Credit markets shrug off geopolitical turmoil as investors seek yield, SocGen says

Credit markets shrug off geopolitical turmoil as investors seek yield, SocGen says

Source link

Chipotle Mexican Grill on track to reverse losses after JPMorgan upgrades to Overweight

Chipotle Mexican Grill on track to reverse losses after JPMorgan upgrades to Overweight

Source link

European markets open mixed as AI stocks sell-off hits Asia, South Korea drops 5%

As the rally in AI stocks fades, investors were cautious at the open on Friday, with European markets opening to mixed sentiment following steep falls in Asian markets.

ADVERTISEMENT

ADVERTISEMENT

Indices in London and Frankfurt quickly moved into negative territory, with the FTSE 100 dropping nearly 0.4% and the DAX losing 0.3% right after the opening. The Paris CAC 40 and the IBEX 35 in Madrid were both up 0.3%, while Milan’s main index was flat. So was the EURO STOXX 50, a benchmark index of 50 blue-chip companies from the eurozone.

Investors are awaiting the latest US non-farm payrolls report and keeping an eye on developments in the Middle East.

The US job data is important for forecasting what the Fed’s next move could be. Kathleen Brooks, research director at XTB, said in a market note, “There is now a near 40% chance of a rate hike by year-end. We expect financial markets to be extremely sensitive to today’s data,” adding that this will be the first such report with Kevin Warsh as chairman of the Federal Reserve.

In the UK, the latest data from Halifax showed that house prices unexpectedly declined in May. House prices fell 0.1% month on month, but were still up 0.5% year on year, missing expectations for a 1% jump.

Oil markets are awaiting further direction

Oil prices stabilised after falling on Thursday. Brent crude, the international benchmark, was slightly down and traded at $94.73 per barrel at 10:00 CET. It had been trading at about $70 per barrel before the start of the war in late February.

Benchmark US crude was little changed at $92.51 a barrel.

Oil prices remain under pressure as the Strait of Hormuz, a narrow waterway crucial for global oil and natural gas transport, remains effectively closed, and the war-induced energy shock is threatening to slow economic growth and fuel inflation in many countries.

American and Iranian negotiators reached a tentative deal last week to extend their ceasefire, but the agreement has not been finalised. Meanwhile, developments in Lebanon have cast doubt on the prospects for a permanent end to the conflict.

On Thursday, the Iran-backed Lebanese militant group Hezbollah rejected the latest ceasefire agreement between the Lebanese and Israeli governments.

“While there are few signs of progress in US-Iran talks, the oil market continues to trade on expectations of an imminent deal that would resume flows through the Strait of Hormuz,” ING commodities strategists Warren Patterson and Ewa Manthey wrote in a report.

Asian markets lose steam as AI craze cools

Wall Street rallied on Thursday after falling oil prices and bond yields eased pressure on US stocks. Banks, small-cap companies and other stocks that had previously been left behind by the euphoria around artificial intelligence led the gains.

Banks also helped lead the market, including gains of 5% for Goldman Sachs, 4.7% for Fifth Third Bancorp and 4.4% for U.S. Bancorp.

They helped to more than make up for losses among some AI stocks, which took a sudden back seat after dominating the market. Analysts have been saying AI stocks may have run too high, becoming too expensive, and that the broader US stock market may be set for a slowdown following an unrelenting streak of nine straight winning weeks for the S&P 500, its longest since 2023.

On Wall Street on Thursday, computer chipmaker Broadcom’s shares sank 12.6% after it issued guidance that fell short of investors’ expectations, raising concerns about the wider AI and technology sector.

US memory chip maker Micron Technology dropped 7.7%, and cybersecurity company CrowdStrike Holdings fell 3.8%.

Still, the benchmark S&P 500 climbed 0.4%, and the Dow Jones Industrial Average gained 1.7% to a record high. The tech-heavy Nasdaq Composite edged 0.1% lower.

But in Asia, investors dumped key AI-related shares, with South Korea’s SK Hynix plunging 8.6% and Samsung Electronics shedding 5.4%.

The Kospi dropped 5.1% to 8,199.44. The index has roughly doubled over the past year, lifted by gains in major technology companies.

Japan’s Nikkei 225 slipped 1.3% to 66,573.85, with technology shares leading the decline, even as official data showed that Japan’s real wages rose for the fourth consecutive month. Chip equipment maker Tokyo Electron’s shares fell 7%.

Hong Kong’s Hang Seng declined 1.2% to 24,948.96, while the Shanghai Composite Index fell 0.3% to 4,045.45.

Australia’s S&P/ASX 200 fell 0.7% to 8,623.50.

Taiwan’s Taiex gave up 1.3%, while India’s Sensex was up 0.1%.

In other trading early on Friday, the US dollar fell to 159.96 Japanese yen from 160.03 yen. The euro was trading at $1.1635, up 0.2%. Gold prices were down 0.3%, trading at around $4,490.70.

Getlink May shuttle traffic mixed:Passenger volumes gain 4% Y/Y as fre

samafoto/iStock via Getty Images

Getlink SE (GRPTF) reported a mixed performance for its Channel Tunnel shuttle services in May 2026, LeShuttle Freight transported 95,641 trucks during the month, representing a 2% decline Y/Y compared to May 2025.

This volume also marked a sequential contraction of

Asian equities largely decline on tech rotation; yen remains pinned near critical 160 mark

Asian equities largely decline on tech rotation; yen remains pinned near critical 160 mark

Source link

Argan anticipates adding new projects over the next 10 to 18 months while buyback authorization rises to $200M (NYSE:AGX)

Earnings Call Insights: Argan, Inc. (AGX) Q1 fiscal 2027

Management View

-

“Our strong first quarter fiscal 2027 results reflect exceptional execution across our business with all 3 of our operating segments achieving significant revenue growth and maintained healthy backlog.” (CEO, President & Director David

Seeking Alpha’s Disclaimer: This article was automatically generated by an AI tool based on content available on the Seeking Alpha website, and has not been curated or reviewed by humans. Due to inherent limitations in using AI-based tools, the accuracy, completeness, or timeliness of such articles cannot be guaranteed. This article is intended for informational purposes only. Seeking Alpha does not take account of your objectives or your financial situation and does not offer any personalized investment advice. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank.

Delcy Tries to Show She Has a Debt Strategy

One of the memorable moments of Venezuela’s crazy January ‘26 was ExxonMobil Chairman Darren Woods sitting across from President Trump, telling him Venezuela was “uninvestable.” His company is owed billions from Chávez-era expropriations, spent years in arbitration tribunals, and had watched its assets nationalised without fair compensation. Four months later, ExxonMobil’s technical teams were on the ground in Venezuela, evaluating assets including the Cerro Negro project. Woods was telling investors he felt positive about the opportunities.

The arc from expropriated creditor to ¿partner? is not happening by accident. In April 2026, the IMF and World Bank resumed dealings with Venezuela for the first time since 2019, opening the path to a formal economic assessment and potentially unlocking $4.9 billion in frozen special drawing rights. In May, the Delcy administration announced a “comprehensive restructuring of its sovereign debt” and PDVSA obligations, appointing Centerview Partners as financial adviser and pledging a macroeconomic framework by June. This did not include a request for a macroeconomic programme established by the Fund, which distanced itself from Venezuela’s announcement shortly after. According to Reuters, Venezuela’s total liabilities could be above $150 billion.

On June 2, Venezuela added Hogan Lovells as legal counsel for the restructuring under a dual mandate that also covers strategic lobbying for the Venezuelan embassy in Washington. The account is led by Norm Coleman, a former Republican senator with deep political connections in the capital. Neither selection has been free of political entanglement. Former Trump official Mauricio Claver-Carone, earmarked by The Washington Post as Venezuela’s unofficial viceroy, has vouched for Centerview. His business partner, Jessica Bedoya, was on the same chartered flight to Caracas as two Centerview executives on February 12, weeks before the firm finalized its contract (Centerview denied Bedoya played any role in their assignment).

Some of the companies that spent a decade winning arbitration awards against Venezuela may now be considering turning those claims into something more useful: an operating agreement, a new oil deal. Whether the game is actually changing, and the extent to which Delcy’s technical cadres can manage the process her government is trying to kickstart, are two of the huge questions for Venezuela’s “transition” observers.

Without the IMF as an anchor, the most aggressive litigants will extract preferential recoveries while others are left with worthless paper.

The shape of how Venezuela got here is also visible in a Delaware courthouse. In December, a judge signed the order transferring Citgo to Amber Energy, an affiliate of Wall Street hedge fund Elliott Management, for 5.9 billion dollars. The gavel came down, but the sale did not close. CITGO is now in legal and political limbo.

The transaction requires approval from OFAC, which has repeatedly extended the freeze on CITGO-related transactions. The State Department is now the main barrier blocking the sale, while Treasury, Commerce, and Energy favour letting it proceed. Ten days ago, OFAC issued General License 5W, extending the freeze on CITGO share transfers to June 19. A World Bank delegation visited Caracas last month. Everything suggests Delcy Rodríguez now feels compelled to show she can find a way to pay them back. That she has a plan.

In the meantime, Amber Energy is pressing daily for access to CITGO’s financial and operational details even though it is not formally in control, while CITGO itself cannot make major investment decisions or hire key personnel. A company valued at $13 billion is being run in slow motion, waiting for Washington to decide what Venezuela’s most valuable foreign asset is actually worth, to whom, and under what terms.

None of this happened overnight. The process was set in motion by Hugo Chávez when he went on a nationalisation spree that expropriated the assets of ConocoPhillips, ExxonMobil, Crystallex, and dozens of other foreign companies across the oil, mining, and manufacturing sectors. Those companies didn’t go home quietly. They went to arbitration. And they won.

The restructuring announcement tries to change the terms of the conversation. Venezuela is no longer being asked whether it will engage with its creditors. It has begun doing so. Centerview Partners is on the ground. A macroeconomic framework is due soon. The creditor committee, which includes GMO, Greylock Capital, Fidelity, and T. Rowe Price has been ready to negotiate since January.

ConocoPhillips has been explicit: recovering the billions owed from past expropriations takes priority over any new drilling.

An IMF programme, if it materialises, could signal credibility. It would serve as the anchor for the entire restructuring process. IMF conditionality establishes a debt sustainability framework that defines how much Venezuela can actually pay, which in turn defines what creditors can realistically expect. It also catalyses coordination. Rather than pursuing individual enforcement actions against Venezuelan assets, creditors have an incentive to wait for an orderly process. Without that anchor, the most aggressive litigants will extract preferential recoveries while others are left with worthless paper.

Delcy Rodríguez announced the restructuring without first securing that anchor. She has stated there are “no plans” to contract an IMF loan. The IMF, for its part, says it is willing to support a programme but requires clarity on economic data and external debt that Caracas has not yet provided. Very soon, we will find out whether Venezuela is building toward an IMF-anchored process or trying to engineer one without it.

Several of the companies owed the largest arbitration awards are well positioned to operate Venezuelan assets: ExxonMobil at Cerro Negro, ConocoPhillips at its former Petrozuata and Hamaca projects. ConocoPhillips has been explicit: recovering the billions owed from past expropriations takes priority over any new drilling. A negotiated settlement that converts arbitration claims into operational stakes, with revenue streams tied to production, would give creditors a return and Venezuela a rebuilt industry. The OFAC licensing architecture already enables this. Since January 2026, OFAC has issued or updated more than eight general licenses expanding authorised activity in Venezuela’s energy and financial sectors. Washington has built the tools, such as General License 58. The question is whether Venezuela can use them.

What this push does not resolve is the harder question: whether Venezuela has the institutional capacity to negotiate on its own terms rather than simply accept whatever is offered. Woods’s shift from “uninvestable” to “positive” in four months signals appetite, not commitment. ExxonMobil wants its assets back or a return on its claims. So does ConocoPhillips. So does every creditor in the queue. The question is whether Venezuela can show up to this negotiation as a party with a strategy, not just a debtor with a problem.

The path forward requires exactly what fifteen years of chavismo didn’t build: legal capacity, a coherent negotiating strategy, and the institutional infrastructure to distinguish between claims that should be settled, claims that should be contested, and claims that might be converted into something more useful than a judgment. The latter could amount to an oil agreement like the one Chevron got in the early 2020s. Venezuela’s reformed Hydrocarbons Law allows international arbitration to resolve disputes in the oil and gas sector. So does the new Mining Law for gold and strategic minerals.

The framework now exists in writing. Whether Venezuela can implement it coherently, and whether it can hold up against the inevitable tension between Venezuelan law as established in the new statutes and US jurisdiction as required by OFAC licenses, are the open questions that will determine whether this moment becomes the start of something durable or another lost opportunity.

None of that sounds like glamorous policymaking. It doesn’t play well in a speech. But the alternative, continuing to treat international arbitration as someone else’s problem, has a documented price tag. It is measured in refineries.

EU trade chief to meet China envoy amid heated trade tensions

Published on

The European Commission confirmed to Euronews on Wednesday that EU trade chief Maroš Šefčovič will meet his Chinese counterpart, trade envoy Li Chenggang, on the sidelines of an OECD ministerial meeting in Paris on Thursday.

ADVERTISEMENT

ADVERTISEMENT

The visit comes as EU-China relations remain strained, with Brussels seeking to crack down on Chinese overcapacity and tackle a record-high €359.9 billion trade deficit with Beijing.

After the EU unveiled the so-called Industrial Accelerator Act and the Cybersecurity Act which could exclude Chinese companies from the EU market, China threatened retaliation, fuelling fears of a trade war between the two trading partners.

Tensions escalated further last week when EU commissioners met to discuss the bloc’s strategy towards the Asian giant.

“The current state of the trade and investment relationship is not sustainable,” the Commission said in a statement after the meeting.

An EU official told Euronews that a majority of the Commissioners had agreed to strengthen the EU’s trade defence tools to help counter China. Proposals will be made to EU leaders during their summit on 18 June.

However, member states remain divided over the EU’s China policy. A non-paper signed by France, Italy, Spain, the Netherlands and Lithuania called for faster use of tariffs and quotas on imports threatening EU industrial sectors, with China the principle target. The idea is to restore a level playing field against Chinese trade practices that many in Europe describe as unfair.

Among those countries taking a different line is Germany, whose policy is to preserve access to the Chinese market for its companies even as it faces a deep trade deficit.

Meanwhile, the Commission said it will continue engaging with China. There have been reports that Commerce Minister Wang Wentao could visit Brussels on 28 and 29 June, but the visit has not yet been publicly confirmed.

How the Dangote IPO Will Test African Markets

A $50 billion refinery valuation tests liquidity across African capital markets.

Dangote Refinery’s initial public offering is shaping up to be one of the most historic capital markets events for the continent—a referendum on whether Africa can mobilize the liquidity and investor confidence required to finance a globally competitive industry.

Chinenyem Anyanwu, CEO of Lagos-based Dependable Securities, said the offering is attracting both institutional investors and first-time investors, including Nigerians in the diaspora.

“The expectation is very high among the investing public,” Anyanwu tells Global Finance. “Some are Nigerians outside the country, while others are foreign investors looking for exposure to a strategic African industrial asset.” Aliko Dangote, chairman of the Dangote Group, disclosed that requests for private placement had surpassed $2 billion.

Speaking during a visit by executives from First HoldCo, the parent company of First Bank of Nigeria, Dangote said the company would be unable to meet all requests. He added that the response demonstrates investors’ confidence in the project.

Interest has also come from prominent Nigerian investors. Femi Otedola, chairman of First HoldCo, has said he plans to invest $100 million in a private placement ahead of the IPO, with proceeds from the sale of his stake in Geregu Power.

Although early market estimates put the refinery at about $50 billion, Dangote has said advisers are still determining the final valuation. Despite plans to offer only 10% of the equity to the public, the IPO would still be unprecedented for African exchanges.

“Ten percent of the refinery is still a substantial offering,” Anyanwu said. “It is larger than the market capitalization of many companies currently listed on the Nigerian Exchange, so demand is unlikely to be a problem.”

The refinery, which began operations in 2024, has already begun reshaping Nigeria’s energy trade by reducing reliance on imported fuel and positioning the country as an exporter of refined petroleum products. Built at an estimated cost of $20 billion, the 650,000-barrels-per-day facility in Lagos, where Dangote Group is headquartered, is expected to expand capacity in the coming years.

This article appears in the June 2026 issue of Global Finance Magazine.

Why Wall Street & China Have the Same Problem in Venezuela

Venezuela holds the largest proven oil reserves on earth. It has lithium. It has agriculture, a coastline three hours away from Miami, and—for the first time in a generation a political window. The reconstruction investment case is real. So is the obstacle for every actor, across every ideology, that wants Venezuelan assets to perform.

The obstacle is not the oil price. It is not the OFAC sanctions framework, which has been substantially liberalized since January 2026. It is not even the absence of functioning institutions, though that is the proximate problem every investor will encounter. The obstacle has a nucleus with name, a title, and an active intelligence apparatus. And his continued presence in power is not merely a moral affront.

This is not a story about mismanagement. Mismanagement leaves a paper trail.

What happened across Venezuela’s infrastructure ministries between 2002 and 2012 lest almost none, deliberately. Over $150 billion in documented railway, housing, and infrastructure contracts were disbursed across that decade. The projects largely do not exist. The documentation largely does not exist. The Tinaco-Anaco railway, a $7.5 billion contract signed with China Railway Engineering Corporation, produced looted campsites and empty concrete columns. The National Railway Plan, budgeted at $150 billion, produced less than one percent of its projected track.

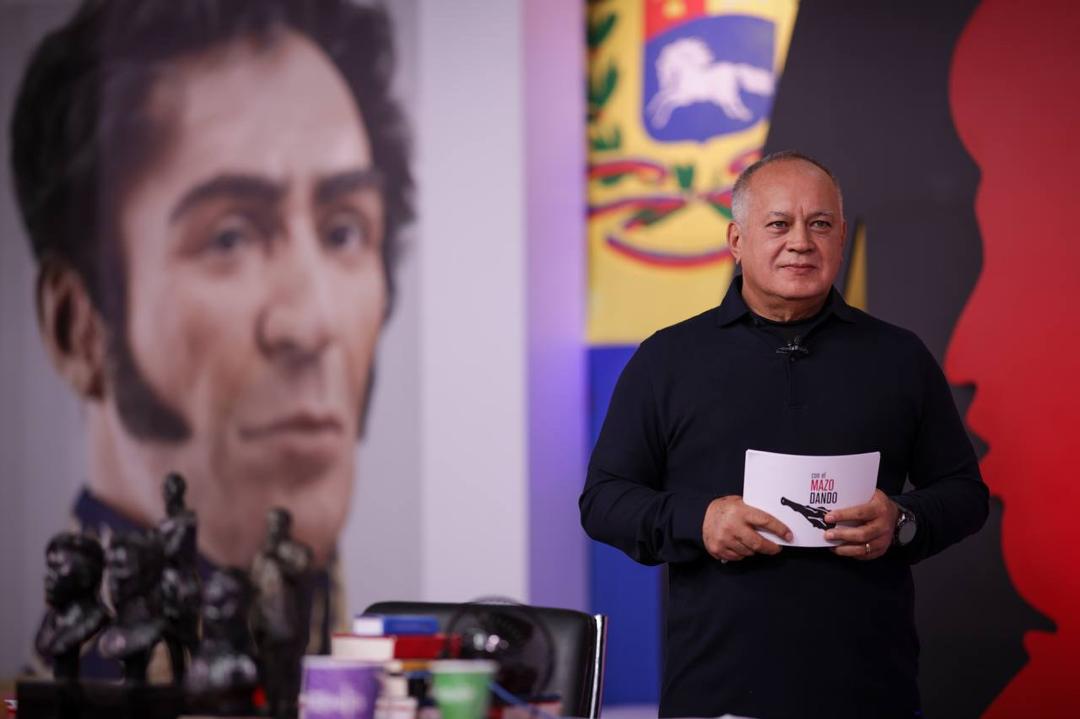

One of the ministers who oversaw that disbursement period of the infrastructure that is so dire, and who preserved an influence only surpassed by Hugo Chávez and Nicolás Maduro, today is the Interior Minister of Venezuela. He controls the national intelligence apparatus, the police, and the armed colectivos. He is Diosdado Cabello, your competing General Partner that has acted without impunity. He carries a live indictment from a New York court on narco-trafficking charges. He is sanctioned by the US Treasury. He hosts a television program that airs every Wednesday evening.

By 2011, the beneficial ownership architecture built by Venezuela’s ruling network spanned more than forty trustees across multiple jurisdictions: a parallel private equity structure embedded inside a sovereign state.

The distinction that every institutional investor must internalize is this: a mismanaged State is recoverable. A State whose productive apparatus was deliberately extracted (not ruined by incompetence but hollowed out because extraction was more profitable than production) presents a categorically different investment problem. The destruction was not the side effect of the governance model. It was the point of it. Cabello remains an icon of that governance model.

The counterparty problem

Conventional private equity rests on a foundational assumption: your counterparty has an interest in the underlying asset performing. Returns depend on it. Exit depends on it. The entire structure of an LP agreement, a term sheet, a co-investment right, all of it assumes a counterparty whose incentive is aligned with asset value.

In Venezuela, the sophisticated actor on the other side of the table for two decades was running a competing structure. One with no limited partners, no fiduciary duty, no quarterly reporting, and a sovereign intelligence apparatus for compliance. That structure had a single mandate: maximum extraction, minimum documentation, zero accountability. It executed that mandate with precision.

By 2011, the beneficial ownership architecture built by Venezuela’s ruling network spanned more than forty trustees across multiple jurisdictions. This is not a warlord’s operation. This is a parallel private equity structure embedded inside a sovereign state.

That sophistication is precisely what makes the residual presence of these networks so consequential for reconstruction capital. They did not disappear with the January 2026 transition. They repositioned. The structures that governed Venezuela’s extraction apparatus are experts at corporate layering: shell companies, nominee directors, off-channel financial instruments designed to distance beneficial owners from the assets they control.

This is the counterparty environment that reconstruction capital is walking into. Not a post-conflict landscape with residual corruption. An active, sophisticated, multi-jurisdictional extraction network that has spent 25 years perfecting its operational security

These are not improvised operations, they are multi-jurisdictional corporate architectures spanning Switzerland, Brazil, Spain, the Caribbean, and more recently Turkey and the Middle East. Each node chosen for its specific regulatory gap or enforcement lag. The $5.2 billion in gold shipped to Switzerland between 2013 and 2016, the Alex Saab procurement network running through Turkey and Cape Verde, the Zapatero indictment revealing consulting structures designed to siphon money from China, Venezuela, and Spain simultaneously these are documented examples of the same operational capability.

These networks retain the best advisors money can pay. Former heads of state, international law firms, financial intermediaries operating across jurisdictions. The Zapatero case is not the exception, it is the template. And they operate with the enforcement discipline of a cartel: strategic asset moves backed by the implicit and sometimes explicit willingness to use coercion when commercial pressure is insufficient. The SDNY indictments against senior regime figures on narco-trafficking charges are not separate from the financial architecture. They are evidence that the same command structure manages both.

This is the counterparty environment that reconstruction capital is walking into. Not a post-conflict landscape with residual corruption. An active, sophisticated, multi-jurisdictional extraction network that has spent 25 years perfecting its operational security, asset acquisitions by “patriotic”expropriations to serve their drug-logistic hubs and is now repositioning for the reconstruction window.

Why China doesn’t actually want this

China’s position in Venezuela is widely misread as unconditional support. The reality is more commercially specific. China has over $60 billion in loan-for-oil exposure through CNPC and the China Development Bank. Those loans require one thing: barrels flowing. Barrels require functional production infrastructure. Functional production infrastructure requires institutional stability, contract enforcement, and (critically) a counterparty with an interest in assets performing.

Beijing understands this better than any outside observer because its own institutions have investigated the damage. Xi Jinping’s Central Commission for Discipline Inspection placed a CITIC Group vice president under investigation for serious disciplinary violations, the same CITIC that embedded confidentiality clauses in Venezuelan housing contracts barring the Venezuelan government from accessing financial information about its own projects. An Andorran court documented $100 million in bribes paid by CAMC Engineering to Venezuelan officials. China did not need backchannel meetings to understand the corruption. Its own companies were defendants in it.

China also enforces its own code of conduct internally. The CCP’s anti-corruption apparatus, operating through the Central Commission for Discipline Inspection, has a long reach, including over state enterprise executives who participated in overseas schemes that damaged China’s institutional reputation. Chinese firms implicated in Venezuelan bribery networks in Andorra for payments to PDVSA lobbyists related to Venezuela’s electricity system did not operate without consequence within their own system. Beijing does not publicize these accountability mechanisms, but they exist. The party does not tolerate reputational exposure that undermines its economic diplomacy, regardless of the geography.

Every dollar that disappears into the extraction apparatus is a dollar that does not produce the barrel that services the Chinese loans.

The Trump-Xi summit concluded in Beijing on May 15, 2026, the same day Lamargas exploded on Lake Maracaibo, a facility operated by China Concord Resources Corp under a PDVSA joint venture contract. At the moment, the US and Chinese governments are navigating toward economic stabilization and a framework for managed competition, building on their South Korea thaw. That G2 stabilization has direct implications for Venezuela: a China that is repositioning toward US capital markets, Boeing purchases, and agricultural commitments is a China with diminishing strategic incentive to backstop a Venezuelan network that embarrasses it commercially.

The Chevron model—US-anchored, internationally governed, with Chinese off-take embedded through structured contracts—is precisely the kind of framework that serves Beijing’s debt recovery needs without requiring it to defend the indefensible.

A ministry based in a kleptocracy whose financial architecture is premised on assets not performing for the state is structurally incompatible with Chinese debt recovery. Beijing is not sentimental about this. It is calculating.

China’s $50-60 billion in loan-for-oil exposure to Venezuela requires one thing above all else: barrels flowing. Barrels require functional production infrastructure. Functional production infrastructure requires institutional stability, contract enforcement, and a counterparty whose economic interest is aligned with assets performing. When the ministry overseeing oil production is the same apparatus that systematically extracted value from every sector it touched, railways that produced concrete columns and nothing else, housing programs with $76 billion in unaccounted deficits, power plants that were paid for and never built, you can see that the problem for Beijing is not political. Every dollar that disappears into the extraction apparatus is a dollar that does not produce the barrel that services the loans.

China tried to correct this internally before abandoning the effort. In 2018, Margaret Myers at the Inter-American Dialogue pointed out that Beijing “tried over the past couple of years to guide decision-making in Caracas by providing advice or by tying loans to production capacity projects in the oil sector, in order to try to help Venezuela right itself economically. That has not proven successful.”

By 2016, China stopped issuing new loans entirely. That is not a diplomatic signal. That is a credit committee decision. The same kind of decision any institutional lender makes when the counterparty’s governance structure has made repayment structurally unlikely.

The Brazilian vector

Brazil’s relationship to Venezuela’s reconstruction is complicated by a paper trail that runs through the largest corruption scandal in Latin American history. Odebrecht paid the highest figure of any country outside Brazil itself. Venezuela’s own former prosecutor general, Luisa Ortega Díaz, formally linked those payments to senior Socialist Party figures including Diosdado Cabello after being removed from office and forced to flee the country. The investigation was halted by Venezuela’s highest court. The Swiss banking system was asked to provide a list of Venezuelan recipients. Neither process was allowed to reach its conclusion.

In Brazil, the Odebrecht network reached the highest levels of political life. Federal prosecutors investigated Lula for allegedly lobbying foreign governments on Odebrecht’s behalf after leaving the presidency, and for his role in directing state development bank BNDES financing toward Odebrecht projects abroad. The contracts that linked Odebrecht to Venezuela were not arm’s-length commercial transactions. They were, by Odebrecht’s own admission in its US Department of Justice plea agreement, instruments of a coordinated bribery architecture that spanned twelve countries and operated through a dedicated internal division (the Division of Structured Operations) whose sole purpose was managing political payments.

What does not yet exist is the decision—by US institutional capital—to arrive with a governance structure that the extraction network cannot penetrate.

Brazil has significant commercial interests in Venezuela’s reconstruction, across energy, agriculture, and infrastructure. Those interests are legitimate and Brazilian private capital is a natural reconstruction partner. The complication is not Brazil. It is the specific political-commercial network that governed Brazil’s prior engagement with Venezuela. Odebrecht did not select its Venezuelan counterparties through competitive markets. Contracts were directed through political relationships — between heads of state, with BNDES as the financing instrument, and with the Odebrecht Division of Structured Operations managing the payments in between.

Political networks have institutional memory. The preferred partners that flow through certain diplomatic channels into Venezuela’s reconstruction window carry relationships forged in that prior architecture. A governance framework serious about reconstruction cannot simply exclude Odebrecht, the legal entity. It must screen for the network that Odebrecht served. That screening is structural, not political. It is the difference between Brazilian capital that competes on merit and Brazilian capital that arrives pre-selected by the same diplomatic infrastructure that enabled the extraction.

The structure that worked and the decision that remains

One Venezuelan asset survived twenty-six years of chavismo with its value intact. One. CITGO Petroleum, incorporated in Delaware, governed under US fiduciary law, with its governance architecture anchored entirely outside Venezuelan legal jurisdiction. It survived not because of political protection but because of structural protection. US law held when every Venezuelan institution around it failed. That is not a coincidence. It is the blueprint.

Venezuela sits very close to Miami. Capital will flow in. The question is whether it arrives with a governance structure equal to the threat, or whether it arrives the way it always has in captured states: trusting counterparties who already demonstrated, at extraordinary scale, that trust was the wrong instrument.

The SDNY indicted the man who sits in the Interior Ministry. The US Treasury sanctioned him. He is still in the building. Turkish construction conglomerates, Asian commodity traders, and European energy juniors are already positioning—without FCPA compliance costs, without fiduciary obligations, without LP reporting requirements. They will move faster. They will price lower. This is what happened in Iraq after 2003. It is what happened in Libya.

The architecture to do this differently exists. Human capital exists in the diaspora: eight million Venezuelans left and within them there are over a million that hold verifiable credentials embedded in US and European institutions, carrying the technical and legal knowledge to rebuild what was taken. The OFAC licensing framework exists. The proof of concept exists in CITGO’s survival. What does not yet exist is the decision—by US institutional capital—to arrive with a governance structure that the extraction network cannot penetrate. That decision is the only thing standing between reconstruction and a second extraction with better letterhead.

Zara owner Inditex defies Iran war concerns with strong sales as shares surge

Published on •Updated

The Spanish fashion giant behind Zara, Inditex, posted net income of €1.4 billion in the first quarter, up 5.4% year-on-year and ahead of market expectations.

ADVERTISEMENT

ADVERTISEMENT

Sales rose 5.8% to €8.7bn, or 8.8% at constant exchange rates, ahead of the roughly 8% analysts had anticipated.

Gross profit rose 6.9% to €5.4bn, helped by an improvement in profit margins, meaning the company kept a larger share of revenue as profit. EBITDA, a measure of underlying earnings, increased 7.3% to €2.6bn.

Inditex shares rose more than 5% on Wednesday after the company reported a strong start to the second quarter, with sales increasing 11.5% between 1 May and 1 June, reassuring investors that the Zara owner remains resilient despite signs of weakening consumer spending.

“Inditex continued its strong momentum with its latest results beating first quarter expectations, and also seen a strong start to the second quarter too, as sales grew more or less in line with the rate the company exited with in the previous quarter,” said Mamta Valechha, consumer discretionary analyst at Quilter Cheviot.

The revenue jump from one of the world’s largest listed clothing retailers points to solid consumer appetite heading into the summer, despite concerns that a more uncertain economic and geopolitical backdrop could weigh on spending in the months ahead.

Navigating geopolitical risks

The results come as businesses around the world face growing uncertainty over the global economy and concerns that consumers may cut back on spending.

Inditex said its wide-ranging supply chain and flexible transport network had helped it keep products flowing to stores around the world despite recent disruptions.

“Ultimately, Inditex continues to have a resilient business model that can withstand significant economic pressures and currency headwinds,” said Mamta Valechha, consumer discretionary analyst at Quilter Cheviot.

Valechha said strong customer demand and the company’s ability to source products close to its key markets had helped it keep collections up to date while limiting the need for discounts. Productivity improvements had also helped protect profitability.

Inditex also said that the current “geopolitical challenges” had an impact on the sales in the Middle East, a region that Barclays estimates accounts for about 5% of its revenue.

The company also warned that ongoing instability in the region could affect its performance in the months ahead.

Inditex faces a number of other challenges, including higher shipping costs and rising prices for raw materials such as cotton and polyester. Currency movements are also expected to weigh on results this year.

Inditex ended the quarter with 5,456 stores and a net cash position of €10.8bn.

The board has proposed a dividend of €1.75 per share for the last fiscal year, comprising an ordinary component of €1.20 and a bonus of €0.55, payable in two instalments in May and November 2026.

Despite the strong start to the year, Inditex left its outlook unchanged. It said it expects sales growth to continue into the second quarter, supported by strong demand for its spring and summer collections and ongoing improvements to its stores and operations.

However, the company said currency fluctuations are likely to reduce sales growth by around 1% over the full year. It also expects to invest about €2.3bn in the business during the current financial year.

Palo Alto Networks projects $3.345B-$3.355B Q4 revenue while targeting 40% free cash flow margin in fiscal 2028 (NASDAQ:PANW)

Seeking Alpha’s Disclaimer: This article was automatically generated by an AI tool based on content available on the Seeking Alpha website, and has not been curated or reviewed by humans. Due to inherent limitations in using AI-based tools, the accuracy, completeness, or timeliness of such articles cannot be guaranteed. This article is intended for informational purposes only. Seeking Alpha does not take account of your objectives or your financial situation and does not offer any personalized investment advice. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank.

Yesway outlines $210M-$220M fiscal 2026 adjusted EBITDA outlook while planning 6-8 new stores (NASDAQ:YSWY)

Earnings Call Insights: Yesway, Inc. (YSWY) Q1 2026

Management View

- Chief Executive Officer Thomas Trkla framed the quarter as the company’s first as a public issuer, highlighting scale and footprint: “As of March 31, 2026, we operated 449 stores, making Yesway the 15th largest convenience

Seeking Alpha’s Disclaimer: This article was automatically generated by an AI tool based on content available on the Seeking Alpha website, and has not been curated or reviewed by humans. Due to inherent limitations in using AI-based tools, the accuracy, completeness, or timeliness of such articles cannot be guaranteed. This article is intended for informational purposes only. Seeking Alpha does not take account of your objectives or your financial situation and does not offer any personalized investment advice. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank.

UK Mortgage Approvals Hit 15-Month High Despite Iran War

(Bloomberg) — UK mortgage approvals unexpectedly rose in April as the housing market displayed ongoing resilience to the economic fallout from war in Iran. Read More

Source link

Mega-Cap IPOs Make Major Waves for Index Investors

As SpaceX and Anthropic eye public listings, index providers brace for major market dislocations.

When mega-cap companies go public, index providers and investors will see it as dropping battleships into the old fishing pond. The resulting waves are going to soak everyone.

Privately held artificial intelligence (AI) vendor Anthropic announced its filing of a draft registration statement with the U.S. Securities and Exchange Commission (SEC) for an initial public offering at a later date. According to the company’s website, Anthropic has not decided on the number of shares it will offer, nor at what price. The company recently closed a $65 billion fundraising round, valuing the company at $965 billion post-money.

The news comes as the SEC published SpaceX’s revised Form S-1 on the market regulator’s EDGAR database. The conspicuously absent OpenAI reportedly is filling out its underwriters bench for a possible September IPO. The AI company reached a post-money valuation of $852 billion, according to CNBC.

The Index Aspect

If index providers add these firms that would instantly become one of the 10-largest listed companies by market cap before their trading prices stabilize, it could cost them dearly due to resulting massive price dislocations.

“Leaving out a mega-cap company means the index is not doing its job,” James Angel, associate professor and faculty affiliate at Georgetown University’s Psaros Center for Financial Markets and Policy, tells Global Finance. “It thus makes sense to include a big IPO fairly quickly.”

“Big IPO” is not an understatement. Wall Street consensus expects SpaceX’s IPO to result in a market capitalization between $1.75 trillion and $2 trillion, would lower Meta’s and Tesla’s rankings in the10-largest Nasdaq-100 Index components by market capitalization while move Micron Technology out of the Top 10. If rumors of a SpaceX-Teslamerger prove true, only Nvidia, Alphabet, and Apple would have a larger market capitalization than the resulting $3.4 trillion behemoth.

The Fast Path

Nasdaq has already addressed the mega-cap issue by updating the methodology for inclusion in its Nasdaq-100 Index, which represents the 100 largest Nasdaq-listed non-financial companies, in May.

Among the major changes made by Nasdaq was introducing quarterly index reconstitutions in March, June, and September, in addition to its regular December reconstitution. Nasdaq has also incorporated a “Fast Entry” pathway for new listings that rank among the top 40 of the current Nasdaq-100 constituents by full market capitalization, based on both listed and unlisted shares.

“These companies are evaluated on their seventh trading day and, if eligible, added shortly thereafter, with all existing liquidity requirements still applying,” explained Emily Spurling, Global Head of Index at Nasdaq Global Indexes, in an interview posted on the Nasdaq website. “The quarterly rebalance handles the broader population of eligible companies; Fast Entry ensures the index can respond in a timely way when a company of significant scale enters the public market.”

SpaceX stock could see its highest price jump not on June 12, its reported IPO day, but on July 7, the earliest it could be added to the Nasdaq-100 Index, according to The Motley Fool’s Sean Williams.

“Taking into account the Juneteenth (June 19) and Independence Day (July 3) holidays for the stock market, the 15th trading day, including its IPO day, is July 6,” he wrote. “Index funds that attempt to mirror the market-cap-weighted Nasdaq-100 will be required to purchase a jaw-dropping number of shares after this 15-day period comes to a close. Mandatory purchases from exchange-traded funds and index funds are estimated at $22 billion to $27 billion.”

“Nasdaq made the biggest change in the Nasdaq-100 rules as an inducement to listing on Nasdaq,” says Angel. “The other index providers have no similar incentive to shorten the seasoning period. I get the impression they are just doing it to make their indices more reflective of what is going on in the market.”

The Not-So-Fast Path

Meanwhile, S&P Dow Jones Indices (S&P DJI) is mulling methodology changes to its S&P U.S. Indices and Dow Jones U.S. Total Stock Market Indices. The company is considering whether to implement a “narrowly defined rule exception for MegaCap companies and adjustment to the IPO seasoning period,” according to a prepared statement.

The index vendor defines mega-cap companies as those with a market capitalization equal to or greater than the 100th largest company in the S&P Total Market Index, which was approximately $150 billion at the start of June.

According to reports from Bloomberg News, the major consideration is whether to reduce the seasoning period for IPOs before they are eligible for inclusion in an index to six months from 12 months

The consultation period ended on May 28, and any changes that S&P DJI proposes to implement would take effect “prior to the market open on Monday, June 8, 2026, unless otherwise announced,” the statement continued.

The company declined to comment beyond its published statement.

SK Hynix to double wafer capacity to ease memory shortage (HXSCL:OTCMKTS)

Wolterk/iStock Editorial via Getty Images

SK Hynix (HXSCL) plans to double its memory-chip wafer production capacity over the next five years as it works to address soaring demand for AI-related memory chips.

Chairman Chey Tae-won told reporters in Taipei that the company is responding to