the stakes remain high. Wood Mackenzie projects roughly 15 million barrels per day (mbpd) of Gulf oil exports could be lost if the Strait of Hormuz remains disrupted. They note that alternatives like US shale and uncompleted wells might only add a few hundred thousand barrels per day over months — not even close to filling the 15 million‑barrel gap.

The circumstances are enough to give analysts pause, given the cavalier attitude coming from the US.

Turnquist echoed a point his firm’s chief macro strategist made during a recent call: “You can’t shake the hornet’s nest and then put it back away.” Once geopolitical issues ignite, they rarely resolve quickly, he said, pointing to wars in Iraq, Afghanistan and Russia-Ukraine as examples.

“There’s really no concrete signs that it’s going to end anytime soon,” he added.

Warning comes as 400 million barrels of oil are being released from global reserves during waterway’s closure.

Published On 11 Mar 202611 Mar 2026

Share

Iran’s Islamic Revolutionary Guard Corps (IRGC) says it will not allow “a litre of oil” through the Strait of Hormuz as the closure of the key Gulf waterway continues to roil global energy markets during the US-Israeli war on Iran.

A spokesperson for the IRGC’s Khatam al-Anbiya Headquarters said on Wednesday that any vessel linked to the United States and Israel or their allies “will be considered a legitimate target”.

Recommended Stories

list of 3 itemsend of list

“You will not be able to artificially lower the price of oil. Expect oil at $200 per barrel,” the spokesperson said in a statement. “The price of oil depends on regional security, and you are the main source of insecurity in the region.”

Global oil prices have fluctuated wildly this week during continued US-Israeli attacks against Iran, which has retaliated by firing missiles and drones at targets across the wider Middle East.

The closure of the Strait of Hormuz, through which about one-fifth of the world’s oil supplies transit, and production slowdowns in some Gulf countries have raised concerns of further disruptions.

Concerns around the duration of the war, which began on February 28 and has shown no sign of abating, are also adding to uncertainty, sending oil prices soaring.

On Wednesday, three ships were hit by projectiles in the Strait of Hormuz, maritime security and risk firms said, including a Thai-flagged cargo vessel that came under attack about 11 nautical miles (18km) north of Oman.

Release of oil reserves

World leaders, including members of the Group of Seven (G7) and the European Union, have been mulling what action to take in response to the war’s impact on global economies.

Christian Bueger, a professor of international relations at the University of Copenhagen and an expert in maritime security, said Europe will be facing “a major energy supply crisis” if the Strait of Hormuz is not reopened.

“For the shipping industry right now, it’s impossible to go through the Strait of Hormuz,” Bueger told Al Jazeera. “And if there are not stronger signals in the near future that they can at least try to go through the strait, then we are looking at a major shipping crisis, which can last weeks if not months.”

On Wednesday, the International Energy Agency (IEA) announced that its 32 member countries had unanimously agreed to release 400 million barrels of oil from their emergency reserves to try to lower prices.

“This is a major action aiming to alleviate the immediate impacts of the disruption in markets,” IEA Executive Director Fatih Birol said during an address from the agency’s headquarters in Paris.

“But to be clear, the most important thing for a return to stable flows of oil and gas is the resumption of transit through the Strait of Hormuz,” he added.

The reserve supplies will be made available “over a timeframe that is appropriate” for each member state, the IEA said in a statement without providing details.

German Economy and Energy Minister Katherina Reiche said earlier in the day that the country would comply with the release while Austria also said it would make part of its emergency oil reserve available and extend its national strategic gas reserve.

Meanwhile, Japan’s Ministry of Economy, Trade and Industry said it would release about 80 million barrels from its private and national oil reserves.

Japanese Prime Minister Sanae Takaichi said the country, which gets about 70 percent of its oil imports through the Strait of Hormuz, would begin releasing the reserves on Monday.

South Korea is in discussions with the IEA over the agency’s proposal to release strategic oil reserves, Seoul officials said Wednesday. This photo, taken Mar. 10, shows a gas station in Seoul. Photo by Yonhap

The South Korean government is “closely involved” in discussions with the International Energy Agency (IEA) over the agency’s reported proposal to release strategic oil reserves to help stabilize soaring oil prices, Seoul officials said Wednesday.

Officials at the Ministry of Trade, Industry and Resources confirmed Seoul’s participation in the reported IEA discussions to Yonhap News Agency, following media reports saying that the IEA has proposed the largest-ever release of oil reserves to its 32 member countries, including South Korea.

According to the report by the Wall Street Journal, IEA members are expected to soon decide on the proposal in an extraordinary meeting.

“South Korea is closely involved in discussions over a coordinated release of strategic oil reserves by the IEA,” a ministry official said.

The country currently holds around 1.9 billion barrels of oil reserves, which is enough to last more than 200 days.

“We have yet to decide how much oil will be released from our reserves with the IEA’s decision,” a ministry official said.

The Seoul government has released its strategic oil reserves on five occasions since 1990, all through international coordination.

The occasions included the 1991 Gulf War, the 2011 Libya crisis and the outbreak of the Russia-Ukraine War in 2022.

Copyright (c) Yonhap News Agency prohibits its content from being redistributed or reprinted without consent, and forbids the content from being learned and used by artificial intelligence systems.

WASHINGTON — Russia is emerging as one of the few early economic beneficiaries of the war with Iran, as disruptions to energy infrastructure drive up demand for Russian exports and the world casts its gaze to the Middle East and away from Moscow’s war in Ukraine.

The U.S. and its European counterparts slapped severe sanctions on Russia in March 2022, barely a month into Russian President Vladimir Putin’s full-scale invasion of Ukraine. The effect was a stranglehold on Russia’s exports, depriving Putin’s war effort of at least $500 billion, experts say. But over the last week, as President Trump’s war in the Middle East choked energy markets worldwide, the White House began easing its restrictions on Moscow.

“It is traitorous conduct for you to help Russia,” California Rep. Ted Lieu (D-Torrance) said on X, demanding the Trump administration reverse course. “Russia is giving intelligence info to Iran that helps Iran target American forces.”

Crude droplets rained over Tehran after Israeli airstrikes decimated oil depots, draping the Iranian capital in a dense smog. Iranian counterattacks have also targeted refineries and oil fields in Saudi Arabia and Bahrain. Crude oil prices have surged, and traffic through the Strait of Hormuz has all but ceased, sending energy importers in search of alternate sources.

Those spikes are giving Russia, one of the world’s largest oil and gas exporters, a rare advantage. After spending a decade as the world’s most sanctioned nation over his aggression in Ukraine, Putin is finally starting to regain some leverage in global markets.

“In the current economic situation, if we refocus now on those markets that need increased supplies, we can gain a foothold there,” Putin said at a meeting at the Kremlin on Monday, according to Russian state media. “It’s important for Russian energy companies to take advantage of the current situation.”

On March 4, the Treasury Department issued a temporary 30-day waiver allowing Indian refiners to purchase Russian oil. The appeal by the Trump administration was described as a way to ease demand for Mideast oil, but was criticized as a reversal of sanctions placed against Putin meant to deny him the capital needed to fund his occupation of eastern Ukraine.

Now, Moscow is poised to press that advantage further, after Trump said Monday he will further lift sanctions on oil-producing countries to ease the trade friction and reintroduce additional oil and gas supplies. The only countries with U.S. oil sanctions are Russia, Iran and Venezuela.

“So, we have sanctions on some countries. We’re going to take those sanctions off until this straightens out,” Trump said at a news conference at his golf club in Doral, Fla. “Then, who knows, maybe we won’t have to put them on — they’ll be so much peace.”

Trump’s announcement followed an unscheduled hourlong call with Putin about the situation in the Middle East.

The war has also set the stage for Russia to make gains in Ukraine, as hostilities draw the global spotlight away from Kyiv and its struggle to hold back the bigger Russian army. U.S.-brokered talks between the two adversaries have been sidelined as Washington shifts focus to its war in Iran.

“At the moment, the partners’ priority and all attention are focused on the situation around Iran,” Ukrainian President Volodymyr Zelensky said on X. “We see that the Russians are now trying to manipulate the situation in the Middle East and the Gulf region to the benefit of their aggression.”

Putin is unlikely to intervene militarily on Iran’s behalf, according to Robert English, an international foreign policy expert at USC. Instead, Putin is expected to play his position carefully, reap the economic rewards, and keep focused firmly on Ukraine at a time when key air defense systems are diverted from Ukraine to the Persian Gulf.

“Russia is winning the Iran-U.S.-Israel war, at least so far. Oil and natural gas prices have soared, filling Putin’s Ukraine war chest,” he said. “Russia is gathering forces for a big spring offensive in Eastern Ukraine, and it’s not even front-page news.”

Ukraine has dispatched drone interceptors and ordered its anti-drone experts to pivot from their war with Russia to help Western allies help intercept Iranian attacks. Zelensky’s allegiance may not pay off, English said.

“When will Ukraine see the benefits of helping the U.S. with anti-drone technology? No time soon, apparently,” he said.

Even several weeks of interruption in Gulf energy supplies could bring the largest windfall to Russia, the Associated Press reported, citing energy analysts.

The economic turmoil caused by the war has exposed vulnerabilities in Europe’s energy system, particularly its lingering dependence on Russian fuel.

Despite sanctions, the European Union remains a major purchaser of Russian natural gas and crude oil. Russian gas accounted for approximately 19% of E.U. gas imports in 2025. Allied Europeans have agreed to completely stop importing Russian liquefied natural gas, oil and pipeline gas by late 2027.

Putin expressed no desire Monday to rescue the European market now that U.S.-Israeli escalations and Iranian retaliation have choked oil production and shipping. The Russian president instead proposed to divert volumes away from the European market “to more promising areas” like the Asia-Pacific region, Slovakia and Hungary, which he said were “reliable counterparties.”

European leaders have been criticized for being “stunned, sidelined, and disunited” since hostilities began in late February. Excluded from the initial military planning by the U.S. and Israel, Europe entered the conflict with gas storage at only 30% capacity, the lowest levels in years. Instead of bold action, English said, European leaders have quarreled over internal divisions and rivalries.

“Sky-high energy prices are the underlying cause of many of these frictions, as Europe struggles now more than ever to find affordable alternatives to the cheap Russian petroleum,” English said.

Antonio Costa, president of the European Council, told European leaders in Brussels on Tuesday that rising energy prices and the world’s shifting attention risk strengthening the Kremlin at a critical moment in the war in Ukraine.

“So far, there is only one winner in this war,” Costa said. “Russia.”

G7 energy ministers will hold a call on Tuesday to discuss sharply rising energy prices triggered by the ongoing war in Iran, officials said. A separate call later in the day will see European Union leaders addressing similar concerns, reflecting heightened global anxiety over fuel supply and costs.

Oil prices surged to their highest levels since mid-2022 on Monday, driven by fears of reduced Gulf output and disruptions to tanker traffic through key shipping routes. Even before the Iran conflict, European energy prices were generally higher than those in the United States and China.

G7 Prepares Response, But Stops Short of Releases

G7 finance ministers signalled readiness to take “necessary measures” in response to the price surge but did not commit to coordinated emergency releases of strategic oil reserves.

The G7, which includes United States, Canada, Japan, Italy, Britain, Germany, and France, will hold the call at 1245 GMT. French Finance Minister Roland Lescure, whose country holds the G7 presidency this year, said that Europe and the U.S. currently do not face immediate supply shortages.

EU Leaders Target Competitiveness and Energy Costs

Later on Tuesday, EU leaders will discuss energy prices and competitiveness, joining German Chancellor Friedrich Merz, Italian Prime Minister Giorgia Meloni, Belgian Prime Minister De Wever, and others.

The EU is highly exposed to global energy volatility, importing more than 90% of its oil and roughly 80% of its gas. EU Commission President Ursula von der Leyen has pledged proposals at next week’s EU summit to address rising prices.

Officials have already discussed measures including adjustments to energy taxes and potential amendments to the EU carbon price, which contributes around 11% to industrial power costs.

Coordinated Action Sought but Uncertain

The calls by the G7 and EU reflect a growing urgency to manage energy price shocks caused by the Iran war. While governments have the tools to intervene, officials are balancing the need to stabilize prices with broader fiscal and strategic considerations.

With oil and gas markets highly sensitive to geopolitical developments, both G7 and EU leaders face pressure to act quickly to prevent price spikes from translating into economic slowdowns or political unrest across their regions.

WASHINGTON — Some 140 American service members have been wounded since start of the Iran war, with eight of them “severely injured” and receiving medical care, the Pentagon said Tuesday.

“The vast majority of these injuries have been minor, and 108 service members have already returned to duty,” Pentagon spokesperson Sean Parnell said in a statement.

The casualty toll adds to the seven American troops killed so far in the war, which entered its 11th day with no clear sign of slowing down as U.S. officials indicated that the military campaign was likely to intensify.

Iran, too, took new actions that could escalate the conflict, reportedly laying mines in the Strait of Hormuz, a potentially devastating development for the global energy market.

President Trump said that if Iran put mines in the strait and did not remove them immediately, the U.S. military would hit Iran “at a level never seen before.”

“If, on the other hand, they remove what may have been placed, it will be a giant step in the right direction!” Trump wrote on Truth Social.

The warning was yet another escalation that came after Defense Secretary Pete Hegseth said Tuesday would bring the “most intense day of strikes” inside Iran, a fighting tempo that is at odds with Trump’s own assessment that the war is “very complete” and could end “very soon.”

At a Pentagon news conference, Hegseth said “the most fighters, the most bombers, the most strikes” would be deployed, but declined to say how much longer U.S. forces would be expected to fight in the region. He instead said the president will be the one to “control the throttle.”

“It’s not for me to say whether this is the beginning, the middle, or the end. He will continue to communicate that,” Hegseth told reporters.

That deference places the focus squarely on Trump, who a day earlier delivered mixed signals about the duration of the war, telling reporters at one point that the war is “very much complete” and a later time that it is “the beginning of building a new country.”

At a briefing on Tuesday, White House Press Secretary Karoline Leavitt said the U.S. military was “way ahead of schedule” on reaching its objectives in Iran, but reiterated that the president alone will decide what victory looks like.

“President Trump will determine when Iran is in a place of unconditional surrender and when they no longer pose a credible and direct threat to the United States of America and our allies,” Leavitt said.

The president’s shifting positions on the war’s conclusion have played out as Trump threatens to hit Iran “twenty times harder” if it attempts to halt the flow of oil in the Strait of Hormuz, a key channel for the world’s oil supply — and as Democrats in Congress says they are growing concerned about the possibility of Trump sending U.S. ground troops inside Iran.

“We seem to be on a path toward deploying American troops on the ground in Iran to accomplish any of the potential objectives here,” Sen. Richard Blumenthal (D-Conn.) told reporters after being briefed on the Iran war.

When asked about Democrats’ concerns, Leavitt said Trump “wisely … does not rule options out as commander-in-chief.”

“I would hesitate to confirm anything that a Democrat says right now about the president’s thinking,” she added.

U.S. says Iran’s fire power is diminishing

As Washington plans out its next steps, the war has shown little signs of slowing. U.S. military officials say Iran’s military capabilities are eroding under sustained strikes that have targeted “deeply buried missile launchers” and made “substantial progress toward destroying” Iran’s navy.

Hegseth said “the last 24 hours have seen Iran fire the lowest amount of missiles they have fired yet.”

Gen. Dan Caine, chairman of the Joint Chiefs of Staff, told reporters that Iran’s ballistic missile attacks “continue to trend downward 90%” since the start of the war, and that drone attacks have decreased by 83%.

U.S. forces are also targeting Iran’s “industrial base in order to prevent the regime from being able attack Americans, our interests and our partners for years to come,” Caine said.

Caine said the Iranian military is adapting to the U.S. strategy, but remains confident in Washington’s ability to overpower Tehran. “They are adapting, as are we, of course. We have very entrepreneurial war fighters out there,” he said. “We are watching what they are doing, and we are adapting faster than they are.”

Asked whether Iran had proved to be a stronger adversary than anticipated, Caine said: “They are fighting, and I respect that, but I don’t think they are more formidable than what we thought.”

Iran, meanwhile, has refused to bow down to Trump’s demands and has issued warnings of its own.

Ali Larijani, Iran’s top national security official, called Trump’s threat against their targets on the Strait of Hormuz “hollow” and told him that he should instead focus on taking care of himself so that he is not “eliminated.”

Iran’s parliament speaker, Mohammed Bagher Qalibaf, however, said Iran was determined to keep fighting and was “definitely not looking for a ceasefire.”

“We believe that the aggressor should be punched in the mouth so that he learns a lesson so that he will never think of attacking our beloved Iran again,” Qalibaf said.

New attacks on neighbors

Meanwhile, Iran launched new attacks at Israel and gulf Arab countries. In Bahrain, authorities said an Iranian attack hit a residential building in the capital, Manama, killing a 29-year-old woman and wounding eight people.

Saudi Arabia said it destroyed two drones over its oil-rich eastern region and Kuwait’s National Guard said it shot down six drones. In the United Arab Emirates, firefighters battled a blaze in the industrial city of Ruwais — home to petrochemical plants — after an Iranian drone strike. No injuries were reported.

In Tel Aviv, explosions could be heard as Israel’s defense systems worked to intercept barrages from Iran.

Along with firing missiles and drones at Israel and at American bases in the region, Iran has also targeted energy infrastructure and traffic through the Strait of Hormuz, a vital waterway for traded oil, sending oil prices soaring. The attacks appear aimed at generating enough global economic pain to pressure the U.S. and Israel to end their strikes.

Brent crude, the international standard, spiked to nearly $120 on Monday before falling back but was still at around $90 a barrel Tuesday, nearly 24% higher than when the war started on Feb. 28.

“The president and his energy team are closely watching the markets, speaking with industry leaders and the U.S. military is drawing up additional options, following the president’s directive to continue keeping the Strait of Hormuz open,” Leavitt said. “I will not broadcast what those options look like but just know the president is not afraid to use them.”

So far, the president has offered to have the U.S. Navy escort oil tankers.

The White House has insisted that soaring gas prices are temporary, but the shock in the energy markets has already prompted the Trump administration to lift oil-related sanctions on some countries, including Russia.

“We are going to take those sanctions off until this straightens out,” Trump said Monday. “And then who knows, maybe we won’t have to put them on because there will be so much peace.”

The war has created an opportunity for Russia to make gains in Ukraine, as hostilities draw the global spotlight away from Kyiv and its struggle to hold back the bigger Russian army. U.S.-brokered talks between the two adversaries have been sidelined as Washington shifts focus to its war in Iran.

As Russia enjoys economic gains from the war-fueled energy crisis in the Middle East, Russian President Vladimir Putin has been gathering forces for a renewed offensive in eastern Ukraine.

Key air defense systems have already been diverted from Ukraine to the Persian Gulf, and Ukrainian President Volodymyr Zelensky has dispatched drone interceptors to the region and ordered anti-drone experts to pivot from their war with Russia to help Western allies help intercept Iranian attacks.

“At the moment, the partners’ priority and all attention are focused on the situation around Iran,” Zelensky said on X. “We see that the Russians are now trying to manipulate the situation in the Middle East and the gulf region to the benefit of their aggression.”

Times staff writers Gavin J. Quinton and Michael Wilner, in Washington, D.C., contributed to this report, which also includes reporting from the Associated Press.

The World Health Organization has warned that “black rain” caused by Israeli strikes on Iran’s oil facilities could pose health risks, especially for children. Iranian authorities have advised residents stay indoors as fires and thick smoke worsen air quality.

International Energy Agency chief says talks aim to assess conditions as US-Israel war on Iran fuels global uncertainty.

Published On 10 Mar 202610 Mar 2026

Share

The International Energy Agency (IEA) is set to hold an emergency meeting to assess the situation in the Middle East as the US-Israeli war on Iran continues to roil global energy markets.

Fatih Birol, the agency’s executive director, said representatives of IEA member states would meet on Tuesday to assess “the current security of supply and market conditions” amid the conflict.

Recommended Stories

list of 3 itemsend of list

“I have convened an extraordinary meeting of IEA member governments, which will take place later today to assess the current security of supply and market conditions to inform a subsequent decision on whether to make emergency stocks of IEA countries available to the market,” Birol said.

This week, oil prices hit their highest levels since mid‑2022 amid concerns of prolonged shipping disruptions linked to the war and reduced output from some key producers in countries that have been targeted by retaliatory Iranian strikes.

While the market reversed late in the day on Monday, with benchmarks falling below $90 a barrel, uncertainty persists around how long the United States-Israel war will drag on.

The Strait of Hormuz, a critical Gulf waterway through which about one-fifth of the world’s oil supplies passes, has effectively been shut down as a result of the war.