More than a dozen names are on the ballot, but analysts say the race is between President Lazarus Chakwera and his predecessor Peter Mutharika.

Polls have opened in Malawi with the incumbent president and his predecessor vying for a second chance to govern the largely poor southern African nation, battered by soaring costs and severe fuel shortages, in a closely and fiercely contested election where a run-off is widely expected.

Polls opened at 6:00am (04:00 GMT) on Tuesday with 17 names on the ballot.

Recommended Stories

list of 3 itemsend of list

Analysts say the race is between President Lazarus Chakwera, 70, and his predecessor, law professor Peter Mutharika, 85, both of whom have campaigned on improving the agriculture-dependent economy battered by a series of climate shocks, with inflation topping 27 percent.

Tuesday’s elections mark Malawi’s first national elections since the 2019 presidential vote was nullified and ordered to be redone in 2020 because of widespread irregularities.

However, both of the men have been accused of cronyism, corruption and economic mismanagement during their first presidential terms, leaving voters a choice between “two disappointments”, political commentator Chris Nhlane told the AFP news agency.

Though both drew large crowds to colourful final rallies at the weekend, many younger Malawians were reportedly uninspired.

With about 60 percent of the 7.2 million registered voters aged less than 35, activists have been mobilising to overcome apathy and get young voters to the polls.

“We are frustrated,” said youth activist Charles Chisambo, 34. “If people vote for Mutharika, it is just to have a change,” told AFP.

“We don’t need a leader, we need someone who can fix the economy.”

The cost of living in one of the world’s poorest countries has surged 75 percent in 12 months, according to reports citing the Centre for Social Concern, a nongovernmental organisation.

Two seasons of drought and a devastating cyclone in 2023 have compounded hardships in a country where about 70 percent of the 21 million population lives in poverty, according to the World Bank.

Chakwera, from the Malawi Congress Party that led the nation to independence from Britain in 1964, has pleaded for continuity to “finish what we started”, flaunting several infrastructure projects under way.

Days earlier, he announced a huge drop in the high cost of fertiliser, a major complaint across the largely agricultural country.

Lydia Sibale, 48, a hospital administrator who had been in a petrol queue in Lilongwe for an hour, told AFP she still had confidence in Chakwera. “The only challenge is the economic crisis, which is worldwide,” she said.

Chakwera was elected with about 59 percent of the vote in the 2020 rerun, but, five years later, there is some nostalgia for Mutharika’s “relatively better administration”, said analyst Mavuto Bamusi.

“Chakwera’s incumbency advantage has significantly been messed up by poor economic performance,” he said.

“I want to rescue this country,” Mutharika told a cheering rally of his Democratic Progressive Party in the second city of Blantyre, the heartland of the party that has promised a “return to proven leadership” and economic reform.

“I will vote for APM (Mutharika) because he knows how to manage the economy and has Malawians’ welfare at heart,” 31-year-old student Thula Jere told AFP.

With a winner requiring more than 50 percent of votes, a run-off within 60 days is likely.

New York, USA – Next week, the United States Federal Reserve will hold a two-day policy meeting to decide whether to lower interest rates.

The meeting follows a months-long pause in rates and comes amid heightened pressure on the central bank.

Recommended Stories

list of 4 itemsend of list

US President Donald Trump recently dismissed Federal Reserve Governor Lisa Cook on allegations of mortgage fraud, which she is contesting in court, and has escalated his loud and repeated criticism of Fed Chair Jerome Powell.

The Fed, which emphasises its independence from political influence, will weigh new economic data as it considers its next move. The benchmark interest rate has remained at 4.25 percent – 4.50 percent since December.

So far, the Fed has held rates steady, saying the stance preserves flexibility to respond to economic shocks tied to shifting trade policy. But many economists now believe a rate cut is imminent.

They point to signs of a cooling labour market and tariff-related pressure on inflation as factors that could support lowering rates, not political pressure.

“I think that the Fed has made it pretty clear that they’re going to cut rates in September, and the market certainly expects that,” Daniel Hornung, policy fellow at Stanford Institute of Economic Policy Research and former deputy director of the National Economic Council, told Al Jazeera.

CME FedWatch, which tracks the probability of Fed policy moves, puts the likelihood of a quarter of one percentage point cut at 94.5 percent, echoing research from JPMorgan last month.

“For Fed Chair Jerome Powell, the risk management considerations may go beyond balancing employment and inflation risks, and we now see the path of least resistance is to pull forward the next cut of 25 basis points to the September meeting,” Michael Feroli, chief US economist at JP Morgan, said at the time.

Prices jump

Consumer prices rose 0.4 percent in August from the previous month, the sharpest increase in seven months, according to the Labor Department’s consumer price index (CPI) report released on Thursday.

The gain followed a 0.2 percent rise in July. Economists surveyed by Reuters had forecast a 0.3 percent monthly increase in core CPI.

Energy costs climbed 0.7 percent, fueled by a 1.9 percent jump in gasoline. Airfares climbed 5.9 percent, apparel prices rose 0.5 percent, shelter increased 0.4 percent, grocery prices were up 0.6 percent, and restaurant meals rose 0.3 percent.

Some goods saw particularly steep increases. Coffee prices jumped 3.6 percent on the month as Brazil, the world’s top coffee exporter, redirected shipments away from the US following new tariffs.

The Producer Price Index (PPI), which tracks prices businesses receive for goods and services, showed coffee up nearly 7 percent from July and more than 33 percent over the past year.

There is a comparable phenomenon with beef, for which the US relies heavily on Brazil. CPI data showed a 2.7 percent increase, while the PPI measured a 6 percent monthly rise and a 21 percent yearly increase.

Overall, the PPI slipped 0.1 percent, suggesting some businesses are absorbing tariff costs rather than passing them to consumers. Service prices fell 1.7 percent, driven by a 3.9 percent decline in margins for machinery and vehicle wholesalers, which offset a 0.1 percent increase in goods prices. That came after wholesale inflation was revised higher to 0.7 percent in July, which was well above economists’ forecasts.

Even so, companies are beginning to warn that they cannot continue absorbing higher costs. In recent weeks, Campbell’s Co, which makes Campbell’s Soup and Goldfish crackers, and Procter & Gamble have both said they plan to raise prices on consumer goods in the months ahead as tariff pressures persist.

Labour market tumbles

The US labour market, a key factor in the Federal Reserve’s interest rate decisions, has cooled sharply.

Approximately 263,000 people submitted initial jobless claims last week, the most in four years, Department of Labor data released on Thursday showed.

On Tuesday, the Bureau of Labor Statistics also revised down job gains over the past few months, as well as between April 2024 and March 2025, when the US economy added 911,000 fewer jobs than had been previously reported.

All of that is echoed by poor jobs numbers last week. In August, the economy added only 22,000 jobs, with gains concentrated in healthcare (which added 31,000 jobs) and social assistance (which added 16,000). The unemployment rate climbed to 4.3 percent, the Labor Department reported.

Revisions showed July job growth slightly stronger at 79,000, up from 73,000, while June was cut from a modest gain to a loss of 13,000.

“The recent job numbers were really, especially the revision of the earlier numbers, were really kind of problematic for the economy,” Michael Klein, professor of International Economic Affairs at the Fletcher School at Tufts University, told Al Jazeera.

Job openings and turnover also declined, leaving more unemployed workers than available positions for the first time since April 2021.

A report from Challenger, Gray & Christmas highlighted the strain, noting a 39 percent jump in job cuts between July and August. Private payroll growth slowed as well, according to the ADP National Employment Report, which showed just 54,000 jobs added, down from 106,000 the prior month.

Competing forces

Typically, high inflation prompts higher interest rates, which discourage borrowing and spending and help rein in prices.

“The Fed is in a very difficult position right now because there is both a weakening labour market and evidence of higher inflation. Typically, if the Fed is facing a weaker labour market, it would want to lower interest rates. And if it’s facing higher inflation, it would want to raise interest rates. But we’re in a situation now where there are countervailing forces,” Klein said.

The labour market is already weighing on consumer spending. Rising layoffs and slower hiring have made shoppers cautious, and the latest consumer confidence index shows plans to buy big-ticket and discretionary items are slipping.

With Trump’s shifting tariffs and hardline immigration policies, businesses are stuck in a “wait-and-see” mode, increasing uncertainty.

“We are seeing immigration and tariff policies that have the simultaneous effect of raising prices and slowing growth in the labour market,” Hornung said.

The request comes after a federal court earlier this week blocked Lisa Cook’s firing while her lawsuit challenging her dismissal moves forward.

The administration of United States President Donald Trump has asked an appeals court to remove Lisa Cook from the Federal Reserve’s board of governors by Monday, before the central bank’s next vote on interest rates.

The request on Thursday represents an extraordinary effort by the White House to shape the board before the Fed’s interest rate-setting committee meets next week on Tuesday and Wednesday.

Recommended Stories

list of 4 itemsend of list

At the same time, Senate Republicans are pushing to confirm Stephen Miran, Trump’s nominee to an open spot on the Fed’s board, which could happen as soon as Monday.

In a court filing on Thursday, the Department of Justice asked the US Court of Appeals for the DC Circuit to pause US District Judge Jia Cobb’s Tuesday ruling temporarily blocking Cook’s removal, pending the administration’s appeal.

Trump moved to fire Cook in late August. Cook, who denies any wrongdoing, filed a lawsuit saying Trump’s claim that she engaged in mortgage fraud before she joined the central bank did not give him legal authority to remove her, and was a pretext to fire her for her monetary policy stance.

Cobb’s ruling prevents the Fed from following through on Cook’s firing while her lawsuit moves forward.

In their emergency appeal, Trump’s lawyers argued that even if the conduct occurred before her time as governor, her alleged action “indisputably calls into question Cook’s trustworthiness and whether she can be a responsible steward of the interest rates and economy”.

The administration asked an appeals court to issue an emergency decision reversing the lower court by Monday. If their appeal is successful, Cook would be removed from the Fed’s board until her case is ultimately resolved in the courts, and she would miss next week’s meeting.

If the appeals court rules in Cook’s favour, the administration could seek an emergency ruling from the Supreme Court.

The case, which will likely end up before the US Supreme Court, has ramifications for the Fed’s ability to set interest rates without regard to politicians’ wishes, widely seen as critical to any central bank’s ability to keep inflation under control.

The Supreme Court and lower appeals courts, including the DC Circuit, have temporarily lifted several other rulings that briefly blocked Trump from firing officials at agencies that have historically been independent from the White House.

On Wednesday, however, the DC Circuit blocked Trump from firing US Copyright Office director Shira Perlmutter while she appeals a lower court’s refusal to reinstate her to the post.

Trump has demanded that the Fed cut rates immediately and aggressively, repeatedly berating Fed Chair Jerome Powell for his stewardship over monetary policy. Cook has voted with the Fed’s majority on every rate decision since she started in 2022, including on both rate hikes and rate cuts.

Fed’s independence

The law that created the Fed says governors may be removed only “for cause”, but does not define the term nor establish procedures for removal. No president has ever removed a Fed governor, and the law has never been tested in court.

Cobb on Tuesday said the public’s interest in the Fed’s independence from political coercion weighed in favour of keeping Cook at the Fed while the case continues.

She said that the best reading of the law is that a Fed governor may only be removed for misconduct while in office. The mortgage fraud claims against Cook all relate to actions she took prior to her US Senate confirmation in 2022.

Trump and William Pulte, the Federal Housing Finance Agency director appointed by the president, say Cook inaccurately described three separate properties on mortgage applications, which could have allowed her to obtain lower interest rates and tax credits.

The Justice Department has also launched a criminal mortgage fraud probe into Cook and has issued grand jury subpoenas out of both Georgia and Michigan, according to documents seen by Reuters and a source familiar with the matter.

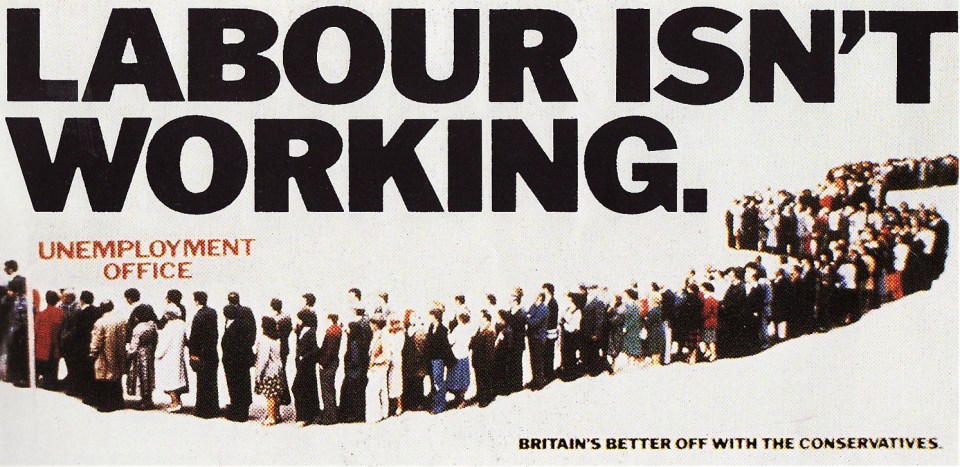

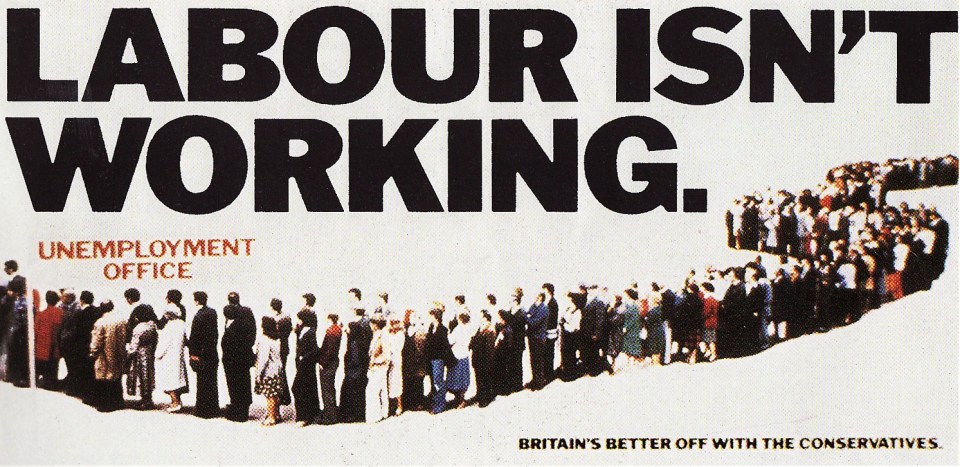

IT was perhaps the most famous poster in election history. “Labour Isn’t Working,” proclaimed its simple slogan above a photo of a long, snaking queue outside an unemployment office.

The image helped Margaret Thatcher’s Tories to win a decisive victory in 1979.

4

The iconic ‘Labour Isn’t Working’ poster helped MargaretThatcher secure a historic election victory in 1979 – and it again rings true todayCredit: handout

4

Sir Keir Starmer, seems to be trapped in a kind of doom loop created by his party’s epic mismanagement of the economyCredit: Getty

That poster could be revived today as the beleaguered Labour Prime Minister, Sir Keir Starmer, seems to be trapped in a kind of doom loop created by his party’s epic mismanagement of the economy.

Growth is anaemic, the tax burden colossal. Just like in the late 70s, Britain is gripped by rising debt, inflation and unemployment, as well as increasing militancy in the public sector workforce, where recent generous pay settlements have fuelled a mood of greedy irresponsibility.

Only yesterday the distinguished business leader Lord Stuart Rose, the former head of Marks & Spencer, warned that Starmer and his bumbling Chancellor Rachel Reeves had dragged Britain “to the edge of crisis.”

In a bleak analysis, Lord Rose argued that because “there is no growth in the economy,” neither wealth nor jobs are being created.

The parallel with the 1970s is at its most stark in the hostility to hard work. Fifty years ago Britain became known as “the sick man of Europe” because of its addiction to strikes, with an astonishing 29million working days lost in 1979 alone.

Modern Britain has yet to plumb those depths, though the pig-headed unions are trying to go in that direction, as shown by the current miserable strike on the London Underground, which has paralysed the capital this week.

What makes this strike so ridiculous is that the Tube drivers are extremely well-paid, typically earning around £72,000-a-year, and enjoy excellent job security, pensions, hours and holidays. Yet they act like they are oppressed members of the proletariat.

London Tube Strikes Cause Travel Chaos: Everything You Need to Know

These grotesque demands are part of a wider culture of self-serving entitlement that is destroying Britain’s work ethic, reducing productivity and weakening the dynamism of business.

That destructive spirit can be seen in the recent surge of sick leave in the national workforce, a phenomenon caused not by harsher conditions but by more indulgent management, and the fashion for treating normal emotions as mental health problems.

Mental-health crisis

Yesterday a study by the Chartered Institute of Personnel and Development revealed that employees are now taking an average of nearly two weeks off sick every year.

Only two years ago absenteeism stood at an average of 7.8 days a year. Now that figure has risen to 9.4 days a year, with the mental-health crisis the key driving force.

All too predictably, the record of the public sector is much worse than the private sector. That is not because work on the state payroll is tougher. Just the opposite is true.

The heavily unionised culture of public employment, with its emphasis on workplace rights and victimhood, promotes weak management and a lack of accountability.

The rise in absenteeism is mirrored by the growth in welfare dependency where ever increasing numbers of people think that the state owes them a living. Social security is no longer just a temporary safety net but has become a comfortable lifestyle choice.

There are now 6.5million adults of working age who are claiming out-of-work benefits, while some forms of incapacity payments have become a sort of subsidy for early retirement.

As Lord Rose puts it, “We have arrived in a situation in Britain today where there is effectively no obligation to work, absolutely none.”

In a recent newspaper interview, one claimant called Clare Russell gave an insight into the mentality of some of the worst freeloaders.

Labour likes to boast that it is the party of ‘working people’. Now it should live up to that description.

Ten years ago she gave up work at the age of 46 and since then has lived off the disability benefits she receives for a bad back, as well as a substantial rental income from some property, plus a carer’s allowance to look after her mother who lives 30 miles away.

In her sickening interview, she said that she has “a lovely life, thanks to the great British taxpayer.”

Just to heighten the outrage she added, “when I am at the gym, I watch young people scuttle past the window on the treadmill of work and I must admit to feeling smug.”

The disappearance of the work ethic is neither morally defensible nor financially affordable.

The disability benefits bill is expected to reach £100billion by 2030 while the overall cost of welfare is forecast to go up from £210billion a decade ago to £380billion by 2030.

The welfare leviathan is tracking us ever deeper into debt and towards national bankruptcy.

In the depths of its current political crisis, France — which has an even more lavish benefits system than Britain — shows what can happen when the cost of welfare spirals out of control.

We were the nation of the industrial revolution. We must revive that kind of drive and determination. This should be an absolute priority for the new Labour cabinet.

Reform of welfare and the workplace is not an option, it is a necessity.

Labour likes to boast that it is the party of “working people”. Now it should live up to that description.

4

London is currently paralysed by Tube strikes, despite drivers earning £72,000 and enjoying top job perksCredit: Alamy

4

Business leader Lord Stuart Rose, the former head of Marks & Spencer, warned that Starmer and bumbling Chancellor Rachel Reeves had dragged Britain ‘to the edge of crisis’Credit: PA

Pret will trial meal deals in October, November and DecemberCredit: Alamy

Pret plans to trial the meal deal format in the final three months of the year.

Boss Pano Christou said the chain’s focus is on “offering great value for money” as part of its medium-term strategy to grow and return to sustainable profits.

Details on pricing and locations for the trial have yet to be revealed.

Pret’s latest accounts showed a pre-tax loss of £525.2 million for the year to January 2 – largely due to a £552.9 million write-down after a reassessment by owner JAB, which bought the chain in 2018.

This followed a £61.7 million loss the year before.

Despite the losses, Pret said its earnings before adjustments rose 36 per cent to £98 million for the year.

Meanwhile, total revenue dipped 4.2 per cent to £868.4 million compared to the previous year.

Like-for-like sales grew by 2.8 per cent, helped by an 11 per cent expansion to 717 shops as the business continued to grow internationally.

Pret said it is keen to expand further in the US, especially around city centres and travel hubs.

I went to the UK’s best sandwich shop that’s gone viral on TikTok due to amazing family history and huge portions

Christou, Pret’s CEO, said: “2024 was another year of growth for Pret, where we took disciplined decisions to protect sales, despite intense strains on the hospitality industry.

“Going forward our priority will be to drive transactions and sustainable growth by offering great value for money for Pret customers.

“Our focus will be on growing Pret’s market share in the UK and internationally, prioritising city centres and travel hubs, backed by the experience and expertise of additional world-class board members and a strengthened management team.”

Pret opened its first shop in London in 1986 and now employs 12,500 staff across over 700 locations in 21 countries.

The new purple tubs have approximately 57 chocolates – down from 63.

A Nestlé spokesperson cited the cost of manufacturing, “ingredients and transport” for the cut.

Deal expert Tom Church previously told The Sun that the best way to beat size reductions was to look for cut-price deals, such as multi-buy offers in the supermarkets or Nectar and Clubcard prices.

Shrinking chocolate

All major manufacturers are shrinking the size of their treats to help combat rising material costs.

We all love a bit of chocolate from now and then, but you don’t have to break the bank buying your favourite bar.

Consumer reporter Sam Walker reveals how to cut costs…

Go own brand – if you’re not too fussed about flavour and just want to supplant your chocolate cravings, you’ll save by going for the supermarket’s own brand bars.

Shop around – if you’ve spotted your favourite variety at the supermarket, make sure you check if it’s cheaper elsewhere.

Websites like Trolley.co.uk let you compare prices on products across all the major chains to see if you’re getting the best deal.

Look out for yellow stickers – supermarket staff put yellow, and sometimes orange and red, stickers on to products to show they’ve been reduced.

They usually do this if the product is coming to the end of its best-before date or the packaging is slightly damaged.

Buy bigger bars – most of the time, but not always, chocolate is cheaper per 100g the larger the bar.

So if you’ve got the appetite, and you were going to buy a hefty amount of chocolate anyway, you might as well go bigger.

KINDER has crunched multipacks of its iconic Bueno bars from eight sticks to six in the latest blatant example of shrinkflation ripping off hard-up Brits.

President Donald Trump said US workers are already benefitting from his economic policies.

“The average American worker has already seen a $500 wage increase this year,” Trump said during an August 26 Cabinet meeting.

Trump’s White House cherry-picked data that favours a higher earnings gain. Experts prefer a different measure, based on a larger sample size, that shows a smaller increase.

How the White House calculated a $500 pay bump

When we asked the White House press office for Trump’s data source, a spokesperson pointed us to Bureau of Labor Statistics figures for median usual weekly earnings of full-time wage and salary workers, seasonally adjusted.

This data shows that median weekly earnings rose from $1,185 in the fourth quarter of 2024 to $1,206 in the second quarter of 2025, which closely aligns with Trump’s second term in office.

Because those figures represent weekly earnings, we multiplied them by 26 to see how much a typical worker gained during the half-year period. Multiplying by 26 weeks produces a cumulative $546 rise in wages. This measure does not include part-time workers, who account for about a quarter of the workforce, or account for inflation.

Experts consider other measures more reliable

Economists said the White House’s chosen dataset isn’t as reliable as a different set – and the more reliable study shows a smaller wage increase.

The other dataset – average weekly earnings of all private-sector employees – is produced monthly by the Bureau of Labor Statistics.

Over the first six months of 2025, this statistic found a cumulative pay increase of about $121. That’s about one-quarter of what Trump said.

Several economists told us this is the preferred statistic for measuring wages, because it’s based on the Current Employment Statistics programme, which surveys 121,000 businesses and government agencies, collectively representing approximately 631,000 worksites. By comparison, the Current Population Survey, from which the White House’s data is drawn, samples 60,000 eligible households.

“I always trust the payroll series more,” said Douglas Holtz-Eakin, president of the centre-right American Action Forum.

Dean Baker, cofounder of the liberal Center for Economic and Policy Research, agrees, saying the data in the smaller household survey “is highly erratic”.

In addition, according to this dataset, the wage rise during President Joe Biden’s last two quarters was $884. This undercuts the notion that Trump’s gains have been unusually high.

Factoring in inflation

Because both of these measures fail to factor in inflation, they overestimate workers’ gains.

Another statistic, median usual weekly inflation-adjusted earnings for full-time wage and salary workers, 16 years and over, also from the US Bureau of Labor Statistics, is produced quarterly using the smaller sample-size household survey and takes inflation into account.

By this metric, workers’ pay increased by $1 per week between the final quarter of 2024 and the second quarter of 2025.

Multiplied by 26 weeks, this adds up to a $26 pay rise after inflation.

Our ruling

Trump said: “The average American worker has already seen a $500 wage increase this year.”

The White House cited wage statistics that show median wages for full-time workers rose by a cumulative $546 during the first two quarters of 2025.

A different set of statistics – one that economists consider more accurate because it’s drawn from a much larger sample that includes full- and part-time workers, and with less volatility – shows a much smaller rise in the average US worker’s pay over that period, about $121 over six months.

When inflation is factored in, full-time workers’ take-home pay rose by even less – by about $26 during the first six months of 2025.

The statement is partially accurate but leaves out important details. We rate it Half True.

HOUSEHOLDS across the country are being warned to brace for a financial squeeze as the cost of government borrowing skyrockets to levels not seen since 1998.

This now directly threatens to push up mortgage rates and could usher in a new wave of tax hikes.

1

The rise in government borrowing costs is putting serious pressure on household budgets in two key waysCredit: Getty

The pound has tumbled in response to the growing unease, highlighting investor concern over the UK’s economic stability.

At the heart of the issue are government bonds, known as “gilts,” which the government issues to borrow money.

These bonds offer investors a return, referred to as the “yield.”

In recent weeks, gilt yields have been rising rapidly, making it more expensive for the government to borrow.

This morning, yields soared further, with 30-year gilts reaching 5.72% – the highest level in nearly 30 years – while 10-year gilts climbed to 4.85%.

This spike signals that investors are nervous.

They are demanding a higher return to lend to the UK, worried about stubborn inflation and a gaping £51billion hole in the nation’s finances.

The rise in government borrowing costs is putting serious pressure on household budgets in two key ways

Firstly, it’s driving up mortgage rates.

The link between government gilt yields and mortgage rates is direct and unavoidable.

Lenders use “swap rates,” which closely track gilt yields, to set the prices of fixed-rate mortgage deals.

As these rates climb, fixed mortgages become more expensive.

Since August 1, two-year swaps have risen from 3.56% to 3.74%, while five-year swaps have gone from 3.63% to 3.83%.

Major lenders like Barclays have already started increasing rates, and even a small rise can add significantly to monthly payments on a typical £200,000 mortgage.

With swap rates continuing to rise in recent weeks, experts warn that mortgage rates are likely to increase further.

Separately, Chancellor Rachel Reeves faces a difficult challenge in her Autumn Budget, scheduled for November.

Higher borrowing costs are eating into public funds, and many economists believe tax increases will be necessary to fill the financial gap.

Although the government has promised not to raise income tax, national insurance, or VAT for “working people,” other tax measures are reportedly being considered.

One proposal is applying National Insurance to rental income, which critics fear could result in landlords passing on the cost to tenants through higher rents.

Another idea being debated is replacing stamp duty with an annual property tax, which could affect homeowners.

There are also rumours of reducing pension tax relief or cutting the tax-free lump sum, moves that could generate billions but might hurt savers.

Plus, there’s speculation about lowering the VAT threshold, which would bring more small businesses into the tax system.

This could increase their costs and potentially lead to higher prices for consumers.

Reeves is expected to make economic growth the centrepiece of her next Budget, warning that Britain’s economy is “stuck” and in need of bold solutions.

What can you do about it?

None of the proposed changes have been confirmed yet, and the government hasn’t ruled them out either.

However, any new measures won’t take effect until after the Budget in November.

It’s important not to make rash decisions based on speculation.

If changes are announced, you’ll have time to act and protect your finances before they come into effect.

For instance, if stamp duty is replaced by an annual property tax from a certain date, you could move house before the deadline to avoid the extra cost.

Similarly, if the government introduces capital gains tax on high-value properties, you might consider downsizing to a smaller home before the change is implemented.

Rob Morgan, chief analyst at Charles Stanley, said: “Taking pre-emptive action can outright backfire.

“Last year some people were concerned about restrictions around taking tax free cash from pension and took withdrawals they wouldn’t have otherwise made.

“This removed the money from a tax-efficient environment and potentially stored up tax issues that will come back to haunt them.

“Instead, it’s best to wait to see what happens, consider the consequences, and take advice as required before acting.”

Most of the proposed measures are likely to affect only the very wealthy, so you may not be impacted at all.

If you’re concerned, there are steps you can take to prepare and safeguard your finances.

Check your financial health

If you are worried about your finances then you should speak to a financial adviser.

They will be able to offer you advice about your situation and explain if any of the measures will affect you.

You can find one using unbiased.co.uk – but remember, you will pay a fee.

It’s good practice to sit down and take stock of your finances every six months and work out a plan.

Work out all your bills and outgoings and what income you have and factor in any changes, such as bills going up or new income streams.

Think about what you need to do to make the most of your money. For example, do you need to prioritise paying off debts or saving for a house deposit.

If your mortgage deal is coming to an end soon, act now.

Locking in a fixed rate could shield you from rising rates and market uncertainty.

Aaron Strutt, of mortgage broker Trinity Financial, said “For the moment there have not been significant price hikes but it’s probably worth locking in a mortgage rate if you are buying somewhere or due to remortgage, to try and keep away from any market turbulence.”

If you are coming to the end of a fixed deal, most lenders let you lock in a new rate up to six months beforehand, which can be worth doing.

If rates fall after you agree a new deal, some lenders will let you sign a new one at a lower rate.

How to get the best deal on your mortgage

IF you’re looking for a traditional type of mortgage, getting the best rates depends entirely on what’s available at any given time.

If you’re remortgaging and your loan-to-value ratio (LTV) has changed, you’ll get access to better rates than before.

Your LTV will go down if your outstanding mortgage is lower and/or your home’s value is higher.

A change to your credit score or a better salary could also help you access better rates.

And if you’re nearing the end of a fixed deal soon it’s worth looking for new deals now.

You can lock in current deals sometimes up to six months before your current deal ends.

Leaving a fixed deal early will usually come with an early exit fee, so you want to avoid this extra cost.

But depending on the cost and how much you could save by switching versus sticking, it could be worth paying to leave the deal – but compare the costs first.

You can also go to a mortgage broker who can compare a much larger range of deals for you.

Some will charge an extra fee but there are plenty who give advice for free and get paid only on commission from the lender.

You’ll also need to factor in fees for the mortgage, though some have no fees at all.

You can add the fee – sometimes more than £1,000 – to the cost of the mortgage, but be aware that means you’ll pay interest on it and so will cost more in the long term.

The average bank customer has around £10,000 in savings, according to Raisin.

If that £10,000 is kept in an easy access account earning 1.5% interest, it would generate just £150 in interest each year.

But switching to Cahoot’s 5% easy access account would boost that to £500, earning you an extra £350.

If your savings account pays less than the current inflation rate of 3.8%, it’s time to look for a better deal.

How can I find the best savings rates?

WITH your current savings rates in mind, don’t waste time looking at individual banking sites to compare rates – it’ll take you an eternity.

Research price comparison websites such as Compare the Market, Go.Compare and MoneySupermarket.

These will help you save you time and show you the best rates available.

They also let you tailor your searches to an account type that suits you.

As a benchmark, you’ll want to consider any account that currently pays more interest than the current level of inflation – 3.4%.

It’s always wise to have some money stashed inside an easy-access savings account to ensure you have quick access to cash to deal with any emergencies like a boiler repair, for example.

If you’re saving for a long-term goal, then consider locking some of your savings inside a fixed bond, as these usually come with the highest savings rates.

WASHINGTON — President Trump’s attempt to fire a member of the Federal Reserve’s governing board has raised alarms among economists and legal experts who see it as the biggest threat to the central bank’s independence in decades.

The consequences could affect most Americans’ everyday lives: Economists worry that if Trump gets what he wants — a loyal Fed that sharply cuts short-term interest rates — the result would likely be higher inflation and, over time, higher borrowing costs for things like mortgages, car loans and business loans.

Trump on Monday sought to fire Lisa Cook, the first Black woman appointed to the Fed’s seven-member Board of Governors. It was the first time in the Fed’s 112-year history that a president has tried to fire a governor.

Fed independence ‘hangs by a thread’

Trump and members of his administration have made no secret about their desire to exert more control over the Fed. Trump has repeatedly demanded that the central bank cut its key rate to as low as 1.3%, from its current level of 4.3%.

Before trying to fire Cook, Trump repeatedly attacked the Fed’s chair, Jerome Powell, for not cutting the short-term interest rate and threatened to fire him as well.

“We’ll have a majority very shortly, so that’ll be good,” Trump said Tuesday, a reference to the fact that if he is able to replace Cook, his appointees will control the Fed’s board by a 4-3 vote.

“The particular case of Governor Cook is not as important as what this latest move shows about the escalation in the assaults on the Fed,” said Jon Faust, an economist at Johns Hopkins and former advisor to Powell. “In my view, Fed independence really now hangs by a thread.”

Some economists do think the Fed should cut more quickly, though virtually none agrees with Trump that it should do so by 3 percentage points. Powell has signaled the Fed is likely to cut by a quarter point in September.

Why economists prefer independent central banks

The Fed wields extensive power over the U.S. economy. By cutting the short-term interest rate it controls — which it typically does when the economy falters — the Fed can make borrowing cheaper and encourage more spending, growth and hiring. When it raises the rate to combat the higher prices that come with inflation, it can weaken the economy and cause job losses.

Most economists have long preferred independent central banks because they can take unpopular steps that elected officials are more likely to avoid. Economic research has shown that nations with independent central banks typically have lower inflation over time.

Elected officials like Trump, however, have much greater incentives to push for lower interest rates, which make it easier for Americans to buy homes and cars and would boost the economy in the short run.

A political Fed could boost inflation

Douglas Elmendorf, an economist at Harvard and former director of the nonpartisan Congressional Budget Office, said that Trump’s demand for the Fed to cut its key rate by 3 percentage points would overstimulate the economy, lifting consumer demand above what the economy can produce and boosting inflation — similar to what happened during the COVID-19 pandemic emergency.

“If the Federal Reserve falls under control of the president, then we’ll end up with higher inflation in this country probably for years to come,” Elmendorf said.

And while the Fed controls a short-term rate, financial markets determine longer-term borrowing costs for mortgages and other loans. And if investors worry that inflation will stay high, they will demand higher yields on government bonds, pushing up borrowing costs across the economy.

In Turkey, for example, President Recep Tayyip Erdogan forced the central bank to keep interest rates low in the early 2020s, even as inflation spiked to 85%. In 2023, Erdogan allowed the central bank more independence, which has helped bring down inflation, but short-term interest rates rose to 50% to fight inflation, and are still 46%.

Other U.S. presidents have badgered the Fed. President Johnson harassed then-Fed Chair William McChesney Martin in the mid-1960s to keep rates low as Johnson ramped up government spending on the Vietnam War and antipoverty programs. And President Nixon pressured then-Chair Arthur Burns to avoid rate hikes in the run-up to the 1972 election. Both episodes are widely blamed for leading to the stubbornly high inflation of the 1960s and ‘70s.

Trump has also argued that the Fed should lower its rate to make it easier for the federal government to finance its tremendous $37-trillion debt load. Yet that threatens to distract the Fed from its congressional mandates of keeping inflation and unemployment low.

Independence vs. accountability

Presidents do have some influence over the Fed through their ability to appoint members of the board, subject to Senate approval. But the Fed was created to be insulated from short-term political pressures. Fed governors are appointed to staggered, 14-year terms to ensure that no single president can appoint too many.

Jane Manners, a law professor at Fordham University, said there is a reason that Congress decided to create independent agencies like the Fed: Lawmakers preferred “decisions that are made from a kind of objective, neutral vantage point grounded in expertise rather than decisions are that are wholly subject to political pressure.”

Yet some Trump administration officials say they want more democratic accountability at the Fed.

In an interview with USA Today, Vice President JD Vance said, “What people who are saying the president has no authority here are effectively saying is that seven economists and lawyers should be able to make an incredibly critical decision for the American people with no democratic input.”

Stephen Miran, a top White House economic advisor, wrote a paper last year advocating for a restructuring of the Fed, including making it much easier for a president to fire governors.

The “overall goal of this design is delivering the economic benefits” of an independent central bank, Miran wrote, “while maintaining a level of accountability that a democratic society must demand.” Trump has nominated Miran to the Fed’s board to replace Adriana Kugler, who stepped down unexpectedly Aug. 1.

There could be more turmoil ahead

Trump said he wants to oust Cook from the Board of Governors because of allegations raised by one of his advisors that she has committed mortgage fraud.

Cook has argued in a lawsuit seeking to block her firing that the claims are a pretext for Trump’s desire to assert more control over the Fed. A court may decide this week whether to temporarily block Cook’s firing while the case makes its way through the legal process.

Cook is accused of claiming two homes as primary residences in July 2021, before she joined the board, which could have led to a lower mortgage rate than if one had been classified as a second home or an investment property. She has suggested in her lawsuit that it may have been a clerical error but hasn’t directly responded to the accusations.

Trump also has personally insulted Powell for months, but his administration now appears much more focused on the Fed’s broader structure.

The Fed makes its interest rate decisions through a committee that consists of the seven governors, including Powell, as well as the 12 presidents of regional Fed banks in cities such as New York, Kansas City and Atlanta. Five of those presidents vote on rates at each meeting. The New York Fed president has a permanent vote, while four others vote on a rotating basis.

While the reserve banks’ boards choose their presidents, the Fed board in Washington can vote to reject them. All 12 presidents will need to be reappointed and approved by the board in February, which could become more contentious if the board votes down one or more of the 12 presidents.

Reappointing the reserve bank presidents and upending that structure would be “the nuclear scenario,” said Adam Posen, president of the Peterson Institute for International Economics.

That, he said, “would be the signal that things are truly going off the rails.”

IF you’re wondering where your money’s going each month, it might not be big bills or bad luck to blame but small, repeated mistakes that add up fast.

From letting your savings sit in low-interest accounts, to underestimating the real cost of long mortgage terms, financial experts warn that common habits could be quietly emptying your bank accounts.

2

Small, repeated mistakes could be the reason your bank balance is dwindlingCredit: getty

2

Money experts revealed the biggest habits that are keeping people poorCredit: Getty

We asked money experts and behavioural scientists to reveal the biggest habits that are holding people back.

1. Not knowing what’s coming in and going out

It’s hard to feel in control of your money when you don’t know where it’s actually going.

Many people assume they have a rough idea, but the reality is that forgotten subscriptions, auto-renewing services and small daily purchases quickly add up.

Without visibility, your budget can slowly unravel, and by the time you realise, you’ve slipped into the red.

Vix Leyton, consumer expert at Thinkmoney, says the fix starts with routine: “Take time to know what your outgoings are and what is coming in.

“Some apps, like Thinkmoney, offer a snapshot of what you’re spending, and can even ringfence bill money for you so you don’t accidentally end up facing penalties and late fees.”

Even a five-minute weekly check-in can help avoid nasty surprises and highlight where cutbacks are needed.

2. Living without a savings buffer

It’s hard to save money – but not having a buffer can leave you exposed to high credit when you need cash quickly.

Whether it’s a broken boiler, a car that won’t start or a sudden cut in hours at work, not having a cushion means falling back on credit cards or payday loans just to stay afloat.

The result is a constant feeling of stress, and a budget that can be thrown off by the smallest shock.

Thomas Mathar, behavioural researcher and host of The Money:Mindshift Podcast, says a little slack goes a long way.

He said: “Even a modest buffer, like one month’s rent, can give you the breathing space to make better decisions and avoid high-cost debt.

“It’s not just about the numbers, it’s about having mental and financial slack when life throws you a curveball.”

3. Letting debt pile up month after month

More and more people have credit card debt, which means it can be easy to think it’s business as usual, especially when the minimum payments are low.

But ultimately, you’re paying interest to the bank instead of putting that money toward your own goals. Over time, that can add up to hundreds or even thousands of pounds in lost savings.

“Too many people accept credit card debt as a normal state of affairs. It’s not,” says Mathar.

I’ve made over £56k with a side hustle anyone can do – skint people must stop being scared and should try something new

“Paying down high-interest debt quickly is one of the most powerful things you can do for your long-term well being. It’s buying yourself back freedom, and peace of mind.”

If you’re juggling multiple debts, focus on the most expensive ones first and look into 0% balance transfer options if your credit score allows.

4. Having psychological armour to support you

In the age of side hustles and flashy online success stories, it’s tempting to ditch steady work for riskier pursuits.

But without a reliable income it’s hard to build long-term security.

Inconsistent earnings often mean falling behind on bills, using credit to bridge the gap, and struggling to plan ahead.

Mathar warns that it’s important to have some sort of regular income, even if you’re pursuing other hustles on the side.

He says: “A steady income isn’t just about covering bills, it’s psychological armour.

“When you’re living month-to-month or under-earning compared to your potential, the stress compounds.

“You don’t need to chase big money, but you do need income that’s ‘good enough’ to support a resilient, happy life.”

5. Leaving savings in a dead-end account

You might feel good about putting money aside, but if it’s sitting in an easy-access account earning barely any interest, your savings are losing value in real terms.

With inflation still high, the cost of leaving cash in low-yield accounts is higher than many realise.

Adam said: “The likes of HSBC, Lloyds Bank, Santander, NatWest and Barclays all have easy access accounts paying around 1.1 to 1.2 per cent interest, far below the typical returns savers could expect, which is currently 3.51 per cent.”

The top performing options can pay even more, and shopping around and switching accounts only takes a few minutes online.

How to effectively manage your money

Kara Gammell, finance expert at MoneySuperMarket, gives tips on how to get a handle on your finances so you have more left for saving,

If you’re struggling to get a grip on your finances, the way to start is to do a proper inventory.

Try Emma, the money management app, which uses open banking to combine information from all your bank accounts, savings accounts and credit cards, plus investments. The app then highlights any wasteful subscriptions and costly debt and helps streamline your savings.

What’s more, it analyses your personal finances and recommends ways to conserve money so that you can get on track financially more easily than ever.

If you want to have a deep dive into your spending habits, go through your bank statement at the end of each month and give every purchase a rating of one, two or three.

Mark with a ‘one’ any purchases that didn’t make you feel good; give a ‘two’ rating to things that felt ‘sort of good but indifferent’; and mark with ‘three’ any purchases that you would make all over again in a heartbeat.

You’ll be surprised by what you learn.

Monitor your credit report

From overdrafts to loans, credit cards, mobile phones and mortgages, it can be hard to keep track of your finances, and it can be all too simple to find yourself in the dark about how much debt you have in total.

But this information forms your credit score, which is used by lenders to determine whether you’ll be offered competitive rates and offers for financial products, or even whether you will even be accepted when you make an application.

I’m automatically notified when my credit report is updated monthly, which can be a huge help in avoiding any financial problems from spiralling and means I always know what my overall financial situation is.

The tool also suggests ways to improve your credit score, so you’re more likely to be offered competitive interest rates, which helps you save money in the long run.

6. Not making the most of your ISA allowance

More savers than ever are being hit with tax bills they could have avoided.

Frozen tax thresholds mean that even modest savers can end up over the personal savings allowance, paying tax on any interest they earn.

That means, if you’re not using your ISA allowance, you’re potentially giving money away for free.

French explains: “Saving and investing are some of the best ways to build wealth over time.

“But it’s important that savers are aware of their tax liability on any profits they make – which can add up over the course of a few years.

Plenty of savers can avoid this tax bill by making use their yearly ISA allowances.

You can save or invest up to £20,000 a year tax-free, and every pound sheltered from tax is a pound that keeps working for you.

7. Only saving for retirement, and nothing else

Putting money into a pension is smart, but it shouldn’t be your only savings plan.

Many people now take career breaks, retrain, care for relatives or start businesses, and those transitions need funding too.

Mathar says ignoring this reality can leave people exposed.

“We don’t live three-stage lives anymore – education, work, retirement… A ‘transition fund’ – even just a few months’ salary – makes those big life pivots possible without financial panic.”

8. Being too harsh on yourself when things go wrong

Money mistakes happen. But too often, people fall into a cycle of guilt and avoidance, especially if they’re already struggling.

That mindset can stop you from facing your finances or reaching out for help, which only makes things worse in the long run.

Mathar believes the solution starts with self-empathy. “Here’s the truth: we’re all a bit messed up when it comes to money.

Our brains are wired for short-term wins, not long-term planning.

The goal isn’t to be perfect with money; it’s to build enough slack, mental and financial, so that one mistake or setback doesn’t knock you flat.”

9. Not overpaying your mortgage when you could

With mortgage rates still high and household budgets under pressure, many borrowers are choosing longer terms to keep monthly payments manageable.

But unless you’re also making overpayments, that strategy can come at a serious long-term cost.

French says small changes now can lead to huge savings later: “Overpaying by £200 per month on that same £250,000 40-year mortgage could shave almost 13 years off the mortgage term, saving them around £123,000 in interest payments.

“This is all without being tied to having to consistently make higher payments every single month – boosting the flexibility of their budget and their financial resilience.”

Most lenders allow up to 10 per cent overpayment each year.

Even £50 a month can help you become mortgage-free sooner and pay far less in interest overall.

Top tips for becoming an ISA millionaire

SAVING into a stocks and shares ISA can help you build wealth faster over the long term than cash savings. Dan Coatsworth, investment analyst at savings platform AJ Bell, gives his advice…

Start as early as you can

Time in the market is important, not just so you can ride the market ups and downs but also to let your wealth build up.

Not everyone can afford to invest the full £20,000 ISA allowance each year, particularly younger people who might be on a lower salary.

The trick is to start as early as possible with what you can afford to invest. Increase your contributions as you get older, such as when you get a pay rise.

Maximise your contributions

Try to invest as much as you can each month once you’re sure all the essentials are covered.

Create a budget so you can pay bills in full and clear any expensive debt, such as personal loans or credit cards.

The remaining money can be used to fund your lifestyle and to top up your ISA.

Be consistent with contributions

Feeding your account on a regular basis means you get into the habit of squirrelling money away for your future.

After a while you get accustomed to that money going into your ISA that you may not even think about alternative uses for it, such as going shopping or down the pub with your friends.

Keep an eye on costs and charges

Costs can add up over time and eat into your returns. Try not to fiddle too much with your portfolio as trading in and out of investments incurs transaction charges.

It is important to be patient with investing, especially for someone hoping to be an ISA millionaire as the journey to build up this wealth could last for decades.

Having a diversified portfolio is good practice for any investor and essentially means keeping different types of investments to help balance out the risk.

Then if something goes wrong with one of your investments, you’ve got the rest to hopefully act as a cushion to minimise the pain.

Diversification can involve investing in different industry sectors, geographies and asset types. For example, a diversified portfolio might have exposure to shares, funds and bonds from around the world.

Companies and funds often pay dividends every three to six months.

Think of these as rewards for taking the risk of owning their shares or fund units. While it can be tempting to pocket that income stream to spend on yourself, history suggests one of the biggest contributors to investment returns is reinvesting dividends back into your account to grow wealth faster.

Aug. 29 (UPI) — Inflation rose in July, according to the Personal Income and Outlays report from the Bureau of Economic Analysis, the Fed’s preferred measure.

Core inflation, which excludes food and energy costs, was at a 2.9% seasonally adjusted annual rate, according to the personal consumption expenditures price index. That showed a rise of 0.1% from June and the highest annual rate since February.

The core PCE index increased 0.3% monthly, which is in line with expectations, CNBC reported.

Personal outlays, which is the sum of PCE, personal interest payments, and personal current transfer payments, increased $110.9 billion in July. Personal saving was $985.6 billion in July, and the personal saving rate — personal saving as a percentage of disposable personal income — was 4.4%.

The increase in current-dollar personal income in July primarily reflected an increase in compensation. Personal income increased $112.3 billion, 0.4% at a monthly rate, in July. Disposable personal income — income less personal current taxes — increased $93.9 billion or 0.4%.

Many policy-makers consider core inflation to be a better indicator of trends because it excludes the gas and groceries figures, which are volatile, CNBC said. Central bankers prefer inflation at 2%. Friday’s report shows the economy isn’t near where the Fed wants it.

“The Fed opened the door to rate cuts, but the size of that opening is going to depend on whether labor-market weakness continues to look like a bigger risk than rising inflation,” said Ellen Zentner, chief economic strategist at Morgan Stanley Wealth Management, to CNBC. “Today’s in-line PCE Price Index will keep the focus on the jobs market. For now, the odds still favor a September cut.”

It’s probably safe to say that almost no one following the news believes that Donald Trump has a solid, defensible reason to fire Federal Reserve Board Governor Lisa Cook, as he purported to do Monday, notwithstanding his assertion that she is guilty of “potentially criminal conduct.”

It’s not only that the charge she falsified information on mortgage applications is unproven, or that even on their face the accusations are thinner than onion-skin paper.

It’s that Trump has telegraphed his true objective loud and clear virtually from the inception of his current term: to destroy the Fed’s independence so he can force it to act in accordance with what he sees as his immediate political advantage, chiefly by cutting interest rates at a time when that would be economically irrational.

No one’s claiming that central bankers are going to be perfect at their jobs. What we’re saying is that they’re going to be better than the alternative.

— Peter Conti-Brown, Wharton School

He has pursued this objective in several ways. He has consistently denigrated the work of Fed Chairman Jerome Powell, questioning why Powell was ever appointed (and forgetting that he was the president who appointed Powell).

He has carried on about the cost of a renovation of the Fed’s Washington headquarters building, even misrepresenting the cost and nature of the project, suggesting that it points to Powell’s managerial ineptitude.

Newsletter

Get the latest from Michael Hiltzik

Commentary on economics and more from a Pulitzer Prize winner.

You may occasionally receive promotional content from the Los Angeles Times.

And now he’s trying to fire Cook, one of Powell’s supporters on the Fed board. Whether he can do so in the face of Cook’s refusal to go is unclear, and likely to be judged on by the Supreme Court.

That leads us to the principle of Federal Reserve independence and its critical importance for the health of the U.S. economy.

The Fed isn’t the only central bank that cherishes its independence. Most central banks in developed countries do too, although they solidified their status at different times — the Bank of England gaining operational independence over monetary policy in Britain only in 1997.

To be fair, the character of central bank independence has always been murky. “Central banks do not and should not operate in a vacuum,” Tobias Adrian and Ashraf Khan of the International Monetary Fund observed in 2019, acknowledging that “as public institutions, central banks should be held properly accountable to lawmakers and to society.”

Indeed, to paraphrase Finley Peter Dunne’s Mr. Dooley, throughout its own history the Fed, like the Supreme Court, has “followed the election returns.”

That is, it’s rare for the central bank to range too far from what the public expects from government economic management. In any event, the Fed is a creation of Congress, which could theoretically expand or narrow its monetary policy authority and structure its board to make it more responsive to partisan politics.

The consensus among economists is that doing so would be unwise. Political leaders who have made their central banks subservient to their own policies have almost invariably learned the consequences the hard way, as economists across the economic spectrum observe.

“If a legislature or executive can order the central bank to print money,” wrote Thomas L. Hogan of the conservative American Institute for Economic Research in 2020, “then the government can spend without limit …which can lead to hyperinflation and economic disaster as seen in countries such as Zimbabwe, Venezuela, and Argentina.”

That’s a lesson that economists began urging on Trump as he stepped up his attacks on the Fed. “No one’s claiming that central bankers are going to be perfect at their jobs,” Peter Conti-Brown of the Wharton School said recently. “What we’re saying is that they’re going to be better than the alternative. The alternative is setting interest rate policy from the Oval Office, according to the whims of whatever the president wants to see that day. That’s the main alternative to central banking. And that’s what’s under threat today.”

The United States also learned the value of an independent Fed the hard way. For more than three decades after its creation in 1913, the Fed was largely a handmaiden of the U.S. Treasury; the Treasury secretary and comptroller of the currency were ex officio members of its board, and the Treasury secretary presided over its meetings.

That version of the Fed proved unequal to managing macroeconomic policy as the Great Depression deepened. It had few powers with which to set policy, especially with Franklin Roosevelt taking the reins of economic policy in his own hands.

FDR unilaterally took the U.S. off the gold standard in 1933. He would set the price of gold every morning with aides at his bedside, prompting the British economic sage John Maynard Keynes to complain directly to Roosevelt that “the recent gyrations of the dollar” looked to him “like a gold standard on the booze.”

Roosevelt eventually gave up on manipulating the price of gold and consequently the value of the dollar. He also recognized that the nation needed a firmer, professional hand on the monetary faucet. The solution came from the progressive-minded Utah banker Marriner Eccles, whom FDR tasked with remaking the Fed.

Eccles is almost entirely unknown to the public, but he’s revered among economic policy wonks — which explains why his name is on the Fed headquarters building. After FDR appointed him to head the Federal Reserve Board, Eccles oversaw the drafting of the Banking Act of 1935, which centralized monetary policy in the Fed board and gave it new powers to manage the money supply. Eccles remained the board’s chairman until 1948 and remained a board member until 1951.

Despite those reforms, however, the Fed remained tied to political imperatives, chiefly the financing of America’s fiscal needs during World War II, policies firmly under the control of the Treasury. “We are not masters in our own house,” one Fed bank governor lamented.

That began to change in 1950, when the process of paying for war expenses had triggered an inflationary spiral. The consumer price index rose by 17.6% in 1946-47 and another 9.5% the following fiscal year, thanks in part by the end of wartime price controls and the “pegging” of long-term treasury bond rates at 2.5%.

The onset of the Korean War in 1950 threatened more inflation. President Truman insisted on leaving the peg at 2.5% in order to limit the cost of government spending on the new war. Eccles and others on the Fed board feared, however, that keeping the rate from rising above 2.5% would require the Fed to keep buying T-bonds, which pumped more dollars into the money supply and fueled inflation. The Fed wanted to allow rates to rise, which was anathema to the White House.

This concern placed the Fed in open conflict with Truman and his Treasury secretary, his crony John Wesley Snyder. The Fed and Snyder engaged in increasingly acrimonious meetings, after one of which the White House issued a communique that falsely stated that the Fed had agreed to follow the administration’s demands. The Fed then issued its own statement, directly contradicting Truman’s.

Truman maintained publicly that keeping rates low was crucial for the fight against communism. “I hope the Board will … not allow the bottom to drop from under our securities,” Truman said, referring to the decline of treasury prices if the board let rates rise. “If that happens, that is exactly what Mr. Stalin wants.” Eccles, for his part, told Congress that if the Fed were forced to maintain the 2.5% peg, that would make the Fed itself “an engine of inflation.”

The war of words continued, until Assistant Treasury Secretary William McChesney Martin took over negotiations with the Fed from Snyder, who was recovering from surgery. Martin broke the logjam. The result was the Treasury-Fed Accord of March 4, 1951, a landmark document in Federal Reserve history. The accord gave the Fed full rein to manage short-term interest rates in return for its keeping long-term rates within the peg until the end of that year.

Truman appointed Martin as Fed chairman a few weeks later; some saw the appointment as a Treasury takeover, but Martin proved to be a firm advocate of Fed independence. The accord, as explained by Robert L. Hetzel of the Richmond Fed and Ralph Leach, who personally witnessed the 1951 negotiations, “marked the start of the modern Federal Reserve System” and established the central bank’s “dual mandate” of promoting stable prices and maximizing employment.

That doesn’t mean that the Fed rigorously honored its hard-won independence. Fed Chairman Arthur Burns acceded to Richard Nixon’s urging to keep rates low in advance of the 1972 presidential election. It was a disastrous misstep. Inflation soared, especially during the Arab oil embargo, peaking at nearly 15% in 1980.

It fell to Paul Volcker, who became chairman in 1979, to use the Fed’s authority to slay the inflationary beast. Volcker drove the Fed’s key rate nearly to 20%, provoking a recession and a sharp rise in unemployment. But the inflation rate fell back to 3.8% by 1983 and as low as 1.1% in 1986. Volckeer’s actions arguably set the stage for Ronald Reagan’s defeat of Jimmy Carter in 1980, but arguably he could not have taken the stringent measures needed to bring inflation down if he bowed to Carter’s electoral needs.

Former Fed Chair Ben Bernanke set forth the perils of political influence on the Fed in 2020, warning that central banks subjected to political pressure might “overstimulate the economy to achieve short-term … gains.” Those may be “popular at first, and thus helpful in an election campaign, but they are not sustainable and soon evaporate, leaving behind only inflationary pressures that worsen the economy’s longer-term prospects.”

That’s the prospect facing the U.S. as Trump keeps trying to erode the Fed’s independence, insisting on a rate cut no matter the overall economic environment. As it happens, he may get the rate cut he desires, but only because his tariff and immigration policies are sapping America’s economic strength, producing a slump that warrants a reduction.

Where will we go from here? Powell’s term as Fed chair expires next May. He has been admirably protective of the bank’s independence while in office, but it’s a safe bet that his Trump-appointed successor won’t be so solicitous. Harder times for the Fed, and the economy, may lurk over the horizon.

BRITAIN’S top restaurant chains have seen profits soar by almost a fifth after replacing staff with self-service tills and apps.

They hit £365million at the top 100 groups this year, up from £308million in 2024.

Accountancy group UHY Hacker Young also found that turnover was up 19 per cent to £12.9billion, from £10.8billion.

It said growth had been particularly strong for the fast food and casual dining sector, with burger and steakhouse chains enjoying some of the largest turnover increases.

UHY Hacker Young partner Martin Jones said chains had been investing in technology such as touchscreen tills in fast-food outlets.

Many had also upgraded menu offerings to increase prices, as a way of boosting earnings.

He said: “While many chains are still suffering from depressed margins and weak demand, there’s enough innovation and expansion to deliver better results.”

Hospitality has been particularly hard-hit by the increase in employers’ National Insurance.

Half of all job losses since the Budget have been in that sector, according to analysis of data from the Office for National Statistics by UKHospitality.

It means one in every 25 jobs in pubs, hotels, cafes, restaurants and bars has been axed.

1

Britain’s top restaurant chains have seen profits soar by almost a fifth after replacing staff with self-service tills and appsCredit: Getty

T&C’s ARE KAFKA-ESQUE

BANKS and insurance firms need to stop writing terms and conditions that are “longer than some classic novels”, campaigners urge.

Policies on travel insurance and investment products are the worst, clocking in at 26,000 words — around the same length as Franz Kafka’s Metamorphosis, analysis by Fairer Finance claims.

It comes despite the financial regulator in 2023 introducing rules forcing firms to prove that customers understand such documents.

Fairer Finance said the longer the documents were, the less likely customers were to know what they mean — or to engage with them at all.

Managing director James Daley added: “The grace period is now over, and we expect the regulator to start holding companies to account.”

ENERGY CRISIS

HOUSEHOLDS cannot afford more energy price hikes, the regulator has been warned.

More than 12 million people are struggling to pay already — but Ofgem is expected to announce tomorrow a rise in the energy price cap to £1,737 from October.

Commenting on the research from York University, Simon Francis of the End Fuel Poverty Coalition, said: “The time for tinkering with the price cap is over.”

RENT CONS UP

RENTERS have been warned to watch out for fake landlord scams after crooks made £20million from them last year.

The average victim lost £4,711, Action Fraud said. The total haul was up by 45 per cent on the previous year.

Richard Daniels, of TSB, said: “Scammers prey on a competitive rental market with too-good-to-be-true listings that trick house- hunters into making advanced payments.”

WASHINGTON — President Trump said Monday night that he’s firing Federal Reserve Gov. Lisa Cook, an unprecedented move that would constitute a sharp escalation in his battle to exert greater control over what has long been considered an institution independent from day-to-day politics.

Trump said in a letter posted on his Truth Social platform that he is removing Cook effective immediately because of allegations that she committed mortgage fraud. Bill Pulte, a Trump appointee to the agency that regulates mortgage giants Fannie Mae and Freddie Mac, made the accusations last week.

Pulte alleged that Cook had claimed two primary residences — in Ann Arbor, Mich., and Atlanta — in 2021 to get better mortgage terms. Mortgage rates are often higher on second homes or those purchased to rent.

Trump’s move is likely to touch off an extensive legal battle that will probably go to the Supreme Court and could disrupt financial markets, potentially pushing interest rates higher.

The independence of the Fed is considered critical to its ability to fight inflation because it enables it to take unpopular steps such as raising interest rates. If bond investors start to lose faith that the Fed will be able to control inflation, they will demand higher rates to own bonds, pushing up borrowing costs for mortgages, car loans and business loans.

Legal scholars noted that the allegations are likely a pretext for the president to open up another seat on the seven-member board so he can appoint a loyalist to push for his long-stated goal of lower interest rates.

Fed governors vote on the central bank’s interest rate decisions and on issues of financial regulation. Although they are appointed by the president and confirmed by the Senate, they are not like Cabinet secretaries, who serve at the pleasure of the president. They serve 14-year terms that are staggered in an effort to insulate the Fed from political influence.

No president has sought to fire a Fed governor before. In recent decades, presidents of both parties have largely respected Fed independence, though Richard Nixon and Lyndon Johnson put heavy pressure on the Fed during their presidencies — mostly behind closed doors.

Still, that behind-the-scenes pressure to keep interest rates low, the same goal sought by Trump, has widely been blamed for touching off rampant inflation in the late 1960s and ‘70s.

The announcement came days after Cook said she wouldn’t leave despite Trump previously calling for her to resign. “I have no intention of being bullied to step down from my position because of some questions raised in a tweet,” Cook said in a previous statement issued by the Fed.

Senate Democrats had expressed support for Cook, who has not been charged with wrongdoing.

Another Fed governor, Adriana Kugler, stepped down unexpectedly Aug. 1, and Trump has nominated one of his economic advisors, Stephen Miran, to fill out the remainder of her term until January.

“The Federal Reserve has tremendous responsibility for setting interest rates and regulating reserve member banks. The American people must have the full confidence in the honesty of the members entrusted with setting policy and overseeing the Federal Reserve,” Trump wrote in a letter addressed to Cook, a copy of which he posted online. “In light of your deceitful and potentially criminal conduct in a financial matter, they cannot and I do not have such confidence in your integrity.”

Trump argued that firing Cook was constitutional, even if doing so will raise questions about control of the Fed as an independent entity.

“The executive power of the United States is vested to me as President and, as President, I have a solemn duty that the laws of the United States are faithfully enacted,” the president wrote in the letter to Cook. “I have determined that faithfully enacting the law requires your immediate removal from office.”

Among the unresolved legal questions are whether Cook could be allowed to remain in her seat while the case plays out. She may have to fight the legal battle herself, as the injured party, rather than the Fed.

In the meantime, Trump’s announcement drew swift rebuke from advocates and former Fed officials who worry that Trump is trying to exert too much power and control over the nation’s central bank.

“The President’s effort to fire a sitting Federal Reserve Governor is part of a concerted effort to transform the financial regulators from independent watchdogs into obedient lapdogs that do as they’re told. This could have real consequences for Americans feeling the squeeze from higher prices,” Rohit Chopra, former director of the Consumer Financial Protection Bureau, said in a statement.

It is the latest effort by the administration to take control over one of the few remaining independent agencies in Washington. Trump has repeatedly attacked the Fed’s chair, Jerome H. Powell, for not cutting its short-term interest rate, and even threatened to fire him.

Forcing Cook off the Fed’s governing board would provide Trump an opportunity to appoint a loyalist. Trump has said he would appoint only officials who would support cutting rates.

Powell signaled last week that the Fed may cut rates soon even as inflation risks remain moderate. Meanwhile, Trump will be able to replace Powell in May 2026, when Powell’s term expires. However, 12 members of the Fed’s interest-rate-setting committee have a vote on whether to raise or lower interest rates, so even replacing the chair might not guarantee that Fed policy will shift the way Trump wants.

Rugaber and Weissert write for the Associated Press.

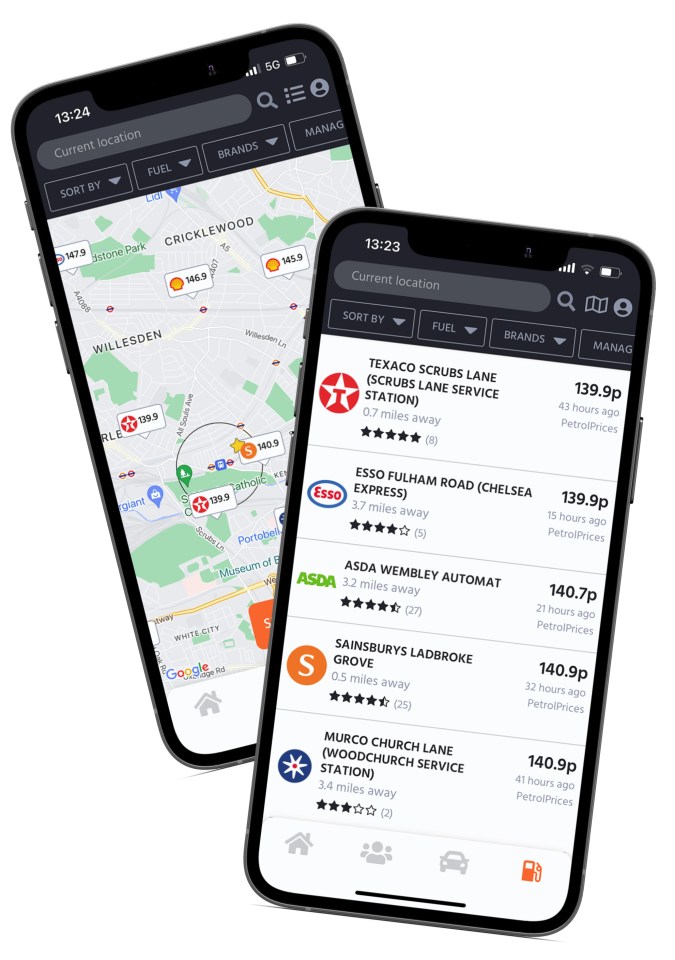

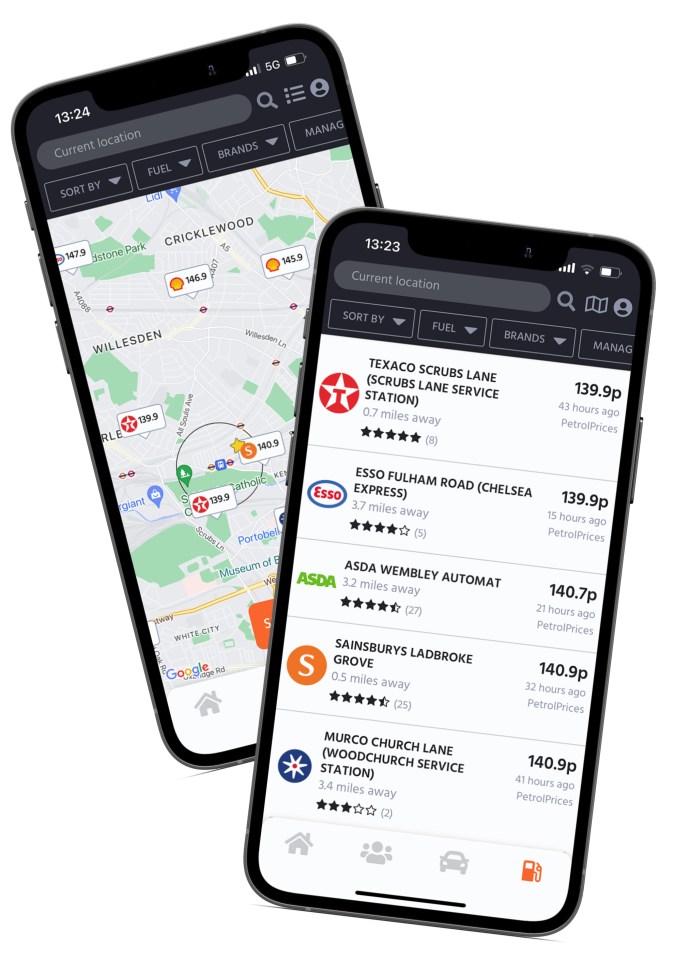

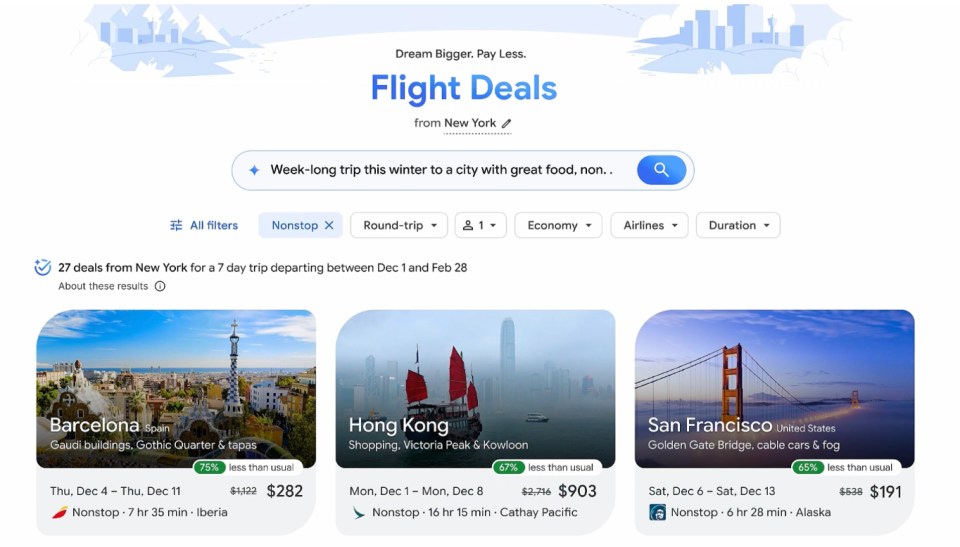

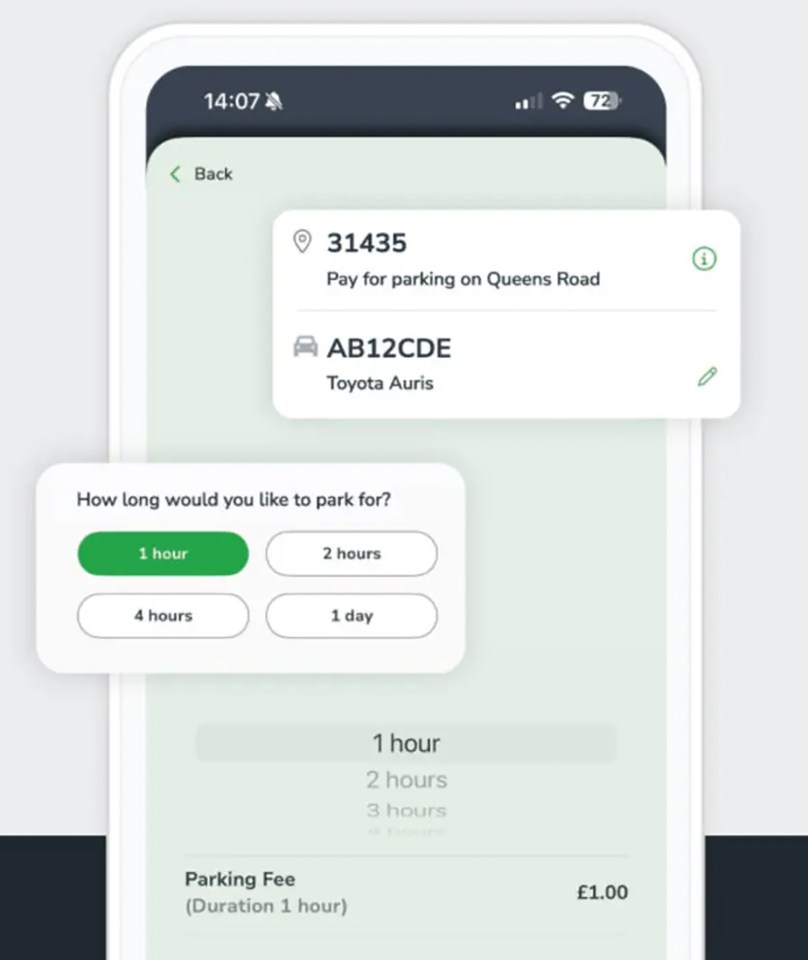

THERE are loads of ways for Brits to use apps to slash bills this summer.

You can easily find the cheapest prices for food, petrol, flights and parking. If you use them regularly, you could easily save hundreds a year.

8

PetrolPrices is one easy way to bring down your fuel billsCredit: PetrolPrices

CHEAPER PETROL

One great option for drivers is the PetrolPrices.