Commentary on a JPMorgan podcast raised hopes that the company could be in line for some government support.

Shares of USA Rare Earth(USAR 7.86%) spiked higher by as much as 15.6% in early trading today. The move comes after commentary on a JPMorgan podcast created optimism that the company could be the next in line for government investment following the landmark deal with MP Materialsannounced recently.

What JPMorgan said

In the internal podcast, JPMorgan’s co-head of mid-cap mergers and acquisitions, Andrew Castaldo, discussed the recent MP Materials deal and said JPMorgan believes that “there’s a whole slew of different critical minerals” that “the administration is also focused on, that could potentially be ripe for this type of collaboration.” He also noted that “we’ve had no less than 100 calls with clients to talk about the MP transaction as well as what this means for other industries.”

What it could mean for USA Rare Earth

It’s natural for investors to hear this kind of commentary and conclude that USA Rare Earth could be next. After all, the company is on track to begin producing rare-earth magnets at its Stillwater, Oklahoma, facility in 2026.

That will help reduce America’s dependence on foreign-sourced rare-earth magnets. The company plans to use the near-term revenue and earnings from magnet production to ultimately develop the Round Top Mountain in Texas, which it controls the mining rights to, to provide its own supply of rare-earth materials for magnet production.

Image source: Getty Images.

Clearly, it will take time and likely a lot of capital to fulfill the plan. Given the strategic importance of securing a domestic supply of rare-earth materials and magnets, it’s perfectly feasible that the current administration could also consider providing some form of support to USA Rare Earth.

JPMorgan Chase is an advertising partner of Motley Fool Money. Lee Samaha has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends JPMorgan Chase. The Motley Fool recommends MP Materials. The Motley Fool has a disclosure policy.

We’re about a month away from an official number, but estimates for next year’s COLA are moving higher.

Social Security may be the most valuable retirement asset most Americans have. The pension for retired workers accounted for 20% of families’ total wealth in 2022, according to a study by the Congressional Budget Office. That’s based on a calculation valuing all future payments at present value.

Those future payments get a boost every year, which could make them even more valuable to Americans. The annual cost-of-living adjustment (COLA) helps benefits keep up with inflation. And while we won’t have the official 2026 COLA number until mid-October, it looks like it’ll come in higher than what analysts anticipated at the start of the year.

But a bigger COLA isn’t necessarily reason for Social Security recipients to celebrate. Here’s what retirees need to know.

Image source: Getty Images.

What’s pushing the 2026 COLA higher?

The annual COLA is based on a standard measure of inflation published every month by the Bureau of Labor Statistics called the Consumer Price Index for Urban Wage Earners and Clerical Workers, or CPI-W.

The CPI-W is one of several Consumer Price Index measurements the government publishes. The BLS surveys thousands of businesses and households across the country to collect pricing data on over 200 line items. Those prices are then indexed to a standard price from when the BLS first started collecting data, and weighted according to typical spending patterns of the group the index is supposed to follow. In the case of the CPI-W, the basket of goods represents the spending of working-age adults living in cities.

The Social Security Administration calculates the COLA by taking the average year-over-year increase in the CPI-W during the third quarter, i.e. July, August, and September. The BLS just published August’s CPI numbers on Sept. 11, with the CPI-W climbing 2.8% year over year. That follows a 2.5% increase in July. The final reading to determine the 2026 COLA will come out on Oct. 15.

Based on expectations for that reading, both The Senior Citizen’s League and independent analyst Mary Johnson have published their expectations for next year’s COLA. The former expects it to come in at 2.7% while the latter expects retirees to receive a 2.8% bump. Both estimates are higher than the 2.5% initial estimate The Senior Citizen’s League published before the start of the year.

The reasons for a higher COLA are bad news for 70 million beneficiaries

A bigger-than-expected raise is usually great news for those receiving it, but in the case of Social Security’s 70 million beneficiaries, it signals a challenging economic environment.

The biggest challenge is that the CPI-W doesn’t perfectly match the spending of most seniors. Most people don’t spend their money in retirement the same way they did when they were working age. They probably commute less and spend less on new clothing. They probably have different dining habits. And it’s almost certain that their medical bills have climbed higher as they grow older.

To that end, some of the biggest expenses seniors face are climbing faster than the overall CPI-W numbers. Medical care services were notably 4.2% higher this August than the year before. While gasoline prices were down, utilities were way up. Shelter expenses climbed 3.6%. Despite a 2.7% or 2.8% raise coming in January, most seniors have seen their real cost of living climb much more over the past year.

Rising medical costs are most prominently seen in the Medicare Trustees’ estimate for next year’s Medicare Part B premium. They expect the program will have to charge a standard monthly premium of $206.20 next year, an 11.5% increase from 2025. For those keeping track, that far outpaces the expectations for Social Security’s COLA. Beneficiaries age 65 and older enrolled in Medicare will see that amount come right out of their new monthly payments.

The Senior Citizens League contends this situation isn’t unique to this year’s COLA. It ran a study that estimates the buying power of someone’s benefits who started Social Security in 2010 has decreased 20% through 2024.

The best economic environment for Social Security has historically been slow, steady, and predictable inflation. Under the current administration, which has gone back and forth on trade policies numerous times since the start of the year, prices have become anything but predictable. While many businesses have taken preemptive steps to curb and delay the impact of tariffs, the costs will eventually get passed through to consumers. That could result in even more pain for those on a fixed income next year.

While a 2.7% or 2.8% raise might be bigger than anticipated, many seniors may find that it doesn’t go far enough next year.

A peer across the Pacific Ocean has purchased the rights to one of the biotech’s pipeline drugs.

On Monday, investors clearly saw excellent value in the stock of Ocugen(OCGN 11.68%), a biotech that concentrates on treatments for eye disorders. They traded the company’s shares up by more than 12%, on the back of a fresh licensing agreement signed with a peer in Asia. That 12% absolutely trounced the 0.5% rise of the S&P 500 index today.

A licensing deal with a major Asian pharma

Ocugen announced that it has signed a licensing deal with Kwangdong Pharmaceutical in South Korea. Under the terms of the arrangement, Kwangdong will own the exclusive rights throughout South Korea for OCU400, an investigational drug targeting retinitis pigmentosa (RP). This is a disorder of the retina that causes progressive loss of vision.

Image source: Getty Images.

For the license, Ocugen is to be paid up-front fees and near-term development milestones amounting to as much as $7.5 million. The healthcare company can also earn milestones of $1.5 million for each $15 million of sales through Kwangdong. Ocugen said that if and when commercialized, OCU400 could hit sales of at least $180 million in the first 10 years of being on that market.

Lastly, the American company stands to earn royalty payments of 25% of the net sales of the drug in South Korea.

The start of something big?

Ocugen’s hopes for the drug seem quite realistic, given that — according to its research — roughly 7,000 people in South Korea suffer from RP. And that’s the potential in only one country; if the drug is successfully brought to market elsewhere, this might be only the tip of the iceberg.

Eric Volkman has no position in any of the stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.

One pundit believes the share price could rise in excess of 50%.

Monday was a good day to be invested in Scholar Rock(SRRK 6.19%) stock. The clinical-stage biotech received a nod from an analyst initiating coverage on its shares, a move that sent its price more than 6% higher across the day. That rate was well higher than the 0.5% increase of the S&P 500 index.

A bullish start

Well before market open, Leerink Partners’ Mani Foroohar launched his coverage of Scholar Rock, rating the healthcare stock as an outperform (i.e., buy) at a price target of $51 per share. That anticipates considerable growth in the value of the company’s equity, as it’s — coincidentally — more than 51% higher than Scholar Rock’s most recent closing price.

Image source: Getty Images.

The biotech’s leading investigational drug is apitegromab, an add-on therapy that targets a disorder called spinal muscular atrophy (SMA). According to reports, Foroohar’s main source of optimism is the prospects for the drug, which is currently being reviewed for approval by both the U.S. Food and Drug Administration (FDA) and the European Medicines Agency (EMA, a regulator for the European Union).

In his inaugural note on Scholar Rock, the analyst also waxed bullish on the background of the company’s team, characterizing it as the most experienced in the commercialization of rare diseases among its covered healthcare stocks.

High potential

If Scholar Rock can win approval from one or both of those major regulators for apitegromab, it would be well positioned for success. However, I need to caution that getting the green light isn’t enough for a biotech — a new medicine must be effectively rolled out and marketed if it’s going to have any chance at success. So far, though, the indications look good for the company.

Eric Volkman has no position in any of the stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.

Memory chip leader SK Hynix released its latest high-bandwidth memory chip.

Shares of Micron (MU 4.59%), the U.S.-based memory chipmaker, were moving higher today in sympathy with SK Hynix, the world’s largest memory chip company, which hit an all-time high today after it announced the world’s first HBM4 product.

Though SK Hynix is a competitor to Micron, the news was seen as a positive for the broader memory-chip industry, as it should spark more demand for HBM. It also comes during a week when artificial intelligence (AI) stocks have been flying higher after Oracle gave blowout guidance for cloud infrastructure growth earlier this year.

Micron stock closed up 4.6% on the news.

Image source: Getty Images.

A rising tide in memory chips

SK Hynix, based on South Korea, jumped 7% today after it said this morning that it completed development of HBM4, its next-generation memory product for ultra-high performance AI.

Touting its capabilities, the company said that HBM4’s bandwidth has doubled, and its power efficiency improved 40% compared with the previous generation. HBM4 marks its sixth generation of HBM.

While that development might be seen as bad news for Micron, the memory chip sector is subject to many of the same supply and demand trends. Micron has already sold out its HBM capacity for the year, so the news shouldn’t have an immediate impact on its results, but it could help lift prices in the industry.

What’s next for Micron?

Today’s gain marks the second day in a row of upward momentum for Micron, as the stock moved higher yesterday after Citigroup raised its price target to $175 and reaffirmed its buy rating, noting that pricing for DRAM and NAND chips are trending higher.

Micron will report fiscal fourth-quarter earnings on Sept. 23, with analysts expecting revenue to jump 43% to $11.1 billion and for adjusted earnings per share to more than double from $1.18 to $2.85.

If the company tops those estimates, the stock could soar as Micron still looks cheap at a forward P/E of just 12.

Citigroup is an advertising partner of Motley Fool Money. Jeremy Bowman has positions in Micron Technology. The Motley Fool has positions in and recommends Oracle. The Motley Fool has a disclosure policy.

A good one-week stretch is capped by a substantial analyst price target raise.

According to data compiled by S&P Global Market Intelligence., AppLovin‘s (APP 1.87%) stock was among the market’s most-loved this week, rising by nearly 19% in price over the period. That was entirely understandable, as the shares were tapped for an inclusion on one of the top stock indexes in the world, and capped the week by being the subject of an analyst price target raise.

Index inclusion

Just after market close last Friday, index compiler S&P Dow Jones Indices, a division of S&P Global, announced that AppLovin would be a component stock of its bellwether S&P 500(^GSPC -0.05%). This was among a series of adjustments made by S&P Dow Jones Indices as part of its quarterly “rebalancing” to reflect changes in market cap for certain stocks.

Image source: Getty Images.

AppLovin is being accompanied by next-generation brokerage Robinhood Markets and mechanical/electrical systems specialist EMCOR Group in the current round of S&P 500 advancement. The three stocks are displacing current components MarketAxess Holdings, Caesars Entertainment, and Enphase Energy.

These changes will take effect before market open on Monday, Sept. 22.

Double-digit potential

Friday morning, Wedbush analyst Alicia Reese added to the generally positive sentiment on AppLovin by raising her price target on the stock. That hike was substantial, as the pundit cranked it 17% higher to $725 per share, well up from the previous $620. At AppLovin’s most recent closing price, the new level anticipates upside of nearly 25%.

According to reports, Reese’s move was based on what she considers to be strong and sustainable growth in several of the company’s customer segments, including gaming and e-commerce.

Eric Volkman has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends EMCOR Group and S&P Global. The Motley Fool recommends Enphase Energy and MarketAxess. The Motley Fool has a disclosure policy.

In a dynamic world where higher education is a gateway to opportunity, far too many talented youth remain locked out—trapped behind financial, social, and political barriers. For marginalized and conflict-affected youth, the dream of attending university is often deferred, if not entirely extinguished. Yet, there is a proven solution hiding in plain sight: inclusive, quality and relevant scholarship programs.

Scholarships must not be seen as charity, but as investments in human capital and development in society. Inclusive scholarships do more than fund tuition. They serve as transformative interventions—paving futures and restoring dignity. And for higher education institutions (HEIs), these scholarships can be catalysts for innovation, reshaping the global education landscape.

Overcoming the Persistent Barriers to Higher Education

According to international organizations, millions of young people worldwide face multiple, overlapping challenges that limit access to higher education. Refugees, internally displaced persons, underserved women, students with disabilities, and those from low-income backgrounds often encounter systemic marginalization and underfunding.

Access to higher education opportunities is only the first step. UNHCR signals that 7% of refugees today have access to higher education compared to only 1% in 2019. This is far below the global average of higher education enrollment among non-refugees, which currently stands at around 42%. To achieve the target of 15% enrolment by 2030, UNHCR emphasizes that coordination, commitment and the sustained engagement of a range of partners as well as a focus on HEIs and systems in primary hosting countries will be required.

Tuition fees on the rise remain out of reach for many. Even when financial aid exists, students struggle with hidden costs—transportation, learning materials, digital access, and psychosocial support. In fragile or conflict-affected contexts, political instability and displacement further disrupt educational continuity. For these students, a scholarship can mean the difference between social exclusion and becoming a leader in their community.

One of the biggest challenges in scaling scholarship programs is sustainable financing. Traditional donor-driven models, while foundational, are insufficient on their own. According to UNESCO, an alarming potential loss of US$21 trillion—equivalent to 17% of global GDP—could occur in lifetime earnings for students due to escalating education inequities, learning poverty, and loss of learning opportunities. Hence, innovation in how scholarships are funded, sustained, and delivered is becoming paramount. Blended finance models, cost-sharing mechanisms, and outcome-based funding are key to building effective and resilient partnerships.

Scholarship Programs that Transform Higher Education Institutions

Scholarships significantly ease the financial burden on students and families, particularly in low-income economies and crisis-affected contexts. When this burden is lifted, students are less likely to drop out and more likely to excel. Improved retention, higher completion rates, and stronger academic performance enhance the reputation and competitiveness of HEIs on the global stage.

Inclusive scholarships also foster diversity and equity in higher education. By supporting underserved communities and individuals, scholarships not only close the access gap but also transform campus demographics and academic discourse. When students from diverse backgrounds thrive, institutions become more representative, socially responsive, and globally relevant.

Moreover, high-quality scholarship programs attract high-caliber applicants who might otherwise be excluded. These students often become some of the most driven and impactful members of their communities and societies. Their presence raises the standard of academic engagement and reinforces a virtuous cycle of inclusion and excellence. Scholarships also support adult learners, foster career mobility, and promote lifelong learning—vital in a world where cross-skilling and adaptability are key to navigating complex futures.

For HEIs most compellingly, scholarships drive innovation. With more diverse learners come stronger demands for accessible technology, inclusive pedagogy, support services, and flexible learning models. These needs accelerate institutional investment in blended learning, digital inclusion, and universal design. Such advancements of HEIs are also directly aligned with global priorities such as the Sustainable Development Goals (SDGs). A recent research highlights that the successful implementation of the SDGs depends on the existence of well-functioning and capacitated HEIs in every society. It adds that inclusive scholarship programs contribute to the investment in local higher education systems and institutions, strengthening their infrastructure in the host countries.

Stories of Resilience, Ambition, and Transformation

For scholarship programs to be truly impactful, they should also be relevant and designed around the lived realities of the underserved students. A scholarship is not merely a ticket to the classroom—it must serve as a bridge to employability and social contribution. Thus, market-driven higher and tertiary education programs should align to both the needs of society and future trends in workforce.

Facts and feedback from the Education Above All (EAA) Foundation scholarship recipients and alumni show how inclusive and quality higher education scholarships drive positive change. For marginalized and conflict-affected youth, these opportunities are not just financial—they have become lifelines. EAA’s Qatar Scholarship programs, spearheaded by Al Fakhoora Program and in collaboration with key partners, has empowered recipients to access sustainable employment and thrive within society. The programs provide holistic support by covering tuition, ending social isolation, and offering pathways to dignity and opportunity.

In one of EAA’s scholarship programs, for instance, nearly 91% of the recent graduates from top-tier universities found employment within six months of completing their degree studies. The remaining 9% did so within a year. Most graduates now work in fields aligned with their studies, contributing meaningfully to their communities and professions. According to the recipients themselves, these scholarships did more than alleviate financial pressure—they enabled inclusion, ensured access to quality education, and fostered a sense of belonging and equality.

A Call to Action

We are at a pivotal moment. Global displacement is at an all-time high. Conflict, climate change, and economic inequality are creating new education emergencies. If we fail to act now, we risk consigning generations of youth to exclusion and despair. But there is another path. We can choose to invest in the futures of those left long behind. The impact is proven, the means exist, and the moral imperative is undeniable.

Over time, inclusive scholarships do more than serve individual students—they create ripple effects. They enhance the institutional reputation, strengthen the social contract between universities and communities, and even empower the scholars to contribute to the advancement of society through civic engagement, peace and global citizenship, and intergenerational mobility.

No single actor can do this alone. Real impact requires coordination across borders and sectors. The private sector, more than ever before, also has a critical role to play—from tech companies enhancing digital access to employers offering internships and job opportunities. The future of work is global, and so must be the response to educational inequality.

EAA continues to advocate with the global higher education community and beyond for inclusive, quality-driven, and scalable scholarship solutions. EAA has pioneered multi-stakeholder collaboration, bringing together UN agencies, development banks, universities, philanthropic organizations, and local governments to co-fund scholarship pathways. These models are scalable, replicable, and demonstrate that with institutional will and strategic partnerships, solutions are within reach.

*Amir Dhia is the Technical Manager of Higher Education at the Education Above All (EAA) Foundation. His career spans over twenty-five years of global experience in the private, public, non-governmental, and state institutions. He has held several senior executive positions internationally, including Advisor, Dean, and Director General, contributing to the advancement of higher and executive education, certification institutions, language institutes, and international education partnerships. Amir holds a PhD (summa cum laude), specializing in the Knowledge Society and Diplomacy, along with a number of designations in leadership, management, and business development.

About the Education Above All (EAA) Foundation

The Education Above All (EAA) Foundation is a global foundation established in 2012 by Her Highness Sheikha Moza bint Nasser. EAA Foundation aims to transform lives through education and employment opportunities. We believe that education is the single most effective means of reducing poverty, creating peaceful and just societies, unlocking the full potential of every child and youth, and creating the right conditions to achieve Sustainable Development Goals (SDGs).

Through our multi-sectoral approach, unique financing models, focus on innovation as a tool for social good, and partnerships, we aim to bring hope and real opportunities to the lives of impoverished and marginalised children and youth. EAA Foundation is comprised of the following programmes: Educate A Child (EAC), Al Fakhoora, Reach Out To All (ROTA), Silatech, Protect Education in Insecurity and Conflict (PEIC), Innovation Development (ID) and Together project.

More than a month after publishing impressive quarterly results, investors and pundits alike are still feeling good about the company.

Internet discussion forum operator Reddit(RDDT 0.55%) was the talk of numerous investors on Thursday, and for the most part, the chatter was positive. The company’s share price rose by nearly 1% — good enough to notch an all-time high — thanks in no small part to a bullish move from a researcher on Wednesday afternoon. That increase more or less matched that of the bellwether S&P 500 index that day.

Untapped potential

That Reddit-tracking company was Jefferies, whose analysts reiterated their buy recommendation on the stock while slightly increasing their price target to $320 per share (formerly it was $300).

Image source: Getty Images.

Reddit is lumped in with the social media stocks grouping, but within this small cabal, it’s unique. It doesn’t focus on updating acquaintances like Meta Platforms‘ Facebook or photo-sharing like the same company’s Instagram. Instead, it offers users the chance to discuss, debate, and explain any topic they’re curious about.

According to reports, the Jefferies team is particularly encouraged by what they consider to be Reddit’s potential to boost revenue significantly. In their modeling, they believe that the specialized tech company could post full-year 2027 revenue topping the current consensus analyst estimate by a rich 35%.

The analysts also pointed out that the company’s U.S. average revenue per user (ARPU; a crucial metric in the social media industry) is well below that of certain peers, offering significant upside potential.

Second-quarter surges

To an extent, Reddit is still basking in the glow of its impressive second quarter, the figures for which were published at the end of July. The company managed to boost its revenue by a robust 78% year-over-year (to $500 million), and flip to a net profit that was well in the black, at $89 million. Both headline figures, by the way, trounced the average analyst estimates.

Eric Volkman has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Jefferies Financial Group and Meta Platforms. The Motley Fool has a disclosure policy.

There’s nothing like a double-digit dividend raise to get the bulls running.

There are few things income investors like more than a meaty dividend raise. Argan (AGX 3.95%) declared one on Wednesday, and the market rewarded the construction company with a nearly 4% bump in its share price. That was significantly better than the 0.3% increase posted by the benchmark S&P 500 index.

A healthy boost

Most dividend raises are cautious, representing only incremental improvements over their predecessors. This sure isn’t the case with Argan’s latest hike. The company is increasing it by 33%, or more than $0.12 per share, to $0.50. The new dividend would yield just under 1% on Argan’s most recent closing stock price. It is to be paid on Oct. 31 to shareholders of record as of Oct. 23.

Image source: Getty Images.

This dividend raise is Argan’s third in as many years. The company is thriving, and wants to reflect this in the payout.

In its press release about the dividend, the company quoted CEO David Watson as saying that “The ongoing electrification of everything requires an uninterrupted supply of reliable, high-quality energy, and we believe we are well-positioned with our diverse capabilities, proven track record and long-standing customer base, to benefit from the current demand environment as the industry responds to the urgent need for reliable energy resources to strengthen the power grid.”

Second quarter not as prosperous as it looked

Argan’s second-quarter earnings, published last week, have clearly filled management with enthusiasm. For the period, revenue and, especially, GAAP net income grew on a year-over-year basis, and the company notched a very convincing beat on the bottom line. However, analysts tracking the stock had expected a higher top-line figure, while profitability was impacted by events that appear to be one-off occurrences.

Eric Volkman has no position in any of the stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.

Oracle’s blowout RPO number bodes well for Bloom, which inked a partnership with Oracle back in July.

Shares of Bloom Energy(BE 12.51%) rocketed 18.5% higher on Wednesday as of 12:35 p.m. ET.

There wasn’t any news specifically from Bloom today; however, last night’s bombshell guidance from Oracle(ORCL 33.94%) is likely boosting Bloom by association, given that Bloom inked an important data center partnership with Oracle in July.

Oracle announces AI hypergrowth, and it will need lots of energy

Bloom surged in July after it announced a landmark deal with Oracle on July 24. For reference, Bloom’s energy servers can transform natural gas or hydrogen into electricity without combustion, producing electricity from an abundant source like natural gas in a cleaner way to meet escalating electricity demand.

Bloom had served utilities and other power users in the past, but the July deal with Oracle was the first direct agreement with a cloud hyperscaler.

Therefore, when Oracle provided astonishing backlog growth in its cloud infrastructure (IaaS) business last night, that also improved the outlook for Bloom, which will likely play a role in providing electricity to those data centers. Oracle reported $455 billion in remaining performance obligation in its cloud IaaS business, up an astounding 359%. On the conference call with analysts, CEO Safra Catz noted she expects cloud infrastructure revenue to grow from $18 billion this year to a stunning $144 billion in fiscal 2030 — over just a matter of four years.

Needless to say, that much growth will require Oracle to build a lot more data centers, which will likely be served in part by Bloom’s energy servers.

Image source: Getty Images.

Bloom looks expensive, but AI growth is off the charts

After today’s rally, Bloom trades at 76.5 times next year’s earnings estimates. That’s very expensive for a low-margin hardware business, but Oracle’s multiyear guide appears to have lifted the prospects for Bloom’s growth over the 2027-2030 time frame.

So while Bloom’s valuation makes it risky at these levels, its artificial intelligence (AI)-related growth story keeps getting better.

Billy Duberstein and/or his clients have no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Oracle. The Motley Fool has a disclosure policy.

This artificial intelligence (AI) specialist leveraged decades of expertise in information technology (IT) and cloud systems and is on a path to earn membership in a very exclusive fraternity.

There’s no denying the trajectory of artificial intelligence (AI) over the past few years. Many of the companies that have pivoted to adopt this game-changing technology have ascended the ranks of the world’s largest companies when measured by market cap. When the stock market closed on Tuesday, there were 11 members of the vaunted $1 trillion club, the vast majority of which have significant ties to AI.

After the market close, industry stalwart Oracle(ORCL 1.37%) reported its recent quarterly results, and despite missing Wall Street’s expectations, the stock surged higher and never looked back. Why? In a stunning turn of events, the company signed numerous multibillion-dollar contracts that kicked its future growth potential into overdrive.

Given the magnitude of these deals, it seems the writing is on the wall for Oracle to join this elite fraternity. The company’s growth is at a tipping point, and management’s commentary suggests the company has a long AI-centric runway for growth ahead.

Image source: Getty Images.

A trusted partner

Oracle holds a coveted place in the technology community, as roughly 98% of Global Fortune 500 companies make up its customer rolls. The industry stalwart provides its customers with a strategic combination of cloud, database, and enterprise software. Naturally, when the shift to AI began in earnest, this captive audience began to turn to Oracle for its expanding collection of cloud and AI solutions.

The company’s growth has been uneven, but the future looks bright. During Oracle’s fiscal 2026 first quarter (ended Aug. 31), total revenue grew 11% year over year to $14.9 billion, while its adjusted earnings per share (EPS) of $1.47 grew by 6%. Both numbers accelerated compared to Q4, but missed Wall Street’s consensus estimates, which called for revenue of $15 billion and adjusted EPS of $1.48.

However, that wasn’t the headline. Last quarter, CEO Safra Catz noted that the company had reached a “tipping point,” noting that revenue growth was accelerating, “and it’s only going up from here.”

That turned out to be an understatement. Oracle reported explosive growth in its remaining performance obligation (RPO) — or contractual obligations not yet included in revenue — which skyrocketed 359% year over year to $455 billion, up from $138 billion in Q4.

Catz explained, “We signed four multibillion-dollar contracts with three different customers in Q1,” calling the results “astonishing.” He went on to say that demand for Oracle Cloud “continues to build.” The company expects to sign “several additional multi-billion-dollar customers and RPO is likely to exceed half a trillion dollars.”

Looking to the future, Oracle is forecasting Oracle Cloud Infrastructure revenue to grow 77% to $18 billion this year — but that’s just the beginning:

Fiscal 2027 cloud revenue of $32 billion, up 78%.

Fiscal 2028 cloud revenue of $73 billion, up 128%.

Fiscal 2029 cloud revenue of $144 billion, up 97%.

Mind you, this is just Oracle Cloud Infrastructure revenue, and Catz noted that “most of the revenue in this five-year forecast is already booked in our reported RPO.” That means that any future contracts will probably increase those growth targets.

The path to $1 trillion just got much shorter

Oracle is leveraging its position as a trusted partner to help customers choose suitable AI and cloud solutions and profit from the growing adoption of generative AI.

Before today’s results, Wall Street was expecting Oracle to generate revenue of $66.75 billion in its fiscal 2026 (which began June 1), giving it a forward price-to-sales (P/S) ratio of about 10. Assuming its P/S remained constant, Oracle needed to generate revenue of approximately $98 billion annually to support a $1 trillion market cap. Given those figures, Oracle could have achieved a $1 trillion market cap before 2028.

Wall Street hasn’t yet had time to update its models, but given the magnitude of the company’s results, previous forecasts are out the window. Barring unforeseen circumstances, I predict Oracle will join the $1 trillion club within the next 12 months.

Estimates regarding the market potential of generative AI continue to ratchet higher. Big Four accounting firm Price Waterhouse Coopers (PwC) calculates the opportunity could be worth as much as $15.7 trillion annually by 2030, which illustrates the magnitude of the opportunity.

Given the recent contract wins, Oracle has proven that it is leveraging its experience to profit from this windfall. The writing is on the wall, and Oracle is poised to join the fraternity of trillionaires in short order.

Danny Vena has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Oracle. The Motley Fool has a disclosure policy.

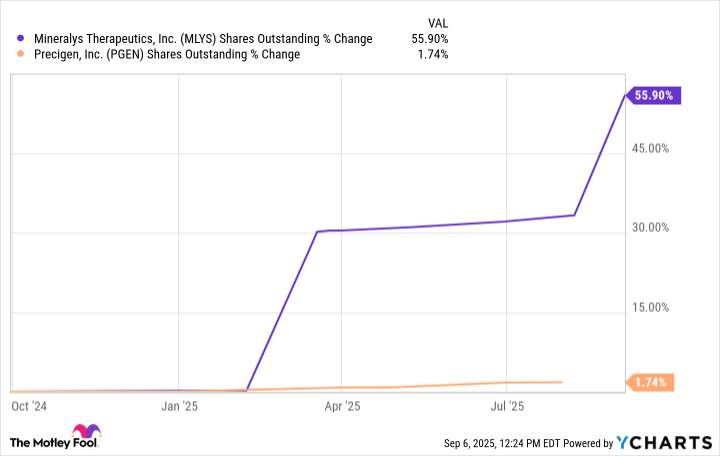

Experts who follow these stocks think they can fly higher despite already gaining over 100% since the end of July.

Investors in search of stocks that can produce dramatic gains in a short time frame will want to turn their heads toward the healthcare sector. A handful of stocks in the space more than doubled in price recently.

Shares of Precigen(PGEN -4.61%) and Mineralys Therapeutics(MLYS 4.86%) have already risen more than 100% since the end of July. Despite the recent run-ups, Wall Street experts who follow these stocks believe they could soar even further.

Image source: Getty Images.

1. Precigen

From the end of July through Friday, Sept. 5, shares of Precigen shot 155% higher. The market cheered because the drugmaker earned approval from the Food and Drug Administration (FDA) for its first treatment. Papzimeos is a cell-based immunotherapy for the treatment of recurrent respiratory papillomatosis (RRP), a rare disease that results in tumors lining the respiratory tract.

Papzimeos is the first and only treatment approved by the FDA to treat an estimated 27,000 patients with RRP. The agency granted the drug full approval instead of waiting for a confirmatory study. In the single-arm trial supporting its application, 18 out of 35 patients responded well enough to avoid tumor removal surgery for at least 12 months after treatment with Papzimeos.

The agency and analysts following Precigen were encouraged by the fact that 15 out of the initial 18 responders remained surgery-free 24 months after treatment with Papzimeos. In response, Swayampakula Ramakanth from HC Wainwright reiterated a buy rating and an $8.50 price target that implies a 95% gain in the year ahead.

2. Mineralys Therapeutics

Shares of Mineralys Therapeutics rose 146% from the end of July through Sept. 5. Investors were excited about a successful new funding round to support continued development of lorundrostat, its lead candidate. On Sept. 2, Mineralys suspended an at-the-money equity offering and, within a couple of days, completed a secondary offering that ended up raising $287.5 million.

In August, investors hardly noticed a presentation of phase 3 trial results regarding lorundrostat. Patients who added the aldosterone inhibitor to the medications they were already taking reduced their systolic pressure by 16.9 millimeters of mercury after six weeks on treatment, compared to just 7.9 millimeters of mercury for patients who received a placebo.

Mineralys’ stock shot higher after AstraZeneca reported arguably inferior 12-week data for an aldosterone inhibitor it’s developing called baxdrostat. At week 12, it reduced patients’ systolic pressure by 15.7 millimeters of mercury, compared to 5.8 millimeters of mercury for the placebo group.

Less than a week ahead of Mineralys’ successful secondary stock offering, Bank of America analyst Greg Harrison boosted his target for the stock to $43 per share. The raised target implies a gain of about 24% from recent prices.

Time to buy?

Before you get too excited about Mineralys and its hypertension candidate, it’s important to realize the pre-commercial-stage business finished June with $325 million in cash, or enough to last into 2027. Diluting shareholder value to raise additional capital that could now push the stock price higher means the company isn’t super confident that it can quickly submit an application and earn approval for its lead candidate before the beginning of 2027.

At recent prices, Mineralys sports a huge $2.7 billion market cap that could shrink significantly if it looks like timing will become an issue that allows AstraZeneca’s candidate to gain and maintain a large share of the market for new hypertension drugs. It’s probably best to wait and see whether this company can earn approval for lorundrostat in a timely manner before adding the stock to your portfolio.

With a market cap of $1.3 billion at recent prices, expectations for Precigen are lower than they probably should be. Papzimeos is already approved and will launch unchallenged in its niche market.

Papzimeos’ addressable patient population is small, but a list price north of $200,000 per year per patient means it could rack up more than $1 billion in annual sales at its peak. Since drugmaker stocks generally trade at mid- to high-single-digit multiples of total sales, adding some shares to a diversified portfolio now looks like a smart move.

Bank of America is an advertising partner of Motley Fool Money. Cory Renauer has no position in any of the stocks mentioned. The Motley Fool recommends AstraZeneca Plc and Mineralys Therapeutics. The Motley Fool has a disclosure policy.

Ciena is an under-the-radar artificial intelligence (AI) play in the age of multi-data center clusters.

Shares of Ciena(CIEN -0.20%) rallied 23.9% this week through 1:46 p.m. ET Friday, according to data from S&P Global Market Intelligence.

Ciena is a leader in optical transceivers and other IP networking and routing hardware and software. That’s a market that has typically served large telecom players, but which has now reaccelerated in the age of artificial intelligence (AI), and the increased networking demands required for it.

On Thursday, Ciena showed off a new AI-powered acceleration, delivering fiscal third-quarter results that handily beat analyst expectations.

Ciena blows past estimates on the back of AI networking needs

In its fiscal third quarter, Ciena grew revenue 29.4% to $1.22 billion, while adjusted non-GAAP (generally accepted accounting principles) earnings per share nearly doubled, up 91.4% to $0.67. Both figures handily beat analyst expectations, especially the bottom-line figure, which bested estimates by $0.14.

Ciena is capitalizing on the newfound demand for inter-data center networking, stemming from the growth of generative AI. AI training companies are now connecting multiple data centers to function as a single AI “cluster,” which increases bandwidth needs. Moreover, as AI becomes infused into many enterprise and edge applications, the need for lighting-fast “inferencing” is also growing networking demand by leaps and bounds.

While Ciena’s traditional telecom market is only growing at a 4% pace, newer markets in metro routing and data center communications are forecast to grow at a 26% compound annualized growth rate through 2028, wherein the new markets will equal the size of Ciena’s traditional markets.

Image source: Getty Images.

Ciena: An underappreciated AI star?

After its rally this week, Ciena currently trades around 27.5 times next year’s earnings estimates. Its fiscal year ends in October 2026.

That’s not exactly cheap anymore, but it is a lower valuation than other AI stars that have recently come onto the scene. That being said, the company could make for a solid addition to a high-quality AI-oriented “basket” portfolio for those bullish on the long-term prospects of the AI build-out.

Billy Duberstein and/or his clients have no position in any of the stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.

Wednesday might have been a Hump Day of a slog to some investors, but not for those holding shares of Immunovant(IMVT 10.82%). On some rather encouraging news from the laboratory, the clinical-stage biotech‘s shares gained almost 11% in value, easily topping the 0.5% rise of the benchmark S&P 500(^GSPC 0.51%).

Proven results

That afternoon, Immunovant shared data from a proof-of-concept study of its batoclimab. This is an investigational drug targeting Grave’s disease (GD), an autoimmune disorder that results in the body producing too much thyroid hormone (also known as hyperthyroidism).

Image source: Getty Images.

The study, which lasted nearly one year, saw 17 of the 21 patients dosed with the drug maintain normal thyroid function six months after the completion of treatment. Eight of the 17 also did not require anti-thyroid drugs to keep the hormone in check.

The participants in the study suffered from Grave’s disease, and continued to experience hyperthyroidism despite taking standard anti-thyroid medication.

In the press release trumpeting these results, Immunovant quoted its CEO Eric Venker as saying, “We believe these data have the potential to be transformative for patients and practice-changing for physicians, if approved by the Food and Drug Administration, by addressing a significant unmet need in Grave’s disease.”

A flexible drug?

As Grave’s disease is a chronic condition, it is an appropriate target for an advanced treatment like batoclimab. Immunovant is also investigating the treatment for other indications, such as Sjögren’s syndrome, a disorder of the salivary and tear glands. The company is in the early stages of development for these.

Eric Volkman has no position in any of the stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.

HOUSEHOLDS across the country are being warned to brace for a financial squeeze as the cost of government borrowing skyrockets to levels not seen since 1998.

This now directly threatens to push up mortgage rates and could usher in a new wave of tax hikes.

1

The rise in government borrowing costs is putting serious pressure on household budgets in two key waysCredit: Getty

The pound has tumbled in response to the growing unease, highlighting investor concern over the UK’s economic stability.

At the heart of the issue are government bonds, known as “gilts,” which the government issues to borrow money.

These bonds offer investors a return, referred to as the “yield.”

In recent weeks, gilt yields have been rising rapidly, making it more expensive for the government to borrow.

This morning, yields soared further, with 30-year gilts reaching 5.72% – the highest level in nearly 30 years – while 10-year gilts climbed to 4.85%.

This spike signals that investors are nervous.

They are demanding a higher return to lend to the UK, worried about stubborn inflation and a gaping £51billion hole in the nation’s finances.

The rise in government borrowing costs is putting serious pressure on household budgets in two key ways

Firstly, it’s driving up mortgage rates.

The link between government gilt yields and mortgage rates is direct and unavoidable.

Lenders use “swap rates,” which closely track gilt yields, to set the prices of fixed-rate mortgage deals.

As these rates climb, fixed mortgages become more expensive.

Since August 1, two-year swaps have risen from 3.56% to 3.74%, while five-year swaps have gone from 3.63% to 3.83%.

Major lenders like Barclays have already started increasing rates, and even a small rise can add significantly to monthly payments on a typical £200,000 mortgage.

With swap rates continuing to rise in recent weeks, experts warn that mortgage rates are likely to increase further.

Separately, Chancellor Rachel Reeves faces a difficult challenge in her Autumn Budget, scheduled for November.

Higher borrowing costs are eating into public funds, and many economists believe tax increases will be necessary to fill the financial gap.

Although the government has promised not to raise income tax, national insurance, or VAT for “working people,” other tax measures are reportedly being considered.

One proposal is applying National Insurance to rental income, which critics fear could result in landlords passing on the cost to tenants through higher rents.

Another idea being debated is replacing stamp duty with an annual property tax, which could affect homeowners.

There are also rumours of reducing pension tax relief or cutting the tax-free lump sum, moves that could generate billions but might hurt savers.

Plus, there’s speculation about lowering the VAT threshold, which would bring more small businesses into the tax system.

This could increase their costs and potentially lead to higher prices for consumers.

Reeves is expected to make economic growth the centrepiece of her next Budget, warning that Britain’s economy is “stuck” and in need of bold solutions.

What can you do about it?

None of the proposed changes have been confirmed yet, and the government hasn’t ruled them out either.

However, any new measures won’t take effect until after the Budget in November.

It’s important not to make rash decisions based on speculation.

If changes are announced, you’ll have time to act and protect your finances before they come into effect.

For instance, if stamp duty is replaced by an annual property tax from a certain date, you could move house before the deadline to avoid the extra cost.

Similarly, if the government introduces capital gains tax on high-value properties, you might consider downsizing to a smaller home before the change is implemented.

Rob Morgan, chief analyst at Charles Stanley, said: “Taking pre-emptive action can outright backfire.

“Last year some people were concerned about restrictions around taking tax free cash from pension and took withdrawals they wouldn’t have otherwise made.

“This removed the money from a tax-efficient environment and potentially stored up tax issues that will come back to haunt them.

“Instead, it’s best to wait to see what happens, consider the consequences, and take advice as required before acting.”

Most of the proposed measures are likely to affect only the very wealthy, so you may not be impacted at all.

If you’re concerned, there are steps you can take to prepare and safeguard your finances.

Check your financial health

If you are worried about your finances then you should speak to a financial adviser.

They will be able to offer you advice about your situation and explain if any of the measures will affect you.

You can find one using unbiased.co.uk – but remember, you will pay a fee.

It’s good practice to sit down and take stock of your finances every six months and work out a plan.

Work out all your bills and outgoings and what income you have and factor in any changes, such as bills going up or new income streams.

Think about what you need to do to make the most of your money. For example, do you need to prioritise paying off debts or saving for a house deposit.

If your mortgage deal is coming to an end soon, act now.

Locking in a fixed rate could shield you from rising rates and market uncertainty.

Aaron Strutt, of mortgage broker Trinity Financial, said “For the moment there have not been significant price hikes but it’s probably worth locking in a mortgage rate if you are buying somewhere or due to remortgage, to try and keep away from any market turbulence.”

If you are coming to the end of a fixed deal, most lenders let you lock in a new rate up to six months beforehand, which can be worth doing.

If rates fall after you agree a new deal, some lenders will let you sign a new one at a lower rate.

How to get the best deal on your mortgage

IF you’re looking for a traditional type of mortgage, getting the best rates depends entirely on what’s available at any given time.

If you’re remortgaging and your loan-to-value ratio (LTV) has changed, you’ll get access to better rates than before.

Your LTV will go down if your outstanding mortgage is lower and/or your home’s value is higher.

A change to your credit score or a better salary could also help you access better rates.

And if you’re nearing the end of a fixed deal soon it’s worth looking for new deals now.

You can lock in current deals sometimes up to six months before your current deal ends.

Leaving a fixed deal early will usually come with an early exit fee, so you want to avoid this extra cost.

But depending on the cost and how much you could save by switching versus sticking, it could be worth paying to leave the deal – but compare the costs first.

You can also go to a mortgage broker who can compare a much larger range of deals for you.

Some will charge an extra fee but there are plenty who give advice for free and get paid only on commission from the lender.

You’ll also need to factor in fees for the mortgage, though some have no fees at all.

You can add the fee – sometimes more than £1,000 – to the cost of the mortgage, but be aware that means you’ll pay interest on it and so will cost more in the long term.

The average bank customer has around £10,000 in savings, according to Raisin.

If that £10,000 is kept in an easy access account earning 1.5% interest, it would generate just £150 in interest each year.

But switching to Cahoot’s 5% easy access account would boost that to £500, earning you an extra £350.

If your savings account pays less than the current inflation rate of 3.8%, it’s time to look for a better deal.

How can I find the best savings rates?

WITH your current savings rates in mind, don’t waste time looking at individual banking sites to compare rates – it’ll take you an eternity.

Research price comparison websites such as Compare the Market, Go.Compare and MoneySupermarket.

These will help you save you time and show you the best rates available.

They also let you tailor your searches to an account type that suits you.

As a benchmark, you’ll want to consider any account that currently pays more interest than the current level of inflation – 3.4%.

It’s always wise to have some money stashed inside an easy-access savings account to ensure you have quick access to cash to deal with any emergencies like a boiler repair, for example.

If you’re saving for a long-term goal, then consider locking some of your savings inside a fixed bond, as these usually come with the highest savings rates.

In a social media post on August 22 2025 the German Ambassador to India Dr Philip Ackermann said:‘New numbers are out! Almost 60,000 students from India are currently studying in Germany – a leap of 20 % over a year.’ He also said that public universities in Germany were a “great choice” due to their reputation and affordability.

The number of Indian students, surpass Chinese students for two successive years

In recent years, the number of Indian students studying in Germany has risen significantly. In 2018-2019, this number was estimated at a little over 20,000 but it has been growing steadily and in 2023-2024 it reached 49,000. Another important point is that Indian students emerged as the largest international student group — surpassing Chinese students — in Germany for the second year in a row. For long, India and China have been the largest contributors to the International Student Pool in the Anglosphere – US, UK, Canada and Australia. Apart from Canada – especially in the recent past — the number of students from China exceeded students from India in other nations in the Anglosphere. As ties between Washington and Beijing deteriorated, this began to change and the number of Indian students in US higher education institutions surpassed that of Chinese students in 2024.

Indian students and higher education in the US

With the US making several revisions to its student visa policies, the enrolment of Indian students has witnessed a significant decline. In July 2025, the number of Indian student arrivals was estimated at 79,000. This is a dip of 46%. Apart from the policy changes of the Trump administration, it is the delays in visa processing which are discouraging Indian students from pursuing higher studies in the US. One more step which could further discourage Indian students is the proposal of removing the Optional Practical Training (OPT) program. The OPT gives students, on an F-1 Visa, an opportunity to gain experience post their degrees often leading to full time employment and getting a work visa and residency eventually. This is especially handy for STEM students (it was the George W Bush Administration which had raised the duration of the OTP from 12 months to 29 months). In 2024, 200,000 students gained experience via the OPT. Apart from using the OPT for gaining work experience, it is also important since several of the individuals on F1 visas use the visa as a means for re-paying student loans. The US Department of Homeland Security is also planning some drastic changes to the existing F-1 visa rules.

The recent criticisms of the H1-B Visas by senior officials in the Trump Administration, and possible overhaul of the H1-B visa regime could also discourage several Indian students from going for higher studies to the US.

Indian students showing more interest in Germany

If one were to look at Indian students opting for European countries like Germany, it is important to bear in mind, that while some of the policies of the Trump administration may have encouraged students to look at alternative destinations. Germany by itself has been attractive for several reasons even earlier. The first is affordability. Public universities in Germany charge a nominal-fees (and no tuition fees). Second, the high academic standards of programs in the Sciences and Engineering, along with the fact that the programs are run in English. At a time when the US is thinking of removing the OPT, Germany provides an 18-month job seeker permit after completion of the degree. After this, students can apply for a Blue Card. Germany’s relaxation of citizenship rules and work visas could also add to the country’s attractiveness as

While several German Universities are reputed for having excellent departments of engineering, the country is also home to some top higher education institutions in humanities.

Both the employment opportunities as well as Germany’s growing emphasis on strengthening the country’s Research and Development – R &D eco-system – also could make it an attractive destination for international students.

Germany looking to draw Indian talent

In June 2025, the German Ambassador made a strong pitch for Germany pointing to the strengths it possesses as well as the predictability and stability in immigration policies:

“We are interested in Indian talent, we are interested in Indian brains. We are interested in those Indians who really want to achieve something, and Germany will always be a partner for such people. So, we are not erratic, we are not volatile, we are very, very steady,”

Apart from all the advantages discussed during the article, predictable and stable student visa policies are likely to be an important factor in drawing international students.

Conclusion

Given the strengths which Germany possesses – both in terms of academic standards and logistics – discussed in the article it is likely, that Germany has the potential of emerging as an important destination for higher education for international students – especially from India.

The cloud-native database specialist showed its artificial intelligence (AI) strategy is paying dividends.

Shares of MongoDB(MDB 34.70%) charged sharply higher on Wednesday, surging as much as 34.3%. As of 11:47 a.m. ET, the stock is still up 34%.

The catalyst that drove the database-as-a-service provider higher was the company’s financial results, which were far better than even the most bullish forecast.

Image source: Getty Images.

Blowing past expectations

For its fiscal 2026 second quarter (ended Jul. 31), MongoDB delivered revenue of $591.4 million, up 24% year over year, signaling that its strategy to address the booming demand for artificial intelligence (AI) is paying off. As a result, the company delivered adjusted earnings per share (EPS) of $1.00, compared to a loss per share of $0.70 in the prior-year quarter.

The results blew past management’s previous guidance and caught Wall Street off guard. Analysts’ consensus estimates were calling for revenue of $554 million and adjusted EPS of $0.67, so MongoDB sailed past even the loftiest expectations.

Further fueling investor enthusiasm was the company’s robust customer acquisitions. MongoDB added 2,800 net new customers, with the total growing to 58,300, up 18% year over year.

The company also continues to generate plenty of cash, with operating cash flow of $72.1 million and free cash flow of $69.9 million.

The AI wildcard

Over the past couple of years, MongoDB has been focused on providing its users with the tools they need to use AI. CEO Dev Ittycheria noted that while AI is not yet a “material driver” of the company’s growth, he noted that “enterprise uptake of AI is still early.” He went on to say that the “real enduring value” will come from custom AI solutions that will transform their businesses, and that MongoDB provides the tools that will help developers prosper.

Management gave investors other reasons to celebrate, as the company raised its full-year forecast for the second consecutive quarter. MongoDB is now guiding for fiscal 2026 revenue of $2.35 billion, or roughly 17% growth. The company also significantly increased its profit outlook to $3.68, up from $3.03 at the midpoint of its guidance. This shows the company is focusing on expanding its profit margins.

MongoDB stock isn’t cheap, selling for 11 times sales. However, that’s roughly half its average multiple of 20 since the company’s IPO in late 2017.

The market might have been irrationally exuberant, given the action camera maker’s recent performance.

Investors sure liked what they saw when peering through the viewfinder of GoPro(GPRO 35.54%) stock on Monday. Absent of any proprietary, share price-moving news, the company seemed to benefit from what appeared to be the latest meme stock rally.

With this considerable tailwind, GoPro shares closed the day almost 36% higher in price, numerous orders of magnitude better than the S&P 500‘s (^GSPC -0.43%) 0.4% drop.

A modern watercooler stock

GoPro is one of the latest crop of meme stocks, and as ever, that clutch of titles can rocket higher or plunge lower, depending on internet chatter.

Image source: Getty Images.

This has happened to GoPro before, and it seems as if it fueled Monday’s surge — after all, the company had no news of its own to report, nor did it disclose any developments in its operations (or with its stock) in any regulatory filing.

One key element that puts GoPro in a position where it can be very volatile on the market is its extremely low price (which was barely over $1.20 Monday morning before the rally kicked in). At such a level, it doesn’t take much to move a stock drastically either up or down, so even a little bit of online buzz can move GoPro sharply.

A concerning quarter

Although the company didn’t have any news to report today, it’s hit the headline in recent trading sessions. Earlier this month it published its second-quarter earnings report, revealing a worrying (18%) year-over-year decline in revenue, on the back of a 23% decline in action cameras, its main product category.

It also posted the latest in a string of bottom-line losses, although that latest deficit was narrower than that of the year-ago period.

Eric Volkman has no position in any of the stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.

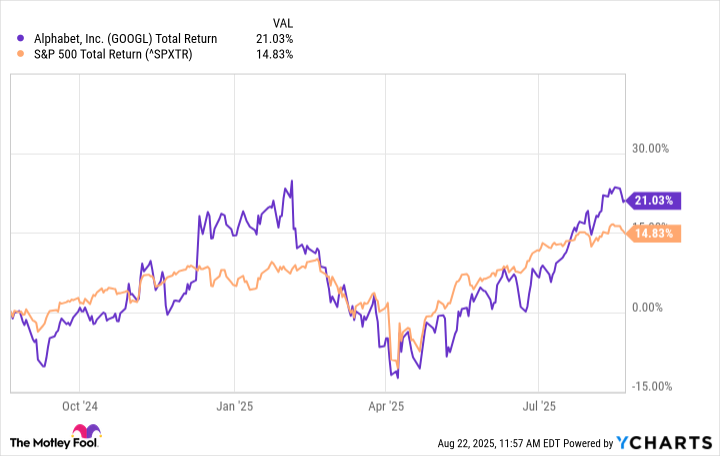

Meta will pay Alphabet $10 billion over six years for access to Google Cloud’s infrastructure.

The stocks of Google parent Alphabet (GOOGL 3.10%)(GOOG 2.98%) and Meta Platforms (META 2.04%) shot higher in Friday trading. Although most stocks rose because the Federal Reserve strongly hinted at a September cut in interest rates, another factor was likely the announcement of Meta’s cloud deal with Google, as reported by The Information.

Considering the $10 billion size of the deal, one has to assume it is critical, particularly to Alphabet. Still, considering the state of the artificial intelligence (AI) stock, it could serve as a much-needed catalyst for the company’s investors. Here’s why.

Image source: Getty Images.

Terms of the partnership

Under the terms of the deal, Meta will pay Google $10 billion over six years. In exchange, it will receive access to Google Cloud’s storage, server, and networking services, along with other products.

Meta has previously relied on Amazon‘s Amazon Web Services (AWS) and Microsoft‘s Azure for such services. The deal does not necessarily mean it will deal less with these companies. More likely, it speaks to Meta’s insatiable demand for cloud infrastructure as it seeks to become a major player in the AI space.

Additionally, Meta and Alphabet are each other’s largest competitors in the digital advertising market. And in the first half of 2025, 98% of Meta’s revenue came from digital ads. Hence, in a sense, it is remarkable that these two would become partners in a different business.

How it helps Alphabet

However, in another sense, this is a huge step forward for Alphabet’s future. In the first half of this year, Alphabet earned 74% of its revenue from the digital ad market, down from 76% in the same period in 2024. This is also by design, as Alphabet has purchased dozens of businesses unrelated to the digital ad market in its efforts to transition into a more diversified technology enterprise.

So far, Google Cloud is the only one of these enterprises to appear in Alphabet’s financials. It accounted for 14% of Alphabet’s revenue in the first two quarters of 2025, up from 12% in the same year-ago period.

Additionally, Google Cloud generated over $49 billion in revenue over the trailing 12 months, implying the $10 billion from Meta over six years will make up a relatively small portion of Google Cloud’s business.

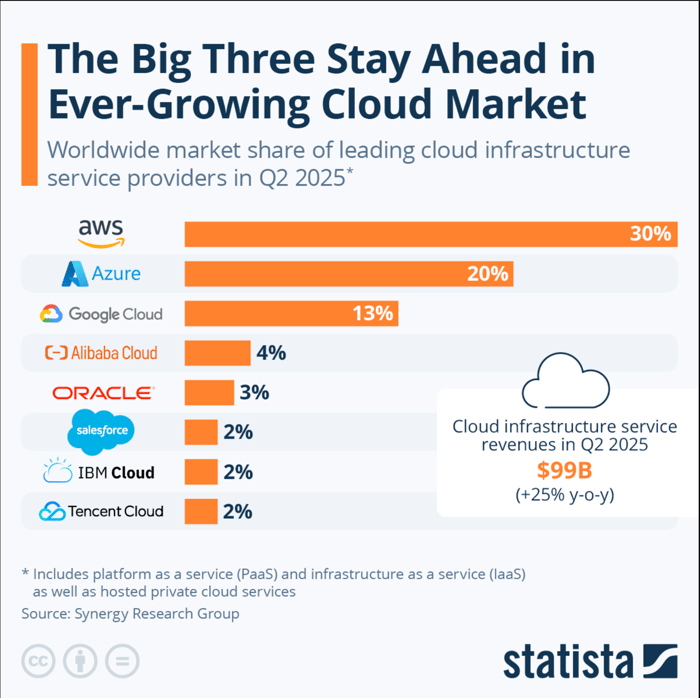

Nonetheless, the deal serves as a vote of confidence for Alphabet’s cloud business, one that continues to lag AWS and Azure in terms of market share.

Image source: Statista. Y-o-y = year over year.

The investor perspective is also crucial. Over the last year, Alphabet stock has outpaced the total returns of the S&P 500 by a significant but not eye-popping margin. However, it may help that Alphabet’s price-to-earnings (P/E) ratio of 22 is the lowest among “Magnificent Seven” stocks. Hence, the Meta deal could prompt investors to look more favorably upon that earnings multiple.

Furthermore, if the Meta deal prompts other companies to do more business with Google Cloud, it could provide a boost to its market share and, by extension, Alphabet stock.

The Meta deal and Alphabet stock

Ultimately, Meta’s deal with Google Cloud will more than likely take Alphabet stock a leg higher, but investors should expect the effects to be more indirect. Indeed, the deal is remarkable in that it serves as a boost for third-place Google Cloud and is notable since the two companies are direct competitors in each other’s largest enterprises.

Although $10 billion in added business over six years is substantial, Google Cloud generated $49 billion over the last 12 months. Thus, it is a significant but not game-changing boost to the enterprise.

However, the deal may make Google Cloud more attractive to prospective customers, and the low P/E ratio could attract more investors to Alphabet. In the end, those could become the more significant benefits of the deal.

Will Healy has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Alphabet, Amazon, Meta Platforms, and Microsoft. The Motley Fool recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

It’s always encouraging to get what appears to be good news from the FDA.

On a very good Friday for the stock market, Biohaven‘s (BHVN 6.33%) performance was exceptional. The clinical-stage biotech‘s share price inflated by over 6% that trading session thanks to regulatory news it delivered in the morning. Even the surging S&P 500 index couldn’t come close to that kind of increase, with its 1.5% gain on the day.

Regulatory progress

Biohaven revealed in a filing with the Securities and Exchange Commission (SEC) that it has been updated on the progress of its New Drug Application (NDA) for troriluzole. The company said that the Food and Drug Administration (FDA) informed it that an advisory committee meeting to discuss the submission at the regulator was no longer necessary.

Image source: Getty Images.

Troriluzole is a drug that targets spinocerebellar ataxia, a cluster of inherited and progressive neurological disorders that affect the body’s movement. The development and regulatory application process for the drug has been halting, with the FDA initially refusing to accept the company’s filing. Biohaven ran a new late-stage clinical trial and is using its data for the current NDA.

Although the cancellation of the advisory meeting implies the regulator has, in effect, already reached a decision, it might not necessarily be one favorable to the company. Investors are best advised to wait until the actual decision is rendered to make a decision on whether or not to buy this stock.

Good chance for success, apparently

Having said that, according to research from RBC Capital Markets analyst Leonid Timashev cited by Investor’s Business Daily, around two-thirds of applications where an advisory committee meeting is cancelled ultimately won approval (from 2019 until the present). Given that, the market’s very bullish reaction to the news is understandable.

Eric Volkman has no position in any of the stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.