In a significant retrenchment, media mogul Byron Allen has retained investment banking firm Moelis & Co. to sell his network-affiliate television stations after spending more than $1 billion to scoop up outlets in smaller markets.

The Allen Media Group announced the news Monday morning. It owns nearly two dozen stations, including in Northern California near Redding, as well as Honolulu; Flint, Mich.; Madison, Wis.; and Tupelo, Miss.

The company needs to pay down debt, Allen said in a statement.

Allen’s firm declined to provide details on its finances.

The Los Angeles firm has spent big bucks during the last six years buying stations with a goal of becoming the largest independent television operator in the U.S. Many of Allen’s stations have standing in their markets with programming from one of the Big Four broadcast networks: ABC, CBS, NBC and Fox.

“We have received numerous inquiries and written offers for most of our television stations and now is the time to explore getting a return on this phenomenal investment,” Allen, chairman and chief executive, said in a statement. “We are going to use this opportunity to take a serious look at the offers, and the sale proceeds will be used to significantly reduce our debt.”

The Los Angeles entrepreneur and former stand-up comedian had been steadily expanding his empire for more than a decade.

However, the television advertising market has become increasingly challenged in recent years as media buyers shift their budgets to digital platforms where they are more likely to find younger consumers. The television advertising market has become more strained with the addition of streaming services, including Netflix, Amazon Prime Video and Paramount+ competing with legacy stations for dollars.

A decade ago, Allen brought a high-profile $20-billion lawsuit against two of the nation’s largest pay-TV distributors, Comcast and Charter Communications, alleging that racism was the reason his small TV channels were not being carried on those services.

The case ultimately reached the U.S. Supreme Court and was legally significant because it relied on the historic Civil Rights Act of 1866, which was enacted a year after the Civil War ended and mandated that Black citizens “shall have the same right … to make and enforce contracts … as is enjoyed by white citizens.”

But the Supreme Court struck down many of Allen’s arguments. In a 9-0 decision in March 2020, the high court said it was not enough for a civil rights plaintiff to assert that his race was one of several factors that motivated a company to refuse to do business with him. Instead, the person must show race was the crucial and deciding factor.

Last month, CBS picked up his show “Comics Unleashed with Byron Allen” to run at 12:35 a.m.

WASHINGTON — President Trump faces the challenge of convincing Republican senators, global investors, voters and even Elon Musk that he won’t bury the federal government in debt with his multitrillion-dollar tax breaks package.

The response so far from financial markets has been skeptical as Trump seems unable to trim deficits as promised.

“All of this rhetoric about cutting trillions of dollars of spending has come to nothing — and the tax bill codifies that,” said Michael Strain, director of economic policy studies at the American Enterprise Institute, a right-leaning think tank. “There is a level of concern about the competence of Congress and this administration and that makes adding a whole bunch of money to the deficit riskier.”

The White House has viciously lashed out at anyone who has voiced concern about the debt snowballing under Trump, even though it did exactly that in his first term after his 2017 tax cuts.

White House press secretary Karoline Leavitt opened her briefing Thursday by saying she wanted “to debunk some false claims” about his tax cuts.

Leavitt said the “blatantly wrong claim that the ‘One, Big, Beautiful Bill’ increases the deficit is based on the Congressional Budget Office and other scorekeepers who use shoddy assumptions and have historically been terrible at forecasting across Democrat and Republican administrations alike.”

House Speaker Mike Johnson (R-La.) piled onto Congress’ number crunchers on Sunday, telling NBC’s “Meet the Press,” “The CBO sometimes gets projections correct, but they’re always off, every single time, when they project economic growth. They always underestimate the growth that will be brought about by tax cuts and reduction in regulations.”

Speaker Mike Johnson has said the non-partisan Congressional Budget Office are “always underestimates growth” spurred by tax cuts.

(Kevin Dietsch / Getty Images)

But Trump himself has suggested that the lack of sufficient spending cuts to offset his tax reductions came out of the need to hold the Republican congressional coalition together.

“We have to get a lot of votes,” Trump said last week. “We can’t be cutting.”

That has left the administration betting on the hope that economic growth can do the trick, a belief that few outside of Trump’s orbit think is viable.

Most economists consider the non-partisan CBO to be the foundational standard for assessing policies, though it does not produce cost estimates for actions taken by the executive branch such as Trump’s unilateral tariffs.

Tech billionaire Musk, who was until recently part of Trump’s inner sanctum as the leader of the Department of Government Efficiency, told CBS News: “I was disappointed to see the massive spending bill, frankly, which increases the budget deficit, not just decreases it, and undermines the work that the DOGE team is doing.”

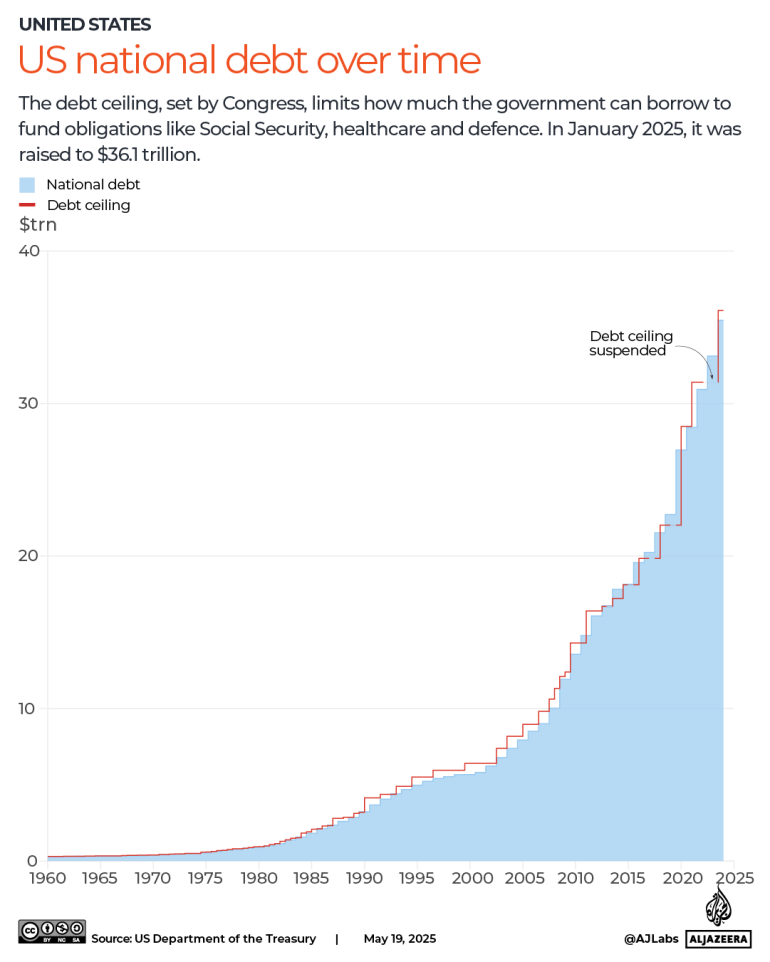

Federal debt keeps rising

The tax and spending cuts that passed the House last month would add more than $5 trillion to the national debt in the coming decade if all of them are allowed to continue, according to the Committee for a Responsible Financial Budget, a fiscal watchdog group.

To make the bill’s price tag appear lower, various parts of the legislation are set to expire. This same tactic was used with Trump’s 2017 tax cuts and it set up this year’s dilemma, in which many of the tax cuts in that earlier package will sunset next year unless Congress renews them.

But the debt is a much bigger problem now than it was eight years ago. Investors are demanding the government pay a higher premium to keep borrowing as the total debt has crossed $36.1 trillion. The interest rate on a 10-year Treasury note is around 4.5%, up dramatically from the roughly 2.5% rate being charged when the 2017 tax cuts became law.

The White House Council of Economic Advisers argues that its policies will unleash so much rapid growth that the annual budget deficits will shrink in size relative to the overall economy, putting the U.S. government on a fiscally sustainable path.

The council argues the economy would expand over the next four years at an annual average of about 3.2%, instead of the Congressional Budget Office’s expected 1.9%, and as many as 7.4 million jobs would be created or saved.

Council chair Stephen Miran told reporters that when the growth being forecast by the White House is coupled with expected revenues from tariffs, the expected budget deficits will fall. The tax cuts will increase the supply of money for investment, the supply of workers and the supply of domestically produced goods — all of which, by Miran’s logic, would cause faster growth without creating new inflationary pressures.

“I do want to assure everyone that the deficit is a very significant concern for this administration,” Miran said.

White House budget director Russell Vought told reporters the idea that the bill is “in any way harmful to debt and deficits is fundamentally untrue.”

Economists doubt Trump’s plan can spark enough growth to reduce deficits

Most outside economists expect additional debt would keep interest rates higher and slow overall economic growth as the cost of borrowing for homes, cars, businesses and even college educations would increase.

“This just adds to the problem future policymakers are going to face,” said Brendan Duke, a former Biden administration aide now at the Center on Budget and Policy Priorities, a liberal think tank. Duke said that with the tax cuts in the bill set to expire in 2028, lawmakers would be “dealing with Social Security, Medicare and expiring tax cuts at the same time.”

Kent Smetters, faculty director of the Penn Wharton Budget Model, said the growth projections from Trump’s economic team are “a work of fiction.” He said the bill would lead some workers to choose to work fewer hours in order to qualify for Medicaid.

“I don’t know of any serious forecaster that has meaningfully raised their growth forecast because of this legislation,” said Harvard University professor Jason Furman, who was the Council of Economic Advisers chair under the Obama administration. “These are mostly not growth- and competitiveness-oriented tax cuts. And, in fact, the higher long-term interest rates will go the other way and hurt growth.”

The White House’s inability so far to calm deficit concerns is stirring up political blowback for Trump as the tax and spending cuts approved by the House now move to the Senate. Republican Sens. Ron Johnson of Wisconsin and Rand Paul of Kentucky have both expressed concerns about the likely deficit increases, with Johnson saying there are enough senators to stall the bill until deficits are addressed.

“I think we have enough to stop the process until the president gets serious about the spending reduction and reducing the deficit,” Johnson said on CNN.

Trump banking on tariff revenues to help

The White House is also banking that tariff revenues will help cover the additional deficits, even though recent court rulings cast doubt on the legitimacy of Trump declaring an economic emergency to impose sweeping taxes on imports.

When Trump announced his near-universal tariffs in April, he specifically said his policies would generate enough new revenues to start paying down the national debt. His comments dovetailed with remarks by aides, including Treasury Secretary Scott Bessent, that yearly budget deficits could be more than halved.

“It’s our turn to prosper and in so doing, use trillions and trillions of dollars to reduce our taxes and pay down our national debt, and it’ll all happen very quickly,” Trump said two months ago as he talked up his import taxes and encouraged lawmakers to pass the separate tax and spending cuts.

The Trump administration is correct that growth can help reduce deficit pressures, but it’s not enough on its own to accomplish the task, according to new research by economists Douglas Elmendorf, Glenn Hubbard and Zachary Liscow.

Ernie Tedeschi, director of economics at the Budget Lab at Yale University, said additional “growth doesn’t even get us close to where we need to be.”

The government would need $10 trillion of deficit reduction over the next 10 years just to stabilize the debt, Tedeschi said. And even though the White House says the tax cuts would add to growth, most of the cost goes to preserve existing tax breaks, so that’s unlikely to boost the economy meaningfully.

Many of the world’s poorest countries are due to make record debt repayments to China in 2025 on loans extended a decade ago, at the peak of Beijing’s Belt and Road Initiative, a report by the Sydney-based Lowy Institute think tank has found.

Under the Belt and Road Initiative (BRI), a state-backed infrastructure investment programme launched in 2013, Beijing lent billions of dollars to build ports, highways and railroads to connect Asia, Africa and the Americas.

But new lending is drying up. In 2025, debt repayments owed to China by developing countries will amount to $35bn. Of that, $22bn is set to be paid by 75 of the world’s poorest countries, putting health and education spending at risk, Lowy concluded.

“For the rest of this decade, China will be more debt collector than banker to the developing world,” said Riley Duke, the report’s author.

“Developing countries are grappling with a tidal wave of debt repayments and interest costs to China,” Duke said.

What did the report say?

China’s BRI, the biggest multilateral development programme ever undertaken by a single country, is one of President Xi Jinping’s hallmark foreign policy initiatives.

It focuses primarily on developing country infrastructure projects like power plants, roads and ports, which struggle to receive financial backing from Western financial institutions.

The BRI has turned China into the largest global supplier of bilateral loans, peaking at about $50bn in 2016 – more than all Western creditors combined.

According to the Lowy report, however, paying off these debts is now jeopardising public spending.

“Pressure from Chinese state lending, along with surging repayments to a range of international private creditors, is putting enormous financial strain on developing economies.”

High debt servicing costs can suffocate spending on public services like education and healthcare, and limit their ability to respond to economic and climate shocks.

The 46 least developed countries (LDCs) spent a significant share – about 20 percent – of their tax revenues on external public debt in 2023. Lowy’s report implies this will increase even more this year.

For context, Germany used 8.4 percent of its budget to repay debt in 2023.

Lowy also raised questions about whether China will use these debts for “geopolitical leverage” in the Global South, especially with Washington slashing foreign aid under President Donald Trump.

“As Beijing shifts into the role of debt collector, Western governments remain internally focused, with aid declining and multilateral support waning,” the report said.

While Chinese lending is also beginning to slow down across the developing world, the report said there were two areas that seemed to be bucking the trend.

The first was in nations such as Honduras, Burkina Faso and Solomon Islands, which received massive new loans after switching diplomatic recognition from Taiwan to China.

The other was in countries such as Indonesia and Brazil, where China has signed new loan deals to secure critical minerals and metals for electric batteries.

How has China responded?

Beijing’s Ministry of Foreign Affairs said it was “not aware of the specifics” of the report but that “China’s investment and financing cooperation with developing countries abides by international conventions”.

Ministry spokesperson Mao Ning said “a small number of countries” sought to blame Beijing for miring developing nations in debt but that “falsehoods cannot cover up the truth”.

For years, the BRI has been criticised by Western commentators as a way for Beijing to entrap countries with unserviceable debt.

An often-cited example is the Hambantota port – located along vital east-west international shipping routes – in southern Sri Lanka.

Unable to repay a $1.4bn loan for the port’s construction, Colombo was forced to lease the facility to a Chinese firm for 99 years in 2017.

China’s government has denied accusations it deliberately creates debt traps, and recipient nations have also pushed back, saying China was often a more reliable partner than the West and offered crucial loans when others refused.

Still, China publishes little data on its BRI scheme, and the Lowy Institute said its estimates, based on World Bank data, may underestimate the full scale of China’s lending.

In 2021, AidData – a US-based international development research lab – estimated that China was owed a “hidden debt” of about $385bn.

Does the Lowy report lack ‘context’?

Challenging the “debt-trap” narrative, the Rhodium consulting group looked at 38 Chinese debt renegotiations with 24 developing countries in 2019 and concluded that Beijing’s leverage was limited, with many of the renegotiations resolved in favour of the borrower.

According to Rhodium, developing countries had restructured roughly $50bn of Chinese loans in the decade before its 2019 study was published, with loan extensions, cheaper financing and debt forgiveness the most frequent outcomes.

Elsewhere, a 2020 study by the China Africa Research Initiative at Johns Hopkins University found that, between 2000 and 2019, China cancelled $3.4bn of debt in Africa and a further $15bn was refinanced. No assets were seized.

Meanwhile, many developing countries remain in hock to Western institutions.

In 2022, the Debt Justice Group estimated that African governments owed three times more to private financial groups than to China, charging double the interest in the process.

“Developing country debt to China is less than what is owed to both private bondholders and multilateral development banks (MDBs),” says Kevin Gallagher, director of the Boston University Global Development Policy Center.

“So, Lowy’s focus on China lacks context. The truth is, even if you remove China from the creditor picture, lots of poor countries would still be in debt distress,” Gallagher told Al Jazeera.

Following the COVID-19 pandemic and Russia’s invasion of Ukraine, inflation prompted the United States Federal Reserve, as well as other leading central banks, to hike interest rates.

Attracted to higher yields in the US, investors withdrew their funds from developing country financial assets, raising yield costs and depreciating currencies. Debt repayment costs soared.

Global interest rates have since come down slightly. But according to the UN, developing country borrowing costs are, on average, two to four times higher than in the US and six to 12 times higher than in Germany.

“A crucial aspect about Chinese lending,” said Gallagher, “is that it tends to be long-term and growth enhancing. That’s precisely why a lot of it is focused on infrastructure investment. Western lenders tend to get in and out faster and charge higher rates.”

Moody’s ratings agency has stripped the US of its last perfect credit rating.

United States debt has long been considered the safest of all safe havens. But, Washington has just lost its pristine reputation as a borrower. Moody’s has downgraded the nation from its top-notch AAA rating, becoming the last of the big three agencies to do so. The ratings agency has cited the United States’s growing debt – now at $36 trillion, almost 120 percent of gross domestic product – and rising debt service costs. Against this backdrop, President Donald Trump is pushing what he calls the “one big, beautiful bill”. Critics warn his tax cut package could add trillions more to the already ballooning deficit.

Economists echo Dimon’s concerns as US credit downgrade and tariff-driven uncertainty continue.

JPMorgan Chase CEO Jamie Dimon has warned that he can’t rule out the possibility that the United States will fall into what is called stagflation— an economic term that refers to a period when inflation and unemployment are high as economic growth is slow.

In an interview with Bloomberg Television on Thursday, Dimon said, “I don’t agree that we’re in a sweet spot” in response to a question about some US Federal Reserve officials saying that the US economy was in a sweet spot.

Dimon made his comments while at JPMorgan’s Global China Summit in Shanghai. His comments come against the backdrop of the US facing increasing geopolitical tensions, rising deficits and pressure on consumer prices from changing government policies on tariffs that have led retailers to announce a need to raise prices and left businesses in a wait-and-watch mode over all the economic uncertainties.

Economists like Stuart Mackintosh, executive director of the financial think tank Group of Thirty, echoed Dimon’s concerns to Al Jazeera.

“Stagflation is a real risk we cannot rule out. We’re in a circumstance where we have uncertainty on tariffs, uncertainty on many policies that increase the downward pressure on growth in America.”

Last week Moody’s Ratings downgraded the US economy’s credit rating. The firm lowered its gold-standard Aaa to an Aa1 credit rating for the US, citing its growing national debt.

Dimon’s Thursday comments were underscored by his remarks at the company’s investor day on Monday.

“Credit today is a bad risk,” Dimon said.

While at the summit, Dimon also offered comments on US President Donald Trump’s “big beautiful bill”, the tax and spending bill passed by the US House of Representatives that includes key parts of the Trump administration agenda including tax cuts, slashes to Medicaid and the Supplemental Nutrition Assistance Program (SNAP), increased funding for immigration enforcement, and new taxes on colleges and universities.

“I think they should do the tax bill. I do think it’ll stabilise things a little bit, but it’ll probably add to the deficit,” Dimon said in a record first obtained by the Reuters news agency.

The nonpartisan Congressional Budget Office has said that the tax bill would add $3.8 trillion to the national debt.

‘Inflation going up’

In the Bloomberg interview, Dimon added that the US Federal Reserve is doing the right thing to wait and see before it decides on monetary policy. The central bank opted to hold rates steady at its last policy meeting, which was largely in line with economists’ expectations.

Policymakers weighed a stable labour market at the time, even as they acknowledged that could be short-lived.

“This is unsustainable. We might get into a much worse economic picture almost immediately,” Mackintosh said.

More information on the state of the US labour market is expected in the next couple of weeks as both the US Department of Labor and the payroll and human resources firm ADP are slated to release their monthly report on the rate of job growth.

Dimon has also long warned that inflation and stagflation will continue to increase.

“I think the chance of inflation going up and stagflation is a little bit higher than other people think,” he noted.

On Wall Street, JPMorgan Chase’s stock has trended up following Dimon’s remarks. As of noon in New York (16:00 GMT), it was 0.2 percent higher than yesterday’s market close after opening lower this morning.

The Republican-controlled US House of Representatives has passed the “Big, Beautiful Bill”, the sweeping tax and spending bill by a single vote.

The legislation, which would enact much of President Donald Trump’s policy agenda, passed early Thursday morning after an overnight session.

The bill, which is now headed to the Senate, will cut taxes, but also saddle the country with trillions of dollars more in debt.

The bill would fulfil many of Trump’s populist campaign pledges, delivering new tax breaks on tips and car loans and boosting spending on the military and border enforcement. It will add about $3.8 trillion to the federal government’s $36.2 trillion in debt over the next decade, according to the nonpartisan Congressional Budget Office.

“This is arguably the most significant piece of Legislation that will ever be signed in the History of our Country!” Trump wrote on social media.

The package passed in a 215-214 vote after a marathon push that kept lawmakers debating the bill through two successive nights.

All of the chamber’s Democrats and two Republicans voted against it, while a third Republican voted “present”, neither for nor against the bill. Another Republican missed the vote because he was asleep.

With a narrow 220-212 majority, House Speaker Mike Johnson could not afford to lose more than a handful of votes from his side, and he made several last-minute changes to satisfy various Republican factions.

“The House has passed generational, truly nation-shaping legislation,” Johnson said.

The bill is now headed to the Republican-controlled Senate, where it will likely be changed further during weeks of debate.

The 1,100-page bill would extend corporate and individual tax cuts passed in 2017 during Trump’s first term in office, cancel many green-energy incentives passed by Democratic former President Joe Biden and tighten eligibility for health and food programmes for the poor.

It also would fund Trump’s crackdown on immigration, adding tens of thousands of border guards and creating the capacity to deport up to one million people each year. Regulations on firearm silencers would be loosened.

The bill passed despite growing concerns about the US debt, which has reached 124 percent of gross domestic product (GDP), prompting a downgrade of the country’s top-notch credit rating by Moody’s last week. The US government has recorded budget deficits every year of this century, as Republican and Democratic administrations alike have failed to bring spending into alignment with revenue.

Interest payments accounted for one out of every eight dollars spent by the US government last year, more than the amount spent on the military, according to the CBO. That share is due to grow to one out of every six dollars over the next 10 years as an ageing population pushes up the government’s health and pension costs, even if Trump’s budget bill is not taken into account.

A mixed response

“We’re not rearranging deck chairs on the Titanic tonight. We’re putting coal in the boiler and setting a course for the iceberg,” said Representative Thomas Massie of Kentucky, one of the two Republicans to vote against the bill.

The growing debt has paradoxically given urgency for Republicans to pass the bill, as it would raise the federal government’s debt ceiling by $4 trillion. That would avert the prospect of a default, which officials have warned could otherwise come sometime in the middle of this year.

Republicans have also argued that failure to pass the bill would mean an effective tax hike for many Americans, as Trump’s 2017 tax cuts are due to expire at the end of the year.

Hardliners on the party’s right flank had pushed for deeper spending cuts to lessen the budget impact, but they met resistance from centrists who worried that would fall too heavily on the 71 million low-income Americans enrolled in the Medicaid health programme. Johnson made changes to address conservatives’ concerns, pulling forward new work requirements for Medicaid recipients to take effect at the end of 2026, two years earlier than before. That would kick several million people off the programme, according to the CBO. The bill also would penalise states that expand Medicaid in the future.

Johnson also expanded a deduction for state and local tax payments from $30,000 to $40,000, which was a priority for a handful of centrist Republicans who represent high-tax states like New York and California. Democrats blasted the bill as disproportionately benefitting the wealthy while cutting benefits for working Americans. The CBO found it would reduce income for the poorest 10 percent of US households and boost income for the top 10 percent.

“This bill is a scam, a tax scam designed to steal from you, the American people, and give to Trump’s millionaire and billionaire friends,” Democratic Representative Jim McGovern said.

Investors, unnerved by the fiscal position of the US and Trump’s erratic tariff moves, are increasingly selling the dollar and other US assets that make up the bedrock of the global financial system. The three major indices the Dow, Nasdaq and S&P 500 are trending upwards slightly after its worst day in a month following a bond market sell-off yesterday.

JPMorgan Chase Chief Executive Jamie Dimon gave a mixed response to the bill’s passage.

“I think they should do the tax bill. I do think it’ll stabilise things a little bit, but it’ll probably add to the deficit,” Dimon said at JPMorgan’s Global China Summit in Shanghai.

The “One Big Beautiful Bill” is one big, ugly mess.

We’ve seen false advertising in naming laws before — the Democrats’ 2022 Inflation Reduction Act jumps to mind. Yet no legislation has been as misbranded as the Republican tax and spending cuts that President Trump, the branding aficionado himself, is pushing along a tortuous path in Congress.

Trump’s appeal to many Americans has always been his purported penchant for “telling itlike it is.” But he’s doing the opposite by labeling as the “One Big Beautiful Bill” a behemoth that encompasses just about everything he can’t even try to do by unilateral executive orders — deeper tax cuts, more spending on the military and on his immigration crackdown and, yes, Medicaid cuts. His so-called beauty is a beast so frightening that ratings firm Moody’s saw the details last week, calculated the resulting debt and on Friday downgraded the United States’ sterling credit rating for the first time in more than 100 years. That likely means higher interest costs for the nation’s increased borrowing ahead.

And yet, in another example of the gaslighting at which Trump and his party are so adept, the White House and House Republican leaders dismissed the rebuke of their bill. Treasury Secretary Scott Bessent said it would spur economic growth — the old, discredited “tax cuts will pay for themselves” argument. Speaker Mike Johnson said the Moody’s downgrade just proved the urgent need to pass the big, beautiful bill with its “historic spending cuts.” Which only proved that Johnson didn’t read Moody’s rationale, explaining that spending cuts would be far exceeded by tax cuts, thereby reducing the government’s revenues and piling up more debt.

The Republican Party, which postures as the fiscally conservative of the two parties despite decades of evidence to the contrary, would add about $4 trillion in debt over the next 10 years if its bill becomes law, according to Moody’s. Other nonpartisan analyses — including from the Congressional Budget Office, the Committee for a Responsible Federal Budget and the Penn Wharton Budget Model of the University of Pennsylvania, similarly project additional debt in the $3-trillion-plus to $5-trillion range, more if the tax cuts are made permanent as Trump and Republicans want.

No surprise: Trump, after all, set a record for the most debt in a single presidential term: $8.4 trillion during Trump 1.0, nearly twice what accrued under his successor, President Biden. Most of Trump’s first-term red ink stemmed from his 2017 tax cuts and spending, which predated the COVID-19 pandemic and the government’s costly response.

“This bill does not add to the deficit,” White House Press Secretary Karoline Leavitt insisted to reporters on Monday, showing yet again why such a facile dissembler was chosen to speak for the habitually prevaricating president.

“That’s a joke,” Republican Rep. Thomas Massie of Kentucky responded.

Worse, it’s a lie.

And no surprise here, either, but Trump’s tariffs — another economic monstrosity that he’s declared “beautiful” — aren’t paying for this bill despite his claims. Yet the president repeated that falsehood on Tuesday (along with others), when he visited the Capitol to strong-arm Republican dissidents, including Massie, into supporting the measure ahead of a House vote. (Inside a closed caucus with House Republicans, the president reportedly called for Massie to be unseated; the Kentuckian remains opposed.)

“The economy is doing great, the stock market is higher now than when I came to office. And we’ve taken in hundreds of billions of dollars in tariff money,” Trump told reporters at the Capitol. Every point a lie.

(This week provided yet more evidence that he’s utterly wrong to keep insisting that foreign countries pay his tariffs, not American consumers. After Walmart, the largest U.S. retailer, said late last week that it would have to raise prices, Trump posted that it should “ ‘EAT THE TARIFFS.’ ” He added: “I’ll be watching, and so will your customers!!!” This after a Walmart exec said that “the magnitude of these increases is more than any retailer can absorb.”)

While details of the budget bill shift as Republican leaders dicker with their dissidents, here’s the ugly general outline, according to Penn Wharton:

Extending and expanding Trump’s 2017 tax cuts, which otherwise expire this year, would cost nearly $4.5 trillion over 10 years, $5.8 trillion if the cuts are permanent. (Mandating that tax cuts expire after a time, as Trump did in 2017, is an old budget gimmick to understate a bill’s cost. The politicians know they’ll just extend the tax breaks, as we’re seeing now.) The bill’s proposed spending increases for the military, immigration enforcement and deportations would cost about $600 billion more.

Spending cuts over 10 years, mostly to Medicaid as well as to Obamacare, food stamps and clean-energy programs, would save about $1.6 trillion. That offsets as little as one-quarter of the cost of Trump’s tax cuts and added spending.

Also, the bill is inequitable. The tax cuts would disproportionately favor corporations and wealthy Americans. Its spending cuts, however, would mostly cost lower- and some middle-income people who benefit from federal health and nutrition programs. Changes to Medicaid, including a work requirement (92% of recipients under 65 already work full or part-time, according to the health research organization KFF), and to Obamacare would leave up to 14 million people without health insurance.

Penn Wharton found that people with household income less than $51,000, for example, would see their after-tax income reduced if the bill becomes law, and the top 0.1% of income-earners would get hundreds of thousands of dollars more over the next 10 years. Beyond that time, Penn Wharton projected, “all future households are worse off” given the long-term impact of spiraling debt and a tattered safety net.

“Don’t f— around with Medicaid,” Trump told Republicans at the Capitol, according to numerous reports. How cynical, given that he was pressuring them to vote for a bill that would do just that.

All of which recalls an acronym that’s popular these days: FAFO.

Public spending cuts across six African countries have resulted in the incomes of health and education workers falling by up to 50 percent in five years, leaving them struggling to make ends meet, according to international NGO ActionAid.

The Human Cost of Public Sector Cuts in Africa report published on Tuesday found that 97 percent of the healthcare workers it surveyed in Ethiopia, Ghana, Kenya, Liberia, Malawi and Nigeria could not cover their basic needs like food and rent with their wages.

The International Monetary Fund (IMF) is to blame for these countries’ failing public systems, the report said, as the agency advises governments to significantly cut public spending to pay back foreign debt. As the debt crisis rapidly worsens across the Global South, more than three-quarters of all low-income countries in the world are spending more on debt servicing than healthcare.

“The debt crisis and the IMF’s insistence on cuts to public services in favour of foreign debt repayments have severely hindered investments in healthcare and education across Africa. For example, in 2024, Nigeria allocated only 4% of its national revenue to health, while a staggering 20.1% went toward repaying foreign debt,” said ActionAid Nigeria’s Country Director Andrew Mamedu.

The report highlighted how insufficient budgets in the healthcare system had resulted in chronic shortages and a decline in the quality of service.

Women also appear to be disproportionally affected.

“In the past month, I have witnessed four women giving birth at home due to unaffordable hospital fees. The community is forced to seek vaccines and immunisation in private hospitals since they are not available in public hospitals. Our [local] health services are limited in terms of catering for pregnant and lactating women,” said a healthcare worker from Kenya, who ActionAid identified only as Maria.

Medicines for malaria – which remains a leading cause of death across the African continent, especially in young children and pregnant women – are now 10 times more expensive at private facilities, the NGO said. Millions don’t have access to lifesaving healthcare due to long travel distances, rising fees and a medical workforce shortage.

“Malaria is an epidemic in our area [because medication is now beyond the reach of many]. Five years ago, we could buy [antimalarial medication] for 50 birrs ($0.4), but now it costs more than 500 birr ($4) in private health centres,” a community member from Muyakela Kebele in Ethiopia, identified only as Marym, told ActionAid.

‘Delivering quality education is nearly impossible’

The situation is equally dire in education, as budget cuts have led to failing public education systems crippled by rising costs, a shortage of learning materials and overcrowded classrooms.

Teachers report being overwhelmed by overcrowded classrooms, with some having to manage more than 200 students. In addition, about 87 percent of teachers said they lacked basic classroom materials, with 73 percent saying they paid for the materials themselves.

Meanwhile, teachers’ wages have been gradually falling, with 84 percent reporting a 10-15 percent drop in their income over the past five years.

“I often struggle to put enough food on the table,” said a teacher from Liberia, identified as Kasor.

Four of the six countries included in the report are spending less than the recommended one-fifth of their national budget on education, according to the UNESCO Institute for Statistics.

“I now believe teaching is the least valued profession. With over 200 students in my class and inadequate teaching and learning materials, delivering quality education is nearly impossible,” said a primary school teacher in Malawi’s Rumphi District, identified as Maluwa.

Action Aid said its report shows that the consequences of IMF-endorsed policies are far-reaching. Healthcare workers and educators are severely limited in the work they can do, which has direct consequences on the quality of services they can provide, it said.

“The debt crisis and drive for austerity is amplified for countries in the Global South and low-income countries, especially due to an unfair global economic system held in place by outdated institutions, such as the IMF,” said Roos Saalbrink, the global economic justice lead at ActionAid International. “This means the burden of debt falls on those most marginalised – once again. This must end.”

On Sunday, a key congressional committee in the United States approved President Donald Trump’s new tax cut bill, which could pass in the House of Representatives later this week.

The bill extends Trump’s 2017 tax cuts and may add up to $5 trillion to the national debt, deepening worries after a recent US credit ratings downgrade by Moody’s on Friday, which cited concerns about the nation’s growing $36 trillion debt.

The US has the highest amount of national debt in the world and is facing growing concerns about its long-term fiscal stability.

What is US debt?

Debt is simply the total amount of money the US government owes to its lenders, currently amounting to $36.2 trillion. This represents 122 percent of the country’s annual economic output or gross domestic product (GDP), and it is growing by about $1 trillion every three months.

The highest debt-to-GDP ratio was during the pandemic in 2020, when the ratio hit 133 percent. The US is among the top 10 countries in the world with the highest debt-to-GDP ratio.

What is the debt ceiling, and why does it keep increasing?

When the government spends more money than it collects, it creates a deficit.

To cover this deficit, the government borrows more money. To ensure that borrowing is subject to legislative approval, the US Congress sets a limit to how much the government can borrow to fund existing obligations like Social Security, healthcare and defence. This limit is known as the debt ceiling.

Once the ceiling is reached, the government cannot borrow more unless Congress raises or suspends the limit. Since 1960, Congress has raised, suspended or changed the terms of the debt ceiling 78 times, allowing the US to borrow more money.

The federal deficit under different presidents

The federal deficit is how much more money the government spends than it brings in during a single year. A federal surplus would mean the US is bringing in more money than it is spending.

The deficit grew sharply during Trump’s first term, especially in 2020 during the COVID-19 pandemic, when the government spent heavily while tax revenues dropped due to job losses. That year, the deficit reached nearly 15 percent of the entire economy (GDP).

Under former President Bill Clinton, there was a federal surplus – the result of favourable economic conditions such as the dot-com boom, as well as tax increases which raised more revenues.

What are Treasury bills, notes and bonds?

When the US wants to borrow money, it turns to the Treasury – the finance department of the federal government.

To borrow money, the Treasury sells various types of debt securities, such as Treasury bills, Treasury notes and Treasury bonds to investors.

These securities are essentially loans made by investors to the US government, with a promise to repay them with interest.

US Treasuries have long been considered a safe asset because the risk of the US failing to repay its investors has been very low.

Different debt securities mature over different times – this is when the debt is repaid to the investor.

Treasury bills (T-bills) are short-term and mature within one year

Treasury notes (T-notes) are medium-term and mature between 2 and 10 years

Treasury bonds (T-bonds) are long-term and mature in 20 to 30 years.

(Al Jazeera)

Who holds US debt?

Three-quarters of the $36.2 trillion US debt, approximately $27.2 trillion, is held domestically, of which:

$15.16 trillion (42 percent) is held by US private investors and entities, mostly in the form of savings bonds, mutual funds and pension funds.

$7.36 trillion (20 percent) is held by intra-governmental US agencies and trusts.

$4.63 trillion (13 percent) is held by the Federal Reserve.

Among individuals, Warren Buffett, through his company Berkshire Hathaway, is the single largest non-government holder of US Treasury bills, valued at $314bn.

Foreign investors hold the remaining quarter, valued at $9.05 trillion (25 percent).

Over the past 50 years, the share of US debt held by foreign entities has increased fivefold. In 1970, only 5 percent was owned by overseas investors; today, that figure has risen to 25 percent.

Which countries hold the most foreign debt?

Countries buy US debt because it offers a safe, stable investment for their foreign currency reserves, helps manage exchange rates and provides reliable interest income.

Foreign investors hold $9.05 trillion of debt, of which:

Japan holds $1.13 trillion

The United Kingdom holds $779.3bn, overtaking China in March as the second-largest non-US holder of treasuries

China holds $765.4bn

The Cayman Islands ($455.3bn) holds a large amount of US debt because it is a tax haven

Canada ($426.2bn)

In response to Trump’s tariffs, both Japan and China have indicated they will use their substantial holdings of US treasuries as leverage in trade negotiations with the Trump administration.

Earlier this month, Japanese Finance Minister Katsunobu Kato said Japan’s massive holding of US treasuries could be a “card on the table” in trade negotiations.

Similarly, China has been gradually selling US treasuries for years. In February, China’s US treasury holdings dropped to their lowest level since 2009, reflecting efforts to diversify reserves and ongoing trade tensions.

(Al Jazeera)

What does high US debt mean for the average American?

If the US government is spending more on debt interest repayments, it can affect budgets and public spending as it becomes more costly for the government to sustain itself.

The government may raise taxes to generate more revenue to pay down its national debt, increasing costs for average people. Increasing debt could also lead to higher interest rates, making mortgages, car loans and credit card debt more expensive.

May 17 (UPI) — Moody’s Ratings downgraded U.S. debt, becoming the last of the three major credit rating agencies to move in that direction.

The New York-based agency downgraded government long-term issuer and senior unsecured ratings to Aa1 from Aaa this week, while also changing its outlook to negative from a previous rating of stable, Moody’s said in a media release.

“This one-notch downgrade on our 21-notch rating scale reflects the increase over more than a decade in government debt and interest payment ratios to levels that are significantly higher than similarly rated sovereigns,” Moody’s said in the company’s statement.

“Successive U.S. administrations and Congress have failed to agree on measures to reverse the trend of large annual fiscal deficits and growing interest costs. We do not believe that material multi-year reductions in mandatory spending and deficits will result from current fiscal proposals under consideration.”

Standard & Poor’s in 2011 became the first of the three nationally recognized statistical rating organizations to lower its U.S. debt rating. It later accused the Justice Department of “retaliation” for filing a $5-billion lawsuit against the credit rating agency.

Moody’s in 2023 signaled it could move in the same direction, putting U.S. banks on a negative watch list and warning of a ‘mild’ recession, and later that year lowering its outlook of U.S. debt.

The agency in November then warned of a potential downgrade.

“Over more than a decade, U.S. federal debt has risen sharply due to continuous fiscal deficits. During that time, federal spending has increased while tax cuts have reduced government revenues. As deficits and debt have grown, and interest rates have risen, interest payments on government debt have increased markedly,” Moody’s said in its statement this week.

“If the 2017 Tax Cuts and Jobs Act is extended, which is our base case, it will add around $4 trillion to the federal fiscal primary deficit over the next decade. While we recognize the U.S.’ significant economic and financial strengths, we believe these no longer fully counterbalance the decline in fiscal metrics.”

The White House attempted to shift the blame to former President Joe Biden‘s administration.

“The Trump administration and Republicans are focused on fixing Biden’s mess by slashing the waste, fraud, and abuse in government and passing The One, Big, Beautiful Bill to get our house back in order,” White House spokesperson Kush Desai told reporters Friday.

“If Moody’s had any credibility, they would not have stayed silent as the fiscal disaster of the past four years unfolded.”

Moody’s said it does not expect further downgrades in the near future.

“The U.S. economy is unique among the sovereigns we rate. It combines very large scale, high average incomes, strong growth potential and a track-record of innovation that supports productivity and GDP growth. While GDP growth is likely to slow in the short term as the economy adjusts to higher tariffs, we do not expect that the US’ long-term growth will be significantly affected,” the agency said in its statement.

Moody’s cited rising debt, saying US had repeatedly failed to end the trend of large annual fiscal deficits and interest.

Moody’s Ratings has stripped the United States government of its top credit rating, citing successive governments’ failure to stop a rising tide of debt.

On Friday, Moody’s lowered the rating from a gold-standard Aaa to Aa1. “Successive US administrations and Congress have failed to agree on measures to reverse the trend of large annual fiscal deficits and growing interest costs,” it said as it changed its outlook on the US to “stable” from “negative”.

But, it added, the US “retains exceptional credit strengths such as the size, resilience and dynamism of its economy and the role of the US dollar as global reserve currency.”

Moody’s is the last of the three major rating agencies to lower the federal government’s credit rating. Standard & Poor’s downgraded federal debt in 2011, and Fitch Ratings followed in 2023.

In a statement, Moody’s said: “We expect federal deficits to widen, reaching nearly 9 percent of [the US economy] by 2035, up from 6.4 percent in 2024, driven mainly by increased interest payments on debt, rising entitlement spending, and relatively low revenue generation.’’

Extending President Donald Trump’s 2017 tax cuts, a priority of the Republican-controlled Congress, Moody’s said, would add $4 trillion over the next decade to the federal primary deficit, which does not include interest payments.

The White House adopted an aggressive tone towards Moody’s after the ratings agency downgraded the US credit rating.

White House communications director Steven Cheung reacted to the downgrade via a social media post, singling out Moody’s economist, Mark Zandi, for criticism. He called Zandi a political opponent of Trump.

“Nobody takes his ‘analysis’ seriously. He has been proven wrong time and time again,” Cheung said.

A gridlocked political system has been unable to tackle the huge deficits accumulated by the US. Republicans reject tax increases, and Democrats are reluctant to cut spending.

On Friday, House Republicans failed to push a big package of tax breaks and spending cuts through the Budget Committee. A small group of hard-right Republican lawmakers, insisting on steeper cuts to Medicaid and President Joe Biden’s green energy tax breaks, joined all Democrats in opposing it, a rare political setback for the Republican president.

Avelo Airlines, a Texas-based budget carrier, is facing backlash from both customers and employees over its decision to operate deportation flights under a new contract with the Trump administration.

Avelo, which has been struggling financially, signed a contract with the United States Department of Homeland Security (DHS) last month to transport migrants to detention centres inside and outside the US, according to an internal company memo reviewed by the Reuters news agency.

On Monday, the airline flew its first flight under the deal from Arizona to Louisiana, data from flight-tracking services FlightAware and Flightradar24 showed.

Avelo plans to dedicate three aircraft to deportation operations and has established a charter-only base in Mesa, Arizona, specifically for these flights, according to the company memo.

The union representing Avelo’s flight attendants called the contract “bad for the airline”, and one customer has helped organise a petition urging travellers to boycott the airline.

US President Donald Trump has launched a hardline crackdown on undocumented immigration, including the deportation of Venezuelan migrants he accuses of being gang members to a maximum-security prison in El Salvador. Immigration authorities also detained and moved to deport some legal permanent US residents. Trump’s policies have triggered a rash of lawsuits and protests.

Tricia McLaughlin, assistant secretary for public affairs at DHS, said Immigration and Customs Enforcement (ICE) was deporting illegal aliens who broke the country’s laws. She called the protests “nothing more than a tired tactic to abolish ICE by proxy”.

“Avelo Airlines is a sub-carrier on a government contract to assist with deportation flights,” McLaughlin said in a statement. “Attacks and demonization of ICE and our partners is wrong.”

On defence

The airline on Wednesday confirmed its long-term agreement with ICE and said it was vital to Avelo’s financial stability. It also shared a statement from CEO Andrew Levy acknowledging that it is a “sensitive and complicated topic”, but saying that the decision on the contract came “after significant deliberations”.

The statement added that the deal would keep the airline’s “more than 1,100 crewmembers employed for years to come”.

Avelo said it will use three Boeing 737-800 planes in Mesa, Arizona.

“Flights will be both domestic and international,” the company said, declining to share more details of the agreement.

Avelo, which launched in 2021, was forced to suspend its most recent fundraising round after reporting its worst quarterly performance in two years.

In a message to employees last month, Levy said the airline was spending more than it earned from its customers, forcing it to seek repeated infusions of capital from investors.

“I realize some may view the decision to fly for DHS as controversial,” Levy wrote in the staff memo, which was reviewed by Reuters, but said the opportunity was “too valuable not to pursue”.

Widespread backlash

The Association of Flight Attendants-CWA, which represents Avelo’s crew, has urged the company to reconsider its decision, which it said would be “bad for the airline”.

“Having an entire flight of people handcuffed and shackled would hinder any evacuation and risk injury or death,” the union said. “We cannot do our jobs in these conditions.”

The Trump administration has deported hundreds of migrants labelled as Venezuelan gang members to El Salvador. Photos and videos have shown deportees in handcuffs and shackles.

Customers have also expressed outrage. Anne Watkins, a New Haven, Connecticut, resident, said she has stopped flying with Avelo. She and her co-members at the New Haven Immigrants Coalition have launched an online petition urging travellers to boycott the airline until it ends its ICE flight operations. The petition has garnered more than 38,000 signatures.

Watkins, 55, said the coalition also organised a vigil on Monday to mark the launch of Avelo’s deportation flights.

“Companies can decide to operate in wholly ethical and transparent ways,” she said. “Avelo is not choosing to do that right now.”

Connecticut Attorney General William Tong, a Democrat, has threatened to review the state’s incentives for Avelo, which has received more than $2m in subsidies and tax breaks.

In California, Los Angeles resident Nancy K has co-founded a campaign called “Mothers Against Avelo”. She plans to lead weekly protests every Sunday in May at Hollywood Burbank airport, one of Avelo’s six operating bases.

Fault Lines and Mother Jones investigate how a private equity firm gutted a hospital chain for profit, endangering patients.

Fault Lines and Mother Jones magazine investigate how a private equity firm gutted a major United States hospital chain in pursuit of profit, leaving patients without critical care and families shattered.

The film follows Nabil Haque, whose wife died after childbirth at a Boston hospital that lacked essential equipment. It also tells the story of Lisa Malick, whose newborn daughter died after delays at a Florida facility that lacked a functioning neonatal intensive care unit. Together, their stories reveal the devastating consequences of turning healthcare into a business.

The investigation uncovers how Steward Health Care executives drained hospitals of resources, saddled them with crushing debt and triggered one of the largest hospital bankruptcies in US history – while walking away with millions.