Explore the exciting world of Garmin(NYSE: GRMN) with our contributing expert analysts in this Motley Fool Scoreboard episode. Check out the video below to gain valuable insights into market trends and potential investment opportunities! *Stock prices used were the prices of Jul. 30, 2025. The video was published on Aug. 27, 2025.

Should you invest $1,000 in Garmin right now?

Before you buy stock in Garmin, consider this:

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now. Learn More »

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Garmin wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004… if you invested $1,000 at the time of our recommendation, you’d have $661,220!* Or when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $1,114,162!*

Now, it’s worth noting Stock Advisor’s total average return is 1,069% — a market-crushing outperformance compared to 185% for the S&P 500. Don’t miss out on the latest top 10 list, available when you join Stock Advisor.

Anand Chokkavelu, CFA has positions in Garmin. Rick Munarriz has no position in any of the stocks mentioned. Travis Hoium has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Garmin. The Motley Fool has a disclosure policy.

Agilent Technologies(A 0.33%), a global leader in laboratory instruments and scientific solutions for life sciences and diagnostics, released its Q3 fiscal 2025 results on Aug. 27, 2025. The company delivered revenue of $1.74 billion, coming in over its own projected revenue guidance and achieving a 10.1% increase over the prior year period. Non-GAAP earnings per share were $1.37, which was at the high end of management’s forecast and matched analyst expectations. Profitability also improved compared to last year.

However, operating margins narrowed in all business units due to increased costs, including tariffs and higher operating expenses. Overall, the quarter demonstrated broad-based growth across the company, with management responding by raising both annual revenue and profit forecasts for fiscal 2025.

Metric

Q3 2025

Q3 2024

Y/Y Change

EPS (Non-GAAP)

$1.37

$1.32

3.8%

Revenue

$1.74 billion

$1.58 billion

10.1%

Net Income

$336 million

$282 million

19.1%

Operating Margin – Agilent CrossLab Segment

33.3%

35.9%

(2.6 pp)

Revenue – Life Sciences and Diagnostics Segment

$670 million

$585 million

14.5%

What does Agilent Technologies do?

Agilent Technologies provides analytical instruments, software, and consumables for laboratories worldwide. Its customers work primarily in life sciences, pharmaceutical research, diagnostics, food testing, and chemical analysis. The company’s products help scientists analyze everything from new medicines to food safety and environmental samples. Its technology range includes mass spectrometry systems, which identify molecular structures; liquid chromatography platforms, which separate chemical mixtures; and automated pathology diagnostics used in hospitals.

It operates through three main segments: Life Sciences and Applied Markets, Diagnostics and Genomics, and Agilent CrossLab. It has strengthened its position through sustained investment in new technologies, a broad portfolio of instruments and software, and a global footprint. Key drivers of success include technological leadership, regulatory compliance, access to emerging markets, and the flexibility to reorganize segments in line with growth opportunities.

Quarter in review: Growth, margins, and market trends

During the quarter, Agilent achieved notable top-line gains, with revenue growing 10.1% year over year, well above its own guidance. All three major business units and every geographic region posted year-over-year increases in sales, underscoring both resilient demand and the effectiveness of its execution initiatives.

The Life Sciences and Diagnostics segment, which includes laboratory instruments and automated diagnostic tools, posted the fastest growth at 14%. This reflects demand for technologies used in scientific research, biopharmaceuticals, and hospital labs. The Applied Markets unit, which provides testing systems for food, environmental, and chemical analysis, and Agilent CrossLab, which offers services and consumables that support overall laboratory workflow, also saw revenue increases.

The broad-based growth was coupled with a sequential and year-over-year decline in operating margins across segments. In the Life Sciences and Diagnostics group, higher sales were accompanied by a decrease in both gross and operating margins, with gross margin down to 50.5% from 54.4% a year ago.

The CrossLab segment’s operating margin slipped to 33.3%, down from 35.9% a year earlier, while Applied Markets diminished as well. Tariffs and higher costs, including an increase in the cost of goods sold and operational expenses, were cited as factors affecting profitability. Even though overall operating income improved in dollar terms, the reduced operating margin as a percentage of revenue points to elevated cost pressures that management is committed to addressing.

The company reported both strong cash and a solid balance sheet, with operating cash flow for the first nine months of fiscal 2025 totaling $1,014 million, down 20% compared to the same period a year earlier. The company noted that the cash flow decrease was mainly due to inventory building as a strategy to manage ongoing supply chain and tariff risks, as well as higher capital spending. Cash and cash equivalents rose to $1.54 billion as of the end of the quarter. Research and development spending decreased 12.6% compared to the same period last year.

The company continued its regular share repurchase and dividend programs.

What’s new and what stands out this quarter?

The most significant theme was continued strong demand from biopharma firms and hospitals in both developed and emerging markets. The Life Sciences and Diagnostics segment in particular, linked to testing tools and systems for analyzing biological samples and automating clinical workflows, delivered both the fastest growth rate and the largest sales increase. Applied Markets, supplying instruments for food safety, environmental, and forensics labs, and CrossLab, focused on laboratory consumables and support, both contributed to broad revenue gains.

While the quarter was marked by revenue growth, each segment also experienced some profit margin compression. This was attributed to ongoing tariff exposure and increases in operating expenses, including supply chain investment. To hedge against these risks, Agilent continued its Ignite Transformation initiative, aimed at driving operational efficiencies, expanding its innovation pipeline, and mitigating cost increases. While Ignite has helped offset some headwinds, cost inflation and tariffs have outpaced some efficiency benefits, as reflected in lower segment gross and operating margins. Management indicated it would continue focusing on price realization, localized manufacturing, and supply chain adjustments in future quarters.

Management reaffirmed continued investment in new technologies, including advanced mass spectrometry products, which are devices for analyzing molecules. Prior quarters emphasized portfolio expansion in life sciences instrumentation and informatics, and the company reiterated its commitment to innovation. All global regions contributed to growth.

There were no new sustainability or environmental disclosures in the quarter. The company’s public goal to achieve net-zero greenhouse gas emissions by 2050 remains in place, though no new progress updates were provided. Agilent reported no regulatory compliance issues or fines; compliance remains a critical factor because its diagnostic and analytical tools must meet health and safety regulations in all relevant markets.

Looking ahead: Guidance and key areas for investors

Management raised its full-year guidance for fiscal 2025, now expecting revenue of $6.91–$6.93 billion and non-GAAP earnings per share of $5.56–$5.59, both meaningfully higher than previous projections. For the fourth quarter of fiscal 2025, Agilent projects revenue between $1.822 billion and $1.842 billion, with non-GAAP earnings between $1.57 and $1.60 per share. This stronger guidance points to continued broad demand across end markets and signals confidence in ongoing portfolio and geographic expansion.

Investors should keep an eye on margin trends, as inflation, tariffs, and supply chain dynamics continue to present risks to profitability. The company is prioritizing operational resilience through supply chain strategy, efficiency programs like Ignite, and targeted price increases. Emerging markets, new product launches, and ongoing regulatory compliance will remain important watchpoints.

Agilent Technologies pays a regular dividend and continued its dividend program during the quarter.

Revenue and net income presented using U.S. generally accepted accounting principles (GAAP) unless otherwise noted.

Phibro Animal Health(PAHC -1.56%), a veterinary pharmaceutical and nutrition provider, reported earnings for Q4 FY2025 on August 27, 2025, covering the three months ending June 30. Driven by its largest-ever acquisition and strong international appetite for its medicated feed additives, the company’s sales, adjusted earnings, and profit margins all surpassed expectations. GAAP revenue reached $378.7 million, up 39% from the previous year. Adjusted diluted earnings per share (EPS) climbed to $0.57 from $0.41, also beating consensus expectations. Management described the result as a step-change, reflecting both solid underlying product demand and successful integration of new product lines, though a decline in gross margin showed that rising input and distribution costs remain a concern.

Metric

Q4 2025

Q4 2024

Y/Y Change

Adjusted Diluted EPS (Non-GAAP)

$0.57

$0.41

39 %

Revenue

$378.7 million

$273.2 million

38.6 %

Adjusted EBITDA (Non-GAAP)

$50.0 million

N/A

N/A

Adjusted Net Income (Non-GAAP)

$23.2 million

$16.7 million

39 %

Gross Margin

29.0 %

31.9 %

(2.9 pp)

Phibro Animal Health’s Business and Strategies

Phibro Animal Health manufactures and sells products that support animal health and nutrition across more than 90 countries. Its main product lines include medicated feed additives, which help prevent disease in livestock; nutritional specialty products that enhance animal health; and vaccines to combat specific animal diseases. The company’s clients include food producers, veterinarians, and animal health distributors.

Recently, Phibro has focused on expanding its reach and product portfolio through acquisitions and global growth. The October 2024 purchase of Zoetis’s medicated feed additive portfolio added 37 products and six new manufacturing sites to its business. Success in this market relies on regulatory compliance, strong product innovation, and a global presence, with about 55% of animal health sales coming from outside the United States.

Quarter Highlights: Growth, Product Mix, and Margin Trends

The quarter marked a pivotal moment for Phibro, with GAAP revenue climbing 39% compared to the prior year. The acquisition of Zoetis’s medicated feed additive (MFA) products played a central role, contributing $94.5 million in additional sales. Animal Health segment sales increased by 53%, primarily due to the Zoetis MFA acquisition. Vaccine revenues grew 21%, fueled by high demand in Latin America, while nutritional specialties posted solid gains of 11%.

Adjusted EBITDA, a measure of profit excluding both non-cash and one-off items, rose faster than revenue, up 49%, reflecting successful integration of acquired assets and improvements in operating leverage. Adjusted net income followed suit, reaching $23.2 million. Phibro’s ability to quickly benefit from the recent acquisition shows its execution on large, cross-border deals and boosts its long-term earnings potential.

Not all trends were positive, however. Gross margin, a measure of how much profit remains after covering production costs, slipped from 31.9% to 29.0% (GAAP). Management cited several causes, such as higher distribution costs, inventory write-offs, and a less favorable product mix. Despite these cost pressures, adjusted gross margin for the full fiscal year rose slightly, showing that the cost impact was most pronounced in the fourth quarter.

Looking at the company’s broader portfolio, Mineral Nutrition sales (GAAP) inched up 3%, while Performance Products rose 13%. Mineral Nutrition and Performance Products Adjusted EBITDA increased $4.4 million and $2.9 million, respectively, with Mineral Nutrition’s adjusted EBITDA up 4% and Performance Products by 38%. Free cash flow was $41.8 million, just below the previous period. Phibro maintained its quarterly dividend at $0.12 per share, continuing a stable return to shareholders.

Business Segments and Drivers: Product Lines Explained

The company’s core Animal Health segment is built on three main product lines: medicated feed additives (medicines delivered in animal feed), nutritional specialties (products that enhance animal health and growth), and vaccines (biological products to prevent livestock disease). The recent strength in this segment has been driven mostly by medicated feed additives, especially the new Zoetis-acquired products, which led to a 77% year-over-year jump in sales for this line. Vaccines saw demand rise due to success in international poultry markets.

Mineral Nutrition products supply trace minerals like copper and zinc, important for healthy livestock. Growth here was modest but steady, driven by broader demand for feed minerals. Performance Products comprise specialty chemicals used in industrial applications, rounding out Phibro’s diversified offerings. Each of these areas supports the company’s efforts to reduce dependence on any single customer group or geographic market.

Financial Outlook and What to Watch

For FY2026, management expects continued double-digit growth. Guidance points to net sales between $1.43 billion and $1.48 billion, representing about 12% projected growth. Adjusted EBITDA is anticipated to rise 25%. This outlook reflects management’s confidence in continued growth across all segments.

Investors should watch margin trends closely. The drop in quarterly GAAP gross margin, if it continues, could signal sustained cost or mix pressures. Free cash flow and leverage levels are also important to monitor, as integration and expansion require capital, and gross leverage ended the year at 3.1x. Management made no notable changes to its dividend policy, with a quarterly payout of $0.12 per share continuing as before.

Revenue and net income presented using U.S. generally accepted accounting principles (GAAP) unless otherwise noted.

Motley Fool Markets Team is a Foolish AI, based on a variety of Large Language Models (LLMs) and proprietary Motley Fool systems. The Motley Fool takes ultimate responsibility for the content of these articles. Motley Fool Markets Team cannot own stocks and so it has no positions in any stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.

One Wall Street analyst isn’t buying management’s turnaround plan.

Shares of donut maker Krispy Kreme(DNUT -3.48%) fell on Wednesday, down as much as 10.2%, before reverting to a 3.6% decline on the day.

Krispy Kreme has had a tough 2025, which has seen the stock plunge 64% on the year. Tepid sales, falling profits, and the cancellation of a high-profile partnership with McDonald’s have all been headwinds for the company.

Today, a Wall Street analyst piled on, lowering his rating on the stock from neutral to underweight, following the company’s recent unveiling of its turnaround plan.

J.P. Morgan says to sell the turnaround enthusiasm

For reference, Krispy Kreme unveiled its turnaround efforts on Aug. 7, during its second-quarter earnings. The plan has several components, including cutting costs associated with the now-defunct McDonald’s partnership, as well as others. The most notable proposed change has to do with refranchising Krispy Kreme’s international store footprint. Krispy Kreme also seeks to outsource its logistics to a third party.

While each franchise agreement is different, franchising one’s stores means typically means offloading the operations and bulk of profits (or losses) to third parties, while the brand makes revenue on sales of ingredients along with a franchise fee, which is usually a single-digit percent of sales.

But J.P. Morgan analyst Rahul Krotthapalli sees a risk to the plan, as it will take time to execute, while current sales trends remain negative. Last quarter, the company’s organic growth rate declined 0.8%. And while franchising lowers operational risk, it also lowers revenue and profits. Krotthapalli sees that as another risk, given Krispy Kreme’s existing $957 million in debt.

Image source: Getty Images.

Krispy Kreme is a risky turnaround play

Krotthapalli may be a bit harsh in his assessment of the plan, given that it focuses on cost cuts and return on invested capital, which should at least lead to profitability improvements. Nevertheless, Krispy Kreme remains growth-challenged at the moment, so all the focus on streamlining costs won’t amount to much until revenues stabilize and get going back in a positive direction. It’s pretty hard to predict such a turnaround, so investors should probably steer clear of this high-risk story for now.

Billy Dubersteinand/or his clients has no position in any of the stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.

J.M. Smucker missed expectations as tariffs took a bite out of profit margins.

Shares of packaged food giant The J.M. SmuckerCompany(SJM -3.89%) fell on Wednesday, declining as much as 9.3% before recovering to a 5.1% decline as of 1:05 PM EDT.

J.M. Smucker, home to a variety of food brands such as Smucker’s, Folgers, and Hostess, gave its fiscal-third-quarter earnings report this morning. The numbers missed expectations, with tariffs especially taking a bite out of the bottom line.

A tariff-related miss leaves a bitter taste

In the fiscal third quarter, J.M. Smucker’s revenue declined 1% to $2.1 billion, although absent the effect of divestitures over the past year, revenue would have actually increased 2%. On a more pessimistic note, adjusted (non-GAAP) earnings per share of $1.90 fell a more severe 22% from the prior year. Both top and bottom lines missed expectations.

But while the quarter came in a bit soft, management actually increased full fiscal year guidance, now expecting full-year revenue to grow between 3% to 5%, compared with 2% to 4% previously. While the earnings-per-share range with $9.00 per share at the midpoint was left unchanged, management also raised guidance for free cash flow by $100 million to $975 million.

The free cash flow uplift was nice to see, but was actually the result of tax benefits in the recently passed “big, beautiful bill.” Meanwhile, revenue gains are coming from price hikes, especially on coffee, in response to increased commodity prices, which have been affected by recent tariffs.

Image source: Getty Images.

Tariffs are clearly biting Smucker’s profits

While Smucker appears to be raising prices with some success, it doesn’t appear the increases are totally compensating for higher commodities and tariff impacts, as evidenced by the decline in earnings. This is especially true in the coffee segment, which makes up about a third of revenue and is the company’s largest. Unfortunately, that’s where tariffs on green coffee are hurting the most. And the tariff effect will get bigger because President Trump decided to institute a 50% tariff on Brazil at the end of July.

Still, shares trade for a low valuation, at just 11.5 times this year’s free-cash-flow guidance with a healthy 4% dividend yield. Assuming tariffs are a one-time cost, and that’s not a demanding valuation for investors.

Billy Duberstein and/or his clients have no position in any of the stocks mentioned. The Motley Fool has positions in and recommends J.M. Smucker. The Motley Fool has a disclosure policy.

Two media companies, two business models, one clear winner. Let’s follow the money instead of the politics.

The media sector offers some distinctly different investment options. Newsmax(NMAX -1.47%) entered the stock market as recently as March 2025, and the largely digital provider of conservative news coverage has only one quarterly earnings report under its belt. By contrast, The New York Times Company(NYT 0.77%) was founded in 1851 and entered the public stock market 56 years ago.

You can look at this matchup as a political struggle, but I’m more interested in their business models. Which media stock operates from the stronger financial foundation, setting shareholders up for better long-term returns?

Newsmax and The New York Times, by the numbers

Both companies recently published their results for the period ending on June 30, 2025. Let’s see how they stack up.

Newsmax posted strong top-line growth. Its second-quarter sales rose 18.4% year over year, landing at $46.4 million. The company reached 26 million cable news viewers in this quarter.

With $198 million of cash equivalents and no long-term debt to speak of, Newsmax’s balance sheet looks robust at first glance. However, its bottom-line profits are consistently negative, and the cash balance was built on $426.6 million of additional paid-in capital — financial backing provided by founder Christopher Ruddy and the stock offering in March.

Investors should watch how this shareholder-backed company manages its return on equity in the long run. It’s a negative number for now, even if you back out a $68.4 million legal expense from Newsmax’s expenses.

New York Times saw a slower 9.7% revenue increase in the same reporting period, as expected from a more mature company. Revenue landed at $685.9 million, with 51% coming from digital-only subscription sales. Net income rose 26.6% to $82.9 million, while free cash flow fell 30% year over year to $72.6 million.

New York Times’ cash balance stood at $951.5 million by the end of June. Like Newsmax, this company doesn’t carry any long-term debt. Once again, return on equity is an important financial metric to watch, with the current value perched at 17.1%.

Long story short, The New York Times is an older and larger business with slower growth but robust profits. The return-on-equity figures weigh heavily in the larger company’s favor at this point, due to Newsmax’s unprofitable operations.

Image source: Getty Images.

The stock performance scorecard

That brings me over from financial statements to the stocks themselves.

Newsmax shares are trading 94% below their all-time high, which was set amid the frenzied market action on the IPO date. Skipping ahead to calmer times, the three-month return as of August 26 is a negative 29.7%.

Profit-based valuation metrics don’t make sense for this stock yet, and Newsmax hasn’t reported a full year of revenue figures, so it’s hard to pin a reasonable market value on the stock. For what it’s worth, Newsmax trades at 18.5x the company’s book value and 10x its net cash balance.

New York Times investors pocketed a 7.8% total return in the last three months and a market-beating 92.5% in three years. Neither a market darling nor a bargain, the stock trades at a modest 30.7x trailing earnings and 21.3x free cash flow.

It’s a mixed bag if you compare the two stocks on the metrics that actually apply to Newsmax. The New York Times stock trades at 5x book value and 18x its cash reserves.

Boring beats volatile in this media matchup

Newsmax is still finding its bearings on the public market. The stock has been volatile in the first few months, and the company’s main revenue source is the unpredictable flow of advertising sales.

The New York Times has been around forever and runs a more robust business model with more subscription revenue than ad sales. The stock isn’t exactly cheap, but its valuation isn’t terribly lofty, either.

For better or worse, many people might pick either one of these stocks to match their political leanings. That’s fine, as long as you keep the investment on the small side.

Emotional investing is rarely a recipe for strong returns. If you turn down the adrenaline spigot, The New York Times looks like a modestly priced value stock, while Newsmax seems too hot to handle in 2025.

Anders Bylund has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends The New York Times Co. The Motley Fool has a disclosure policy.

The cloud-native database specialist showed its artificial intelligence (AI) strategy is paying dividends.

Shares of MongoDB(MDB 34.70%) charged sharply higher on Wednesday, surging as much as 34.3%. As of 11:47 a.m. ET, the stock is still up 34%.

The catalyst that drove the database-as-a-service provider higher was the company’s financial results, which were far better than even the most bullish forecast.

Image source: Getty Images.

Blowing past expectations

For its fiscal 2026 second quarter (ended Jul. 31), MongoDB delivered revenue of $591.4 million, up 24% year over year, signaling that its strategy to address the booming demand for artificial intelligence (AI) is paying off. As a result, the company delivered adjusted earnings per share (EPS) of $1.00, compared to a loss per share of $0.70 in the prior-year quarter.

The results blew past management’s previous guidance and caught Wall Street off guard. Analysts’ consensus estimates were calling for revenue of $554 million and adjusted EPS of $0.67, so MongoDB sailed past even the loftiest expectations.

Further fueling investor enthusiasm was the company’s robust customer acquisitions. MongoDB added 2,800 net new customers, with the total growing to 58,300, up 18% year over year.

The company also continues to generate plenty of cash, with operating cash flow of $72.1 million and free cash flow of $69.9 million.

The AI wildcard

Over the past couple of years, MongoDB has been focused on providing its users with the tools they need to use AI. CEO Dev Ittycheria noted that while AI is not yet a “material driver” of the company’s growth, he noted that “enterprise uptake of AI is still early.” He went on to say that the “real enduring value” will come from custom AI solutions that will transform their businesses, and that MongoDB provides the tools that will help developers prosper.

Management gave investors other reasons to celebrate, as the company raised its full-year forecast for the second consecutive quarter. MongoDB is now guiding for fiscal 2026 revenue of $2.35 billion, or roughly 17% growth. The company also significantly increased its profit outlook to $3.68, up from $3.03 at the midpoint of its guidance. This shows the company is focusing on expanding its profit margins.

MongoDB stock isn’t cheap, selling for 11 times sales. However, that’s roughly half its average multiple of 20 since the company’s IPO in late 2017.

The Mediterranean dining chain has been cut in half since peaking nine months ago. It could be a bargain here.

Cava Group(CAVA 1.28%) and its customers know all about dips. The chain’s tzatziki, spicy hummus, Greek green goddess, and signature “crazy feta” are so popular that even some local grocers stock them in eight-ounce containers. Investors are also learning all about Cava dips.

Shares of the fast-growing operator of fast-casual restaurants specializing in Mediterranean cuisine have fallen sharply in recent months. Cava stock is down 62% since peaking in November. A feel-good rebuttal is that the stock has roughly tripled since going public at $22 two years ago, but that doesn’t help the investor who warmed up to the the Cava story late last year.

How did the stock get here? Will it continue to head lower? There’s a lot to cover here, but like its crazy feta, I also want to argue that it’s a tasty dip worth buying.

Mediterranean goes subterranean

Cava is a leader in fast casual, a potent subset of eateries bridging the gap between fast food and casual dining. It’s also riding high on consumers embracing the health benefits of savory Mediterranean diets. When Cava hit the market in the springtime of 2023, its prospectus spelled out the unique characteristics of its customer base as primarily well-off and young. Household income was north of $150,000 for 37% of its patrons (and above $100,000 for 59% of its base). Cava also noted that 28% of its visitors are between 25 and 34 years old. Female-identifying guests accounted for 55% of its visitors.

Backed by heady expansion and stellar comps, Cava became a new industry darling for investors. As the pandemic-era recovery found more companies calling employees back to in-office work, Cava would become even more popular as a hotspot for workday lunches or picking up food on the way home from work. The affluent nature of its fans made it less likely to fall into a funk if the economy should falter.

The stock’s initial ascent was fueled by its improving fundamentals. It turned profitable in its first quarter as a public company, and continues to pad its bottom-line results. Revenue growth would accelerate in 2023 as well as 2024. The chain has been feeling a bit more mortal lately. Year-over-year revenue growth has decelerated for three straight quarters. Same-restaurant sales are also slowing. Let’s size up where Cava stands now, and if its deflated share price during the slowdown makes it a compelling buy here.

Image source: Cava Group.

Stepping on the scale

There are two sides to Cava’s latest quarter. Compared to most restaurants that slumped with sluggish sales, negative comps, and bottom-line hits through the second quarter of this year, Cava’s report two weeks ago was a breath of fresh feta. Revenue rose 20% to $278.2 million, up an even tastier 63% compared to where it was two springtimes earlier. It ended the quarter with 398 locations, a nearly 17% increase over the past year. Comps were up 2.1%. This is well below its previous store-level leaps, but a rare positive showing in a quarter of industry negativity. Chipotle Mexican Grill — the gold standard in fast casual — saw its second-quarter revenue inch just 3% higher with a 4% decline in comps.

Slowing growth isn’t a good look, but it does move the bar higher. Average sales volume for a Cava store over the past 52 weeks is now $2.9 million, up from $2.7 million a week earlier. Cava’s reported net income of $18.4 million was lower than it was a year earlier, but it was 10% higher on an adjusted basis. The chain’s adjusted net income margin contracted during the quarter, but its adjusted earnings before interest, taxes, depreciation, and amortization (EBITDA) moved higher. It wasn’t a great report, but most eateries would’ve loved to put out numbers like that in this challenging climate.

It’s true that 20% top-line growth is nearly half the 39% jump that it posted back in November of last year when its stock hit an all-time high. Growth has been cut in half. Why shouldn’t the stock’s market value be cut by more than half? It’s not a fair judgment for Cava.

The chain is still posting double-digit revenue growth and positive comps at a time when many of its peers are struggling. It’s not a failure risk. There is no long-term debt on its balance sheet, just the long-term lease obligations of its growing company-operated empire.

Cava’s trading at an enterprise value that is 7.2 times its trailing revenue. This is higher than Chipotle’s multiple of 5.2, but it’s a historical discount for a company that is now proven with more than $1 billion in sales over the past 12 months. If you think Chipotle’s P/E ratio is rich at 38, you won’t be relieved to see Cava trading for 58 times its trailing inflated profitability. However, companies deserve a premium when they are operating at a higher level than their peers. There is still a long runway for growth. It still expects to top 1,000 locations by 2032, a 150% burst in the next seven years. Scalability will boost profitability under a kinder climate.

Cava may not seem textbook cheap, but it doesn’t mean that it will get cheaper. Buying quality at a discount — and that’s where Cava finds itself right now — could be the right move for opportunistic investors.

Rick Munarriz has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Chipotle Mexican Grill. The Motley Fool recommends Cava Group and recommends the following options: short September 2025 $60 calls on Chipotle Mexican Grill. The Motley Fool has a disclosure policy.

High-end wellness resorts, clinics, and spas are part of ambitious national development programs in Saudi Arabia and its neighbors.

According to the medical journal The Lancet, the Gulf Cooperation Council countries, along with the rest of the Middle East and North Africa, will lead the world in youth obesity by 2050. The GCC region would not seem an obvious candidate to lead a global drive in wellness tourism, then. Right?

Think again. The GCC wellness tourism market is set to grow at a compound annual growth rate (CAGR) of around 17%, reaching $1.4 trillion by 2027, according to projections by the Global Wellness Institute (GWI), a Miami-based nonprofit. The Middle East, including the GCC, accounts for only about 2% of today’s booming global market, which is expected to surpass $1 trillion this year, but it is the fastest growing region for wellness tourism spending, the GWI calculates.

GCC governments see wellness as a good fit because it brings together two fields they are betting on for fast growth: tourism, and biotechnology, pharmaceuticals, and medical innovation. On the tourism side, they are already building several large-scale projects, including Saudi Arabia’s AlUla, its Red Sea project; Diriyah, Qiddiya, and NEOM. Oman, Qatar, and the United Arab Emirates are all pursuing similarly ambitious initiatives.

Vivek Madan, partner, Strategy & Middle East, PwC

While not all related to wellness, over 600 hotel projects with 140,000-plus rooms were under development in the Middle East in early 2024, according to “The Future of Wellness: 2025 Trends,” a reported published recently by the Global Wellness Summit (GWS), a sister company of the GWI.

Ambitious national development programs launched in the last decade, such as Saudi Arabia’s Vision 2030, the UAE’s Vision 2031, and Qatar’s National Vision 2030, are driving the stunning numbers, experts say. Designed to reduce dependence on oil and gas and encourage economic diversification, these programs help channel investment into target sectors.

Priorities vary, but most include tourism, health care, sports, and cultural heritage.

“Tourism has become a central pillar in national diversification agendas, particularly in countries like Saudi Arabia, the UAE, and Qatar,” says Vivek Madan, partner, Strategy & Middle East, part of PwC’s global strategy consulting business. “These governments are investing heavily in infrastructure and destination branding to reduce reliance on hydrocarbons and unlock long-term, sustainable economic growth.”

Before its diversification drive kicked off, Saudia Arabia was already receiving considerable inflows of religious and business travelers.

“You have an ecosystem in place” that includes international operators and a talent pool, says Oussama El Kadiri, head of Hospitality, Tourism, and Leisure Advisory for the MENA region at Knight Frank, a London-based global real estate consultancy. “It’s low-hanging fruit to attract additional players to the game and open the country to the leisure part. It seemed like the immediate path towards diversification.”

The GWS report notes, “Saudi Arabia’s wellness market alone is valued at $19.8 billion, with wellness tourism growing at an annual rate of 66%.”

Wellness As Import Substitution

The wellness travel market is increasingly split into two distinct segments, albeit with some cross-pollination. “Softcare” tends to be less expensive, simpler and slower, according to GWS. Think nutrition programs, alternative therapies, meditation, fitness classes, health assessments, and stress management programs. “Hardcare” means high-end, high-tech medicine, such as biohacking and longevity clinics. Most GCC countries are investing in both.

In addition to attracting foreign visitors, state-of-the-art centers are also designed to cater to high-end locals who would previously have traveled abroad for high-quality treatment: the health and wellness industry as import substitution.

“People from the Middle East like to go to health and wellness clinics in Switzerland and Germany,” observes Corina Goetz, founder and CEO of Star-CaT, a London-based business consultancy specializing in the region. “Of course, it makes sense to partner up [with foreign investors] so you can keep the money in the country.”

Oussama El Kadiri, head of Hospitality, Tourism, and Leisure Advisory for the MENA region at Knight Frank

The range of projects on the softcare side is varied, reflecting its ambitions.

SHA Emirates will open next year as an outpost of the Spanish wellness clinic, the GWS report notes. “Billing itself as the world’s first ‘healthy living island,’” the resort will include 100 residences and combine “clinical care with mindful living.”

Saudi Arabia’s Red Sea Project has captured the imagination of locals and foreigners alike, thanks in part to promotional social media posts by the Portuguese footballer Cristiano Ronaldo, made during a break from representing the local side, Al-Nassr FC. Tourism boosters “actually created a whole program around him,” says Goetz. “You can do the Ronaldo experience at the Red Sea, and you can do exactly what he did.”

The development, which Madan says, “integrates wellness into ultra-luxury resorts like Desert Rock and AMAALA,” spans 28,000 square kilometers, encompasses over 90 islands, and is targeting 150 million visitors a year by 2030 for a $5.3 billion contribution to Saudi GDP.

With a price tag topping $500 million, Therme Dubai promises to become the world’s tallest wellness center when it opens in 2028. In the spirit of Ski Dubai, the desert city’s famous indoor slopes, the center will feature the world’s largest indoor botanical garden, three 18-meter waterfalls, and a water park in addition to a myriad of spa facilities inspired by ancient traditions from around the world. Capacity will be 1.7 million visitors a year.

“It’s like a tropical wellness concept,” says El Kadiri. “You will be in this place where they will recreate tropical weather conditions,” bestowing the associated wellness benefits.

In contrast to ostentatious Dubai, Oman is developing coastal, mountain, and thermal spring attractions, “leveraging its natural assets to attract eco-conscious wellness tourists,” in the words of Alwaleed Alkeaid, founder of Fitlee for Corporate Wellness, a Riyadh-based corporate wellness service provider, and former CEO of the Saudi Boxing Federation. The Omanis want to focus on “quiet luxury” and “authenticity,” El Kadiri notes. Nearby heritage sites are to be combined with wellness offerings to emphasize cultural travel, he adds.

Qatar’s Zulal Wellness Resort by Chiva-Som, a Bangkok-based wellness resort operator, aims to become “the region’s first family-wellness offering,” Madan says. The project “signals a shift toward scale and sophistication in wellness infrastructure. It is one of the largest wellness destinations and the first and only full-immersion resort in the Middle East, founded on traditional Arabic and Islamic medicine (TAIM).”

Dubai and Abu Dhabi lead the region in hardcare. Last year, Dubai inaugurated a Longevity Hub by Clinique La Prairie in partnership with the renowned Swiss longevity clinic. In April, Abu Dhabi launched the HELM Abu Dhabi cluster, a hub for research and development in health, endurance, longevity, and medicine. It is projected to contribute $25.6 billion to the emirate’s GDP, create 30,000 new jobs, and bring in $11.5 billion in investment by 2045 by tapping into a global health care market projected to reach $25.3 trillion by then.

“While the wellness tourism push and the HELM cluster initiative are distinct efforts, they do share complementary goals,” says Sami Khawaja, partner at PwC’s Strategy& Middle East. “The HELM cluster has a broader focus that includes advanced biotech, pharmaceutical manufacturing, digital health, AI integration, and precision and preventive medicine: all supported by cutting-edge infrastructure.”

Upscale mega-projects command most of the attention, but there are early indications that the wellness economy may be spreading to average GCC citizens.

“These [big tourism] initiatives not only attract international visitors but also promote local wellness cultures, fostering a more health-conscious population,” the GWS report argues.

Locals and resident expatriates are packing newly opened fitness clubs. From around 100 two decades ago, Saudi Arabia now boasts 2,100 and counting.

As Ethereum soars in value, this little-known cryptocurrency could go along for the ride.

Approximately one-half of the top 100 cryptocurrencies (as ranked by market cap) have outperformed Bitcoin(BTC 1.40%) over the past 90 days. During that time period, Bitcoin is up an unremarkable 2%. In comparison, a number of top altcoins have soared 75% or more.

So which is the next crypto that’s ready to explode in 2025? To answer that question, it’s helpful to understand which altcoins are currently soaring in value, and what they all have in common. Let’s take a closer look.

Which cryptocurrencies are outperforming Bitcoin?

Right now, 45 altcoins are beating Bitcoin soundly. The list of top performers includes a few meme coins, such as Pudgy Penguins(PENGU 0.58%), which is up a head-spinning 148% over the past 90 days on August 26. The good news is that investors can safely ignore these meme coins due to their mercurial, volatile nature. If anyone can explain why digital penguins have gone viral over a long, hot summer, please tell me.

The name that really jumps off the list of top performers is Ethereum(ETH 1.49%), which is up 75% over the past 90 days. The world’s second-largest cryptocurrency is attracting the attention of both retail and institutional investors, due to its recent explosive run.

Image source: Getty Images.

Moreover, several top decentralized finance (DeFi) cryptocurrencies have turned in some stunning performances over the past 90 days. For example, both Chainlink(LINK 1.45%) and Uniswap(UNI 0.44%) are up 55%. Not to go too deep into the weeds here, but both of these are ERC-20 tokens, meaning that they were designed to run on the Ethereum blockchain.

Both of these cryptocurrencies are direct plays on the growth potential of decentralized finance, and especially on the surge in new activity happening within the Ethereum blockchain ecosystem. From my perspective, these DeFi tokens are exactly the sorts of cryptocurrencies that can explode later in 2025.

Based on the above, it’s possible to put together a convincing investment thesis for the second half of 2025. The spate of new crypto legislation coming out of the United States, combined with the growing pace of crypto adoption around the world, is leading to new opportunities for DeFi tokens, and especially those that run on top of the Ethereum blockchain. If any cryptocurrency is going to pop soon, it will likely be one of these.

Meet Ondo, the crypto that could explode soon

It may be too late to get in on Ethereum, but there are some intriguing options lurking elsewhere within Ethereum’s blockchain ecosystem. One that has my attention is Ondo(ONDO 2.92%). It’s currently ranked No. 38 among all cryptocurrencies, with a nearly $3 billion market cap.

Ondo is also an ERC-20 token (just like Chainlink and Uniswap), but is probably off the radars of most investors. It is only down 2% over the past 90 days, so it’s basically running neck-and-neck with Bitcoin.

What’s tempting about Ondo is that it’s a direct play on all the goodness happening within DeFi. It’s a token primarily favored by institutional investors, and promises to bring “institutional grade” finance to crypto.

Ondo is primarily used for real-world asset (RWA) tokenization, which is one of the hottest investment ideas within DeFi right now. This refers to the process of transforming real-world assets (such as stocks and bonds) into blockchain assets.

This cryptocurrency also has the support of World Liberty Financial, the crypto venture affiliated with the Trump family. In February, World Liberty Financial scooped up nearly $500,000 worth of Ondo tokens.

Moreover, I’ve already seen a recent glimpse of the amazing upside potential of Ondo. At the end of last year, Ondo more than tripled in value and hit an all-time high of $2.14. Given that Ondo is now trading for around $1, this implies that Ondo could have the potential to double in value, in order to regain its all-time high. Asking for Ondo to do much more than that, though, might be too much.

Picking winners in crypto

Be aware: It is notoriously difficult to pick the next big winner in crypto. Investment narratives fall in and out of favor. Meme coins come and go, and top cryptos can rise or fall, often based on no apparent reason. Risk and volatility are very much an issue any time you venture beyond Bitcoin or Ethereum.

But if you’re willing to take on the risk, then it might be time to look for coins that haven’t popped yet. The best investment opportunities are those that are linked to the Ethereum DeFi investment narrative. This narrative jas already worked with Chainlink and Uniswap, both of which are up big over the past 90 days.

Could Ondo be next?

Dominic Basulto has positions in Bitcoin, Chainlink, Ethereum, and Ondo. The Motley Fool has positions in and recommends Bitcoin, Chainlink, Ethereum, Ondo, and Uniswap Protocol Token. The Motley Fool has a disclosure policy.

You may be surprised to know which cryptocurrency has had the best year so far.

When Bitcoin was created in 2009, it was seen as nothing more than a niche internet experiment. There are plenty of stories about people using the cryptocurrency to buy items like pizza, gift cards, or coffee (a decision they likely rue now).

But as Bitcoin became more popular, many other cryptocurrencies emerged. Some of these have legitimate use cases, and some can be viewed as nothing but a quick cash grab from their creators and early insiders. One cryptocurrency that falls into the former category is XRP(XRP 3.48%).

XRP is a cryptocurrency that enables fast and cheap cross-border payments, and it has had a great run over the past 12 months, up over 390%. That’s over five times the returns of Bitcoin and Ethereum in that span. The recent rally may have investors thinking they missed the wave, but there’s one big reason why there’s still time to hop on the boat.

Image source: Getty Images.

Cross-border payments are becoming more frequent

Sending money from one country to another has traditionally been expensive because of the reliance on banks (and pre-funded accounts) and high intermediary fees. However, with the introduction of XRP and other nontraditional sources, these transactions are increasingly becoming cheaper and more frequent.

According to Allied Market Research, the global cross-border payments market was around $206 trillion at the end of 2024. By 2034, it’s expected to be around $414 trillion. This is great news for XRP because it feeds right into its main use case of being a bridge currency to facilitate these transactions.

What traditionally could cost someone 5% to 7% of the transfer amount , XRP is able to do it for fractions of a cent and much faster. If XRP can capture even a small fraction of the cross-border payment flow, it can be a good investment for some time.

Stefon Walters has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Bitcoin, Ethereum, and XRP. The Motley Fool has a disclosure policy.

With a little planning, you could lower your healthcare costs substantially.

There’s a reason so many retirees worry about running out of money. Once you move over to a fixed income, it’s important to keep your costs as fixed as possible. But as we all know, inflation has a sneaky way of driving living costs up.

This especially holds true in the context of healthcare. Fidelity says that a 65-year-old who’s leaving the workforce this year can expect to spend $172,500 on healthcare costs in retirement. That’s a 4% increase from last year, and a pretty daunting number overall.

Image source: Getty Images.

That’s why it’s so important to be strategic when it comes to all things Medicare. With that in mind, here are a few Medicare moves that could save you big money in retirement.

1. Enroll on time

Although Medicare eligibility generally begins at 65, you don’t have to wait until you turn 65 to sign up. Your initial enrollment period begins three months before the month of your 65th birthday, and it ends three months after the month you turn 65.

If you don’t enroll during that initial window, but rather much later, you’ll put yourself at risk of lifelong Medicare surcharges. Specifically, you’ll face a 10% increase in your Part B premium costs for each 12-month period you were able to get Medicare but didn’t enroll. And that surcharge is one that applies for life.

For this reason, it’s best to plan to enroll in Medicare on time unless you have qualifying group health coverage through an employer. In that case, you’ll generally qualify for a special enrollment period and won’t be penalized for failing to enroll during your seven-month initial enrollment window.

2. Review your plan choices annually

Each year, Medicare holds an open enrollment period from Oct. 15 through Dec. 7. During this window, existing Medicare enrollees can make a host of changes, such as:

Joining a Medicare Advantage plan for the first time.

Switching Medicare Advantage plans.

Switching Part D drug plans.

Moving from Medicare Advantage to original Medicare.

It’s important to review your plan choices each year, even if you’re reasonably happy with your existing coverage. That’s because:

Your plan’s rules and costs can change.

Your healthcare needs can change.

There may just be a better plan out there for you.

Switching Medicare plans could, depending on the circumstances, result in lower premiums and copays. So it pays to do your research each fall.

3. Buy a Medigap plan

If you’re planning to stick with original Medicare, as opposed to Medicare Advantage, then it pays to buy Medigap coverage early on. Medigap is supplemental insurance, and it could kick in when you’re facing hefty costs like coinsurance for a hospital stay or skilled nursing facility.

Your initial Medigap enrollment window begins the month you’re enrolled in Medicare Part B and are 65 or older. And that window lasts six months.

It pays to buy your Medigap coverage during that time because you can’t be denied for pre-existing conditions. If you wait, you risk being denied coverage for your plan of your choice, or getting coverage at a (much) higher premium rate.

It’s natural to worry about money in retirement. But if you’re smart about Medicare, you can potentially lower some of your health-related expenses and stretch your nest egg further. So it pays to make these essential Medicare moves if you like the idea of having healthcare in retirement cost less.

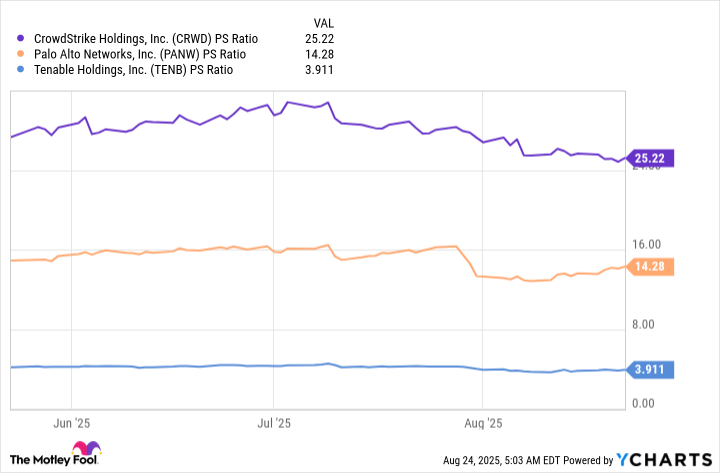

Demand continues to grow for Tenable’s expanding portfolio of cybersecurity solutions.

Enterprises are using artificial intelligence (AI) at an increasing rate, which is creating a new attack surface for hackers to exploit. AI-powered attacks are also on the rise, which calls for highly sophisticated cybersecurity solutions.

Palo Alto Networks and CrowdStrike lead the cybersecurity industry, but they aren’t the only vendors experiencing a surge in demand for their products. Tenable(TENB -1.50%) is a specialist in vulnerability management, helping enterprises thwart the very threats posed by AI.

With a market capitalization of just $3.7 billion, Tenable is still a tiny player in the cybersecurity space. However, the company’s operating results for the recent second quarter of 2025 (ended June 30) revealed accelerating revenue growth, an uplift in guidance, and a record number of high-spending customers.

Tenable stock remains 49% below its 2022 record high, but here’s why it’s time for investors to pay attention to this up-and-coming cybersecurity powerhouse.

Image source: Getty Images.

A vulnerability management specialist

Tenable owns Nessus, which is the cybersecurity industry’s most accurate and most widely deployed vulnerability management platform. It proactively scans devices, networks, and operating systems to identify potential weak points, so they can be patched before malicious actors exploit them.

But Nessus has become an onramp to Tenable’s growing portfolio of other advanced cybersecurity products. The company has consolidated many of them to create a comprehensive exposure management platform called Tenable One, which protects cloud networks, employee identities, endpoints, infrastructure, and more.

Tenable has the world’s largest repository of exposure data, which allows Tenable One to proactively surface and mitigate threats better than any other platform of its kind.

The company also offers a product called AI Exposure, which helps enterprises secure their AI software, AI platforms, and AI agents. It gives managers visibility into how employees are using AI across the organization, and it allows them to build guardrails to reduce risk. This is especially useful when employees are plugging sensitive internal data into large language models (LLMs) from third-party developers.

Accelerating revenue growth and increased guidance

Tenable generated $247.3 million in revenue during the second quarter of 2025, which was comfortably above management’s forecast of $241 million to $243 million. It represented a year-over-year increase of 12%, which marked an acceleration from the 11% growth the company delivered in the first quarter.

The strong result was driven by high-spending enterprises. Tenable had a record 2,118 customers with at least $100,000 in annual contract value during the second quarter, which highlights how important advanced cybersecurity solutions are becoming to large organizations.

Tenable’s recent momentum might be a sign of things to come, because management adjusted its 2025 full-year revenue guidance to $984 million (at the midpoint of the range), which was an increase of $9 million from its previous forecast three months ago.

Management also made further progress at the bottom line during the second quarter. The company suffered a small loss on a GAAP (generally accepted accounting principles) basis, but after excluding one-off and non-cash expenses like stock-based compensation, the company generated an adjusted (non-GAAP) profit of $41.4 million. That figure was up by almost 9% compared to the year-ago period.

Tenable’s ability to deliver accelerating revenue growth without sacrificing profitability is a sign of strong organic demand for its products.

Tenable stock looks attractive at the current level

The 49% decline in Tenable stock since 2022, combined with the company’s consistent revenue growth, has pushed its price-to-sales (P/S) ratio down to just 3.9. That is a substantial discount to the valuations of industry leaders like Palo Alto and CrowdStrike:

Palo Alto and CrowdStrike operate much larger businesses than Tenable, and they are also delivering faster revenue growth. However, considering Tenable’s momentum right now, I think the valuation gap deserves to be much narrower. Plus, Tenable values its addressable market at $50 billion in the exposure management space alone, and the company’s current revenue suggests it has barely scratched the surface of that opportunity.

As a result, Tenable could be a great long-term buy for investors who are looking to add a cybersecurity stock to their portfolio.

Anthony Di Pizio has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends CrowdStrike. The Motley Fool recommends Palo Alto Networks. The Motley Fool has a disclosure policy.

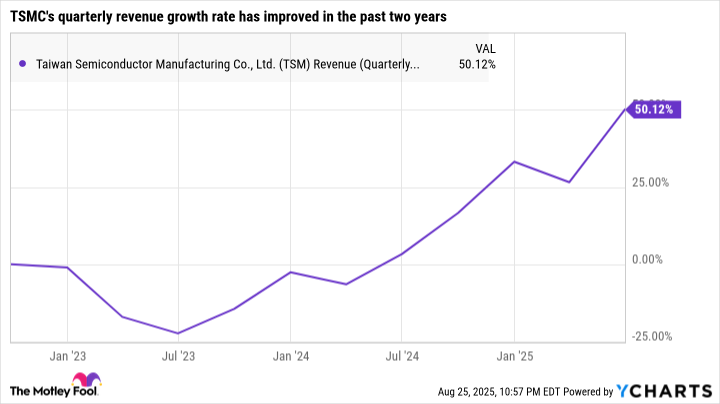

This semiconductor giant has outperformed the Nasdaq Composite index handsomely in the past decade.

The tech-laden Nasdaq Composite index clocked impressive gains in the past decade, rising 374% during this period and outpacing the S&P 500 index’s jump of 240%. The disruptive nature of technology companies is a key reason why the Nasdaq has delivered above-average returns. Tech companies can grow at faster rates thanks to the innovation taking place in this sector. New products, services, and features can witness rapid adoption by customers, organizations, and governments, leading to robust revenue and earnings growth for tech stocks.

Taiwan Semiconductor Manufacturing(TSM 1.26%), popularly known as TSMC, enables innovation and disruption with its advanced chip manufacturing processes. Not surprisingly, TSMC stock has shot up a remarkable 12.5x in the past decade, significantly outpacing the Nasdaq Composite index’s jump.

Let’s look at the reasons why it has real potential to keep outperforming the Nasdaq Composite in the next 10 years.

Image source: Getty Images.

TSMC’s growth is likely to accelerate in the coming decade

TSMC is the world’s largest semiconductor foundry. According to Counterpoint Research, it controlled 35% of the global Foundry 2.0 market in the first quarter of 2025, growing its share by almost six percentage points from the year-ago period.

The Foundry 1.0 market is defined by pure chip manufacturing, while Foundry 2.0 includes ancillary services such as advanced packaging, assembly and testing, and photomasking. TSMC, which was a pure-play chip manufacturer earlier, has been expanding its expertise to offer Foundry 2.0 solutions to its customer base.

This explains why the company keeps gaining a bigger share of this market. TSMC established a massive lead over its rivals in the Foundry 2.0 space, with second-placed Intel controlling just over 6% of this market in the first quarter. Another thing worth noting is that the Foundry 2.0 market saw a 13% year-over-year increase in revenue in Q1 2025 to $72 billion, driven by the growth of artificial intelligence (AI) and high-performance computing chips.

TSMC’s advanced chip manufacturing processes are tapped by several fabless chip designers such as AMD, Nvidia, Broadcom, Sony, Apple, Qualcomm, and others, who don’t have manufacturing facilities of their own. These companies have been tapping TSMC’s 3nm (nanometer) and 5nm process nodes to fabricate AI chips that go into multiple applications ranging from data centers to consumer electronics devices to vehicles.

Specifically, 60% of TSMC’s revenue came from the high-performance computing (HPC) segment in the previous quarter, while smartphones accounted for 27%. The Internet of Things (IoT) and the automotive segment aren’t moving the needle in a significant way for the company right now. However, all these end markets are expected to clock healthy growth over the next decade, paving the way for secular growth at TSMC.

Deloitte, for instance, points out that the growth of AI is expected to lead to a 30x increase in data center power demand by 2035. This rapid surge will be driven by the construction of more data centers needed to tackle AI workloads. According to one estimate, AI-focused data center spending is expected to jump by almost 4x by 2030, which should allow TSMC to sell more of its advanced chips.

Meanwhile, the adoption of AI in other areas, such as robotics and the automotive industry, can create more lucrative growth opportunities for TSMC. In all, the AI chip market expects to clock an annual growth rate of close to 35% through 2035. TSMC’s solid share of the foundry market puts it in a solid position to make the most of this massive growth opportunity.

Product development moves should help it maintain its solid position

TSMC’s growth picked up impressively in the past couple of years on account of the AI boom.

The company expects 30% revenue growth this year. It can sustain such impressive growth levels in the future as well, since it is focused on further advancing its manufacturing processes, which should enable it to maintain its healthy lead in this market. For example, TSMC is already constructing 2nm and A16 (1.6nm) chip fabrication facilities.

These new processes are expected to deliver significant performance and efficiency gains over the company’s current 3nm chip node. The 2nm process, for instance, is expected to deliver a 10% to 15% increase in performance while reducing power consumption by 20% to 30%. The A16 process is also expected to replicate such gains when compared to the 2nm process.

The improved performance of TSMC’s new chips should come in handy while tackling AI workloads in the cloud and in edge devices such as smartphones and personal computers. So, TSMC seems set to retain its lead in the foundry market in the future. As such, it is a no-brainer buy right now at 25 times earnings since its healthy financial performance can help this AI stock outpace the Nasdaq Composite’s gains over the next 10 years.

Harsh Chauhan has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Advanced Micro Devices, Apple, Intel, Nvidia, Qualcomm, and Taiwan Semiconductor Manufacturing. The Motley Fool recommends Broadcom and recommends the following options: short August 2025 $24 calls on Intel. The Motley Fool has a disclosure policy.

Following rallies in excess of 2,000%, both of these widely owned industry leaders may be set for epic pullbacks.

Arguably, nothing has commanded the attention of professional and everyday investors quite like artificial intelligence (AI). In Sizing the Prize, the analysts at PwC forecast AI would provide a $15.7 trillion boost to the global economy by 2030, with $6.6 trillion tied to productivity improvements, and the remainder coming from consumption-side effects.

Excitement surrounding this technology has sent some of the market’s largest and widely held AI stocks soaring, including AI-data mining specialist Palantir Technologies(PLTR 2.37%) and electric-vehicle (EV) manufacturer Tesla(TSLA 1.42%).

But just because these stocks have been (thus far) unstoppable, it doesn’t mean optimism is universal among analysts. Two Wall Street analysts who are respective longtime bears of Palantir and Tesla stock believe both companies will lose most of their value.

Image source: Getty Images.

1. Palantir Technologies: Implied downside of 72%

There’s a solid argument to be made that Palantir has been the hottest AI stock on the planet since 2023 began. Shares have rallied approximately 2,370%, with Palantir adding more than $360 billion in market value, as of the closing bell on Aug. 22.

Both of the company’s core operating segments, Gotham and Foundry, lean on AI and machine learning. Gotham is Palantir’s breadwinner. It’s used by federal governments to plan and execute military missions, as well as to collect/analyze data. Meanwhile, Foundry is an enterprise subscription service that helps businesses better understand their data and streamline their operations. Neither operating segment has a clear replacement at scale, which means Palantir offers a sustainable moat.

But in spite of Palantir’s competitive edge, RBC Capital Markets’ Rishi Jaluria sees plenty of downsides to come. Even though Jaluria raised his price target on Palantir shares for a second time since 2025 began, his $45 target implies downside of up to 72% over the next year.

If there’s one headwind Jaluria consistently presents when assigning or reiterating a price target on Palantir, it’s the company’s aggressive valuation. Shares closed out the previous week at a price-to-sales (P/S) multiple of roughly 117!

Historically, companies that are leaders of next-big-thing technology trends have peaked at P/S ratios of approximately 30 to 40. No megacap company has ever been able to maintain such an aggressive P/S premium. While Palantir’s sustainable moat has demonstrated it’s worthy of a pricing premium, there’s a limit as to how far this valuation can be stretched.

Jaluria has also previously cautioned that Foundry’s growth isn’t all it’s cracked up to be. Specifically, Jaluria has opined that Foundry’s tailored approach to meeting its customers’ needs will make scaling the platform a challenge. Nevertheless, Palantir’s commercial customer count surged 48% to 692 clients in the June-ended quarter from the prior-year period, which appears to be proving RBC Capital’s analyst wrong.

There’s also the possibility of Palantir stock being weighed down if the AI bubble were to burst. History tells us that every next-big-thing trend dating back three decades has undergone a bubble-bursting event early in its expansion. While Palantir’s multiyear government contracts and subscription revenue would protect it from an immediate sales decline, investor sentiment would probably clobber its stock.

Image source: Tesla.

2. Tesla: Implied downside of 94%

Over the trailing-six-year period, shares of Tesla have skyrocketed by more than 2,200%. Though Tesla hasn’t moved in lockstep with other leading AI stocks, its EVs are increasingly reliant on AI to improve safety and/or promote partial self-driving functionality.

Tesla was the first automaker in more than a half-decade to successfully build itself from the ground up to mass production. It’s produced a generally accepted accounting principles (GAAP) profit in each of the last five years, and it delivered in the neighborhood of 1.8 million EVs in each of the previous two years.

In spite of Tesla’s success and it becoming one of only 11 public companies globally to have ever reached the $1 trillion valuation mark, Gordon Johnson of GLJ Research sees this stock eventually losing most of its value. Earlier this year, Johnson reduced his price target on Tesla to just $19.05 per share, which implies an up to 94% collapse.

Among the many concerns cited by Johnson is Tesla’s operating structure. Whereas other members of the “Magnificent Seven” are powered by high-margin software sales, Tesla is predominantly selling hardware that affords it less in the way of pricing power. Tesla has slashed the price of its EV fleet on more than a half-dozen occasions over the last three years as competition has ramped up.

Johnson has also been critical of Tesla’s numerous side projects, which are providing minimal value to the brand. Although energy generation and storage products have been a solid addition, the company’s Optimus humanoid robots and extremely limited robotaxi service launch have been grossly overhyped.

This builds on a larger point that Tesla CEO Elon Musk has a terrible habit of overpromising and underdelivering when it comes to game-changing innovations at his company. For instance, promises of Level 5 full self-driving have gone nowhere for 11 years, while the launch of the Cybertruck is looking more like a flop than a success.

Furthermore, Tesla’s earnings quality is highly suspect. Though the company has been decisively profitable for five straight years, more than half of its pre-tax income in recent quarters has been traced back to automotive regulatory credits and net interest income earned on its cash. In other words, a majority of Tesla’s pre-tax income derives from unsustainable and non-innovative sources that have nothing to do with its actual operations. Worse yet, President Trump’s flagship tax and spending bill, the “Big, Beautiful Bill” Act, will soon put an end to automotive regulatory credits in the U.S.

What investors are left with is an auto stock valued at north of 200 times trailing-12-month earnings per share (EPS) whose EPS has been declining with consistency for years. While Johnson’s price target appears excessively low, paying over 200 times EPS for a company that consistency underdelivers is a recipe for downside.

I’m watching overtourism in action. Within the iridescent marvel that is Croatia’s Blue Cave, four boats holding about a dozen people each have an allotted 10 minutes before we motor back out again so that the next batch of visitors can float in. About 1,500 people a day visit this beautiful grotto on the island of Biševo, the biggest attraction within the Vis archipelago, two hours and 20 minutes south of Split by ferry. After paying the €24 entrance fee, I’m left underwhelmed by this maritime conveyor belt. At least the 45-minute foot ferry from Komiža, on the archipelago’s main island of Vis, to Biševo’s Mezoporat Bay, the launch point for boats to the Blue Cave, is only €4.

Many of the other cave visitors are on one of the countless speedboat tours departing from all over Dalmatia and crowding into Mezoporat Bay before whizzing off elsewhere. I’m staying on Vis itself to take a longer, slower, more satisfying look at the island, where I spent a night three years ago and which I’ve been hankering to revisit ever since. Despite the overwhelming popularity of the nearby Blue Cave and its speedboat tours, plus the boost in tourism on Vis after much of Mamma Mia! Here We Go Again was filmed here in 2017, I know there’s a quieter, mellower side to the island, and it doesn’t take long to find it.

In sleepy Rukavac on Vis’s south-eastern coast, British couple Xania and Craig Wear welcome me into one of their four guest rooms in the large stone house they renovated after moving here 20 years ago. The former PE teachers run WearActive, offering yoga, kayaking, paddleboarding and cycling in Rukavac. On their seven-day, “relaxingly active” holidays you can do as much or as little as you like. “Actively relaxing”, I find, is just as fitting a description.

Kayaking just off Stiniva beach, Vis. Photograph: Mary Novakovich

Xania serves delicious plant-based food on the large shaded terrace, which has views of the sea. But before breakfast we walk to the flat rocks of Bili Bok beach, where Craig puts me through my yoga paces. Clean, salty air fills my lungs as I lunge and stretch by the Adriatic. I follow this with a swim at nearby Srebrna beach. Late afternoons are spent lazing on the pebbles at Tepluš beach, 10 minutes’ walk from the house. I could get used to this.

The next morning, my hosts suggest kayaking 6 miles (10km) from Rukavac to Stiniva Bay, Vis’s most famous beach and a place of peerless beauty. Two giant limestone cliffs curve round the pebbly beach, nearly meeting in the middle. From the top of the hill behind the cliffs there’s a steep, rocky footpath to the beach, but it’s infinitely more enjoyable to paddle on to the beach, where only kayaks, paddleboards and small rubber dinghies are allowed. Craig is on a paddleboard, while Xania and I share a kayak, and my husband has a single kayak. At 8.30am there are only about four people here, and we have a blissful, peaceful swim.

The Blue Cave of Biševo is beautiful but can be very busy with visitors. Photograph: Mary Novakovich

Craig knows I’ve always wanted to learn how to paddleboard, so on the way back to Rukavac we stop in tranquil Ruda bay. After some expert instruction, I’m on the board and paddling away, initial jitters soothed by the hypnotic motion of gliding on the water. Now I see what all the fuss is about.

Away from the water, my husband and I get to know Vis more intimately, crisscrossing its vineyard-covered interior and heading up and down its winding mountain roads. Its capital, Vis town, dozes during the day, most restaurants closing while the sailing crowd cruises. It comes alive at night, the restaurant terraces along the Venetian harbour buzzing in the summertime warmth.

Smaller Komiža is the place for lunch, with everything from cheap pizzerias to smart restaurants. Near Gusarica beach we find Konoba Jastožera, a restaurant built on stilts over the water, where lobster pots hold the restaurant’s speciality.It’s only when I hear the soundtrack to the Mamma Mia! films that I realise we’ve stumbled on one of the sequel’s filming locations, and instantly expect high prices and low quality. Wrong on both counts. As long as we don’t order lobster, it’s one of the most affordable restaurants we’ve seen so far, with two courses for €25. It’s not all money, money, money here.

Mary Novakovich in Konoba Jastožera. Photograph: Adam Batterbee

For an island that was off limits to foreigners until 1989, when the Yugoslav army base here closed down, Vis seems to be taking its time in developing its tourism (Biševo’sBlue Cave aside). I spot a few military tours about, taking people to the huge network of tunnels and bunkers left behind by the army. I get a fascinating glimpse into 1944 Vis when I hike up to the collection of caves at the foot of Mount Hum, where future Yugoslav president Tito and his fellow partisans hid from the Nazis.

Then there’s the growth of active holiday companies bringing more people to the island, which Xania sees as a positive thing, even if it means more competition. “Vis would then become an island that’s known for its adventure holidays,” she says. “And then you have more people coming to do that kind of tourism.” I nod in agreement. The island’s natural rhythm – slow, unhurried – is one to be savoured, not raced through.

The trip was provided by WearActive, which offers seven-night active holidays from €1,590pp, including breakfast, four lunches, three dinners with wine, five days of activities, transfers to restaurants on four evenings and from Vis town ferry terminal

Watching what billionaires are doing is just step one of a larger investment process.

There are over 2,900 people in the world with a net worth of over $1 billion, according to the World’s Billionaires List from Forbes. Some build wealth by running a business, and others just allow trust fund managers to build wealth for them. But many of the world’s billionaires continue to grow their wealth through investing in stocks.

Among them are Warren Buffett, Bill Ackman, and David Tepper. Let’s look at one stock each of these investors has bought recently.

Image source: Getty Images.

1. Warren Buffett

Warren Buffett became CEO of Berkshire Hathaway through investing. And after taking over the company, he continued to invest in stocks with the company’s cash. That’s continued for decades now, allowing Buffett’s net worth to climb to over $150 billion today. And in recent months, Buffett’s Berkshire has been buying shares of Domino’s Pizza(DPZ -1.96%).

Buffett’s top rule for investing is: “Never lose money.” And I believe Domino’s Pizza stock will adhere to this rule over the long term. Here’s why.

Domino’s is the world’s largest pizza chain. But it mostly franchises its restaurants. The company operates a huge supply chain on behalf of its franchisees, which is a big reason they can run their restaurants profitably. And for its part, Domino’s makes high-margin revenue from franchise fees.

In my view, Domino’s size and supply chain are competitive advantages. The business likely won’t struggle with profitability, and management uses the profits to reward shareholders with stock buybacks and a dividend that routinely goes up.

Domino’s has underperformed the S&P 500 in recent years and could struggle to outperform in coming years. But it will likely increase in value over the long term, which is why it follows Buffett’s top rule.

Berkshire didn’t purchase many shares of Domino’s in the most recent quarter. But its stake did increase, and it now holds over 2.6 million shares of the pizza chain.

2. Bill Ackman

Before he was famous, Bill Ackman was studying Buffett’s investing philosophy to learn what he could. Considering Ackman’s net worth is over $9 billion today, I’d say it worked out pretty well. And in the second quarter, he made an investment in Amazon(AMZN 0.29%) that he believes can carry his net worth higher still.

It’s hard to argue against an investment in Amazon stock. Its relevance to consumers as the largest e-commerce company in the world is impossible to understate.

But it’s also majorly important to businesses as well. Third-party sellers reach customers with Amazon’s marketplace, advertisers can find new customers with its advertising slots, and corporations can get a tech upgrade by using the tools and products on Amazon Web Services (AWS).

Specifically with AWS, Amazon has a cash cow that can reward shareholders for years to come. Over the last 12 months, this cloud-computing division has generated over $110 billion in net sales and has earned the company almost $43 billion in operating income. It’s a huge profit stream for the company that should only continue for the long term, especially with drivers such as artificial intelligence (AI) still ramping up.

Ackman’s hedge fund, Pershing Square, bought 5.8 million shares of Amazon in the second quarter of 2025. It makes the company worth 9% of the portfolio’s value, demonstrating Ackman’s conviction in this stock.

3. David Tepper

Lastly, David Tepper has a net worth of over $21 billion. And his hedge fund, Appaloosa Management, has been busy buying shares of Vistra(VST 2.86%). This used to be a more-sleepy stock. But it’s been a top performer in recent years due to surging demand for electricity.