Oil price jumps despite deal to release record amount of reserves

It comes as Iranian attacks on ships intensify in the crucial Strait of Hormuz waterway.

Source link

It comes as Iranian attacks on ships intensify in the crucial Strait of Hormuz waterway.

Source link

Two foreign tankers were seen ablaze in Iraqi territorial waters after a strike near the al-Faw port. Authorities say they evacuated 25 crew members but have confirmed at least one death and are battling to control the flames.

Published On 11 Mar 202611 Mar 2026

Share

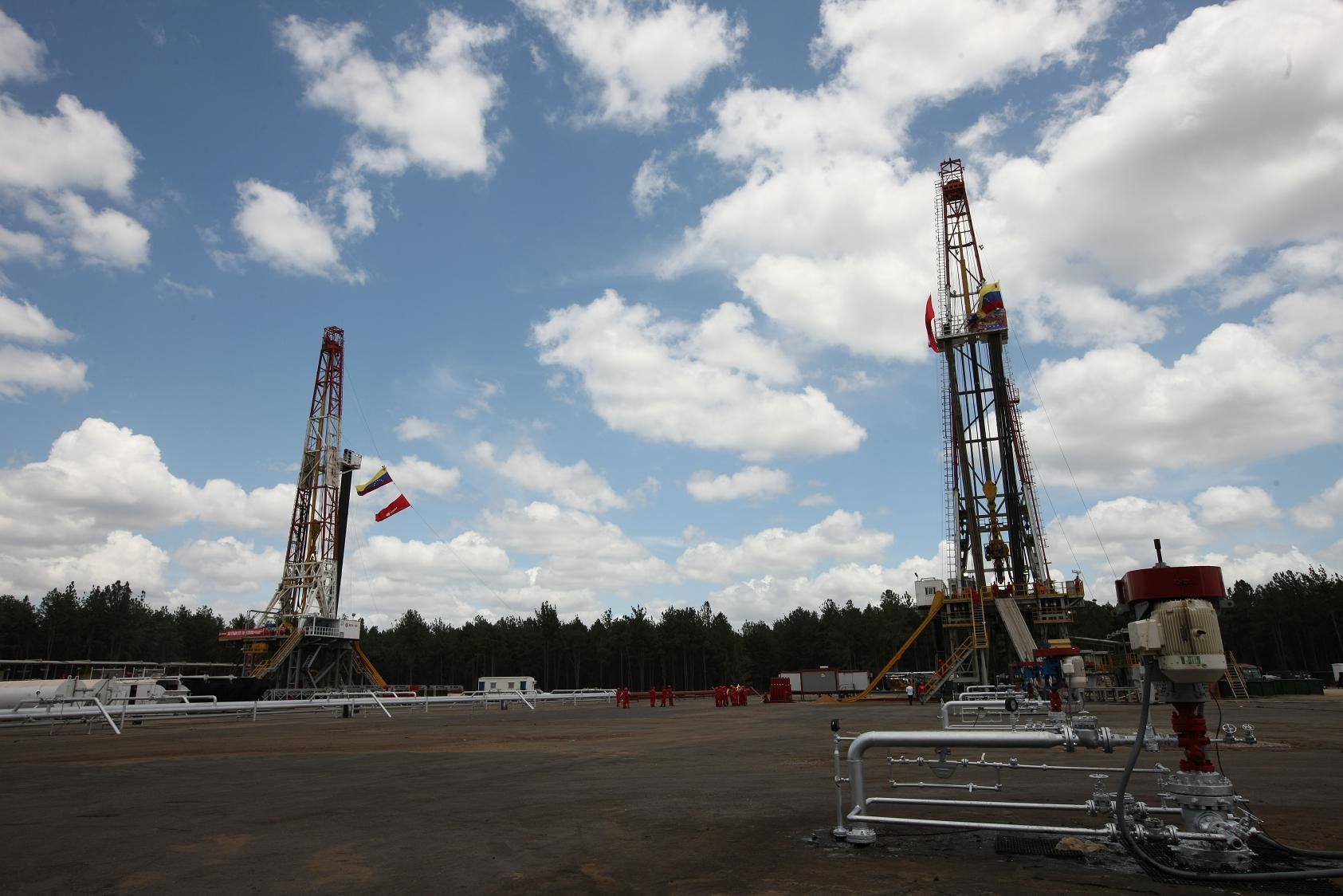

The Punta de Mata division produced over 400,000 bpd in the 2000s. (PDVSA)

Caracas, March 11, 2026 (venezuelanalysis.com) – Energy conglomerates Chevron and Shell are reportedly securing major oil deals in Venezuela following the recent pro-business reform of the country’s Hydrocarbon Law.

According to Reuters, joint venture Petropiar, where Chevron holds a minority stake, will expand its operations into the Ayacucho 8 bloc of Venezuela’s Orinoco Oil Belt.

Venezuelan state oil company PDVSA completed exploration and appraisal of the 510 square-kilometer area located south of Petropiar’s current operations, but its development has been limited. Under the agreement, Chevron looks to significantly expand its extra-heavy crude output from the Orinoco Oil Belt, which holds three-quarters of Venezuela’s oil reserves.

Chevron is reportedly looking to secure reduced royalties and taxes under the recently reformed Hydrocarbon Law in order to launch operations in the new area. Petropiar currently produces 90,000 barrels per day (bpd) of upgraded Hamaca crude. PDVSA’s joint ventures with Chevron have a total present output of around 250,000 bpd.

In January, Venezuela’s National Assembly approved a legislative overhaul that significantly improved conditions and benefits for private corporations in the oil and natural gas sector. Royalty and income tax levies, previously set at 30 and 50 percent, respectively, can now be slashed at the Venezuelan executive’s discretion.

In addition, joint venture minority partners can directly manage crude operations and sales, while legal disputes can be taken to international arbitration instances. Furthermore, PDVSA can also lease out projects to private operators in exchange for a percentage of the oil output.

Under the latter model, Shell is reportedly set to take over operations in PDVSA’s Punta de Mata division in eastern Monagas state, one of the most historically productive and profitable regions for Venezuela’s oil industry. The division produced over 400,000 bpd of light and medium crude grades in the 2000s but recent production was around 90,000 bpd.

The London-based multinational, which had a strong presence in the Venezuelan energy sector throughout the twentieth century, is likewise interested in capturing and processing natural gas that is currently flared in oil extraction processes.

Shell is additionally set to lead the Dragon offshore natural gas project alongside Trinidad and Tobago’s National Gas Corporation (NGC) in Venezuelan waters. The Nicolás Maduro government had suspended all joint initiatives with Trinidad due to its administration’s support for Washington’s Caribbean military buildup and threats against Venezuela last year.

Since the January 3 US military strikes and kidnapping of President Maduro, the acting Venezuelan authorities led by Delcy Rodríguez have fast-tracked a diplomatic rapprochement with the Trump administration while also vowing to “adapt” legislation to attract foreign investment. Following the hydrocarbon reform, a new mining law has also been preliminarily approved by the Venezuelan parliament.

US Energy Secretary Chris Wright and Interior Secretary Doug Burgum have visited Venezuela in recent weeks and hailed the investment opportunities in oil and minerals for US conglomerates.

Since January, the Trump administration has taken control of Venezuelan oil exports, with crude shipments handled by commodity traders Vitol and Trafigura and proceeds deposited in accounts run by the US Treasury. US authorities so far have only returned US $500 million, out of a reported $2 billion agreement, to the Caribbean nation.

The White House has also issued a number of licenses in an effort to boost US involvement in the Venezuelan energy sector, including limited waivers to export inputs and technology. In addition, Washington has allowed several corporations to negotiate agreements with Caracas while mandating that contracts be subject to US jurisdiction and that all royalty, tax and dividend payments be made to US Treasury-run accounts.

Alongside Chevron and Shell, the other companies with early access to the Venezuelan energy sector are BP, Eni, Maurel & Prom, and Repsol. The latter two held meetings with Rodríguez in February to discuss investment opportunities, while ExxonMobil has announced plans to send a delegation to the country in the coming weeks.

Venezuela’s oil production rebounded in February, with OPEC secondary sources registering an output of 903,000 bpd, up from 823,000 bpd in January. A US naval blockade since December had forced PDVSA to cut back production before exports began to flow again under Washington’s control. The oil sector remains under US financial sanctions.

For its part, PDVSA reported a February output of 1.02 million bpd, up from 924,000 bpd the prior month. The direct and secondary measurements have differed over time due to disagreements over the inclusion of natural gas liquids and condensates.

Edited by Lucas Koerner in Fusagasugá, Colombia.

Global currency and commodity markets stabilised slightly on Tuesday after a volatile start to the week triggered by the war involving Iran, United States and Israel. The U.S. dollar steadied against major currencies after earlier declines, following remarks from U.S. President Donald Trump that the conflict could end “very soon.”

Financial markets had been thrown into turmoil a day earlier amid fears that a prolonged war could trigger a major global energy shock. The conflict has disrupted oil and gas exports through the critical Strait of Hormuz, a vital shipping route for global energy supplies.

Although markets calmed somewhat after Trump’s comments, the broader environment remains highly uncertain as investors continue to assess the potential economic fallout from the conflict.

In Asian trading, the U.S. dollar was largely steady against other major currencies after retreating from the highs reached during Monday’s market turbulence.

The currency traded at around 157.73 yen against the Japanese yen and about $1.1632 against the euro, reflecting a stabilisation following the sharp movements seen earlier.

Meanwhile, oil prices remained elevated but declined from the dramatic peaks reached at the start of the week. Brent crude traded at roughly $93 per barrel, still significantly higher than levels before the outbreak of the war but well below Monday’s surge toward $120.

The pullback in oil prices helped ease immediate concerns about a severe energy shock, although analysts caution that volatility could continue if the conflict escalates again.

Despite the relative calm in currency markets, analysts say investors are far from convinced that the crisis is nearing resolution.

Rodrigo Catril, a currency strategist at National Australia Bank, warned that markets could continue to experience sudden shifts in sentiment as geopolitical developments unfold.

According to Catril, it remains unclear whether the Iranian leadership would be willing to pursue de-escalation, suggesting that the risk of renewed market volatility remains high.

The Islamic Revolutionary Guard Corps in Iran dismissed Trump’s suggestion that the conflict could end quickly, describing the remarks as “nonsense.”

Currencies closely linked to global economic sentiment weakened as investors remained cautious.

The Australian dollar slipped to around $0.7063, while the New Zealand dollar fell to roughly $0.5912. These currencies often decline during periods of geopolitical uncertainty or when investors shift toward safer assets.

The dollar, by contrast, has benefited from its traditional role as a safe-haven currency during times of crisis. The escalation of the conflict and disruption to energy markets prompted investors to move funds into U.S. assets, supporting the currency.

The British pound recovered from losses earlier in the week to trade around $1.3434.

Investors remain concerned that sustained high energy prices could slow global economic growth. Rising oil costs increase expenses for businesses and households, effectively acting as a tax on economic activity.

At the same time, higher energy prices could complicate monetary policy by pushing inflation upward and making it harder for central banks to lower interest rates.

Analysts at Deutsche Bank noted that a broader market sell-off in risk assets would likely require several conditions to occur simultaneously: persistently high oil prices, a shift in central bank policy expectations and clear evidence of a slowing global economy.

Strategist Henry Allen said markets are now significantly closer to those thresholds than they were just a week ago, though the full conditions for a major downturn have not yet materialised.

The market reaction to the Iran war underscores how closely global financial conditions are tied to geopolitical developments in the Middle East.

While Trump’s comments about a possible quick end to the conflict helped stabilise markets temporarily, the underlying risks remain substantial. The disruption of energy supplies through the Strait of Hormuz continues to threaten global oil flows and could trigger renewed price spikes if the conflict intensifies.

For investors, the situation presents a delicate balance. On one hand, hopes for de-escalation could stabilise energy prices and reduce pressure on financial markets. On the other, continued fighting or further disruptions to oil shipments could quickly reignite volatility across currencies, commodities and equities.

Until there is clearer evidence of either de-escalation or escalation, markets are likely to remain highly sensitive to political developments, with the dollar continuing to benefit from its role as a global safe haven.

With information from Reuters.

Attacks on multiple commercial ships in the waters around Iran on Wednesday increased global energy concerns, pushed nations to unleash strategic oil reserves and sparked fresh critiques of the Trump administration’s readiness for a war it started.

As Trump administration and U.S. military officials continued to claim increasing success and advantage in the conflict — and authorities downplayed a reported threat of drone attacks on California — leaders around the world scrambled to respond to the latest attacks and the International Energy Agency’s call for the largest ever release of strategic oil reserves by its members to help stem energy price spikes.

President Trump also faced renewed questions about a deadly strike on an Iranian elementary school at the start of the war, after the New York Times reported Wednesday that a military investigation had determined the U.S. was responsible.

“I don’t know about it,” Trump said when asked about the report.

In an address Wednesday morning, IEA Executive Director Fatih Birol said energy shipments through the Strait of Hormuz had “all but stopped” amid the conflict, driving massive global competition for oil and gas in wealthier countries and fuel rationing in poorer nations.

He said the IEA’s 32 member nations have brought a “sense of urgency and solidarity” to recent discussions on the matter, and had unanimously agreed to “launch the largest ever release of emergency oil stocks in our agency’s history,” making 400 million barrels of oil available.

However, he said the most needed change is the “resumption of traffic through the Strait of Hormuz.”

A vendor pumps petrol from Iranian fuel oil tankers for resale near the Bashmakh border crossing between Iraq and Iran.

(Ozan Kose / AFP/Getty Images)

Several countries, including Germany, Austria and Japan, had already confirmed their plans to release reserves.

The White House did not immediately respond to a request for comment on any U.S. plans to release its strategic reserves, or how much would be released. The U.S. is an IEA member.

Trump told reporters Wednesday that the U.S. has hit Iran “harder than virtually any country in history has been hit,” including by wiping out its naval fleet and eliminating other vessels capable of laying mines, and that he believes oil companies should resume shipments through the strait despite the recent attacks.

U.S. Interior Secretary Doug Burgum backed the idea of releasing oil reserves in a Fox News interview.

“Certainly these are the kinds of moments that these reserves are used for, because what we have here is not a shortage of energy in the world; we’ve got a transit problem, which is temporary,” Burgum said. “When you have a temporary transit problem that we’re resolving militarily and diplomatically — which we can resolve and will resolve — this is the perfect time to think about releasing some of those, to take some pressure off of the global price.”

Burgum said that while Iran is “holding the entire world hostage economically by threatening to close the strait,” Trump has made the consequences of such actions “very clear,” and “there’s a lot of options between ourselves and our allies in the region, including our Arab friends in the region, to make sure that those straits keep open and that energy keeps flowing for the global economy.”

The IEA did not provide details as to the release of the 400 million barrels, part of a broader reserve of some 1.2 billion barrels held by its members. It said the reserves “will be made available to the market over a time frame that is appropriate to the national circumstances of each Member country and will be supplemented by additional emergency measures by some countries.”

The agency said an average of 20 million barrels of crude oil and oil products transited the strait per day in 2025, and that options for bypassing the strait are “limited.”

While some tankers believed linked to Iran were still getting through the Strait of Hormuz, which under normal circumstances carries about 20% of the world’s oil and natural gas, Iranian officials threatened attacks on other vessels — saying they would not allow “even a single liter of oil” tied to the U.S., Israel or their allies through the channel, which connects to the Persian Gulf.

Trump has repeatedly claimed that the U.S. and its powerful Navy would support commercial vessels and ensure the strait remains open to oil shipments, but that has not been the case.

Tankers wait off the Mediterranean coast of southern France on Wednesday.

(Thibaud Moritz / AFP/Getty Images)

The United Kingdom Maritime Trade Operations center, run by the British military, reported at least three ships struck in the region Wednesday — including ships off the United Arab Emirates and a cargo ship that was struck by a projectile in the strait just north of Oman, setting it ablaze.

The Trump administration and the U.S. military, meanwhile, have been pushing out messaging about wiping out Iran’s ability to plant mines in the strait — posting dramatic videos of major strikes on tiny boats on small docks.

Adm. Brad Cooper, the leader of U.S. Central Command, said in a video posted to X on Wednesday morning that “in short, U.S. forces continue delivering devastating combat power against the Iranian regime.”

“I’ve said this before, but it bears repeating: U.S. combat power is building, Iranian combat power is declining,” he said.

The U.S. has struck more than 60 Iranian ships, and just “took out the last of four Soleimani-class warships,” he said. “That’s an entire class of Iranian ships now out of the fight.”

Cooper said Iranian ballistic missile and drone attacks have “dropped drastically” since the start of the war, though “it’s worth pointing out that Iranian forces continue to target innocent civilians in gulf countries, while hiding behind their own people as they launch attacks from highly populated cities in Iran.”

He also addressed the attacks on commercial shipping in the region directly, saying that “for years, the Iranian regime has threatened commercial shipping and U.S. forces in international waters,” and that the U.S. military’s “mission is to end their ability to project power and harass shipping in the Strait of Hormuz.”

Other U.S. leaders called the U.S. war plan — and specifically its approach to protecting the Strait of Hormuz — into question.

In a series of posts to X late Tuesday, which he said followed a two-hour classified briefing on the war, Sen. Chris Murphy (D-Conn.) slammed the administration’s plans as “incoherent and incomplete.”

Murphy wrote that the administration’s goals for the war seemed to be focused primarily on “destroying lots of missiles and boats and drone factories,” and without a clear plan for what to do when Iran — still led by “a hardline regime” — begins rebuilding that infrastructure, other than to continue bombing them. “Which is, of course, endless war,” he wrote.

Murphy also specifically criticized the administration’s plan for the Strait of Hormuz — which he said simply doesn’t exist.

“And on the Strait of Hormuz, they had NO PLAN,” he wrote. “I can’t go into more detail about how Iran gums up the Strait, but suffice it [to] say, right now, they don’t know how to get it safely back open. Which is unforgiveable, because this part of the disaster was 100% foreseeable.”

Ships in the strait remained under threat of various forms of attack Wednesday, as did much of the region as the war raged on.

There was an attack on a U.S. Embassy operations center at Baghdad’s airport, which officials attributed to a drone launched by Iranian proxies based in Iraq. No casualties were reported.

Lebanon’s Health Ministry reported the death toll there — from fighting between Israel and Iranian-backed Hezbollah fighters — had risen to 634 since last week, including 91 children. Another 1,500 people had been wounded, the ministry said.

Iranian authorities have said U.S. and Israeli attacks have killed 1,255 people since Feb. 28. That includes many Iranian leaders, including then-Supreme Leader Ayatollah Ali Khamenei. U.S. officials have said Iranian attacks in the region have killed seven U.S. service members, with another 140 wounded.

CBS News reported Wednesday that dozens of those injuries were sustained by service members in the March 1 Iranian drone attack on a tactical operations center in Kuwait — which is also where six of the seven deaths occurred.

The outlet reported that the attack was more severe than the Trump administration has revealed, with more than 30 military members still in hospitals Tuesday with a range of battle injuries including “brain trauma, shrapnel wounds and burns.”

Threats extended beyond the Middle East, too — including to California, where law enforcement agencies were warned by federal authorities that Iran “allegedly aspired to conduct a surprise attack” on California using drones launched from a vessel off the U.S. coast.

However, sources told The Times that advisory was cautionary and not backed by credible intelligence.

Times staff writer Gavin J. Quinton, in Washington, D.C., contributed to this report.

The executive director of the International Energy Agency Fatih Birol said he is glad to see IEA’s 32 member countries unanimously agree to release 400 million barrels of oil from its emergency stockpile.. File Photo by Ole Berg-Rusten/EPA-EFE

March 11 (UPI) — The International Energy Agency agreed to take emergency action and release 400 million barrels of oil into the market, the coalition announced Wednesday.

The 32 members of the IEA unanimously agreed to tap into their emergency reserves in response to the strain on the oil market from the war in Iran.

“The oil market challenges we are facing are unprecedented in scale, therefore I am very glad that IEA member countries have responded with an emergency collective action of unprecedented size,” Fatih Birol, IEA executive director, said in a statement.

“Oil markets are global so the response to major disruptions needs to be global too. Energy security is the founding mandate of the IEA, and I am pleased that IEA members are showing strong solidarity in taking decisive action together.”

The IEA said oil will be released to the market “over a timeframe that is appropriate to the national circumstances of each member country.”

The release of emergency reserves is the sixth in the coalition’s history since being founded in 1974.

Japanese Prime Minister Sanae Takaichi said Wednesday that Japan plans to begin releasing oil from its stockpile possibly next week. Japan is an IEA member.

Oil prices soared after the United States and Israel launched military operations against Iran. Iran has threatened vessels traveling through the Strait of Hormuz, a critical route in the oil trade, in response.

About 25% of the world’s seaborne oil is transported through the Strait of Hormuz.

The IEA has an emergency stockpile of more than 1.2 billion barrels of oil, There are 600 million additional barrels obligated by member governments.

Home ![]() News

News ![]() Oil Underinvestment Could Hinder US’ Iran-Crisis Response: Here’s Why

Oil Underinvestment Could Hinder US’ Iran-Crisis Response: Here’s Why

No matter how the Iran war gets resolved, the US and other countries will be forced to reckon with a global oil market in complete disarray.

Underinvestment in the oil industry makes the current supply shock much riskier worldwide, industry experts say, forcing the US, the EU, and various Gulf countries into a scramble over where and how to extract.

Prior to the US’ attack on Iran on February 28, the situation had already been precarious. Iran basically controls the Strait of Hormuz, the world’s busiest oil shipping channel. Transportation through this channel is currently closed, despite President Donald Trump’s promise to keep it open. Regardless of how this situation resolves, the broader implications of structural underinvestment across the oil and gas value chain have exposed just how unstable the global energy infrastructure is.

“This is not your father’s energy sector anymore,” Adam Turnquist, Chief Technical Strategist for LPL Financial, says.

Essentially, there was a shift from “drill drill drill” to returning cash to shareholders through dividends and free cash flow, he explained. This change led to better stock performance and improved financial metrics, such as credit spreads and default swaps. But, Turnquist adds, “there’s evidence of under-investment.”

Recall the 2011‑2014 time frame when oil prices were above $100 per barrel. Major oil companies like ExxonMobil, Chevron Corp, BP plc, Shell plc and TotalEnergies SE enjoyed strong cash flows, allowing them to generate substantial profits and reward shareholders.

When oil prices collapsed between 2014 and 2016, institutional shareholders pushed hard for capital discipline instead of growth. Corporations, rather than drilling aggressively, returned troves of cash to investors via buybacks and dividends.

In 2023, alone, Exxon, Chevron, Shell, TotalEnergies, and BP returned a record $114 billion to shareholders — 76% higher than their average payouts.

“That translated into lower reinvestment rates, fewer long‑cycle megaproject sanctions, and a bias toward short‑cycle barrels, even as global demand continued to grow,” Benny Wong, Senior Energy Analyst at PitchBook, told Global Finance.

There was also an energy transition, and companies prioritized ESG (environmental, social, and governance) over long-term oil projects, leading major funds to reduce fossil fuel investments.

“The result is a thinner spare capacity buffer and a smaller pipeline of readily deployable projects, which limits the industry’s ability to backfill a sudden, multi‑million‑barrel disruption like the one arising from the Iran conflict,” Wong added.

So far, the shock is reverberating across the globe. Brent crude, the international benchmark, entered 2026 oversupplied, with forward prices in the $50s, according to Chas Johnston, CreditSights senior analyst.

On Monday, the price of Brent crude spiked to $119.50 per barrel—the highest it has been since the summer of 2022, when Russia invaded Ukraine.

“It’s nearly the same cadence,” Turnquist says, citing Bloomberg data. See the chart below.

West Texas Intermediate (WTI), the U.S. benchmark, also saw similar price spikes, briefly reaching $119.48 per barrel. By late Monday, prices fell back below $90 per barrel, following mixed signals from US leadership, including contradictory statements from Trump and Defense Secretary Pete Hegseth about the conflict’s timeline.

And it could get worse, according to Wood Mackenzie, a consultancy firm for the energy sector. On Tuesday, the firm determined that $200 per barrel “is not outside the realms of possibility in 2026.”

To quell the panic, extreme measures are under consideration. The 32 member countries of the International Energy Agency (IEA) agreed on Wednesday to make 400 million barrels of oil from their emergency reserves available to the market to address the current disruption. That’s double the amount the IEA put into the market in 2022.

Over the weekend, Energy Secretary Chris Wright said the US could potentially release oil from its 400 million barrels of reserve to lower gas prices.

Trump subsequently confirmed that he would ease sanctions on certain countries to help reduce oil prices. This followed a recent 30-day waiver announced by US Treasury Secretary Scott Bessent on sanctions for Russian oil sales to India, due to global supply pressures.

Further complicating matters, oil-producing countries like Bahrain and Kuwait declared “force majeure,” stopping production as storage nears capacity and exports falter. With Iran, Israel, and the U.S. each targeting energy infrastructure and the narrow Strait of Hormuz under threat, it remains unclear which alternative transport routes or supply sources could fill the gap.

Saudi Arabia and the United Arab Emirates remain two key options because they hold most of OPEC’s effective spare capacity. However, analysts still question how much cushion truly exists and how long they can sustain it. Reports already suggest Saudi Arabia and the UAE have begun reducing output by several million barrels per day.

“In other words,” Wong says, “the buffer is meaningful but not unlimited, particularly if the disruption is prolonged or widens regionally.”

West African and Guyanese deepwater projects won’t quickly replace lost supply, either. However, they could strengthen global production over the medium to long term, Wong says. Guyana’s rapidly developing offshore sector, for example, could add more output in the coming years, though expansion will still take time.

Then there’s Namibia, which has had significant offshore discoveries in recent years. BP, Shell and TotalEnergies are among the companies that have set up shop there, but as Wong puts it: “Commercial production is still a few years away.”

As for the US, a rapid ramp now requires more than just a strong price signal.

“Producers are operating with much tighter capital discipline, and scaling quickly requires having available rigs, completion crews, frac sand and pipeline takeaway capacity, all of which can act as bottlenecks,” Wong says.

CreditSights’ Johnston agrees.

“The ability for US producers to respond is also quite limited, because it still takes six to nine months to bring new production online, even from the short-cycle shale industry,” he says.

Until then, the stakes remain high. Wood Mackenzie projects roughly 15 million barrels per day (mbpd) of Gulf oil exports could be lost if the Strait of Hormuz remains disrupted. They note that alternatives like US shale and uncompleted wells might only add a few hundred thousand barrels per day over months — not even close to filling the 15 million‑barrel gap.

The circumstances are enough to give analysts pause, given the cavalier attitude coming from the US.

Turnquist echoed a point his firm’s chief macro strategist made during a recent call: “You can’t shake the hornet’s nest and then put it back away.” Once geopolitical issues ignite, they rarely resolve quickly, he said, pointing to wars in Iraq, Afghanistan and Russia-Ukraine as examples.

“There’s really no concrete signs that it’s going to end anytime soon,” he added.

Warning comes as 400 million barrels of oil are being released from global reserves during waterway’s closure.

Published On 11 Mar 202611 Mar 2026

Share

Iran’s Islamic Revolutionary Guard Corps (IRGC) says it will not allow “a litre of oil” through the Strait of Hormuz as the closure of the key Gulf waterway continues to roil global energy markets during the US-Israeli war on Iran.

A spokesperson for the IRGC’s Khatam al-Anbiya Headquarters said on Wednesday that any vessel linked to the United States and Israel or their allies “will be considered a legitimate target”.

list of 3 itemsend of list

“You will not be able to artificially lower the price of oil. Expect oil at $200 per barrel,” the spokesperson said in a statement. “The price of oil depends on regional security, and you are the main source of insecurity in the region.”

Global oil prices have fluctuated wildly this week during continued US-Israeli attacks against Iran, which has retaliated by firing missiles and drones at targets across the wider Middle East.

The closure of the Strait of Hormuz, through which about one-fifth of the world’s oil supplies transit, and production slowdowns in some Gulf countries have raised concerns of further disruptions.

Concerns around the duration of the war, which began on February 28 and has shown no sign of abating, are also adding to uncertainty, sending oil prices soaring.

On Wednesday, three ships were hit by projectiles in the Strait of Hormuz, maritime security and risk firms said, including a Thai-flagged cargo vessel that came under attack about 11 nautical miles (18km) north of Oman.

World leaders, including members of the Group of Seven (G7) and the European Union, have been mulling what action to take in response to the war’s impact on global economies.

Christian Bueger, a professor of international relations at the University of Copenhagen and an expert in maritime security, said Europe will be facing “a major energy supply crisis” if the Strait of Hormuz is not reopened.

“For the shipping industry right now, it’s impossible to go through the Strait of Hormuz,” Bueger told Al Jazeera. “And if there are not stronger signals in the near future that they can at least try to go through the strait, then we are looking at a major shipping crisis, which can last weeks if not months.”

On Wednesday, the International Energy Agency (IEA) announced that its 32 member countries had unanimously agreed to release 400 million barrels of oil from their emergency reserves to try to lower prices.

“This is a major action aiming to alleviate the immediate impacts of the disruption in markets,” IEA Executive Director Fatih Birol said during an address from the agency’s headquarters in Paris.

“But to be clear, the most important thing for a return to stable flows of oil and gas is the resumption of transit through the Strait of Hormuz,” he added.

The reserve supplies will be made available “over a timeframe that is appropriate” for each member state, the IEA said in a statement without providing details.

German Economy and Energy Minister Katherina Reiche said earlier in the day that the country would comply with the release while Austria also said it would make part of its emergency oil reserve available and extend its national strategic gas reserve.

Meanwhile, Japan’s Ministry of Economy, Trade and Industry said it would release about 80 million barrels from its private and national oil reserves.

Japanese Prime Minister Sanae Takaichi said the country, which gets about 70 percent of its oil imports through the Strait of Hormuz, would begin releasing the reserves on Monday.

South Korea is in discussions with the IEA over the agency’s proposal to release strategic oil reserves, Seoul officials said Wednesday. This photo, taken Mar. 10, shows a gas station in Seoul. Photo by Yonhap

The South Korean government is “closely involved” in discussions with the International Energy Agency (IEA) over the agency’s reported proposal to release strategic oil reserves to help stabilize soaring oil prices, Seoul officials said Wednesday.

Officials at the Ministry of Trade, Industry and Resources confirmed Seoul’s participation in the reported IEA discussions to Yonhap News Agency, following media reports saying that the IEA has proposed the largest-ever release of oil reserves to its 32 member countries, including South Korea.

According to the report by the Wall Street Journal, IEA members are expected to soon decide on the proposal in an extraordinary meeting.

“South Korea is closely involved in discussions over a coordinated release of strategic oil reserves by the IEA,” a ministry official said.

The country currently holds around 1.9 billion barrels of oil reserves, which is enough to last more than 200 days.

“We have yet to decide how much oil will be released from our reserves with the IEA’s decision,” a ministry official said.

The Seoul government has released its strategic oil reserves on five occasions since 1990, all through international coordination.

The occasions included the 1991 Gulf War, the 2011 Libya crisis and the outbreak of the Russia-Ukraine War in 2022.

Copyright (c) Yonhap News Agency prohibits its content from being redistributed or reprinted without consent, and forbids the content from being learned and used by artificial intelligence systems.