Karooooo performed well in the second quarter, but investors may be concerned about how the company’s results will hold up during the rest of fiscal 2026.

Here’s our initial take on Karooooo‘s (KARO -12.09%) second-quarter financial report.

Key Metrics

Metric

Q2 2025

Q2 2026

Change

vs. Expectations

Revenue

ZAR1.11 billion

ZAR1.34 billion

+21%

Beat

Earnings per share (adjusted)

ZAR7.35

ZAR8.28

+13%

Beat

Cartrack subscribers

2.14 million

2.46 million

+15%

n/a

Gross margin

70%

68%

-2 pp

n/a

Subscription Revenue Growth Accelerates

Karooooo’s overall revenue rose by 21% year over year in the second quarter, a bit faster than the 18% growth rate the company reported in the first quarter. Subscription revenue from its Cartrack vehicle tracking service increased by 20%, also an acceleration compared to the first quarter. Cartrack subscription revenue accounted for roughly 90% of Karooooo’s total revenue.

The total number of Cartrack subscribers jumped by 15% year over year to 2.46 million. The company added 70,740 net new Cartrack subscribers during the second quarter, a slowdown compared to the 89,168 additions in the same period last year. Outside of Cartrack, the delivery-as-a-service offering from Karooooo Logistics saw revenue soar 38% year over year to ZAR139 million. Karooooo owns 74.8% of Karooooo Logistics, while Cartrack is wholly owned.

Overall gross margin dipped slightly in the second quarter, but the company still grew adjusted earnings per share by 13%. Operating margin was 26%, down from 27% in the prior-year period, although Cartrack’s operating margin remained steady at 29%. The company is investing in sales and marketing to acquire new customers, with sales and marketing expenses up 34% in the second quarter. This spending is putting some pressure on the bottom line.

Immediate Market Reaction

Shares of Karooooo were down about 12% by late Wednesday morning. The stock has more than doubled since the start of 2024, so while the company’s results were generally positive, valuation could be playing a role in the decline. Karooooo’s forward price-to-earnings ratio topped 30 earlier this year, and it sits around 25 following Wednesday morning’s slump.

What to Watch

Karooooo maintained its previous guidance for fiscal 2026 after adjusting for the impact of a secondary public offering in June. The company expects Cartrack subscription revenue to grow by 16% to 21% for the full year, while operating margin should come in between 26% and 31%. Karooooo also expects adjusted earnings per share in a range of ZAR32.50 to ZAR35.50.

The lack of a guidance increase or a narrowing of its guidance ranges despite accelerating Cartrack subscription revenue could be one reason why the stock sank on Wednesday. Given the macroeconomic backdrop, caution is likely warranted. Karooooo performed well in the second quarter, but investors may be concerned about how the company’s results will hold up during the rest of fiscal 2026.

Helpful Resources

Timothy Green has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Karooooo. The Motley Fool has a disclosure policy.

On October 14, 2025, CCLA Investment Management disclosed it had sold its entire position in NICE(NICE -1.26%) in an estimated $120.03 million transaction.

What Happened

According to a filing with the Securities and Exchange Commission dated October 14, 2025, CCLA Investment Management exited its holding in NICE by selling all 710,865 shares, with an estimated trade value of $120.03 million.

What Else to Know

CCLA Investment Management sold out of NICE, reducing its post-trade stake to zero; the position now represents 0% of 13F AUM.

Top holdings following the filing:

NASDAQ:MSFT – $369.63 million (5.9% of AUM) as of September 30, 2025

NASDAQ:GOOGL – $345.87 million (5.5% of AUM) as of September 30, 2025

NASDAQ:AMZN – $269.0 million (4.3% of AUM) as of September 30, 2025

NASDAQ:AVGO – $207.92 million (3.3% of AUM) as of September 30, 2025

NYSE:V – $180.65 million (2.9% of AUM) as of September 30, 2025

As of October 13, 2025, shares of NICE were priced at $132.00, marking a 23.8% decrease over the year ended October 13, 2025. Over the same period, shares have underperformed the S&P 500 by 35.5 percentage points.

Company Overview

Metric

Value

Revenue (TTM)

$2.84 billion

Net Income (TTM)

$541.15 million

Price (as of market close 2025-10-13)

$132.00

One-Year Price Change

(23.83%)

Company Snapshot

NICE Ltd. delivers AI-powered cloud software solutions designed to optimize customer experience and enhance compliance for enterprises and public sector organizations worldwide. The company leverages a broad portfolio of proprietary platforms and analytics tools to address complex business needs in digital transformation, financial crime prevention, and operational efficiency.

The company offers AI-driven cloud platforms for customer experience, financial crime prevention, analytics, and digital evidence management, including flagship products such as CXone, Enlighten, and X-Sight.

NICE Ltd. serves a global client base of enterprises, contact centers, financial institutions, and public safety agencies seeking advanced automation, compliance, and customer engagement solutions. It operates a subscription-based business model, generating revenue from cloud services, software licensing, and value-added solutions for enterprise and public sector clients.

Foolish Take

In a recent regulatory filing, CCLA Investment Management revealed that it has completely sold out of its ~$120 million position in NICE, an Israeli software company. This move comes following a tough period for NICE stock.

Over the last five years, the company’s stock has consistently underperformed the broader market. Shares have logged a total return of (44%) over this period, equating to a compound annual growth rate (CAGR) of (11%). This compares quite unfavorably to the S&P 500, which has generated a total return of 105% over the last five years, equating to a CAGR of 15%.

All that said, NICE’s stock performance doesn’t reflect its underlying fundamentals. Total revenue, net income, and free cash flow have all increased significantly over the last five years, indicating strength in the company’s business model, which relies on artificial intelligence (AI) to power applications serving contact centers, financial institutions, and public safety organizations. Moreover, the company recently announced plans to buy back up to $500 million worth of its outstanding shares, which could help put a floor under its share price.

While CCLA’s recent sale does indicate the deterioration of some institutional support, retail investors may want to take a look at NICE — an under-the-radar AI growth stock.

Glossary

13F reportable assets: Assets disclosed by institutional investment managers in quarterly SEC Form 13F filings.

AUM (Assets Under Management): The total market value of investments managed by a fund or investment firm on behalf of clients.

Quarterly average price: The average price of a security over a specific quarter, often used to estimate transaction values.

Post-trade stake: The number of shares or value held in a position after a trade is completed.

Flagship products: A company’s leading or most prominent products, often representing its brand or core offerings.

Cloud platforms: Online computing environments that provide scalable software and services over the internet.

Digital evidence management: Systems for storing, organizing, and analyzing electronic data used in investigations or compliance.

Financial crime prevention: Technologies and practices designed to detect and stop illegal financial activities, such as fraud or money laundering.

Compliance: Adhering to laws, regulations, and industry standards relevant to a business or sector.

TTM: The 12-month period ending with the most recent quarterly report.

Operational efficiency: The ability of a company to deliver products or services using minimal resources and costs.

Jake Lerch has positions in Alphabet, Amazon, and Visa. The Motley Fool has positions in and recommends Alphabet, Amazon, Microsoft, Nice, and Visa. The Motley Fool recommends Broadcom and recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

Juicy dividends are only part of the attraction with these beaten-down stocks.

Don’t just look at share price appreciation. Why? It doesn’t tell the whole story. Thousands of stocks pay dividends. And those dividends often significantly boost the stocks’ total returns.

You can especially make a lot of money when you invest in stocks with juicy dividend yields in addition to tremendous share price growth potential. Here are two ultra-high-yield dividend stocks with a total return potential of up to 41% over the next 12 months, according to select Wall Street analysts.

Kenvue

Kenvue(KVUE 1.98%) ranks as the largest pure-play consumer health company in the world. Johnson & Johnson(JNJ 0.31%) spun off Kenvue as a separate entity in 2023. The new business inherited an impressive lineup of products, including Band-Aid bandages, Listerine mouthwash, Neutrogena skin care products, and over-the-counter pain relievers Motrin and Tylenol .

In addition, Kenvue inherited J&J’s status as a Dividend King. The consumer health company has continued to increase its dividend since the spin-off two years ago. It now boasts an impressive streak of 63 consecutive annual dividend hikes. Kenvue’s forward dividend yield also tops 5.1%.

However, one reason why Kenvue’s yield is so high is that its stock has performed dismally. Revenue growth has been weak. Profits have declined sharply since the company became a stand-alone entity.

More recently, Kenvue announced a shake-up at the top in July with Kirk Perry stepping in as interim CEO while Thibaut Mongon was shown the door. The company also underwent a public relations crisis after President Donald Trump and Secretary of Health and Human Services Robert F. Kennedy Jr. claimed that the use of Tylenol during pregnancy could be linked with autism in children.

Kenvue responded quickly to refute those claims adamantly. So did several healthcare organizations, including the American College of Obstetricians and Gynecologists, the American Academy of Pediatrics, the Autism Science Foundation, and the Society for Maternal-Fetal Medicine.

Several Wall Street analysts think that the worst could be over for Kenvue. For example, Bank of America(BAC 5.11%) and JPMorgan Chase(JPM 2.80%) have price targets for the stock that reflect an upside potential of roughly 29%. If they’re right and Kenvue continues to pay dividends at least at the current level, investors could enjoy a total return of more than 34% over the next 12 months.

United Parcel Service

United Parcel Service(UPS 0.10%) is the world’s largest package delivery company. It operates in more than 200 countries and territories. UPS delivers roughly 22.4 million packages every business day.

Image source: United Parcel Service.

Although UPS isn’t a Dividend King like Kenvue, it has a pretty good dividend pedigree. The company has increased its dividend for 16 consecutive years. It has never cut the dividend since going public in 1999. UPS’ forward dividend yield is a mouthwatering 7.9%.

The bad news is that UPS’ tremendous yield is due largely to its atrocious stock performance over the last few years. Plenty of factors contributed to this decline, including higher costs resulting from a contract with the Teamsters union and lower shipment volumes following the COVID-19 pandemic.

Management’s decision to significantly reduce the shipments handled for Amazon(AMZN 0.05%) is causing revenue to decline. The Trump administration’s tariffs are especially hurting UPS’ business in its most profitable lane between China and the U.S.

However, some analysts on Wall Street are nonetheless upbeat about UPS’ prospects. As a case in point, Citigroup‘s (C 0.66%) latest 12-month price target is around 35% higher than UPS’ current share price. With such an ambitious target and the package delivery giant’s hefty dividend yield, UPS stock could deliver a total return in the ballpark of 42%.

Are these analysts right about Kenvue and UPS?

I’m iffy about whether or not Kenvue and UPS can deliver the lofty total returns over the next 12 months that some analysts predict. However, I think both stocks could be winners for investors over the long run. Kenvue and UPS could also be solid picks for investors seeking income.

JPMorgan Chase is an advertising partner of Motley Fool Money. Citigroup is an advertising partner of Motley Fool Money. Bank of America is an advertising partner of Motley Fool Money. Keith Speights has positions in Amazon and United Parcel Service. The Motley Fool has positions in and recommends Amazon, JPMorgan Chase, Kenvue, and United Parcel Service. The Motley Fool recommends Johnson & Johnson and recommends the following options: long January 2026 $13 calls on Kenvue. The Motley Fool has a disclosure policy.

At a roundtable at the bank’s headquarters in Cairo, CIB’s leadership team discusses expansion in Africa, commitment to sustainable finance, growing digital banking tools, and the future for the bank.

Global Finance celebrated the 50th anniversary of Commercial International Bank (CIB), Egypt’s largest private sector bank and a driving force in the transformation of Egypt’s banking sector, by holding a roundtable discussion.

The event, hosted at CIB’s headquarters in Cairo, gathered the bank’s top leadership team to discuss the bank’s history, how CIB has positioned itself as the leader in Egypt’s banking sector, and how it will continue to pursue growth while delivering innovative banking services for its clients.

The panel included:

CEO and Executive Board Member Hisham Ezz Al-Arab

Deputy CEO and Executive Board Member Amr El-Ganainy

Group Chief Finance and Operations Officer and Executive Board Member Islam Zekry

Global Markets CEO Omar El-Husseiny

Chief Retail, Commercial Banking, and Financial Inclusion Executive Rashwan Hammady

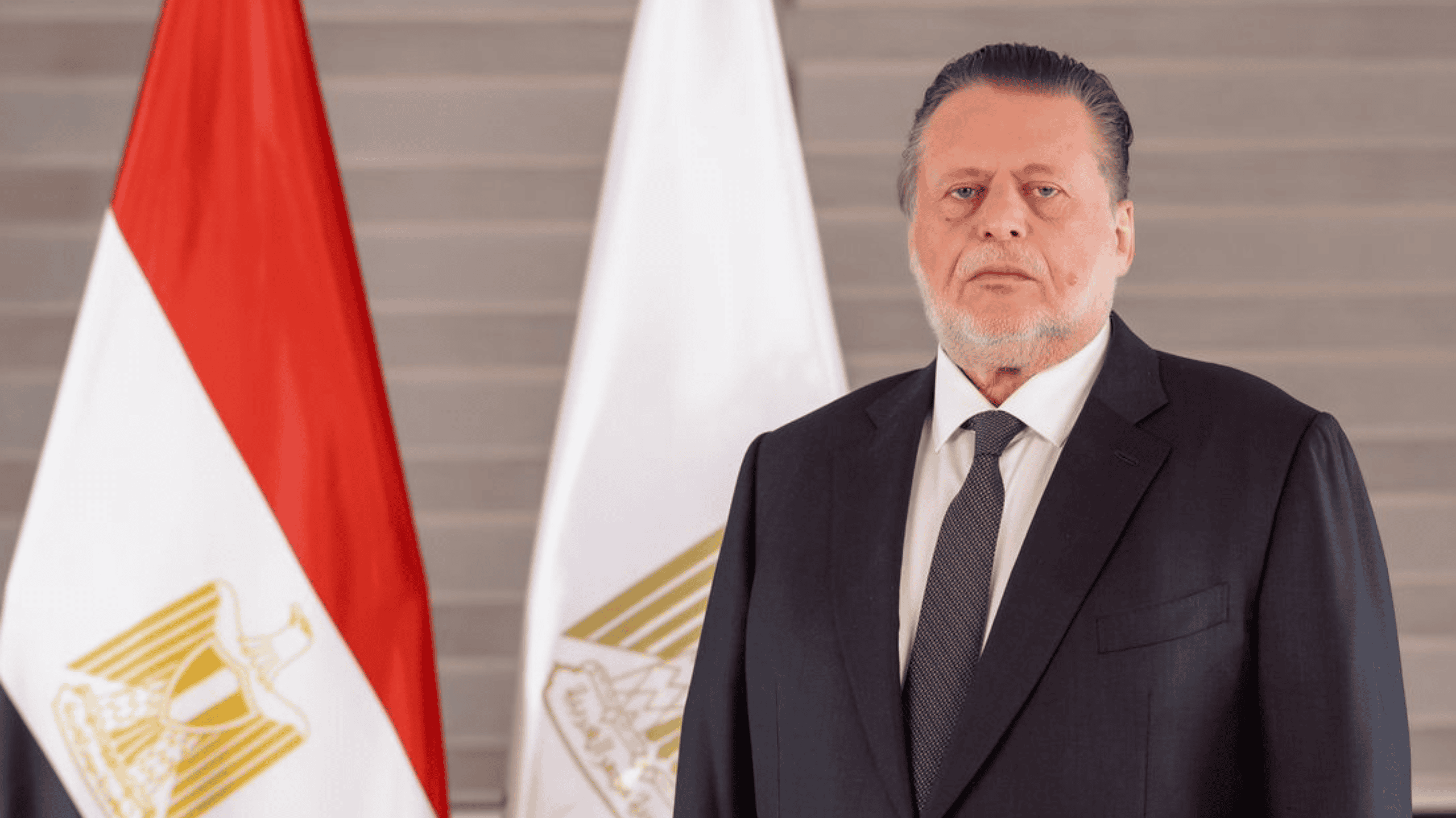

Hisham Ezz Al-Arab | CEO

Hisham Ezz Al-Arab was reappointed CEO of Commercial International Bank (CIB) – Egypt in September 2024. With over 40 years of international banking experience, he has served as CIB’s chairman (2023-2024), and as Chairman and MD (2002–2020). He also founded and chairs the CIB Foundation, which provides healthcare access for over 7 million underprivileged Egyptian children.

Global Finance: What major milestones has the bank achieved over the past 50 years, and what are some of the lessons learned?

Hisham Ezz Al-Arab: Well, you have to give credit to National Bank of Egypt (NBE) and Chase Manhattan for setting up CIB back in the 1970s, because it changed how commercial banking is being conducted. CIB at the time it was Chase National Bank—was the leader in credit lending. They changed the concept of asset lending into cash flow lending, and that was new. People used to lend against collateral and not against expected cash flow; that was a major change in the way of thinking. This was the tip of the iceberg that led the change. Below that there’s a very solid culture, to accept change, to innovate, to have something new all the time, and that carried on over the years. When I joined the bank in 1999, it was one of the large private sector banks. The management at the time and the board decided that we needed to make what you call a “major change.” We needed to be market leaders, and this was the time the bank made a lot of changes. From 1999 until about 2004, CIB was a market leader, applying all international standards and doing things really not required by domestic regulation but applied internationally.

CIB was the market leader in implementing the Basel III requirements in 2012 for asset liability management, not only for the credit flow and cash flow lending. We started to move to other areas of the commercial economy. Establishing for instance the World Risk Committee, Governance Committee, Immigration Committee, Illumination Committee—all of those things were not required by the Egyptian Law.

In 2005, NBE exited from CIB. We were very meticulous, as a board to make sure that the buyer would add value. And this is where the other journey started, in 2006. A consortium led by Ripplewood in the US became the key shareholders, with three representatives on the board. And this is another era when the bank started to change. We had solid board members who added a lot of value, selecting board members meticulously became a part of our culture. When ADQ bought a stake in CIB back in 2022, the quality of the board members was also outstanding. The critical thing is not the money, it’s the contribution of the board members.

Amr El-Ganainy | Deputy CEO

Amr El-Ganainy has served as deputy CEO and an Executive Board member of CIB since October 2023. He joined CIB in 2004 as general manager, Financial Institutions Group, and he successfully led the department through his strong business relationships in the market on the local and regional fronts.

GF: CIB has a growing presence across Africa with operations in Kenya and Ethiopia. Tell us about this experience and where the opportunities for further cross-border expansion are.

Islam Zekry: CIB’s expansion into Africa reflects our long-term vision to position the bank as a leading regional financial institution, exporting banking excellence into high-growth, strategically relevant markets. Our cross-border growth strategy prioritizes: sustainable value creation over pursuit of scale for its own sake, digital enablement to overcome infrastructure limitations and accelerate access, and facilitation of intra-African trade and investment flows, leveraging Egypt’s pivotal regional position.

Our ultimate objective is to build a resilient, scalable, and commercially viable cross-border banking model that reinforces CIB’s footprint across the continent.

So for an Egyptian bank operating from Cairo, there are two value corridors we can chase. One is the more-than-famous remittance corridor and the other is the East African trade corridor. This is basically the natural expansion for our corporate clients based here in Cairo, and this is where most of the trade exposure for the Egyptian customer is coming from.

Second, the go-to-market was completely different, because when you approach a country like Kenya, where it’s very cloudfriendly, very digitally savvy, very advanced from a payments perspective, we thought what kind of value we could bring to the market? So we brought cash flow lending and enhanced the quality of the payment processes with our global partners. By the end of the year, we will also introduce private and wealth management services.

We are ready to reposition Nairobi as our East Africa headquarters because of huge operational synergies. It’s not about expanding the footprint or putting another flag on the CIB global map; it is about amplifying Cairo and Nairobi’s synergies. We also set an exploration phase in Ethiopia and some other targets on the east coast of Africa, but what matters for us is the value creation.

Islam Zekry | Group Chief Finance and Operations Officer

Islam Zekry is the group chief finance and operations officer at CIB, serving as an Executive Board director and a member of CIB’s Executive Committee and CIB Kenya’s board. He joined CIB in 2004 and became its first chief data officer in 2016, leading data analytics and quant finance platforms.

GF: And where is the room for growth in Africa or elsewhere?

Zekry: We see strong growth potential across East Africa and tradelinked corridors in Northeast Africa. Beyond the continent, the Gulf markets and selected European hubs with strong diaspora links offer promising opportunities in remittances and digital cross-border services.

What differentiates CIB is our ability to combine deep banking expertise with local market insights, digitally enabled platforms tailored for premier banking services and underserved segments, and a client-centric model integrating transaction banking, advisory, and customer advanced and tailored solutions.

As an example, in Kenya, we’re enhancing SME lending through digital partnerships, leveraging the country’s well-developed ecosystem. We’re also advancing digital channels to scale access and deepen client engagement.

Al-Arab: Regional expansion is also about Egyptians outside of Egypt. How can we reach them and how can we facilitate their banking transactions? That’s something that is critical for our future banking services.

GF: Sustainable finance has been a true commitment for CIB. Tell us about the bank’s major achievements in this sector and CIB’s commitment to integrating sustainable finance across the board.

Amr El-Ganainy: CIB launched the first corporate green bond in Egypt, with a value of $100 million. This was a landmark transaction in Egypt and was important in supporting Egypt’s transition to a greener economy. Our aim is to play a pivotal role for all companies, and we are committed to helping the private sector transition to a more carbon-neutral future.

Zekry: At CIB, sustainable finance is not treated as a side initiative, it’s at the core of how we operate and grow.

When we partnered with the IFC to issue Egypt’s first green bond, that was virtually unheard of at the time. Today, that kind of financing is embedded in our business model. In fact, when we launched our five-year strategy just last week, ESG wasn’t a separate chapter, it was present throughout.

As we expand across Africa, a significant share of our growth will come from transitional finance, particularly in agricultural and underserved communities. We’re introducing specialized services in these areas: not just as a development goal, but because they make strong business sense.

Even internally, we’ve evolved how we assess performance. For example, our Green Asset Ratio is now a core part of our capital adequacy review, with a clear target to grow it by additional 1% to 2% annually. That’s how seriously we take it.

And to be clear, this is not just a corporate responsibility exercise. It’s part of our value creation strategy. In fact, transitional finance has been shown to deliver enhanced returns, often generating 50 to 100 basis points above conventional lending. So it’s both impactful and commercially sound.

Omar El-Husseiny | Chief Global Markets Executive

Omar El-Husseiny is the Chief Global Markets at CIB and a member of the Bank’s Executive Committee. As Chief Global Markets, he is responsible for key strategic areas including Financial Institutions, Debt Capital Markets, Treasury, Enterprise Governmental Relations, and Global Transaction Banking, ensuring alignment with the Bank’s broader growth agenda.

Mr. El-Husseiny spent his career at CIB, having joined after completing his Bachelor of Business Administration at the Faculty of Commerce at Cairo University in 2001. He holds an MBA in Banking and Finance from the Maastricht School of Management (MsM) and a Graduate School of Banking Diploma from the University of Wisconsin, Madison. In 2019, he completed the Corporate Finance & Credit Program at J.P. Morgan.

GF: Another item on top of the agenda, naturally, is digital banking and transformation. Walk us through CIB’s digital journey.

Rashwan Hammady: Our penetration of digital products across the base, whether in the consumer part, commercial banking, or SMEs or corporate banking, continues to grow over the past couple years. We’ve reached a stage where digital isn’t just about technology, it’s about understanding human needs and behavior. Our core focus now is reshaping our internal culture to understand and serve the next-generation consumer, those who are digitally native, community-led, and brand-critical. Gen Z and digital entrepreneurs will shape the next 20 years of financial services. Our job is to anticipate, not react to, how they live, earn, and make decisions. We’re embedding design thinking, real-time analytics, and personalization into our operating model. It’s less about digital “products” and more about building bespoke and lifestyle-driven experiences.

Omar El-Husseiny: Combining digital transformation and international expansion is no longer a luxury; as a financial service provider, it’s a must. This is where we see the bank moving forward. This is the only way we can expand locally and internationally, therefore, maximizing shareholder value. One takeaway from the past 50 years is how the bank continuously adapts to evolving trends and developments.

GF: How do you use digital tools to target regional expansion?

Al-Arab: For now, there are certain regulatory requirements that we are working on with the regulator, and when that is completed, it will allow us to provide services for individuals overseas. We want to do it seamlessly: simple, easy. The idea is that you are sitting on your sofa somewhere and you want to send money to your family. You don’t need to go to the bank. You want to pay your bills? You don’t need to travel. You don’t even need to make a phone call. It’s a new lifestyle. If you don’t keep developing, you will be left behind.

One thing I want to stress is that CIB is an Egyptian company. Apple is an American company. Where do you manufacture your product? That’s irrelevant. The idea that because we are an Egyptian company, we have to be local and not use the world to grow our market, is wrong. We have to use the world.

Hammady: We were one of the first players in the mobile wallet space. We’ve acquired more than 1.5 million customers via CIB’s mobile wallet. Our strategy now is more geared towards partnerships; we don’t need to build everything. So that maybe we’ll be the manufacturer of products and digital assets and a partner will be responsible for distribution, service, and access. True financial inclusion isn’t about opening accounts, it’s about changing behavior. We’ve realized that literacy and trust gaps in Egypt require a hybrid approach, yes, but more importantly, we need localized design experience. That’s why we’ve built a partnership model where we develop financial products while distribution and education are handled by partners with community reach.

This is how we unlock scale: regulatory-grade infrastructure with grassroots access. The WE partnership will bring banking to millions of new users. They have more than a thousand branches, and this partnership helps us promote financial inclusion across the country. We are expecting to launch that within the coming six to nine months, and that will cater to millions of customers, especially in non-urban communities, small cities, and villages across the country.

El-Husseiny: Egypt’s economy continues to rely heavily on cash transactions. This reliance places additional pressure on the money supply and constrains tax revenue collection, exacerbating inflation and expanding the budget deficit. Therefore, encouraging financial inclusion and digital transformation benefits CIB and the banking sector and is critical for border economic prosperity.

Rashwan Hammady is chief retail, commercial banking and financial inclusion executive at CIB. With over two decades of experience at the bank, he has spearheaded the launch of several landmark and innovative products and segment propositions, enhancing CIB’s ability to serve its growing customer base of over 3 million clients.

GF: You were mentioning partnerships. Are we talking partnerships with fintechs? With other players? How do you choose your partners?

Hammady: Our philosophy is simple: We build bespoke, compliant, scalable financial infrastructure and services; our partners provide complementary customer reach and engagement. Whether it’s telcoms, e-commerce platforms, or government entities, we choose collaborators who already command trust and attention across Egypt. This allows us to plug into ecosystems where our products become invisible, but indispensable. We’re now scaling this partner-led model not only in Egypt but also as part of our pan-African expansion.

Zekry: Our partnership model is quite unique in that it brings together three core pillars: data, digital, and design.

We’re data-driven, always seeking deeper insights into customer behavior and proactively working to enhance demand capacity. We’re digital by design, using technology to extend our reach and optimize cost-to-serve, especially in high-potential but underserved markets. And we focus strongly on experience design, because we believe that how customers engage with banking still matters, perhaps now more than ever.

When it comes to choosing partners—whether fintechs, infrastructure providers, or even talent networks—we look for alignment on those three dimensions.

We’re also deeply committed to building from the region, for the region. The team here is working tirelessly to reverse the brain drain—attracting top talent from Egypt and across Africa—to help build the banking operating system of tomorrow. We see partnerships as tactical and strategic enablers of long-term innovation.

GF: How is AI opening new doors?

Zekry: While AI has been around conceptually since the 1960s, what’s fundamentally different today is that we’re finally placing these technologies in a meaningful economic and operational context. We’re using AI and data analytics not just to automate, but to understand customer behavior, personalize services, and improve decision-making at scale.

At CIB, we’re investing heavily in building a group-wide data infrastructure: not only in Egypt, but across our African footprint. One clear opportunity lies in streamlining KYC and compliance processes. By creating an integrated data warehouse and sharing verified customer intelligence across our markets, we expect to reduce the cost to serve by 20%-30%. To put that in perspective, I recently came across a study citing EGP2 billion in redundancy costs from duplicative KYC efforts in London’s financial sector. Now imagine the potential savings if we could address that at a pan-African scale. The impact is enormous.

GF: What is the future of CIB?

El-Ganainy: Being Egypt’s largest publicly listed firm and the country’s leading private bank we set our strategy not only to respond to the opportunities emerging today, but to actively shape the Egypt of tomorrow.

We are the leaders in Egypt, and the future is expanding our leadership and investments across Africa and the Middle East.

Zekry: I see CIB evolving into a true business platform: not just in the digital sense, but as a regional and global enabler of investment, innovation, and growth.

We aspire to be a platform that attracts capital, connects businesses, and delivers a new standard of banking experiences—all while being proudly rooted in Egypt. Whether it’s manufacturers expanding from Egypt to the world or clients across Africa and beyond accessing seamless financial services, CIB will be there: facilitating, enabling, and leading.

The future of CIB is not only about being a great bank, but about becoming a trusted gateway to opportunity: for customers, investors, and the economies we serve.

El-Husseiny: I joined the bank 23 years ago, at a time when most of our work was conducted on paper. I’ve taken part in a remarkable transformation, from manual processes to desktop computers, and eventually to digital-first services. CIB will continue to be Egypt’s leading private-sector bank, and our ambition goes beyond national borders. What sets us apart is our ability to adapt to customers’ evolving needs. It’s not just about providing exceptional banking services; it’s about being a trusted financial advisor.

Integrating AI and technologies into our operations is essential. What endures is the customer experience. People will continue to need physical bank branches. CIB has significant room to grow in Egypt. During our strategy process, we asked our staff where they envision the bank in the next 5,10,20, or even 50 years.

The vast majority of our team shared a common vision: we have spent the past 50 years building a strong and successful institution in Egypt, and for the next 50 years, it’s time to expand beyond our borders. As we have developed a proven model, it is time to take that knowledge and expertise abroad, creating shared value through knowledge exchange. Expanding internationally aligns with diversity- a core element of our culture.

We’ve been very successful over the past 50 years in cultivating diversity in Egypt. It’s time to take that success global, where we believe we have the experience and strength to compete.

Hammady: Innovation, for us, is the art of institutional selfdisruption. Over the last decade, CIB has reinvented its business model multiple times: from a corporate-first bank to an inclusive, data-led, multi-segment powerhouse. We are now moving toward a model where the bank is a modular service provider, able to plug into ecosystems across borders. My belief is that our next evolution will see us not only as a bank but as a financial operating system for the region.

Al-Arab: The thing I tell the team and my colleagues is: We are as good as our dreams. You dream small, you remain small. You dream big, you will get there. Be ambitious.

For years, I parked my savings at Wells Fargo because it felt safe and familiar. The problem is it was earning almost nothing.

Wells Fargo’s standard savings account still pays just 0.01% APY, which means every $10,000 earns $1 a year in interest. One dollar.

Then I finally moved my money into a high-yield savings account (HYSA) paying around 4.00% APY, and it completely changed the math. Even if rates dip as the Fed starts cutting, I’ll still earn over $1,000 in interest over the next two years.

Here’s how that adds up, and why I keep telling everyone I know to switch.

Earning hundreds more, even if rates fall

Right now, the best HYSAs are still offering between 4.00% and 4.50% APY.

To stay realistic, let’s assume rates drop gradually:

Year 1: 3.60% APY

Year 2: 3.20% APY

I keep about $20,000 in savings. Here’s what that earns me:

Year

APY

Interest

1

3.60%

$720

2

3.20%

$640

Total (2 years)

—

$1,360

Data source: Author’s calculations.

Now compare that with Wells Fargo:

Year

APY

Interest

1

0.01%

$2

2

0.01%

$2

Total (2 years)

—

$4

Data source: Author’s calculations.

That’s a $1,356 difference, just for moving my money to a better bank.

Lower balances still earn serious money

You don’t need a big balance to make this work. Even smaller amounts can grow fast in a high-yield account.

Switching accounts used to sound intimidating, but now it’s incredibly simple. Once you open a new HYSA, you can link it to your checking account, transfer funds, and start earning immediately.

Your money stays FDIC-insured up to $250,000, just like it was at Wells Fargo — only now it’s actually working for you.

If I’d switched years ago, I’d probably have several thousand dollars more by now. Don’t make the same mistake I did.

Don’t let your bank keep your interest

It takes less than 15 minutes to move your savings to a high-yield account that pays you what your money deserves.

European stocks rose on Wednesday morning after a string of strong corporate results a day earlier, while equities were also boosted by remarks from Federal Reserve Chair Jerome Powell. In Philadelphia on Tuesday, Powell suggested that another interest rate cut could come later this month in the US.

In Europe, shares in Netherlands-headquartered ASML, which makes equipment used in the production of AI chips, jumped after the company posted promising results on Wednesday.

The shares rose more than 4%, after Europe’s largest company by market value reported third-quarter earnings fuelled by the AI boom. ASML’s stocks have rallied by almost 50% since August.

Meanwhile, on Wednesday, French multinational luxury group LVMH said its organic growth re-entered positive territory in the third quarter. The luxury giant’s shares jumped by more than 14% by 13.00 CEST.

The mood in France also shifted on news that the government had significantly improved its chances of surviving a looming no-confidence vote on Thursday.

On Tuesday, Prime Minister Sébastien Lecornu won the much-needed support of the Socialist Party in France’s National Assembly, in exchange for suspending a pension law that raises the retirement age. The CAC 40 in Paris jumped over 2% by 13.00 CEST.

The main European benchmark stock exchanges were also in the green, except for London’s FTSE 100, which lost 0.43%. Meanwhile, the DAX in Frankfurt gained less than 0.1%. Milan’s FTSE MIB was up by 0.36%, Madrid’s Ibex 35 gained 0.71% and the STOXX 600 saw a 0.6% gain.

Gold continued its rally, hitting a high of $4,217 per ounce. Gold has soared over 60% in 2025 as investors seek a safe haven during a period of uncertainty, notably driven by US tariffs and trade tensions.

Global markets are on the rise after the Fed Chair’s words

Federal Reserve Chair Jerome Powell signalled on Tuesday that the Fed is slightly more worried about the job market, raising expectations that the central bank will come through with another rate cut.

“Rising downside risks to employment have shifted our assessment of the balance of risks,” he said at a meeting of the National Association of Business Economics in Philadelphia.

Traders took his words to heart, particularly as the US government shutdown has prevented the release of fresh economic data.

“[Investors were] reading Powell like a haiku — every pause, every syllable weighed for hidden meaning,” Stephen Innes of SPI Asset Management said in a commentary.

“The message, once decoded, was clear enough: two rate cuts aren’t just a possibility, they’re the main course,” Innes said.

The central bank cut its benchmark interest rate by a quarter of a percentage point in September amid worries that unemployment could worsen.

“Markets have been lifted by the rekindling of rate cut expectations in the US after comments from Fed chair Jerome Powell, which highlighted sluggish hiring were taken as an indication that not one, but two further cuts were very much on the table for 2025,” said Danni Hewson, AJ Bell head of financial analysis.

“Buoyed by continued deal-making in the frothy AI sector, investors seem prepared to overlook the growing number of warnings about the potential for a market correction at the moment, but this earnings season will be crucial if that optimism is to continue.”

S&P 500 futures rose 0.64% during the early afternoon in Europe, while Dow Jones Industrial Average futures gained 0.41%. Nasdaq futures were up by 0.79%.

On Tuesday, US markets closed a mixed trading day, with the S&P 500 giving up 0.16% and the Dow climbing 0.44%. The Nasdaq composite dropped 0.76%.

Markets remain volatile as the US and China exchange threats of new trade sanctions and tariffs.

Technology stocks are hypersensitive to trade issues since big chipmakers and other companies rely on China for raw materials and manufacturing. China’s large consumer base is also important for its sales growth.

In other dealings early Wednesday, US benchmark crude oil was circling around $58.65 per barrel (€50.43) and Brent crude, the international standard, was traded around $62.24 (€53.52) per barrel.

The US dollar slipped 0.25% against the Japanese yen, while the euro rose 0.19% against the dollar. The British Pound gained 0.35% against the greenback.

These three stocks have strong growth opportunities still ahead.

Technology stocks continue to help lead the market higher and remain a great space to find investment ideas. Let’s look at three top tech stocks to buy right now.

1. Nvidia

There has been a lot of news recently around new artificial intelligence (AI) chip challengers, but Nvidia(NVDA -4.33%) remains the company at the forefront of AI infrastructure. The company’s graphic processing units (GPUs) are powering most of the world’s AI workloads today, and that dominance doesn’t look to be slipping anytime soon.

Image source: Getty Images.

Nvidia is much more than a chipmaker. Its edge comes from its CUDA software platform, which it smartly provided for free to universities and research labs that were doing the early work on AI. That led to early AI foundational code being written for its chips and locked in a generation of developers into its ecosystem. Today, the company’s chips, networking, and software work together as one integrated tech stack, giving customers performance advantages.

The company’s huge commitment to partner with OpenAI is another sign that it’s not content to sit back. While other chipmakers have struck deals with OpenAi, Nvidia is the only company getting a significant equity stake in the AI model leader. Together, the two companies will work together to help shape where AI is going.

With demand for AI infrastructure still far outpacing supply, Nvidia’s growth story is nowhere near finished. Nvidia is arguably the most important stock in the market today, and one to own.

2. Alphabet

If there is one company that will challenge Nvidia as an AI leader, it’s Alphabet(GOOGL 0.62%)(GOOG 0.75%). The company has its fingers in multiple aspects of AI, with a unique positioned.

Arguably, no company has as complete of an AI tech stack as Alphabet. Its strength starts with its Gemini large language models (LLMs), which rival those of OpenAI. Meanwhile, the company has developed its own custom AI chips, called tensor processing units (TPUs), that were designed to optimally run its cloud computing infrastructure. The chips are in their 7th generation, and far ahead of most other custom AI chips.

Its software stack, which includes Vertex AI, meanwhile, is top-notch. Alphabet even owns the largest private fiber network in the world, which ensures low latency. Its pending acquisition of cloud cybersecurity company Wiz also adds to its vertical offering.

Right now, this vertical AI integration is helping power revenue growth and operating leverage at Google Cloud. Last quarter, Google Cloud revenue climbed 32% to $13.6 billion, while its operating income more than doubled to $2.8 billion. Meanwhile, it’s using its Gemini model to help power its search and AI chatbot offerings, as well.

Fears that chatbots would eat into Google’s search business have faded as the company blended its Gemini models directly into its core products. Features such as AI Overviews, Circle to Search, and Lens have made search more dynamic, leading to more queries, while its new AI mode lets users easily shift from AI-powered search to a traditional AI chatbot. Alphabet is no longer just playing defense when it comes to search and AI; it’s clearly playing offense, and it is well-positioned to win given its distribution and data advantages.

Alphabet is also making early progress in new areas such as robotaxis through Waymo and in quantum computing, which could eventually open new growth streams. Between search, cloud, and its AI push, Alphabet is a growth stock to buy right now.

3. GitLab

Compared to the two stocks above, GitLab(GTLB 1.11%) is certainly flying under the radar. However, this is a company that has been seeing strong growth. It’s grown its revenue by between 25% to 35% for eight consecutive quarters, including 29% last quarter, and more strong growth could be in store as the company continues to evolve.

GitLab started as a platform for developers to securely write and store code, but has evolved into a full software development lifecycle solution. Its Duo AI agent has the potential to be a big growth driver, as it helps automate repetitive work that eats up most of a developer’s day. Freeing up time to actually write code means more software projects, which drives more demand for GitLab’s tools.

Meanwhile, the company is starting to shift to a hybrid seat-plus-usage pricing model. This could be a huge growth driver for Gitlab, as it lets the company capture more revenue from usage and the increased value its offering is now bringing to its customers. A usage model also counteracts the biggest bear argument against the stock, which is that AI will reduce the number of coders.

That bearish argument has driven the stock to an attractive valuation, with it trading at a forward price-to-sales (P/S) multiple of 6.5 times 2026 analyst estimates. For a company with approximately 90% gross margins growing revenue near 30%, that’s a huge bargain.

Serve Robotics(SERV -0.55%) develops autonomous last-mile logistics solutions. It has a major deal with Uber Technologies(NYSE: UBER) that will see thousands of its latest robots deployed into the Uber Eats food delivery network. But this is more than just a commercial partnership, because Uber is also one of Serve’s largest shareholders.

Uber acquired a company called Postmates in 2020, and in 2021, it spun Postmates’ robotics division out into a new company that became Serve Robotics. Serve is still relatively small with a market capitalization of just $890 million, but at the time of this writing, its stock has soared by 67% over the past year alone.

Serve has identified an enormous addressable market for its delivery robots, so should investors join Uber and buy the stock?

Image source: Getty Images.

A potential $450 billion opportunity

Existing last-mile logistics networks are quite inefficient, because they rely on cars with human drivers to deliver relatively small commercial loads from restaurants and retail stores. Serve is betting those workloads will increasingly shift to autonomous robots and drones, creating a potential $450 billion opportunity by 2030.

Serve’s latest Gen 3 robots have achieved Level 4 autonomy, meaning they can safely operate on sidewalks in designated areas without any human intervention. This makes them ideal for transporting small food orders, which is why 2,500 restaurants in five U.S. cities have used them to make 100,000 deliveries since 2022.

The Gen 3 robots use Nvidia‘s Jetson Orin platform, which includes all of the computing hardware and artificial intelligence (AI) software they need to operate autonomously. Having such a powerful technology partner will help Serve scale as quickly as possible, which is key to bringing costs down to management’s target of just $1 per delivery. At that point, using robots will be substantially cheaper than using human drivers.

Serve has a contract with Uber Eats to deploy 2,000 robots across Los Angeles, Miami, Dallas, Atlanta, and Chicago before the end of 2025. The company rolled out its 1,000th robot on Oct. 6, meaning its capacity will double in just the next few months.

But it won’t stop there, because last week Serve announced a new multiyear deal with DoorDash, which operates the largest food delivery network in the U.S. The two companies are yet to provide firm numbers, so it’s unclear how many more robots Serve will have to deploy.

Scaling a robotics business is not cheap

Despite its status as a publicly traded company, Serve is still very much a start-up. Its revenue tends to be quite lumpy, which is typical when a product is in the early stages of commercialization. The company brought in just $642,000 in revenue during the second quarter of 2025 (ended June 30), which is a tiny amount relative to its $890 million market cap.

But Serve’s business could scale extremely quickly. Management thinks the company will generate up to $80 million in annual revenue once all 2,000 Gen 3 robots are up and running, which bodes well for 2026. Wall Street predicts Serve will generate $3.6 million in total revenue this year (according to Yahoo! Finance), so $80 million would be a monumental jump.

But so far, the road to commercialization has been paved with substantial losses. Serve lost $33.7 million on a generally accepted accounting principles (GAAP) basis during the first half of 2025, so it’s on track to exceed its 2024 loss of $39.2 million by a very wide margin. The company spent $16 million on research and development alone during the first half of this year, so based on its minuscule revenues, its losses are no surprise.

Serve had $183 million in cash on hand as of June 30, and it raised a further $100 million from investors in October, so it has enough cushion to sustain its losses for the next few years (assuming they don’t materially increase). However, if the company doesn’t chart a pathway to profitability by then, it might have to raise even more money, which will dilute existing shareholders.

As a result, there is a lot riding on the successful commercialization of Serve’s 2,000 Gen 3 robots.

Serve stock trades at a sky-high valuation, but is it a buy?

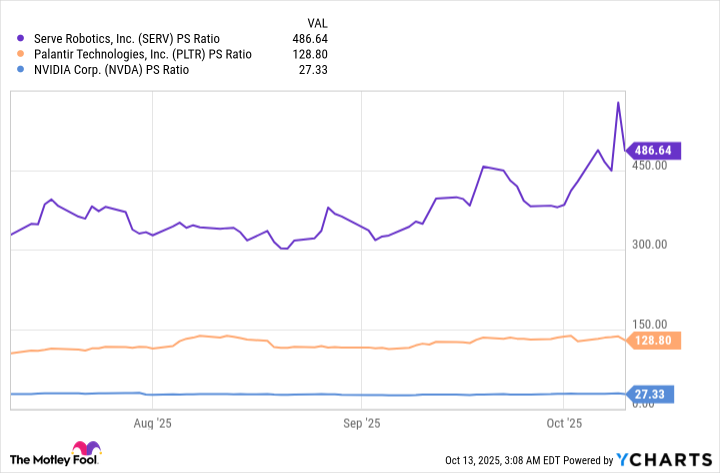

Serve stock is extremely expensive right now. Its price-to-sales (P/S) ratio is a mind-boggling 486, making it substantially more expensive than any other major AI stock. Palantir Technologies, which also trades at a sky-high valuation, looks cheap by comparison because its P/S ratio is 128. For some further perspective, Nvidia stock has a P/S ratio of just 27.

With that said, if we assume Serve will generate around $80 million in revenue next year, its forward P/S ratio is just 11. In other words, it almost looks like a bargain.

But investors can’t always rely on management’s guidance, especially in this case because it assumes a perfectly smooth transition to commercialization for the Gen 3 robot. As with any new product, there will probably be bumps in the road, and we simply don’t know if it will scale successfully.

As a result, investors might be better off waiting a few more quarters to see if the rollout of the robots actually translates into as much tangible revenue as management expects. If it doesn’t, Serve stock could suffer a sharp correction because of its current valuation.

Between the 10th and 15th of every month, the U.S. Bureau of Labor Statistics (BLS) releases the previous month’s inflation data. This information is used by the Social Security Administration (SSA) to calculate the annual cost-of-living adjustment (COLA).

The BLS was slated to release the September inflation report — the final piece of data needed to unveil the 2026 COLA — at 08:30 a.m. ET on Oct. 15. But due to the federal government shutdown, the most-anticipated announcement of the year has been pushed back.

Social Security’s 2026 COLA reveal will occur on Oct. 24

In its simplest form, Social Security’s COLA is the near-annual “raise” passed along to beneficiaries to offset the impact of inflation (rising prices). If benefits weren’t adjusted for the effects of inflation, Social Security recipients would see their income lose buying power most years.

For the last half-century, the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W) has served as Social Security’s inflation measuring stick. With more than 200 different spending categories, each with its own unique percentage weightings, the CPI-W can be reported as a single figure by the BLS each month.

The quirk with Social Security’s COLA calculation is that only the months of July, August, and September (the third quarter) matter. The other nine months of the year can be helpful in spotting trends, but they aren’t used in the COLA calculation.

With CPI-W readings from July and August already known, the only puzzle piece missing is September. Unfortunately, most economic data reports from federal agencies are delayed indefinitely during government shutdowns.

However, some BLS staffers are going back to work and will be releasing the September inflation report on Friday, Oct. 24, at 08:30 a.m. ET, according to information provided to CNBC. The SSA will announce the 2026 COLA on Oct. 24, as well.

Based on estimates from nonpartisan senior advocacy group The Senior Citizens League and independent Social Security and Medicare policy analyst Mary Johnson, next year’s COLA is forecast to come in at 2.7% or 2.8%, respectively. This would work out to an extra $54 to $56 per month for the typical retired-worker beneficiary, and $43 to $44 extra each month for the average worker with disabilities and survivor beneficiary.

While little is set in stone — other than the expectation of the BLS reporting the last piece of data needed to calculate the 2026 COLA on Oct. 24 — retirees are very likely getting the short end of the stick with next year’s raise. COLAs have consistently come up short for retirees, and a projected 11.5% increase in the 2026 Medicare Part B premium isn’t going to help.

Image source: Getty Images.

No speculating here! This is the one guaranteed Social Security change for 2026

Though the government shutdown has delayed the release of key pieces of information, such as next year’s COLA, the maximum taxable earnings cap, the maximum monthly payout at full retirement age, and the withholding thresholds tied to the retirement earnings test, there is one Social Security change that’s guaranteed to take place in 2026. However, you’ll have to go to the state level to see it.

Firstly, yes, Social Security benefits may be taxable at the federal and state levels.

Individuals whose provisional income — adjusted gross income (AGI) + tax-free interest + one-half benefits — tops $25,000, or $32,000 for couples filing jointly, can have some of their Social Security income exposed to federal taxation.

When the calendar flips to Jan. 1, 2026, West Virginia will officially become one of 42 states that don’t tax Social Security income.

In the 2022 tax year, West Virginia made Social Security income exempt from state-level taxation for individuals and jointly filing couples with respective AGIs of $50,000 or less and $100,000 or less.

In March 2024, West Virginia’s legislature passed, and its governor signed, a new law that phases out the taxation of Social Security benefits over a three-year period for those folks who didn’t qualify for this previous AGI adjustment.

Beginning in the 2024 tax year, West Virginians who received Social Security benefits and generated more than $50,000 in AGI (or $100,000 in AGI, if filing jointly) saw 35% of their Social Security benefits exempted from state-level taxation. In 2025, this exemption increased to 65% of Social Security income. In 2026, 100% of Social Security income will be exempted at the state level.

West Virginia will join Kansas, Missouri, Nebraska, and North Dakota as states that have shelved the taxation of Social Security benefits since this decade began.

While this has been anything but a normal COLA announcement month for Social Security, the one thing we do know is that Social Security recipients in West Virginia will be all smiles when the new year arrives.

Those annual raises have a major flaw that cannot be overlooked.

There’s one piece of news seniors on Social Security have been itching to get for months now — news of an official cost-of-living adjustment, or COLA, for 2026.

At this point, it’s pretty clear that 2026 is not going to be one of those 0% COLA years. Though there have been 0% COLAs in the past, inflation has risen enough to date that experts can say with confidence that Social Security benefits will, indeed, be going up in the new year. The question is by how much.

Image source: Getty Images.

Current estimates seem to be floating in the 2.7% to 2.8% range. But we won’t know what next year’s COLA is for sure until the Social Security Administration makes its big announcement.

That said, Social Security’s upcoming COLA is probably going to be bad news no matter what it actually amounts to. It’s important to understand why — and take steps to work around that.

Why Social Security’s upcoming COLA probably won’t cut it

There’s a reason not to get too excited about Social Security’s 2026 COLA. That reason boils down to the fact that Social Security COLAs have been failing seniors for decades.

In fact, the Senior Citizens League, an advocacy group, says that seniors on Social Security lost 20% of their buying power between 2010 and 2024 due to insufficient COLAs. So chances are, next year’s COLA won’t keep up with inflation, either.

The problem stems from how Social Security COLAs are calculated. They’re based on annual third-quarter changes to the Consumer Price Index for Urban Wage Earners and Clerical Workers.

Now, let’s look at that index’s name carefully. Notice the terms “urban,” “wage earners,” and “clerical workers.” Do those describe the typical Social Security recipient?

It’s true that plenty of retirees reside in cities. But that’s certainly not a given. In fact, many retirees are able to move outside of cities to lower their costs once they no longer have to worry about proximity to a job.

Many Social Security recipients, by nature, are also not workers. They’re retired. So it’s pretty silly to base Social Security COLAs on an index that measures the costs a different subset of people face.

Advocates have been pushing to base Social Security COLAs on the Consumer Price Index for the Elderly, or CPI-E. But lawmakers haven’t exactly been jumping to make that change, so it’s not one to expect anytime soon.

Prepare to be disappointed now

No matter what raise Social Security recipients end up eligible for in 2026, chances are, it won’t cut it. Plus, if you’re on Medicare as well, any increase in the cost of Part B will eat away at your COLA.

If you want to improve your financial picture for 2026, you can’t sit back and wait for your COLA to take effect for that to happen. Instead, you should take matters into your own hands.

Here are some specific steps to take:

Do a thorough review of your retirement budget

Identify a few expenses you can reduce or even eliminate

Explore options for going back to work, whether as an hourly employee or a gig worker

See if it’s possible to downsize your home or rent out a room for income

Explore moving in with a family member if money is very tight

Review your Medicare plan choices carefully during open enrollment to lower your healthcare costs

There may be other steps you can take to improve your finances, too, and it’s worth exploring them. What you don’t want to do is assume that your Social Security COLA will be the solution to your financial problems.

Even if Social Security’s 2026 COLA is more generous than expected, chances are good that it won’t do the job of keeping up with inflation that it’s supposed to. The sooner you’re able to accept that, the sooner you can start making positive changes that have a real effect.

Argent Capital Management LLC pared its holding in Copart (CPRT 1.70%) by 1,262,984 shares during Q3 2025, an estimated $59.52 million trade based on the average price for the quarter, according to an SEC filing dated October 14, 2025.

What happened

According to its Form 13-F filed with the Securities and Exchange Commission on October 14, 2025 (see filing), the firm reduced its Copart position by 1,262,984 shares during Q3 2025.

The estimated value of the shares sold, calculated using the period’s average closing price, was $59.52 million. The fund reported a remaining position of 162,339 shares at quarter-end.

What else to know

This was a reduction in the Copart stake, which now represents 0.2% of the firm’s 13F reportable assets under management as of Q3 2025.

Argent’s top holdings after the filing:

Microsoft: $251.95 million (6.9% of AUM as of 2025-09-30)

Nvidia: $237.98 million (6.5% of AUM as of 2025-09-30)

Amazon: $213.08 million (5.8% of AUM as of 2025-09-30)

Alphabet: $194.75 million (5.3% of AUM as of 2025-09-30)

Mastercard: $126.28 million (3.5% of AUM as of 2025-09-30)

As of October 13, 2025, Copart shares were priced at $44.07, down 20% over the one-year period ending October 13, 2025, underperforming the S&P 500 by 36 percentage points over the same time.

Company Overview

Metric

Value

Market Capitalization

$43.41 billion

Revenue (TTM)

$4.65 billion

Net Income (TTM)

$1.55 billion

Price (as of market close 2025-10-13)

$44.07

Company Snapshot

Copart provides online auctions and vehicle remarketing services, including virtual bidding, salvage estimation, and end-of-life vehicle processing across North America, Europe, and select international markets.

It operates a digital marketplace facilitating the sale and purchase of vehicles, generating revenue through transaction fees, service charges, and value-added offerings such as vehicle transportation and title processing.

The company serves insurance companies, banks, fleet operators, dealerships, vehicle dismantlers, exporters, and individual buyers seeking to acquire or dispose of vehicles efficiently.

Copart, Inc. provides online auctions and vehicle remarketing services internationally, leveraging advanced virtual auction technology to connect sellers and buyers of vehicles across multiple continents. With a scalable digital platform and a comprehensive suite of remarketing and logistics services, Copart enables efficient disposition of vehicles for institutional and individual clients alike.

Foolish take

While Argent Capital Management still holds a few shares of Copart, the firm all but sold out of its position, reducing its portfolio allocation in the stock from 2% to 0.2%.

Since the stock seemed to be a longer-term holding for Argent, this seems mildly worrisome to Copart shareholders — myself included.

Though it’s impossible to know what exactly prompted the firm to nearly liquidate its holdings in the company, Copart’s results have been underwhelming this year, causing its slightly expensive stock to slide 30% from its high.

After growing sales by 15% annually over the last decade, Copart’s revenue growth slid to 13%, 7%, and finally 5% over the previous three quarters.

That said, Copart still trades at 28 times earnings, even after this year’s drop, so Argent may have simply thought it had grown beyond its valuation as a more mature company.

Glossary

13F reportable AUM: Assets under management that must be disclosed by institutional investment managers in quarterly SEC Form 13F filings. Form 13-F: A quarterly SEC filing by institutional investment managers listing their U.S. equity holdings. Quarter (Q3 2025): The third three-month period of a company’s fiscal year, here referring to July–September 2025. Transaction value: The total dollar amount generated by a specific buy or sell trade. Stake: The ownership interest or investment a fund or individual holds in a particular company. Assets under management (AUM): The total market value of investments managed on behalf of clients by a fund or firm. Digital marketplace: An online platform where buyers and sellers conduct transactions for goods or services, such as vehicles. Vehicle remarketing: The process of reselling used or end-of-lease vehicles, often through auctions or specialized platforms. Salvage estimation: The process of assessing the value of damaged or end-of-life vehicles for resale or parts. End-of-life vehicle processing: Handling and disposing of vehicles that are no longer operational, often for recycling or parts. Value-added offerings: Additional services provided beyond basic transactions, such as transportation or title processing, to enhance customer value. TTM: The 12-month period ending with the most recent quarterly report.

Josh Kohn-Lindquist has positions in Alphabet, Copart, Mastercard, and Nvidia. The Motley Fool has positions in and recommends Alphabet, Amazon, Copart, Mastercard, Microsoft, and Nvidia. The Motley Fool recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

Broadcom(NASDAQ: AVGO) is playing a key role in supplying data centers with custom chips and networking products. Strong revenue and free-cash-flow growth have pushed the stock to new highs this year, with shares up 54% year to date through market close Oct. 13.

The stock is up more than 500% since the end of 2022, when the artificial intelligence (AI) boom started. However, there are important reasons why the stock will likely climb higher in 2026 and beyond.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now. Continue »

Image source: Getty Images.

Broadcom is printing cash

Broadcom has a long history of delivering profitable growth, which has led to market-beating returns. Its free-cash-flow growth has accelerated over the last year. Free cash flow through the first three quarters of fiscal 2025 was 40% larger than the year-ago period. This shows Broadcom’s margins expanding from higher sales of custom AI accelerators and strong growth from its software business.

Its order backlog hit a record $110 billion, which is significantly higher than its trailing-12-month revenue of $60 billion. Spending on AI infrastructure by hyperscalers is expected to reach $350 billion this year, meaning more money could be headed Broadcom’s way. Data center spending is expected to grow into the trillions by the end of the decade.

Broadcom’s cash-rich business should fuel investment in more innovation that rewards shareholders. This is a quality semiconductor stock to profit off of the AI boom.

Should you invest $1,000 in Broadcom right now?

Before you buy stock in Broadcom, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Broadcom wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004… if you invested $1,000 at the time of our recommendation, you’d have $657,412!* Or when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $1,154,376!*

Now, it’s worth noting Stock Advisor’s total average return is 1,075% — a market-crushing outperformance compared to 190% for the S&P 500. Don’t miss out on the latest top 10 list, available when you join Stock Advisor.

Look past the hype and access whether it has strong fundamentals.

With shares up 2,500% over the last 12 months, Quantum Computing(QUBT 1.49%) is sure to attract the attention of growth-focused investors. The stock is surging based on industrywide optimism. But is this rally driven by fundamentals or hype? Let’s dig deeper into the pros and cons of Quantum Computing, also known as QCi, to decide if the shares are a solid long-term buy.

What is special about quantum computing?

Quantum computing is a branch of computer science and physics that aims to create devices capable of solving the world’s most difficult problems exponentially faster than today’s fastest supercomputers. And we aren’t talking 30 minutes faster; we are talking over a million years faster. If the technology works, it will allow humans to do things that were previously impossible with current technology.

It doesn’t take a supercomputer to see the vast commercial opportunities that viable quantum computers could unlock. Analysts expect them to help rapidly discover new pharmaceutical drug candidates and chemical structures, and even help train artificial intelligence (AI) models.

Quantum Computing (QCi) aims to position itself on the picks-and-shovels side of this opportunity, supplying hardware products like chips, sensors, and communication devices. It also claims to have the first of its kind foundry for processing thin-film lithium niobate (TFLN), a next-generation material useful for advanced telecommunication platforms.

QCi’s TFLN foundry is located in Tempe, Arizona, and its made-in-America approach could attract government support amid the accelerating technology arms race between the U.S. and China.

But what about the fundamentals?

While cutting-edge technologies often sound exciting, it is essential to remember that they won’t always translate to commercial success, especially in the near term. Furthermore, the start-ups with the most valuable patents and processes are often acquired by larger companies or kept private to maximize returns for their owners. So when small speculative companies like QCi go public, it’s important to ask why.

Image source: Getty Images.

The company’s second-quarter earnings report gives some clues about the pressure it is under. Revenue collapsed 67% year over year to just $61,000 (that’s less than the median annual salary of a U.S. tech worker). Meanwhile, operating costs are spiraling out of control, with research and development more than doubling to $5.98 million.

As a speculative tech company, QCi probably can’t trim its research and development outflows too much without risking falling behind other players in the industry. And it is important to note that quantum computing is shaping up to be a competitive arena, with tech giants like Alphabet and Nvidia also aiming to establish themselves in the picks-and-shovels niche. These larger, well-capitalized companies will be able to spend more on research and leverage larger supply chains.

Is Quantum Computing a millionaire-maker stock?

QCi is clearly under a lot of pressure because of its minuscule revenue, heavy losses, and the pressure to keep up its research spending. By going public, management now has the ability to raise more money by creating and selling more units of its own stock. While this strategy keeps the business afloat, it can hurt existing shareholders by diluting their ownership stake in the company and their claim on its future profits.

In August, QCi announced a $500 million share offering, which increased its share count by a jaw-dropping 26.9 million. And the company already has 159,883,187 shares outstanding as of the second quarter. Expect this number to continue expanding over time.

While QCi could potentially be a millionaire-maker stock in the right conditions, the risks far outweigh the rewards right now. And fundamentals-focused investors should look for better opportunities.

Will Ebiefung has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Alphabet and Nvidia. The Motley Fool has a disclosure policy.

Despite the company’s run in recent years, it’s not too late to buy.

Eli Lilly(LLY -0.82%) has been one of the best-performing healthcare giants over the past decade. It now stands as the largest in the sector by market cap.

Even with headwinds it has encountered this year, the drugmaker is arguably one of the top stocks in its industry to buy right now. Here’s why.

Image source: Getty Images.

Innovation pays off

It’s hard to find a drugmaker that has proven more innovative than Eli Lilly in recent years. Within its core areas of diabetes and weight management, Lilly launched tirzepatide, marketed as Mounjaro for diabetes and Zepbound for obesity. Tirzepatide was a significant breakthrough, as the first dual GLP-1 (glucagon-like peptide-1) and GIP (gastric inhibitory polypeptide) agonist, a medicine that mimics the action of these two gut hormones.

That’s one of the reasons tirzepatide has proved more effective than traditional GLP-1 drugs, and is racking up sales the likes of which have almost never been seen in the history of the industry. That’s not hyperbole. Most compounds never reach $1 billion in annual sales. Most of those that do, never get to $5 billion, and those that do, typically take years on the market to get there. In its third full year on the market, tirzepatide will generate well over $20 billion this year.

The next chapter

Last year, Eli Lilly earned approval for Kisunla, a medicine indicated to treat Alzheimer’s disease, an area that had long been considered the graveyard of investigational medications. So Lilly’s innovative prowess extends beyond its core markets. And the company is leveraging its success in weight management and obesity to establish a strong foundation for the future.

Thanks to acquisitions and licensing deals, it has significantly expanded its pipeline, which should power clinical and regulatory success over the next few years and strong financial results well into the next decade. That’s why Eli Lilly is one of the top healthcare stocks to buy right now.

On Tuesday, Oriental Harbor Investment Master Fund disclosed selling 59,274 shares of ProShares UltraPro QQQ(TQQQ -1.88%) in an estimated $5.4 million trade, according to a recent SEC filing.

What Happened

According to a filing with the Securities and Exchange Commission, Oriental Harbor Investment Master Fund sold 59,274 shares of ProShares UltraPro QQQ during the quarter. The estimated transaction value was $5.4 million. The fund’s TQQQ position now stands at about 1.2 million shares, valued at $124.2 million.

What Else to Know

Following the sale, TQQQ represents 9.6% of the fund’s reportable assets under management.

Top holdings after the filing:

NASDAQ:NVDA: $236.2 million (18.3% of AUM)

NASDAQ:GOOGL: $224.1 million (17.4% of AUM)

NYSEMKT:FNGU: $144.6 million (11.2% of AUM)

NASDAQ:TQQQ: $124.2 million (9.6% of AUM)

NASDAQ:META: $99.5 million (7.7% of AUM)

As of Tuesday’s market close, shares of TQQQ were priced at $101.13, up 33% over the past year, outperforming the S&P 500 by 20 percentage points.

ETF Overview

Metric

Value

AUM

N/A

Price (as of market close on Tuesday)

$101.13

One-year total return

44%

Dividend yield

0.65%

Company Snapshot

TQQQ’s investment strategy seeks to deliver daily performance consistent with the fund’s objective through the use of financial instruments.

Underlying holdings are composed of the 100 largest non-financial companies listed on the Nasdaq Stock Market.

The fund structure is non-diversified.

ProShares UltraPro QQQ is an ETF that seeks daily returns consistent with its investment objective by tracking the Nasdaq-100 Index. By employing financial instruments, the fund aims to achieve its daily return objective.

Foolish Take

Hong Kong–based Oriental Harbor Investment Master Fund pared back its position in ProShares UltraPro QQQ last quarter, selling roughly $5.4 million worth of shares. Despite the reduction, TQQQ remains a core holding, accounting for nearly 10% of the fund’s reported assets. The ETF continues to rank just behind Nvidia, Alphabet, and FNGU, reflecting the fund’s deep concentration in leveraged and technology-driven strategies.

TQQQ, which seeks three times the daily performance of the Nasdaq-100 Index, has soared 33% in the past year, outpacing the S&P 500 by about 20 percentage points. Its top underlying exposures—Nvidia, Microsoft, Apple, and Amazon—mirror Oriental Harbor’s own equity bets, creating both alignment and amplification across the portfolio.

While leveraged ETFs like TQQQ can magnify gains, they also heighten risk when markets turn volatile. For Oriental Harbor, trimming the position may be a prudent rebalancing move after strong returns, especially given its already substantial exposure to the same megacap tech names through direct holdings and other leveraged funds like FNGU. The strategy suggests discipline, not retreat, as the fund locks in profits while maintaining a high-conviction tilt toward tech-fueled growth.

Glossary

ETF: Exchange-traded fund; a pooled investment fund traded on stock exchanges, similar to stocks.

UltraPro: Indicates an ETF aiming for leveraged returns, typically providing a multiple of the daily performance of an index.

Assets under management (AUM): The total market value of assets a fund manages on behalf of investors.

Non-diversified: A fund that invests a large portion of assets in a small number of holdings, increasing concentration risk.

Leveraged ETF: An ETF using financial instruments to amplify returns, often targeting a multiple of an index’s daily performance.

Dividend yield: Annual dividends paid by an investment, expressed as a percentage of its current price.

Underlying holdings: The individual securities or assets that make up a fund’s portfolio.

Nasdaq-100 Index: An index of the 100 largest non-financial companies listed on the Nasdaq Stock Market.

Daily return objective: The fund’s goal to match or multiply the performance of its benchmark index each trading day.

Financial instruments: Contracts such as derivatives or swaps used to achieve specific investment outcomes.

Outperforming: Achieving a higher return than a specific benchmark or index over a given period.

Reportable assets: Assets that must be disclosed in regulatory filings, such as those reported to the SEC.

Jonathan Ponciano has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Alphabet, Meta Platforms, and Nvidia. The Motley Fool has a disclosure policy.

BigBear.ai Holdings Inc(NYSE: BBAI) gained 1.14% to close at $8.91. Trading volume reached 172.3 million shares, almost two times its three-month average of 94.5 million.

The S&P 500(SNPINDEX: ^GSPC) slipped 0.16% to 6,644.31, while the Nasdaq Composite(NASDAQINDEX: ^IXIC) fell 0.76% to 22,521.70 as investors digested renewed U.S.–China trade tensions.

Peers were mixed across the AI sector. C3.ai Inc(NYSE: AI) declined 1.96% to $18.99, while Palantir Technologies Inc(NASDAQ: PLTR) rose 1.43% to $179.74.