Warren Buffett has spent decades championing the importance of Social Security benefits.

Warren Buffett has built a reputation for studying the landscape and spotting financial issues before others realize there’s a problem. Twenty years ago, at a 2005 Berkshire Hathaway meeting, Buffett was blunt: “I basically believe that anything that would take Social Security payments below their present guaranteed level is a mistake.”

Image source: Getty Images.

The problem has been brewing

Based on any retirement planning you’ve done, you’ll probably not be surprised that the Social Security trust is in serious danger of running dry. The program collects payroll taxes under the Federal Insurance Contributions Act (FICA). Both employees and employers contribute 6.2% of the employees’ wages, up to the annual wage base limit of $176,100.

The money collected today goes toward paying Social Security benefits to current beneficiaries. When the Social Security Administration (SSA) collects more than it pays out, the remaining money goes into the Old-Age and Survivors Insurance Trust Fund (OASI) and is invested in Treasury securities. When the SSA collects less in Social Security payroll taxes than it pays out, the SSA must dip into the trust fund for the money it needs to pay the benefits earned.

According to the SSA’s 2024 Trustees Report, the OASI trust fund is projected to become depleted in 2033, unless Congress intervenes to shore up the program. While several factors have played a role in draining the fund, demographics may be the most critical. In 1960, there were 5.1 workers for every Social Security recipient. Today, that number is just 2.8 and expected to continue falling.

The SSA cannot pay full Social Security benefits once the money invested in Treasury securities is gone. At that point, the Trustees say that Social Security benefits would be reduced by 23%.

Buffett’s proposals to get Social Security back on solid ground

Buffett has been consistent about recommending moderate changes to the program, including:

Remove the taxable earnings cap

As of 2025, Social Security taxes only apply to incomes up to $176,100. For example, a person who earns $400,000 annually only pays Social Security taxes on the first $176,100. No Social Security taxes are collected on the remaining $223,900.

Buffett believes that the U.S. should eliminate this cap so that higher earners can contribute more to the program. This approach would boost Social Security revenue significantly and is unlikely to affect the financial stability of wealthier taxpayers.

Slightly increase payroll taxes

No one enjoys a tax hike, which may help explain why politicians have been so hesitant to suggest them. Politicians want to be seen as the people who cut taxes. There’s only one problem with that: Cutting taxes isn’t always good for the long term. For example, President Donald Trump’s “Big, Beautiful Bill“ expanded the standard deduction for seniors and lowered how much can be collected in taxes on benefits.

Add that to the Social Security Fairness Act signed into law by President Joe Biden in early January 2025. The Social Security Fairness Act eliminated the Windfall Elimination Provision (WEP) and Government Pension Offset (GPO) rules. These two programs decreased the amount that over 3.2 million people — including teachers, police officers, firefighters, and federal employees — were eligible to receive in Social Security benefits.

While each tax break may have come as welcome news to most, the Committee for a Responsible Federal Budget (CRFB) found that they shaved a full year off the expected solvency timeline, meaning money is being drained from the Social Security trust fund at a faster rate than believed just last year.

Buffett suggests a slight boost in Social Security payroll taxes, saying even a modest hike would generate additional funds over time. In addition, a small tax hike would help secure the program’s financial stability without unfairly burdening workers or employers.

Raise the full retirement age (FRA)

In 1960, American men could expect to live to age 66.6 on average, and American women to age 73.1. Today, American men can expect to live to 77.2 on average, and American women to age 82.1. This increase in life expectancy means more years in retirement, and more Social Security benefits paid out. The SSA could stretch the Social Security trust fund further by raising the FRA.

Reduce Social Security benefits for wealthy retirees

Buffett, who once famously pointed out that his secretary paid a “far higher tax rate“ than Buffett himself, believes that the wealthiest retirees will do fine if their benefits are scaled back. According to Buffett, adjusting payments for high earners allows the SSA to direct more resources to those retirees who depend on their monthly benefits the most.

Given the number of Americans who collect Social Security, it’s fair to assume that many have done everything they can to maximize benefits and don’t want to see their benefits slashed. Warren Buffett has spent the past two decades offering potential fixes to the issue. Now, if Congress can get on board, a solution may be found.

A rare earth peer announced an expansion of its rare earth production operations.

Markets may be nudging slightly higher today, offering investors the hope of ending the week on a positive note, but the same can’t be said for rare earth stock USA Rare Earth(USAR -3.85%). While the company hasn’t reported anything negative, news related to a rare earth peer has USA Rare Earth investors heading for the exits.

As of 2:44 p.m. ET, shares of USA Rare Earth are down 3.5%, recovering from their earlier decline of 10%.

Image source: Getty Images.

Rare earth businesses in the U.S. are growing, and USA Rare Earth investors aren’t happy

Thanks to its holding in ReElement Technologies, American Resources (AREC) announced a 141% expansion of its critical mineral refining facility located in Indiana. With the expansion, the company now has near-term annual refining capacity of over 200 metric tons of ultrapure separated defense elements and rare earth oxides of 99.9% to 99.999% purity.

Nearing completion of its rare earth magnet production facility, USA Rare Earth has emerged as one of the key players among those involved in rare earth elements production. The company has drawn considerable interest from investors over the past year as President Trump has issued executive orders addressing a commitment to shoring up the domestic supply of rare earths.

Is now as good time to dig into USA Rare Earth stock?

Instead of digging deeply into the news from American Resources, investors in USA Rare Earth likely responded to the news with a knee-jerk reaction and trimmed their positions, surmising that the growth prospects of USA Rare Earth is now impeded. For USA Rare Earth shareholders, though, today’s announcement shouldn’t do much to sway them that the bull case is broken.

Of course, there are plenty of risks that remain for USA Rare Earth with the construction of its magnet production facility, and the company’s success is far from guaranteed. But if you were optimistic about the prospects of USA Rare Earth yesterday, nothing has changed. In fact, today’s pullback provides a great chance to build your position even further.

Scott Levine has no position in any of the stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.

The long-term data for stock market returns paints a clear picture.

The Vanguard Total Stock Market Index Fund ETF(VTI 0.21%) is one of the most popular exchange-traded funds (ETFs) on the planet. The fund has net assets of nearly $2 trillion.

With stock indexes hovering near all-time highs, many investors are worried that this historically successful ETF will struggle in the years to come. But there’s one critical piece of data that suggests otherwise.

This ETF remains a data-backed investment

The Vanguard Total Stock Market Index Fund ETF is a classic pick for savvy long-term investors. That’s because the ETF tracks the holdings of the CRSP US Total Market Index, which includes almost every type of company imaginable — everything from small-caps and large-caps to value stocks and growth stocks.

The ETF is incredibly diversified with more than 3,000 holdings, but investors should note that only U.S. companies are included. Many of those U.S. companies, however, have global operations, providing some level of international diversification.

Image source: Getty Images.

With an expense ratio of just 0.03%, the Vanguard Total Stock Market Index Fund ETF is one of the cheapest ways investors can get broad access to nearly the entire stock market. But with the indexes already at all-time highs, is this ETF still a smart pick? If your holding period is 20 years or more, the answer is absolutely. That’s because there has never been a 20-year period where the U.S. stock market has posted a negative return.

Of course, returns for any given 20-year period vary widely. But here’s a good example of how buying market indexes like this, even at their peaks, is a wise long-term decision. If you purchased shares of VTI in 2007 at their pre-cash peak, you still would have accumulated a 338% return over the next 18 years. So long-term investors can rejoice: The Vanguard Total Stock Market Index Fund ETF remains a solid pick for the decades ahead.

Ryan Vanzo has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Vanguard Total Stock Market ETF. The Motley Fool has a disclosure policy.

Tracking the S&P 500 is one of the simplest and most popular ways to profit from the stock market’s long-term growth.

If you want to invest in the stock market with little time and effort, a good strategy can be to simply “buy” the S&P 500 (^GSPC -0.50%). This benchmark index includes 500 of the biggest U.S. companies, and it’s a popular choice for many investors.

While you cannot invest in the S&P 500 directly, index funds that track its performance are widely available. Below, I’ll look at what kind of returns the index has historically averaged and how it has performed recently to build out a forecast of what a $20,000 investment in the S&P 500 might be worth after 20 years.

Image source: Getty Images.

The S&P 500 boasts a 10% annual return, but can that continue?

If you look at nearly a century of historical data, the S&P 500 has enjoyed an annualized growth rate of about 10% (including dividends). For 2025, it’s up 14% as of this writing, and that’s with the index already coming off strong years when its total return was more than 25% in both 2023 and 2024. The index has effectively been punching well above its weight for a while, which is why some analysts and investors worry the market may be in a bubble, and a slowdown may be coming.

For that reason, it’s important to brace for lower, more modest gains in the future. New investors may have become accustomed to these elevated returns, but the reality is there have been no shortage of years when the index’s returns have been in the single digits or even negative.

The good news is that regardless of what happens in any single year, over the long term, the S&P 500 is likely to rise in value. That’s why tracking it with an exchange-traded fund (ETF) such as the SPDR S&P 500 ETF (SPY -0.49%) can be a winning strategy.

What could a $20,000 investment in the S&P 500 be worth in the future?

I’m not going to try to predict the exact rate of return the S&P 500 will deliver over the next two decades. But I can show you what a $20,000 investment in the SPDR ETF may be worth at various points over the next 20 years based on a range of growth rates.

Year

8% Growth

9% Growth

10% Growth

11% Growth

12% Growth

5

$29,387

$30,772

$32,210

$33,701

$35,247

10

$43,178

$47,347

$51,875

$56,788

$62,117

15

$63,443

$72,850

$83,545

$95,692

$109,471

20

$93,219

$112,088

$134,550

$161,246

$192,926

Data source: Clculations by author.

Even at 8%, the value of your position can more than quadruple after 20 years to about $93,000. And you shouldn’t expect 11% or 12% annualized returns going forward, especially given the S&P 500’s hot streak in recent years. However, I included those bullish growth rates to illustrate how significant the gap in the final investment value can be, even when the difference is only a few percentage points.

This highlights why it’s important to go with a low-cost fund such as the SPDR S&P 500 ETF, where the expense ratio is only 0.09%. It’s crucial to keep those fees as low as possible so you can maximize your returns.

David Jagielski has no position in any of the stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.

Some business pivots are successful. So far, this company’s pivot hasn’t been one of them.

Is a recovery story in the works for Wolfspeed(WOLF -7.88%)? After all, the next-gen semiconductor maker says it’ll soon emerge from Chapter 11 bankruptcy protection with a much cleaner balance sheet; it also faces a promising market for the silicon carbide and gallium nitride products in which it specializes.

Perhaps it might even recoup some of the significant losses its shares have incurred over the years.

A dimming light

Across a five-year stretch, a $500 investment in what’s now Wolfspeed would have withered to only $16.42. This, combined with the company entering bankruptcy proceedings, has made it something of a meme stock.

Image source: Getty Images.

Wolfspeed pivoted its business in 2021, changing its name (from Cree) and eschewing the light-emitting diode (LED) products that had been its main focus since the 1993 founding.

Instead, it embraced technology based on the aforementioned materials, which promise greater efficiency and speed than conventional silicon solutions. Promise isn’t fusing with reality, however, as demand in the crucial yet ultracompetitive electric vehicle (EV) components space hasn’t been as strong as hoped.

The company consistently books bottom-line losses, with its generally accepted accounting principles (GAAP) net shortfall nearly quadrupling in its most recently reported quarter to $669 million from the year-ago frame’s less than $175 million. Net revenue also declined, sliding to $197 million from under $201 million.

Emerging from the den of bankruptcy

One piece of good news is that, earlier this month, Wolfspeed received approval for its plan of reorganization to emerge from bankruptcy. It reached an agreement with creditors to slice outstanding debt by around 70%, or approximately $4.6 billion, leading to a roughly 60% reduction in interest payments.

The considerable downside for current stock investors is that Wolfspeed’s existing equity will be eliminated, with current shareholders receiving a collective figure of merely 3% to 5% of new common stock.

So Wolfspeed’s future is cloudy at best, and it hardly looks like today’s investors will be tomorrow’s gainers. I feel this stock is too risky for a buy just now.

The plunge highlights high levels of leverage by crypto investors.

Cryptocurrency prices slumped Sept. 22 with Ethereum(ETH 0.01%) losing 9% in the early hours of Monday morning. The second-biggest cryptocurrency fell from almost $4,500 to $4,075, before finishing the day at $4,200. Bitcoin(BTC 1.56%) dropped 3% and the total crypto market cap slipped back below $4 trillion.

Crypto positions saw more than $1.6 billion in liquidations in 24 hours — the biggest liquidation this year, according to CoinGlass data. Ethereum was hardest hit with more than $500 million wiped out. It’s a reminder of the way excessive leverage in crypto can quickly snowball. The market moved against investors who had borrowed to fund bullish positions. As it did, their positions were forcibly closed, which added to the broader downward pressure.

Let’s dive in to find out what the rocky start to the week means for crypto investors.

What investors need to know about the sell-off

When cryptocurrency prices are rising, it’s often easy to forget about the risk involved. Dramatic shifts and liquidations remind us that this is still a relatively new and evolving asset class.

1. Cryptocurrency volatility hasn’t gone away

Bitcoin is still a volatile asset. That volatility has lessened as it has gained traction as a store of value and attracted institutional investment, particularly through exchange-traded funds (ETFs). According to Fidelity, Bitcoin was less volatile than shares of Netflix in the two years running up to March 2024. However, the volatility is still there.

This is even more so for Ethereum, which serves a different purpose than Bitcoin and has not yet benefited from the same inflows of corporate and institutional capital. Ethereum is starting to be viewed as the smart contract workhorse of crypto, supporting a wealth of stablecoin and decentralized finance applications. However, it is still more volatile than Bitcoin as this week’s dramatic price swing demonstrates.

2. Keep an eye on crypto leverage

Investing using margin and leverage involves using borrowed funds to take a larger position in an investment. It can work in different ways, but for many crypto investors, it involves depositing assets as collateral to increase purchasing power. As an investor, it can be risky because you could lose your collateral — known as liquidation — if the market doesn’t rise or falls.

On a broader level, leverage amplifies market activity. That’s why it’s concerning that the levels of crypto leverage are coming close to those of Q4 2021 and Q1 2022. An August Galaxy report showed that total crypto-collateralized lending increased to more than $53 billion in the second quarter of 2025. That’s a 27% increase from on the quarter before.

In 2022, we saw the way that excessive leverage can quickly spiral and exacerbate market volatility. Markets are cyclical by nature, and history shows us that cryptocurrency bull runs don’t last forever. When prices start to fall, as they did at the start of the week, those declines are magnified by the various forms of buying crypto using borrowed money.

There’s also growing concern about crypto corporate treasury companies, some of which are using debt to fund their Bitcoin and Ethereum purchases. Adding crypto to company balance sheets using borrowed money has become popular this year. The danger is that when prices fall, they may need to sell their crypto to service debts, causing prices to fall further.

Image source: Getty Images.

3. Bitcoin and Ethereum are still trending upward

Dramatic price swings are always unsettling, but it’s important to keep them in context. Bear in mind that both Bitcoin and Ethereum are still outperforming the S&P 500 — in spite of the recent sell off. As of Sept. 24, the S&P 500 has gained about 16% year over year. Bitcoin is up almost 77% and Ethereum increased 57% in the same time period.

Prepare for further turbulence

Crypto prices seem to have stabilized today, with Bitcoin holding its head over the $113,000 mark and Ethereum at almost $4,200. However, Bloomberg warns that the market is braced for further volatility. It says Bitcoin options traders are betting on two extremes — a slide to $95,000 or a rally to over $140,000, showing that we may yet see more dramatic price swings.

Bitcoin and Ethereum have rallied this year, buoyed by a crypto-friendly administration, changes in regulation, and — most recently — hopes for Federal Reserve interest rate cuts. Potential Securities and Exchange Commission approvals of spot altcoin ETFs may also give the industry a boost in the coming months. Even so, economic doubts and inflation concerns continue to weigh on prices. If further rate cuts do not materialize as anticipated, crypto prices may not be able to sustain recent gains.

As a long-term investor, one way to manage volatility is to use dollar-cost averaging, buying a set amount of crypto at regular intervals rather than in a lump sum. It’s also important that crypto only make up a small amount of your portfolio, and that you set clear goals to avoid making panic investment decisions.

Nvidia makes another aggressive move to control the AI market.

Nvidia(NVDA -0.73%) is no stranger to investing in its customers. The company has put billions to work to expand the artificial intelligence (AI) ecosystem, aiming for more growth and investment from its core growth market. The company’s latest deal with OpenAI — the maker of ChatGPT — is a prime example of this strategy.

Here’s what the deal between Nvidia and OpenAI means

The first thing to understand about this deal is that it is simply a letter of intent. That means the partnership is non-binding, with no legal obligation for either of the companies to follow through on the deal framework discussed below. Even if the deal is non-binding, however, the spirit of the partnership is clear: Nvidia and OpenAI will be working closely together to enable each other’s businesses.

Next, let’s discuss the figures you may have seen in the headlines. Nvidia, for example, has pledged to invest $100 billion into OpenAI. The details, however, paint a slightly different picture than the headlines. What the deal essentially outlines is OpenAI’s intention to purchase Nvidia hardware for a massive, multiyear infrastructure buildout. According to a press release, OpenAI intends to “build and deploy at least 10 gigawatts of AI data centers with NVIDIA systems representing millions of GPUs for OpenAI’s next-generation AI infrastructure.” In return, Nvidia will invest in OpenAI equity in tranches, with each funding tranche being initiated as the infrastructure gradually expands.

OpenAI gets two things from this partnership. First, it gets funding in the form of direct cash for equity. Second, it gets preferential treatment from Nvidia when it comes to technology sourcing. Nvidia’s chips are in high demand, at one point facing 12-month shipping delays. OpenAI has now secured a long-term strategic advantage, gaining the ability to scale its infrastructure with the best chips on the planet, chips that the competition may not be able to source.

Nvidia, meanwhile, gains an even stronger backlog. It locks in a huge customer for years to come. It also helps fund an accelerated buildout of AI infrastructure — another long-term tailwind for its business.

Image source: Getty Images.

Should you buy even more Nvidia stock?

This is the type of deal that only Nvidia and OpenAI could pull off. Both are industry heavyweights with sizable competitive advantages. By joining forces, both companies stand to gain even more ground on the competition.

Should you buy stock in Nvidia due to this deal alone? Probably not. The deal, as mentioned, is simply a signal of intent. Nothing is legally binding. Plus, the tie-up could draw the scrutiny of regulators. According to Reuters:

The scale of Nvidia’s latest commitment could attract antitrust scrutiny. The Justice Department and Federal Trade Commission reached a deal in mid-2024 that cleared the way for potential probes into the roles of Microsoft, OpenAI and Nvidia in the AI industry. However, the Trump administration has so far taken a lighter approach to competition issues than the Biden administration.

Even if there are changes to the deal due to regulators or external influences, investors should be very bullish simply about Nvidia’s ability to forge such a deal. It has a huge lead on the competition when it comes to real-world chip performance, access to capital, and industry influence. By making moves like this, the company is ensuring that its dominant market shares have the possibility of continuing far into the future. So while shares aren’t a buy simply due to the deal with OpenAI, investors should take this news as a strong positive for Nvidia’s future.

Ryan Vanzo has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Microsoft and Nvidia. The Motley Fool recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

OPENING the thick, posh envelope with an embossed school logo in her council house, single mum Sophie Goffin was shaking and unable to catch her breath.

This was no ordinary mail delivery. The contents of the letter would decide whether her little girl had been offered a life-changing place at a top-ranking private school for FREE.

5

Sienna Goffin went to private school for free thanks to a bursary

5

Sienna’s bursary included school trips in Year 4 and 5, and an overseas trip in Year 6

5

Sophie said applying to a private school can feel intimidating, but it is worth it

Sophie says: “It was a nerve-wracking moment. I was about to learn if my daughter was going to get a free private school education.

“When I read Sienna had been offered a full bursary, I screamed with joy. I will never forget the sense of pride I felt and the huge smile on my daughter’s face.

“It was like winning the lottery. Even today, I cannot believe it happened. She’d received a private education for free.”

Sophie, who runs her own cat care business, The Purry Godmother, and lives in Uxbridge, West London, could never have afforded the £30k a year plus expenses it costs to send a child to school.

But she believed that a private school would help support Sienna better.

Sophie said: “Sienna started reception in September 2016 at a local government school. She was extra bright and, in the first two years, hit her milestones early.

“I asked the school to give her extra work, but with large class sizes, she was held back slightly. She ended up helping other children instead of moving forward herself.

“If I didn’t act, she would have been bored and frustrated. So I focused on securing a fully funded bursary.”

Private schools, also called independent schools, are run outside government control and paid for by parents, while Grammar schools are state-funded but selective.

Applying to a private school can feel intimidating, Sophie admits, but she knew it was the right move for Sienna and so set about applying.

Exposing the dark side of black market gambling in Britain

She added: “It can feel overwhelming, but really it’s just about proving what you earn and showing your child is the right fit.”

Sophie contacted the Independent Schools Bursars’ Association and the Boarding Schools’ Association for guidance, then checked schools’ websites to see who still had bursary places.

She says: “Most scholarships are awarded on merit and achievement. They usually mean only a small discount.

“Bursaries are the golden ticket to elite private schools. They are means-tested, with bigger awards for lower incomes. Some schools also factor in talent in music or sport.”

Bursary or Scholarship – what’s the difference?

Scholarship: Awarded for talent or achievement – academic, sport, music or art. • Partial: Usually 5–10% off the fees, sometimes up to 25%. Covers tuition only. • Full: Rare. May cover full fees, but extras like meals, trips and uniforms are usually not included.

Bursary: Means tested, based on family income. The bigger the financial need, the bigger the award. • Partial: Covers a percentage of school fees, parents still pay the rest. Extras are usually extra. • Full: The golden ticket. Can cover all tuition plus extras such as meals, trips, uniforms, even spending money on overseas visits.

Finding the right setting

Sophie and Sienna visited Maltman’s Green Girls School in Gerrards Cross, which was within commuting distance for them.

The school takes girls from as young as two up to 11 and has been operating for more than 100 years.

Fees range from £3,210 a term for nursery up to over £8,000 a term, or £32,000 a year for Year 6 pupils.

Sophie says: “Sienna’s eyes lit up when we visited. It was an educational wonderland.

“The school had a pool, science labs, 3D printers, art and drama rooms, small class sizes and an amazing Special Educational Needs department. I knew she would flourish there.”

Sophie and Sienna’s father, a chef, 32, had to complete forms because the full bursary is awarded to parents with low incomes who could not normally afford to send their child to the school.

What a full bursary can include

All tuition fees covered – no charges for lessons or exams

Uniform – including shoes, sports kit and even the school’s distinctive extras (like hats or blazers)

Meals – free school lunches, and sometimes breakfast or after school snacks

Books and learning materials – everything from textbooks to art supplies

Trips – day trips, residentials and in some cases overseas visits

Spending money – some schools even provide pocket money for foreign trips

After school care – wraparound support at no extra costs

Specialist support – SEN services, music lessons or sports coaching if needed

Specialist Dance, music drama classes – various specialist facilities

Specialist sports -often included

Day Attendance or Boarding School – some schools offer boarding facilities others just day attendance

As part of the means testing, parents must provide earnings information, tax forms, and bank statements and are assessed regularly once their child receives a place.

She says: “Having all your financial information up to date is critical to your application.

“Sienna had to do a written assessment for English literature and maths, which helps the school assess her level.

“We also met with the school head, and Sienna had a chance to explain why she wanted to attend.

“Bursaries are highly competitive, and the final decision is made by a specialist committee.

“Waiting for the letter was a roller coaster. Everyone wants the best for their child. It all rests on the letter.

“Sienna wanted to go to the school, and I knew it would change her life dramatically.”

After three months, Sophie says the confirmation letter’s arrival in March 2021 was a “game changer.”

Sienna joined the Year three class in the 2021 summer term, proudly wearing the school’s distinct straw hat and its blue and green check uniform.

Sophie added: “Within ten minutes of arriving, another girl had said hello and invited her on an afternoon play date.

“A free private education can happen. Sienna is proof that the impossible is possible, no matter what your income is.”

Sienna’s mum Sophie

“The school pushed her abilities, and she started to thrive and shine.”

Sienna’s bursary included school trips in Year 4 and Year 5, and in Year 6, an overseas trip.

Sophie says: “That even included her spending money. School meals are included, free after-school care is offered, and you receive all-round support.

“For parents like me, it’s an education we could never afford but one our children deserve.

“During her three and a half years there, Sienna got to use an amazing computer kit, do photography, use the school pool, learn about coding, AI technology and use their 3D printer.

“I was amazed at the facilities and the friends she made.

“The smaller class sizes helped her learn at an even faster rate.”

Top five private schools for your children

Top 5 Private Girls’ Schools

St Paul’s Girls’ School – London — Fees up to £35,751 a year for day pupils.

North London Collegiate School – London — Fees up to £25,413 a year.

Guildford High School for Girls – Surrey — Fees up to £22,308 a year.

Wycombe Abbey School – Buckinghamshire — Fees up to £20,500 per term for boarders, £15,600 for day pupils.

The Godolphin and Latymer School – London — Fees up to £25,722 a year.

Top 5 Private Boys’ Schools

St Paul’s School – London — Fees up to £17,981 per term for boarding in the Senior School.

Eton College – Berkshire — Fees up to £63,300 a year.

Winchester College – Hampshire — Fees up to £52,500 a year for boarding.

Tonbridge School – Kent — Fees up to £16,946 per term for boarding.

Abingdon School – Oxfordshire — Fees up to £22,530 a year.

5

Sophie was impressed with the school’s facilities, which included a pool and 3D printer

5

Sienna is being home-educated but is still in touch with her private school friends

Sienna has now finished Year 6 and is being home-educated for her secondary education, but remains in contact with all her private school pals.

Sophie said: “I had only ever dreamt of her having access to that standard of education, and when it became a reality, I had to pinch myself.

“I was also shocked at how many parents are not aware that bursaries exist or that they may be eligible.

“It has been life-changing, and it proves that it isn’t always some other family that gets the gold ticket.

“Government schools suit many people, but for Sienn,a the system wasn’t working.

“I was also stunned that many of my friends had no idea bursaries existed or that they would be eligible.

“It is possible to win a bursary place. If you don’t get one the first year, keep trying.

“It’s the golden ticket to helping a child like Sienna learn at the speed she needs to and thrive.

“Many children do that at standard schools. I was lucky enough that Sienna secured a bursary place.

“A free private education can happen. Sienna is proof that the impossible is possible, no matter what your income is.”

List of private schools offering free places

TRY these big-name schools which offer ‘transformational bursaries’ of 100% or even more.

Benenden School – Princess Anne’s old school offers means-tested bursaries up to 110%, covering fees plus extras such as uniforms, trips). School fees are over £56,000 a year for boarding

Bolton School -14% of bursary recipients at Sir Ian McKellen’s old school pay no fees.

Christ’s Hospital – This West Sussex school with a Tutor uniform boasts the UK’s most generous bursary scheme; 665 out of 857 students are on bursaries, with nearly 300 receiving 90% off the fees.

Eton College – The alma mater of Prince William and Boris Johnson spends over £7m a year on bursaries, with the average subsidy being around 70% per student, while some places are fully funded.

Fettes College- Tony Blair’s former school, in Edinburgh, offers 100% means-tested bursaries for eligible pupils.

Gordonstoun – At King Charles’ old school, about 34% of students receive means-tested bursaries, some exceeding 100% with a top up for travel and uniform.

Latymer Upper School (London) – At Hugh Grant’s old school a quarter of students are on bursaries, ranging from 25% to 100% of fees.

Malvern College – Jeremy Paxman and C.S Lewis attended this school which offers means-tested bursaries of up to 110% of fees.

Manchester Grammar School (MGS) – At this former state grammar school, 1 in 6 pupils are bursaries and 85% of bursary holders pay nothing at all

Radley College – The Keys Award provides fully funded places (including extras such as uniform and trips). Currently there are 25 pupils on full bursaries.

Reigate Grammar School – Sir Keir Starmer’s old school offers bursaries up to 100%, often including uniform, meals, and travel.

Sevenoaks School – Orland Bloom’s old school has 28 pupils on full (100%) bursaries.

Shrewsbury School – Spends ~£4m annually on scholarships and bursaries, with some full awards.

Solihull School – Offers bursaries from 10% to 100%+ (including meals and trips).

St Catherine’s, Bramley – Means-tested bursaries up to 100%, including extras (uniform, iPad, travel, etc.).

St Edward’s School (Oxford) – Scholarships + bursaries can combine to cover up to 100% of fees at Florence Pugh’s old school.

St George’s School, Ascot – Offers means-tested bursaries up to 100%.

St Helen & St Katharine (Abingdon) – Offers bursaries up to 100% of fees.

St Hilary’s School, Godalming – In some cases, bursaries cover 100% of fees.

St James’ Senior Girls’ School (West Kensington) – Bursarial support up to 100% of fees.

St Mary’s, Ascot – Bursaries up to 100%, supported by school and charitable funds.

St Paul’s Girls – Provides bursaries to families with incomes up to £140,000, with some receiving 100% bursaries plus money for trips. The school has no uniform.

St Swithun’s School, Winchester – Offers means-tested awards up to 100% of tuition fees.

St Leonards School (Scotland) – Offers financial assistance up to 100% of fees.

Stowe School – Scholarships typically 5% fee remission, but means-tested bursaries can cover up to 100% of fees at Sir Richard Branson’s old school

Tonbridge School – Foundation Awards and bursaries can cover up to 100% of the over £44,000 a year fees at this school.

Wellington College – The Prince Albert Foundation offers 110% bursaries (fees + extras) with support extending until age 25. This school was attended by 1984 author Geoge Orwell and comedian Rory Bremner

Whitgift School – A quarter of students are on ‘significant’ bursaries at this school in Croydon with peacocks in the grounds. Nearly 50% get some form of aid. Some bursaries exceed 100% (including uniform, travel, trips).

Winchester College – Means-tested bursaries cover 5% to 100% of fees at Rishi Sunak’s old school, which has just started accepting girls.

Seeing one of your portfolio’s positions generate a 10-year return of 50,000% is truly mind-boggling. But this is exactly what Bitcoin(BTC -0.25%) has done (as of Sept. 17). A $2,000 starting investment in September 2015 would be worth $1 million today.

With such a fantastic historical return, it’s understandable if investors think that it’s too late to put money to work. But that’s a pessimistic view. Here’s the biggest reason you haven’t missed out on Bitcoin.

Image source: Getty Images.

Unsustainable financial situation

It’s safe to assume that the U.S. federal debt, now at $37 trillion, will keep increasing in the decades ahead. It doesn’t matter who’s in the White House. The country will continue to run massive fiscal deficits. For what it’s worth, the last surplus was in 2001.

This unfavorable trend supports ongoing growth in the money supply, as the government keeps borrowing to fund spending. Something must eventually break.

The counterargument is that because the U.S. has the biggest and most powerful economy, and the U.S. dollar is the global reserve currency, things can continue on this path. To be fair, unsustainable trends can last longer than people might think.

But the situation is becoming more fragile as time passes. Imagine if you kept opening new credit cards to pay off the balances of your old cards. This is financially reckless, but this is essentially what the U.S. government does.

Capital flowing to a scarce asset

Bitcoin has a fixed supply of 21 million units. No single entity has control over it. It transcends borders. And it’s permissionless. This makes it a unique asset for more capital to flow to, particularly as more money and debt keep being created in the financial system.

Therefore, as long as governments across the globe continue operating in fiscally irresponsible ways, Bitcoin will have uncapped upside.

Neil Patel has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Bitcoin. The Motley Fool has a disclosure policy.

Nvidia(NVDA -0.18%) has made an incredible ascent to the top of the stock market, and it’s in a league of its own as the only stock with a market cap above $4 trillion. It’s up 1,300% over the past five years, and it doesn’t look like it’s anywhere near done.

Its growth prospects are up for debate amid increasing competition and its sheer size, which makes it harder to report high percentage growth. Still, there are many reasons to believe in Nvidia’s future. Here’s one reason investors still have time to buy Nvidia stock.

Image source: Getty Images.

Hyperscalers are spending

There are several ways to envision Nvidia’s opportunity, and one of them is to analyze how its largest clients are spending money on its products.

Nvidia works with the largest cloud operators in the world, the hyperscalers like Amazon, Microsoft, and Meta Platforms. These companies are building out their large language models (LLM) and offering top artificial intelligence (AI) solutions to their millions of customers, who in turn are using these platforms to create the next generation of generative AI apps.

This is the AI revolution that’s changing how people do business, shop, pay, and more, and these hyperscalers need Nvidia’s powerful chips to drive their AI models.

Just take a look at how much these three companies are spending this year on capital expenditures, and you can see how Nvidia’s business is going to be a crucial part of this process for the foreseeable future. Amazon is spending at a run rate of $120 billion, Microsoft at $100 billion, and Meta at about $65 billion. These are accelerations from last year, and as companies require more power, those numbers are likely to keep going up. Nvidia doesn’t collect every dollar of these sales, but it dominates this market.

I wouldn’t bet on Nvidia offering the same kind of growth it has in the past over the next five years, but it’s still likely to beat the market and offer value for shareholders.

Jennifer Saibil has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Amazon, Meta Platforms, Microsoft, and Nvidia. The Motley Fool recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

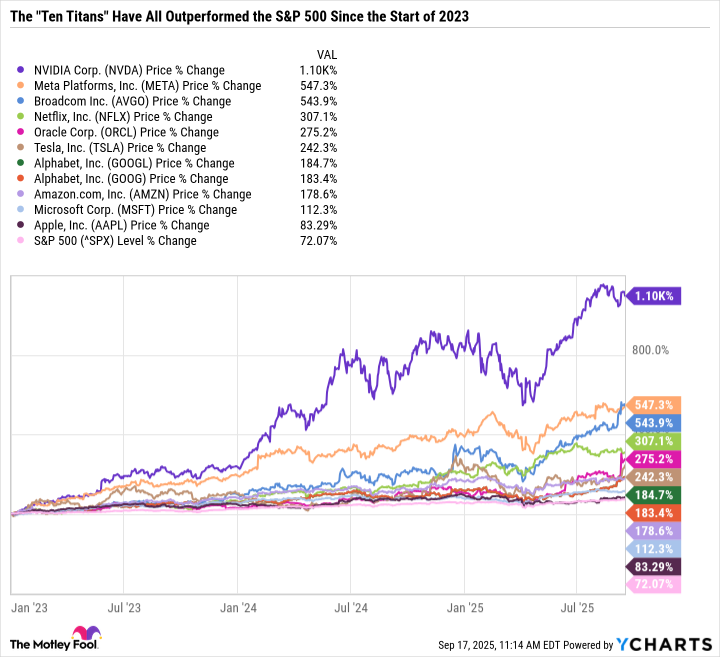

Broadcom and Oracle are crushing the S&P 500 and the “Magnificent Seven” in 2025.

Broadcom(AVGO -0.06%) and Oracle(ORCL 1.72%) have been two of the best-performing mega-cap growth stocks in 2025. As of this writing, Broadcom is up 19% since reporting earnings on Sept. 4, and Oracle soared 36% on Sept. 10 in response to its own blowout earnings and guidance.

Broadcom is getting closer to reaching a $2 trillion in market cap, and Oracle is knocking on the door of $1 trillion. Yet, you won’t find either of these stocks in the “Magnificent Seven,” which only includes Nvidia (NVDA -0.20%), Microsoft(MSFT 0.73%), Apple (AAPL 2.98%), Amazon(AMZN 1.04%), Alphabet(GOOG 0.69%)(GOOGL 0.65%), Meta Platforms(META -1.32%), and Tesla (TSLA 1.48%).

The “Ten Titans” corrects that error by adding Broadcom, Oracle, and Netflix (NFLX 1.38%) to the group. Combined, these 10 growth stocks now make up 39.1% of the S&P 500(^GSPC 0.28%).

Here’s how the Ten Titans have disrupted the stock market in just a few years and why their dominance in the S&P 500 can still impact your investment portfolio, even if you don’t own any of the Ten Titans outright.

Image source: Getty Images.

A lot has changed in less than three years

The S&P 500 is up a staggering 70% since the start of 2023, and a big reason for that is artificial intelligence (AI). Specifically, a few major companies are profiting from AI through semiconductors and associated networking hardware, software infrastructure, cloud computing, automation, and efficiency improvements.

The Ten Titans encapsulate this theme. The group is now double the market cap of China’s entire stock market and is largely responsible for moving the S&P 500 in recent years.

At the end of 2022, the Ten Titans made up 23.3% of the S&P 500. But since then, many of the Titans have increased in value several-fold, with Nvidia and Broadcom leading the pack.

The Ten Titans’ combination of size and rapid gains has redefined the structure of the S&P 500. Here’s a look at each company’s weight in the S&P 500 as of this writing.

Company

S&P 500 Weight (Sept. 16, 2025)

Nvidia

6.98%

Microsoft

6.35%

Apple

5.99%

Alphabet

5.08%

Amazon

4.13%

Meta Platforms

3.26%

Broadcom

2.78%

Tesla

2.25%

Oracle

1.43%

Netflix

0.87%

Total

39.12%

Data source: Slickcharts.

Oracle’s surge on Sept. 10 briefly pole-vaulted it to become the tenth-largest company by market cap. At that time, the nine largest names in the S&P 500 were all tech companies — a far cry from the days when the most valuable U.S. companies were from the oil and gas, consumer staples, financials, and industrial sectors.

The Ten Titans’ influence is growing

Even if you don’t own any of the Ten Titans stocks, their rise may still have ripple effects for your financial portfolio.

The biggest impact would be if you own index funds or exchange-traded funds (ETFs) with exposure to these holdings. Market-cap weighted passive funds that follow a growth theme or the general market will likely have sizable positions in the Ten Titans. And S&P 500 funds that mirror the index, like the Vanguard S&P 500 ETF, SPDR S&P 500 ETF, the iShares Core S&P 500 ETF will all have around 39% of their holdings in the Titans.

The sheer size of the Ten Titans means that the S&P 500 is no longer a balanced index, at least for now. Rather, it’s more of a growth index, similar to how the Nasdaq Composite is typically viewed.

The S&P 500 may contain hundreds of holdings, but its performance is now based on just a couple dozen companies. Investors looking for mid-cap or even large-cap stocks should venture outside the index because the S&P 500 offers little exposure to non-mega-cap names.

Navigating a Ten Titans-dominated market

The rise of the Ten Titans has benefited their shareholders, S&P 500 index fund investors, and folks with exposure to these stocks through ETFs. However, because they are so big, they will likely make the S&P 500 more volatile going forward.

Investors can offset the Ten Titans concentration by investing in value and dividend stocks that no longer make up a large percentage of the S&P 500. On the other hand, if you’re looking for a low-cost and straightforward way to get exposure to top growth stocks, the S&P 500 may be one of the simplest ways to do so.

Daniel Foelber has positions in Nvidia. The Motley Fool has positions in and recommends Alphabet, Amazon, Apple, Meta Platforms, Microsoft, Netflix, Nvidia, Oracle, Tesla, and Vanguard S&P 500 ETF. The Motley Fool recommends Broadcom and recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

Hi, and welcome to another edition of Dodgers Dugout. My name is Houston Mitchell. Don Stanhouse would have been a perfect fit for this bullpen.

Newsletter

Are you a true-blue fan?

Get our Dodgers Dugout newsletter for insights, news and much more.

You may occasionally receive promotional content from the Los Angeles Times.

The big news this week (besides the continuing collapse of the bullpen, which barely qualifies as news anymore): Shohei Ohtani removed after five innings while pitching a no-hitter. He was replaced by Justin Wrobleski to start the sixth with the Dodgers leading the Phillies 4-0. Wrobleski had not given up a run this month. He gave up five in the sixth inning. Whoops.

This was followed by fans on social media and a certain newsletter writer’s inbox to complain about Dave Roberts, how he doesn’t know how to handle a bullpen and how he needs to be fired for general incompetence. The fired part is silly, so we will ignore that. But did Roberts mishandle the situation?

If you were mad about it, ask yourself this: Would you have been mad if the Dodgers had won 6-0, or 6-2? If not, you aren’t mad that he caused Ohtani to miss out on a no-hitter, you are mad the Dodgers lost. Let’s reexamine the situation.

—Ohtani is coming off of his second Tommy John surgery and the Dodgers have been very careful with him. A couple of weeks ago, they decided, in consultation with Ohtani, that he would not pitch more than five innings the rest of the season.

—Roberts: “He’s two players in one. If something happens, then we lose two players. … We haven’t done it all year. So, I’m not gonna do it tonight.”

—Roberts had Wrobleski ready, and Wrobleski has been his best reliever this month. Who else was he supposed to bring in?

—Even if Roberts had let Ohtani pitch the sixth, there is no way he would have been left in for nine innings to complete a no-hitter. And we don’t know how the cards would have played out if Wrobleski had started the seventh inning instead of the sixth.

—The Dodgers fought back to tie the score, until Blake Treinen gave up a three-run homer in the top of the ninth. The same Treinen who was a stud in last year’s postseason.

—The culprit, as it has been all season, was the bullpen, not Roberts. Please tell me what reliable reliever should have pitched. Wrobleski was the most reliable guy on that day, and he failed. Roberts can’t throw the pitches for them.

—When Roberts calls down to the bullpen, he must be thinking, “How should we die today? Should I choose slow poison? Electric shock?” There are no great options. The bullpen is the problem. You could have the greatest manager in major league history, and it won’t matter if everyone in his bullpen is as unreliable as the Dodger bullpen is at this moment.

So, it’s hard to see what Roberts did wrong here. The anger some have at him is misplaced on this occasion.

Roberts’ biggest weakness has always been his handling of the bullpen, no question about it. But this one wasn’t on him.

A trend?

This isn’t the first time Roberts has removed a pitcher who had a no-hitter going into the fifth inning or beyond. A look (click on the result line to be taken to a box score of the game):

April 8, 2016: Ross Stripling, 7 1/3 no-hit innings against San Francisco in his major league debut

Number of pitches: 100

Stripling was coming off elbow surgery and had walked his fourth batter of the game when, with one out in the eighth, Roberts removed him. Reliever Chris Hatcher gave up a two-run homer to the next batter.

Roberts quote: “I wanted to see him throw a no-hitter. It’s a special moment. But we’re looking at the long term. We’re looking at the long view. Ross can help us win many more games. If it would have gone south and something would have happened, I would have never been able to live with myself. Because this is this kid’s livelihood. That’s my job.”

Stripling quote: “I have no ill feelings toward the decision one bit. I’m thinking that’s just the right choice.”

Sept. 10, 2016: Rich Hill, seven perfect innings against Miami.

Number of pitches: 89

Wary of exacerbating the blisters that were forming on Hill’s left hand, Roberts removed him after seven perfect innings. Reliever Joe Blanton gives up a hit with two out in the eighth. Blanton, Grant Dayton and Kenley Jansen finish off the shutout.

Roberts quote: “I’m very, very sensitive to his personal achievements. I really am. But nothing should get in the way, or compromise, our team goal…. I’m going to lose sleep tonight. And I probably should.”

Hill quote: “I get it. I’m very adamant about living in the moment. I did not want to come out of the game.” (Note: Hill was shown slamming a bat into the dugout bench after being told he was coming out). “But I think there’s a bigger picture here, and we all know what it is.”

May 4, 2018: Walker Buehler, six no-hit innings against San Diego

Number of pitches: 93

Buehler had thrown 93 pitches, one shy of his professional high, and was operating under an innings restriction because of Tommy John surgery. Tony Cingrani, Yimi Garcia and Adam Liberatore finished off the no-hitter.

Roberts quote: “He was totally complicit. Just understood where I was coming from, understood where the organization was coming from, what impact he has, how important he is for the organization this year, and going forward.”

Buehler quote: “Obviously, I wanted to keep going. But obviously, it’s above my pay grade. They made the choice. And for these guys to finish it out, it’s pretty cool…. It was the toughest conversation I’ve ever had.”

April 13, 2022: Clayton Kershaw, seven perfect innings against Minnesota

Number of pitches: 80

Coming off an elbow injury the previous season, and with a lockout shortened spring training, Kershaw was on an 80-pitch limit. Alex Vesia gave up a hit with one out in the eighth. Vesia and Justin Bruihl finished off the shutout.

Roberts quote: “There’s a lot of people that are cheering for the Dodgers, not only just for today and Clayton to throw a no-hitter, but for the Dodgers to win the World Series. For us to do that, we need him healthy.”

Kershaw quote: “I knew going in that my pitch count wasn’t going to be 100, let alone 90 or whatever. So I don’t know. It’s a hard thing to do to have to come out of the game when you’re doing that. But we’re here to win and this was the right choice.”

Sept. 16, 2022: Dustin May, five no-hit innings against San Francisco

Number of pitches: 69

May had some arm soreness after his previous start, prompting the team to push back his outing a few days and limit his pitch count. Vesia gave up a hit with two out in the sixth. Vesia, Caleb Ferguson and Phil Bickford finished the shutout.

Roberts quote: “Getting him out of the game, feeling good, is the win. Considering how he threw the baseball the last couple times, building off tonight and [knowing he’s] going on regular rest his next turn, it was the smart decision.”

May quote: “I didn’t even realize I had a no-hitter going.”

June 16, 2023: Emmet Sheehan, six no-hit innings against San Francisco in his major league debut

Number of pitches: 89

Sheehan had been rushed up from double-A to make the start because of injuries. He was averaging fewer than five innings a start in the minors and had never pitched in more than six innings in a game in the minors. He was replaced by Brusdar Graterol, who gave up two runs, then Victor González gave up three runs and Vesia two runs in the loss.

Roberts quote: “I was actually contemplating it after five innings, given the usage he’s had. But where the state of the ‘pen has been, I was trying to squeeze another inning. So to get him through the sixth, I thought was huge.”

Sheehan quote: “To have the Dodger fans and my family behind me, I couldn’t have asked for a better debut. Besides a Dodger win.”

Sept. 21, 2023: Emmet Sheehan, 4 2/3 hitless innings against San Francisco

Number of pitches: 93

It was a tough outing, as Sheehan walked four, hit a batter and gave up a run on a bases-loaded walk. Vesia replaced Sheehan in the fifth, and the first hit was a home run by Joc Pederson off Vesia with one out in the sixth. Shelby Miller, Ryan Brasier, Joe Kelly and Evan Phillips finished off the victory.

Roberts quote: “I think when he got to that fifth inning, there was a little bit of running low on the fuel in the tank, some close misses. … But he pitched a heck of a ballgame.”

Sheehan quote: “I think I definitely build confidence every start.”

Sept. 8, 2025: Tyler Glasnow, seven no-hit innings against Colorado

Number of pitches: 103

Glasnow was pitching for the first time in 10 days because of a sore back. He gave up a run in the second inning on a walk, stolen base, a deep fly ball advancing the runner to third, and a sacrifice fly. He stuck out 11. Blake Treinen pitched a perfect eighth. Tanner Scott gave up a leadoff double in the ninth before getting the save.

Roberts quote: “I do think that there’s certain times, if [the starters] give me the opportunity as far as efficiency and how their stuff is playing, to push them a little more.”

Glasnow quote: “My pitch count was pretty high. I don’t know how many pitches I was going to be allowed to throw. Obviously I want to stay in, no matter what my pitch count is, but given my, like, track record, I kind of understand why. I respect the decision.”

Sept. 16, 2025: Shohei Ohtani, five no-hit innings against Philadelphia

Number of pitches: 68

Ohtani was limited to five innings because he had his second Tommy John surgery in 2023. He was relieved by Justin Wrobleski, who gave up five runs in the sixth, and Edgardo Henriquez, who gave up a run in the sixth. After scoreless innings by Jack Dreyer and Anthony Banda, Blake Treinen gave up three runs in the ninth.

Roberts quote: “We’ve been very steadfast in every situation as far as innings for [Ohtani’s] usage — from one inning to two innings to three to four to five. We haven’t deviated from that. He wasn’t going to go back out.”

Ohtani quote: “The decision of whether to take me out is something I leave completely to the manager.”

The postseason

Here’s how the postseason race pans out after Wednesday’s games:

Wild-cards 4. Chicago, 88-64 5. San Diego, 83-69 6. New York, 78-74

7. Arizona, 77-76 8. San Francisco, 76-76 9. Cincinnati, 76-76

The Phillies have clinched the AL East title. The Brewers and Cubs have clinched a playoff spot. Washington, Pittsburgh amd Colorado have been eliminated from playoff contention.

AL 1. Toronto, 89-63 2. Detroit, 85-67 3. Houston, 84-69

Wild-cards 4. New York, 85-67 5. Seattle, 83-69 6. Boston, 83-69

7. Cleveland, 80-71 8. Texas, 79-74 9. Kansas City, 76-76

Baltimore, Minnesota, Chicago, the Athletics and the Angels have been eliminated from playoff contention.

The top two teams in each league get a first-round bye. The other four teams in each league play in the best-of-three wild-card round, with No. 3 hosting all three games against No. 6, and No. 4 hosting all three against No. 5.

The division winners are guaranteed to get the top three seeds, even if a wild-card team has a better record.

In the best-of-five second round, No. 1 hosts the No. 4-5 winner and No. 2 hosts the No. 3-6 winner. That way the No. 1 seed is guaranteed not to play a divisional winner until the LCS.

Up next

Thursday: San Francisco (Logan Webb, 14-10, 3.34 ERA) at Dodgers (Yoshinobu Yamamoto, 11-8, 2.66 ERA), 7:10 p.m., Sportsnet LA, AM 570, KTNQ 1020

Friday: San Francisco (*Robbie Ray, 11-7, 3.50 ERA) at Dodgers (*Clayton Kershaw, 10-2, 3.53 ERA), 7:10 p.m., Apple TV+, AM 570, KTNQ 1020

Saturday: San Francisco (Kai-Wei Teng, 2-4, 6.41 ERA) at Dodgers (Tyler Glasnow, 3-3, 3.06 ERA), 6:10 p.m., Sportsnet LA, AM 570, KTNQ 1020

Sunday: San Francisco (TBD) at Dodgers (Emmet Sheehan, 6-3, 3.17 ERA), 1:10 p.m., Sportsnet LA, AM 570, KTNQ 1020

Nineteen years ago today, the Dodgers hit four home runs in the bottom of the ninth to tie San Diego, win it on Nomar Garciaparra‘s home run in the 10th. Watch and listen here.

Until next time…

Have a comment or something you’d like to see in a future Dodgers newsletter? Email me at [email protected]. To get this newsletter in your inbox, click here.

A handful of companies are driving the S&P 500’s push to all-time highs, but risks remain.

The S&P 500 closed Sept. 12 up 12% year to date, 62% over the last three years, and 97% over the last five years. Mega-cap growth-focused companies are largely responsible for driving the index to new heights.

The “Ten Titans,” which includes Nvidia, Microsoft, Apple, Amazon, Alphabet, Meta Platforms, Broadcom, Tesla, Oracle, and Netflix, now makes up over 39% of the S&P 500. And the technology sector alone makes up 34% of the index.

Here’s how the S&P 500 being dependent on the performance of a single sector impacts the broader market and your financial portfolio — and is a low-cost and straightforward way to bet on the continued dominance of tech stocks.

Image source: Getty Images.

Tech is even more dominant than it appears

The S&P 500 has a high concentration in the tech sector, namely because of just a handful of stocks. Nvidia, Microsoft, and Apple collectively account for approximately 20% of the S&P 500. Throw in Broadcom and Oracle, and that number jumps to close to 24%. So, nearly a quarter of the index is in just five tech stocks.

Alphabet and Meta Platforms are often thought of as big tech companies, but they are in the communications sector, along with Netflix.

The tech sector, plus these five companies, makes up 48.7% of the S&P 500. So, as big as the tech sector is, purely based on the companies that are classified as tech stocks, the real reach of tech-focused companies is far larger.

Let the S&P 500 work for you

The S&P 500’s concentration in the tech sector has expanded its valuation and made it more of a growth-focused index. This can pay off with outsized gains if tech keeps outperforming, but it can also lead to more volatility.

During the worst of the tariff-induced stock market sell-off in April, the Nasdaq Composite fell 24.3% and the S&P 500 also got crushed, falling as much as 18.9%. So while the S&P 500 used to be led by consumer staples, industrial, and energy companies, it has now become like a lighter version of the Nasdaq.

Any investor with exposure to index funds or market-cap-based exchange-traded funds (ETFs) will be impacted by this change. An S&P 500 index fund may seem diversified at first glance, with over 500 industry-leading companies. But the reality is that the S&P 500 is really betting big on just a handful of companies. This presents a dilemma for risk-averse investors, but an opportunity for risk-tolerant investors.

Risk-averse investors can reduce their dependence on mega-cap tech companies by mixing in value and dividend stocks or value-focused ETFs. Many low-cost ETFs have virtually the same expense ratio as an S&P 500 index fund, meaning there’s next to no added cost for picking an ETF that better suits your investment objectives.

However, some investors may feel that it’s best not to fight the market’s momentum, and if anything, lean into it. The Ten Titans are massive, but they are also extremely well-run companies with high-margin businesses and multi-decade runways for future growth. So some folks may cheer the fact that these companies have gotten so large and are dominating the S&P 500.

In that case, buying an S&P 500 index fund may be more interesting. Or even a sector-based fund like the Vanguard Information Technology ETF, which has a staggering 53.2% invested in Nvidia, Microsoft, Apple, Broadcom, and Oracle.

Navigating a tech-driven market

As an individual investor, you don’t have to measure your own performance against an index like the S&P 500. Rather, it’s best to invest in a way that suits your risk tolerance and puts you on a path to achieving your investment goals.

Regardless of your investment time horizon, I think it’s important for all investors to be aware of the current state of the S&P 500 and what’s moving the index. Knowing that so much of the index is invested in tech-focused companies explains why the S&P 500 has such a low dividend yield and a higher-than-historical valuation.

Put another way, the U.S. stock market is being increasingly valued for where its top companies could be years from now rather than where they are today. And that puts a lot of pressure on leading growth stocks to deliver on earnings and capitalize on trends like artificial intelligence and cloud computing.

Daniel Foelber has positions in Nvidia. The Motley Fool has positions in and recommends Alphabet, Amazon, Apple, Meta Platforms, Microsoft, Netflix, Nvidia, Oracle, and Tesla. The Motley Fool recommends Broadcom and recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

We’re about a month away from an official number, but estimates for next year’s COLA are moving higher.

Social Security may be the most valuable retirement asset most Americans have. The pension for retired workers accounted for 20% of families’ total wealth in 2022, according to a study by the Congressional Budget Office. That’s based on a calculation valuing all future payments at present value.

Those future payments get a boost every year, which could make them even more valuable to Americans. The annual cost-of-living adjustment (COLA) helps benefits keep up with inflation. And while we won’t have the official 2026 COLA number until mid-October, it looks like it’ll come in higher than what analysts anticipated at the start of the year.

But a bigger COLA isn’t necessarily reason for Social Security recipients to celebrate. Here’s what retirees need to know.

Image source: Getty Images.

What’s pushing the 2026 COLA higher?

The annual COLA is based on a standard measure of inflation published every month by the Bureau of Labor Statistics called the Consumer Price Index for Urban Wage Earners and Clerical Workers, or CPI-W.

The CPI-W is one of several Consumer Price Index measurements the government publishes. The BLS surveys thousands of businesses and households across the country to collect pricing data on over 200 line items. Those prices are then indexed to a standard price from when the BLS first started collecting data, and weighted according to typical spending patterns of the group the index is supposed to follow. In the case of the CPI-W, the basket of goods represents the spending of working-age adults living in cities.

The Social Security Administration calculates the COLA by taking the average year-over-year increase in the CPI-W during the third quarter, i.e. July, August, and September. The BLS just published August’s CPI numbers on Sept. 11, with the CPI-W climbing 2.8% year over year. That follows a 2.5% increase in July. The final reading to determine the 2026 COLA will come out on Oct. 15.

Based on expectations for that reading, both The Senior Citizen’s League and independent analyst Mary Johnson have published their expectations for next year’s COLA. The former expects it to come in at 2.7% while the latter expects retirees to receive a 2.8% bump. Both estimates are higher than the 2.5% initial estimate The Senior Citizen’s League published before the start of the year.

The reasons for a higher COLA are bad news for 70 million beneficiaries

A bigger-than-expected raise is usually great news for those receiving it, but in the case of Social Security’s 70 million beneficiaries, it signals a challenging economic environment.

The biggest challenge is that the CPI-W doesn’t perfectly match the spending of most seniors. Most people don’t spend their money in retirement the same way they did when they were working age. They probably commute less and spend less on new clothing. They probably have different dining habits. And it’s almost certain that their medical bills have climbed higher as they grow older.

To that end, some of the biggest expenses seniors face are climbing faster than the overall CPI-W numbers. Medical care services were notably 4.2% higher this August than the year before. While gasoline prices were down, utilities were way up. Shelter expenses climbed 3.6%. Despite a 2.7% or 2.8% raise coming in January, most seniors have seen their real cost of living climb much more over the past year.

Rising medical costs are most prominently seen in the Medicare Trustees’ estimate for next year’s Medicare Part B premium. They expect the program will have to charge a standard monthly premium of $206.20 next year, an 11.5% increase from 2025. For those keeping track, that far outpaces the expectations for Social Security’s COLA. Beneficiaries age 65 and older enrolled in Medicare will see that amount come right out of their new monthly payments.

The Senior Citizens League contends this situation isn’t unique to this year’s COLA. It ran a study that estimates the buying power of someone’s benefits who started Social Security in 2010 has decreased 20% through 2024.

The best economic environment for Social Security has historically been slow, steady, and predictable inflation. Under the current administration, which has gone back and forth on trade policies numerous times since the start of the year, prices have become anything but predictable. While many businesses have taken preemptive steps to curb and delay the impact of tariffs, the costs will eventually get passed through to consumers. That could result in even more pain for those on a fixed income next year.

While a 2.7% or 2.8% raise might be bigger than anticipated, many seniors may find that it doesn’t go far enough next year.

Ripple’s grueling battle with the Securities and Exchange Commission is officially over.

In 2020, the U.S. Securities and Exchange Commission (SEC) sued a company called Ripple, alleging it was in breach of financial securities laws for the way it was issuing its cryptocurrency token, XRP(XRP 1.08%). The lawsuit threatened to derail Ripple’s business model, and it suppressed the price of XRP for years.

But everything changed when President Donald Trump was reelected last November. He promised to make America “the crypto capital of the world,” which involved taking a friendlier approach to regulation. He appointed crypto-advocate Paul Atkins to run the SEC, and the agency has since withdrawn from several active cases against industry giants like Binance and Coinbase.

The SEC also dropped its case against Ripple in August, bringing the brutal five-year legal battle to an official end. Here’s what might be in store for XRP from here.

Image source: Getty Images.

Why the SEC sued Ripple

Ripple created a unique payments network called Ripple Payments. It facilitates instant cross-border transactions by enabling global banks to deal with one another directly, no matter what existing infrastructure they use. Without Ripple Payments, banks using the SWIFT (Society of Worldwide Interbank Financial Telecommunication) network would have to use an intermediary to send money to banks that don’t use the system, delaying payments by several days.

Ripple created XRP as a bridge currency to standardize each transaction within Ripple Payments. For example, an American bank might send XRP to a European bank rather than sending U.S. dollars, cutting out costly foreign exchange fees. The cost of a single transaction using XRP is typically 0.00001 of a token, which is a fraction of one U.S. cent.

XRP has a total supply of 100 billion tokens. There are 59.6 billion in circulation, and the rest are controlled by Ripple, which gradually releases them to meet demand. As a result, XRP is a centralized cryptocurrency. Decentralized cryptocurrencies like Bitcoin(BTC 0.08%) aren’t controlled by any person or company, and they are typically earned through a process called “mining.”

That’s why the SEC sued Ripple in 2020. The regulator argued that XRP should be classified as a financial security, just like stocks and bonds, which are also issued by companies. This would have forced Ripple to operate under a very strict regulatory framework, potentially derailing its business model.

In August 2024, a judge issued a ruling that mostly favored Ripple. The SEC lodged an appeal which could have dragged the legal battle on for several more years, but the Trump administration’s pro-crypto agenda changed things. The Atkins-led SEC officially dropped the appeal last month, formally closing the case.

Here’s what might happen next

XRP hit a new record high in July for the first time in seven years, in anticipation of Ripple’s settlement with the SEC. Bullish sentiment was also fueled by the approval of a new exchange-traded fund (ETF) called the ProShares Ultra XRP ETF on July 18. It invests in futures contracts, so it doesn’t own any XRP directly. But investors are speculating that regulatory approval for spot ETFs could follow, and those funds would start buying up XRP tokens.

There is some precedent, because futures-based Bitcoin ETFs came before spot ETFs, so investors are hoping XRP follows the same path. This proved to be very bullish for Bitcoin because many investors already viewed it as a legitimate store of value, so ETFs gave financial advisors and institutions a safe, regulated way to own it.

I’m not convinced that spot ETFs would have the same effect on XRP, because it doesn’t have a proven reputation as a store of value. It’s a bridge currency in the Ripple Payments network, and ETFs wouldn’t improve that use case at all.

That brings me to a crucial point. Ripple Payments supports the use of fiat currency, so banks don’t have to use XRP. This means that the success of the network won’t necessarily lead to a higher value per token over the long term.

Therefore, if Ripple Payments isn’t a reliable value creator for XRP, and ETFs fail to become a tailwind like they are for Bitcoin, then volatility is likely to be the overriding theme from here. When XRP hit its previous record high in 2018, it plunged by more than 90% over the following year.

The token is in a better position today, but I don’t see a clear fundamental case for sustainable long-term upside from here, which leaves investors exposed to potential price corrections in the future.

Anthony Di Pizio has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Bitcoin and XRP. The Motley Fool recommends Coinbase Global. The Motley Fool has a disclosure policy.

Your retirement budget isn’t ready until you’ve accounted for this.

You’re ready for a change of pace — not just leaving the workforce, but moving to another state or country in order to start fresh. While exciting, you’re probably also prepared for some challenges, like learning your way around your new neighborhood and coming up with a new retirement budget.

Though you might not expect it, you could also face Social Security challenges that affect your benefit delivery or how far your checks go. Fortunately, you can minimize the difficulty these issues pose by planning for them well in advance.

Image source: Getty Images.

Moving to another state

Moving to another state won’t change the monthly Social Security check you’re entitled to, whether you’re receiving a retirement or spousal benefit. But it could affect how far your checks go. For example, if you move from a city with a high cost of living to a rural area where living expenses are cheaper, you might find that your checks go further than they would in your current city. On the other hand, if you move to a pricier area, you may have to pay for more of your expenses out of your own pocket.

Moving could also put you at risk of or help you avoid state Social Security benefit taxes. Only nine states still have these, and each has its own rules that determine who owes these taxes. It’s possible to live in a state with a Social Security benefit tax and not pay any state taxes on your checks. But it’s worth reaching out to your new state’s department of taxation or an accountant in that state to learn how it could affect your tax bill.

You could also find yourself owing federal Social Security benefit taxes wherever you go. These depend on your provisional income — your adjusted gross income (AGI), plus any nontaxable interest you have from municipal bonds and half your annual Social Security benefit. If you’re forced to spend more due to a higher cost of living in your new home, this could increase your AGI and your provisional income, potentially forcing you to pay more in federal income taxes.

Moving to another country

If you decide to move to another country, you sidestep the issue of state Social Security benefit taxes. Depending on where you go, you might also be able to secure a lower cost of living to help your benefits go further.

You will still be responsible for paying federal Social Security benefit taxes if your provisional income is high enough. And you could also run into an accessibility issue if you retire in certain countries.

The Social Security Administration can pay you via direct deposit or a prepaid debit card in most parts of the world. However, if you retire in the following countries, you may not be able to receive your benefit payments:

Azerbaijan

Belarus

Kazakhstan

Kyrgyzstan

Tajikistan

Turkmenistan

Uzbekistan

You may be able to petition the Social Security Administration to make an exception for you if you agree to certain restricted payment terms.

This isn’t an option for those who choose to retire in Cuba or North Korea, however. There, you cannot get Social Security benefits at all.

If you retire in a country where the U.S. government won’t send Social Security checks, you may still be able to receive all your back payments if you later move from that country to a place where the Social Security Administration can send benefits again.

It’s best to contact the Social Security Administration directly if you have any questions about how your move could affect your Social Security checks. This way, you’ll be able to get a personalized answer and then you can adjust your budget accordingly.

As the consumer investment world grows, the bank has a lot to gain.

Bank of America(BAC 0.71%) is one of the largest banks in the world, operating in the U.S. and more than 35 countries worldwide. By market cap, it’s the second-most valuable bank in the world, trailing only JPMorgan Chase. In the past five years, Bank of America has outperformed the S&P 500, with total returns close to 125% in that span, compared to the index’s 112% (through Sept. 12).

Even with Bank of America’s market-beating returns over the past five years, the next five years could continue the same momentum. The reason comes down to one factor: its consumer investment business.

Image source: Getty Images.

The consumer investment business involves standard brokerage accounts, wealth management, and financial advisory services. In the fourth quarter of 2024, Bank of America’s consumer investment assets crossed the $500 billion mark for the first time in the company’s history.