BRITAIN must join the fight against Hamas and not reward terror by recognising a Palestinian state, the former chief of Mossad has said.

Veteran Israeli spy Yossi Cohen vowed to eradicate every last enemy fighter in Gaza – as he fumed that Israel is “doing the world’s job alone”.

12

Yossi Cohen, former director of Mossad, during an interview with The SunCredit: Ian Whittaker

12

Hamas fighters standing in formation as Israeli hostages were handed over to the Red Cross in February earlier this yearCredit: AP

12

UK Prime Minister Keir Starmer has been criticised for his move to recognise a Palestinian stateCredit: Getty

Mr Cohen demanded to know why Britain and other countries were not helping Israel after joining previous fights against other terror groups.

Sitting down with The Sun, he said: “The big question is, will you join us?

“More than 70 countries, including Britain, fought together to defeat one terror organisation with ISIS, and you joined the war against the Taliban in Afghanistan.

“How many armies are fighting with us alongside Hamas? None. The state of Israel is doing the world’s job alone. You’re invited.”

read more on israel hamas war

With or without the support, Mr Cohen said he will hunt down every last Hamas fighter, vowing: “If there are 100 Hamas fighters left in Gaza City… I’ll find them for you.”

Successive UK governments have vowed to recognise a Palestinian state at the point of most impact as part of a peace process – and Starmer felt the time was now.

The PM said the decision was in aid of a two-state solution, which is the “opposite” of what Hamas wants – though the terror group still claimed it as a victory.

But Mr Cohen said the move by Starmer was cynical.

Ex-Mossad chief BACKS Blair to be new ‘Governor of Gaza’ in Trump-approved postwar plan for terror-ravaged strip

It was designed to “strengthen” support for the Labour government at home, Mr Cohen claimed, while serving no purpose on the world stage.

He speculated that Starmer felt forced into the decision to “keep people quiet” in the UK – rather than it being “from his heart”.

“If Hamas are the UK’s partners, that’s very sad,” Mr Cohen said.

Cohen dismissed the declaration as toothless because it is “legally impossible” for other countries to mandate a two-state solution.

Referring to the Oslo Accords of 1993, the only standing agreement Israel has with the Palestinian Authority, he insisted that decisions about statehood may only be made between Israel’s government and the PA.

12

Mr Cohen insists the suffering is a result of Hamas terrorists embedding themselves within civilian infrastructureCredit: Ian Whittaker

12

Almost 70,000 people have been killed in the Gaza Strip and many more woundedCredit: Getty

12

Hundreds of thousands of people are being forced to move south as Israel expands its offensive in Gaza CityCredit: AFP

Earlier this year, Trump also suggested recognising the Palestinian state would risk “rewarding Hamas”.

Cohen said there is a history of governments, including the British, saying one thing to their population and another thing to Israel behind closed doors – and that he “hopes” that remains the case.

He revealed that, in his former roles, he met with foreign diplomats who would be appreciative during private meetings – only to later release “the filthiest statements” about Israel.

‘We take care of Gazans’

Directly addressing the hundreds of thousands of Brits who regularly take to the streets as part of pro-Palestinian marches, Mr Cohen said: “Israel is conducting a just war. This is absolutely the right thing that we have to do.

“Intentionally, we do not kill civilians. Intentionally, we do not starve anyone. Intentionally, we’re taking care of the Gazan people.”

12

Mr Cohen vowed that Israel would hunt down every last Hamas fighterCredit: Alamy

12

The IDF has expanded its offensive in Gaza CityCredit: Alamy

Mr Cohen even claimed he had received criticism in Israel for helping bring in financial support for Gazans from donors.

“Why is it that we do that? Because we do care about the Gazan people,” he insisted.

A United Nations commission determined this month that Israel is committing genocide in Gaza.

Israel’s conduct in the war has faced increased scrutiny over the past year as the humanitarian crisis in Gaza deepens.

Reflecting on why there is such a gulf in feeling between Israel’s public and Brits, Mr Cohen said his country is still reeling from the atrocities committed on October 7 – with hostages still being kept in Gaza.

He said: “Civilians were killed and butchered. Babies included, burned in their beds, raped. The atrocities that we’ve seen are on a different scale.

“This is the reaction of a normal country. We are a normal country.

“Demonstrators will demonstrate whether Israel conducts itself rightly or wrongly. This is part of their agenda.”

Civilians were killed and butchered. Babies included, burned in their beds, raped. The atrocities that we’ve seen are on a different scale

Yossi CohenFormer director of Mossad

Hundreds of civilians in Gaza are being killed every week in air strikes and shootings.

Israel has repeatedly blamed Hamas for the high civilian death toll – claiming the people of Gaza are being used as human shields.

The IDF has recently expanded its military operation in Gaza City where hundreds of thousands of civilian remain.

Confronted with this fact, Mr Cohen said: “The type of war that we conduct is hard.

“It is not something that you can even imagine when you have terrorists living together with kids and babies in kindergartens, UN facilities, hospitals, clinics, and any other thing.

“They just conquered everything, every single house in the region, to create a kind of a terror activity in within.

“So it’s hard to do, but I know for sure that the state of Israel is doing its best to make sure that the Gazan people will not be hurt.”

What does recognising Palestine mean?

BRITAIN’S recognition means that the UK government diplomatically acknowledges Palestine as a country.

The UK had already vowed to recognise a Palestinian state as part of a broader peace process with Israel, but it was long unclear when this might happen.

It does not mean that the UK no longer recognises Israel, with which Britain has had official diplomatic relations since the 1950s.

But Palestine now joins the list of nations formally recognised by Britain, meaning its chief envoy will now have the rank of ambassador.

The conflict between Israel and Palestine stretches back many decades, and it is still unclear what the borders of a Palestinian state would look like.

The West Bank, the Gaza Strip and East Jerusalem are frequently described as occupied Palestinian territories.

But Israel de facto controls much of this land, and has built substantial settlements in the West Bank and East Jerusalem.

Control of Palestinian territory is divided, with Hamas solely ruling over the Gaza Strip.

Almost 70,000 people have been killed in Gaza since October 7, according to Gaza’s Ministry of Health and the Israeli Ministry of Foreign Affairs.

The ex spy master served as Benjamin Netanyahu’s national security advisor – and has hinted at aspirations to become the next Prime Minister of Israel, or returning to the government in some capacity.

“If Netanyahu wants to use me or to use my capabilities… of course he can do that,” Mr Cohen said. “He knows my phone number.”

Hinting at Netanyahu’s handing of the war, he added: “I think the people of Israel need a change that is basically founded on the need of unification.

“It is getting a little bit too intense to my taste.”

12

Yossi Cohen pictured with Sun reporter Patrick HarringtonCredit: Ian Whittaker

12

A wounded man lies in a vehicles as displaced Palestinians move with their belongingsCredit: AFP

12

Smoke rises from an Israeli airstrike in northern GazaCredit: EPA

Blair has reportedly pitched a plan to Donald Trump which would see him lead a Gaza International Transitional Authority (GITA) overseeing the strip before handing over to the Palestinian Authority.

Cohen told us it was an “amazing move from Blair”, and insisted they would work well together.

He said: “This is the main problem – what do we do the day after? And who is going to take care of the close to 2.2 million people?

“We need someone to run the show in the Gaza Strip and stop it deteriorating into the hands of Hamas.

“Tony Blair‘s initiative and willingness to do that is highly appreciated. God bless him.”

Recognition of Palestinian state is ‘hollow gesture’

By Martina Bet, Political Correspondent

SIR Keir Starmer’s recognition of Palestine is being hailed by his allies as “historic”, but the question is what it actually achieves.

It is hard to see it as anything more than a hollow gesture.

It will not free a single hostage, feed a starving family in Gaza, or stop Israel’s bombardment.

The PM knows this, his own deputy, David Lammy, has admitted it. The move smacks of politics at home, throwing red meat to Labour’s left rather than solving a decades-old conflict.

It hands Hamas a propaganda victory and enrages Israel, while doing nothing to bring the two sides closer to peace.

Worse, it drives a wedge with Washington, where Donald Trump has made clear the US will never follow Britain’s lead.

Without America, a two-state solution is dead on arrival and for all the lofty talk, Starmer’s “historic” move looks like empty grandstanding.

12

Much of the Gaza strip has been decimated after nearly two years of bombardmentCredit: EPA

United Parcel Service is deeply out of favor, but it provides a vital service and is preparing for a brighter future.

United Parcel Service(UPS 1.38%), which usually just goes by UPS, has a huge dividend yield of 7.9%. Many investors are likely attracted to it as a dividend stock, but that’s a risky call. It is more appropriate to see this package delivery giant as a turnaround stock. And if that’s how you view it, now could be the time to hit the buy button.

What UPS does is hard to do

Without getting into the logistical details, moving packages quickly and cost-effectively is very difficult. Even after huge capital investments in its own delivery service, Amazon still uses UPS. But Wall Street has a habit of going to extremes, which is a big part of why UPS could be an attractive turnaround stock.

Image source: Getty Images.

During the pandemic, package demand spiked. Investors extrapolated that demand far into the future, bidding up UPS’ stock price. Demand slowed, and UPS’ stock price crumbled when the world learned to live with COVID-19. UPS chose to start a major business overhaul as demand was returning to normal levels. The goal is to increase the use of technology to cut costs and to refocus on the company’s most profitable business lines to increase profit margins.

This is a multiyear effort with material up-front costs. And exiting low-margin business will lower sales even as it helps improve profitability. (Notably, UPS has chosen to proactively reduce its business relationship with Amazon.) Financial results have been ugly lately, which is what you’d expect. An over 97% dividend payout ratio, however, hints that most income investors should tread with caution.

However, there are positives starting to show through. For example, revenue per piece increased 5.5% in the U.S. business during the second quarter of 2025. That could be signaling that deeply out of favor UPS stock is turning a corner and is, thus, ripe for an upturn as investors get more confident in its business overhaul.

Reuben Gregg Brewer has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Amazon and United Parcel Service. The Motley Fool has a disclosure policy.

The long-term data for stock market returns paints a clear picture.

The Vanguard Total Stock Market Index Fund ETF(VTI 0.21%) is one of the most popular exchange-traded funds (ETFs) on the planet. The fund has net assets of nearly $2 trillion.

With stock indexes hovering near all-time highs, many investors are worried that this historically successful ETF will struggle in the years to come. But there’s one critical piece of data that suggests otherwise.

This ETF remains a data-backed investment

The Vanguard Total Stock Market Index Fund ETF is a classic pick for savvy long-term investors. That’s because the ETF tracks the holdings of the CRSP US Total Market Index, which includes almost every type of company imaginable — everything from small-caps and large-caps to value stocks and growth stocks.

The ETF is incredibly diversified with more than 3,000 holdings, but investors should note that only U.S. companies are included. Many of those U.S. companies, however, have global operations, providing some level of international diversification.

Image source: Getty Images.

With an expense ratio of just 0.03%, the Vanguard Total Stock Market Index Fund ETF is one of the cheapest ways investors can get broad access to nearly the entire stock market. But with the indexes already at all-time highs, is this ETF still a smart pick? If your holding period is 20 years or more, the answer is absolutely. That’s because there has never been a 20-year period where the U.S. stock market has posted a negative return.

Of course, returns for any given 20-year period vary widely. But here’s a good example of how buying market indexes like this, even at their peaks, is a wise long-term decision. If you purchased shares of VTI in 2007 at their pre-cash peak, you still would have accumulated a 338% return over the next 18 years. So long-term investors can rejoice: The Vanguard Total Stock Market Index Fund ETF remains a solid pick for the decades ahead.

Ryan Vanzo has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Vanguard Total Stock Market ETF. The Motley Fool has a disclosure policy.

This technology company’s share price crashed recently, creating a buying opportunity for investors.

Electronic design automation (EDA) and engineering simulation software company Synopsys(SNPS -4.08%) recently released a disappointing set of third-quarter earnings, resulting in a collapse in its share price. As ever, Wall Street analysts immediately rushed to lower price targets.

But here’s the thing. Generally, the adjusted price targets remain significantly above the current price. Of the 22 analysts covering the stock, 18 have “buy” or “outperform” ratings, while one has an “underperform” rating.

Wall Street still loves Synopsys

The price targets on the post-earnings analyst updates range from Piper Sandler’s $630 to Berenberg’s $500. This compares to the current price of almost $500 and a post-earnings price of below $390.

One possible reason why Wall Street remains obsessed (in a good way) with the stock is that the problems revealed in the update relate to its smaller Design Intellectual Property (IP) segment. In contrast, its core EDA segment (sales up 23.5% year over year) is performing well, and the exciting recent addition of engineering simulation software company Ansys adds a new growth dimension.

The idea is that Ansys’ broader range of end-market customers will naturally align with Synopsys’ core EDA business as more industries and customers begin to incorporate semiconductors and AI-driven applications into their products. As such, the opportunity to offer what Synopsys management calls “silicon to systems” solutions to customers has a natural appeal. Customers can both design chips with Synopsys’ EDA and test the interactions between these chips and their embedded products.

Image source: Getty Images.

Where next for Synopsys?

It will take time for management to turn things around in the Design IP segment, but a few quarters of ongoing growth in EDA, combined with the successful integration of Ansys, will help strengthen the long-term case for the company. Wall Street believes that the potential of the latter outweighs the downside risk associated with the former.

Lee Samaha has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Synopsys. The Motley Fool has a disclosure policy.

Obviously, both things can’t be true, so which is it?

That depends on which of the polls you choose to believe.

Political junkies, and the news outlets that service their needs, abhor a vacuum. So there’s no lack of soundings that purport to show just where Californians’ heads are at a mere six weeks before election day — which, in truth, is not all that certain.

Newsom’s pollster issued results showing Prop. 50 winning overwhelming approval. A UC Berkeley/L.A. Times survey showed a much closer contest, with support below the vital 50% mark. Others give the measure a solid lead.

Not all polls are created equal.

“It really matters how a poll is done,” said Scott Keeter, a senior survey advisor at the Pew Research Center, one of the country’s top-flight polling organizations. “That’s especially true today, when response rates are so low [and] it’s so difficult to reach people, especially by telephone. You really do have to consider how it’s done, where it comes from, who did it, what their motivation is.”

Longtime readers of this space, if any exist, know how your friendly columnist feels about horse-race polls. Our best advice remains the same it’s always been: Ignore them.

Realizing, however, the sun will keep rising and setting, that tides will ebb and flow, that pollsters and pundits will continue issuing their prognostications to an eager and ardent audience, here are some suggestions for how to assay their output.

The most important thing to remember is that polls are not gospel truth, flawless forecasts or destiny carved in implacable stone. Even the best survey is nothing more than an educated guess at what’s likely to happen.

That said, there are ways to evaluate the quality of surveys and determine which are best consumed with a healthy shaker of salt and which should be dismissed altogether.

Given the opportunity, take a look at the methodology — it’s usually there in the fine print — which includes the number of people surveyed, the duration of the poll and whether interviews were done in more than one language.

Size matters.

“When you’re trying to contact people at random, you’re getting certain segments of the public, rather than the general population,” said Mark DiCamillo, director of the nonpartisan Berkeley IGS Poll and a collaborator with The Times. “So what needs to happen in order for a survey to be representative of the overall population … you need large samples.”

Which are expensive and the reason some polls skimp on the number of people they interview.

The most conscientious pollsters invest considerable time and effort figuring out how to model their voter samples — that is, how to best reflect the eventual composition of the electorate. Once they finish their interviews, they weight the result to see that it includes the proper share of men and women, young and old, and other criteria based on census data.

Then pollsters might adjust those results to match the percentage of each group they believe will turn out for a given election.

The more people a pollster interviews, the greater the likelihood of achieving a representative sample.

That’s why the duration of a survey is also something to consider. The longer a poll is conducted — or out in the field, as they say in the business — the greater the chances of reflecting the eventual turnout.

It’s also important in a polyglot state like California that a poll is not conducted solely in English. To do so risks under-weighting an important part of the electorate; a lack of English fluency shouldn’t be mistaken for a lack of political engagement.

“There’s no requirement that a person be able to speak English in order to vote,” said Keeter, of the Pew Research Center. “And in the case of some populations, particularly immigrant groups, that have been in the United States for a long time, they may be very well-established voters but still not be proficient in English to the level of being comfortable taking a survey.”

It’s also important to know how a poll question is phrased and, in the case of a ballot measure, how it describes the matter voters are being asked to decide. How closely does the survey track the ballot language? Are there any biases introduced into the poll? (“Would you support this measure knowing its proponents abuse small animals and promote gum disease?”)

Something else to watch for: Was the poll conducted by a political party, or for a candidate or group pushing a particular agenda? If so, be very skeptical. They have every reason to issue selective or one-sided findings.

Transparency is key. A good pollster will show his or her work, as they used to say in the classroom. If they won’t, there’s good reason to question their findings, and well you should.

A sensible person wouldn’t put something in their body without being 100% certain of its content. Treat your brain with the same care.

The last thing you may expect to come across in the depths of the rural Charenteis a scone, clotted cream and strawberry jam served with a hot pot of correctly brewed breakfast tea, but in Tusson, France, you’ll find just this.

Tusson is home to many artisanal workshops and independent artists(Image: Creative Commons)

In the heart of rural Charente, France, you might be surprised to find a scone, clotted cream and strawberry jam served with a properly brewed pot of breakfast tea.

But in Tusson, this is exactly what you’ll discover. You’ll also hear plenty of English accents.

Gateaux, with its bold lettering and pink exterior, is impossible to miss.

Step inside and you’re greeted by a verdant oasis and an impressive array of beautifully baked cakes, reports the Express.

As I have relatives nearby, I visit Tusson annually, and the lemon meringue cake has never disappointed me.

Other highlights include the chocolate Guinness cake and the cappuccino cupcakes.

There’s also a wonderful selection of teas and barista-made coffees, as well as ice creams and some savoury bakes.

Run by two biologists, Gateaux is adorned with the unexpected beauty of molecular structures, intricate scientific drawings and equations.

Despite having a population of just 240, this tiny village isn’t widely known.

The nearest city is Angouleme, renowned as the capital of comic books and the filming location for Wes Anderson’s ‘The French Dispatch’, featuring Timothee Chalamet.

Yet, Tusson is something of an artistic hub.

It boasts a pottery workshop, a few other artists’ residences and The Maison du Patrimoine.

This is where Francis I of France’s elder sister stayed upon learning of her brother’s death in the 16th century.

It was constructed from a fortified enclosure dating back to the 14th century.

The expansive fields surrounding Tusson are adorned with sunflowers during the summer, their faces tracking the often blistering summer sun.

Tusson’s primary eatery, Le Compostelle, is a bit of a splurge but could be worth your time. With lobster on the menu and their renowned soup de chocolat, a dessert that’s a spectacle in itself, one chuffed reviewer penned on Tripadvisor: “We all sat outside in a charming courtyard under cover in the heat of a full cover of awnings etc. Lovely atmosphere. We all opted for the 25- 30 euro set lunch. Absolutely fantastic value for money. The food was simply exquisite. Michelin standard. If you’re a chocolate lover, you must try the Soupe au Chocolat. Beyond wonderful.”

The area is a hit with ex-pats, many of whom reside in the nearby villages Ville Jesus, known for its brilliant annual village fair, and Aigre, a slightly larger town boasting a tourist office and a town hall.

Here, you can savour a pizza at La Square while taking in the frequent bric-a-bracs, France’s version of a car boot sale. Here, you’ll discover a variety of items from children selling their collages to boxes covered in dust filled with vintage postcards capturing snippets of holidays from half a century ago.

If you’re after a bit more excitement than browsing antiques, Nautilus is the place to be. However, gents, be warned – this water park enforces a strict speedo-only policy.

But don’t let that put you off, as there’s something for everyone here. Keen swimmers can clock up some serious lengths in the full-sized Olympic pool, while thrill-seekers can take on the diving board or brave the outdoor rapids slide that promises a wild ride.

Joanna said: “There are always going to be predators in an environment like this when you’ve got young, beautiful girls who are desperate to get a job.

“It is so hard to get that job.”

“Most of the time the people who are giving you those jobs are older men and they know that you want the job and there’s a million girls out there trying to get the job.”

She continued: “You don’t ever go, ‘Oh God, I’m going to report this’, because in those days you kind of didn’t, you just got on with it, it was what happened at work.

“It wasn’t every single job I went into, but in lots of different jobs there would be one type of thing.”

Mum-of-four Joanna, who is promoting her memoir Lush!, does not name the perpetrator as she says: “The legal people said, ‘Be careful’.”

A BBC spokesperson told The Sun earlier this year: “What started as a six month project turned into more than a year of joyous TV chatter, and over 80 heart-warming episodes.

Watch as Joanna Page reveals she was in floods of tears filming final scenes

“Though they both loved making the series, Natalie Cassidy and Joanna Page have very busy schedules and on the 21st May, the final episode of Off the Telly will be released on BBC Sounds.

“Thank you to Nat and Jo for their warm recommendations and insider analysis, and to the whole team for keeping listeners in the loop with what to watch.

“We look forward to working with Nat and Jo again soon!”

3

‘You’re a woman…and it’s so hard to get jobs anyway and you don’t want to make a fuss’, said the actressCredit: Rex

The company’s business model and strategy help secure an ongoing stream of income for investors.

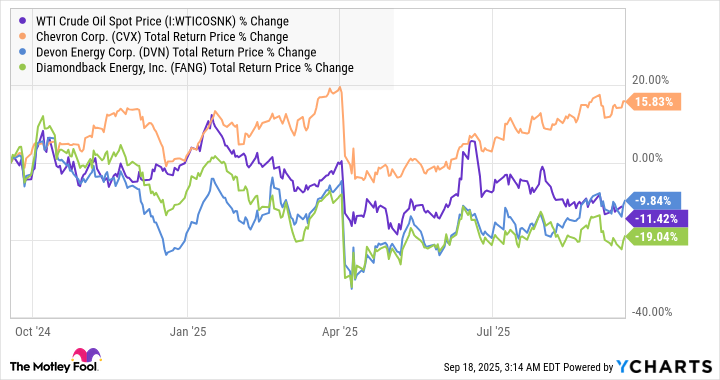

Investors in energy stocks, such as Chevron(CVX -1.71%), always need to keep a close eye on energy commodity prices. That’s one significant reason why the stock is intriguing right now, as the share price has outperformed during a period of downward drift in oil prices. That makes it particularly appealing for passive income investors looking to buy Chevron shares for a 4.3% dividend yield.

Chevron offers protection

The chart below compares Chevron to two higher-quality energy exploration and production companies, Devon Energy and Diamondback Energy. While the others have performed in line with the declining price of oil, Chevron has outperformed.

This is a valuable demonstration of what many income-seeking investors are looking for from energy stocks. While pure-play exploration and production stocks have demonstrated a correlation with the price of oil, the benefits of Chevron being a vertically integrated oil major are becoming increasingly apparent.

This means it combines upstream operations (exploration and production) with downstream operations (refining, marketing, and chemicals), and in doing so secures the cash-flow generation to support a growing dividend.

In addition, Chevron’s $53 billion acquisition of Hess Corporation has added significant international assets (in Guyana) that tend to have a lower break-even cost (the minimum price of oil a producer can cover costs in producing oil), and adds assets in the Bakken (North Dakota) to Chevron’s existing strength in the Permian (West Texas and New Mexico).

Image source: Getty Images.

What it means to investors

While Chevron will never be completely immune from falling oil prices, its downstream assets and efforts to diversify by acquiring lower break-even-cost international assets protect it from a moderated decline, which is good news for income-seeking investors. At the same time, it has upside potential coming from a possible increase in oil prices.

Lee Samaha has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Chevron. The Motley Fool has a disclosure policy.

There are lots of reasons to like PepsiCo(PEP 0.77%) as a possible investment for your long-term portfolio. One of the best reasons is its generous dividend yield — recently at 4.1%. That yield is far above the S&P 500‘s recent yield of just 1.2%, and better still, it’s a payout that’s been growing at a good clip — an annual average of more than 7% over the past decade.

But wait — there’s more! Its payout ratio — the percentage of earnings paid out in dividends — was recently quite reasonable, too, at 67%. That leaves plenty of room for further growth. (PepsiCo has upped its dividend for 53 years in a row!)

Image source: Getty Images.

Many people might imagine PepsiCo as mainly a beverage business, but they’d be wrong. It’s very much a snack business, too, with brands such as Lay’s, Doritos, Cheetos, and Quaker alongside Gatorade, Pepsi-Cola, Mountain Dew, and SodaStream. PepsiCo has a new pending acquisition, too, of the prebiotic soda brand Poppi.

PepsiCo’s stock looks appealing at recent levels, with a forward-looking price-to-earnings (P/E) ratio of 16.5, well below the five-year average of 21.9. The low valuation is due to the stock having slumped in recent years, as it tries to adapt to changing tastes. It’s doing so, including via the Poppi acquisition, and it’s cutting costs, too.

Chairman and CEO Ramon Laguarta recently noted:

As we look ahead, we will continue to build upon the successful expansion and growth of our International business and accelerate initiatives to improve our North America business performance. These initiatives include more portfolio innovation and cost optimization activities that aim to stimulate growth and profitability. As a result, for fiscal 2025, we remain confident in our ability to deliver low-single-digit organic revenue growth…

Selena Maranjian has no position in any of the stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.

Seeing one of your portfolio’s positions generate a 10-year return of 50,000% is truly mind-boggling. But this is exactly what Bitcoin(BTC -0.25%) has done (as of Sept. 17). A $2,000 starting investment in September 2015 would be worth $1 million today.

With such a fantastic historical return, it’s understandable if investors think that it’s too late to put money to work. But that’s a pessimistic view. Here’s the biggest reason you haven’t missed out on Bitcoin.

Image source: Getty Images.

Unsustainable financial situation

It’s safe to assume that the U.S. federal debt, now at $37 trillion, will keep increasing in the decades ahead. It doesn’t matter who’s in the White House. The country will continue to run massive fiscal deficits. For what it’s worth, the last surplus was in 2001.

This unfavorable trend supports ongoing growth in the money supply, as the government keeps borrowing to fund spending. Something must eventually break.

The counterargument is that because the U.S. has the biggest and most powerful economy, and the U.S. dollar is the global reserve currency, things can continue on this path. To be fair, unsustainable trends can last longer than people might think.

But the situation is becoming more fragile as time passes. Imagine if you kept opening new credit cards to pay off the balances of your old cards. This is financially reckless, but this is essentially what the U.S. government does.

Capital flowing to a scarce asset

Bitcoin has a fixed supply of 21 million units. No single entity has control over it. It transcends borders. And it’s permissionless. This makes it a unique asset for more capital to flow to, particularly as more money and debt keep being created in the financial system.

Therefore, as long as governments across the globe continue operating in fiscally irresponsible ways, Bitcoin will have uncapped upside.

Neil Patel has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Bitcoin. The Motley Fool has a disclosure policy.

The Solana blockchain is pulling away from the competition in one critical dimension.

Much like the companies that issue stocks, blockchains that issue cryptocurrencies can be analyzed by the amount of revenue they produce. Assets with more revenue and more revenue growth are likely to be better investments than those without.

By that standard, Solana(SOL 0.87%) is worth looking at closely as a potential investment. On Sept. 18 alone, its decentralized applications (dApps) generated roughly $6.9 million in revenue, more than the next 10 chains combined, and nearly three times the next largest competitor’s tally for the day. That certainly adds to the case for buying it, but when that fact is put in context, investors will also find some reasons to be a little bit cautious here.

Image source: Getty Images.

A reason to buy: A booming app economy

Before getting into the weeds, let’s start with a quick definition. In this context, “application revenue” is the sum of revenue earned by apps on a chain, which is distinct from base gas fees. By convention, the metric excludes stablecoin issuers, liquid staking, and gas itself. It’s a basic measurement of the level to which actual users are paying apps for their services.

So when Solana’s apps pulled in millions of dollars over a 24-hour period, outpacing not just its biggest competitor, Ethereum, but the rest of the field in aggregate, it was a big deal. What’s even more salient is that over the prior 30 days, Solana’s total application revenue of $211 million was more than twice Ethereum’s, so these results were not just a blip.

If you want one reason to buy Solana right now, this is it: There are customers consistently paying to use the applications on its chain, and far more of them than on any other network.

But why does this matter in the bigger scheme of things? The main reason is that app revenue tends to compound.

When app developers see users paying for services, they’re heavily incentivized to make and ship more of their products to that venue. Then the growth flywheel spins even faster as customers see that they can address multiple needs within the same ecosystem. Solana is thus where many developers perceive the growth to be.

Investors should also understand how this value generation accrues to Solana itself rather than just to application-related tokens.

In a nutshell, application revenue does primarily accrue to the applications and their treasuries or tokenholders, not directly to Solana holders. With that said, more usage generally boosts demand for blockspace and the network’s fee markets. And satisfying a customer’s demand for Solana app services requires them to buy and hold Solana to cover their fees. In other words, the ownership flywheel to Solana’s value is more indirect than on chains that burn a larger portion of fees, but strong app revenue still signals a healthy economy that can attract capital and talent, and more activity on the chain does induce more demand for the coin, and thus, drives its price higher.

A reason to be cautious: The headline numbers don’t tell the whole story

There’s an important catch here with Solana’s application revenue. A lot of the applications generating the largest proportion of the network’s revenue are not exactly focused on serious lines of business.

In fact, a large slice of Solana’s application revenue currently depends on applications that streamline the launching and trading of meme coins, which are cyclical, highly speculative, and often simply a stand-in for gambling. That makes sense given that meme coins accounted for roughly 70% of Solana’s decentralized exchange volume at one point, with over 60% of Solana app revenue being closely related to meme coin investing. If market conditions become a bit less frothy, that volume and those revenues are likely to dry up rapidly.

Does that make Solana uninvestable? Not at all. It just means that investors should be aware that its casino-like projects are the ones that are the most successful at the moment. Casinos can be profitable to own, but it’s still important to recognize that you’re (at least in part) buying a portion of one by buying Solana right now.

Assuming that the revenue mix gradually broadens — and it likely will — Solana can convert today’s traffic into longer-lived and more serious segments, and hang onto its mindshare among developers. If its mix stays overly dependent on meme coins, it might be a volatile ride, and the crypto’s upside might have a lower cap.

The investment thesis for buying this coin still rests on the real economic signal that users are paying to use apps at scale on this chain, and at a vastly higher rate than they’re doing that elsewhere. There are a lot of reasons to be bullish about Solana’s future, so the balance of risk and reward here does still tilt heavily toward buying it.

One way to have your cake and eat it too is to accept a long holding period and restrict yourself to a modest position sizing, at least until there’s clearer evidence of the ecosystem widening a bit. Until then, just remember that casinos wouldn’t be so large and opulent if they were bad at making money.

Ever wondered why there’s specific times during your air travel when you can’t use the toilet on-board? Now pilot Steve revealed the ‘dangerous’ reason behind it…

Christine Younan Deputy Editor Social Newsdesk

07:07, 20 Sep 2025Updated 08:06, 20 Sep 2025

There’s a reason you can’t pee when the plane is sometimes stationary(Image: Getty Images/iStockphoto)

It can be frustrating to sit strapped to your seat on the plane then all of a sudden, nature calls. There are secret areas passengers aren’t allowed anywhere near, but the toilet, surely not?

But if you’re a regular air traveller, you kind of know the deal by now. The cabin crew talk you through the safety, then you’re asked to fasten your seatbelt. This might all be familiar to many, but occasionally what happens is, we need to use the loo. Now one pilot revealed the ‘dangerous’ reason this is not always allowed in a post which went viral on TikTok.

American Airlines captain Steve, who boasts 401,000 followers on the platform, has been doing a Q&A series with his many fans.

Recently one person asked: “Why can’t I pee while the plane is stationary on the ground?”

The pilot explained the reason and it’s mainly because if one person does it, everyone follows…

Content cannot be displayed without consent

He said: “Well, LAX tie 23, because if you get up to go to the bathroom, then everybody else is going to get up and go to the bathroom.

“And we’re taxiing on an active runway or taxiway and one of the most dangerous times of flights is actually during taxiing, because if I have to hit the brakes and you’re standing up in the aisle, you’re going to fall.

“You’re going to hit your head on something. If you’re in the bathroom, good things are not going to happen in there.

“Have I had people get up and have to go use the bathroom? Yes, sometimes nature calls and you can’t hold it off anymore.”

He also explained how the pilot would usually have to stop until the traveller comes out of the bathroom and returns to their seat.

“It holds up the entire airport. It’s really a hassle when that happens,” he concluded.

Further on in the video, the pilot then began discussing safety briefings and making jokes with colleagues.

But since he shared the information on the toilet trouble, many people fled to the comments section as the post racked up nearly 2,900 likes.

One said: “Thank you for your wonderful, informative post!” Another added: “I’ll admit I’ve done that before… I was on a Southwest flight and we were holding before the runway and I had to pee…”

A third commented: “Take it from an FA. That’s so true.”

Nvidia(NVDA -0.18%) has made an incredible ascent to the top of the stock market, and it’s in a league of its own as the only stock with a market cap above $4 trillion. It’s up 1,300% over the past five years, and it doesn’t look like it’s anywhere near done.

Its growth prospects are up for debate amid increasing competition and its sheer size, which makes it harder to report high percentage growth. Still, there are many reasons to believe in Nvidia’s future. Here’s one reason investors still have time to buy Nvidia stock.

Image source: Getty Images.

Hyperscalers are spending

There are several ways to envision Nvidia’s opportunity, and one of them is to analyze how its largest clients are spending money on its products.

Nvidia works with the largest cloud operators in the world, the hyperscalers like Amazon, Microsoft, and Meta Platforms. These companies are building out their large language models (LLM) and offering top artificial intelligence (AI) solutions to their millions of customers, who in turn are using these platforms to create the next generation of generative AI apps.

This is the AI revolution that’s changing how people do business, shop, pay, and more, and these hyperscalers need Nvidia’s powerful chips to drive their AI models.

Just take a look at how much these three companies are spending this year on capital expenditures, and you can see how Nvidia’s business is going to be a crucial part of this process for the foreseeable future. Amazon is spending at a run rate of $120 billion, Microsoft at $100 billion, and Meta at about $65 billion. These are accelerations from last year, and as companies require more power, those numbers are likely to keep going up. Nvidia doesn’t collect every dollar of these sales, but it dominates this market.

I wouldn’t bet on Nvidia offering the same kind of growth it has in the past over the next five years, but it’s still likely to beat the market and offer value for shareholders.

Jennifer Saibil has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Amazon, Meta Platforms, Microsoft, and Nvidia. The Motley Fool recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

Gemma and Gorka have been dating since 2018Credit: Instagram

5

The duo met in 2017 as Strictly Come Dancing cast-matesCredit: Instagram

5

They’re now engaged and share two childrenCredit: instagram/glouiseatkinson

But funnily enough Gemma, 40, and Gorka, 35, weren’t actually coupled up during their time on the show.

Their relationship blossomed off-screen, with the duo beginning to officially date in 2018.

They got engaged three years later and now share a son and a daughter – Mia, five, and son Thiago, two.

After years of being engaged, Gemma has revealed why the couple have been waiting so long to walk down the aisle – and why they plan to wait even longer.

Read Strictly Come Dancing

In an interview Gemma said: “We’ve toyed about doing it in Spain so his [Gorka’s] family can come.

“We’ve even thought about doing it in a registry office or a hotel in Manchester, just the two of us, and then have a big party after.”

But what the lovebirds have settled on couldn’t be sweeter or more thoughtful.

“I think now we want to wait until Thiago is a bit older, so maybe next year or the year after, as he’s only two.

“If he’s a bit older, he could be involved in it, which would be really nice.”

Back in 2022 Gemma announced that herself and Gorka had to postpone their previously-planned wedding.

Strictly’s Gorka Marquez breaks down in tears as he pays tribute to Gemma Aktinson as he leaves her and their kids for weeks

The cancellation came about due to incredibly busy schedules on both ends, with Gorka busy as a professional dancer and Gemma as a radio host.

The pair were also wishing to prioritise trying for another baby instead of splashing out on a lavish event.

The wedding update comes only months after Gemma and Gorka found out that their reality TV show Gemma and Gorka: Life Behind The Lens had not been renewed for a third season on Apple TV.

It was devastating news for the couple, as the show had performed really well.

5

They’re waiting to tie the knot so their youngest child can participate in the dayCredit: Instagram

5

They weren’t dance partners during their Strictly daysCredit: PA

Chewy’s recent dip after earnings could be an opportunity for investors willing to look five years down the road.

Despite its stock price already doubling since 2024, leading online pet goods retailer Chewy (CHWY 0.05%) remains one of my favorite stocks to buy right now.

One particular reason stands out to me as to why Chewy stock is worth owning, and that is the potential for its profit margins to keep rising.

Since the company’s focused on an array of higher-margin growth areas, Chewy’s profitability could continue improving — and investors should be very excited about it.

Chewy’s burgeoning profit margins

Over the past two years, Chewy has become consistently profitable and cash-generative.

Chewy’s Autoship subscription plans account for 83% of total sales. This large base of Autoship sales means that most of Chewy’s revenue is predictable, steady, and ripe for further streamlining.

Image source: Getty Images.

Chewy Vet Care

The company plans to have 20 Chewy Vet Care clinics running by year’s end. These clinics give the company a physical presence and also offer the higher margins that veterinary shops typically achieve.

Get Real

Chewy recently launched its own private-label healthy and fresh dog food, Get Real. This premium-priced product offers higher margins (particularly as a private label good) and ties in perfectly with Chewy’s Autoship subscriptions.

Advertising

Chewy’s sponsored ads business remains a major driver of the company’s growing profitability. Management believes that these high-margin placements should one day grow to account for between 1% and 3% of total revenue.

Chewy+

The company’s new $49 annual membership program, Chewy+, received a positive reaction following its launch. Chewy+ provides members with free shipping, 5% rewards on purchases, and exclusive offers. Chewy+ members already accounted for 3% of the company’s June sales, and the program could generate substantial high-margin membership fees annually.

Trading at 29 times forward earnings — but with these earnings potentially set to rise — Chewy is a top stock to consider today.

Share prices of IBM have nearly doubled in just three years. Investors are excited by the company’s shift into hot technologies.

International Business Machines(IBM 1.15%), which is usually referred to by its ticker IBM, is a global icon in the technology sector. The company has a surprising ability to change with the times, and it’s been doing so for more than 100 years now. Indeed, when IBM was founded back in 1911, it made things like scales and clocks. Today, it makes all sorts of equipment, including quantum computers, and it supports the cloud computing industry, which is the backbone of artificial intelligence (AI).

Wall Street loves IBM again

Even after a fairly sizable drawdown since July, shares of IBM still trade up around 20% or so over the past year. Over the trailing three years, the stock has nearly doubled in price. That’s a pretty sizable return and highlights the fact that Wall Street is obsessed with IBM shares again. As noted, the company has shifted into key areas like quantum, cloud computing, and AI.

Image source: Getty Images.

But what’s special about IBM is that it hasn’t always been focused on these areas. Just a few years ago, investors pretty much hated the stock because it was out of step with the technology sector. The concern about IBM was so bad that between 2012 and 2020, the stock actually lost roughly half of its value. Contrarian investors with a long-term view, however, realized that IBM had updated its business many times before.

IBM is worth loving most of the time

The business revamp was difficult and took many years. It involved a large corporate spin-off, asset sales, and acquisitions, the largest of which was Red Hat. But IBM did what needed to be done to remain relevant. So while IBM is popular again because of its current business focus, the real reason to be obsessed with IBM for long-term investors is its proven ability to change with the world around it.

Reuben Gregg Brewer has positions in International Business Machines. The Motley Fool has positions in and recommends International Business Machines. The Motley Fool has a disclosure policy.

As the consumer investment world grows, the bank has a lot to gain.

Bank of America(BAC 0.71%) is one of the largest banks in the world, operating in the U.S. and more than 35 countries worldwide. By market cap, it’s the second-most valuable bank in the world, trailing only JPMorgan Chase. In the past five years, Bank of America has outperformed the S&P 500, with total returns close to 125% in that span, compared to the index’s 112% (through Sept. 12).

Even with Bank of America’s market-beating returns over the past five years, the next five years could continue the same momentum. The reason comes down to one factor: its consumer investment business.

Image source: Getty Images.

The consumer investment business involves standard brokerage accounts, wealth management, and financial advisory services. In the fourth quarter of 2024, Bank of America’s consumer investment assets crossed the $500 billion mark for the first time in the company’s history.

The company noted that this amount has doubled every five years, and it expects to hit $1 trillion in the next five years. In the second quarter of this year, it reached around $540 billion (up 13% year over year).

Hitting this mark won’t guarantee that Bank of America’s stock will soar (nothing guarantees that), but the growth of its consumer investment business means it will earn much more fee-based income and see higher margins than from other revenue sources like traditional lending. This should be a nice boost to Bank of America’s profitability, especially as we anticipate interest rates getting lowered over the next few years, which could impact the bank’s main revenue source.

Bank of America is an advertising partner of Motley Fool Money. JPMorgan Chase is an advertising partner of Motley Fool Money. Stefon Walters has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends JPMorgan Chase. The Motley Fool has a disclosure policy.

At the beginning of September, Ryanair confirmed the closure of the Santiago base and the cancellation of all flights to Vigo and Tenerife North. Simultaneously, it was announced that the airline will maintain the closure of its Valladolid and Jerez bases and decrease capacity in Asturias, Santander, Zaragoza, and the Canary Islands this winter

Ryanair is scaling back its Spanish offering(Image: Dmitri Zelenevski via Getty Images)

Ryanair has been accused of ‘lying’ about the reason why it cut flights to Spain.

In late August, the budget airline revealed plans to drastically reduce its capacity on routes to and from Spain, eliminating a million seats in the forthcoming winter season. The company has stated that these extensive cuts are a reaction to Spain’s airport operator Aena’s announcement of a 6.5% increase in passenger fees by 2026.

Now Spain’s airport operator has accused Ryanair chief executive Michael O’Leary of using it as a scapegoat to avoid incurring passengers’ wrath for cancelling the routes and cutting back flights.

Ryanair has hit back against the allegations, arguing that it chooses locations based on where is cheaper. It also urged Aena to call their bluff by lowering airport fees. A Ryanair spokesperson said: “If we are lying as Lucena claims, then why doesn’t he call our bluff and cut Aena’s high fees at Spain’s empty regional airports? Ryanair always goes where costs are lower and will happily go back to regional Spain when they stop charging Madrid/Barcelona prices. Until then it’s adiós Aena!”

Ryanair announced its route to Tenerife North would be cut(Image: Anadolu via Getty Images)

In an interview with the Financial Times, Maurici Lucena, chair and chief executive of Aena, accused the budget airline boss of “lying continuously”.

“What really bothers me is that they’re not telling the truth. It has nothing to do with Aena’s fees. The reason they lie is that they don’t want to face the political and reputational cost of abandoning some regional airports, and in some cases even causing job losses when they shut down a base. That’s the real underlying issue,” Mr Lucena told the publication.

The airport boss argued that Aena’s proposed 6.5% fee increase averages out at €0.68 per passenger. He assured members of the public that Aena would not be closing any of its smaller regional airports, particularly as it is required by law to keep them operating.

At the beginning of September, Ryanair confirmed the closure of the Santiago base and the cancellation of all flights to Vigo and Tenerife North. Simultaneously, it was announced that the airline will maintain the closure of its Valladolid and Jerez bases and decrease capacity in Asturias, Santander, Zaragoza, and the Canary Islands this winter.

The cuts are part of Ryanair’s plan to reduce its capacity by 41% in the Spanish regions and by 10% in the Canary Islands this winter. Eddie Wilson, CEO of Ryanair, warned that this would lead to “a loss of investment, connectivity, tourism, and employment in regional Spain, as many routes will be economically unviable.”

All flights to Vigo will stop in January next year, and to Tenerife North from the start of the Winter 2025 season. Capacity to Zaragoza will be slashed by 45%, Santander by 38%, Asturias 16% and Vitoria by 2%. When culling is over, Ryanair will have scrapped 36 routes to and from Spain.

At the same time, Ryanair is planning to introduce two million more seats on routes to Italy, Morocco, Croatia and Albania.

This is not the first time that Mr O’Leary has aimed barbed words at those working in the aviation sector. The airline has cancelled flights in France following a dispute over fees, while Mr O’Leary has repeatedly called for the UK’s air traffic control chief to be sacked.

The company’s expanding business is bringing optimism to investors.

If you’ve been paying attention to the tech world for the past couple of years, you’ve likely noticed how unavoidable artificial intelligence (AI) is. Even if you haven’t been tuned into tech news, chances are good that you’ve come across AI in some form or fashion.

This AI hype has made many tech stocks go-tos for investors looking to capitalize on the new technology, but there have been very few stocks that Wall Street has obsessed over quite like Palantir Technologies(PLTR 4.14%). The stock is up over 120% year to date through Sept. 10, and up over 378% in the past 12 months.

Image source: Getty Images.

Why the obsession with Palantir?

The reason why Wall Street has become obsessed with Palantir is that the company has demonstrated that it’s not a one-trick pony.

For a while, Palantir was viewed as a niche data software company that served government agencies like the U.S. Department of Defense and CIA. However, the growth of its U.S. commercial business — thanks to its Artificial Intelligence Platform (AIP) — has shown that the company can scale in the private sector and compete in the mainstream enterprise AI space.

In the second quarter, Palantir’s U.S. commercial business increased its revenue 93% year over year to $306 million. Although it didn’t earn more than Palantir’s U.S. government revenue ($426 million), it was easily its fastest-growing segment.

Should you also be obsessed with Palantir?

Palantir showing additional revenue streams is encouraging, but if you’re not currently an investor, you should proceed with caution before going all in on the stock because of its extremely high valuation. Palantir is currently trading at close to 267 times its forward earnings, which is one of the highest in history on the stock market, regardless of the company.

This doesn’t make Palantir a bad investment, but such a high valuation means that investors have priced a lot of growth into the stock, and anything short of meeting these lofty expectations could result in a sharp pullback.

Stefon Walters has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Palantir Technologies. The Motley Fool has a disclosure policy.

This stock has been a phenomenal performer, and its future looks bright.

If you don’t know much about Intuitive Surgical(ISRG 1.71%), you might want to remedy that. It’s a very impressive growth stock. Its past performance is likely to wow you, and its future looks very promising.

Over the past decade, Intuitive Surgical stock has grown in value at an average annual rate of 23%. Over the past three years, that growth rate ramped up to nearly 30%! If you had invested $10,000 in Intuitive a decade ago, your stake would be worth roughly $80,610 today. The S&P 500 index, in contrast, averaged 13.6% in that period, turning $10,000 into $33,720 — a still-quite-solid performance.

Image source: Gertty Images.

Intuitive Surgical is a leader in robotic surgery equipment. It has more than 9,900 of its million-dollar-plus da Vinci robotic surgery systems installed in 72 countries. Together, the systems have been used to perform more than 16 million procedures.

Its business model is delightful, too, as it derives 84% of its revenue not from the costly systems themselves but from rather dependable recurring sales of servicing, supplies, and accessories for the machines. Once a hospital has committed to a da Vinci machine, it can’t go elsewhere for servicing and supplies.

And as our world’s population ages, there’s likely to be more demand for the kinds of procedures that Intuitive Surgical’s machines facilitate, such as colorectal surgery, cardiac surgery, hernia surgery, and more. Intuitive’s Ion systems also facilitate lung procedures.

According to some metrics, Intuitive’s stock is not a bargain right now; for example, its forward-looking price-to-earnings (P/E) ratio was recently 51, which is on the steep side. But that’s still well below the stock’s five-year average of 56. That’s because the stock has pulled back recently, presenting a tempting buying opportunity for interested long-term investors.