The Bermuda bank agrees to buy a 91.7% stake in CIBC Caribbean Bank for $1.8 billion, creating a regional giant.

This article appears in the July/August issue of Global Finance Magazine.

Butterfield Group has agreed to acquire a 91.7% stake in CIBC Caribbean Bank Limited for $1.8 billion — $1.09 billion in cash and the remainder in shares — in a deal that would create one of the region’s largest banking groups.

“This deal combines two storied, complementary banks with significant local scale advantages and time-honored customer relationships in their respective core jurisdictions,” said Michael Collins, Butterfield’s chairman and chief executive, in a statement.

The new banking group will hold an estimated $29 billion in assets. The Bermuda-based Butterfield Group—formerly The Bank of N.T. Butterfield & Son Limited—also operates in The Bahamas, the Cayman Islands, the Channel Islands, Singapore, Switzerland, and the U.K. CIBC has a presence in 10 countries and is based in Barbados.

CIBC will hold about 22% of the enlarged Butterfield Group and will have the right to appoint two directors to the board.

The bank’s top brass says the deal underscores a shift in the Caribbean financial sector.

“This is really a change in Butterfield’s positioning because it now picks up both a retail and a business portfolio that spans the entire gamut of the region, and it probably could make it the biggest bank in the region,” former Butterfield CEO Mariano Browne told the Trinidad and Tobago Guardian.

Butterfield has promised to maintain CIBC’s Barbados office. Customers should expect no immediate changes. Existing branches will remain open, and clients can expect improved cross-border payments and expanded consumer, digital, and merchant banking.

The deal, pending regulatory approval, should close in the first half of 2027.

In 2018, CIBC attempted to list FirstCaribbean on U.S. stock markets to raise up to $240 million but withdrew the application less than a month later after failing to drum up sufficient investor interest. A 2019 deal to sell 66.7% of CIBC to GNB Financial Group for $797 million fell through after the deal failed to secure regulatory approval.

Nic Wirtz is a contributing writer based in Guatemala.

Breaking a six-month record, the investment banking giant capitalizes on a surging wave of global megadeals.

Goldman Sachs said it had advised on more than $1 trillion of announced global mergers and acquisitions so far this year, the fastest any investment bank has reached that milestone in a six-month period, citing data from capital markets data provider Dealogic.

The bank attributed the milestone to a string of marquee mandates, including serving as co-financial adviser to Dominion Energy on its roughly $67 billion sale to rival utility NextEra Energy, announced last month, along with other major transactions.

Rise of the Megadeal

Goldman reported that its investment banking fees rose 48%, to $2.8 billion in the first quarter. It’s a reflection of the “K-shaped” M&A market, where megadeals are the dominant force, but deal volumes are declining, and mid-market activity is subdued.

Data compiled by PwC revealed that the global M&A market is on track to reach $4 trillion in 2026, a 13% annual increase, with major sales estimated to account for 48% of deal value worldwide, a significant expansion from two years ago.

“Goldman has been the global leader in M&A advisory fees for more than 90 consecutive quarters. The fact that it’s reaping benefits from a moment of megadeal activity simply proves the strength of its franchise,” said Mark Narron, senior director at Fitch Ratings. “However, advisory revenues are generally a small share of total revenues. In 2021, which was Goldman’s record year for advisory, advisory revenues contributed only 10% of total revenues.”

Fitch says it’s difficult to forecast whether Goldman’s advisory revenues will continue to climb, given the cyclical nature of advisory fees and uneven regional M&A trends — with most deal activity still concentrated in the U.S.

Fitch expects M&A activity to be sensitive to market conditions, economic growth, geopolitical events, and interest rates. Global growth is estimated to decelerate to 2.8% this year, according to the latest OECD economic outlook report. Inflationary pressures are rising in advanced and emerging economies due to energy shocks from the Iran conflict. Prices in the G20 economies are expected to climb to 4% in 2026. In a “prolonged disruption” scenario, inflation could rise further, which may prompt hawkish interest rate responses from central banks.

Peter Taberner is a contributing writer based in the U.K.

“Little House on the Prairie” is the third television adaptation to bear the name of Laura Ingalls Wilder’s 1935 autobiographical novel of life on the Kansas plains in 1869 to 1870. The first, the Michael Landon television series that debuted in 1974, set in Walnut Grove, Minn., is really based on Wilder’s subsequent volume, “On the Banks of Plum Creek,” while a 2005 miniseries, shown as part of “The Wonderful World of Disney,” was generally faithful to the letter and spirit of the text. The record shows that I liked it.

The new “Little House,” created by Rebecca Sonnenshine and streaming on Netflix, is fairly faithful to its spirit, and less so to its letter. At its center is the Ingalls family: father Charles (Luke Bracey), or Pa; mother Caroline (Crosby Fitzgerald), or Ma; serious older sister Mary (Skywalker Hughes), and adventurous Laura (Alice Halsey), whose story this is. They are heading out to Kansas to what they imagine is free land, though they will have a thing or two coming on that account. “This will be our new forever,” says Laura, who doesn’t yet know that her future will be in Minnesota.

To be sure, the character relations remain essentially the same. Pa will play his fiddle. Laura and Mary will dance, when not getting in one another’s hair, or sulking. There will be singing, frequently. Major episodes from the book — when Jack got lost, (Jack is the dog, and he will be found), the incident of Mr. Scott (Maclean Fish) down the well, Christmas, the one about malaria, and all the business of building the eponymous log house — are accounted for, if in some cases expanded upon or altered. So extensive are its innovations that, although I am going to point out certain departures from or additions to the text, because I am that sort of pedant, it may be best just to regard this “Little House” as an original thing, a variation on a theme by Laura Ingalls Wilder, or a reboot of the television show.

Some touches are drawn from Wilder’s own history. Her mother was a teacher before she married Charles Ingalls; her maternal grandfather died from drowning. The black cowboy hat Laura sports is straight from a photograph of Wilder as a girl. Laura is made a sort of mini-Scheherazade to foreshadow the writer she’ll become (though she’ll also ask, “What am I ever going to need in a book?”). Baby Carrie, in the novel from the start, is born, as she really was, in Kansas, meaning that Ma is pregnant through much of the season — a condition that may have seemed too complicated for a 1935 children’s book, but which adds new strains of drama to the miniseries. It also introduces a theme in which Ma, who has lost “so many” babies, is trying to give Pa a boy, though he is not the sort to be disappointed in another girl.

Also new to the story is Independence, Kan., itself, which in the book is an offstage place to which Pa will sometimes go to fetch necessities, disappearing from the story until he returns. Here it’s nearby — a nicely realized little movie town to which the whole family will sometimes repair, to shop, raise a church or join in a Founders Day celebration. It’s dominated by a less than transparent booster, Eli James (Michael Hough), who comes with a self-important wife, Jemma (Mary Holland), and a pair of teenage twin girls who might be described as all dressed up with nowhere to go.

Notably, the series’ treatment of Native Americans feels intended to rectify, or at least deepen, their portrayal in the book — naive or romantic, maybe, though not, I’d argue, negative — with added native characters and discussions regarding the land and treaties and such. While Ma frets about the natives in the neighborhood, for no reason she can articulate — one juvenile delinquent steals her cherished china figurine, but we understand that there are social causes for his behavior — Pa, who has built his house unwittingly on an Osage trail, has sympathy and perspective. (Ma will soften considerably, because this is that kind of show.)

It’s not an issue for guileless, outgoing Laura, who acquires an Indigenous best friend, Good Eagle (Wren Zhawenim Gotts). Her father, Mitchell (Meegwun Fairbrother) will be a friend to Pa and her mother, White Sun (Alyssa Wapanatâhk), will provide a skeptical counterpoint to Ma. Mission-educated, they live in a nice house with a crucifix on the wall and shelves full of literature.

Most every character gets some backstory, some traumatic. The Ingalls left Wisconsin under a cloud. (“Why didn’t anyone come to say goodbye?” wonders Laura.) (Still, it’s good to see Martin Donovan as Pa’s angry father in a fever-induced flashback.) Ma married Pa, her social inferior, against her mother’s wishes. Caleb (Kowen Cadorath), a new character who works for another new character, Emily Henderson (Barrett Doss), at the general store, was abandoned as a small child. Echoing the character played by Victor French in the TV show, Mr. Edwards (Warren Christie) has a drinking problem, brought on by a family tragedy. (In the book he describes himself as a “wildcat from Tennessee”; here he has wild … cats.) Much of the time, someone is sad. Halsey and Hughes, who are very watchable throughout, are especially good with worried looks, and Fitzgerald, perhaps the series’ MVP, is an artist when it comes to expressing concern.

Sonnenshine also invents tentative romances between Edwards and Lacey Aubert (Rebecca Amzallag), who is French, independent, runs the saloon, I guess you’d call it, dresses in black and wears trousers; between Emily and Dr. Tann (Jocko Sims), who is in the book, but much more established here; and between Mary and Caleb. All these storylines sacrifice the centrality of Laura as a character and observer and makes this “Little House” less a story of a family out on its own than a family in the context of community. (That’s for later volumes in Wilder’s nine-book saga.)

It’s very sentimental — which the novel, with its matter-of-fact, if sensually evocative prose, and its child’s-eye view, is not. The dialogue here is ripe with sampler sentiments and weighted with meaning (“Hope is everything,” “What if this is where we finally become who we’re meant to be,” “Life can get away from you if you don’t speak your heart.”) Much of the added material would have easily fit the TV series — temperamentally, it’s very much a case of late 20th century broadcast television — which to some may be a recommendation.

It’s pretty, often very pretty, to look at. The flat expanse of Winnipeg, Canada, where it was filmed, makes a good topographical match for east Kansas. Prairies are prairies.

Value up, volume down — megadeals carry record-chasing M&A market through a year of geopolitical turmoil.

Global mergers and acquisitions are on track to reach roughly $4 trillion in total value in 2026. That’s up 13% from 2025 — only the second-highest spike to the pandemic-era peak of 2021 — that figure obscures a market increasingly defined by a handful of blockbuster transactions.

Deal volume data from PwC and LSEG projects an estimated 42,000 transactions for the full year, down 13% from 2025. Megadeals exceeding $5 billion account for roughly 48% of global deal value — up from 39% in 2025 and just 26% in 2024. Remove them from the equation, and overall deal value falls 4% year over year.

Headwinds likely stymied deal activity in specific sectors. The U.S.-Israeli military campaign against Iran, launched in late February, caused what the International Energy Agency called the largest oil supply disruption in the history of the global oil market, sending energy prices sharply higher.

Despite the recent U.S.-Iran memorandum of understanding to reopen the Strait of Hormuz, the conflict cast a pall over deal activity for much of the first half of the year, particularly for transactions with any exposure to energy, logistics, or the Gulf region.

Geographic Picture Remains Uneven

The U.S. has expanded its dominance, commanding 63% of global deal value in the first half of 2026, up from 54% a year earlier, even as deal volumes fell, according to Dealogic.

Europe’s share of value also increased by 88% ($733.6 billion), buoyed by large individual transactions. The Middle East and Africa, together, saw a 45% increase in deal value ($61.3 billion).

Asia Pacific moved in the opposite direction: its share of global deal value dropped to 29% — reflecting fewer megadeals and smaller average transaction sizes relative to the U.S. and EMEA.

On the advisory side, Goldman Sachs is leading the rankings by a wide margin — $1.161 trillion in deal value across more than 200 transactions so far this year. Among the firm’s marquee assignments: advising Dominion Energy on its $66.8 billion sale to NextEra Energy, counseling Unilever on its planned $65 billion food business merger with McCormick & Company, and serving as lead-left underwriter on the SpaceX IPO.

JPMorgan ranks second with $743 billion, up from $557.1 billion a year earlier — a performance the bank has attributed in part to M&A fees that nearly doubled year over year in the first quarter of 2026. Morgan Stanley rounds out the top three at $622.5 billion.

Anthony Noto covers corporate finance and private credit. Contact him at anoto@gfmag.com

The bank names former Dream Sports executive and investment banker Raj Rathi to lead M&A business in India.

Citigroup Inc. has appointed veteran investment banker Raj Rathi as its new head of mergers and acquisitions in India, effective this month. The appointment comes as Citi deepens its advisory capabilities to capture opportunities in the Asian market.

Rathi’s hiring follows several high-profile additions to the bank’s regional investment banking team. Citi recently lured Bhavin Shukla from JPMorgan Chase & Co. to serve as managing director and head of Infrastructure Investment Banking for Japan, North and South Asia, and Australia. Last year, Citi hired Vikram Chavali from Goldman Sachs Group as its Asia-Pacific head of Global Asset Managers.

From Fantasy to Finance

Rathi was hired from Dream Sports, the multibillion-dollar parent company of fantasy gaming giant Dream11, where he served as head of Strategy and Corporate Development and oversaw the deployment of about $150 million across multiple strategic transactions.

Citi’s moves underscore a trend in which global banks are recruiting seasoned corporate executives to navigate complex digital infrastructure, the energy transition, and cross-border capital flows. Its recent high-profile transactions in the region include advising United Spirits Ltd. on the sale of its 100% stake in the Royal Challengers Bengaluru cricket team and steering Chinese appliance giant Haier Group through the sale of its 49% stake in Haier India to a consortium backed by Bharti Enterprises and Warburg Pincus.

Before his corporate development role at Dream Sports, Rathi spent five years as an executive director at J.P. Morgan, focusing on technology investment banking. He covered the technology, fintech, and consumer internet sectors, executing deals totaling about $35 billion in transaction value.

His career also included positions at Guggenheim Partners and Guggenheim Securities’ investment banking division, as well as at Ernst & Young, where he focused on financial due diligence and transaction advisory services for institutional clients, following early corporate development experience at Sutherland.

This article appears in the June 2026 issue of Global Finance Magazine.

SACRAMENTO — State Treasurer Fiona Ma and former California Senate Majority Leader Gloria Romero have been declared the two winners of a crowded primary election for lieutenant governor, securing themselves spots on the November ballot.

Ma is a Democrat. Romero is a former Democrat who said she registered as a Republican after splitting with Democrats over the push to oust President Biden as the party’s presidential nominee in 2024.

Both were declared as the top-two winners by the Associated Press. Under California’s primary system, the first and second place finisher advances to the November general election, regardless of their political affiliation.

Ma is a certified public accountant serving as state treasurer. She previously sat on the California Board of Equalization and the San Francisco Board of Supervisors. She also served three terms in the California Assembly.

Romero is an adjunct professor at Pepperdine School of Public Policy. She served as a Democrat in the Assembly and state Senate, becoming the Senate’s first woman majority leader in 2005.

Other notable candidates included former Stockton Mayor Michael Tubbs and Josh Fryday, a member of Gov. Gavin Newsom’s cabinet. Both are Democrats.

The position is largely ceremonial. The lieutenant governor serves on various boards that oversee the University of California, California State University and community college systems, and can be called upon to break a tie in the state Senate. If the sitting governor dies, resigns or is removed from office, the lieutenant governor would assume the role.

Ma and Romero have offered some similar viewpoints. Both candidates previously expressed support for the death penalty and opposition to the state’s plan to ban the sale of new gas-powered cars by 2035.

Neither candidate supports the controversial Billionaire’s Tax Act. Romero, however, has further vowed to shun all potential tax increases.

Ma and Romero will now face off in November. The winner will replace Lt. Gov. Eleni Kounalakis, who is finishing her second term and could not seek reelection. Kounalakis instead ran for state treasurer.

An acquisition is the easiest way for the titan to get a leg up with digital nomads and international customers.

At first glance, it seems an absurd idea: JPMorgan Chase & Co., with its roughly $850 billion market cap, acquiring European unicorn Revolut, a private neobank valued at $75 billion.

Seemingly absurd, yes, but also worth considering, because it underscores the challenge that upstart fintechs pose to traditional banks. JPMorgan has already tested the practicality of building a digital-first banking experience internally. It launched Finn in 2017 as a standalone mobile banking brand aimed at younger users, then shut it down in 2019 after it failed to gain traction.

But the Finn experiment was not a clean rebuttal; it looked more like a legacy institution’s attempt to market around a shifting banking relationship than a fundamental rethink. A Revolut acquisition would give JPMorgan an established entry point into a dynamic new field.

I’m old enough to remember when BlackBerry’s CEO scoffed at Steve Jobs, saying, “You don’t need an app for the web.” We know how that played out. It’s easy to dismiss what doesn’t seem to fit your current moment, and just as easy to miss the next shift when you have the means to act.

JPMorgan doesn’t need Revolut. But the point isn’t survival; it’s trajectory. If banking is moving toward super apps as primary accounts, the question is whether JPMorgan can realistically build that future internally, or whether buying it may be the faster path.

Here are four reasons it could actually make sense:

1. The Technology

Ask a senior engineer at Revolut whether JPMorgan could replicate its platform quickly, and you’re likely to get a laugh. Ask JPMorgan’s technology leadership, and you’re likely to hear the opposite.

Both can be true.

By the time JPMorgan was experimenting with the future, Revolut was writing it. The fintech hit 100,000 customers within a year of its funding and scaled to 50 million by the end of 2024. It’s redefining what consumers expect from banking in Europe, and its sights are now set on the U.S. as well. In March, it applied to the U.S. Office of the Comptroller of the Currency and the Federal Deposit Insurance Corporation for a U.S. national bank charter.

2. The Culture

JPMorgan has the resources to succeed in the era of super-apps. But building a globally integrated, mobile-first platform is as much about organizational culture as it is about technology. Revolut was built for speed, iteration, and cross-border functionality from day one. JPMorgan was built for scale, stability, and regulatory complexity.

As Finn illustrates, those traits are not easily interchangeable.

JPMorgan could buy smaller firms in payments, investing, foreign exchange, or onboarding to assemble its own version of a super app. But stitching together components is not the same as acquiring a scaled, integrated platform with tens of millions of users, unified technology, and talent that lives and breathes a culture built around speed and innovation.

Realistically, an acquisition would require a significant premium over Revolut’s most recent private valuation. But that cuts both ways; JPMorgan would be paying for a scaled operating system, not a collection of disconnected parts.

3. The Geography

The difference between the two banks shows up in their approach to competing in Europe. JPMorgan is already expanding its digital retail presence and building out its footprint beyond the U.S. But the approach is incremental.

Revolut is anything but incremental. The company has grown to more than 70 million customers, adding roughly 1 million every 17 days. It provides immediate scale in markets where JPMorgan is still building.

Banks like Banco Santander have spent decades building global retail networks, market by market. For JPMorgan, acquiring Revolut would dramatically shorten that timeline, turning a multi-year expansion into near-instant relevance.

4. The Demographics

Traditional banking still assumes a static customer: one address, one jurisdiction, one primary market. While that remains true for many customers, it doesn’t justify treating digital nomads and international customers as undeserving, which is exactly what many U.S. banks do.

A growing segment — freelancers, remote workers, and globally mobile professionals — lives across borders. They earn in one currency, spend in another, and expect their financial lives to follow them. Revolut was built specifically for this customer.

JPMorgan, for all its scale, still largely adheres to a domestic model. Acquiring Revolut would instantly position it at the center of a shift already underway: one that legacy banking structures are not designed to support.

Regulatory Hurdles

Of course, a deal this large would face serious scrutiny in the U.S. and the U.K. Regulators would question systemic risk, governance, the impact on competition, and whether one of the world’s largest banks should absorb one of fintech’s fastest-growing global challengers.

But “difficult” and “impossible” are not synonyms, especially in modern finance, where every few years brings a deal that once seemed unthinkable. If JPMorgan believed the strategic gap was large enough, regulatory friction would become part of the negotiation, not the automatic death of the deal.

It would also send a signal to regulators and policymakers — intentionally or not — that U.S. banking structures may need to loosen if domestic institutions are to compete more effectively on the global stage. Even floating a deal like a JPMorgan/Revolut tie-up would force a conversation the industry needs to have.

No, JPMorgan doesn’t need Revolut. But at some point, it may have to decide whether to write the future of banking or keep refining the version it already dominates.

Finance leaders shift from AI experimentation to measurable ROI across corporate operations.

We get it. Artificial intelligence is impressive. But how is it saving CFOs money?

Prithwijit Chaki has a take. As Global Leader for Finance Advisory at Genpact, a global professional services firm, Chaki helps chief financial officers harness AI and data to drive measurable business outcomes. With more than two decades of experience advising companies on finance strategy and large-scale transformation, he has seen firsthand how enterprises are rewiring their finance operations for an AI-first era.

Global Finance asked Chaki how that vision is taking shape and whether the conversation is no longer just about how AI can enhance productivity, but about bottom-line business value.

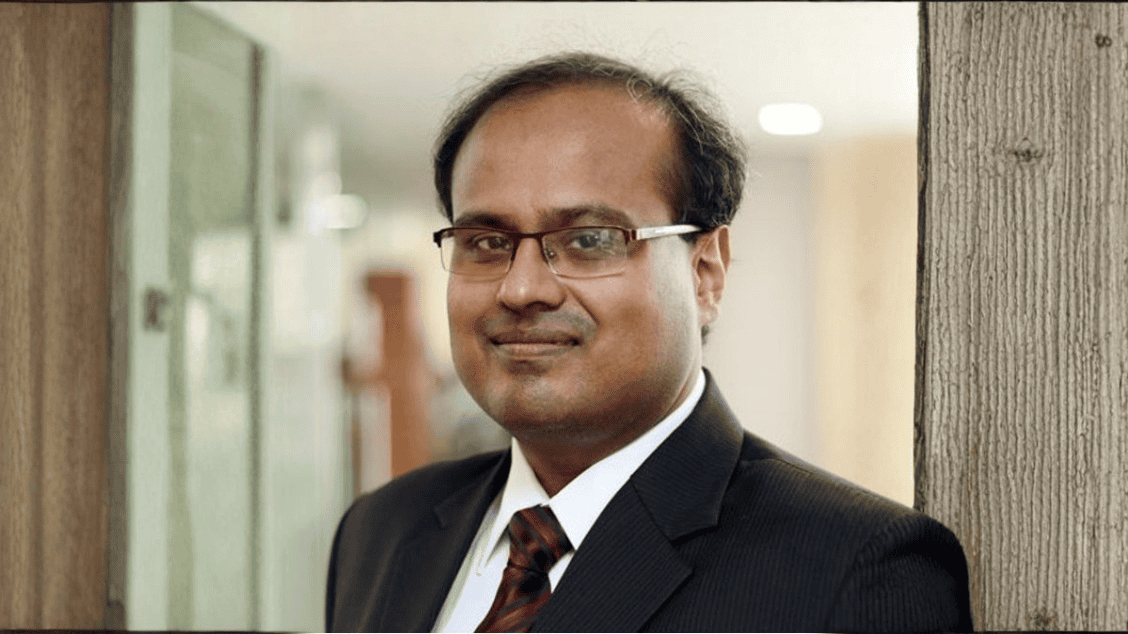

Prithwijit Chaki, Global Finance Advisory Leader, Genpact

Global Finance: CFOs have spent the last two years experimenting with AI pilots. What’s different in 2026?

Prithwijit Chaki: CFOs are moving from AI experimentation to AI accountability. After years of pilots, the question is no longer whether AI can improve individual productivity, but whether those gains translate into enterprise value across the finance function: faster close cycles, better working capital, lower manual review burden, stronger controls, or measurable business outcomes.

According to a Genpact/HFS Research report, investment in agentic AI is expected to rise 38% over the next year. However, 67% of enterprises still rely on outdated productivity metrics that fail to capture the value of autonomous decision-making. That’s the gap CFOs are trying to close in 2026: cutting through the ‘sea of sameness’ in the AI market to determine which applications can deliver real, achievable value versus which are simply adding to the noise.

GF:How does agentic AI change day-to-day finance operations?

Chaki: Traditional automation follows basic rules, and generative AI can help an individual complete a task faster. Agentic AI goes even further. It operates inside finance workflows — deciding, acting, learning, and orchestrating work across processes with people still in the loop where needed. In practical terms, that could mean moving from someone using a copilot to draft a dunning letter faster to a more integrated workflow that identifies the right action, drafts the communication, routes exceptions, applies policy guardrails, and connects the work back to measurable enterprise value.

GF:What’s one example of cost savings or business impact that CFOs see from implementing agentic AI?

Chaki: A good example is a global supply chain and distribution company processing close to 3.5 million invoices a year. After a major merger, their finance team was dealing with disconnected ERP systems, heavy manual intervention, and slow exception resolution—the kind of last-mile complexity that generic automation can’t solve. Working with Genpact, they deployed our AI-powered Genpact AP Suite combined with our agentic operations model — 21 pretrained, domain-specific AI agents that autonomously route, prioritize, and resolve invoice exceptions, with human experts validating where needed.

GF: What were the results?

Chaki: Significant. Touchless invoice processing went from 7% to 65%. Invoice cycle times were nearly halved — from 18–29 days down to 9–14 days. On-time payment rates jumped from 60% to 95%. Data extraction accuracy improved from 40% to 92%. And the system identified approximately $350 million in duplicate invoices, while early-payment discounts captured grew from $35 million to $44 million — real dollars added to the bottom line.

This isn’t a pilot or a proof of concept. It’s agentic AI operating at scale inside a core finance workflow, delivering measurable cost savings, stronger cash flow, and a fundamentally better supplier experience. That’s the kind of outcome CFOs are looking for.

GF:Which finance function is currently seeing the fastest returnsfrom AI deployment—and why?

Chaki: Accounts payable is one of the clearest areas where finance teams can see tangible value. The process has high volume and repeatable workflows, but it also has a clear ‘last mile’ problem. Invoices, approvals, exceptions, regulatory nuances, and fragmented systems still require heavy manual intervention. Generic AI can automate a large share of structured work. However, the final 20% requires domain-driven AI that understands real-world complexity, from vendor history and regional rules to exception patterns, approval chains, and master data issues. That is where agentic AI can move beyond simple extraction or automation. It can start resolving mismatches, escalating exceptions, improving first-pass yield, reducing manual touchpoints, and shortening cycle times.

GF:Through Genpact’s expanded work with Google Cloud, what are CFOs specifically asking for from hyperscalers right now? Is the conversation more about cost reduction or something else?

Chaki: The CFO conversation with hyperscalers has moved beyond ‘what’s the cheapest cloud?’ or ‘show me another AI demo.’ CFOs want production-ready finance operations that deliver real, measurable business outcomes. That’s what Genpact’s alliance with Google Cloud aims to address. By pairing Google’s AI infrastructure with Genpact’s finance expertise, CFOs can improve forecasting accuracy, strengthen cash flow, and scale AI within their existing cloud environments.

The goal is not just to reduce costs. It’s about boosting process efficiency and accuracy, freeing finance teams from manual work, improving decision-making, and giving CFOs a clearer path from AI investment to strategic value.

GF:Are there any guardrails that must be in place before agentic AI can be trusted within core financial workflows?

Chaki: Think of the guardrails for agentic AI as needing to scale alongside the technology itself. The more finance use cases it touches, the more important it becomes to build controls directly into the workflow. What we’re seeing today is the first wave of “agent-ification.” It operates on a machine-led, human-validated model, combining automation efficiency with expert oversight to ensure quality and compliance. Companies will build tools with that future standard in mind—where the guardrails and technology scale together—will be the ones who truly innovate what finance is capable of.

GF:Are there specific examples you can share of how you see AI augmenting finance teams?

Chaki: We’re already seeing AI reshape how finance teams spend their time. In accounts payable, for example, AI agents are handling invoice extraction, three-way matching, and exception routing. This work used to consume entire teams. In financial planning and analysis, AI is accelerating variance analysis, generating narrative commentary on actuals, and enabling rolling forecasts that would have been extremely time-consuming and practically impractical to run manually. When it comes to record-to-report, it’s compressing close cycles by automating reconciliations and surfacing anomalies before they become audit issues.

GF:Do you expect job cuts?

Chaki: The shift this creates is less about job cuts and more about role evolution. Finance teams won’t shrink overnight, but the composition will change. You’ll see fewer people doing repetitive transactional work and more people in roles that require judgment, such as interpreting AI-generated insights, managing agent workflows, overseeing controls, and partnering with the business on strategic decisions. The finance professional of the future looks more like a combination of business partner and orchestrator than a processor.

Over the next three to five years, as agentic AI matures and enterprise vendors begin offering subscription-based finance capabilities built on entire agentic libraries, the operating model will shift. Finance functions will become leaner, faster, and more insight-driven but the organizations that get there first will be the ones investing now in both technology and the talent to work alongside it.