Paramount may have landed Warner Bros., now comes the baggage

It took months of effort, lobbying and mounds of cash for Paramount Skydance to finally clinch its prize of Warner Bros. Discovery.

Now, however, the David Ellison-led company faces a long and challenging road to merge these two media giants and set it up for a successful future.

Key to that will be striking a delicate balancing act between investment and paying down its debt load of $79 billion, which is massive even by Hollywood standards.

Notably, the figure is even greater than Warner’s nearly $55 billion of debt post-merger with Discovery, a burden that hamstrung the company for years and led to successive rounds of layoffs and relentless cost cutting.

Last week, my colleague Meg James wrote about the concerns Fitch Ratings and S&P Global Ratings have about Paramount’s credit, given the mountain of debt the company will now carry. Fitch downgraded its credit to BB+ — “junk” territory — from BBB-, and S&P Global Ratings placed the company’s ratings on “negative watch.”

Carrying that amount of debt comes with significant risks.

For one, a company with a lot of debt that is “junk”-rated is going to be under pressure to cut costs. “Junk status” means a company’s debt is rated below the level that credit agencies consider investment grade. Such a rating means it can be more expensive to refinance or take out new loans, raising the cost of capital.

Paramount executives have already said they plan to find $6 billion in “synergies” within three years, though they’ve emphasized that the majority of their cost cutting will come from “non-labor sources,” including consolidating their streaming technology and cloud providers, combining IT systems across the company and “optimizing the combined real estate footprint and the broader corporate overhead,” among other ideas.

And as I wrote last week, most Hollywood observers and those familiar with Ellison’s plans predict that Paramount will be forced make steep layoffs to offset the cost of the deal and eliminate overlapping roles and functions between the two historic studios.

At the same time, in order to compete with well-funded rivals, Paramount-Warner Bros. will also need to invest in new programming — something that can be difficult for a heavily leveraged business .

Paramount executives have said their cost-cutting efforts won’t include a reduction in production capacity, and Ellison has reiterated that there will be continued spending on programming. Beyond content, he’ll also likely need to invest in improving the technology along with the look and feel of the streaming platforms.

“Whether or not they have the capital to do all of that and to try to get their leverage down is something I’m curious to hear about,” said Naveen Sarma of S&P Global Ratings.

It’s possible that Paramount may not be able to pursue a good opportunity in the future because it has used up all its debt capacity and can’t raise additional financing, said Kelly Shue, a professor of finance at Yale School of Management.

“It might cause them to underinvest in good projects in the future,” she said.

And the company needs to spend on good projects.

The economics of this deal hinge on the combined heft of Paramount and Warner’s two libraries and valuable intellectual property, which will unite Harry Potter, DC Studios, SpongeBob SquarePants and “Mission Impossible” all under one roof.

Building up its streaming platform, which will combine Paramount+ with HBO Max, is important for competing with the behemoth Netflix, which bowed out of the Warner Bros. auction.

And on the theatrical side, Ellison has said the combined company will release 30 films a year — 15 from each studio. That would be a substantial increase from 2025, when the two companies released 18 films — eight at Paramount and 10 from Warner Bros.

“While studios content budgets might not come under immediate focus for cost cutting, we have a hard time seeing no content costs savings considering opportunities to reallocate or pull back from at least the linear networks,” MoffettNathanson’s Robert Fishman wrote in a note to clients last week.

Of course, all of this would come only after the deal’s completion. On the immediate horizon, Paramount needs to secure international regulatory approval as well as at home. Although state attorneys general including Rob Bonta of California have said this is not a “done deal,” most analysts expect that any opposition there is only likely to slow — not stop — the transaction.

A very masculine year in film

A recent study from San Diego State University put a number on something we all suspected: The percentage of female protagonists in the top 100 films last year dropped. A lot.

Female protagonists made up just 29% of the top-grossing films in 2025, down from 42% in 2024, according to the university’s annual study of women’s representation in top films. A selection of film titles from the last year says it all: “The Running Man,” “A Working Man,” “Superman.”

That 29% figure has, unfortunately, been very consistent over the years — it was the same in 2016 and has largely hovered in the range of high 20s to low 30s for the last decade, with a few exceptions (40% in 2019 and 42% in 2024).

Focusing on just the protagonists in the top 100 films means that small fluctuations can change that percentage greatly.

But when the study looked at a broader sample size of the more than 1,900 characters in those films, the results weren’t much better.

The percentage of women in speaking roles was 38%, up just 1% from 2024. And the percentage of major female characters declined to 36% in 2025 from 39% the year before.

The fact that these figures have not moved much, in spite of the countless panels and think pieces about the issue, suggests there isn’t much will in Hollywood to change, said Martha Lauzen, author of the study and founder and executive director of San Diego State’s Center for the Study of Women in Television and Film.

“Representation is social relevancy and social capital,” she told me. “So when you see fewer women than men, that’s a message.”

Stuff We Wrote

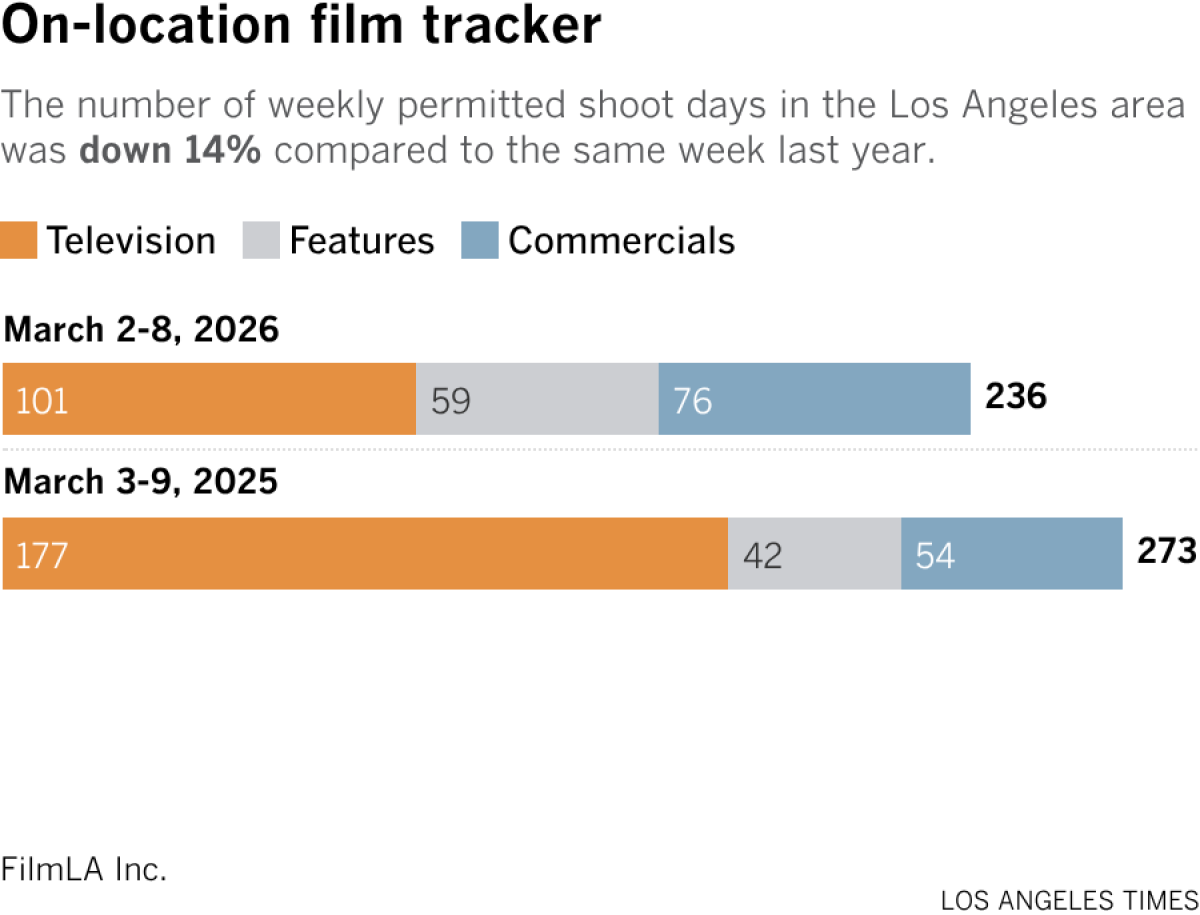

Film shoots

Number of the week

Walt Disney Co. and Pixar’s “Hoppers” came in big at the box office this weekend with a $46-million opening in the U.S. and Canada — the strongest domestic debut for an original animated movie since “Coco” in 2017. Globally, the film made $88 million.

The reception is an encouraging sign for original animated movies, which have largely struggled at the box office since the COVID-19 pandemic while their sequel counterparts have shined.

What I’m watching

Several months ago, some friends and I started a movie club, where we each nominate a film we want to watch and we rotate who gets to make the final selection. Last week, we watched the 1996 comedy “First Wives Club,” which I had never seen but loved for its goofy antics, unexpected song-and-dance number and the focus on the enduring power of female friendships.