The prime minister has given a heavy hint that there will be an extra bank holiday if England win the World Cup.

Thomas Tuchel’s team will play Norway in the quarter-finals on Saturday night.

The final will take place a week on Sunday, on 19 July.

It is widely expected Sir Keir Starmer will step down as prime minister the day after, to be replaced by Andy Burnham.

Should England make the final, it would be likely the prime minister would go to the game, which could briefly delay the handover of power.

As for the idea of an extra day off for people in England were the team to win the World Cup, Sir Keir said: “On the question of a bank holiday, I think I don’t want to jinx it, but ask me again if we get to the final.”

It is understood the extra bank holiday would be on the Friday following England’s triumph – 24 July.

There is, though, the not insignificant matter of England winning a quarter-final, semi-final and final first.

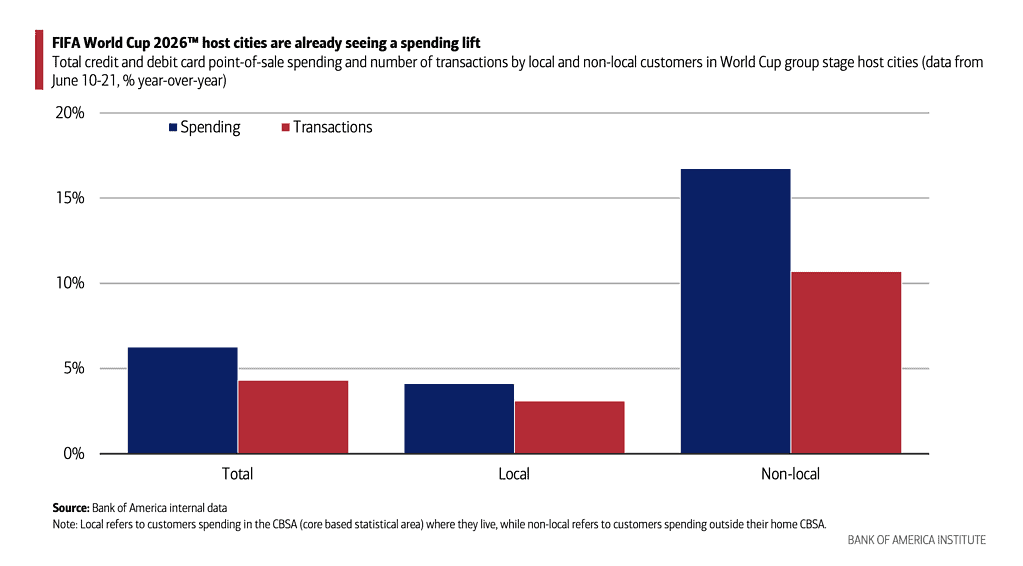

As World Cup spending surges, BofA’s year-long merchant preparation is paying off.

Exorbitant ticket prices be damned. Die-hard soccer fans are flocking to host cities across the U.S., Canada, and Mexico for the first tri-nation tournament in FIFA history. And they are proving to be exceptionally big spenders.

The Bank of America Institute — the firm’s research arm — mined its credit and debit card data and learned that the 2026 FIFA World Cup is delivering a massive economic win for host cities, driven overwhelmingly by these hefty-spending, out-of-town visitors.

During the tournament’s opening days from June 10–21, overall consumer spending in host markets jumped 6.3% year over year. “Non-local” cardholders — a category tracking both international tourists and U.S. residents traveling out of state for matches — fueled the lift. Their spending, according to data shared with Global Finance, climbed 16.7% year over year.

Bank of America’s data also highlighted a lucrative trend for local merchants: visiting fans are out-purchasing non-fans by a nearly 3-to-1 margin.

Pre-Tournament Warmup

“We’re really only halfway through, as you know, so no surprise that the majority of that spend has been driven from non-local residents coming in,” said Sara Walsh, a Bank of America managing director who oversees the bank’s relationships with vendors and networks in payments and has spent more than a year preparing merchants for the tournament. “Restaurants, bars, hotels, of course, make up the majority of that.”

The data tracks with results from last year’s FIFA Club World Cup, a smaller-scale tournament that Bank of America Institute found drove a 7% year-over-year rise in consumer spending in host zip codes. Walsh told Global Finance in a phone interview that the event effectively served as a dry run for the numbers the bank is now seeing at scale.

“The Club World Cup gave us a nice little pilot into what the stats would look like, and they were very consistent with what we’re seeing here,” Walsh said.

Soccer fans, meanwhile, are proving to be especially heavy spenders. A study Bank of America conducted with Visa found that soccer fans spend on average 2.8 times more than non-fans, according to the Institute. Walsh said the bank analyzed customers making purchases tied to FIFA and MLS tickets to reach that conclusion.

The scale of the opportunity is significant. The tournament’s 16 U.S., Mexican and Canadian host cities together represent:

$11 trillion in gross domestic product (GDP)

Roughly 130 million people, and

An expected draw of 33 million international visitors annually.

Historically, host nations have seen an average 0.4 percentage-point lift in GDP growth in the year following the tournament, the Institute found.

A Year of Preparation

Sara Walsh, Bank of America

Bank of America began preparing merchants for the World Cup surge more than a year ago. It drew on its position spanning treasury, card-issuing and merchant-services clients. The prep work centered on three areas: building tools for merchants to capture customer data and loyalty even after fans leave the U.S.; speeding up checkout through contactless and pay-at-table technology; and ensuring cards from international networks, such as Japan’s JCB, are accepted without triggering declines.

“Merchants can either survive the World Cup or prosper from the World Cup,” Walsh said, citing a colleague’s framing of the stakes.

Restaurants and bars needed the most hand-holding, Walsh said, particularly around pay-at-table functionality that’s common internationally but was slower to catch on in the U.S. The bank also coached retailers on when to use 3D Secure authentication — the phone-based verification step common in Europe — given the risk of transaction friction in crowded, high-traffic settings with spotty connectivity.

“We did not want to have customers who are standing in line, they’ve come all this way, get ready to purchase, and have their cards decline,” Walsh said. So far, she said, cross-border approval rates have held up as fans travel from city to city.

Spillover Into Other Events

One surprise for the bank has been spending spillover into unrelated events and sectors. Walsh said Bank of America has seen international visitors attending Major League Baseball games and concerts during their trips, alongside a pickup in merchandise sales tied to breakout national teams.

“You’re going to have people who are purchasing things from some of these teams that maybe a month ago no one had ever even heard of these countries, and all of a sudden they’re winning,” Walsh said, adding that merchandise sales represent a “fun kickback” opportunity for merchants tied to Cinderella-story squads.

Cape Verde’s inspiring World Cup run, for example, captivated fans. The team, representing an island nation of just 535,000, reached the knockout stage unbeaten and pushed Argentina, the reigning champs, to a hard-fought 3-2 extra-time loss.

Bank of America worked with Visa and FIFA, along with industry forums including Money20/20, the Electronic Transactions Association, and the Merchant Advisory Group, to prepare merchants of all sizes through its Merchant Engagement Program, Walsh said.

Looking ahead, Walsh said that the bank plans to apply lessons from the World Cup to future events on U.S. soil. That includes the 2028 Summer Olympics in Los Angeles and the 2031 FIFA Women’s World Cup, which the U.S. will jointly host with Mexico, Costa Rica, and Jamaica.

“We will definitely continue to use these events for learning opportunities to improve where we need to and get ready for those events as well,” she added.

Anthony Noto covers corporate finance and private credit. Contact him at anoto@gfmag.com

Videos show Israeli settlers, protected by Israeli soldiers, trying to seize a house under construction on the outskirts of the town of Qabalan, just south of Nablus, in the occupied West Bank.

Bethlehem, occupied West Bank – In the narrow alleyways of the Dheisheh refugee camp, three children debate which of their encounters with the Israeli military is worth telling, and who gets to tell it.

Yanal, 14, wins the opening round on language skills alone. He speaks three languages: Arabic, English and Spanish, and insists on telling his story in English.

Recommended Stories

list of 3 itemsend of list

“Life in the camp is complex,” he says, because, as he explains, there is nowhere to run away to when the army comes.

Yanal keeps returning to one memory: a football match, soldiers entering the field, and there being no way out.

Mustafa Abu Aliyah, 13, counters with a raid that he ran into as he was on his way to his grandfather’s house. The Israeli army fired live rounds and tear gas, he says. “We were in the middle of the fire.”

He can’t remember his first encounter with soldiers, “but I definitely saw them when I was little, because they are always coming here”.

His sister Diyar, 12, was mid-piano lesson the last time the army came through.

“Whenever the army comes, there will be tear gas,” she says. “People will be beaten. There’s usually someone injured or killed.”

She compares it to life elsewhere. “I see children in other countries, in other worlds, living in safety, but we can’t even leave our front door without suffering.”

The raids happen so often that the children often can’t remember the dates of specific incidents. But what they do remember is the fear they experienced and the aggression displayed by the Israeli soldiers.

In the first nine months of 2025 alone, Israeli forces carried out nearly 7,500 raids across the occupied West Bank, or about 27 a day, and a 37 percent increase compared with the same period in 2024.

‘Essence of childhood destroyed’

The children in the Dheisheh refugee camp reflect a wider pattern of childhood experiences under Israeli occupation, set out in a report the UN’s Independent International Commission of Inquiry on the Occupied Palestinian Territory released on Tuesday.

It examines Israel’s treatment of Palestinian children in Gaza and the occupied West Bank since October 2023.

Titled, “The essence of childhood has been destroyed”, it found that Israeli forces have killed at least 20,179 Palestinian children and wounded more than 44,000 across the occupied territory, most of them in Gaza – where it said that the deliberate targeting of children constituted part of the genocide in the Palestinian territory.

The report also documents a pattern of killings, mass arrests, torture, sexual violence and attacks on schools and hospitals.

In the West Bank, it records a sharp rise in settler violence against children and killings by Israeli forces, among them a two-year-old girl shot dead in January 2025. Children, the report notes, are held in Israeli detention, with no lawyer and no word sent to their parents, a separation it says can amount to enforced disappearance. Schools, too, are targets: 85 across the West Bank are under demolition or stop-work orders, and others have been closed or attacked by soldiers and settlers.

Mustafa Abu Aliyah, 13, and his sister Diyar, 12, sit in the alleyways of Dheisheh refugee camp in the occupied West Bank [Leila Warah/Al Jazeera].

Beyond the casualty count

The UN commission argues that Israel has created conditions in which Palestinians live in a constant state of “diffused, ambient terror, that does not require constant bombing to remain effective”.

“We are talking about repeated shocks, about continuous events that never end,” says Lemis Farraj, a psychologist and the project coordinator at Shorouq in Dheisheh, emphasising that a child’s physical and mental health cannot be separated from each other.

The report calls this continuous traumatic stress, distinct from Post-Traumatic Stress Disorder (PTSD), because there is no single event to recover from. The danger does not just come from experiencing one raid, but from the fear that comes with waiting for the expected raids that will likely come in the future.

Diyar explains that when the army enters her neighbourhood, she has to stay home and wait, no matter what her plans were. “Our life stops,” she says.

Her brother, Mustafa, says that the repetition has worn the fear flat.

“When I see the army, I [am] used to it and I stop being afraid.”

Farraj sees the same in the young children she treats: a startle at an ordinary sound, certainty that a raid has begun, and regression – skills already learned suddenly lost again.

Five-year-old Khour Hammad, who lives a few alleys away from the older children, has experienced the same raids.

She explains that both of her parents are in prison. Israeli forces arrested her father in July 2023 and her mother last March, according to the family.

Khour remembers the night the army came for her mother. Half-asleep, she heard a man’s voice and thought her father had finally come home. She climbed out of bed expecting him. Instead, she found soldiers inside the house.

The soldiers tried to question Khour. She says that she “felt like I was going to throw up”.

Handed an old family photo, she brightens at once, pointing out her mother, Islam Amarna, and her father, Osama Hammad, and rattling off memories in bursts.

Khour Hammad, 5, stands on a rooftop overlooking Dheisheh refugee camp in Bethlehem, in the occupied West Bank. Both of her parents have been arrested by Israeli forces [Leila Warah/Al Jazeera].

Generational trauma

While Palestinian children in Gaza and the West Bank face different lived experiences, the UN finds the same cause behind the harm: a military occupation described as a “long-term mechanism of domination, subjugation and oppression”.

Farraj adds that children are affected not only by their own experiences of trauma, but also by what is passed down from parents and grandparents.

“The first generation of the Nakba lived in shock and passed it on to their children,” she says, referring to the ethnic cleansing of at least 750,000 Palestinians following the formation of the state of Israel in 1948.

The report similarly notes that Palestinian refugees, now in their fifth generation, have internalised a sense of “dispossession from the Nakba” alongside present-day experiences of occupation.

In the West Bank, roughly one in four Palestinians are refugees; in Gaza, it is about 70 percent.

Israeli violence and forcible displacement have been carried through generations of Palestinians, compounding as the cycle repeats. Farraj says trauma recovery depends on stability: family support, schooling, safe spaces and a predictable routine, all of which remain precarious under Israel’s occupation.

For Khour, that stability begins with her parents.

“I want the whole world to listen and see my picture,” Khour says, “and get my mom and dad out of prison.”

Israel is pushing humanitarian groups and rights defenders to scale down operations in Palestinian territories.

Published On 22 Jun 202622 Jun 2026

Children are “increasingly unprotected” as humanitarian groups and rights defenders are forced to scale back their operations in the Palestinian territories, the United Nations has warned.

Many civil society and aid organisations in Gaza and the West Bank have been labelled “terrorists” by pro-Israel groups or politicians, the UN Committee on the Rights of the Child warned in a statement issued on Monday, noting that their absence leaves children vulnerable.

Recommended Stories

list of 4 itemsend of list

“For more than three decades, these organisations have played a vital role in defending Palestinian children, including in the Israeli military courts, and in documenting grave violations against Palestinian children at the hands of Israeli forces,” the committee said.

“Without them, Palestinian children will be even less protected, and violations of their rights risk continuing with impunity,” it added.

Issued by the Office of the United Nations High Commissioner for Human Rights (OHCHR), the statement noted that tactics used to delegitimise these human rights groups also include “military raids, travel bans, personal financial sanctions, threats of arrest, destruction of records, and even threats of secondary sanctions against partners who support their work”.

The committee said this made it “increasingly impossible for these organisations to operate safely or protect the children and families who turn to them for help”.

The committee urged the international community to hold Israeli authorities accountable for the attacks committed against Palestinian human rights defenders.

It urged the Israeli authorities to lift the restrictions faced by humanitarian individuals and groups.

“Despite grave risks and limited resources, child rights defenders have continued to stand with Palestinian children and families in extraordinarily dangerous conditions. They must be protected, not punished,” the committee said.

Israel has cracked down significantly on humanitarian operations in Gaza since the “ceasefire” that began on October 10, banning Doctors Without Borders, known by its French acronym MSF, after it failed to provide a list of its Palestinian staff, further depriving Palestinians in the besieged enclave of life-saving assistance.

In February this year, 17 international aid groups petitioned Israel’s Supreme Court to be allowed to keep working in the Gaza Strip and other areas in the occupied Palestinian territory. The Israeli government has planned to halt their life-saving work.

The occupied West Bank has seen sustained and rising violence amid ongoing conflict between Israelis and Palestinians. Israeli forces conduct frequent raids in Palestinian areas, saying they are targeting militants and preventing attacks, while Palestinians and rights groups accuse the military of using excessive force and say settlement expansion is a major driver of instability. Israeli settlements in the territory are widely considered illegal under international law by the United Nations and most countries, though Israel disputes this and views the West Bank as disputed land with historical and security significance. In recent months, tensions have further escalated with increased restrictions on Palestinian movement near settlements, alongside a rise in attacks by both Palestinians against Israelis and by settlers against Palestinians, contributing to a cycle of violence that continues to claim lives on both sides.

Fatal Shooting Near Beit Ummar

The incident took place near the town of Beit Ummar in the southern West Bank.

Palestinian news agency WAFA identified the victims as teenagers aged 15 and 19. A relative confirmed their ages to Reuters.

Israeli Military’s Account

The Israeli military said its forces confronted three individuals who were throwing fire bombs and burning tyres near the settlement of Karmei Tzur.

According to the military, soldiers opened fire, killing two of the individuals and wounding a third.

Reuters could not independently verify the military’s account.

Third Teenager Hospitalized

WAFA reported that the third person involved in the incident was hospitalized in stable condition.

The Palestinian Red Crescent Society said the wounded individual is 15 years old.

Tensions Remain High in the West Bank

Israeli forces regularly conduct raids across the occupied West Bank and have tightened movement restrictions around Palestinian communities located near Israeli settlements in recent months.

The territory has experienced heightened tensions amid ongoing violence involving Israeli security forces, settlers and Palestinians.

Dispute Over Settlements

The international community, including the United Nations and most countries, considers Israeli settlements in the West Bank illegal under international law and a major obstacle to the creation of a Palestinian state.

Israel rejects that position, describing the territory as disputed and citing historical Jewish ties to the area.

Rising Violence

According to United Nations data, at least 57 Palestinians have been killed this year in incidents involving Israeli settlers and security forces.

At the same time, Palestinians have carried out attacks against Israeli soldiers and settlers in the West Bank, including at least one fatal attack in 2026, according to Israel’s Shin Bet domestic security service.

What’s Next

The Israeli military is expected to continue reviewing the circumstances of the shooting, including whether the individuals posed an immediate threat and how the confrontation unfolded near the settlement.

Palestinian officials are likely to pursue diplomatic and legal avenues, as similar incidents in the West Bank are often raised with international bodies, including the United Nations, amid ongoing disputes over the use of force by Israeli troops.

On the ground, the incident is likely to add to already high tensions in the West Bank, where Israeli raids, settlement activity, and Palestinian attacks have contributed to a cycle of violence in recent months.

Further clashes cannot be ruled out, particularly in areas close to settlements where movement restrictions and security operations have intensified.

International attention on West Bank violence is also likely to continue, especially as reported fatalities involving Palestinians and Israelis have remained elevated this year, keeping pressure on both sides amid an already fragile security situation.

The Bank of England left its benchmark interest rate unchanged at 3.75% on Thursday, extending a pause that began in December 2025, as policymakers weighed the inflationary fallout from the Iran war against signs of resilience elsewhere in the economy.

ADVERTISEMENT

ADVERTISEMENT

Governor Andrew Bailey and fellow Monetary Policy Committee members were widely expected to keep rates on hold and maintain a broadly neutral stance on future policy moves.

The decision came a day after official figures showed UK inflation holding steady. Consumer prices rose 2.8% year-on-year in May, unchanged from April and below economists’ expectations of 3.0%, leaving the headline rate at its lowest level since early 2025.

However, the stable reading masked diverging trends beneath the surface. Transport costs accelerated sharply to 6.8%, driven by higher fuel prices and rising air fares, while food inflation eased to 2.2% and housing costs continued to moderate.

Though inflation remains above the bank’s target of 2%, the figure raised hopes that the upward pressure on prices emanating from the spike in oil and gas prices after the start of the Iran war on 28 February may have been less than anticipated.

Andrew Bailey, the bank’s governor, said the recent fall in oil prices has been “encouraging” while noting they are still higher than before the war.

“Whatever happens in the future, the higher energy prices of the past four months mean there’s already some inflationary pressure in the pipeline,” he said. “The Bank’s job is to make sure that doesn’t turn into sustained inflation above our 2% target.”

Analysts also cautioned that inflation could still accelerate later this year, as higher household energy bills feed through to prices. Lindsay James, investment strategist at Quilter, said: “Whilst inflation was below expectations in May and currently under 3%, it is still likely to jump closer to 4% later in the year due to the coming impact of a higher energy price cap.”

James added that while oil prices have retreated from recent highs, they remain above last year’s levels, suggesting underlying inflation pressures have not fully disappeared.

The decision to hold the key interest rate was not unanimous, with two of the nine Monetary Policy Committee members voting for a quarter-point rate increase, reflecting concerns that higher energy costs could still feed through into broader inflation pressures.

A labour market losing momentum

Thursday’s labour market release painted a mixed picture.

The unemployment rate dipped unexpectedly to 4.9% in the three months to April, down from 5.0% in the first quarter, yet payrolled employee numbers fell over the period, pointing to an underlying loss of momentum even as the headline jobless rate improved.

Wage growth, a metric the Bank of England watches closely for signs of persistent price pressure, held firm, with regular pay excluding bonuses rising 3.4% on the year.

“The labour market is still continuing to lose momentum, with the latest figures showing a further cooling,” stated Richard Carter, head of fixed interest research at Quilter Cheviot.

Sanjay Raja, chief UK economist at Deutsche Bank, struck a similar note, cautioning that “it’s clear that the labour market is not out of the woods yet,” though he added that the mixed data buys the committee more time to wait and see how the economy evolves.

The combination of cooling headline inflation, a softening jobs market and still-robust pay growth underscores the bind facing the committee. Strong earnings keep alive the risk of so-called second-round effects, where higher wages feed back into prices, even as hiring loses steam.

Israeli settlers have vandalised and burned a mosque in the occupied West Bank village of Jaljulia, north of Ramallah. Racist slogans were scrawled on the walls by the settlers.

The central bank’s increase in the uncollateralised overnight rate, by a quarter of a percentage point from 0.75%, puts it at a three-decade high.

ADVERTISEMENT

ADVERTISEMENT

The Bank of Japan has been trying to normalise monetary policy lately after decades of keeping interest rates near or below zero. It adopted ultralow rates to try to encourage more borrowing and spending to counter deflation and pull the economy out of the doldrums.

Inflationary pressures because of the war in Iran, which has sent oil prices soaring in recent months, have hit Japan hard since it imports almost all its oil and gas.

Low interest rates had added to pressures on the Japanese yen, which has fallen lately to about 160 yen to the US dollar.

BOJ Gov. Kazuo Ueda, who has been hospitalised recently, did not attend Tuesday’s policy board meeting. Deputy Gov. Shinichi Uchida was expected to take his place at the news conference set for later in the day.

Before the BOJ decision, Tokyo’s benchmark Nikkei 225 index briefly topped 70,000 early Tuesday before giving up some of those early gains.

Tyra Banks has filed a defamation lawsuit against Netflix and the directors of “Reality Check: Inside America’s Next Top Model” claiming that she was manipulated and misrepresented in the series.

The three-part documentary, directed by married duo Mor Loushy and Daniel Sivan, revisited the reality show’s rise and many controversies, including former contestant Shandi Sullivan discussing what she described as a blackout sexual encounter that took place during Cycle 2 of the series and was a major plot point because Sullivan was in a relationship.

Sullivan said in “Reality Check” that she felt like producers should have stepped in considering she was heavily intoxicated, but instead they followed her into the bathroom and bedroom to record a sexual encounter with a male model. In a following scene, Banks lectures Sullivan about cheating and “carnal” temptation.

“Tyra Banks participated in the Netflix documentary series about ‘America’s Next Top Model’ because she believed viewers deserved a candid conversation about the show’s legacy — its successes and its shortcomings,” reads the lawsuit. “There are aspects of the show for which Ms. Banks takes accountability and she wanted ANTM viewers to hear that from her directly.”

The lawsuit, filed on Saturday in the Central District of California, claims that the supermodel turned media personality participated in a 3½-hour interview, of which about 16 minutes was used.

“The producers used what could be stripped of context and reassembled to support a false and defamatory narrative unrelated to what she actually expressed,” reads the suit. “The accountability Banks took ended up on the cutting room floor.”

The suit alleges that producers used “selective editing, deliberate omission and surgical manipulation of continuous footage” to create a false narrative that Banks “knowingly allowed a contestant to be sexually assaulted on her show, exploited that contestant’s trauma for ratings, and then could not even remember it when asked.”

Banks claims that she asked Netflix and the producers of the docuseries for access to the unedited footage of her 3½-hour interview, and proposed they work together to “correct the record.”

“Had they agreed, Ms. Banks could have made the truth public and this litigation would likely have been unnecessary,” reads the suit.

According to the suit, Banks was pitched the docuseries as a “definitive three-hour Netflix docuseries exploring America’s Next Top Model as a groundbreaking popculture phenomenon.” The pitch had a Netflix logo on its cover, and Banks had “long trusted and admired Netflix.” The streamer’s involvement was the reason Banks claims she considered the project.

Banks claims the pitch included promises that the documentary would unpack the show’s legacy “not as a takedown, but as a thoughtful in-depth reflection on its influence, evolution, and impact on fashion, television, and culture.”

The suit claims Banks was prepared for a fair comeuppance, but ultimately the former supermodel felt hoodwinked. “Nothing suggested that the project would falsely accuse Ms. Banks of covering up a sexual assault, or being indifferent to what a contestant characterizes as a traumatic experience.”

In February, directors for “Reality Check” revealed that Banks wasn’t invited to participate in the docuseries until well after production began

“It was like, ‘Hey, this can be a great addition, but definitely not a necessity,’” Sivan said. “People talking trash about her is very easy to find. … But having her passion, bringing this program to life, is something that only she could tell.”

Sivan and Loushy, who also helmed the acclaimed 2025 docuseries “American Manhunt: Osama bin Laden,” said they treated “Reality Check” with the same level of care as previous heavyweight projects.

“There were things that were sensitive and important for me,” Loushy said, from the harassment that she said “ANTM” contestants endured to the insecurities that “to us as women, are sitting tight and hard every day on our heart.”

The directing duo hoped to examine the good intentions Banks and producers had, of turning the fashion industry on its head, empowering women and championing diversity, and the way those intentions evolved as the show moved through cycles.

“At the end of the day, was it a force of good, or was it a force of evil? I hope people keep debating that,” Sivan said.

Former Times staff writer Malia Mendez contributed to this report.

Both Amnesty International and Oxfam released reports this week documenting a rise in state-backed Israeli settler violence across the occupied West Bank over the past three years. What’s driving the escalation? Al Jazeera’s Marah Rayan breaks it down.

Bank of Korea Gov. Shin Hyun-song delivers a speech during an international conference at the central bank in Seoul, South Korea, 01 June 2026. Photo by YONHAP / EPA

June 11 (Asia Today) — South Korea is facing widening gaps in both wealth and income, with young people and those without homes losing ground economically, Bank of Korea researchers said Wednesday.

The central bank’s research department made the assessment in a report titled “Household Polarization in the Korean Economy and Its Spillover Effects.” The report said South Korea is confronting a form of dual polarization as asset and income inequality expand at the same time.

According to the report, South Korea’s net wealth Gini coefficient fell to 0.584 in 2017 but has since risen, reaching 0.625 last year. A Gini coefficient closer to zero indicates greater equality, while a figure closer to one indicates greater inequality.

The report identified rising real estate prices as a key factor behind the widening asset gap. It said higher property prices have played a central role in explaining movements in wealth inequality.

The Bank of Korea researchers also said real estate assets are concentrated among older generations, making wealth inequality between generations more structural.

The conditions for young people to build assets have deteriorated, the report said. An increasing number of young people earn relatively high incomes but cannot enter the upper wealth bracket because they do not own real estate.

The report said the mobility that once allowed people with middle- to upper-level incomes to move into the top wealth group has weakened, undercutting the asset-building ladder for younger households.

Income inequality also shows signs of widening again. The disposable income Gini coefficient fell from 0.353 in 2016 to 0.323 in 2023 but rose slightly to 0.325 in 2024.

The report said income inequality, which had improved through redistribution policies, could widen again because of K-shaped growth across industries.

Researchers identified the gap between the information technology sector and non-IT industries as a driver of income polarization. In the IT sector, wages have risen sharply, led in part by bonuses, while wage growth has been limited in other industries.

The spread of artificial intelligence could further deepen income gaps, the report said. Researchers said AI technology, combined with advances in robotics, could replace jobs held by low-income workers and young people in the early stages of their careers.

A Bank of Korea survey on AI also found that people in lower income brackets were more likely to believe their jobs could be replaced by AI.

The impact of dual polarization is especially visible among young people. The share of people in their 20s and 30s among households in the bottom quintile for both net wealth and income rose from 7.9% in 2020 to 15.2% in 2025.

The report said this suggests young people without homes are increasingly being pushed into lower economic groups.

The Bank of Korea researchers warned that dual polarization could weaken productivity and consumer vitality across the economy.

An analysis using data from 120 countries found that when the share of wealth held by the top 10% rises by 1 percentage point, total factor productivity falls by 0.16% two years later.

In South Korea, the share of net wealth held by the top 10% increased from 43.0% in 2022 to 46.1% in 2025, up 3.1 percentage points. Researchers said widening wealth inequality could become a constraint on economic growth and productivity improvement.

The social costs could also increase. The report said widening wealth and income gaps may lower expectations for upward mobility, weaken work incentives and reduce social trust.

It also warned that high housing costs for young people could become a barrier to marriage and childbirth.

The researchers said redistribution policies focused mainly on income support are not enough to respond to dual polarization. They said South Korea needs to guide household assets, which are heavily concentrated in real estate, toward more productive sectors and expand opportunities to build productive assets.

The report also called for a more stable tax base in response to economic changes driven by technological development. It said institutions should be reviewed to ensure that the path from labor income to asset formation does not deteriorate further.

Researchers also said South Korea must strengthen new growth industries so the benefits of economic growth can spread more widely across the economy.

Israel continues to expand settlements in the occupied territory, which are illegal under international law.

Published On 11 Jun 202611 Jun 2026

The Israeli government has allocated a first tranche of an expected $388m in new funds for the construction of settlements in the occupied West Bank.

The anti-settlement group Peace Now reported on Thursday that the government had allocated 152 million shekels ($51m) to prepare construction plans for 69 illegal settlements and outposts in the occupied West Bank.

Recommended Stories

list of 3 itemsend of list

The cabinet later reportedly postponed a decision about a 1-billion-shekel ($338m) allocation. That proposal, if passed, would mark one of the largest expansions of illegal Israeli settlements in decades.

“The government decided to postpone the decision [on the 1-billion-shekel allocation] and refer it to the Security Cabinet which is expected to convene on Sunday,” Peace Now wrote.

Under the yet-to-be-approved plan, construction for the settlements, including infrastructure and public buildings, would begin despite necessary planning protocols not having been carried out in accord with Israeli law.

Peace Now accused the government of intending to bypass planning and construction regulations.

“October 7 proved that the right-wing approach has failed: the conflict cannot be ‘managed,’ and the Palestinians cannot be ‘defeated’,” the group said in a statement.

“Israel must reach a political solution and diplomatic agreement, but instead the government is only sinking us deeper into the mire and condemning us to many more years of bloody conflict.”

Israel has come under growing condemnation for expanding settlements in the occupied West Bank, which are illegal under international law.

On Tuesday, the United Kingdom, Australia, New Zealand, Canada, France and Norway imposed sanctions on networks involved in financing, enabling and carrying out settler violence against Palestinians.

According to Peace Now, the current Israeli government has approved 103 settlements since it took office in December 2022. From that figure, 51 are entirely new settlements.

On Wednesday, Amnesty International published a report accusing the Israeli government of playing a central role in what it describes as the ethnic cleansing of Palestinians in the occupied West Bank. The report described the government’s actions as “integral”.

At least 117 villages in the West Bank have been subject to either complete or partial displacement due to settler attacks, according to the United Nations Office for the Coordination of Humanitarian Affairs (OCHA).

Amnesty also condemned the upcoming “Great Israeli Real Estate Event”, which is due to take place in London on Sunday.

The event, which has also been held in the United States and Canada, promotes the sale of properties in the occupied West Bank, which campaigners say is in violation of international law.

The Washington institution cut its global growth forecast by 0.4 percentage points to 2.5 percent, citing surging energy prices, inflation and borrowing costs.

Published On 11 Jun 202611 Jun 2026

The conflict in the Middle East is set to bring global economic growth to its slowest since the COVID-19 pandemic, the World Bank has warned.

In its latest Global Economic Prospects report, published on Thursday, the Washington-based institution cut its global growth forecast for 2026 to 2.5 percent from the 2.9 percent it had predicted in January, citing surging energy prices, rising inflation and higher borrowing costs.

Recommended Stories

list of 3 itemsend of list

The report highlights the significant economic costs of the conflict, which is at risk of flaring up again, as the fragile ceasefire between the United States and Iran is tested on both sides.

The analysis warns that the outlook could decline further if supply disruptions worsen. Iran’s closure of the Strait of Hormuz – a vital passageway for oil and gas transit – in response to the hostilities launched by the US and Israel has put huge stress upon global energy and other supply chains.

The World Bank estimates that Brent crude prices — the international oil benchmark — will average $94 a barrel this year, 36 percent above last year’s average. Fertiliser prices are forecast to increase significantly this year, with knock-on effects for food prices.

Overall, the closure of the strategic waterway will help to push global inflation to 4 percent this year, a substantial increase from last year’s rate of 3.3 percent.

However, the World Bank cautions that global growth could plummet to as low as 1.3 percent this year, should energy supply disruptions worsen, with inflation pushing to 4.4 percent.

The World Bank report also cautions that developing countries are on the front line of the potential impact.

In its report, the institution has downgraded its growth forecasts for two-thirds of countries since January. Global growth is expected to improve to 2.8 percent in 2027, but will remain 0.4 percentage points below the average during the 2010s, during which the world economy was recovering from the global financial crisis.

Excluding China and India, the report worries that developing countries have made little progress towards narrowing their per capita income gap with wealthy nations over the past decade.

“Developing countries have faced a series of challenges over the last decade,” said Ajay Banga, president of the World Bank Group. “The impact differs by country, but the basic test is the same: protect people and preserve stability today, without giving up on growth and jobs tomorrow.”

The World Bank is pledging to assist any developing country experiencing the economic fallout of the Middle East conflict. The organisation says it has set aside up to $60bn to help. It added that if the conflict persists, it can increase its support to $100bn.

Avios points are on offer(Image: imageBROKER/Chris Putnam via Getty Images)

A bank is tempting new customers with 10,000 Avios Points.

J.P Morgan Personal Investing confirmed the deal was running until July 31, 2026. The bank revealed customers could put their points towards flights at a time when concerns are mounting over potential fare increases.

The offer is open to new customers who invest £500 or more in a single payment before the end of July.

To qualify for the points, new clients must keep at least £500 invested from August 1, 2026, until February 1, 2027, after which the Avios will be awarded within 55 days of this holding period concluding. New clients can open a Stocks and Shares ISA, Junior ISA, Lifetime ISA, Personal Pension or General Investment Account.

New investors will need to complete the sign-up form, accessible via the promotional page. J.P Morgan reminded customers that their capital was at risk and that transfers in were excluded from the offer.

Claire Exley, head of advice and guidance at J.P. Morgan Personal Investing, said: “Many UK savers are curious about investing for the first time but unsure when to get started. Over the long term, it’s often more important to stay invested over several years than to try to time the market and pick the ‘perfect’ moment.

“For those thinking about starting to invest, our Avios offer is designed to help make that first step in investing feel a little more rewarding. With the cost of travel on many people’s minds, those Avios points could help towards a future holiday or bring a dream trip a bit closer.

“Whether you’re using a Stocks and Shares ISA for the first time, investing for your children, or topping up your pension, what often matters most is choosing an approach you’re comfortable with and staying invested for the long term.”

The Palestinian Authority condemned Israel’s decision to build 2,162 illegal settlement units in the occupied West Bank, calling for US intervention to halt the Israeli “madness.”

“All settlement activity is illegal under international law and does not confer legitimacy to anyone,” the authority said in a statement carried by the official news agency Wafa.

It said the Israeli decision constitutes a “blatant challenge to international law and UN resolutions,” particularly UN Security Council Resolution 2334, which affirms the illegality of the Israeli settlements in all occupied Palestinian territories, including East Jerusalem.

It held the Israeli authorities responsible for the “serious consequences” of the settlement policies, warning that they would push the region toward “further cycles of violence and escalation.”

The authority called on the US administration to intervene immediately “to stop the Israeli madness if it genuinely seeks to promote security and stability in the region and globally.”

It stressed that the Palestinian people would remain “steadfast on their land and committed to their legitimate national rights,” saying the illegal settlement plans would not deter them from continuing their struggle to establish an independent Palestinian state on the June 4, 1967 borders with East Jerusalem as its capital.

The statement came after Israel’s Higher Planning Council approved the construction of 2,162 new settlement units across several illegal settlements in the occupied West Bank.

The plans include 1,006 units in the Gevaot settlement within the Gush Etzion bloc south of Bethlehem, 922 units in the Har Brakha settlement south of Nablus, and 234 units in Kiryat Arba settlement built on land belonging to the city of Hebron.

Palestinians view the new plans as part of an accelerated Israeli policy aimed at expanding illegal settlements, confiscating Palestinian land and creating new facts on the ground.

A Palestinian father in Hebron has buried his seven-month-old son after the baby was killed by Israeli gunfire directed at the family’s car. The shooting, which also wounded the child’s parents, is the latest deadly incident amid escalating Israeli violence in the occupied West Bank.

A surveillance camera caught a brutal assault by an Israeli soldier and settlers on two young Palestinians in the occupied West Bank. Video shows them slamming the victims onto the ground and repeatedly beating them, including with a plank of wood, leaving them motionless on the ground.

Israeli forces reportedly killed a seven-month-old Palestinian baby, Sam Fahd Abu Haikal, and injured his parents in the Tel Rumeida area near Hebron on Friday evening, according to the Palestinian health ministry. The baby’s grandmother described how the family stopped their car after seeing Israeli military vehicles when shots were fired at them. She recounted that a bullet hit the baby in the face and lodged in his mother’s cheek, while also grazing the father’s finger. The parents were treated for their gunshot wounds.

The Israeli military stated that during operations in Hebron, soldiers fired shots at a vehicle they thought was approaching them quickly. They acknowledged that three Palestinians, later determined to be “uninvolved civilians,” were injured, and the incident is under investigation. Tel Rumeida has a history of violence as Israeli settlers live with military protection among the Palestinian community. Recent EU data indicates over 700,000 settlers reside in East Jerusalem and the West Bank while more than 3 million Palestinians live there.

When the European Union issued its latest tranche of sanctions against Israeli settler groups and their leaders, Regavim, founded in part by the country’s Finance Minister Bezalel Smotrich, these groups welcomed the measures as a “badge of honour.”

Another sanctioned figure, Daniella Weiss, whose movement, Nachala, has held conferences on the Gaza border to discuss plans for settlement expansion into the occupied Palestinian territory, likewise dismissed the European penalties as “ridiculous” and “banal”.

Recommended Stories

list of 4 itemsend of list

In total, the EU sanctioned four entities and three individuals associated with the settler movement, which includes high-profile characters such as Weiss, Regavim and its director, Meir Deutsch, and the Amana cooperative association, which offers logistical and financial support to settlements in the occupied West Bank.

Even government figures have been targeted in recent Western actions. Finance Minister Bezalel Smotrich, a son of the settler movement, was sanctioned by the United Kingdom, Canada and several other countries for his alleged role in supporting or enabling violence in the West Bank, highlighting how the settlement project has the support of the highest echelons of the Israeli state.

Overall, the nonchalant response from the targeted figures and entities suggests that none of the EU measures will do anything to stop settlement expansion or make individuals accountable for the growing wave of violence against Palestinians.

Ironically, the largely toothless measures might instead become a source of domestic prestige for their leaders, analysts say, as few would expect these hardline settler figures to spend their summers in Paris or London and thus be affected by the sanctions. Instead, a wave of terror in the occupied West Bank will likely continue, with the tacit support of the government.

Endemic violence

In the eyes of many activists and observers who spoke to Al Jazeera, the EU’s focus on group and individual “violations” falls far short of articulating the scale of the highly coordinated settler attacks or the extent to which the state and society support them.

Following the Hamas-led attack of October 2023, United Nations and human rights monitors have documented systemic lethal settler attacks in places such as the South Hebron Hills, where residents of villages like Susiya and Umm al-Khair have been killed or seriously injured in collective incursions.

In the northern West Bank, Palestinian residents of villages around Nablus and Ramallah have seen their homes, vehicles and olive groves torched during nighttime settler raids. Entire Bedouin herding communities in the Jordan Valley have also been forcibly displaced following sustained campaigns of intimidation and violence.

All of this underscores the depth and breadth of settler activity, which, according to people on the ground, has the direct support of the Israeli government.

“It’s gotten much worse since October 2023. They now have the courage to attack into the heart of densely populated Palestinian villages. I see them, they came into the heart of my village outside Ramallah, they feel safe to do so,” Tahseen Alayan, deputy director of Al-Haq, told Al Jazeera.

“If you buy a sheep, they will steal it. If you build a house, they will destroy it. If you buy a car, they will burn it.”

Daniella Weiss, founder of the Nachalot Association, described the EU sanctions as “ridiculous” and “banal” [Enes Canli/Anadolu Agency]

Examples of Israeli government complicity in these settler raids are not hard to find, and the statistics indicate collective efforts to entrench Israeli control over the West Bank, which has been occupied since 1967.

Israeli forces and settlers are accused of killing an estimated 1,168 people in the occupied West Bank since October 2023 and injuring a further 12,666 Palestinians. Another 33,000 people have been displaced, while Israel has also detained nearly 23,000 Palestinians in the West Bank during this period, many without charge.

“The violence does not happen in a vacuum,” Alayan continued. “This is an extension of the Israeli government; settlement is at the core of their identity. They are protected by the government and by the occupying services, and they freely admit it.”

A tragic incident that comes to mind is settler Yinon Levi, who allegedly shot dead Palestinian activist Awdah Hathaleen in Masafer Yatta last year. Despite the murder being captured on video, Levi nevertheless remains at large.

“Even if they are ever prosecuted, the sentences rarely reflect the severity of the crime,” Alayan said. “These people return to their homes and are seen as heroes.”

‘Entitlement and superiority’

This sense of impunity that settlers appear to be imbued with cannot be detached from the appointment to ministerial positions of leading figures or sympathisers of the settler movement – notably Ben-Gvir and Smotrich, the latter born in an illegal settlement in the occupied Golan Heights.

In a sign of state-settler cooperation to achieve direct control of the West Bank, in contravention of the Oslo Accords, Israel last year announced plans for the establishment of the E1 settlement that would link occupied East Jerusalem with its growing Maale Adumim bloc.

According to plans outlined by Smotrich, when established, this settlement would kill any hopes of the creation of a Palestinian state in the West Bank and Gaza and fulfil a biblical prophecy that many in the movement have been working towards.

Israeli far-right Finance Minister Bezalel Smotrich holds a map of an area near the settlement of Maale Adumim, a land corridor known as E1, outside Jerusalem in the occupied West Bank, on August 14, 2025, after a news conference at the site [Menahem Kahana/AFP]

Daniel Bar-Tal, a professor of social-political psychology from the Department of Education at Tel Aviv University, interpreted the thinking behind the settlers leading this violence across the West Bank.

“It is divine order to settle West Bank. With divine order you do not argue but achieve it in the way Yehoshua carried it 3,000 years ago when he entered the promised land,” he explained. “He achieved it with sword, so we need to do the same.”

Shai Parnes of the Israeli human rights group B’Tselem told Al Jazeera that the absence of international pressure has bolstered the alliance between the state and settler movement.

“The Israeli regime is an apartheid regime based on Jewish supremacy and institutionalised discrimination against Palestinians,” Parnes told Al Jazeera.

“Any Israeli, civilian or soldier, who harms a Palestinian receives full immunity and support from the Israeli systems, and Israel itself receives this from the international community. These facts explain the Israelis’ sense of entitlement and superiority.”

Palestinian Nazem Saleh Shoman stands inside a pen at a sheep farm that was set on fire the previous night by Israeli settlers in the Palestinian village of Khirbet Abu Falah in the central occupied West Bank [AFP]

Yehouda Shenhav-Shahrabani, one of Israel’s leading sociologists, described the channelling of “Jewish supremacy” from the individual to the group, to the state, and back again, as a “closed loop”.

This, he said, fosters a sense of superiority among individuals, and when combined with a militarised society, makes violence against the native Palestinian population, who are in the way of realising this supposed biblical prophecy, almost inevitable.

“Some believe they’re in the West Bank because God said it was theirs. Others are there because they’re too poor to be anywhere else, and have been told they’re superior anyway,” he said.

“Two-thirds of the time, these same people are soldiers. They carry guns all the time. Looking on while they carry out this violence against Palestinians are other soldiers who believe almost exactly the same thing, and behind them politicians. Like I said, it’s a closed loop.”

A waterfront amphitheater roughly twice the size of the Greek Theatre and two-thirds the size of the Hollywood Bowl is set to open this week in Long Beach — and there’s a lot riding on its success.

City leaders hope F&M Bank Amphitheater of Long Beach, located next to the famed Queen Mary, will supplant declining revenues from oil extraction and lead to an uptick in tourism. Concert promoters, meanwhile, see it as filling an important gap in Southern California’s music venue market.

The temporary amphitheater, which has a maximum capacity of 11,000, is meant to be a precursor to a permanent “Long Beach Bowl,” which is being pitched as the largest waterfront venue on the West Coast. The site opens June 6 with a performance by native son Snoop Dogg, and is expected to last for up to 10 years.

The new amphitheater represents a years-long dream of Mayor Rex Richardson, who began championing an outdoor performance venue on the waterfront in 2023. Soon after the closure of Irvine’s FivePoint Amphitheatre in October of that year, he accelerated those plans by proposing this facility. The general feeling was that Irvine’s loss could be Long Beach’s gain.

“This will be a place where memories are made, where music brings people together and where our city shows up on the big stage,” he said during a January groundbreaking. “The amphitheater represents direction to invest in our city’s future, to embrace our creative economy [and] to shape how people experience Long Beach for generations to come.”

Good vibes by the water is the driving energy behind the temporary venue.

(Eric Thayer / Los Angeles Times)

While Los Angeles and Orange County have no shortage of cavernous indoor arenas, the region has recently lacked a proper “summer shed” capable of hosting many national amphitheater tours, said Nick Storch, head of global artist development for booking agency Independent Artist Group. Those tours typically play venues larger than the Greek, Irvine’s Great Park Live or Costa Mesa’s fairgrounds-adjacent Pacific Amphitheatre, but smaller than the Hollywood Bowl.

Such tours, Storch said, are of “massive” importance to the concert industry. “With amphitheaters, it’s not just the music — it’s the experience of being outside and watching a concert, getting a bite to eat with your friends and all those kinds of things,” said Storch, whose agency’s clients Motley Crue and Five Finger Death Punch will perform at the F&M Bank Amphitheater in September.

“FivePoint was a great venue to help artists that are in that in-between stage, and not fully ready for arenas,” he said. “Long Beach having an amphitheater is going to grow the market again.”

Amphitheaters are also crucial to veteran artists with established fan bases. The long-running hard rock band Tesla — who also will perform at the F&M Bank Amphitheater in September — has not played a show in Los Angeles or Orange counties since the closure of FivePoint, which hosted the group twice.

Brian Wheat, the band’s bassist and manager, said he’s excited the new venue will help change that. “Sheds are great in the summertime, and outdoor summer gigs always create a great atmosphere for both bands and fans,” he said.

Much like the F&M Bank Amphitheater, FivePoint Amphitheatre was designed to serve as a temporary venue following the closure of Irvine Meadows Amphitheatre, which operated from 1981 to 2016. (From 2000 to 2014, it was known as Verizon Wireless Amphitheater.)

At 11,000 seats, the amphitheater is roughly two-thirds the size of the Hollywood Bowl. Its permanent replacement will be “architecturally iconic,” said Mayor Rex Richardson, while this temporary version is likened to a “summer shed.”

(Eric Thayer / Los Angeles Times)

From its opening in October 2017 until its closure, FivePoint hosted nearly 500 concerts, including artists such as KISS, Dave Matthews Band, Charlie Puth, Morgan Wallen and Luke Combs.

Venue operator Live Nation — which manages more than 300 facilities across the country — initially hoped to build a permanent amphitheater nearby, but scrapped those plans in 2023 after the Irvine City Council ended negotiations. Soon after, Live Nation announced the venue would shutter.

After learning of Live Nation’s fallout with Irvine, Richardson and members of his economic development team attended the final FivePoint concert, a performance by the Zac Brown Band, to “explore the feasibility if we were to do the same thing.”

Three months later, Richardson announced plans to build a temporary amphitheater in Long Beach to bridge the gap until a permanent facility — which he envisions as an “architecturally iconic and significant” waterfront venue akin to San Diego’s Rady Shell at Jacobs Park — can be permitted, financed and constructed.

The site’s location is central to its appeal, said Dan Hoffend, executive vice president of North American venues for Legends Global, the operator for F&M Bank Amphitheater. “If you sit in the very top row — what you would consider the worst seat in the house — it’s a spectacular view,” he said. “The Queen Mary is sitting there in all its glory. You’re looking across the harbor. What would be perceived as the worst seat is actually the best seat because you see it all.”

Long Beach Mayor Rex Richardson, left, and amphitheater general manager Tra Jones sit in the stands. Even from the nosebleeds, you still have a view of the waterfront at the F&M Bank Amphitheater.

(Eric Thayer / Los Angeles Times)

Tra Jones, general manager of the new amphitheater and a Long Beach native, said he’s striving to make it feel less stopgap and utilitarian than FivePoint.

“It doesn’t have a temporary feel at all,” he said. “We looked at all our surroundings and said, ‘What does this look like from a stylistic point of view?’ We leaned into the port/SteelCraft vibe — a very cool industrial look. When you walk in, you’re experiencing a vibe. That’s what we want to resonate with concertgoers coming here.”

The word “vibe” also pops up frequently in conversation with Richardson. Under his watch, Long Beach recently started branding itself as “Vibe City,” which he said is an attempt to encapsulate the charm of L.A. County’s second-largest city, and the state’s seventh-largest.

“Long Beach is special, but it’s hard to explain why if you haven’t been here,” he said. “Because you have to experience it for yourself, the best way to describe it is that it’s a vibe.”

Still, Richardson is aware that vibes can only go so far. During an April meeting with residents of downtown Long Beach, attendees were more interested in discussing homelessness and a recent uptick in traffic fatalities than how a new concert venue might add to the city’s cultural cachet. Some downtown residents have circulated a petition regarding noise-related concerns.

“The job of the mayor is to meet the needs of your residents today — keeping a roof over your head, making sure it’s safe to walk down the street, making sure you have access to amenities and services in your community — but also to think about the future,” he said.

That means finding a way to offset revenues from oil extraction, which currently finance many municipal services, and are projected to drop from more than $50 million annually to around $21 million by 2035. According to Richardson, the new amphitheater — managed by Legends Global, but owned by the city — will help cover that shortfall. The venue is projected to be profitable within five years and generate nearly $29 million in revenue by 2036.

Oil revenues, which pay for city services, are projected to drop by more than half. The amphitheater is being pitched as a budget gap solution.

(Eric Thayer / Los Angeles Times)

“We were fortunate that revenue from oil provided a lot of our services and built our beautiful waterfront, but as California moves away from oil production, we have to plan a more sustainable future by investing in what we know will be here in the long haul,” Richardson said. “In order to do that, we have to invest in arts and culture and tourism.”

Richardson is betting on music at a time when other cities — including Los Angeles — are doubling down on sports, warehousing or data centers. The amphitheater is also meant to remind the world of the city’s impact on pop culture.

From War to Warren G and Sublime to Snoop, Long Beach has a rich musical history. The city hosted the first concerts by the Beach Boys and No Doubt, while Rock & Roll Hall of Famers Elvis Presley, the Eagles and Iron Maiden all graced the stage of the Long Beach Arena.

While that venue currently holds more conventions than concerts, Long Beach has hosted notable outdoor music festivals in recent years, including Warped Tour, Day Trip and Dreamstate. Richardson believes the success of those events helped prove the city’s viability as a concert destination.

“This is the first step toward a legacy of leaving our city in a more economically resilient position,” Richardson said. “At every big turn in our city’s economy, we’ve leaned on arts as a way forward, and this is no different.”

Even the bleacher seats represent Long Beach pride at F&M Amphitheater.

![Israeli far-right Finance Minister Bezalel Smotrich holds a map of an area near the settlement of Maale Adumim, a land corridor known as E1, outside Jerusalem in the occupied West Bank, on August 14, 2025, after a press conference at the site. [Menahem Kahana/AFP]](https://i0.wp.com/www.aljazeera.com/wp-content/uploads/2025/08/AFP__20250814__69HV6DR__v1__HighRes__IsraelPalestinianConflictSettlementPolitics-1755194568.jpg?w=640&ssl=1)