The world today is no longer witnessing isolated geopolitical crises. From Ukraine and West Asia to Taiwan and the Indo-Pacific, almost every major flashpoint bears the imprint of an expanding strategic contest between the United States and China. The emerging order increasingly resembles a “Cold War 2.0” — though very different in structure, methods and consequences from the US-Soviet rivalry of the 20th century.

Unlike the earlier Cold War1.0, the present contest is not defined by ideological blocs alone. The US and China remain deeply intertwined economically, technologically and financially even as they posture against each other militarily, diplomatically and strategically. It is therefore a paradoxical competition: adversarial coexistence under conditions of mutual dependence.

The forthcoming summit between US President Donald Trump and Chinese President Xi Jinping in Beijing assumes significance far beyond bilateral optics. It is not merely about tariffs or trade balances. It is about whether the world’s two largest powers can manage competition without pushing the international system into prolonged instability.

Cold War 2.0: Similarities and Differences

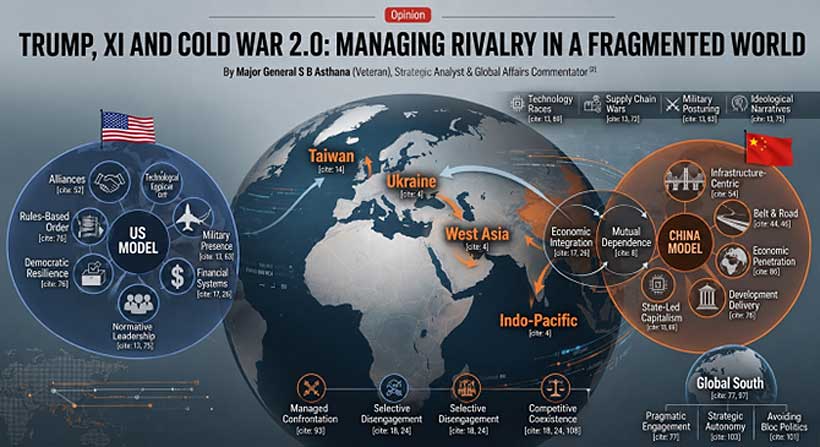

There are unmistakable similarities between the old Cold War and the current strategic rivalry. Technology races, military posturing, proxy theatres, sanctions, espionage, supply-chain wars and ideological narratives are again shaping global politics. Taiwan today resembles what Berlin once symbolised during the original Cold War — a potential trigger point with global implications.

Yet the differences are even more important.

The US and Soviet Union operated largely in separate economic ecosystems. In contrast, America and China remain deeply integrated through trade, manufacturing, investment flows and technological supply chains. As a result, Cold War 2.0 is less about total decoupling and more about selective disengagement, strategic denial, and competitive coexistence. China’s rise has also changed the nature of power transition; unlike the Soviet Union, China is economically embedded within the global capitalist system while simultaneously challenging Western strategic dominance. Beijing does not seek immediate overthrow of the international order; rather, it seeks gradual restructuring of global institutions and norms to reflect Chinese power and preferences.

Because of this interdependence, direct conflict is expensive for both parties. As a result, selective disengagement, strategic denial, and competitive coexistence are more important in Cold War 2.0 than total decoupling.

The nature of power transitions has also changed as a result of China’s growth. China, in contrast to the Soviet Union, both challenges Western geopolitical dominance and is economically integrated into the global capitalist system. Beijing aims to gradually restructure international institutions and norms to reflect Chinese strength and preferences rather than topple the current international order.

Trump’s Return: Strategic Pressure with Transactional Flexibility

President Trump’s return has introduced a more personalised and transactional dimension to US-China relations. His approach combines aggressive economic nationalism with pragmatic deal-making. Trump views geopolitics substantially through the prism of economic leverage, tariffs, industrial revival and negotiated advantage.

During his earlier tenure, Trump launched the trade war against China, challenged Chinese technological expansion and questioned assumptions of unlimited globalisation. In his second term his tariff rhetoric and coercive stance seems tampering down by Beijing’s stiff retaliation and domestic vows through courts; hence appears focused on “managed competition” rather than ideological confrontation.

Current indications suggest that Trump seeks three broad objectives from Beijing:

- Reduction of trade imbalances and greater market access for American companies.

- Chinese restraint regarding Iran, fentanyl precursors and strategic technology transfers.

- Taiwan and Indo-Pacific tensions should be relatively stable to prevent unchecked escalation. At the same time, Trump appears willing to negotiate tactical understandings with Beijing if they produce visible economic or political gains domestically.

This reflects an important distinction between traditional American strategic establishments and Trump’s worldview. Washington’s institutional security establishment and deep state often sees China as a long-term systemic challenger. Trump, however, also sees Beijing through the lens of bargaining opportunity. This creates unpredictability both for allies and adversaries.

Xi Jinping’s China: Strategic Patience and Controlled Assertiveness

If Trump represents transactional nationalism, Xi Jinping represents centralised strategic continuity with greater diplomatic maturity.

Beijing’s military modernisation, naval expansion, technological aspirations, and Belt and Road outreach reflect a long-term strategy aimed at reducing dependence on the West while enhancing China’s centrality in global affairs. Under Xi’s leadership, China has evolved from a cautious economic power into an increasingly assertive geopolitical actor. Beijing’s long-term objective to lessen reliance on the West and increase China’s influence in world affairs is reflected in its military modernisation, navy expansion, technological aspirations, and Belt and Road outreach.

Xi’s leadership style is marked by centralised authority, ideological discipline and strategic patience. Unlike the short electoral cycles of Western democracies, China’s leadership can pursue long-duration geopolitical objectives with consistency.

Beijing today appears more confident than during Trump’s first presidency. Despite economic headwinds, demographic pressures and property-sector challenges, China has strengthened domestic technological capabilities and diversified export networks.

China’s approach to global dominance differs fundamentally from America’s traditional model.

The United States historically exercised leadership through alliances, military presence, financial systems and institutional influence. Its dominance relied substantially on coalition-building and normative legitimacy, an approach, which seems to be eroding under President Trump, America First/America only agenda.

China’s model is more infrastructure-centric, economically transactional and state-driven. Beijing prefers influence through trade dependency, technology ecosystems, strategic investments and manufacturing centrality. It avoids formal alliances but expands leverage through economic penetration and calibrated coercion.

In essence, Washington exports political influence backed by military power to dislodge all potential competitors; Beijing exports economic dependency backed by state capacity aims at not dislodging potential markets to include U.S., EU and India.

The Taiwan Factor and Indo-Pacific Competition

No issue captures Cold War 2.0 more sharply than Taiwan.

For China, Taiwan remains a core sovereignty issue tied to national rejuvenation. For the United States, Taiwan represents strategic credibility, Island chain dominance in the Indo-Pacific and the larger balance of power against China.

Neither side currently appears to seek direct military confrontation. Yet both are steadily preparing for prolonged strategic competition around Taiwan. China continues military signalling and grey-zone pressure, while the US strengthens Indo-Pacific partnerships and defence arrangements.

Trump’s Beijing visit is therefore expected to prioritise “stability management” rather than dispute resolution. Beijing seeks assurances against perceived American encouragement of Taiwanese independence and military capacity building, while Washington seeks deterrence against coercive reunification efforts.

With recent claims of President Trump on Greenland, Canada, and Panama and actions in Venezuela, he doesn’t have any moral leverage to lecture China on Taiwan, because his security concerns over these areas are woefully short of Chinese security concerns of Island chains. Thus the reality of Cold War 2.0 is more of escalation management more than genuine reconciliation, as competition remains.

The Real Issue: Supply Chains and Technology Agendas

Artificial intelligence, semiconductors, rare earths, cyber systems, quantum technologies and critical supply chains have become strategic weapons. Economic security is increasingly inseparable from national security.

America still leads in advanced innovation ecosystems, financial influence and military alliances. China dominates large parts of manufacturing, industrial supply chains and infrastructure scalability.

The contest is therefore asymmetric. Washington seeks to slow China’s technological ascent through export controls and alliance-based restrictions. Beijing seeks self-reliance through indigenous innovation and strategic diversification.

Simultaneously, both nations are competing to shape global narratives.

The US projects democratic resilience and rules-based order. China projects efficiency, development delivery and non-interference. Many countries in the Global South increasingly engage both sides pragmatically rather than ideologically.

US-Israel War on Iran: Uneasy Calm Amid Strategic Contestation

China and the United States both need regional stability in Middle East to avoid economic shockwaves and disruption of global energy flows, but their strategic intentions are quite apart. Trump led America’s action plan, duly influenced by Israeli lobby includes military action, coercive deterrence, and the retaining American strategic dominance in West Asia, especially Petro-dollar domination. China, on the other hand, is attempting calibrated balance, openly supporting de-escalation while covertly defending its long-term geopolitical, economic, and energy links with Tehran.

Beijing will refrain from any overt alignment that could lead to direct conflict with Washington, but it is unlikely to desert Iran. China seems confident that it can endure supply chain crisis in Strait of Hormuz longer than Trump and Iran. In any case a over-engaged US with depleted reserves works towards Chinese strategic advantage.

The larger strategic picture shows for Beijing, the crisis offers an opportunity to project itself as a responsible stabilising power while gradually expanding influence through economic leverage and diplomatic positioning; as a result, the likely outcome is not cooperation in the classical sense, but competitive crisis management—limited convergence to avoid uncontrolled escalation, while China advances through strategic patience, economic penetration, and calibrated diplomacy. Demonstrating credibility and deterrence to adversaries, such as China, is another goal for Washington in the Iran theatre.

Thus, Iran becomes yet another arena in which China gains through strategic patience, economic penetration, and calibrated diplomacy, while the US primarily depends on military power and a weakening alliance structures.

Likely Outcomes of the Trump–Xi Engagement: Competitive Coexistence, Not Resolution

Expectations from the Trump–Xi engagement must remain realistic and free from rhetorical overstatement. The structural contradictions driving US–China rivalry — Taiwan, technological dominance, supply chain control, military competition, sanctions regimes and competing visions of global order — are too deep to be resolved through summit diplomacy alone. At best, both sides may seek temporary stabilisation of tensions to avoid simultaneous economic disruption and strategic overstretch. Therefore, the likely outcome is not reconciliation, but managed confrontation under conditions of deep interdependence.

Trump’s pressure tactics may slow certain aspects of China’s technological rise and compel tactical adjustments, but they are unlikely to reverse Beijing’s long-term strategic trajectory or ambition for greater influence in global governance structures.

Equally, China is not positioned to replace the United States as a singular global hegemon, as yet. Internal economic pressures, demographic decline, debt vulnerabilities, trust deficits and the absence of robust alliance structures remain important constraints on Chinese power projection.

Consequently, the more plausible scenario is a prolonged strategic contest marked by partial economic bifurcation in critical technologies, competing digital and AI ecosystems, intensified military signalling in the Indo-Pacific, and expanded geopolitical competition across the Global South through infrastructure financing, trade dependency, arms transfers and narrative warfare.

Emerging World Order: What should remaining World Do?

Cold War 2.0 will not produce a neat bipolar world nor purely multipolar. Unlike the 20th century, today’s international system is multipolar, economically interconnected and technologically diffused. Middle powers such as India, regional blocs and strategic swing states will play increasingly important roles in shaping outcomes through strategic balancing avoiding bloc politics. The aim remains to avoid collateral damage in a competition, which neither U.S. nor China can decisively win in the foreseeable future.

The prudent course lies in strategic autonomy backed by economic resilience, technological self-reliance, diversified partnerships and flexible diplomacy. Nations will increasingly pursue sector-specific alignments while resisting pressure to become instruments of either camp’s maximalist strategic narratives.

In this evolving landscape, Trump’s coercive unilateralism and “America First” orientation may paradoxically accelerate the very multipolarity Washington seeks to resist. Many nations, including close American partners, increasingly seek strategic hedging against unpredictability in US policy, even while remaining cautious of China’s expanding influence and coercive economic practices

Cold War 2.0 is unlikely to end through a dramatic collapse or military victory. It will instead remain a long geopolitical test of endurance, adaptability, economic resilience and strategic patience in an era of competitive coexistence, issue based cooperation and crisis management below the threshold of military confrontation.

Trump’s leadership may make the contest louder, sharper and more transactional, while Xi’s China may continue pursuing calibrated expansion with long-term strategic discipline. Yet the underlying structural reality remains unchanged: the US–China rivalry is here to stay, and the rest of the world must learn to navigate carefully between pressure and prudence, rhetoric and reality, competition and coexistence.