Over the past two decades, China has quietly eclipsed the United States as the dominant trading partner in parts of Latin America.

But since taking office for a second term, United States President Donald Trump has pushed to reverse Beijing’s advance.

Recommended Stories

list of 3 itemsend of list

That includes through aggressive manoeuvres directed at China’s allies in the region.

Already, the Trump administration has stripped officials in Costa Rica, Panama and Chile of their US visas, reportedly due to their ties to China.

It has also threatened to take back the Panama Canal over allegations that Chinese operatives are running the waterway. And after invading Venezuela and abducting President Nicolas Maduro, the US forced the country to halt oil exports to China.

But on Saturday, Trump is taking a different approach, welcoming Latin American leaders to his Mar-a-Lago estate for an event dubbed the “Shield of the Americas” summit.

How he plans to persuade leaders to distance themselves from one of the region’s largest economic partners remains unclear.

But experts say the high-level meeting could signal that Washington is prepared to put concrete offers on the table.

Securing meaningful commitments from Latin American leaders will take more than a photo op and vague promises, according to Francisco Urdinez, an expert on regional relations with China at Chile’s Pontifical Catholic University.

Even among Trump’s allies, Urdinez believes significant economic incentives are required.

“What they’re really hoping is that Washington backs up the political alignment with tangible economic benefits,” he said.

‘Reinforcing the Donroe Doctrine’

Already, the White House has confirmed that nearly a dozen countries will be represented at the weekend summit.

They include conservative leaders from Argentina, Bolivia, Chile, Costa Rica, Ecuador, El Salvador, the Dominican Republic, Honduras, Panama, Paraguay, and Trinidad and Tobago.

Mexico and Brazil, the region’s largest economies, have been notably left out. Both are currently led by left-leaning governments.

In a post on social media, the Trump administration framed the event as a “historic meeting reinforcing the Donroe Doctrine”, the president’s plan for establishing US dominance over the Western Hemisphere.

Part of that strategy involves assembling a coalition of ideological allies in the region.

But rolling back Chinese influence in a region increasingly reliant on its economy will not be an easy feat, according to Gimena Sanchez, the Andes director at the Washington Office on Latin America (WOLA), a US-based research and advocacy group.

The US “is trying to get countries to agree that they’re not going to have China be one of their primary trading partners, and they really can’t at this point”, Sanchez said.

“For most countries, China is either their top, second or third trading partner.”

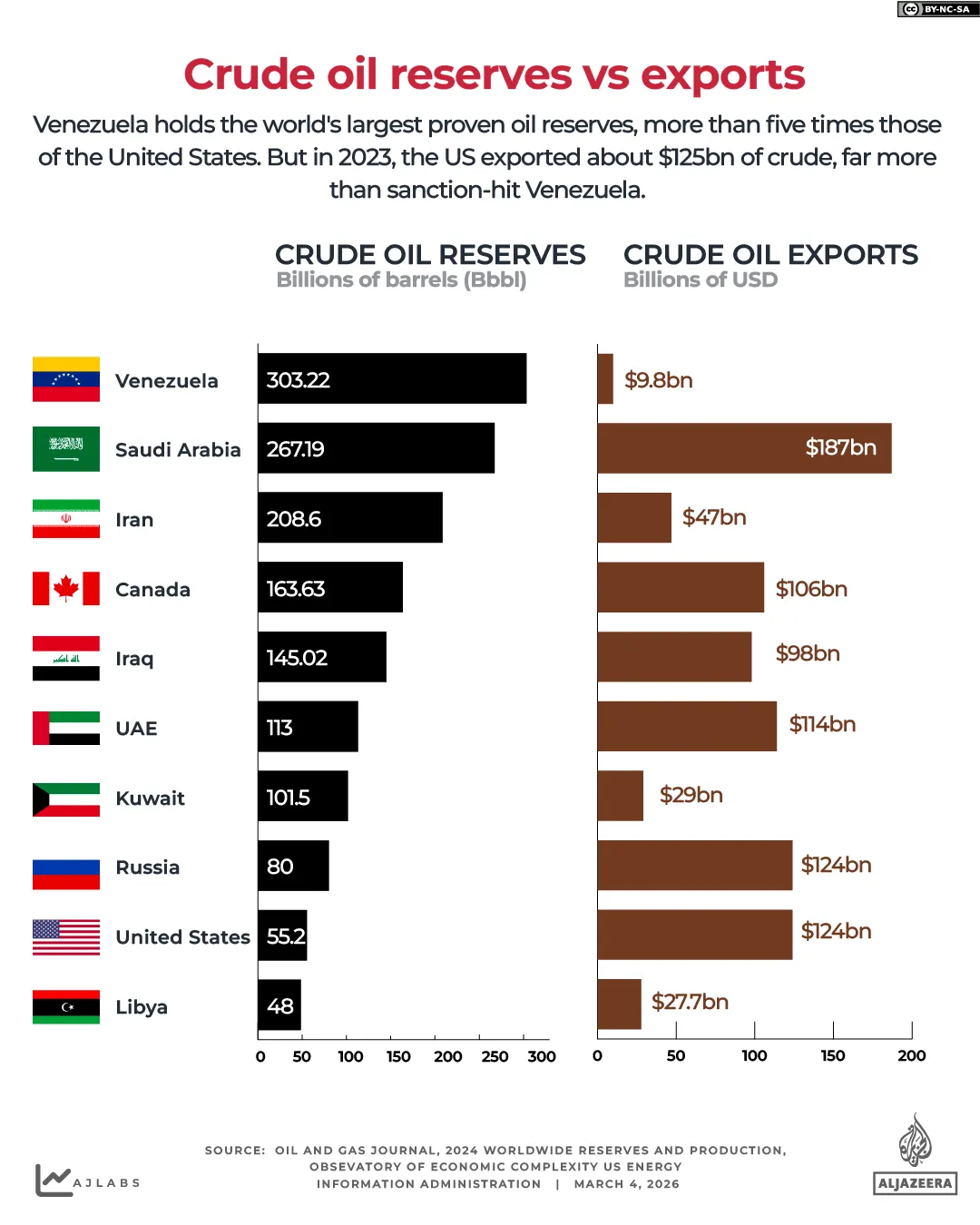

China, after all, has the second-largest economy in the world, and it has invested heavily in Latin America, including through infrastructure projects and massive loans.

The Asian giant has emerged as the top trading partner in South America in particular, with bilateral trade reaching $518bn in 2024, a record high for Beijing.

The US, however, remains the biggest outside trade force in Latin America and the Caribbean overall, due in large part to close relations with its neighbour, Mexico.

As of 2024, US imports from Latin America jumped to $661bn, and its exports were valued at $517bn.

Rather than choosing sides, though, many countries in the region are trying to strike a balance between the two powers, Sanchez explained.

Still, she added that the US cannot come empty-handed to this weekend’s negotiations.

“If the US is very boldly telling countries to cut off strengthening ties with China”, Sanchez emphasised that “the US is going to have to offer them something.”

What’s on the table?

Trump has already extended economic lifelines to Latin American governments politically aligned with his own.

In the case of Argentina, for instance, Trump announced in October a $20bn currency swap, meant to increase the value of the country’s peso.

He also increased the volume of Argentinian beef permitted to be imported into the US, shoring up the country’s agricultural sector, despite pushback from US cattle farmers.

Trump has largely tied those economic incentives to the continued leadership of political movements favourable to his own.

The $20bn swap, for instance, came ahead of a key election for Argentinian President Javier Milei’s right-wing party, which Trump supports.

Isolating China from resources in Latin America could also play to Trump’s advantage as he angles for better trade terms with Beijing.

A show of hemispheric solidarity could give Trump extra leverage as he travels to Beijing in early April to meet with Chinese President Xi Jinping, Urdinez pointed out.

Then there’s the regional security angle. The US has expressed particular concern about China’s control of strategic infrastructure in Latin America and the critical minerals it could exploit in the region to bolster its defence and technology capabilities.

Bolivia, Argentina and Chile, for instance, are believed to hold the world’s largest deposits of lithium, a metal necessary for energy storage and rechargeable batteries.

The Trump administration referenced such threats in its national security strategy, published in December.

“Some foreign influence will be hard to reverse,” the strategy document said, blaming the “political alignments between certain Latin American governments and certain foreign actors”.

But Trump’s security platform nevertheless asserted that Latin American leaders were actively seeking alternatives to China.

“Many governments are not ideologically aligned with foreign powers but are instead attracted to doing business with them for other reasons, including low costs and fewer regulatory hurdles,” the document said.

It argued that the US could combat Chinese influence by highlighting the “hidden costs” of close ties to Beijing, including “debt traps” and espionage.

‘More aspiration than reality’

Henrietta Levin, a senior fellow at the Center for Strategic and International Studies in Washington, believes that many Latin American countries would prefer to deepen economic engagement with the US over China.

But in many cases, that hasn’t been an option.

She pointed to Ecuador’s decision to sign a free trade agreement (FTA) with China in 2023 after it failed to negotiate a similar agreement with the US under President Joe Biden.

Some US politicians had opposed the deal as a threat to domestic industries. Others had encouraged Biden to reject it due to alleged corruption in Ecuador’s government.

Critics, though, said the resistance pushed Ecuador into closer relations with China.

“ When Ecuador signed their free trade agreement with China a couple years ago, their leader actually made quite clear that they had wanted an FTA with the US and would’ve preferred that,” said Levin.

“But the US didn’t want to negotiate such an agreement, and China did.”

As a result, Ecuador became the fifth country in Latin America to ink a free trade pact with China, after Chile, Peru, Costa Rica and Nicaragua.

For Levin, the question looming over this weekend’s summit is whether the Trump administration will step up and provide alternatives to the economic engagement China has already delivered.

Options could include trade agreements, financing for new development and investments with attractive terms.

But without such offers, Urdinez, the Chilean professor, warns that Trump will face limits to his ambitions of checking China’s growth in Latin America.

“Until Washington is willing to fill the economic space it’s asking countries to vacate, the rollback strategy will remain more aspiration than reality,” said Urdinez.

![A customer pays for groceries using bank account transactions [Ola al-Asi/ Al Jazeera]](https://i0.wp.com/www.aljazeera.com/wp-content/uploads/2026/02/When-money-is-scarce-every-choice-counts-bank-cash-or-on-credit.-1772105832.jpg?w=640&ssl=1)

![Abdallah Sukkar, owner of a street grocery stall, writing down customers' details in a notebook [Ola al-Asi/ Al Jazeera]](https://i0.wp.com/www.aljazeera.com/wp-content/uploads/2026/02/When-money-is-scarce-every-choice-counts-bank-cash-or-on-credit-2-1772105835.jpg?w=640&ssl=1)

![People purchasing goods at a grocery shop at Al-Zawya market [Ola al-Asi/ Al Jazeera]](https://i0.wp.com/www.aljazeera.com/wp-content/uploads/2026/02/When-money-is-scarce-every-choice-counts-bank-cash-or-on-credit.-1772105810.jpg?w=640&ssl=1)