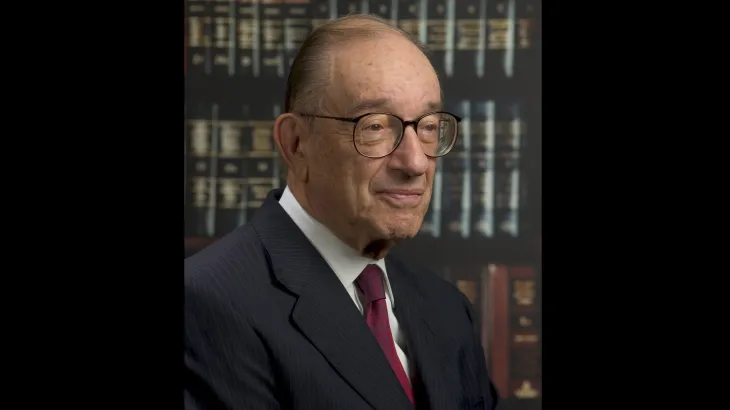

Alan Greenspan, one of the most influential economic policymakers in modern US history, has died aged 100. Greenspan led the Federal Reserve for nearly two decades under four presidents, overseeing a long period of economic growth but also faced criticism linked to the 2008 financial crisis.

WASHINGTON — It is no secret that a lack of job creation has emerged as a pivotal election issue. But a new Los Angeles Times Poll suggests that Americans’ pocketbook concerns extend well beyond the labor market, and the public thinks that Democratic presidential candidate John F. Kerry would better look out for their financial futures than would President Bush.

Asked to name the candidate who would be “best at protecting the financial security of the average American,” 47% named Kerry, while 34% picked Bush.

Among independents, a group that could play a crucial role in determining the winner of the presidential election in November, the gap was even wider: 49% for Kerry and 26% for Bush.

Those polled also view the Bush White House as much more aligned with business interests than the interests of ordinary workers, and they express widespread doubts about the integrity of corporate America.

A 63% majority said the president was more concerned about corporations, while 21% said he was more concerned about workers. The view that the president sides with big business over rank-and-file workers has become more prevalent over time. In an August 2002 Times Poll, 55% felt that way.

The results suggest that the economic battleground in the presidential election campaign is taking an untraditional shape that transcends meat-and-potatoes issues such as employment and price levels. These days, people are also concerned about corporate scandal and the integrity of the financial markets — and the way their leaders are dealing with these matters.

“This poll tells me that Bush’s economic troubles are of the new post-inflation, post-unemployment form,” said Samuel L. Popkin, a UC San Diego political scientist and a Democrat.

It further indicates that “Bush hasn’t been able to convert military security into financial security,” he added.

The Times Poll of 1,616 adults nationwide was conducted between March 27 and March 30. The margin of sampling error is plus or minus 3 percentage points.

In the survey, 69% of those earning less than $50,000 a year saw the president as more concerned with corporations. That figure dipped to 56% among those earning $50,000 or more.

Follow-up interviews with some of those surveyed underscore that Americans have mixed feelings about Bush’s approach to corporate America and the economy.

Greg Voorhees, a registered independent from Bradenton, Fla., feels the economy has changed for the worse, with corporations aiming only for the bottom line, deserting employees for cheap labor overseas and paying top executives “millions and millions while their workers barely get the minimum wage.”

The Bush administration, he is convinced, has been too quick to craft policies that benefit corporate interests at the expense of the public. Ordinary Americans, the 51-year-old said, are not informed of the real agenda on matters ranging from energy policy to drugs and Medicare: The White House, he said, is “hiding something.”

But others disagree. Curtis Blevins, a warehouse worker in northeast Ohio, said he believed the president was helping regular employees by responding to the needs of large corporations.

“Ordinary people work for big business,” said Blevins, 38. “If he doesn’t help big business, ordinary people are out on their duff…. I’m an ordinary person. I work for a big company. The more he helps the big companies, the more we get to hire. The easier our jobs become.”

The poll suggests, however, that many Americans harbor strikingly negative feelings about big companies and those who run them.

Revelations of phony bookkeeping at Enron Corp., WorldCom Inc. and other companies first grabbed public attention more than two years ago. Since then, news of financial scandal has remained highly visible — most recently centering on the trials of Tyco International Ltd. executives accused of looting their company and of Martha Stewart, who was convicted of lying to investigators about her stock dealings.

Half of those polled said they would describe corporate fraud as “a widespread problem” in a system that is failing; 40% said only “a few corrupt individuals” engaged in such behavior. Three out of four Americans said they could trust executives “only some of the time” or “hardly ever.” Slightly fewer than 1 in 4 said they could trust executives most of the time.

Revelations of fraud also have affected personal behavior. Thirty-seven percent said they were less willing to invest in the stock market in light of the corporate scandals, while 31% said the revelations had not affected their willingness to invest. Many of the rest said they did not own stock.

Almost half of those surveyed — 45% — ranked economic issues as the most important problem facing the nation, about the same percentage that put security concerns at the top.

Democrats contend that the ongoing attention to corporate scandal aggravates public worries about financial security, in part because the series of high-profile frauds rattled the stock market and eroded long-term savings accounts for college and retirement. The scandals also raise questions about whether a greedy business elite operates on a different ethical playing field from the rest of society.

“Every day there’s a new scandal on television that makes our point,” said Jenny Backus, a Democratic strategist. “You want to have somebody looking out for the economy that makes sure that corporations play by the rules and stockholders are protected.”

But Republicans maintain that corporate corruption is not an issue that will harm Bush. They often point out that the president has supported Justice Department prosecutions of white-collar criminals and ultimately endorsed sweeping legislation for corporate reform.

“Voters don’t hold the commander in chief in a position of corporate leadership,” said Scott Reed, a Republican consultant. “It’s very difficult for Kerry in his campaign to tie this knot around Bush’s neck.”

Reed asserted that strong economic growth, combined with Bush’s “optimistic message of hope,” presents a winning case for the president when it comes to financial security.

*

(BEGIN TEXT OF INFOBOX)

Financial assessment

Q: ‘He would be the best at protecting the financial security of the average American’: Does this apply more to George W. Bush or more to John Kerry?

Neither 9%

Bush 34%

Kerry 47%

Both equal 2%

Don’t know 8%

Q: Do you think George W. Bush cares more about protecting the interests of ordinary working people, or more about protecting the interests of large business corporations?

Ordinary people 21%

Large corporations 63%

Both 8%

Don’t know 8%

Q: Have corporate scandals in this country made you more willing or less willing to invest in the stock market, or have corporate scandals not played a role in your investing in the stock market one way or the other?

Don’t invest 23%

More willing 6%

Less willing 37%

No role 31%

Don’t know 3%

*

How the Poll Was Conducted

The Times Poll contacted 1,616 adults nationwide by telephone March 27 through 30, 2004. Telephone numbers were chosen from a list of all exchanges in the nation and random digit dialing techniques were used to allow listed and unlisted numbers to be contacted. The entire sample of adults was weighted slightly to conform with census figures for sex, race, age and education. The margin of sampling error is 3 percentage points in either direction. For certain subgroups the error margin may be somewhat higher. Poll results may also be affected by factors such as question wording and the order in which questions are presented.

Former Top Gear host Jeremy Clarkson headed to the auction house on the Prime Video series

Jeremy Clarkson’s net worth after farm show proves massive success BigCityLife

Jeremy Clarkson and Kaleb Cooper bid farewell to an iconic member of Diddly Squat Farm.

Season five of Clarkson’s Farm saw Jeremy selling off the fan-favourite Lambo tractor after it wasn’t getting much use, following his purchase of the AgBot in the new series.

The AgBot, a fully autonomous, driverless tractor, was busy ploughing the fields of Diddly Squat Farm and sowing seeds.

Jeremy and Kaleb could monitor the tractor’s progress on their computer while they got on with other things on the farm, which meant the 2016 Deutz-Fahr tractor wasn’t getting much use.

The veteran broadcaster decided to sell it off, explaining in voiceover: “”The green Lambo hadn’t turned a wheel in weeks, so I decided to sell it, which meant getting it valued by an agricultural auctioneer.”

The valuation on the prized piece of agricultural kit from Oliver Godfrey left Jeremy somewhat surprised and dismayed.

Oliver responded: “It’s not the easiest thing to sell in the world, I’ll be honest, but I would look somewhere in the region of between £50,000 and £60,000.”

Jeremy revealed that the valuation was “quite a lot less” than he’d initially paid for it when he bought it for £80,000.

On the day of the auction, Jeremy didn’t appear too hopeful about his Lambo’s prospects and said: “Here it is. There’s going to be a frenzy of bidding…”

However, the bidding did start to pick up as people put in their offers for the green tractor that Jeremy had customised and adorned with Lamborghini badges.

As the offers went up, Jeremy remarked: “We are actually getting closer to the £80,000 that I had paid for it.”

Despite the valuation, both Jeremy and Kaleb were left astonished and rather relieved when the Lambo ended up getting snapped up for the sum of £70,500.

Get 30 days of Prime Video totally free

This article contains affiliate links, we will receive a commission on any sales we generate from it. Learn more

TV lovers can get 30 days’ free access to binge great shows like Clarkson’s Farm by signing up to Amazon Prime. Just remember to cancel at the end and you won’t be charged.

Once the hammer went down, Jeremy said: “Well, it was a financial hit, but it wasn’t a financial kick in the nuts.”

The auction comes ahead of tomorrow’s Clarkson’s Farm season five finale, when audiences will get the final two episodes titled Sickening and Reaping – referring to the TB outbreak and the harvest at Diddly Squat.

Clarkson’s Farm season 5 concludes tomorrow on Prime Video

US stocks have rallied on hopes that the tentative deal to end the US-Israel war on Iran will restore stability to energy supply chains roiled by months of disruption in the Strait of Hormuz.

The S&P 500 rose 1.7 percent on Monday, taking the benchmark index within touching distance of its all-time high.

Recommended Stories

list of 4 itemsend of list

The tech-focused Nasdaq Composite jumped 3.1 percent, aided by a 19.6 percent gain by SpaceX, which on Friday made the biggest market debut in history and minted the world’s first trillionaire in Elon Musk.

The blue-chip Dow Jones Industrial Average climbed 0.9 percent, closing at a record high.

Brent crude futures, the primary benchmark for global oil prices, fell nearly 5 percent to just above $83 a barrel, the lowest price since the first week of the conflict.

Asian stock markets were largely flat on Monday morning, after surging the previous day on the back of US President Donald Trump’s announcement of his deal with Tehran.

As of 01:30 GMT, Japan’s benchmark Nikkei 225 was 0.01 percent lower, while South Korea’s Kospi, the best-performing major index this year, was down 0.06 percent.

In Taiwan, the TAIEX was up 0.2 percent.

Hong Kong’s Hang Seng Index was down 0.07 percent.

Jay Goldberg, a senior analyst for tech-related equities at the Chicago-based Seaport Research Partners, said the announcement of the US-Iran deal had tilted investors’ risk balancing act towards buying into the market.

“To oversimplify, the debate has been: AI spending is strong, but there’s a war going on,” Goldberg told Al Jazeera.

“The war is over, it seems, so that side of the argument falls away. Investors are now feeling better about taking on more risk,” Goldberg said.

While Washington and Tehran’s framework has raised hopes for a return to stability in global energy markets, it is expected to take months before energy flows fully return to normal, due to the massive backlog of vessels around the Strait of Hormuz and the need to ensure the waterway is safe from Iranian naval mines.

According to the International Shipping Chamber, about 500 ships are still waiting to pass through the strait, which normally carries about one-fifth of global supplies of oil and liquefied natural gas.

Labs are rethinking banking, as AI remains king, but human insight directs banking improvements.

So, the robot banker remains a long way off. But S&P Global estimates that up to 59% of financial institutions worldwide were actively using artificial intelligence in 2025. Beyond simply relying on technology for research (“Summarize new anti-money laundering mandates for me”), financial institutions have begun operationalizing AI processes.

This is a significant advancement. Instead of using AI like an intelligent chatbot, banks now direct systems to perform complex, multi-step tasks—saving untold human hours while both speeding up and improving operations.

How does this newer type of AI (called “agentic AI”) work?

Consider loan processing as an example. Someone applies for a loan. AI agents retrieve credit reports, verify income, calculate debt-to-income ratios, apply underwriting rules, approve or reject applications (or forward them to a human underwriter for approval), and generate documentation. In compliance monitoring, agents can read regulatory texts, map new mandates to internal policies and processes, identify where the financial institution (FI) falls short, generate remediation tasks, and track progress.

For proof of the increased operationalization of AI, look at some of the innovations germinated in the world’s best fintech labs, incubators, and accelerators.

At inovabra, a lab hosted by Banco Bradesco, innovators have developed an AI product that can generate initial drafts of legal pleadings. The Bank of Georgia’s AI Research Lab has launched Software Developer: Powered by Code2Doc.

This software can write other software. And Garanti BBVA Partners has nurtured Skymod, an AI-orchestration platform that enables financial institutions to securely delegate operational workflows to intelligent AI agents.

Knowing When AI Isn’t The Answer

Then there’s TD Lab. TD Lab is now experimenting with Physical AI, or AI-embedded machines (think robots, drones, and smart devices) capable of interacting with the physical world.

“Physical AI is about convergence,” said Chris Halabecki, senior manager and lab leader. “It’s about combining AI with objects that can sense or maneuver through the real world. As a lab team, we’re exploring how we can use physical AI to integrate more intelligence into everyday scenarios to better serve our colleagues and clients today and in the future.”

The lab has already developed proprietary software for a quadruped (robotic dog) device. Using LiDAR (Light Detection and Ranging), which is a sensing technology that uses pulsed laser light to measure distances, and AI together, the quadruped can detect and learn about objects in the surrounding area, then follow commands linked to those objects. Halabecki provided examples such as “Walk to the white couch” and “Go find Evan.”

Future use cases for these technologies may include robots that can count, sort, and verify cash.

One day, robotic relationship managers may recognize when a customer walks into a branch and guide them in making investment decisions. In the field, physical AI may be able to conduct home appraisals and complete other tasks.

With the much-ballyhooed capabilities of artificial intelligence, it’s a little surprising to hear Kadry Boutaina, chief of innovation for the digital transformation lab of Morocco’s Attijariwafa bank, say, “Sometimes, the answer is not AI.”

That doesn’t mean the lab, called Wenov, isn’t driving technological advancements. It works with external startups to offer “more and more digital services for our customers — both retail and business.” Boutaina notes that Attijariwafa faces significant competition in this field, from both established banks and newcomers — notably neobanks entering the Moroccan and broader West African markets.

But providing digital services does not always entail a wholesale AI revolution.

When Banks Let Employees Innovate

The Moroccan Ministry of Economy and Finance recently formalized laws governing crowdfunding in the country. The first regulated platform of this kind is being provided by Kiwi Collecte, a fintech company. Under Moroccan law, Kiwi Collecte may not directly hold or move funds. It must partner with a licensed Moroccan bank for those tasks. A partnership with Attijariwafa empowers the bank to hold and safeguard funds, process payments, and disburse money to beneficiaries.

Fraud prevention is ever important. Sandbox CAIXA has found an old-school way to fight it. Sandbox CAIXA is the innovation lab of Caixa Econômica Federal, a major state-owned bank in Brazil. Lucas Zaccaro, Sandbox CAIXA manager, said that in his country, technologically unsophisticated people are often victimized by scammers. When the bank is closed, thieves stand near ATMs. They then offer to help patrons who are unsure how to use the machines. These criminals “help” by tricking users into revealing their PINs, then stealing their cards.

A “really great idea” from a rank-and-file Caixa employee led the bank to broadcast recorded messages at 10 of these ATMs, warning patrons about the scam. Theft at those banks has stopped.

Zaccaro says that this fraud-prevention idea was submitted through an established process designed to encourage rank-and-file employees to submit innovative ideas. Employees use Microsoft Copilot to refine their concepts and submit them to Sandbox CAIXA for review and potential testing. The lab will now assess the feasibility of rolling out its scam warning across the ATM network—potentially using cameras to detect when people are at the ATM and triggering automated messages.

At the Banking and Financial Institutions Association of Colombia (Asobancaria), the focus is less on rapidly advancing technologies and more on meeting existing societal needs. One development from the Asobancaria Social Innovation Lab is a reference framework for identifying, classifying, and reporting on the banking sector’s social portfolios. This proposal—the second of its kind in Latin America after Guatemala’s Social Taxonomy—was developed through multiple sessions of analysis, technical feedback, and sector-wide validation with member institutions. To create this framework, Asobancaria worked closely with the Global Green Growth Institute (GGGI), which develops social-portfolio standards aligned with the United Nations Sustainable Development Goals.

Andrea Guzmán, GGGI’s sustainable finance officer, said the problem with sustainability reporting among Asobancaria member banks was a lack of alignment on standards, with each bank setting its own measures of success for its social portfolios.

The framework addresses issues such as financial inclusion, social infrastructure, affordable housing, and services for small and medium-size businesses. A single framework to which all member banks agree “improves transparency,” Guzmán says. “It supports better decision-making by investors and helps mobilize more resources for our social sector. It’s a framework we can base bonds on. It’s a framework that helps banks avoid accusations of greenwashing.”

Consider the framework for sustainable and affordable housing. Guzmán notes that in rural Columbia, many houses lack access to water and may have only dirt floors. Therefore, a bank could claim success in affordable housing if it funded units with wood floors, fully plumbed and connected to the electrical grid. But what if those apartments are so far from public transportation that no one can get to work or school? Guzmán said that under the framework, banks agree that any affordable housing projects they fund would have access to the nation’s external infrastructure and social services.

Here’s a closer look at some of the world’s best fintech labs and the innovations they’re nurturing.

SpaceX lands on public markets as the sixth largest US company by market value.

Published On 12 Jun 202612 Jun 2026

SpaceX has debuted on US markets with a market valuation of more than $2 trillion, minting CEO Elon Musk as the world’s first trillionaire.

Shares are set to open on Friday at $150 per share, marking a 6.6 percent increase from the initial public offering (IPO) price, valuing the company at $1.96 trillion putting the aerospace company on track to become the sixth-largest company in the United States.

Recommended Stories

list of 4 itemsend of list

The company sold $75bn in shares, immediately valuing it at $1.77 trillion. The IPO was oversubscribed four times higher than was otherwise expected, according to the Reuters news agency.

Of the institutional investors allocated, according to Bloomberg News, as much as 70 percent went to what are called long-only investments — a strategy in which holders buy assets based on the expectation that their value will grow over time — and sovereign wealth funds, including those from Saudi Arabia and Kuwait as well.

SpaceX President Gwynne Shotwell and Chief Financial Officer Bret Johnsen rang the Nasdaq MarketSite in New York City opening bell at 9:30am local time as US markets opened.

On Thursday, protesters gathered outside the MarketSite to protest the IPO amid continued allegations that Grok, part of xAI, a subsidiary of SpaceX, allowed users to create non-consensual deepfake sexualised images before the IPO debut.

Shares of SpaceX did not trade until the middle of the trading day as the exchange collected buy and sell orders and underwriters delayed trading until supply and demand were balanced.

“We would expect SpaceX to see an immediate pop in trading due to the hype around the deal, north of 20 percent perhaps,” said Samuel Kerr, global head of equity capital markets at Mergermarket. “Anything lower would actually make me nervous.”

Exchanges and trading firms are eager to avoid the technical mishaps that marred Meta’s 2012 debut. With SpaceX widely viewed as a dress rehearsal for a new generation of mega-listings, market participants will also be watching for signals on investor appetite in advance of forthcoming IPOs for AI heavyweights Anthropic and OpenAI.

The landmark listing cemented Musk’s status as the first trillionaire ever and propelled SpaceX into the ranks of the world’s most valuable companies — even though the firm posted a loss of nearly $5bn last year and generated only a fraction of the revenue brought in by similarly valued tech giants.

The surge comes amid growth driven by its Starlink subsidiary, which drives as much as 80 percent of its revenue.

On Friday, SpaceX launched its Falcon 9 rocket with 29 satellites into space from Cape Canaveral in Florida.

Wall Street and Asian markets rally on hopes for an end to the US-Israel war on Iran.

Published On 12 Jun 202612 Jun 2026

Stock markets have surged following US President Donald Trump’s announcement that he called off planned strikes against Iran and a peace deal with Tehran is imminent.

Wall Street’s benchmark S&P500 index finished nearly 1.8 percent higher on Thursday, ending a three-day streak of losses for the biggest single-day gain since April.

Recommended Stories

list of 4 itemsend of list

The tech-focused Nasdaq Composite jumped 2.5 percent, while the older, blue-chip Dow Jones Industrial Average gained about 1.9 percent.

The rally continued in the Asia Pacific on Friday, with markets in Japan, South Korea, Taiwan, Hong Kong, and Australia racking up gains.

South Korea’s Kospi, the best-performing major index this year, surged more than 8 percent in morning trading, while Japan’s benchmark Nikkei 225 rose as much as 4 percent.

Taiwan’s TAIEX gained about 2.4 percent, and Australia’s ASX 200 rose about 1.8 percent.

In Hong Kong, the Hang Seng Index was up more than 1 percent.

Brent crude, the primary international benchmark for oil prices, fell about 1 percent to below $89.50 a barrel on hopes for a return to normality in the Strait of Hormuz, which in peacetime carries about one-fifth of global energy supplies.

The market rebound came after Trump on Thursday suggested that a deal to end the war on Iran could be signed as soon as this weekend.

“We just made a great settlement of the war with Iran… subject to finalisation of documents,” Trump told reporters in the Oval Office of the White House.

Iran has not publicly confirmed Trump’s claims, but a Ministry of Foreign Affairs spokesman told reporters a memorandum of understanding with the US is “under consideration”.

“For the rally to be sustained, investors will want to not only see the actual deal being signed, but a complete reopening of the Strait of Hormuz,” Khoon Goh, head of Asia research for ANZ Bank, told Al Jazeera.

“Only then will we see the gains extend.”

Fabien Yip, a market analyst at the online broker IG Group in Sydney, Australia, said the rally reflected a “meaningful easing of geopolitical risk”, as well as anticipation over Friday’s market debut of SpaceX, set to be the largest of its kind in history.

“The broader read on today’s Asian follow-through is that dip-buying interest remains genuine,” Yip told Al Jazeera.

“That matters for how you characterise what’s happened over the past week.

“This looks less like a structural break in the bull market and more like a healthy reset after a rapid, near-straight-line advance, the kind of consolidation that can potentially extend a rally’s longevity.”

GEMMA Collins spent years convincing the world she was living her best diva life – but behind the designer handbags and larger-than-life personality, there was a time when the empire she had worked so hard to build started crumbling around her.

Incredibly, the GC pulled herself back from the brink and banked more than £1.4 million last year. But friends say the feat would have been nearly impossible without the help of one very special man.

Gemma has admitted that Alan is the gatekeeper to her fortuneCredit: GettyGemma’s Dad is her rock and keeps her groundedCredit: Instagram

Those closest to Gemma have revealed the secret to the Romford-born star’s success is her dad, Alan, who is credited as the only person who can keep Gemma grounded.

A source tells us: “People see Gemma as this unstoppable force of nature, but behind the scenes, Alan has always been her rock.

“When things got difficult financially, he stepped in and took control.

“Gemma trusts him completely. There aren’t many people she would hand that responsibility to.”

For years, Gemma has openly admitted that Alan is effectively the gatekeeper to her fortune.

In one interview, she confessed: “My dad controls all my money. Seriously, I have to ask him if I want to upgrade my car.”

It’s a remarkable admission for a woman who has built a reported £4million fortune and can command up to £75,000 for a single sponsored Instagram post.

But those who know the family say it perfectly sums up their relationship.

Another source tells us: “Alan has always kept Gemma grounded.

“She’s the star, but he’s the sensible head behind the scenes.

“When she gets excited about a new project, he’s often the person asking the difficult questions.”

The latest figures suggest that the approach is paying off.

Accounts for her personal brand, Gemma Collins Ltd, show the company landed profits of around £1.4 million last year.

For fans who remember the financial turmoil of previous years, this is a huge turnaround.

A separate clothing business was later voluntarily dissolved, while her cosmetics venture, GemmaCollagen Ltd, survived for just a matter of months before disappearing altogether.

One insider tells us: “There was a period where it felt like every business venture came with a headache.

“Gemma never stopped working, but there were definitely lessons learned.

“That’s when Alan became more involved.”

It is perhaps fitting that Gemma’s biggest supporter is also somebody who understands business himself.

Alan built a successful career in shipping and has long been regarded as one of the most influential figures in his daughter’s life.

Fans caught a glimpse of their bond on her reality shows, where Alan frequently offered advice, not just about money but about life itself.

During one emotional conversation about her turbulent romance with James Argent, he told her: “You’ve just got to find some stability in your life when you find the right person.

Gemma’s parents, Alan and Joan, live with Gemma in her £1.3 million Essex home alongside fiancé RamiCredit: Refer to CaptionGemma will return to screens with a new Sky reality series, Four Weddings and a Baby, with RamiCredit: Splash

“As much as we all like Arg, you’ve got to decide if he’s the right person.”

He later added: “For my daughter, I want somebody who’s top dollar.”

Those close to the family say that attitude explains exactly why Gemma places so much trust in him.

One source tells us: “Alan isn’t interested in celebrity.

“He cares about Gemma being secure and looked after. That’s always been his focus.”

Their relationship has only strengthened in recent years.

She has also supported both Alan and mum Joan through a series of serious health scares, including Joan’s breast cancer diagnosis and terrifying hospitalisation last year after she stopped breathing.

The ordeal brought the family even closer together.

These days, Alan and Joan live with Gemma in her £1.3 million Essex home alongside fiancé Rami.

According to Abs Mechial, there is a specific minute every day in which holidays can be booked for cheaper on average – but you may need to set your alarm to take advantage of it

A financial adviser has revealed the best time to book your 2026 holiday (stock)(Image: Ralf Hahn via Getty Images)

If you are yet to book a getaway this year and are wondering when the ideal moment might be to do so, a financial expert has identified precisely when you should – and shouldn’t – make your move. Abs Mechial turned to TikTok to reveal that not only are certain days preferable for booking, but specific times of day matter too.

“When is the worst time to book a holiday and when is it actually cheapest? he asked his followers in a video. Surprisingly, according to research, Abs claimed there is a one-hour window in each day when holidays can cost you significantly more money to book.” he asked his followers.

Content cannot be displayed without consent

“According to the data, the most expensive time to book is between 9am and 10am,” he explained. “Bookings in that window came in around 30 per cent more than the cheapest time of the day – so no more booking holidays as soon as you log in for the day.”

As for the most economical time of day, Abs warned that you might need to set your alarm. “Early… and I mean really early,” he said. “Between 4am and 5am – and the logic does make sense.”

Abs highlighted that overnight, demand “drops off” and consequently prices “reset” to their baseline.

He elaborated: “Then as the day goes on, the more searches and more clicks result in prices starting to creep back up again.”

For those reluctant to wake up before sunrise, however, Abs provided guidance for anyone wanting to book during “more realistic hours”.

“Late evening, around 8pm to 10pm tends to be noticeably cheaper than the morning rush,” he enthused. “But if you want to go even further and want the exact moment – not just the hour, but the minute – according to the data, the single cheapest minute to book a holiday is 2:48am.”

Surprisingly, bookings made at that precise time worked out up to 60 per cent cheaper on average, according to Abs.

He concluded with a word of caution, however: “Now, definitely take that with a pinch of salt – booking at 2:48am isn’t going to make every holiday 60 per cent cheaper, but the pattern is clear – if you want to save money, avoid peak booking hours because timing, just like everything else with money, makes a massive difference.”

Responding in the comments, one TikTok user offered their own unverified tip: “Best to search in private browser so prices do not increase if you are searching for same destinations. Prices increase with demand so private searching will prevent this.”

A second person added: “I usually book mine within 72 hours of departure… like 50% cheaper! I find the hotels I want and then I wait for them to deal them off.”

A third exclaimed: “Wow that’s crazy how the time of day can cost you!”

While a fourth TikTok user pointed out: “Doesn’t change if you want a certain resort at a certain time of year.”

Benchmark Nikkei 225 tops 68,000 for first time as AI-driven buying frenzy shows no signs of slowing down.

Published On 3 Jun 20263 Jun 2026

Japan’s stock market has hit an all-time high as a global buying frenzy driven by AI shows no signs of slowing down.

The Nikkei 225 rose nearly 3 percent on Wednesday, lifting the benchmark index above 68,000 for the first time.

Recommended Stories

list of 4 itemsend of list

The latest surge continues a banner year for Japan’s stock market, which is up nearly 33 percent so far in 2026.

“Investor enthusiasm over the AI boom is helping drive Asian equity markets higher,” Khoon Goh, head of Asia research at ANZ, told Al Jazeera.

“While strong demand for high-end chips has seen the top semiconductor companies in Taiwan and South Korea rally strongly, this is also benefiting Japanese markets, which are also getting some tailwind from a weak yen.”

Japanese firms involved in the semiconductor business led the gains.

Tokyo Electron, Japan’s largest manufacturer of semiconductor equipment, soared as much as 14 percent in morning trading.

Advantest, which supplies testing equipment to the semiconductor industry, rose more than 5.5 percent.

Shin-Etsu Chemical, a supplier of silicon wafers used in integrated circuits, gained about 4 percent.

Softbank, which is heavily invested in AI models, chips and data centers, fell about 3 percent, after overtaking auto giant Toyota on Monday to become Japan’s biggest company by market capitalisation.

Ferocious demand for AI chips has been driving record-breaking rallies in stock markets across the globe, taking key indexes in the US, Japan, South Korea, Taiwan to record highs.

During the past month, three memory chip makers – South Korea’s SK Hynix and Samsung Electronics, and US-based Micron – entered the elite club of firms with a market capitalistion of at least $1 trillion.

Only 17 companies have hit the milestone, all but five of which are based in the United States.

Despite concerns about the sustainability of the sky-high valuations in the sector among some investors, tech companies are continuing to commit huge sums to AI-related infrastructure.

US tech giants are expected to spend about $800bn on AI-related capital investment in 2026, according to Goldman Sachs.

Google parent company Alphabet on Monday became the latest Silicon Valley giant to outline its AI-related investment plans, announcing that it would sell $80bn worth of shares to help fund expected capital expenditures of $180-190bn in 2026.

Deepfake fraud is becoming a persistent, multiyear corporate risk as synthetic voices circulate undetected.

Deepfake-enabled fraud, which began as novel technical exploits, is now a persistent operational risk with a multi-year shelf life within the corporate ecosystem. According to deepfake-detection provider Resemble.AI, deepfakes typically remain in circulation for three-and-a-half years.

Resemble.AI’s 2025 Deepfake Threat Report, published in March, references an incident in which a voice clone of a German energy company CEO remained in circulation for nearly six years, although it resulted in only a €243,000 loss in 2019.

Determining losses from such attacks is difficult; for the 41 documented incidents last year cited by the research, only $74.9 million in verified losses were reported, with a median per-incident loss of $243,000. However, the authors noted that 71% of victims did not report financial losses, suggesting a higher volume of hidden liabilities.

“What makes them so effective is that they enable both real-time impersonation and the creation of synthetic identities stitched together from real and fake data,” said Dominic Forrest, CTO of biometric security vendor Iproov. “These are extremely difficult to detect, and once trusted, they can be used to bypass controls and commit fraud.”

AI Arms Race

Detecting deepfakes is a growing concern; the authors of the Resemble.AI report estimate that deepfake-based fraud attacks on corporations reached 8.5 billion potential incidents, ranging from audio impersonations of executives to doctored or fake images. The most common targets, Forrest noted, are on account openings, payment authorization, credential reset, and high-value transactions.

Telling a deepfake from the genuine article has become an AI-on-AI battle, experts warn.

The generative AI models producing deepfakes improve continuously via scaling and data, while deepfake detectors rely on signals like artifacts and inconsistencies, which disappear as models improve, said Siwei Lyu, professor of Computer Science and Engineering and director of the Institute for AI and Data Science at the State University of New York at Buffalo.

“In practice, detectors lag by about six to 18 months on specific modalities,” he said. “But more importantly, they are chasing a moving target whose failure modes are actively being optimized away.”

Forrest suggests that firms move their identity verification from single checks to a multi-layered approach: “You need to confirm that a real person is physically present, not a deepfake, while also analyzing the digital environment for signs of compromise. No signal should be trusted in isolation.”

This article first appeared in the May edition of Global Finance Magazine.

Global Finance’s World’s Best IFI winners outperformed the sector in 2025, emphasizing innovation and AI adoption. But new Mideast conflicts pose new challenges.

Islamic financial institutions (IFIs) modestly improved their performance in 2025, recording an average Return on Average Assets of 2% and a 12% increase in total assets. This compares to 1.9% and 9%, respectively, in the prior year. The winners of Global Finance’s World’s Best Islamic Financial Institutions Awards all achieved above-average profitability and growth.

Digitalization and AI remain strong areas of focus and investment as IFIs seek to drive customer growth, increase financing assets and deposits, and strengthen their competitiveness against conventional banks. Retail banking remains the main pillar of most Islamic banks, but IFIs are strengthening their commercial banking delivery as well. Corporate finance, capital markets, and wealth management activities are also becoming increasingly important to the sector.

A relatively low cost of funds contributes to Islamic banks’ positive margins. The biggest of the group, which dominate their domestic markets, continue to outperform their rivals, reflecting funding advantages and cost efficiencies.

The winners of Global Finance’s 2026 World’s Best Islamic Financial Institutions Awards have also distinguished themselves as innovative by introducing new Islamic banking products, consolidating their market share, improving service quality, and achieving good financial results. Collectively, they have shown themselves to be well managed with clear strategies. Like all Middle Eastern banks, however, they face a more challenging road ahead due to the new conflicts in the region, particularly the Iran war that’s disrupted the Persian Gulf.

This year’s top winner, Kuwait Finance House (KFH), enjoyed asset growth of 17% last year, to $139 billion, helping the bank maintain its position as the second-largest Islamic institution globally. KFH has the most diverse geographical reach of any IFI, with operations throughout the Middle East, Europe, and Asia. It has advanced its digital transformation by shifting from basic digitization to value-driven technology adoption.

Meanwhile, Boubyan Bank claimed Global Finance’s inaugural award as Most Innovative Islamic Bank. The bank stands apart for its innovation, technology-driven strategy, and strong commitment to offering financial solutions that enhance the customer experience. Boubyan made significant progress last year in embedding AI into services offered through its app.

Emirates Islamic Bank (EIB) took home the Best Islamic Financial Institution in The Middle East. The bank notched 19% growth in net profit last year, to $910 million, driven by robust balance-sheet growth. Lending grew 26% over both retail and corporate banking. Supported by a sophisticated digital offering, EIB has seen its franchise strengthen through a wide range of Shariah-compliant pro-duct offerings.

HomeAwardsAward WinnersWorld’s Best Islamic Financial Institutions 2026: Country and Territory Winners

In 2026, Islamic financial institutions continue to demonstrate resilience, innovation, and regional impact.

Across the Middle East, Asia, and beyond, leaders are balancing robust growth with Shariah-compliant practices, setting new standards in both domestic and cross-border markets.

Institutions are harnessing digital transformation to deliver more efficient, accessible, and customer-focused banking, from mobile apps and AI-powered services to fully digitized payment and investment platforms. Their portfolios span retail, corporate, and wealth banking, while many are pioneering new products in sukuk, digital savings, and Shariah-compliant investment solutions.

Regional leaders are also championing financial inclusion, SME support, and sustainable initiatives, reflecting a commitment to both community development and responsible growth. Across markets, the combination of innovative technology, solid performance, and ethical finance is positioning these institutions as benchmarks of excellence in the global Islamic finance landscape.

Regional Winners

Bilal Parvaiz, CEO

Asia-Pacific

Standard Chartered Saadiq (SCS)

SCS is a leading Islamic financial institution throughout Asia and particularly in Malaysia, Pakistan, Brunei, Singapore, and Indonesia, providing innovative solutions for Shariah-compliant financial needs. With the support of parent Standard Chartered Bank, it also provides access to the global banking and financial markets. SCS is active across corporate and investment banking, trade finance, wealth management, and retail and private banking as well as the sukuk market.

Farid Al Mulla, CEO

Middle East

Emirates Islamic Bank (EIB)

EIB had a banner year in 2025, reporting net profit up 19% at 3.3 billion UAE dirhams ($899 billion), driven by robust balance-sheet growth and higher recoveries. Financing growth was 26% over the retail and corporate banking segments. Total income in retail banking and wealth management increased 14%, driven by increased customer liabilities and Islamic financing growth. Total income from corporate and institutional banking increased 15%. Supported by a sophisticated digital offering, EIB’s franchise has strengthened across a broad menu of Shariah-compliant products.

Country and Territory Winners

Bahrain

KFH Bahrain

Part of the KFH Group, KFH Bahrain continued to develop its domestic franchise last year; to focus more closely on the local Islamic market, it sold its stake in Oman’s Ahlibank. A signal achievement in 2025 was the successful, $400 billion Additional Tier 1 Sukuk offering, the largest of its kind ever in Kuwait. Also last year, KFH Bahrain launched the KFH Gold Account, Bahrain’s first digital gold investment and savings account. KFH’s MyHassad Savings Scheme is now the island kingdom’s largest prize-based savings product, with a record-breaking deposit portfolio of $675 million following 17% growth last year. The bank also completed its fully digitized Liquidity Management Solution in 2025.

Brunei Darussalam

Bank Islam Brunei Darussalam

Bank Islam Brunei Darussalam is the dominant bank in Islamic finance in Brunei Darussalam, with assets of $8.3 billion covering a range of Islamic SME and consumer financing products.

Egypt

ADIB Egypt

A leading performer in Egypt’s Islamic banking sector, ADIB Egypt reported assets of $7.3 billion last year, up by 42% in US dollar terms, thanks to growing market share as net profit grew 25% to $256 million. ADIB Egypt offers retail and corporate banking services together with investment banking, leasing, asset management, and microfinance.

Indonesia

Bank Muamalat

Indonesia’s first Islamic bank, founded in 1991, Bank Muamalat today holds total assets of $4 billion. It provides a comprehensive range of Shariah-compliant financial services and has pioneered many Islamic banking products in Indonesia.

Jordan

Islamic International Arab Bank (IIAB)

IIAB takes the title as 2026 Best IFI for Jordan thanks to a strong performance in 2025, significant digital progress, and a widening business reach. Growth was in double figures and assets now total some $6 billion. IIAB holds a 22% market share of Islamic assets in the kingdom. IIAB serves individuals, SMEs and large corporates, in addition to financing large projects. It has been an initiator of multiple domestic SME enablers, including the Kafalah Scheme, Jordan’s first Shariah-compliant finance guarantee scheme, and jointly organized the first Islamic funds mobilization with the Central Bank of Jordan, the Arab Fund, the World Bank, and other regional players.

IIAB’s digital banking services include a high-end mobile app that includes digital onboarding, seamless access to most of IIAB’s banking services, personal finance management, and third-party services via the bank’s ecosystem. IIAB is also an active AI adopter, embedding it at the core of its digital transformation to enhance customer experience, operational efficiency, and Shariah-complaint innovation.

Kuwait

Kuwait Finance House (KFH)

Kuwait’s second-largest bank, KFH now controls over 60% of domestic Islamic banking assets and is by far the kingdom’s largest Islamic institution. It holds a 30% share of conventional and Islamic banking assets. Domestically, KFH dominates the Islamic financing and deposit market—and, in turn, has a strong presence in the overall banking sector for both deposits and financing/loans—as well as a strong positions in retail, private, and corporate banking.

Malaysia

Maybank Islamic

Maybank Islamic, Malaysia’s flagship Islamic institution, is innovative, well managed, and over the long term, has recorded impressive performance. It is often first in introducing innovative Shariah-compliant financial products. In its home country, the bank controls around 30% of Islamic assets, but its activities extend across other Asian markets as well, making it the largest Islamic bank outside the Middle East and fifth-largest globally with $90 billion in assets. It also holds a prominent position in the global sukuk market. Maybank’s financial metrics are solid, with a strong capital base and good returns.

Morocco

Umnia Bank

Umnia Bank was Morocco’s first Islamic bank, established in 2017. Shareholders include Qatar International Islamic Bank, CIH Bank (Credit Immobilier et Hotelier), and Caisse de Dépôt et de Gestion (CDG). Unmia operates the country’s largest Islamic banking network and is its largest by total assets, with around 50% market share in financings and 40% in deposits. Its main areas of financing are automobiles, real estate, and equipment finance.

Oman

Bank Nizwa

With $5.2 billion in assets at the end of last year, Bank Nizwa is Oman’s seventh-largest bank, with a focus on innovation that has helped broaden its reach in its home market. Oman’s first digital Islamic bank, it remains focused on digital expansion.

Reinforcing its commitment to leveraging strategic partnerships, Bank Nizwa launched the Tranna app last year in collaboration with Zappit, a financial technology company. The app is designed for expatriates living and working in Oman, enabling instant transfers to six countries: India, Sri Lanka, Pakistan, Nepal, the Philippines, and Bangladesh. Also last year, Bank Nizwa launched its Electronic Mandate (E-Mandate) for Direct Debit service that streamlines recurring transactions and enhances the overall banking experience for corporate and retail customers.

Pakistan

Meezan PAKISTAN

Meezan Pakistan had a strong 2025, launching several new products. Totall deposits increase by 28% to $17.2 billion, aided by a large branch and ATM network and solid digital infrastructure.

Meezan continued to strengthen its digital offerings via WhatsApp Banking, a simple, secure, and accessible transactions channel, and its highly rated mobile app, which is recognized for its simplicity, speed, and reliability. The app expanded its user base 40% to over 4.3 million while financial transactions increased 40% to 553 million.

The bank offers one of the industry’s most comprehensive portfolios of debit cards, supported by advanced payment technologies including NFC-enabled payments, chip and PIN security, mobile-based contactless transactions, and 3D secure e-commerce payments.

Qatar

Qatar Islamic Bank

The emirate’s largest Islamic bank and its second-largest bank overall, QIB enjoys a strong franchise and market position, when ranked by total banking assets. QIB reported 2025 net profit of $1.3 billion as total assets reached $61 billion, as total assets rose to 10% to $61 billion, QIB is also active in the Islamic capital markets, including sukuk-related activities, structured financing, and transaction execution. QIB has significant government backing, with the Qatar Investment Authority its largest shareholder.

Saudi Arabia

Al Rajhi Bank

Al Rajhi Bank is the world’s largest Islamic financial institution and Saudi Arabia’s flagship Islamic bank with $278 billion in total assets and $6.6 billion in net profit at the end of last year. It operates a strong retail banking network in its home market, particularly measured by deposits and income. It ranks first in banking transactions with 1 billion per month and first in remittances for the Middle East by payment value. Al Rajhi has 20.6 million customers in Saudi Arabia and the leading market share in deposits at 22.6%. Financial metrics are good, particularly capital ratios with total CAR at 21.9% at the end of 2025 and ROAA of 2.4%.

Sri Lanka

Commercial Bank of Ceylon

Al-Adalah, Commercial Bank of Ceylon’s Islamic banking window, offers a diverse portfolio of innovative Shariah-compliant products. Assets grew 67% last year as the financing portfolio doubled. The bank also made a strategic pivot in 2025 toward SME financing and sustainable energy projects.

Turkey

Kuveyt Türk Katilim Bankasi (KTKB)

KTKB is KFH’s Turkish subsidiary. The largest Islamic bank in Turkey and one of the country’s top 10 banks, its business model has proved resilient amid a challenging operating environment. Commanding a 34% market share in Turkish Islamic banking, it also operates an Islamic bank in Germany under the name KT Bank AG as well as a Bahrain office that serves as a bridge between Turkey and the Gulf Cooperation Council states.

United Arab Emirates

Emirates Islamic Bank (EIB)

EIB’s market position grew significantly in 2025 as assets increased 30% to $39.7 billion and deposits grew 33%, bolstered by a strong balance sheet and strong capital and liquidity position. The third-largest Islamic bank in the UAE, EIB has been improving its digital infrastructure and increasing its AI utilization. It has expanded its wealth management services and products, becoming the first Islamic bank in the UAE to launch a Shariah-compliant digital wealth offering and equity trading via mobile banking app.

Global Finance: Please describe BSIC Group and why the Sénégal subsidiary is important to its African strategy.

Sami Gargouri: BSIC Group, or the Banque Sahélo-Saharienne pour l’Investissement et le Commerce, is a pan-African public bank established in 1999 as a key institution of the Community of Sahel-Saharan States (CEN-SAD). Headquartered in Tripoli, Libya, it is owned by the governments of 14 African nations, including Libya (majority stakeholder), Senegal, Cóte d’Ivoire, Gambia, Benin, Burkina Faso, Mali, Chad, Guinea Conakry, Togo, Central African Republic (CAR), Niger, Sudan, Ghana, and 2 representative offices in Morocco and Tunisia, with a focus on mobilizing public and private financial resources to drive economic and social development, combat poverty, and boost intra-regional trade across the Sahel-Sahara zone. Operating as both a commercial and investment bank, BSIC offers services ranging from loans and asset management (BSIC Capital) to trade financing, supporting SMEs, agro-industry, and cross-border commerce. Its strategy emphasizes regional integration, financial inclusion, and innovation to foster growth in underserved areas, aligning with CEN-SAD’s goals of poverty alleviation and economic unity.

The Senegal subsidiary, BSIC Sénégal SA, is pivotal to this African strategy due to its location in a stable, dynamic West African economy with strong a entrepreneurial ecosystemand high mobile money penetration. Launched in Dakar, it serves over 50,000 clients through a network of branches in key areas like Thiès, Mbour, Saint Louis, Touba and Kaolack, channeling resources into local sectors such as agriculture, SMEs, and exports directly supporting BSIC’s mission of intra-regional trade. As a bridge between French- and English-speaking Africa, BSIC Sénégal enhances the group’s diversification, gains market share in Senegal’s competitive banking sector (aiming for top rankings), and tests scalable innovations that can be rolled out group-wide, amplifying BSIC’s role as a pan-African development engine.

GF: How has BSIC Sénégal become an innovation hub for the group?

SG: BSIC Sénégal has evolved into an innovation hub for the BSIC Group by leveraging customer insights, a test-and-learn approach, and cross-functional collaboration to pioneer digital solutions tailored to West Africa’s mobile-first economy. Since its establishment, the subsidiary has prioritized digitalization, drawing from direct feedback from SMEs and merchants during meetings to address pain points like payment delays and limited access to diverse transaction channels. This led to the creation of a dedicated project management office involving departments such as Marketing, IT, Risk, Compliance, Legal, and Logistics, alongside fintech partners for seamless API integrations—enabling rapid prototyping and deployment of products like the SMART TPE in November 2023.

BSIC Sénégal has positioned itself as a dynamic player, launching innovative offers that combine digital tools with client-centric design, such as enhanced Visa cards, a dealing room for economic operators, and mobile payment expansions resulting in market share gains and improved client experiences. Its pilot-to-scale model, starting with select merchants before group-wide rollout, has made it a testing ground for group initiatives. This approach fosters financial inclusion, serves as a model for other subsidiaries in digital transformation and SME support, and solidifies Sénégal’s role in BSIC’s pan-African innovation ecosystem.

GF: What is SMART TPE and how is it part of the BSIC Group’s digital transformation?

SG: SMART TPE (Smart Terminal de Paiement Électronique) is an innovative electronic payment terminal launched by BSIC Sénégal in November 2023, designed to enhance financial inclusion and merchant efficiency in mobile money-dominant markets. It transforms traditional card-based POS terminals into versatile devices that offer customers dual payment options: bank card or mobile money via operators like Orange Money or Wave. When a customer selects mobile money, the terminal displays operator choices and generates a QR code for instant scanning and transaction completion – ensuring funds deposit directly into the merchant’s BSIC account within the same day, bypassing multi-day delays from direct operator payouts. This first-of-its-kind integration on existing POS disrupts the status quo by empowering merchants with better cash management, reduced commissions, and diversified payment channels. It leverages fintech APIs for quick, secure development – ultimately boosting sales by 30-50% in pilots and simplifying user experiences for both merchants and non-banked customers.

As a cornerstone of BSIC Group’s digital transformation, SMART TPE exemplifies the group’s shift toward tech-driven inclusion, born from customer needs and deployed via a collaborative pilot involving IT, monetics, and fintech. It supports BSIC’s broader strategy of digitalizing services across subsidiaries – enhancing API ecosystems, combating fraud, and scaling mobile solutions regionally—to make banking more accessible, efficient, and aligned with Africa’s fintech boom, while advancing goals of poverty reduction and economic growth.

Published reports say Sen. Flavio Bolsonaro negotiated a multimillion-dollar sponsorship deal to finance a film about his father, former President Jair Bolsonaro, with a banker now jailed on suspicion of leading a criminal organization involved in financial fraud. Photo by Andre Borges/EPA

May 14 (UPI) — Just five months before Brazil’s October elections, the presidential campaign of right-wing Sen. Flávio Bolsonaro has become entangled in what authorities describe as the country’s largest recent banking fraud case.

According to reports published by Intercept Brasil, Bolsonaro negotiated a multimillion-dollar sponsorship deal to finance a film about his father, former President Jair Bolsonaro, with a banker now jailed on suspicion of leading a criminal organization involved in financial fraud.

The Brazilian news outlet released audio recordings and messages allegedly tied to negotiations between the senator and Daniel Vorcaro, owner of the collapsed Banco Master. Vorcaro is being held in pretrial detention as part of a financial and political scandal that has expanded to include Brazilian politicians and judges.

The scandal erupted after Brazil’s Federal Police intercepted Vorcaro’s phone messages, which reportedly reveal a close relationship between the two men — with Flávio Bolsonaro referring to the banker as “brother.”

In the conversations, Bolsonaro allegedly pressured Vorcaro to release payment for a sponsorship worth 134 million reais, or about $26 million, according to Brazilian outlet G1 Globo. The funds were intended for the Hollywood production of The Dark Horse, a biographical film aimed at improving Jair Bolsonaro’s public image.

In one audio recording, Flávio Bolsonaro discussed the urgency of the payments and the importance of the film project, according to Agência Brasil.

“Even though you gave us the freedom to hold you accountable, I feel uncomfortable having to ask,” the senator said in the recording. “We are at a crucial point in the movie’s production, and because many payments are still pending, everyone is tense, and I worry this could have the opposite effect from what we expected for the film.”

Authorities say the controversy extends beyond the size of the sponsorship and centers on the source of the money. Brazil’s Central Bank liquidated Banco Master after discovering an accounting shortfall estimated at between $7.6 billion and $10 billion.

Investigators allege the bank operated a scheme involving fraudulent securities sales and the theft of pension savings belonging to public-sector workers. Brazilian media reported that while retirees lost savings, members of the banker’s family purchased luxury homes in Miami and private aircraft.

Hours before the audio recordings became public, Flávio Bolsonaro denied having a business relationship with Vorcaro and dismissed the allegations as false during television interviews.

After the recordings surfaced and his voice allegedly could be heard in the conversations, the senator acknowledged contact with the banker, but argued the deal involved legitimate private sponsorship.

Bolsonaro later wrote on X that he was the victim of political persecution and said the leaked chats only showed a lawful business negotiation.

“It was a son seeking private sponsorship for a private film about his father. Zero public money,” the senator wrote, insisting he did not know the banker’s funds allegedly originated from purported fraud.

The market reaction was immediate. After publication of the recordings, the São Paulo stock exchange fell nearly 2% and the Brazilian real weakened against the U.S. dollar, reflecting investor concerns over political instability.

Recent polls show Flávio Bolsonaro statistically tied with President Luiz Inácio Lula da Silva in a potential runoff election.

Government allies have launched an offensive to capitalize on the scandal, demanding Bolsonaro’s removal from office through ethics proceedings in the Senate. According to Gazeta do Povo, lawmakers are seeking to suspend his political rights for eight years.

Those aligned with Lula also are pushing to create a congressional investigative committee into Banco Master. The proposed inquiry would seek access to Bolsonaro’s banking and tax records to trace the millions of reais allegedly negotiated in the sponsorship deal.

Left-wing parties argue the movie financing arrangement served as a front for money laundering and illicit enrichment, linking the failed bank’s expansion to political protection networks allegedly built during Jair Bolsonaro’s administration.

Prosecutor calls for leftist candidate to be jailed for five years and four months over false financial disclosures.

Published On 13 May 202613 May 2026

Peru’s public prosecutor’s office has accused leftist presidential candidate Roberto Sanchez of financial crimes, calling for him to be imprisoned for five years and four months.

The charges, unsealed on Tuesday, came hours after electoral authorities confirmed Sanchez was on track to advance to the country’s presidential run-off, scheduled for June 7.

Recommended Stories

list of 4 itemsend of list

According to the El Comercio newspaper, prosecutors allege that Sanchez, who is the candidate of the Juntos por el Peru (Together for Peru) party, filed false financial disclosures with the National Office of Electoral Processes related to campaign contributions between 2018 and 2020.

Prosecutors say Sanchez and his brother, William Sanchez, received more than 280,000 Peruvian soles ($81,720) in contributions and membership fees that were never disclosed in the party’s financial filings.

Sanchez is also accused of making false statements in administrative proceedings.

In addition to the jail term, prosecutors were also seeking a “permanent disqualification” of Sanchez from holding the office of president for the Juntos por el Peru party, according to El Comercio.

Sanchez’s lawyer rejected the accusations, telling local outlet RPP that the party’s treasurer, not Sanchez, was responsible for its financial filings.

A judge is expected to decide on May 27 whether the case will go to trial.

The charges emerged as vote counting from last month’s first-round election showed Sanchez advancing to a run-off against conservative rival Keiko Fujimori.

With 99.76 percent of ballots counted, Fujimori, the daughter of late former President Alberto Fujimori and a four-time presidential candidate, held a commanding lead with 17.17 percent of the vote.

Sanchez, running with the backing of jailed former President Pedro Castillo, stood at 12 percent, narrowly ahead of ultra-conservative former Lima Mayor Rafael Lopez Aliaga at 11.91 percent, a margin of roughly 15,000 votes.

WASHINGTON — The chair of the House Oversight Committee has sent a letter to OpenAI Chief Executive Sam Altman requesting information about potential conflicts of interest between Altman’s personal investments and his operation of the company.

The letter, sent Friday, comes amid a high-stakes legal battle currently playing out in an Oakland federal courtroom between one-time partners Altman and Elon Musk, the world’s richest man, who in 2015 co-founded the AI company best known for creating ChatGPT.

The company was first established solely as a non-profit corporation and the letter sent to Altman by Rep. James Comer (R-Ky.), the Republican chair of the Oversight committee, indicates that the committee is “investigating potential conflicts of interest involving capital from nonprofit corporations invested in startups and other for-profit companies.”

Comer has requested by May 22 a briefing from the company official responsible for oversight of potential conflicts involving company officers and directors, including Altman, as well as all documents related to conflict of interest policies and guidance for those executives.

While OpenAI was created as a non-profit designed to responsibly harness the power of the emerging artificial intelligence technology, the company created a for-profit subsidiary in 2019 and three years later released ChatGPT, which jumpstarted widespread adoption of the technology.

Musk, the chief executive of Tesla, left Open AI’s board in 2018, one year before the creation of the for-profit arm. He is arguing that Altman and another co-founder, Greg Brockman, betrayed the original mission of the non-profit organization, driven by their desire to “cash in” on the technology.

Musk added Microsoft, a significant investor in OpenAI, to the lawsuit in 2024. OpenAI is rumored to be gearing up to go public later this year or early next, and was recently valued at $852 billion.

Musk has said that he invested $38 million in the OpenAI non-profit, but he does not stand to benefit from a potential OpenAI public offering.

He created a rival company xAI in 2023 that was later folded into his company SpaceX

In the lawsuit, Musk is seeking $150 billion in damages, for Altman to be removed from the company and for the company to be fully returned to its non-profit status.

Musk’s complaint also alleges that Altman engaged in self-dealing by directing OpenAI to pursue deals with companies in which he also held a personal stake, including nuclear fusion power company Helion.

Comer’s letter cites reporting that Altman’s pursuit of a Helion deal, which is still ongoing, would come at a lofty valuation of the power-company, boosting the company’s worth, and the value of Altman’s investment.

Altman was briefly forced to step down from leadership of OpenAI in 2023 in part due to concerns about potential conflicts between his personal investments and his operation of the company, but was soon reinstated.

While the company’s board created an audit committee to investigate the potential conflicts of Altman and other officers, the findings were never disclosed.

Comer has requested that Altman turn over all documents and communication related to that audit committee.

Representatives for OpenAI did not immediately respond to requests for comment.

Financial sector jobs grew in April, but a record wage gap challenges the industry’s recovery.

There might be a light at the end of the tunnel for job safety in commercial banking — or it could be the light of an oncoming train.

After more than 12 months of continuous job losses, commercial banks may be turning the corner. The ADP National Employment report for April 2026 noted that the financial activities sector grew by 9,000 positions, 5,000 more than the previous month.

The sector added the fourth-most jobs, behind education and health services (61,000); trade, transportation, and utilities (25,000); and construction (10,000). Only professional and business services saw a decline, with 8,000 jobs lost in April.

Meanwhile, the Bureau of Labor Statistics (BLS) is both more bullish and bearish compared to the ADP findings. The BLS calculated that the economy added 115,000 non-farm payroll jobs in April, while ADP saw private sector employment increase by 109,000 jobs, based on the anonymized weekly payroll data of more than 26 million private-sector employees.

On the other hand, BLS noted that employment in financial activities “showed little change over the month.”

AI Warning

The slight upswing seen by ADP could be a reversal of monthly job losses in commercial banking from February 2025, according to research by KBRA Financial Intelligence (KFI). But there’s a catch.

“Recent declines have been markedly narrower than those recorded in 2023 and 2024, suggesting that a consolidation of the commercial banking workforce could be slowing, but the ongoing implementation of AI within the industry could continue to shrink headcount at some banks,” according to a KFI Insight report.

Growth Spurt

So, where’s the greatest job growth? At the smallest and largest organizations.

The micro/small (1-19 employees) and large enterprises (more than 500 employees) led in job growth, with 43,000 and 42,000 positions, respectively. Only companies at the upper end of the mid-sized enterprise range (250-499 employees) cut, jettisoning 3,000 jobs in April.

“Small and large employers are hiring, but we’re seeing softness in the middle,” said Dr. Nela Richardson, chief economist at ADP. “Large companies have resources to deploy, and small ones are the most nimble, both important advantages in a complex labor environment.”

Wage Worries

It’s not all good news. According to Bank of America Institute, which bases its numbers on aggregated and anonymized bank transaction data, unemployment payments continued to slow, but a large K-shape in wage growth continued into April.

“In April, higher-income households saw their after-tax wage growth rise to 6.0% year-on-year (YoY) — the highest rate we’ve observed since August 2021,” wrote the authors of the April 2026 Employment Report from the Institute.

“In fact, even within this cohort, there is a divergence, with after-tax wage growth for the highest 5% of households by income stronger than that of the rest of the higher-income cohort,” the authors noted.

“Middle- and lower-income households also saw increases in their after-tax wage growth in April, to 2.3% YoY and 1.5% YoY, respectively,” the researchers found. “But the gap between these cohorts and higher-income households remains at its widest level since our data series began in 2015.”

A humanoid robot jointly developed by KB Financial Group and GENON is demonstrated at the AI EXPO Korea 2026 in Seoul on Friday. Photo by KB Financial Group

SEOUL, May 10 (UPI) — South Korea’s KB Financial Group unveiled a humanoid robot for senior care during AI EXPO Korea 2026 held in southern Seoul.

During the three-day event last week, KB Financial showcased the humanoid robot, named “GenP,” which was jointly developed with domestic AI company GENON.

KB Financial noted that GenP was specifically designed for senior care, as it is equipped with upgraded finger-module capabilities to perform precise movements suited for assisting elderly users.

During the exhibition, the humanoid robot carried out five demonstrations, including greeting visitors and delivering daily information, such as rehabilitation schedules.

The Seoul-based financial conglomerate said that the presentation demonstrated its transition from text-based agentic AI to physical AI geared toward engaging directly with the everyday lives of senior customers.

Next month, KB Financial’s affiliate plans to introduce an AI-powered care robot, dubbed “KeBi,” at a South Korean facility for senior citizens.

South Korea is widely regarded as having one of the world’s fastest-aging societies, as the proportion of people age 65 or older topped 20% of the population. As of the end of last year, it was 21.21%, according to the Ministry of the Interior and Safety.

“Starting with this demonstration, we plan to gradually verify the feasibility of applying physical AI to care settings. Based on those results, we will further expand our service scope and business operations,” KB Financial said in a statement.

“Going forward, we will concentrate our capabilities on realizing the future of senior care solutions, which combine advanced technology and compassionate care,” it said.

The share price of KB Financial rose 0.31% on the Seoul bourse Friday.

South Korea’s Financial Supervisory Service has reportedly decided to suspend the business operations of Lotte Card for 4 1/2 months over a personal data breach, along with a $3.4 million penalty. File Photo by Jeon Heon-kyun/EPA

May 1 (UPI) — South Korea’s Financial Supervisory Service (FSS) reportedly decided Thursday to suspend the business operations of Lotte Card for 4 1/2 months over a data breach.

The financial watchdog is also reported to have finalized the disciplinary measure, including a $3.4 million penalty and a reprimand warning for its former CEO Cho Jwa-jin.

The FSS declined to confirm the reports, while Lotte Card acknowledged it.

“Imposing a business suspension over a hacking case would be an unprecedented level of sanction,” Lotte Card said in a statement.

“As follow-up procedures remain, including a resolution by the Financial Services Commission (FSC), we will fully explain our position regarding the severity of the punishment, as well as our post-incident response efforts,” it added.

Nearly 3 million Lotte Card customers had their personal information compromised last year. The state-run Personal Information Protection Commission has already imposed a $64 million fine on the firm over the incident.

Following the FSS decision, the FSC is expected to make the final call in the coming months.

In 2019, South Korea’s leading private equity company, MBK Partners, teamed up with Woori Bank to acquire a 79.8% stake in Lotte Card for about $1 billion. MBK took 59.8%, and Woori held the remaining 20%.

MBK Partners sought to sell its stake in Lotte Card in 2023 but failed to find a buyer, and a similar effort last year also yielded limited results.

A former executive at Live Nation, the world’s largest live entertainment company, is suing the company, alleging that he was wrongfully terminated after he raised concerns about alleged financial misconduct and improper accounting practices.

Nicholas Rumanes alleges he was “fraudulently induced” in 2022 to leave a lucrative position as head of strategic development at a real estate investment trust to create a new role as executive vice president of development and business practice at Beverly Hills-based Live Nation.

In his new position, Rumanes said, he raised “serious and legitimate alarm” over the the company’s business practices.

As a result, he says, he was “unlawfully terminated,” according to the lawsuit filed Thursday in Los Angeles County Superior Court.

“Rumanes was, simply put, promised one job and forced to accept another. And then he was cut loose for insisting on doing that lesser job with integrity and honesty,” according to the lawsuit.

He is seeking $35 million in damages.

Representatives for Live Nation were not immediately available for comment.

Rumanes’ lawsuit describes a “culture of deception” at Live Nation, saying its “basic business model was to misstate and exaggerate financial figures in efforts to solicit and secure business.”

Such practices “spanned a wide spectrum of projects in what appeared to be a company-wide pattern of financial misrepresentation and misleading disclosures,” the lawsuit states.

Rumanes says he received materials and documents that showed that the company inflated projected revenues across multiple venue development projects.

Additionally, Rumanes contends that the company violated a federal law that requires independent financial auditing and transparency and instead ran Live Nation “through a centralized, opaque structure” that enables it to “bypass oversight and internal checks and balances.”

In 2010, as a condition of the Live Nation-Ticketmaster merger, the newly formed company agreed to a consent decree with the government that prohibited the firm from threatening venues to use Ticketmaster. In 2019 the Justice Department found that the company had repeatedly breached the agreement, and it extended the decree.

Rumanes contends that he brought his concerns to the attention of the company’s management, but his warnings were “repeatedly ignored.”

April 22 (UPI) — Federal prosecutors Tuesday evening announced an 11-count indictment against the Southern Poverty Law Center, accusing the non-profit of defrauding donors by using their money to pay informants within hate groups they were monitoring.

Acting Attorney General Todd Blanche announced the indictment from a Montgomery, Ala., grand jury during a press conference, alleging that between 2014 and 2023, the SPLC paid more than $3 million to informants in hate groups the organization had vowed to dismantle.

“As the indictment described, the SPLC was not dismantling these groups, but it was instead manufacturing the extremism it purports to oppose by paying sources to stoke racial hatred,” he said, alongside FBI Director Kash Patel.