The resignation calls intensify Trump’s attempts to yield influence over the central bank.

United States President Donald Trump has called on Federal Reserve Governor Lisa Cook to resign, intensifying his effort to gain influence over the central bank on the basis of allegations made by one of his allies about mortgages Cook holds in Michigan and Georgia.

US Federal Housing Finance Agency Director Bill Pulte alleged in a post on X earlier on Wednesday that Cook had designated a condo in Atlanta as her primary residence after taking a loan on her home in Michigan, which she also declared as a primary residence.

Loans for a primary residence can carry easier terms than for second homes or investment properties. Pulte said the loans date to mid-2021, before Cook was appointed to the Fed by former President Joe Biden and confirmed by the Senate the following year. She is a native of Georgia and, at the time, was an economics professor at Michigan State University.

Pulte asked Attorney General Pam Bondi to investigate, and Trump quickly amplified the allegation. The Department of Justice was taking the matter very seriously, a department official told Reuters.

“We’re also probing some property that she has in Massachusetts to see if there’s something there. But I don’t have anything yet on that,” Pulte said in an interview on CNBC.

Cook’s federally filed financial disclosure documents show three mortgages taken out in 2021, including a 15-year 2.5 percent loan on an investment property and two loans for personal residences, including a 30-year 3.25 percent mortgage and a 15-year 2.875 percent mortgage. The weekly average rate for 30-year loans during 2021 ranged between 2.9 percent and 3.3 percent, Mortgage Bankers Association data shows. Cook started at the Fed in 2022 and was reappointed to a 14-year term in 2023.

Spokespersons for the Fed and for Cook did not immediately respond to a request for comment.

“Cook must resign, now!!!” Trump wrote in a post on his social media platform, his latest remarks aimed at reshaping the makeup of the US central bank, a body designed to set benchmark interest rates independent of White House influence.

Trump has told aides he is considering attempting to fire Cook, according to the Wall Street Journal, which cited a senior White House official and another person familiar with the matter.

White House at odds with the central bank

Cook is one of three Biden appointees to the Fed whose term extends beyond Trump’s time in office, complicating the president’s efforts to get more control by appointing a majority of its seven-member board.

Currently, two of the Fed’s remaining six board members were appointed by Trump: Governor Christopher Waller and Vice Chair for Supervision Michelle Bowman.

Trump has repeatedly blasted Fed Chair Jerome Powell over benchmark rates that he wants sharply reduced, calling for his resignation while acknowledging that the Fed’s unique status in US governance prevents him from firing Fed board members over monetary policy disputes.

Trump can name a new chair when Powell’s term ends in May, but claiming a majority on the board may take more time. Powell could continue serving as a governor until 2028, near the end of Trump’s term, should he buck convention and continue sitting on the board under a new chair.

Until Powell’s departure, Trump at this point has only one other seat to fill, vacated recently by the surprise resignation of former Governor Adriana Kugler. Earlier this month, Trump nominated Council of Economic Advisers Chairman Stephen Miran to serve out the rest of her term.

LYING in bed at night 68-year-old Melanie O’Reilly lay awake worrying about how she couldn’t afford to quit her £23,500 a year, 37.5-hour a week job working in a call centre.

She was £13,000 in debt and knew she couldn’t afford to pay the £500 a month repayments to the bank – but she was desperately unhappy in her job.

1

Melanie O’Reilly, 68, thought she’d never retire due to debt

Her days were spent fielding angry calls from Hounslow residents complaining about council tax and housing benefit.

She had moved from South Africa to England in September 2019 with no savings but found a job quickly due to her past career in office furniture sales.

However, the pandemic hit and in October 2020 she was made redundant before struggling to find a job at a call centre in the local council in Hounslow, West London in February 2022.

“I couldn’t stand it anymore. I was sitting there most days in full-blown migraine feeling like I had sandpaper in my eyes, until I couldn’t see the screen anymore,” Melanie, now 69, said.

“I had been very good at my job in South Africa, and I was excellent at sales.”

“Suddenly I was being micromanaged by a 26-year-old, who would count how many times I went to the toilet in a day, and tell me off if I took 31 seconds on a call instead of 30 seconds.

“The staff turnover was ridiculously high and it started to affect my physical and mental health.”

Melanie, who had previously worked as an insurance PA in London before the move to South Africa, was utterly fed up, and knew she had to retire – but had no idea how she could do so with her mounting debt.

She had lent her son and daughter-in-law, who had also moved to the UK, money for a deposit on a home in Colne, Lancashire – but then disaster struck.

Suddenly her daughter-in-law was made redundant shortly after they had their first child, meaning they couldn’t pay Melanie back as quickly as they’d planned.

Melanie was also dealing with the financial fall out of splitting from her partner and she took out a £15,000 personal loan and she had mounting credit card debt of £3,000.

Worryingly one in three people approaching retirement now have debt, with the average over-65 borrower owing £17,000, according to Money Wellness.

Financial anxiety among the 65 to 74 age group has more than doubled since 2021.

“I had the personal loan, but I was not behind in my payments and I just knew, ‘I’ve got to leave. I have to retire.

“If I don’t, I am going to have a breakdown’,” Melanie said.

“I decided to retire and I did, in April 2024. I called up Lloyds Bank and I said, ‘I’ve got this personal loan with you and I know that a few months from now I’m going to end up not being able to pay you.’

“I knew I had to take preventative measures before I got behind in any of my payments.

“I was hugely concerned about how to get Lloyds Bank to agree to a reduced monthly payment.

“I knew I couldn’t pay them back £500 a month, and I knew they wouldn’t negotiate a new loan with me because I was unemployed, as I was now retired with no real income.”

Lloyds put Melanie in touch with Money Wellness, one of the largest providers of debt advice and debt solutions in the UK.

Money Wellness provides free, confidential support to anyone struggling with money or debt, with support available online 24/7 or over the phone, so people can get help in the way that suits them best.

Melanie still owed £13,000 of the £15,000 personal loan. She called Money Wellness, and they asked her to draw up an income and expense statement.

Advisors went through her statement in detail, making allowances for everything from clothing to haircuts, and calculating how much she could afford to pay back each month to help Melanie put a debt management plan in place.

“They were so empathetic and professional,” Melanie explains.

“We revised the budget down to a manageable figure that I could pay Lloyds Bank back and by the end of it, it felt like this was too good to be true.

“They took the burden of negotiations off my shoulders and it was all done seamlessly for me without me having to worry about anything.”

The adviser told Melanie that they would negotiate the figure she had to pay back directly with Lloyds Bank, to the extent of setting up a debit order.

“After the call, I sat back and wept,” Melanie remembers.

“I was hugely concerned because when I was working at the council, I had people calling me up saying, ‘I’ve got the bailiffs at my door. They’re bashing my door down. What do I do?’

“I did not want to be in that position, and I knew that that is a reality that can and does happen.

“I did not want to go anywhere near being that person who’s got the bailiff bashing at your door. That is why I nipped it in the bud before it became a problem.”

From paying £500 a month back, Melanie now pays back £134 a month, with no added interest.

She lives in a HMO in Burnley so she doesn’t pay utility bills or council tax and receives housing benefits and pension credit.

Her repayments come from a small state pension, pension credit and housing benefits.

She receives £456.64 state pension, £451.56 pension credit and £368.20 housing benefit every four weeks.

She’d had to spend her small private pension on replacing her car after a car accident, and buying essentials like furniture.

Money Wellness reviews her plan annually, adjusting the amount if her income changes.

Melanie feels positive about the future and says the debt advice she received from Money Wellness is “the best decision I ever took”.

“For so long, I’d sat with this worrisome burden, thinking ‘I need to retire but I’ve got this debt. What do I do?’ Then these angels from heaven stepped up and helped me,” she adds.

“I feel as though a mountain had been lifted off my shoulders.”

How to cut the cost of your debt

IF you’re in large amounts of debt it can be really worrying. Here are some tips from Citizens Advice on how you can take action.

Check your bank balance on a regular basis – knowing your spending patterns is the first step to managing your money

Work out your budget – by writing down your income and taking away your essential bills such as food and transport If you have money left over, plan in advance what else you’ll spend or save. If you don’t, look at ways to cut your costs

Pay off more than the minimum – If you’ve got credit card debts aim to pay off more than the minimum amount on your credit card each month to bring down your bill quicker

Pay your most expensive credit card sooner – If you have more than one credit card and can’t pay them off in full each month, prioritise the most expensive card (the one with the highest interest rate)

Prioritise your debts – If you’ve got several debts and you can’t afford to pay them all it’s important to prioritise them

Your rent, mortgage, council tax and energy bills should be paid first because the consequences can be more serious if you don’t pay

Get advice – If you’re struggling to pay your debts month after month it’s important you get advice as soon as possible, before they build up even further

Groups like Citizens Advice and National Debtline can help you prioritise and negotiate with your creditors to offer you more affordable repayment plans.

Bulawayo, Zimbabwe – When Lloyd Muzamba was critically injured in a car accident on the Harare–Bulawayo highway in 2023, he needed an urgent blood transfusion to save his life. Despite being admitted at Mpilo Central Hospital, the biggest public health facility in Zimbabwe’s Matabeleland region, a shortage of supplies meant the doctors didn’t have enough for him.

In desperation, Muzamba’s family turned to their only other option – a nearby private hospital that sold them the three pints of blood. But at a cost of $250 per pint, Muzamba – who earned a $270 monthly salary and had no savings – could not afford it.

With time running out, the family had to make a plan. Eventually, Muzamba’s uncle sold a cow for $300 and asked other relatives to contribute the balance.

Two years on, the now recovered Muzamba says the incident has left him psychologically wounded, as he worries about other emergencies when people may need lifesaving blood.

“Three pints can be a small number; others might need more than that. But due to the costs involved, it becomes life-threatening,” said the 35-year-old, who works in a hardware store in Bulawayo.

“I could not get the blood without paying or making a payment plan. It was a painful experience for an ordinary Zimbabwean like me.”

Muzamba’s is not an isolated case.

With ongoing currency woes, rising costs of living and high levels of poverty, desperate Zimbabweans in need of care face life-threatening delays due to financial barriers. This includes blood shortages – despite supplies being free in public health facilities.

Tanaka Moyo, a mother of two in the capital Harare, also experienced the stress of needing to pay for emergency blood supplies during the delivery of her second child.

After excessive postpartum haemorrhaging, the 38-year-old street vendor needed four pints of blood.

Together with her husband, a security guard, she had struggled to raise money for the birth of their child. The sudden need for a blood transfusion was a shocking unplanned cost.

“My husband ran around and borrowed money from a microfinance institution. The interests are steep and conditions stringent, but he had to act quickly,” said Moyo.

“At the hospital, they insisted the blood was free – but it was not available.”

Plaxedes Charuma, a gynaecologist in Bulawayo, says “postpartum haemorrhage is the leading cause of maternal mortality”. The prevalence of the condition means that hospitals should always have supplies on hand to deal with maternal blood loss emergencies that arise, health experts say.

A maternity ward at a hospital in Harare, Zimbabwe [Philimon Bulawayo/Reuters]

According to the Community Working Group on Health (CWGH), a network of civic health organisations in Zimbabwe, the country faces a high demand for blood transfusions, and those most affected are pregnant women.

“About half a million pregnancies are expected in Zimbabwe, and in some of these, there is excessive blood loss, requiring transfusion of at least three pints of blood,” said Itai Rusike, CWGH’s executive director.

“Maternal mortality in Zimbabwe remains unacceptably high,” Rusike told Al Jazeera. “Timely blood transfusion prevents maternal deaths, which in Zimbabwe stands at 212 women dying per every 100,000 live births.”

‘Free blood for all’

Generally, there are two major types of blood transfusions: allogeneic and autologous. Autologous transfusion refers to self-same blood donation by an individual for their own use later. Allogeneic transfusion, which is the most common in Zimbabwe, involves administering blood donated by one person to another who matches their blood type.

The National Blood Service Zimbabwe (NBSZ) is the body that oversees blood donation and distribution in the country. It operates as an independent not-for-profit entity, but it is mandated by law to collect, process and distribute blood throughout Zimbabwe.

While the Ministry of Health and Child Care is permanently represented on its board of directors, NBSZ functions independently of hospitals and government health institutions. It is not present in every facility, but maintains decentralised distribution from five regional centres: Harare, Bulawayo, Gweru, Masvingo and Mutare.

Historically, patients in Zimbabwe paid for blood, but over the years the government worked on lowering costs – from $150 a pint in 2016 and prior to $50 by 2018.

The government then went a step further in July that year, deciding that blood would be made free at all public health institutions.

“The free blood for all move is going ahead as planned and mechanisms have already been put in place to finance the move, and come July 1 [2018], blood will be available for free,” said then-Minister of Health and Child Care Dr David Parirenyatwa during the June 2018 World Blood Donor Day celebrations.

However, despite the policy, hospitals continue to face shortages.

This May, there was a critical lack of blood in public hospitals, a situation that threatened the lives of thousands of people, the Ministry of Health and Child Care said in a statement. Al Jazeera contacted ministry spokesperson Donald Mujiri to ask about the shortage and the implementation of the free blood policy, but he did not respond to our requests for comment.

NBSZ, meanwhile, said that May’s shortage was due to operational and systemic challenges that disrupted its ability to carry out routine blood collection activities.

“Without timely financial support, we faced constraints in mobilising outreach teams, securing fuel, and procuring essential supplies,” Vickie Maponga, NBSZ communications officer, told Al Jazeera.

“Additionally, the crisis was exacerbated by a seasonal dip in donations, particularly from youth, who make up over 70 percent of our donor base.”

These shortages regularly result in patients on the front line needing to buy blood at private clinics. In most cases, the patient is physically transferred to the private facility for the transfusion, where they pay the costs. In some cases, the patient pays and the private hospital sends the blood to them in the public hospital.

A World Blood Donor Day awareness street march in Zimbabwe [Courtesy of NBSZ]

Crucial blood donations

The World Health Organization (WHO) aims to ensure that all countries practicing blood transfusions obtain their blood supplies from voluntary blood donors.

The NBSZ told Al Jazeera that a sustainable blood supply in Zimbabwe depends on cultivating a culture of regular, voluntary donations, particularly among the youth and underserved communities.

The service has a mobile outreach model, through which it brings blood donation drives directly to schools and communities. To further engage the youth, Maponga said they also started a club that “encourages young people to commit to donating blood at least 25 times in their lifetime”.

“We also integrate blood donation awareness into school programmes and partner with tertiary institutions to maintain continuity post-high school,” she said.

Ivy Khumalo, 32, is one of those who has been donating blood since she was in high school. But she says the lack of blood donation centres around her now limits her ability to give as an adult.

“As a school child, it was [first started] as a result of peer pressure, but I found it fascinating,” Khumalo said. “It was only when I was an adult that I made a personal decision to continue donating out of love to save life and help those in need.”

But since moving from Bulawayo to Hwange, she said, donating blood has become expensive as the nearest centre is in Victoria Falls, over 100km (62 miles) away.

NBSZ says it routinely deploys mobile blood drives around the country. It also says it offers donors incentives.

“Regular donors who meet specific criteria such as having made at least 10 donations, with the most recent within the past 12 months, qualify for free blood and blood products for themselves and their immediate family members … in times of medical need,” explained Maponga.

However, for keen donors like Khumalo, the effort to reach a far-off donation site is a barrier to entry.

“In such circumstances, it is no longer a free donation as I spent money going there. In the end, most of us decide to stay home despite the passion for blood donation,” she said.

CWGH’s Rusike says the NBSZ and Ministry of Health and Child Care must urgently devise innovative and sustainable ways to increase the number of eligible blood donors.

“The government should utilise the Health Levy Fund of 5 percent tax on airtime and mobile data as it was set up to specifically subsidise the cost of blood and assist public health institutions to replace obsolete equipment and address the perennial drug shortages in our public health institutions,” he said. “That money should be ring-fenced and used for its intended purpose in a more accountable and transparent manner.”

A woman works at a National Blood Service Zimbabwe (NBSZ) lab [Courtesy of NBSZ]

Promises and shortages

Authorities say that as of mid-2025, Zimbabwe’s national blood supply is showing good progress, and NBSZ has already collected over 73 percent of its half-year target (the 2025 annual target is 97,500 units).

The blood service also says the Ministry of Health and Child Care plays a central role in both subsidising and overseeing the cost of blood within the public health sector.

“Since 2018, this [free blood policy] is made possible through a government-funded coupon system, which absorbs the full cost of $250 per unit, resulting in zero cost to the recipient [in public hospitals],” said Maponga.

The NBSZ maintains that it operates on a cost recovery basis. It says the entire chain of collecting, processing and distributing a pint of blood costs $245. The agency charges $250, making a $5 profit per pint.

However, prices at some private facilities can reach as much as $500 per pint, Zimbabweans say. This has sparked heated debate on social media, as the high cost remains far out of reach for many people.

“NBSZ does not have regulatory authority over how those institutions price their services to patients,” said Maponga, explaining that while blood itself is donated freely, the journey from “vein to vein” involves a complex and resource-intensive process.

Observers, however, say more can be done to lower the costs of blood transfusions.

“At closer look, the whole chain of blood transfusion can cost less than $150 by strategically deploying available resources, use of financial donor stakeholders like corporates, and also holding the government accountable to fund the whole process,” said Carlton Ntini, a socioeconomic justice activist in Bulawayo.

The issue of free blood in the public hospitals is noble, Ntini said, but without full implementation, it remains a false hope and only benefits the “lucky” few, as shortages are the order of the day.

“In reality, any amount above $50 per pint of blood will still be high to Zimbabweans, and it’s a death sentence,” he said.

Meanwhile, for patients, the cost of essentials only adds to an already stressful situation.

Muzamba was fortunate in that his family did not claim back the money they gave him for his blood transfusion. But Moyo and her husband struggled to settle their $1,000 loan debt, which escalated to $1,400 after interest.

“It psychologically drained me more than the physical pain as I wondered, ‘Where would I get such money in this economy?’” said Moyo. “The government must own up to its promises – it’s not only about being free, but must be accessible.”

President Trump is once again floating the idea of firing Federal Reserve Chair Jerome Powell, ostensibly in objection to excessively high interest rates. But this debate is not about monetary policy. It’s a power play aimed at subordinating America’s central bank to the fiscal needs of the executive branch and Congress. In other words, we have a textbook case of “fiscal dominance” on our hands — and that always ends poorly.

I’m no cheerleader for Powell. During the COVID-19 pandemic, he enthusiastically backed every stimulus package, regardless of size or purpose, as if these involved no trade-offs. Where were the calls for “Fed independence” then? And where were the calls for fiscal restraint after the emergency was over?

Powell failed to anticipate the worst inflation in four decades and repeated for far too long the absurd claim that it was “transitory” even as mounting evidence showed otherwise. He blamed supply-side disruptions long after ports had reopened and goods were moving.

And as inflation was taking a stubborn hold, Powell delayed raising interest rates — possibly to shield the Biden administration from the fiscal fallout of the debt it was piling on — well past the point when monetary tightening was needed.

If this weren’t the world of government, where failure can be rewarded — and if there had been a more obvious alternative — Powell wouldn’t have been invited back for another term. But he was. And so Trump’s pressure campaign to prematurely end Powell’s tenure is dangerous.

I get why with budget deficits exploding and debt-service costs surging, the president wants lower interest rates. That would make the cost of his own fiscal agenda appear more tolerable. Trump likely believes he’s justified because he believes that his tax cuts and deregulation are about to spur huge economic growth.

To be sure, some growth will result, though the effects of deregulation will take a while to arrive. But gains could be swamped by the negative consequences of Trump’s tariffs and erratic tariff threats. No matter what, the new growth won’t lead to enough new tax revenue to escape the need for the government to borrow more. And the more the government borrows, the more intense the pressure on interest rates.

One thing is for sure: The pressure Trump and his people are exerting on the Fed is a push for fiscal dominance. The executive branch wants to use the central bank as a tool to accommodate the government’s frenzy of reckless borrowing. Such political control of a central bank is a hallmark of failed monetary systems in weak institutional settings. History shows where that always leads: to inflation, economic stagnation and financial instability.

So far, Powell is resisting cutting rates, hence the barrage of insults and threat of firing. But now is not the right time to play with fire. Bond yields surged last year as investors reckoned with the scale of U.S. borrowing. They crossed the 5% threshold again recently. Moody’s even stripped the government of its prized AAA credit rating. Lower interest rates from the Fed — especially if seen as the result of raw political pressure — could further diminish the allure of U.S. Treasuries.

While the Fed can temporally influence interest rates, especially in the short run, it cannot override long-term fears of inflation, economic sluggishness and political manipulation of monetary policy driven by unsustainable fiscal policy. That’s where confidence matters, and confidence is eroding.

This is why markets are demanding a premium for funds loaned to a government that is now $36 trillion in debt and shows no intention of slowing down. But it could get worse. If the average interest rate on U.S. debt climbs from 3.3% to 5%, interest payments alone could soar from $900 billion to $2 trillion annually. That would make debt service by far the single largest item in the federal budget — more than Medicare, Social Security, the military or any other program readers care about. And because much of this debt rolls over quickly, higher rates hit fast.

At the end of the day, the bigger problem isn’t Powell’s monetary policy. It’s the federal government’s spending addiction. Trump’s call to replace Powell with someone who will cut rates ignores the real math. Lower short-term interest rates will do only so much if looser monetary policy is perceived as a means of masking reckless budget deficits. That would make higher inflation a certainty, not merely a possibility. It might not arrive before the next election, but it will inevitably arrive.

There is still time to avoid this cliff. Trump is right to worry about surging debt costs, but he’s targeting a symptom. The solution isn’t to fire Powell — it’s to cure the underlying disease, which is excessive government spending.

Veronique de Rugy is a senior research fellow at the Mercatus Center at George Mason University. This article was produced in collaboration with Creators Syndicate.

Believe it or not, France has had a form of social security since the 1600s, and its modern system began in earnest in 1910, when the world’s life expectancy was just 32 years old. Today the average human makes it to 75 and for the French, it’s 83, among the highest in Europe.

Great news for French people, bad news for their pensions.

Because people are living longer, the math to fund pensions in France is no longer mathing, and now the country’s debt is nearly 114% of its GDP. Remember it was just a couple of years ago when protesters set parts of Paris on fire because President Emmanuel Macron proposed raising the age of legal retirement from 62 to 64. Well, now Prime Minister Francois Bayrou has proposed eliminating two national holidays, in an attempt to address the country’s debt.

In 2023, before Paris was burning, roughly 50,000 people in Denmark gathered outside of Parliament to express their anger over ditching one of the country’s national holidays. The roots of Great Prayer Day date all the way back to the 1600s. Eliminating it — with the hopes of increasing production and tax revenue — brought together the unions, opposing political parties and churches in a rare trifecta. That explains why a number of schools and businesses closed for the holiday in 2024 in defiance of the official change.

This week, Bayrou proposed eliminating France’s Easter Monday and Victory Day holidays, the latter marking the defeat of Nazi Germany. In a Reuters poll, 70% of respondents didn’t like the idea, so we’ll see if Paris starts burning again. Or maybe citizens will take a cue from the Danes and just not work on those days, even if the government decides to continue business as usual.

Here at home, President Trump has also floated the idea of eliminating one of the national holidays. However, because he floated the idea on Juneteenth — via a social media post about “too many non-working holidays” — I’m going to assume tax revenue wasn’t the sole motivation for his comments that day. You know, given his crusade against corporate and government diversity efforts; his refusal to apologize for calling for the death penalty for five innocent boys of color; and his approval of Alligator Alcatraz. However, while I find myself at odds with the president’s 2025 remarks about the holiday, I do agree with what he said about Juneteenth when he was president in 2020: “It’s actually an important event, an important time.”

Indeed.

While the institution of slavery enabled this country to quickly become a global power, studies show the largest economic gains in the history of the country came from slavery’s ending — otherwise known as Juneteenth. Two economists have found that the economic payoff from freeing enslaved people was “bigger than the introduction of railroads, by some estimates, and worth 7 to 60 years of technological innovation in the latter half of the 19th century,” according to the University of Chicago. Why? Because the final calculations revealed the cost to enslave people for centuries was far greater than the economic benefit of their freedom.

In 1492, when Christopher Columbus “discovered America,” civilizations had been thriving on this land for millennia. The colonizers introduced slavery to these shores two years before the first “Thanksgiving” in 1621. That was more than 50 years before King Louis XIV started France’s first pension; 60 years before King Christian V approved Great Prayer Day; and 157 years before the 13 colonies declared independence from Britain on July 4, 1776.

Of all the national holidays around the Western world, it would appear Juneteenth is among the most significant historically. Yet it gained federal recognition just four years ago, and it remains vulnerable. The transatlantic slave trade transformed the global economy, but the numbers show it was Juneteenth that lifted America to the top. Which tells you the president’s hint at its elimination has little to do with our greatness and everything to do with the worldview of an elected official who was endorsed by the newspaper of the Ku Klux Klan.

If it does get to the point where we — like France and Denmark — end up seriously considering cutting a holiday, my vote is for Thanksgiving. The retail industry treats it like a speed bump between Halloween and Christmas, and when history retells its origins, it’s not a holiday worth protesting to keep.

The following AI-generated content is powered by Perplexity. The Los Angeles Times editorial staff does not create or edit the content.

Ideas expressed in the piece

LZ Granderson advocates for eliminating national holidays but argues this should start with historically problematic ones, highlighting Thanksgiving’s origins in colonialism and slavery as a prime candidate for removal.

The author criticizes President Trump’s suggestion to reduce holidays—made on Juneteenth—as racially motivated, given Trump’s past controversies involving race and his endorsement by a KKK-linked newspaper.

Granderson defends Juneteenth as economically transformative, citing research that ending slavery spurred unprecedented U.S. growth, and condemns any effort to revoke this holiday.

He supports holiday reduction for fiscal reasons, citing France and Denmark as models, but emphasizes that the choice must prioritize justice over convenience.

Different views on the topic

French Prime Minister François Bayrou proposed cutting Easter Monday and WWII Victory Day to boost economic output and tax revenue, framing it as essential to reducing France’s debt (114% of GDP) and funding defense needs[1][2][4].

The plan faced immediate backlash: 70% of French citizens opposed it in polls, unions condemned it, and the far-right National Rally—Parliament’s largest party—rejected it[2].

Historical precedent warns against such moves; France’s 2003 attempt to scrap Pentecost Monday caused widespread confusion, protests, and enduring public resentment[3].

Denmark’s elimination of Great Prayer Day in 2023 triggered mass defiance, with schools and businesses closing anyway—illustrating deep cultural attachment to holidays.

Unlike Granderson’s focus on racial justice, macroeconomic arguments dominate overseas: Bayrou asserted cutting “holy cheese” holiday clusters would streamline productivity without targeting specific historical narratives[1][2][4].

South Africa promised debt solutions for low income nations during its G20 presidency. Has it kept its word?

Debt is holding back economic growth for many low income countries. When South Africa took over the Group of 20 presidency last year, it promised it would take on that challenge, improve food security and represent African nations from the head of the table.

As the G20’s finance ministers meet in Durban without the United States Treasury secretary and with just four months left in its term, has South Africa lived up to those promises?

Can organisations like the G20 ever really bring about change?

And in a transactional global economy, has South Africa’s leadership role come just as organisations like this matter less?

By Kashana Cauley Atria: 256 pages, $28 If you buy books linked on our site, The Times may earn a commission from Bookshop.org, whose fees support independent bookstores

There are a frightening number of ways an American can become indebted today: there’s medical debt (I won’t be paying off my child’s birth until he’s nearly 5 years old, and I have insurance). Mortgages, of course (though as a millennial living in an expensive city, I wouldn’t know what those look like). And then there’s student loan debt carried by nearly 43 million Americans, and which disproportionately affects Black women. But hey, at least one good thing has come of that, as TV writer and novelist Kashana Cauley graciously acknowledges in her new book, “The Payback”: “To the student loan industry,” reads her dedication, “whose threatening phone calls made this book possible.”

Narrated by Jada Williams, a wardrobe designer turned retail salesperson, “The Payback” is full of such you-gotta-laugh-to-keep-from-crying humor. The book opens at Phoenix, the clothing store at the Glendale mall where Jada now works, and includes a hilarious yet mostly sincere appreciation for the beleaguered centers of suburban America: “I loved mall smell,” Jada narrates, waxing poetic about the scents of the bins at the candy store and the ever-present pizza smell before admitting that she sometimes even leans down to smell the plastic kiddie ride horses. “Sometimes, when there were no kids, I’d lean into the horse and sniff it to get a whiff of plastic, childhood dreams, and dried piss. Yes, I know, nobody’s supposed to savor the aroma of pee, and I wouldn’t rank it first among the smells of the world, but pee is life. It’s humanity. It’s the mall.”

Jada loves the mall, and she even loves her job, which is not a given for anyone who’s lost their dream career like she did. She’s passionate about helping people find the clothes that look and make them feel good, even if she’s doing that for 20% commission. She’s definitely gotten over her sticky fingers habit, too, except that, well, on the day the book opens, someone leaves an expensive watch in the fitting room, and Jada can’t help but pocket it. This eventually leads to her getting fired, but not before the boss she likes, Richard, dies on the store’s floor and Jada and her co-workers get to witness the newly formed debt police in action chasing and beating up Richard’s grieving widower during his wake.

The debt police are exactly what they sound like: cops who come after people in debt. Cauley, a former writer for “The Daily Show With Trevor Noah” who has contributed to the New Yorker, has fun with this concept: she dresses them up in turquoise and makes them all obnoxiously hot and as annoying as the worst Angeleno cliché you can think of (they’re especially obsessed with overpriced new age treatments and diet culture). The cherry on top is their true apathetic evil. “These Leo moon incidents are always the worst,” a debt policeman says, for example, while literally beating Jada up.

Six months after she’s fired, Jada is making money by “eating food on camera in the hope that internet people, mostly guys, according to their screen names and Cash App handles, would pay [her] rent.” She eats shrimp for its pop and the way she can lick it; graham crackers for their whisper and crackle; almonds for their snap; celery sticks for their crunch. On the one hand, she’s paying her rent; on the other hand, her relationship to food has become sonically focused and exhausting.

The saving grace is that Jada manages to stay friends with her former Phoenix co-workers, Lanae (frontwoman of a punk band, the Donner Party) and Audrey (a runner and hacker in her spare time). Together, they come up with a plan to erase their own — and everyone else’s — student loan debt. It’s a heist, of sorts, except instead of getting rich, they’ll stop being in the hole for tens or hundreds of thousands of dollars. But the real pleasure, just like it is in any good heist movie, is witnessing the three women spending time together and becoming closer over the course of the book.

Jada is a deeply imperfect narrator. She’s quick to judge others, slow to trust, and even steals a watch on page 12 (Gasp! She’s a thief!) So, yes, she’s a messy millennial who has some issues to work through, but neither she nor anyone deserves to spend the rest of their life indebted to a system that claimed a college education as the only way to break into the middle class, and which instead ends up keeping so many from it.

The novel is a satire, of course, and the debt police are over the top because it’s generically appropriate, but also because Cauley is using humor to approach the horrifying reality that people really do go to prison for having debt in this country. And even when they don’t, student loan debt ends up increasing the racial wealth gap. According to the latest data from the Education Data Initiative, “Black and African American college graduates owe an average of $25,000 more in student loan debt than white college graduates.” Flash-forward four years after graduation, and “Black students owe an average of 188% more than white students.”

Yet the job of a novelist isn’t to hit you over the head with statistics but to entertain you — if you learn anything along the way or think more deeply about something you’d never considered, that’s great, but it’s not the main point. For all that it deals with systemic racism and economic precarity, “The Payback” is a terrifically fun book that made me laugh out loud at least once every chapter.

Masad, a books and culture critic, is the author of the novel “All My Mother’s Lovers” and the forthcoming novel “Beings.”

Jennifer Geerlings-Simons to lead the impoverished Latin American country through crisis before oil wealth arrives.

Suriname has elected Jennifer Geerlings-Simons as its first female president, with parliament backing the 71-year-old physician and lawmaker to lead the crisis-hit South American nation.

Her election came after a coalition deal was struck in the National Assembly, which voted by a two-thirds majority on Sunday.

The move followed inconclusive May polls and mounting pressure to replace outgoing President Chandrikapersad Santokhi, whose tenure was marred by corruption scandals and harsh austerity.

Geerlings-Simons, leader of the National Democratic Party, ran unopposed and will take office on July 16.

“I am aware that the heavy task I have taken on is further aggravated by the fact that I am the first woman to serve the country in this position,” she said after her confirmation.

She will be joined by running mate Gregory Rusland, as the pair inherit a country struggling under the weight of economic hardship, reduced subsidies, and widespread frustration. While Santokhi’s government managed to restructure debt and restore macroeconomic stability with IMF backing, it also triggered mass protests over deep cuts.

Jennifer Geerlings-Simons (C) greets parliamentarians after the National Assembly election in Paramaribo on July 6, 2025 [Ranu Abhelakh/AFP]

With Suriname expected to begin producing offshore oil in 2028, Geerlings-Simons has promised to focus on stabilising state finances. She has previously pledged to boost revenues by tightening tax collection, including from small-scale gold miners.

Economists warn she faces a rocky road ahead. Winston Ramautarsingh, former head of the national economists’ association, said Suriname must repay about $400m annually in debt servicing.

“Suriname does not have that money,” he said. “The previous government rescheduled the debts, but that was only a postponement.”

Geerlings-Simons will now be tasked with steering the Dutch-speaking country of 646,000 people through a fragile period, balancing public discontent with the promise of future oil wealth.

As Suriname prepares to mark 50 years since gaining independence from the Netherlands this November, the small South American country is pinning its hopes on a new era driven by oil wealth and deepening ties with China.

In 2019, it joined China’s Belt and Road Initiative, becoming one of the first Latin American states to sign on to the vast infrastructure project.

Suriname is one of the continent’s poorest nations, despite its rich ethnic tapestry that includes descendants of Africans, Indigenous groups, Indians, Indonesians, Chinese, and Dutch settlers.

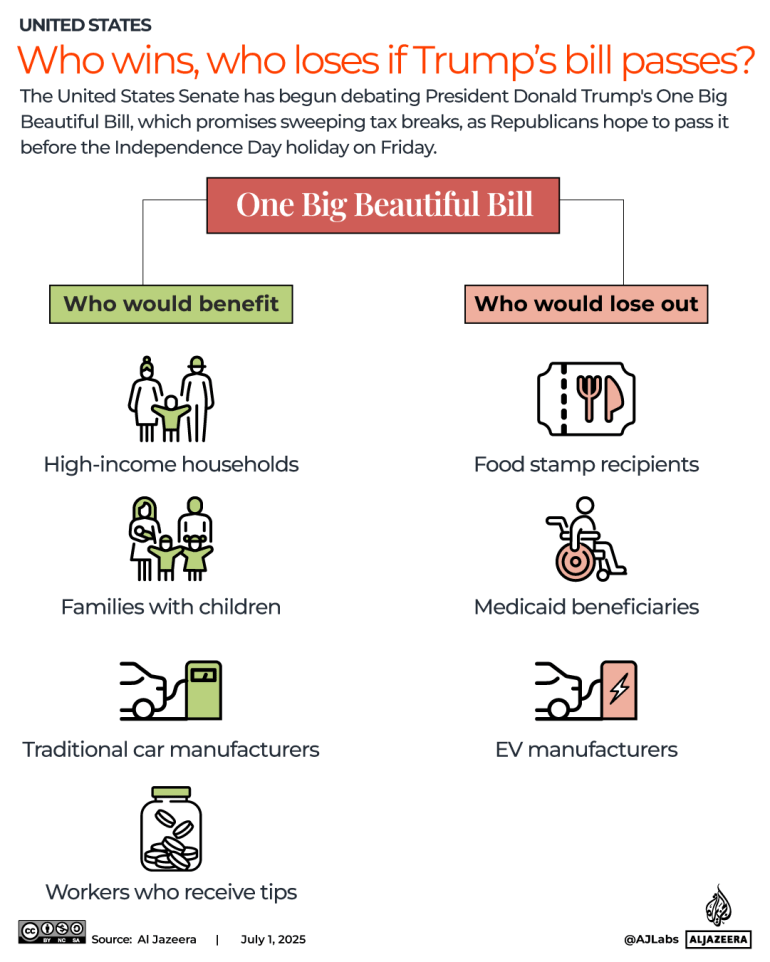

On July 3, the United States House of Representatives passed President Donald Trump’s signature tax cut and spending package, which he has called the “One Big Beautiful Bill“.

The bill combines tax reductions, spending hikes on defence and border security, and cuts to social safety nets.

Democratic Minority Leader Hakeem Jeffries warned that the bill “hurts everyday Americans and rewards billionaires with massive tax breaks”.

Trump’s erstwhile ally, billionaire Elon Musk, publicly opposed the bill, arguing it would bloat expenditure and the country’s already unmatched debt.

Trump is expected to sign the bill into law on Friday, July 4 – the US’s independence day – at 4pm ET.

Here’s what’s next – and whom the bill will affect:

How have taxes been lowered?

The main goal of the bill was to extend Trump’s first-term tax cuts.

In 2017, Trump signed the Tax Cuts and Jobs Act, which lowered taxes and increased the standard deduction for all taxpayers, primarily benefitting higher-income earners.

More than a third of the total cuts went to households with an income of $460,000 or more.

The top 1 percent (roughly 2.4 million people) received average tax cuts of about $61,090 by 2025 – higher than any other income group. By contrast, the middle 60 percent of earners (78 million people) saw cuts in the range of $380 to $1,800.

Those tax breaks were set to expire this year, but the new bill has made them permanent. It also adds some more cuts Trump promised during his latest campaign.

For instance, there is a change to the US tax code called the State and Local Taxes deduction.

This will let taxpayers deduct certain local taxes (like property taxes) from their federal tax return.

Currently, people can only deduct up to $10,000 of these taxes. The new bill would raise that cap from $10,000 to $40,000 for five years.

Taxpayers will also be allowed to deduct income earned from tips and overtime, until 2028, as well as interest paid on loans for buying cars made in the US from this year until 2028.

Elsewhere, the estate tax exemption will rise to $15m for individuals and $30m for married couples.

In all, the legislation contains about $4.5 trillion in tax cuts.

How big are social welfare cuts?

To help offset the cost of the tax cuts, Republicans plan to scale back Medicaid and food assistance programmes for low-income families.

Their stated goal was to focus these programmes on certain groups – primarily pregnant women, people with disabilities and children – while also reducing what they deem to be waste, including by limiting access to immigrants.

Currently, more than 71 million people depend on Medicaid, the government health insurance program.

According to the Congressional Budget Office (CBO), the bill would leave an additional 17 million Americans without health cover in the next decade.

While Medicaid helps Americans suffering from poor health, the Supplemental Nutrition Assistance Program (SNAP) helps poor people afford groceries.

About 40 million Americans currently receive benefits through SNAP, also known as food stamps.

The CBO calculates that 4.7 million SNAP participants will lose out over the 2025-2034 period, due to program reductions.

Changes to Medicaid and SNAP could become permanent provisions, with no sunset clauses attached to them.

A recent White House memo pointed to more than $1 trillion in welfare cuts from the new bill – the largest spending reductions to the US safety net in modern history.

Will there be new money for national security?

The bill sets aside about $350bn, to be spread out over several years, for Trump’s border and national security plans. This includes:

$46bn for the US-Mexico border wall

$45bn to fund 100,000 beds in migrant detention centres

Billions more to hire an extra 10,000 Immigration and Customs Enforcement (ICE) agents by 2029, as part of Trump’s plan to carry out the largest mass deportation effort in US history.

Will clean energy be affected?

Republicans have rolled back tax incentives that support clean energy projects powered by renewables like solar and wind, instead giving tax breaks to coal and oil companies.

These “green” tax breaks were a part of former President Joe Biden’s landmark Inflation Reduction Act, which aimed to tackle climate change and reduce healthcare costs.

A tax break for people who buy new or used electric vehicles will expire on September 30 this year, instead of at the end of 2032 under current law.

How will the bill affect the US debt profile?

The legislation would raise the debt ceiling by $5 trillion, from $36.2 trillion currently (which amounts to 122 percent of gross domestic product or GDP), going beyond the $4 trillion outlined in the version passed by the House in May.

Washington cannot borrow more than its stated debt ceiling. But since 1960, Congress has raised, suspended or changed the terms of the debt ceiling 78 times, facilitating more leverage and undermining the US’s long-term fiscal stability.

In his first term, Trump oversaw a roughly $8 trillion increase in the federal debt, which surged due to 2017 tax cuts and emergency spending, approved by Congress, during the COVID-19 pandemic.

Debt as a share of GDP was already higher last year than it was anytime outside of World War II, the aftermath of the 2008 financial crisis or the COVID-19 pandemic. Deficit concerns contributed to Moody’s downgrading of the US credit score in May.

For its part, the White House claims the new tax bill will reduce projected deficits by more than $1.4 trillion over the next decade, in part by spurring additional growth. But economists on both sides of the aisle have strongly disputed that.

Indeed, according to the non-partisan Committee for a Responsible Federal Budget, interest payments on national debt will rise to $2 trillion per year by 2034 owing to the legislation, crowding out spending on other goods and services.

How did the House of Representatives vote on the bill?

The lower house of the US Congress voted by a margin of 218 to 214 in favour of the bill on Thursday.

All 212 Democratic members of the House opposed the bill. They were joined by Representatives Thomas Massie of Kentucky and Brian Fitzpatrick of Pennsylvania, who broke from the Republican majority.

On July 1, the Senate narrowly passed the bill by a 51–50 vote, with the deciding vote cast by Vice President JD Vance.

Who will benefit the most?

According to Yale University’s Budget Lab, wealthier taxpayers are likely to gain more from this bill than lower-income Americans.

They estimate that people in the lowest income bracket will see their incomes drop by 2.5 percent, mainly because of cuts to SNAP and Medicaid, while the highest earners will see their incomes rise by 2.2 percent.

SEOUL — The third and final season of Netflix’s “Squid Game” broke viewership records on the streaming platform following its release on June 27, marking a fitting close for what has arguably been the most successful South Korean TV series in history.

Although reviews have been mixed, Season 3 recorded more than 60 million views in the first three days and topped leaderboards in all 93 countries, making it Netflix’s biggest launch to date.

“Squid Game” has been transformative for South Korea, with much of the domestic reaction focused not on plot but on the prestige it has brought to the country. In Seoul, fans celebrated with a parade to commemorate the show’s end, shutting down major roads to make way for a marching band and parade floats of characters from the show.

In one section of the procession, a phalanx of the show’s masked guards, dressed in their trademark pink uniforms, carried neon-lit versions of the coffins that appear on the show to carry away the losers of the survival game. They were joined by actors playing the contestants, who lurched along wearing expressions of exaggerated horror, as though the cruel stakes of the game had just been revealed to them.

At the fan event that capped off the evening, series creator Hwang Dong-hyuk thanked the show’s viewers and shared the bittersweetness of it all being over.

“I gave my everything to this project, so the thought of it all ending does make me a bit sad,” he said. “But at the same time, I lived with such a heavy weight on my shoulders for so long that it feels freeing to put that all down.”

Despite the overnight global fame “Squid Game” brought him (it’s Netflix’s most-watched series of all time), Hwang has spoken extensively about the physical and mental toil of creating the show.

Visitors take photos near a model of the doll named “Younghee” that’s featured in Netflix’s series “Squid Game,” displayed at the Olympic park in Seoul in October 2021.

(Lee Jin-man / Associated Press)

He unsuccessfully shopped the show around for a decade until Netflix picked up the first season in 2019, paying the director just “enough to put food on the table” — while claiming all of the show’s intellectual property rights. During production for the first season, which was released in 2021, Hwang lost several teeth from stress.

A gateway into Korean content for many around the world, “Squid Game” show served to spotlight previously lesser-known aspects of South Korean culture, bringing inventions like dalgona coffee — made with a traditional Korean candy that was featured in the show — to places such as Los Angeles and New York.

The show also cleared a path for the global success of other South Korean series, accelerating a golden age of “Hallyu” (the Korean wave) that has boosted tourism and exports of food and cosmetics, as well as international interest in learning Korean.

But alongside its worldly successes, the show also provoked conversations about socioeconomic inequality in South Korean society, such as the prevalence of debt, which looms in the backstories of several characters.

A few years ago, President Lee Jae-myung, a longtime proponent of debt relief, said, “‘Squid Game’ reveals the grim realities of our society. A playground in which participants stake their lives in order to pay off their debt is more than competition — it is an arena in which you are fighting to survive.”

In 2022, the show made history as the first non-English-language TV series and the first Korean series to win a Screen Actors Guild Award, taking home three in total. It also won six Emmy Awards. That same year, the city of L.A. designated Sept. 17 — the series’ release date — as “Squid Game Day.“

Although Hwang has said in media interviews that he is done with the “Squid Game” franchise, the Season 3 finale — which features Cate Blanchett in a cameo as a recruiter for the games that are the show’s namesake — has revived rumors that filmmaker David Fincher may pick it up for an English-language spinoff in the future.

While saying he had initially written a more conventional happy ending, Hwang has described “Squid Game’s” final season as a sobering last stroke to its unsparing portrait of cutthroat capitalism.

“I wanted to focus in Season 3 on how in this world, where incessant greed is always fueled, it’s like a jungle — the strong eating the weak, where people climb higher by stepping on other people’s heads,” he told The Times’ Michael Ordoña last month.

“Coming into Season 3, because the economic system has failed us, politics have failed us, it seems like we have no hope,” he added. “What hope do we have as a human race when we can no longer control our own greed? I wanted to explore that. And in particular, I wanted to [pose] that question to myself.”

Donald Trump says his sweeping tax cuts will grow the economy. But, critics say the bill will increase national debt.

Dubbed the “One Big Beautiful Bill Act”, President Donald Trump’s signature policy bill would slash taxes, largely benefitting the wealthiest Americans.

To pay for it, federal spending would be reduced, including on Medicaid, food stamps and student loans. Supporters say the bill could jumpstart economic growth and create jobs.

Critics, including some Republicans, say millions of Americans would pay the price. And the non-partisan Congressional Budget Office estimates the bill would actually add an estimated $3.3 trillion to debt over a decade.

Why did Canada scrap its digital tax on US tech companies?

The United States Senate narrowly passed President Donald Trump’s massive tax and spending bill on Tuesday, following intense negotiations and a marathon voting session on amendments.

The bill, which still faces a challenging path to final approval in the House of Representatives, would impose deep cuts to popular health and nutrition programmes, among other measures, while offering $4.5 trillion in tax reductions.

The measure was approved after almost 48 hours of debate and amendment battles.

Here is what you need to know:

What is Trump’s ‘Big, Beautiful Bill’?

The bill is a piece of legislation that combines tax cuts, spending hikes on defence and border security, and cuts to social safety nets into one giant package.

The main goal of the bill is to extend Trump’s 2017 tax cuts, which are set to expire at the end of 2025. It would make most of these tax breaks permanent, while also boosting spending on border security, the military and energy projects.

The bill is partly funded by cutting healthcare and food programmes.

The nonpartisan Congressional Budget Office estimates Trump’s measure will increase the US debt by $3.3 trillion over the next 10 years. The US government currently owes its lenders $36.2 trillion.

The key aspects of the bill include:

Tax cuts

In 2017, Trump signed the Tax Cuts and Jobs Act, which lowered taxes and increased the standard deduction for all taxpayers, but it primarily benefitted higher-income earners.

Those tax breaks are set to expire this year, but the new bill would make them permanent. It also adds some more cuts he promised during his campaign.

There is a change to the US tax code called the SALT deduction (State and Local Taxes). This lets taxpayers deduct certain state and local taxes (like income or property taxes) on their federal tax return.

Currently, people can only deduct up to $10,000 of these taxes. The new bill would raise that cap from $10,000 to $40,000 for five years.

Taxpayers would also be allowed to deduct income earned from tips and overtime, as well as interest paid on loans for buying cars made in the US.

The legislation contains about $4.5 trillion in tax cuts.

Children

If the bill does not become law, the child tax credit – which is now $2,000 per child each year – will fall to $1,000, starting in 2026.

But if the Senate’s current version of the bill is approved, the credit would rise to $2,200.

Border wall and security

The bill sets aside about $350bn for Trump’s border and national security plans. This includes:

$46bn for the US-Mexico border wall

$45bn to fund 100,000 beds in migrant detention centres

Billions more to hire an extra 10,000 Immigration and Customs Enforcement (ICE) agents by 2029 as part of Trump’s plan to carry out the largest mass deportation effort in US history.

Cuts to Medicaid and other programmes

To help offset the cost of the tax cuts and new spending, Republicans plan to scale back Medicaid and food assistance programmes for low-income families.

They say their goal is to refocus these safety net programmes on the groups they were originally meant to help, primarily pregnant women, people with disabilities and children – while also reducing what they call waste and abuse.

Medicaid helps Americans who are poor and those with disabilities, while the Supplemental Nutrition Assistance Program (SNAP) helps people afford groceries.

Currently, more than 71 million people depend on Medicaid, and 40 million receive benefits through SNAP. According to the Congressional Budget Office, the bill would leave an additional 11.8 million Americans without health insurance by 2034 if it becomes law.

Clean energy tax cuts

Republicans are pushing to significantly scale back tax incentives that support clean energy projects powered by renewables like solar and wind. These tax breaks were a key part of former President Joe Biden’s landmark 2022 law, the Inflation Reduction Act, which aimed to tackle climate change and reduce healthcare costs.

A tax break for people who buy new or used electric vehicles would expire on September 30 this year if the bill passes in its current form, instead of at the end of 2032 under current law.

Debt limit

The legislation would raise the debt ceiling by $5 trillion, going beyond the $4 trillion outlined in the version passed by the House in May.

Who benefits most?

According to Yale University’s Budget Lab, wealthier taxpayers are likely to gain more from this bill than lower-income Americans.

They estimate that people in the lowest income bracket will see their incomes drop by 2.5 percent, mainly because of cuts to SNAP and Medicaid, while the highest earners will see their incomes rise by 2.2 percent.

Which senators voted against the bill?

Republican Senator Susan Collins of Maine opposed due to deep Medicaid cuts affecting low-income families and rural healthcare.

I strongly support extending the tax relief for families and small businesses. My vote against this bill stems primarily from the harmful impact it will have on Medicaid, affecting low-income families and rural health care providers like our hospitals and nursing homes.

— Sen. Susan Collins (@SenatorCollins) July 1, 2025

Republican Senator Thom Tillis of North Carolina cited concerns over Medicaid reductions to his constituents. Tillis has announced that he will not seek re-election, amid threats from Trump that he would back a Republican challenger to Tillis.

The facts matter. The people matter. The Senate’s Medicaid approach breaks promises and will kick people off of Medicaid who truly need it. The Senate can make one simple fix to make sure that won’t happen. pic.twitter.com/zvW1AgCxBF

— Senator Thom Tillis (@SenThomTillis) June 30, 2025

Republican Senator Rand Paul of Kentucky voted “no” on fiscal grounds, warning that the bill would significantly worsen the national deficit.

Throughout the Vote-a-rama, I was working all night to stop Congress from adding to our debt.

I met with @VP and I reiterated my offer to vote for the bill—if it included a 90% reduction in the debt ceiling.

No earmarks. No handouts. Just real fiscal reform.

Every member of the Democratic caucus, a total of 47 senators, also voted against the bill.

Who supported the bill in the Senate?

The remaining Republicans voted in favour, allowing the bill to pass 51–50, with the deciding vote cast by Vice President JD Vance.

Trump has set a July 4 deadline to pass the bill through Congress, but conceded on Tuesday that it would be “very hard to do” by that date, since the House now needs to vote on it. The House had passed an earlier version of the bill in May, but needs to look at it again due to the amendments brought by the Senate.

Notable Senator supporters include:

Senator Lisa Murkowski (representative of Alaska): Her backing was secured after Republicans agreed to Alaska-specific provisions, including delayed nutrition cuts and a new rural health fund, making her vote pivotal.

“I have an obligation to the people of the state of Alaska, and I live up to that every single day,” she told a reporter for NBC News.

Senators Rick Scott of Florida, Mike Lee of Utah, Ron Johnson of Wisconsin and Cynthia Lummis of Wyoming: These fiscally conservative senators shifted from hesitation to support following amendments to the bill.

Senate Majority Leader John Thune led the push to pass the legislation.

How have lawmakers and the public reacted?

Most Republican lawmakers celebrated it as a historic achievement.

Trump also expressed delight.

“Wow, music to my ears,” Trump said after a reporter told him the news. “I was also wondering how we’re doing, because I know this is primetime, it shows that I care about you,” he added.

Thune said after the vote: “In the end, we got the job done, and we’re delighted to be able to be partners with President Trump and his agenda.”

Democrats opposed it, calling it a giveaway to the wealthy at the expense of healthcare, food aid and climate policy.

“Today’s vote will haunt our Republican colleagues for years to come,” Democrat Chuck Schumer said in a floor speech after the vote.

“Republicans covered this chamber in shame,” he added.

Today’s vote will haunt Senate Republicans for years to come.

Americans will see the damage done as hospitals close, as people are laid off, as costs go up, and as the debt increases.

Democrats will make sure Americans remember the betrayal that took place today. pic.twitter.com/WmwnZa5n9k

The US Chamber of Commerce led a coalition of more than 145 organisations supporting the bill, emphasising it would “foster capital investment, job creation, and higher wages”.

They praised the permanent tax cuts and border security funding.

However, healthcare and hospital associations have warned that millions could lose coverage, driving up emergency and unpaid care costs. Environmental groups have also voiced strong opposition.

Public opinion on the bill is in decline, too.

“Initially, [Trump] had more than 50 percent of the support. Now, it is under 50 percent, and politicians know that,” Al Jazeera’s Alan Fisher said, reporting from Washington, DC.

“They are aware that this could lead to a cut in Medicaid. They are aware, even though Donald Trump had promised to protect it, that this could cut nutritional programmes, particularly for poorer families in the United States.

“And although they will get tax cuts, they have managed a lot of the time to be convinced by the Democratic argument that, yes, there are tax cuts, but billionaires will do much better out of this than the ordinary American people, and that is what’s changed the opinion polls,” he added.

What happens next?

The process begins with the House Rules Committee, which will meet to mark up the bill and decide how debate and consideration will proceed on the House floor.

After the bill passes through the Rules Committee, it will move to the House floor for debate and a vote on the rule, potentially as soon as Wednesday morning.

If the House of Representatives does not accept the Senate’s version of the bill, it could make changes and send it back to the Senate for another vote.

Alternatively, both chambers could appoint members to a conference committee to work out a compromise.

Once both the House and Senate agree on the final text, and it is passed in both chambers of Congress, the bill would go to Trump to be signed into law.

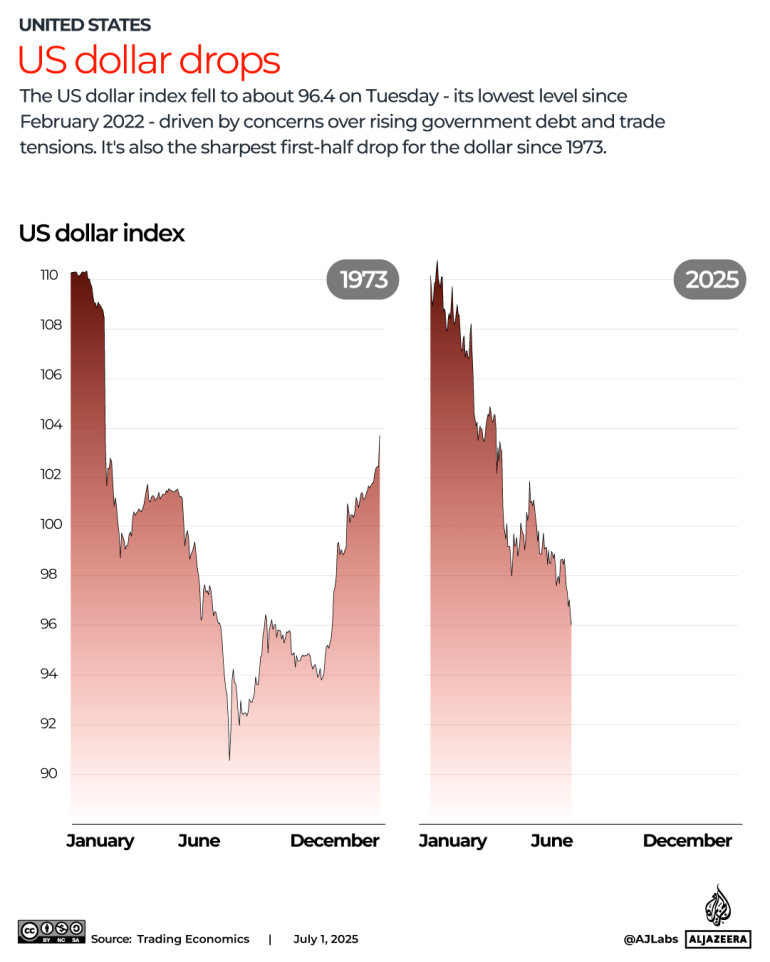

The United States dollar has had its worst first six months of the year since 1973, as President Donald Trump’s economic policies have prompted global investors to sell their greenback holdings, threatening the currency’s “safe-haven” status.

The dollar index, which measures the currency’s strength against a basket of six others, including the pound, euro and yen, fell 10.8 percent in the first half of 2025.

President Trump’s stop-start tariff war, and his attacks that have led to worries over the independence of the Federal Reserve, have undermined the appeal of the dollar as a safe bet. Economists are also worried about Trump’s “big, beautiful” tax bill, currently under debate in the US Congress.

The landmark legislation is expected to add trillions of dollars to the US debt pile over the coming decade and has raised concerns about the sustainability of Washington’s borrowing, prompting an exodus from the US Treasury market.

Meanwhile, gold has hit record highs this year, on continued buying by central banks worried about devaluation of their dollar assets.

What has happened to the dollar?

On April 2, the Trump administration unveiled tariffs on imports from most countries around the world, denting confidence in the world’s largest economy and causing a selloff in US financial assets.

More than $5 trillion was erased from the value of the benchmark S&P 500 index of shares in the three days after “Liberation Day”, as Trump described the day of his tariffs announcement. US Treasuries also saw clear-outs, lowering their price and sending debt costs for the US government sharply higher.

Faced with a revolt in financial markets, Trump announced a 90-day pause on tariffs, except for exports from China, on April 9. While trade tensions with China – the world’s second-largest economy – have since eased, investors remain wary of holding dollar-linked assets.

Last month, the Organisation for Economic Co-operation and Development (OECD) announced that it had cut its US growth outlook for this year from 2.2 percent in March to just 1.6 percent, even as inflation has slowed.

Looking ahead, Republican leaders are trying to push through Trump’s One Big Beautiful Bill Act through Congress before July 4. The bill would extend Trump’s 2017 tax cuts, slash healthcare and welfare spending and increase borrowing.

While some legislators believe it could take until August to pass the bill, the aim would be to raise the borrowing limit on the country’s $36.2 trillion debt pile. The non-partisan Congressional Budget Office said it would raise Federal debt by $3.3 trillion by 2034.

That would significantly raise the government’s debt-to-GDP (gross domestic product) ratio from 124 percent today, raising concerns about long-term debt sustainability. Meanwhile, annual deficits – when state spending exceeds tax revenues – would rise to 6.9 percent of GDP from about 6.4 percent in 2024.

So far, Trump’s attempts to lower spending through Elon Musk’s Department of Government Efficiency have fallen short of expectations. And though import tariffs have raised revenue for the government, they’ve been paid for – in the form of higher costs – by American consumers.

The upshot is that Trump’s unpredictable policies, which prompted Moody’s rating agency to strip the US government of its top credit score in May, have slowed US growth prospects this year and dented the demand for its currency.

The dollar has also trended down on expectations that the Federal Reserve will cut interest rates to support the United States’ economy, urged on by Trump, with two to three reductions expected by the end of this year, according to levels implied by futures contracts.

Is the US becoming a ‘less attractive’ destination?

Owing to its dominance in trade and finance, the dollar has been the world’s currency anchor. In the 1980s, for instance, many Gulf countries began pegging their currencies to the greenback.

Its influence doesn’t stop there. Though the US accounts for one-quarter of global GDP, 54 percent of world exports were denominated in dollars in 2023, according to the Atlantic Council.

Its dominance in finance is even greater. About 60 percent of all bank deposits are denominated in dollars, while nearly 70 percent of international bonds are quoted in the US currency.

Meanwhile, 57 percent of the world’s foreign currency reserves – assets held by central banks – are held in dollars, according to the IMF.

But the dollar’s reserve status is supported by confidence in the US economy, its financial markets and its legal system.

And Trump is changing that. Karsten Junius, chief economist at Bank J Safra Sarasin, says “investors are beginning to realise that they’re over-exposed to US assets.”

Indeed, foreigners own $19 trillion of US equities, $7 trillion of US Treasuries and $5 trillion of US corporate bonds, according to Apollo Asset Management.

If investors continue to trim their positions, the dollar’s value could continue to come under sustained pressure.

“The US has become a less attractive place to invest these days… US assets are not as safe as they used to be,” Junius told Al Jazeera.

What are the consequences of a lower-value dollar?

Many within the Trump administration argue that the costs of the US dollar’s reserve status outweigh the benefits – because that raises the cost of US exports.

Stephen Miran, chair of Trump’s Council of Economic Advisers, has said high dollar valuations place “undue burdens on our firms and workers, making their products and labour uncompetitive on the global stage”.

“The dollar’s overvaluation has been one factor contributing to the US’s loss of competitiveness over the years, and… tariffs are a reaction to this unpleasant reality,” he added.

At first blush, a lower dollar would indeed make US goods cheaper to overseas buyers and make imports more expensive, helping to reduce the country’s trade deficits. However, these typical trade effects remain in flux due to ongoing tariff threats.

For developing countries, a weaker greenback will lower the local currency cost of repaying dollar debt, providing relief to heavily indebted countries like Zambia, Ghana or Pakistan.

Elsewhere, a weaker dollar should boost commodity prices, increasing export revenues for countries exporting oil, metals or agricultural goods such as Indonesia, Nigeria and Chile.

Have other currencies done well?

Since the start of Trump’s second term in office, the greenback’s slide has upended widespread predictions that his trade war would do greater damage to economies outside the US, while also spurring US inflation – strengthening the currency against its rivals.

Instead, the euro has risen 13 percent to above $1.17 as investors continue to focus on growth risks inside the US. At the same time, demand has risen for other safe assets like German and French government bonds.

For American investors, the weaker dollar has also encouraged equity investments abroad. The Stoxx 600 index, a broad measure across European stocks, has risen roughly 15 percent since the start of 2025.

Converted back into dollars, that gain amounts to 23 percent.

Meanwhile, inflation – again belying predictions – has come down from 3 percent in January to 2.3 percent in May.

According to Junius, there is no significant threat to the dollar’s status as the world’s de facto reserve currency anytime soon.

But “that doesn’t mean that you can’t have more of a weakening in the US dollar,” he said. “In fact, we continue to expect that between now and the end of the year.”

Billionaire Elon Musk said on Monday that he would form a new political party in the United States if a Republican-leaning Congress passes President Donald Trump’s “One Big Beautiful Bill”, which proposes tax breaks and funding cuts for healthcare and food programmes.

Musk has voiced criticism of the bill on multiple occasions over the past month and began suggesting the idea of the new party on social media starting early June.

Here is more about Musk’s reservations about the bill, and about his new proposed party.

What has Musk said about the America Party?

Musk has been saying that if the bill is passed, Republicans are no different from Democrats, who are often accused by conservatives of being profligate with spending taxpayers’ dollars.

The version of the bill that the Senate is discussing at the moment, if passed by both chambers of Congress, would expand the national debt by $3.3 trillion between 2025 and 2034. The current US national debt stands at more than $36 trillion.

“If this insane spending bill passes, the America Party will be formed the next day,” Musk posted on his social media platform, X, on Monday.

“Our country needs an alternative to the Democrat-Republican uniparty so that the people actually have a VOICE.”

In an earlier post, Musk wrote: “It is obvious with the insane spending of this bill, which increases the debt ceiling by a record FIVE TRILLION DOLLARS that we live in a one-party country – the PORKY PIG PARTY!!”

The debt ceiling, set by the US Congress, determines the upper limit to the amount of money that the US Treasury can borrow. The current debt limit is $36.1 trillion.

Why does Musk oppose the bill?

Once a key aide and major campaign donor for Trump, Musk had a public online falling out with the president in June over his criticism of the bill.

On June 3, Musk wrote on X: “I’m sorry, but I just can’t stand it anymore. This massive, outrageous, pork-filled Congressional spending bill is a disgusting abomination.”

Musk alleged that Trump was linked to disgraced financier Jeffrey Epstein in a now-deleted post on X. However, Trump and Musk seemed to have reached a detente when Trump told reporters that he wished Musk well while the latter wrote on X on June 11 that he had gone “too far” in his criticism of the US president.

However, since then, Musk has argued in a series of online posts that the bill would increase the debt ceiling, “bankrupt America”, and “destroy millions of jobs in America”.

Musk owns the electric vehicle (EV) manufacturer Tesla. The current version of the bill, with amendments made by the Senate, seeks to end the tax credit for purchases of EVs worth up to $7,500, starting on September 30. This could reduce the consumer demand for EVs in the US.

What is the America Party that Musk proposed?

On June 5, Musk posted a poll on his X account, asking his followers: “Is it time to create a new political party in America that actually represents the 80 percent in the middle?”

While social media polls are known to be nonrepresentative of broader public sentiment, 5.6 million people voted on the poll, and 80.4 percent responded with “yes”. Since then, Musk has repeatedly reposted the poll result, citing it as evidence that most Americans want a new party to be formed.

“Musk believes that 80 percent of Americans are unhappy with the two major parties and are not being represented,” Natasha Lindstaedt, a professor at the Department of Government, the University of Essex, told Al Jazeera.

While that number might not reflect the wider American public, it does point to a trend in the electorate; according to a Gallup poll from 2024, 43 percent of Americans identified as independent, 28 percent identified as Republican and 28 percent identified as Democrat. In other words, more Americans identify as independent than as either Democrat or Republican.

One of Musk’s followers replied to a post on X with an image with the text “America Party”. The world’s richest man responded: “‘America Party’ has a nice ring to it. The party that actually represents America!”

How real is Musk’s threat?

Experts say Musk, whose net worth is $363bn as of Monday according to the Bloomberg Billionaires Index, would realistically be able to fund a third party in the US. However, it is still unclear whether he would go ahead with his plan or whether his party would have a significant effect on US elections.

“Musk certainly has the financial power to back a third party that could be very disruptive to the Republican Party, but it’s not certain if Musk will take on this risk,” Lindstaedt said.