Last week, the Deputy Chief of Staff for Policy and Homeland Security offered a sharply different account of Venezuela’s 1976 oil nationalization. It is provocative, but it does not hold up to the record.

President Carlos Andrés Pérez (1974-1979) proclaimed the takeover of the petroleum industry on January 1, 1976. The announcement occurred at the Mene Grande oilfield in Zulia. Crucially, the transfer from private control to a state-run model went smoothly. The major multinationals were compensated, invited to work with the new state-owned company, Petróleos de Venezuela (PDVSA), as service and technology providers, and the process triggered no diplomatic incident with the United States. A brief look at the facts does not support claims of “theft of American wealth and property,” since “the tyrannical expropriation” was precisely engineered to avoid the kind of rupture Miller describes.

The nationalization of the Venezuelan petroleum industry responded to global events unfolding in the Middle East around 1970. To be sure, Venezuelan politicians had long dreamed of granting the state full control over the most important sector of the country’s economy. However, plans for an eventual state takeover of the oil fields remained nebulous, a goal set for a distant future. Muammar Qaddafi (1969-2011) in Libya, of all figures, provided Venezuelan lawmakers with a concrete horizon for materializing full control over the hydrocarbon sector. The Libyan strongman unilaterally increased royalties and taxes on multinationals, with Iran pursuing a similar approach. OPEC then formalized this push for higher prices at its December meeting that year. What followed in 1971 sent shock waves across the world: Libya nationalized its oil industry, followed by Algeria and Iraq. This process quickly expanded to the rest of the Middle East, setting the backdrop for the fuel shortages of that decade and the energy crisis of 1973.

This global context greeted President Rafael Caldera (1969-1974), a Christian Democrat of COPEI, who was intent on capitalizing on these favorable winds. Soon, every political faction in Congress sought to outdo the other in displaying their anti-corporate credentials. Caldera stood at the top as the most nationalist of the pack, passing an unprecedented package of bills and decrees destined to expand government control over the industry significantly. By the time he handed power to Carlos Andrés Pérez from Acción Democrática (AD), de facto state control over the entire industry was already in place. Nationalization became the only politically safe position when the electoral campaign of 1973 started. Once elected, Carlos Andrés Pérez authorized the creation of a Presidential Commission in charge of studying the state takeover and proposing a bill to that effect, to be approved by Congress in 1975. Ordinary Venezuelans shared this renewed fervor for ownership over the national riches of the country, though in a conflicted way.

Polls by the weekly political magazine Resumen showed broad support for nationalization. Yet respondents also rated working conditions at the foreign oil companies very favorably and many wanted foreign capital to remain involved after the takeover because they trusted the firms’ experienced managers. At the same time, they doubted the state’s capacity to run complex industries, while still believing it could improve over time and that a state-run oil sector was in the nation’s interest. That nuance rarely appeared in Congress.

The nationalization became a fait accompli without antagonism with the U.S. government or the multinationals

COPEI and a constellation of center-left and leftist organizations pushed for an immediate, total takeover without any foreign role. Some opposed compensation altogether and even welcomed a showdown if necessary, seeing local employees working for these multinationals as threats to a “genuine” nationalization of the industry. Venezuelan managers soon came under attack from politicians accused of having “their minds colonized” by the American and British firms. They were also viewed as “centers of anti-Venezuelan activity.” Insults in the press and public spaces galvanized domestic employees to take action. Led by Venezuelan mid-level managers such as Gustavo Coronel from Royal Dutch Shell, the managerial class came together to form Agrupación de Orientación Petrolera (AGROPET). The nonprofit aimed to help the country prepare to take full responsibility for the hydrocarbon sector.

From March 1974 through 1975, AGROPET ran a public campaign for an orderly, compensatory nationalization built on continuity, not a politicized break. Their activities included appearing on radio programs, giving TV interviews, publishing in newspapers, and participating in public forums, including congressional meetings, and talks with members of the Presidential Commission mandated by President Pérez. The irony of this body is that it gathered representatives from prominent sectors of society. And yet the Commission excluded the people who actually ran the industry.

AGROPET quickly steered the nationalization debate back toward a technocratic solution. The organization’s pivotal moment came in January 1975, when its leaders met with President Pérez and laid out what became the blueprint for the 1976 nationalization. They argued for an industry built on administrative efficiency, technological progress, apoliticism, and sound management not a politicized rupture. Their model envisioned a holding company with four affiliates that would absorb concessionaire operations. The new organizational culture would blend practices inherited from the Creole Petroleum Corporation and Shell, and the nationalized industry would retain ties to its foreign predecessors. Under this proposal, Petróleos de Venezuela (PDVSA) became, in effect, the direct descendant of the multinationals that built Venezuela’s modern oil industry. It perpetuated the business philosophy of the multinationals. Persuaded by Venezuelan managers, Pérez sided with the technocrats and sent an amended nationalization bill to Congress, crucially allowing foreign capital to return under Article 5. The AD-dominated legislature defended the bill and enacted it in August 1975. Two months later, Creole and the other firms accepted a compensation package of about $1 billion for their expropriated assets.

The nationalization became a fait accompli without antagonism with the U.S. government or the multinationals. It constituted less a watershed than a continuation of relationships the Venezuelan state and foreign oil companies had built across the twentieth century on new terms. PDVSA quickly signed service and technology agreements with the very companies it had expropriated. What’s more striking is that this smooth outcome became, in part, an unintended consequence of Venezolanization: the deliberate integration of Venezuelans at every level of the corporate ladder, a policy initiated by Creole and Shell in the 1940s. Unusual in the industry at the time, it stood out as a strand within a broader set of corporate social responsibility practices these companies implemented in Venezuela. Locals trained through that system helped make the transition to state control orderly and broadly beneficial.

For much of the political opposition, however, the outcome felt bittersweet. They denounced its chucuta nature (a “half-baked” nationalization) and framed Article 5 as outright betrayal. Many wanted the kind of dramatic showdown associated with Cárdenas in Mexico, Mossadegh in Iran, or Velasco Alvarado in Peru, cases where claims of expropriation and “theft” of U.S. property could at least be mounted. Venezuela in 1976 stood far away from that drama, and once the transfer was complete, business continued as usual despite the lamentations of certain congressmen. Venezuela’s 1976 oil nationalization was engineered to preclude confrontation. Getting the history right matters. If the current U.S. administration wants to cite this episode to justify pressure, escalation, or exceptional measures, it has chosen a poor example, precisely because the process avoided the kind of rupture Mr. Miller invokes. So, por este camino no es.

HomeInsuranceHurricane Melissa Devastation Saddles Jamaica With Multi-Billion-Dollar Bill

Jamaica faces an $8 billion-plus price tag to repair the damage caused by Hurricane Melissa. Wind gusts hit a record-breaking 252 miles per hour between October and November.

The catastrophe claimed 45 lives, 15 remain missing, and a further nine cases are under investigation.

Prime Minister Andrew Holness stated that repairs will be equivalent to 30% of Jamaica’s GDP. However, the World Bank’s and Inter-American Development Bank’s estimates of $8.8 billion would amount to 41% of GDP. That makes Melissa the most expensive hurricane in Jamaica’s history. Housing insurance alone could total between $2.4 billion and $4.2 billion. The Office of Disaster Preparedness and Emergency Management recorded 156,000 homes damaged and 24,000 considered total losses.

According to Verisk Analytics, “Many neighborhoods in St Elizabeth parish … are reporting significant damage, with 80% to 90% and, in certain cases, 100% of roofs destroyed.”

The Cost of Recovery

Jamaica is looking to its insurers and multilaterals for immediate financial relief. The Caribbean Catastrophe Risk Insurance Facility (CCRIF) made two payments totaling $91.9 million. The World Bank added another $150 million.

A further package of aid from the World Bank is forthcoming. This will include emergency finance redeploying existing project funds to speed up repairs and private-sector assistance via the International Finance Corporation. The CCRIF’s payout will come from Jamaica’s cyclone and excessive rainfall parametric insurance policies.

Holness promises that the government will spend each dollar carefully.

“We will spend to relieve human suffering, but every dollar that is spent will be accounted for,” he told reporters while touring disaster sites, “and not just from an accounting point of view, meaning adding up the dollar spent. It will be accounted for from an efficiency point of view, which is really the greater accountability. Every dollar spent, every aid given, every commitment made, will be used in a way that quickly advances the recovery, but at the end of it makes Jamaica stronger.”

This year is on course to become one of the worst years of this century for job cuts, comparable only to the Great Financial Crisis of 2008 and 2009 and the year of the pandemic, 2020.

Corporations are primarily attributing hundreds of thousands of recently announced layoffs to higher operating costs caused by US tariffs. Still, many feel that a workforce-rebalancing strategy to fund investments in artificial intelligence may also be to blame.

Last October, US job losses topped 153,000, the highest level since 2003. In November, the US gained 64,000 jobs, more than expected, but the unemployment rate climbed to a four-year high of 4.6%.

According to The Challenger Report, a leading indicator of the US labor market, American companies laid off over a million employees in the first 10 months of 2025. That’s the highest number since the pandemic-related recession five years ago, and up 65% from the same period last year.

The huge wave of redundancies, begun in January with the Trump Administration’s restructuring of government agencies, is now expanding to most sectors.

The latest round of announcements came from tech giants Intel, Microsoft, IBM, and Verizon, which collectively announced the axing of over 50,000 jobs. Online retail giant Amazon slashed 30,000 positions, while international courier UPS let go of 48,000 employees.

Other major industry players that have significantly reduced their workforce include Accenture (11,000 cuts), Procter & Gamble (7,000), PwC (5,600), Salesforce (4,000), American Airlines (2,700), Paramount (2,000), and General Motors (1,700).

The trend isn’t limited to American firms. In Europe, companies across various sectors also disclosed extensive staff reductions this year, with Nestlé cutting 16,000 jobs, Bosch 13,000 jobs, Novo Nordisk 9,000 jobs, Audi 7,500 jobs, Volkswagen 7,000 jobs, Siemens 5,600 jobs, Lufthansa 4,000 jobs, Lloyds Bank 3,000 jobs.

Asia-Pacific is also affected, with India’s Tata Consultancy dismissing 12,000 employees, Japan’s Nissan dismissing 11,000, and Australia’s second-largest bank, ANZ, dismissing 3,500.

Fears are spreading that this might be the start of an unprecedented, massive recession caused by AI expansion. If Amazon and Palantir dismissed the claim, Nvidia CEO Jensen Huang lately emphasized that “100% of everybody’s jobs will be changed” by AI.

And in a extraordinary step, after axing 1,500 jobs this year, traditional brick-and-mortar retailer Walmart delisted from the NYSE this month and move to tech-focused Nasdaq. The move highlights Walmart’s ‘tech-powered approach’, with decade-long investments in warehouse-automation and its current strong push towards AI.

We live in an interdependent world where no country or region is exempt from the effects of developments elsewhere. The transition into autocracies in other countries is not the exception. Autocratisation has escalated into a global wave. According to the latest V-Dem report, 45 countries are currently moving towards autocracy, up from just 16 in 2009, while only 19 are democratising. By 2024, 40% of the world’s population lived in autocratising countries.

Autocratic expansion represents a threat to liberal democracies in Europe and beyond, as political science’s only near-lawlike finding holds: democracies do not wage war against each other. In contrast, an autocratic Russia invades Ukraine and might quite possibly very soon attack the rest of Europe, as NATO’s General Secretary Mark Rutte alerted in Berlin on December 12: “We are Russia’s next target, and we are already in harm’s way… we must act to defend our way of life now”.

The link between democracy and peace was also at the centre of this year’s Nobel Peace Prize ceremony. In his address, Jørgen Watne Frydnes, Chair of the Norwegian Nobel Committee, emphasised that democracy is not only essential for peace within national borders, but also for peace beyond them. The award to Venezuelan opposition leader María Corina Machado, who insisted that the prize belongs to all Venezuelans, underscored that message.

Russia illustrates this connection with unusual clarity, and the Maduro regime is a close ally of the regime directly threatening Europe. Since Chávez, under whose rule Venezuelan democracy collapsed no later than between 2002 and 2007 (according to V-Dem), the Venezuelan regime has deepened its ties with China and Russia. The latter, particularly, became an important partner in the military and security realms. By providing weapons, equipment and intelligence support, Russia secured a geopolitically strategic foothold in South America. This allows Putin to project power into the Western hemisphere and to undermine US and European strategic interests.

Venezuela’s partnership with Russia follows a foreign policy logic of influence projection within the United States’ regional sphere, much as Washington has done in Eastern Europe. This relationship has taken the form of military cooperation, with Venezuela—alongside Nicaragua—becoming one of Russia’s main partners in Latin America.

A democratic Venezuela could reintegrate into Mercosur, opening an additional market under the forthcoming EU-Mercosur agreement—one of the EU’s tools for diversifying trade partners and reducing excessive economic dependencies.

While earlier cooperation included a visit of nuclear-capable Russian bombers to Venezuela in 2018, more recent ties have focused on military diplomacy: high-level defence meetings, training exchanges, and joint participation in initiatives such as the International Army Games. But despite Russia’s growing resource constraints following its invasion of Ukraine, reports of the construction of a new ammunition factory in Maracay (Aragua) and the presence of Russian “Wagner” mercenaries in Venezuela exemplify the possibility of going back to further military cooperation. The ammunition factory would specifically produce a version of the AK-130 assault rifle (developed in the Soviet Union) and a “steady supply” of 7.62mm ordnance under Russian license in spite of sanctions to avoid Russian ammunition exports.

Beyond the military sphere, Venezuela currently cooperates with Russia to mitigate the effects of Western sanctions. Together with Iran, both countries share shadow shipping networks that allow sanctioned oil exports to continue flowing, primarily towards China (surprise! Another autocratic country).

Thus, from a European Security perspective, Venezuela isn’t really a distant or marginal case. A Russia-aligned autocracy in South America strengthens Moscow’s global reach at a time when Europe is already struggling to contain Russian aggression on its own continent. Supporting democratic survival or democratisation abroad is not only a normative commitment, but a strategic interest: Europe’s democratic stability—and its own way of life—are reinforced when democracies elsewhere endure.

Democratisation in Venezuela could bring concrete benefits. It would weaken Russia’s standing among authoritarian partners that depend on its support and reduce diplomatic alignment against European priorities in multilateral forums. Such alignment was evident, for example, in the 2014 UN resolution condemning Russia’s annexation of Crimea, where several Latin American governments sided with Moscow. Moreover, a democratic Venezuela could reduce the US’ attention diversion from the Russia war on Ukraine, and it could weaken Russia’s potential leverage when looking for US-concessions, in exchange for their own concessions in Venezuela.

But this is also about not missing opportunities. A democratic Venezuela could reintegrate into Mercosur, opening an additional market under the forthcoming EU-Mercosur agreement—one of the EU’s tools for diversifying trade partners and reducing excessive economic dependencies.At a time when economic strength has become an existential priority for Europe amid rising geopolitical tensions, this matters. Before Mercosur, and in the more immediate period following a transition, Venezuela would require substantial investment to rebuild its economy. Historical economic and social ties already exist, shaped in large part by post–Second World War European migration to the country.

Repression is not confined to Venezuelan citizens. More than 80 foreign political prisoners have been reported, including Europeans from Italy, Spain, Poland, Portugal, Hungary, Ukraine and the Czech Republic.

In the path towards the stabilisation of Venezuela as a partner to democracies—instead of being a source of autocratic threat—the democratic mandate expressed by Venezuelans on 28 July 2024, when we elected Edmundo González Urrutia as president, is a crucial element to consider. González has since identified María Corina Machado as his intended vice-president in a potential transition.

In regards to the question about how to get there, the equation toward a democratic Venezuela does not only include measures to weaken the Maduro regime’s repressive capacity, but also strengthening democratic actors inside and outside the country. Many of these active citizens often move within resource-limited bounds—juggling work, precarious living situations and scarce resources for essential tools such as websites, digital security, travel for advocacy, and organisational infrastructure. Migrants in early integration phases do not necessarily count with abundant financial resources, yet they invest what they have into their democratic efforts.

At the same time, the regime’s repressive reach extends beyond Venezuela’s borders. Recent transnational attacks like the murder attempt against Luis Alejandro Peche and Yendri Velásquez in Colombia, the attempted attack on Vente Venezuela’s Alexander Maita, and the assassination of Ronald Ojeda in Chile highlight efforts to intimidate political mobilization even outside the country.

But repression is not confined to Venezuelan citizens. More than 80 foreign political prisoners have been reported until this month, including Europeans from Italy, Spain, Poland, Portugal, Hungary, Ukraine and the Czech Republic. Thus, limiting the regime’s repressive capacity is vital to incentivize crucial pro-democracy mobilization.In summary, Europe faces a choice. Supporting Venezuelan democratisation is not only a matter of global democratic solidarity, human rights, or European soft power in Latin America. It is a matter of self-preservation. The collapse of Venezuela’s once-stable 40-year democracy and Russia’s war on Ukraine both serve as reminders that democracy—and the peace it sustains—is not a given. It must be embodied, defended, and actively built when necessary.

In banking as in other industries, AI is rapidly becoming a core business driver. The biggest gains will come from a foundational rethink of operations, not marginal improvements.

The financial sector is undergoing a profound transformation, powered by AI. Banks’ strategic integration of AI is moving beyond simple efficiency gains to make the technology a core business driver, focused on hyper-personalization, augmentation of human talent, and robust governance.

The real opportunity, says Andy Schmidt, vice president and global industry lead for Banking at CGI, [our AI in Finance judging partner], lies not in simply applying AI to existing workflows, but in fundamentally rebuilding processes with AI at the core.

A key aspect of this transformation is the shift towards an ultra-personalized and predictive customer experience. AI is moving past rudimentary chatbots to become an “agentic, conversational assistant” that can proactively anticipate a customer’s needs: from preventing payment failures by automatically increasing card limits to providing tailored financial guidance and real-time product recommendations.

Going forward, this intensified focus on customer experience will be a significant component of return on investment (ROI), Schmidt predicts.

“The real value comes in improved customer experience,” he stresses. “Being able to onboard customers more quickly, being able to transition from opportunity to revenue more quickly, and optimizing the customer experience so that they remain satisfied and stay with the bank over time.”

Schmidt highlights success stories in wealth and personal finance where GenAI drives personalization recommendations. DBS Bank’s harnessing of AI, for example, has drastically accelerated customer journeys, demonstrating the potential for significant scale and opportunity.

Human-AI Augmentation

The case for AI adoption in banking centers on strategic augmentation, were AI becomes a co-pilot for human experts. The goal is to automate repetitive and low-value tasks, freeing up human capital to focus on such complex, high-value activities as strategic decision-making, advisory sales, and conflict resolution.

Further driving this internal empowerment is the democratization of GenAI tools across the workforce, accelerating research, analysis, and data synthesis. Crucially, banks must commit to the principle of human oversight, ensuring that for complex matters, a human being is always in the loop and remains the final decision-maker.

AI’s role in risk management is evolving from reactive analysis to real-time, predictive analytics. By continuously monitoring vast internal and external data streams, AI can anticipate potential risks and perform complex what-if scenario planning. This capability couples with enhanced fraud detection, where sophisticated AI, including neural networks, provides real-time surveillance and prevention across massive transaction volumes.

AI is also streamlining the traditionally costly and time-consuming realm of regulatory compliance. Schmidt emphasizes the value of AI in bringing “transparency, auditability, and repeatability to key processes, especially when it comes to compliancerelated processes like KYC [know your customer].” Relatedly, AI is automating tasks like credit report preparation and enhancing the rigor of due diligence on complex M&A transactions.

Maximizing ROI Gain

A significant lesson emerging from AI deployment is that the most substantial returns come from a foundational rethink of operations, not marginal improvements. The financial industry is recognizing that “adding AI to existing processes will make them marginally better,” Schmidt notes, but that “optimizing processes to leverage AI will make them dramatically better.” The best way to realize the benefits of AI transformation, he adds, is in “examining these long-standing processes, optimizing them, and fundamentally rebuilding them. The goal is to integrate AI at the core of the process, rather than sprinkling it on top as an afterthought.”

With every aspect of AI adoption, however, the best approach is to proceed in stages. For those beginning their AI journey, Schmidt suggests adopting large language models (LLMs) as a starting point before transitioning to more specialized, purpose-built models. The effective integration of AI requires continuous change management to sustain capabilities and maximize ROI over time.

Methodology

The Global Finance AI In Finance award winners are chosen based on entries provided by financial institutions. Entrants are judged on the impact, adoption, and creativity that AI brings to both systems and services. Winners are chosen from entries submitted by banks and evaluated by a world-class panel of judges at CGI, a leading multinational IT and business consulting-services firm. CGI is a trusted AI expert that combines data science and machine slearning capabilities to generate new insights, experiences, and business models powered by AI. The editors of Global Finance are responsible for the final selection of all winners.

Meet The Winners

Global Winners

Consumer Winners

Corporate Winners

Winner Insights

Gökhan Gökçay, executive VP of Technology at Akbank

Nimish Panchmatia, Chief Data & Transformation Officer, DBS

Artificial intelligence is transforming the banking industry, streamlining operations, improving risk management, and enhancing the customer experience.

Banks are leveraging this burgeoning tech to automate routine tasks, analyze complex data, detect fraud, and deliver personalized financial advice—all with greater speed and accuracy. For consumers, this translates to more efficient services, faster responses, and smarter financial solutions.

The winners below set the standard in AI-driven innovation by using AI to automate back-office operations, accelerate credit assessments, detect fraud in real time, and deliver personalized financial recommendations.

Others leverage AI to monitor customer journeys, identify pain points, and provide seamless virtual assistance. These innovations not only streamline operations but also give consumers faster, smarter, and more tailored banking services, setting a new standard for the industry.

Best Payments

AkBank

Best Chatbots & Virtual Assistants

CaixaBank

Best Enhanced Customer Experience

DBS Bank

Best Personalized Financial Advice

QIB

Best Private Banking

Bank of Georgia

Best Fraud Detection and Prevention

Banamex

Best Credit Assessment

Banamex

Best Risk Management

BBVA

Best Fintech

CTBC

Best Payments

Akbank

Aiming to enhance back-office efficiency and reduce friction, Akbank implemented an AI-driven solution in 2024, training an open-source LLM on over 100,000 banking documents. The custom-tailored LLM tool reinforces secure and compliant operations within the bank’s own data centers and is accelerating back-office automation, significantly improving accuracy, security, and overall efficiency, and underscoring the bank’s dedication to AI innovation and regulatory compliance.

Akbank is utilizing this AI-driven model primarily to automate payment order processing for both customers and regulatory institutions; it also plays an important role in automating back-office transaction orders, significantly reducing the need for manual intervention.

Best Chatbots & Virtual Assistants

CaixaBank

CaixaBank’s employees now have access to NOA, a GenAI-powered assistant designed to provide accurate answers to internal questions using NLP. The tool is a first for CaixaBank, setting a new standard for AI-driven operational efficiency at CaixaBank. Unlike traditional knowledge management systems, it eliminates the need for manual searching by directly retrieving precise information from the bank’s extensive internal documentation. In so doing, NOA has fundamentally altered the process by which 45,000 CaixaBank personnel access information, reducting the necessity for escalating issues and enhancing query resolution efficiency. The system currently handles more than 8 million queries a year, reducing response times and elevating the overall employee experience. User adoption has been swift, attributed to NOA’s intuitive interface and seamless integration within workflows.

Best Enhanced Customer Experience

DBS Bank

DBS Bank pioneered an industry-first Negative Customer Impact (NCI) Control Tower in 2024 that enhances service management by identifying customer pain points and “silent sufferers” in real time. It focuses on key customer journeys to detect performance anomalies early, enabling an effective and timely response while minimizing customer impact.

The NCI Control Tower provides crucial transparency on customer behavior and client performance data to platform and business owners, facilitating ongoing improvement of the customer journey. This comprehensive approach, covering a broad spectrum of service performance dimensions, significantly enhances DBS’s resilience and response capabilities. Since its launch, NCI teams have scaled across more than 15 customer-facing channels, encompassing the delivery of more than 300 customer journeys.

Best Personalized Financial Advice

QIB

QIB’s upgraded AI-driven Next Best Offer (NBO) 2.0 recommendation engine uses deep learning on customer behavior, transactions, and financial patterns to deliver personalized, real-time financial product recommendations. Its key feature is non-intrusive, seamless integration into QIB’s mobile app, providing tailored product information without disrupting core banking.

The AI algorithms evolve, improving accuracy and engagement over time. NBO 2.0 analyzes over 1,600 customer attributes—including demographics, holdings, transactions, and interaction data over five years—to pinpoint the customer’s financial journey stage and suggest the most appropriate products. It also provides valuable data for product portfolio refinement.

Best Private Banking

Bank of Georgia

Bank of Georgia (BoG) is setting a new standard in client acquisition with a dual strategy for identifying and converting high-potential, affluent clients who primarily bank elsewhere. By leveraging these external sources, BoG can detect “invisible” high-income individuals who have minimal engagement with the bank’s current ecosystem: a significant improvement over traditional identification methods that rely on publicly available external data. This fusion of AI and strategic intelligence provides a tailored approach to building the client base, making BOG a leader in data-driven banking innovation.

Best Fraud Detection And Prevention

Banamex

Banamex is employing AI and machine learning, specifically including neural networks, for real-time fraud detection and prevention. The bank reports a 70% reduction in attempted fraud since it integrated AI throughout its operations in March 2024. Banamex combines rules-based systems, data mining, and neural networks to activate a unified system capable of instantaneous analysis and response to potentially fraudulent activities.

A critical element involves implementing the FICO Falcon Fraud Manager solution. The real-time processing capabilities of the tool’s neural network models mitigate fraud-related losses and enhance detection accuracy by identifying fraud at the point of sale, prior to transaction completion. Its AI infrastructure processes voluminous amounts of transaction data in real time to discern patterns, anomalies, and deviations from behavioral norms, enabling it to promptly flag and potentially inhibit suspicious transactions.

Best Credit Assessment

Banamex

Banamex is leveraging AI to revolutionize its credit assessment process, shifting from slow, traditional methods to real-time evaluations. AI algorithms analyze vast datasets, incorporating up to 200 variables—including traditional financial metrics and potential alternative sources like geolocation—to create a comprehensive, multidimensional, and more accurate view of the applicant’s creditworthiness. This dynamic model significantly improves decision-making speed, the bank reports, particularly for high-volume tasks, and enhances overall operational efficiency by automating data processing and analysis.

AI and data analytics deliver tangible customer benefits as well. Faster credit approvals and personalized services, driven by AI insights, elevate the overall customer experience and thereby help Banamex maintain a competitive advantage in Mexico’s rapidly evolving financial sector.

Crucially, AI-powered credit assessment contributes to the goal of financial inclusion by providing the opportunity to enter the formal banking system to prospects with limited or no established financial history. Typically, the options available to low-income individuals or those operating only in the informal economy are limited in capacity, come with substantially higher annual percentage rates, and may involve tough collection practices. Access to financing from a formal player like Banamex can be a life-changing event for these applicants.

Best Risk Management

BBVA

BBVA utilizes Mexico’s extensive transfer network, analyzing both direct and indirect data including recurring client-to-nonclient transactions, to accurately estimate client income. This enables effective assessment of those with limited banking activity, optimizing the credit offer based on true financial stability.

Transfer analysis is the foundation of a sophisticated relationship model that identifies financial links and inherited assets and detects irregular activities like triangular movements and simulated income, enhancing accuracy and mitigating fraud. This enables BBVA to offer better-tailored financial products, promoting responsible and secure credit access.

The model is applied across BBVA’s entire client portfolio—those holding existing credit products and those not—providing a valuable tool for business units needing insights into clients’ economic standing and repayment capacity. Integrating multiple data sources—including credit bureau reports, investments, transactions, relationship graphs, and payroll—ensures thorough evaluation, reducing risk and optimizing credit allocation. This multisource approach yields precise opportunity identification, ensuring BBVA’s marketing campaigns align with its risk appetite while minimizing exposure to clients who lack financial capacity.

A critical component is assigning a predicted income range, refining the bank’s marketing campaigns to align with a predetermined risk level. This leads to enhanced prediction stability and optimized credit offers, ultimately maximizing profitability and reducing default risk.

Best Fintech

CTBC

CTBC Bank’s AI Cheque Check is notable as Taiwan’s first AI-based check recognition system, achieving over 90% accuracy in interpreting traditional Chinese handwriting, the bank reports, by integrating advanced handwriting recognition and centralized processing.

Initially developed for internal use, it has significantly boosted check processing efficiency and accuracy across CTBC Bank’s branch network, eliminating the manual verification bottlenecks inherent in traditional processing, thereby accelerating check clearance and minimizing human error.

AI Cheque Check uniquely combines optical character recognition, structured transaction data, and AI-driven compliance checks to ensure smooth automation while maintaining crucial regulatory accuracy. It benefits the Taiwanese bank’s customers as well by speeding up transaction times and improving service quality.

Gökhan Gökçay, executive VP of Technology at Akbank, explains how his bank—named the World’s Best Consumer AI Bank—uses AI and partnerships to tailor service and secure data.

Global Finance: What impact has Akbank’s AI-powered digital assistant had on customer loyalty, and how does it contribute to your 96% digital migration rate for sales?

Gökhan Gökçay: Akbank Assistant has become a cornerstone of our customer engagement strategy by delivering fast, personalized, and seamless banking experiences across all channels. By enabling customers to complete more than 200 types of transactions autonomously and resolving 250,000 monthly support sessions through the “Help Me” module, it has significantly enhanced convenience and satisfaction.

The Assistant’s proactive and context-aware guidance, combined with human-like voice interaction, has fostered stronger emotional connections and loyalty. This trust and ease of use have been key drivers in Akbank’s remarkable 96% migration rate of transactions, including sales and inquiries, to digital channels.

Moreover, the Assistant’s recommendation engine, powered by advanced analytics and large language models, has increased product conversion rates from 2% to 18%, demonstrating that intelligent personalization directly translates into customer engagement and business growth. Customers now engage with our digital platforms over 700 million times daily, reflecting a deep behavioral shift toward mobile-first, AI-supported banking.

GF: Akbank uses AI to provide “Banking IQ” insights to customers, such as cash flow analysis and spending patterns. How do these insights directly translate into better financial habits for your customers, and what is your approach to turning these insights into proactive, personalized product recommendations?

Gökçay: Through AI-powered “Banking IQ” insights, Akbank analyzes customer cash flow, spending patterns, and savings behavior to provide meaningful, actionable financial guidance. These insights empower customers to make smarter financial decisions, such as optimizing savings, avoiding overdrafts, or rebalancing investments, based on real-time data.

The same infrastructure supports our agentic recommendation engine, enabling customers to better understand their financial habits, stay in control of their goals, and develop long-term financial wellness, turning data into trusted everyday advice that drives healthier financial behavior.

GF: Given your use of AI to create hyper-personalized customer experiences, how do you balance the drive for personalization with customer data privacy concerns, and what specific measures are in place to ensure compliance and maintain customer trust?

Gökçay: At Akbank, personalization is built on trust, transparency, and ethical responsibility. All AI systems are designed in full compliance with Turkey’s banking and data protection regulations. In 2025, we introduced the Akbank Responsible AI Manifesto, publicly affirming our commitment to ethical and responsible AI. The manifesto defines a set of nonnegotiable principles—fairness, transparency, accountability, inclusiveness, and data privacy—that guide every stage of our AI lifecycle, from model design to deployment.

Our dedicated AI governance framework continuously monitors model behavior, bias, and data use, while regular audits ensure compliance with both regulatory and ethical standards. By embedding these principles into our technology, we ensure that personalization always empowers customers, strengthens trust, and reinforces our long-term human-centered AI vision.

GF: Can you describe how Akbank LAB collaborations with fintechs and tech companies accelerate AI innovation, and what role these external partnerships play in Akbank’s overall long-term AI strategy?

Gökçay: Akbank LAB acts as the innovation bridge connecting our bank’s internal R&D ecosystem with fintechs, startups and global technology pioneers. Established in 2016, Akbank LAB has become one of the world’s leading financial innovation centers, recognized as part of Global Finance’s Innovators 2025 list.

Collaborations with companies like Personetics and Jasper accelerate the development of advanced personalization, conversational intelligence, and generative AI capabilities. However, Akbank’s open innovation approach goes beyond specific partnerships. We value every collaboration that enhances or personalizes our customers’ experience. We believe in the power of the ecosystem where shared innovation drives transformation and progress across the financial landscape.

In mid-November, the Hong Kong government priced an approximately HK$10 billion ($1.3 billion) tokenized green bond offering. It is the first global government issuance to permit settlement via digital fiat currencies and one of the largest digital bonds issued globally.

The Hong Kong Monetary Authority, the territory’s de facto central bank and bank regulator, issued the bond in four tranches across several currencies. The Hong Kong dollar and yuan tranches can be settled using e-HKD and e-CNY, digital versions of those currencies based on blockchain technology, alongside traditional settlement methods.

Sovereign tokenized bonds indicate financial centers no longer compete on just cost or liquidity, “they are now competing on infrastructure,” says Dor Eligula, co-founder of BridgeWise. “Hong Kong’s move accelerates a shift toward markets where data is auditable in real-time, and settlement becomes a feature rather than a friction. That ultimately reshapes the global hierarchy of capital markets.”

“Riding on our established strengths in financial services, this issuance will further consolidate Hong Kong’s status as a leading green and sustainable finance hub,” said Christopher Hui Ching-yu, secretary for financial services and the treasury, in the November 11 announcement.

Specifically, investors purchasing the HK$2.5 billion, two-year tranche would receive 2.5% in annual interest for two years. The 2.5 billion yuan ($351 million), five-year tranche yielding 1.9% annually, with the $300 million, three-year tranche returning 3.6%, and the €300 million ($348 million) four-year tranche paying 2.5% annually.

The offering drew total demand of more than HK$130 billion, with subscriptions from a range of international institutional investors, including multinational banks, investment banks, insurers, and asset management firms, according to an HKMA prepared statement.

The current bond offering will finance and refinance projects under the government’s Green Bond Framework. The government issued two batches of tokenized green bonds—an HK$800 million batch in February 2023 and another worth around HK$6 billion in February 2024.

The latest issuance extends the tenor up to five years. Compared with previous issuances, the number of investors has also “expanded markedly,” according to the HKMA.

Following tense negotiations among the 27 member states, Commission President Ursula von der Leyen on Thursday pushed the signature of the contentious Mercosur agreement to January to the frustration of backers Germany and Spain.

The trade deal dominated the EU summit, with France and Italy pressing for a delay to secure stronger farmer protections, while von der Leyen had hoped to travel to Latin America for a signing ceremony on 20 December after securing member-state support.

Without approval, the ceremony can no longer go ahead. There is not set date.

“The Commission proposed that it postpones to early January the signature to further discuss with the countries who still need a bit more time,” an EU official told reporters.

After a phone call with Brazilian President Luiz Inácio Lula da Silva, Prime Minister Giorgia Meloni said she supported the deal, but added that Rome still needs stronger assurances for Italian farmers. Lula said in separate comments that Meloni assured him the trade deal would be approved in the next 10 days to a month.

The Mercosur agreement would create a free-trade area between the EU and Argentina, Brazil, Paraguay and Uruguay. But European farmers fear it would expose them to unfair competition from Latin American imports on pricing and practices.

Meloni’s decision was pivotal to delay

“The Italian government is ready to sign the agreement as soon as the necessary answers are provided to farmers. This would depend on the decisions of the European Commission and can be defined within a short timeframe,” Meloni said after speaking with Lula, who had threatened to walk away from the deal unless an agreement was found this month. He sounded more conciliatory after speaking to Meloni.

Talks among EU leaders were fraught, as backers of the deal – concluded in 2024 after 25 years of negotiations – argued the Mercosur is an imperative as the bloc needs new markets at a time in which the US, its biggest trading partner, pursues an aggressive tariff policy. Duties on European exports to the US have tripled under Donald Trump.

“This is one of the most difficult EU summits since the last negotiation of the long-term budget two years ago,” an EU diplomat said.

France began pushing last Sunday for a delay in the vote amid farmers’ anger.

Paris has long opposed the deal, demanding robust safeguards for farmers and reciprocity on environmental and health production standards with Mercosur countries.

The agreement requires a qualified majority for approval. France, Poland and Hungary oppose the signature, while Austria and Belgium planned to abstain if a vote were held this week. Ireland has also raised concerns over farmer protections.

Italy’s stance was pivotal.

However, supporters of the agreement now fear prolonged hesitation could prompt Mercosur countries to walk away after decades of negotiations for good.

After speaking with Meloni, Lula said he would pass Italy’s request on to Mercosur so that it can “decide what to do.”

An EU official said contacts with Mercosur were “ongoing,” adding: “We need to make sure that everything is accepted by them.”

Dealmakers in 2025 enjoyed a near-record year for mergers and acquisitions, despite a turbulent spring that threatened hopes of a broader revival. So far this year, there were 70 global deals valued at more than $10 billion each, 22 of them in the fourth quarter, according to Dealogic. Total deal value has surpassed $4.8 trillion, up 41% from 2024, though the number of deals fell 6% to 38,395, marking the second-largest year ever behind 2021.

The spike in mega deals reflects a growing focus on scale. “M&A today is all about the mega deals, the race for scale,” said Anu Aiyengar, JPMorgan’s global head of advisory and M&A. There were at least four deals above $50 billion, with two notable bids for Warner Bros. Discovery totaling over $80 billion and Paramount Skydance’s $108 billion hostile offer.

Drivers of Late-Year Rally

A more permissive regulatory environment in the U.S., coupled with a calmer macroeconomic outlook, is encouraging companies to pursue transformative deals. With antitrust scrutiny easing under the Trump administration, boards and executives are seizing opportunities for strategic acquisitions, according to Frank Aquila, partner at Sullivan & Cromwell.

Dealmakers also say valuations are rising, prompting companies to pay higher multiples while expecting their own stocks to maintain relative strength. “Valuations have been bid up and we’ve seen clients be more aggressive in terms of multiples,” said Lazard’s Mark McMaster.

Technology and AI Influence

Technology deals, particularly those tied to artificial intelligence, have played a prominent role. OpenAI raised $40 billion in funding led by SoftBank, and Aligned Data Centers was acquired for $40 billion. Morgan Stanley’s John Collins said companies are pursuing scale to invest in AI-driven changes, both in tech and across other industries.

Cross-Border and Global Trends

Cross-border M&A activity surged in 2025, reaching $1.24 trillion, the highest since 2021. U.S. and UK companies were the most targeted, while U.S., France, and Japan were the most acquisitive. Multinational companies, particularly from Europe and Japan, are investing in the U.S. to capitalize on the world’s largest market. China and Japan are also seeing strong outbound activity, with Japanese deal values boosted by high-profile transactions like OpenAI and Toyota Industries.

Corporate divestitures are rising, up 30% in volume from last year, exemplified by Holcim’s $30 billion spin-off of its North American business, Amrize. Private equity is also regaining momentum, with global buyouts reaching $1.1 trillion, a 51% increase from 2024.

Outlook for 2026

Dealmakers expect the M&A rally to continue into 2026, with $50 billion–$70 billion deals already in the pipeline and a $100 billion tech transaction not ruled out. Analysts see a multi-year run of high-value deals, fueled by scale-seeking corporations, AI-related opportunities, cross-border expansion, and corporate restructuring. While caution remains in politically uncertain markets like the UK, the global appetite for transformative deals appears set to drive another strong year for mergers and acquisitions.

Some argue that warnings about private credit’s risks reflect not just financial caution but tension and competition between banks and private lenders.

Blackstone’s latest move tells the story. In November, the firm led a £1.5 billion ($2 billion) private-credit package to finance London-based Permira’s buyout of JTC plc: a transaction backed by a who’s-who of heavyweight private lenders including CVC Credit, Singapore’s GIC, Oak Hill Advisors, Blue Owl Capital, and PSP Investments, along with Jefferies. The deal, which spanned multiple currencies and combined senior loans with revolving credit facilities, is the kind of complex tie-up that was once synonymous with big banks.

But today, this is what the center of corporate finance looks like.

Private Credit Soaks It In

Private credit, no longer a dimly lit corner of the financial markets, is now the go-to route for blockbuster deals. Since 2010, the market has grown nearly seven-fold and, according to the Bank for International Settlements, has swelled into a $2.5 trillion global industry, putting it on par with the syndicated-loan and high-yield bond markets.

On the surface, private credit seems to be eating the bankers’ lunch. After all, only one of the firms that participated in the Blackstone deal—Jefferies—is a traditional investment bank. But the reality is more complicated. The rise of direct lending hasn’t eliminated the old guard, but forced banks and private-credit firms into an uneasy partnership, with each increasingly intertwined in the other’s success.

Jamie Dimon, Chairman and CEO of the US’s largest bank, doesn’t like it.

Dimon sounded the alarm on an October 14 call with analysts, warning of “cockroaches” lurking in opaque corners of the private credit market. That same day, Blue Owl Capital’s co-CEO Marc Lipschultz clapped back at Dimon’s “fear mongering,” putting the blame on the syndicated loan market, not private credit itself.

Prath Reddy, president of Percent Securities

It’s an “interesting dichotomy,” says Prath Reddy, president of Percent Securities, an investment manager specializing in private credit. The players involved, he argues, are all in bed with each other anyway.

Yes, private credit lenders are largely unregulated and nontransparent about their risky line of business. And traditional banks may be regulated. But banks keep busy lending directly to private businesses and financing the private credit firms themselves.

“All the large investment banks also have major stakes in—and in many cases control over—asset managers that are competing with the existing private credit funds out there that they claim are eating their lunch,” says Reddy. “They’re trying to hedge that lunch from being eaten by playing directly with them.”

How We Got Here

As bank regulations tightened after the 2007-08 financial crisis, traditional lenders found their balance sheets constrained. This opened the door to non-bank lenders. Brad Foster, head of fixed income and private markets at Bloomberg, says this shift reshaped the entire corporate finance ecosystem.

Post-crisis, new regulations put real pressure on bank capital.

“As that happened, obviously more of what was that corporate borrow base shifted from what was traditionally bank capital into non-bank capital,” says Foster.

What began as a simple, one-to-one lending model quickly evolved. Direct lenders grew into “clubs” that mirrored the bank-dominated syndicates; their borrowers expanded from private, middle-market companies to public firms and even investment-grade issuers. Deals once destined for the syndicated-loan or high-yield bond markets increasingly migrated to private credit instead.

“It’s difficult to argue this hasn’t had an impact on banks,” Foster adds. “Large deals are being financed away from the public markets.”

Still, he notes, the relationship isn’t purely competitive. Banks and private-credit managers now frequently partner on transactions, blending capital from both sides. Sponsors today “will pick and choose whether to go to the bank market or the non-bank market:” a choice that didn’t exist at this scale a decade ago.

The result? Highly bespoke capital structures that entice sponsors and investors alike, due to the speed and flexibility with which deals can get done.

Private credit, for example, has helped private equity sponsors orchestrate leveraged buyouts. Notable examples include Vista Equity Partners, which teamed up with Ares Management to finance the $10.5 billion acquisition of EverCommerce. Similarly, Apollo Global Management relied on its private credit division to fund its $8 billion purchase of Ancestry.com, offering custom high-yield loans as banks hesitated in the face of rising interest rates. Additionally, Carlyle Group turned to Oaktree Capital Management for private credit to complete its $7.2 billion buyout of Neiman Marcus, as banks were reluctant to finance retail deals amid economic uncertainty.

By nature, however, the new system is less liquid, and back-leverage facilities can make restructuring more difficult.

So far, there have been no significant defaults or loan losses across the private credit portfolio, according to Matthew Schernecke, partner at Hogan Lovells in New York. But it’s uncertain “how great a risk a broader systemic shock may be if the number of defaults and loan losses are amplified in a significant way,” he adds.

“Banks try to hedge their lunch from being eaten by playing directly with private lenders,”

Prath Reddy, Percent Securities

‘Cockroaches’ To Blame?

The market got a whiff of what that systemic risk test would look like after the collapse of auto sector companies Tricolor and First Brands, whose bankruptcies highlighted private credit exposure’s vulnerabilities.

UBS had more than $500 million committed to First Brands through several of its investment funds. Even though its direct private credit exposure turned out to be relatively small, the situation was severe enough to spark a contentious back-and-forth over whether non-bank “cockroaches” were to blame, as JPMorgan’s Dimon suggested.

Hogan Lovells’ Schernecke sees both sides. On one hand, private credit deals are typically held rather than sold. This allows lenders to earn an illiquidity premium for concentrated risk and limited secondary market opportunities. This structure also enables fast execution; one or a few creditors can approve terms without broader market input.

On the other hand, underwriting standards can become compromised and looser documentation on large-cap deals can affect lower middle-market loans.

“Weaker loan documentation can lead to unintended consequences in private credit in which creditors are generally intending to hold their paper for an extended period and do not want to allow for significant leakage of collateral or value without their consent,” says Schernecke. “Given how fiercely competitive deployment opportunities have become, it is difficult for funds to push back on more ‘aggressive’ terms because they may be replaced by another fund to land the mandate.”

While most private credit funds will resist including the most egregious leakage provisions, being the first mover on any specific issue is difficult when other funds may be more willing to be flexible, he adds.

Banks’ concerns are partly competitive. Private credit has captured significant market share in middle-market and even large-cap lending, prompting Dimon and other executives to view it warily—while also getting cozy with their rivals.

What’s Next

As Percent’s Reddy notes, private credit’s growth—and its competition with banks—isn’t new. More than 15 years after the global financial crisis, bank lending shifted into “the hands of a few key players: Apollo, KKR, Blackstone,” he says. Today, they’re building out syndication desks and structuring loans just like the big banks did.

Reddy points to his former employer, UBS, as being “one of the first movers” when it came to adapting to the times. The bank began partnering with private equity firms and became more “sponsor-driven,” he says, since that’s where the opportunity lies for banks now. “I’ve seen the evolution firsthand.”

But if private credit’s flexibility is its strength, opacity is its Achilles’ heel. When banks originate syndicated loans, borrowers have regulatory oversight. Private credit funds don’t have to disclose much. If they put a deal on their balance sheet, no one knows the terms, the covenants, or even how collateral is verified, Reddy warns. That lack of visibility, he says, is why bank CEOs like Dimon can make ominous but unverifiable warnings.

“When Jamie Dimon speaks, the world listens,” Reddy quips. Dimon knows exactly how much exposure JPMorgan has to private credit funds, but must project vigilance for the sake of financial services in general.

When bank bosses accuse private credit funds of “eating their lunch,” then, Reddy isn’t so sure. At the end of the day, those private credit funds still have massive facilities with the banks, which have indirect exposure; they’re lending to all the largest lenders.

So, has lunch been eaten? Reddy wonders: “Maybe half-eaten.”

As Korea’s largest securities firm, managing USD 393.6 billion in client assets as of Q2 2025, Mirae Asset Securities has established itself as a global institution known for sophisticated investment capabilities and consistently high-quality service. Size is not its only strength; the company sees innovation as a strategic imperative—and is pursuing both organic and inorganic pathways to build a financial ecosystem that anticipates the future.

AI as the Engine of Organic Transformation

Artificial intelligence sits at the heart of Mirae Asset Securities’ transformation efforts. The firm has recruited global top-tier technology talent, overhauled its organisational culture, and embedded AI applications directly into frontline wealth-management operations.

These investments are yielding results. Clients can now access real-time global market information with automatic translation, improving the quality and speed of decision-making. Data shows that investors who use the firm’s AI-driven tools exhibit a 15% higher rate of active investment decisions than those who do not.

Two flagship systems, the Mirae Asset AI Wealth Assistant and the PB Desk Assistant, deliver personalised recommendations, alerts, and investment insights. AI systems have studied roughly 400 internal work manuals, enabling instant guidance on procedures and documentation. For private bankers, the impact is substantial: average preparation time for consultations has dropped to one-quarter of the previous level, directly enhancing the quality of client engagement.

To sustain this momentum, the company launched an AI Digital Finance Expert Program with KAIST(Korea Advanced Institute of Science Technology) and offers a suite of internal training programmes, including online learning through Udemy for all wealth-management and private banking employees. The goal is clear: build a workforce capable of leading, not just responding to, industry change.

Acquisitions Fuel the Next Wave of Innovation

Mirae Asset Securities’ commitment to innovation also extends beyond Korea’s borders through targeted acquisitions and strategic investments. Recent deals by affiliate Mirae Asset Global Investments include the acquisition of Stockspot, an Australian robo-advisor, and the creation of Wealth Spot, an AI-driven asset-management company in New York. These ventures strengthen the firm’s own AI investment models, supporting internally managed robo-advisory assets that now total approximately USD 2.6 billion.

The firm is also collaborating closely with Global X— Mirae Asset Global Investments’s U.S. ETF subsidiary—on AI-enhanced market strategies and expansion into Asia’s fast-growing technology markets, including China Core ETFs.

In a major push into emerging markets, Mirae Asset Securities recently acquired 100% of India’s Sharekhan. Today, roughly 60% of its employees and nearly half its clients are based overseas, reinforcing its position as a global private bank with almost USD 400 billion in client assets.

Shaping the Future Through Digital Assets

Alongside AI, digital assets represent the next major pillar of innovation. Mirae Asset Securities was the first Korean securities company to complete Phase 1 of a Security Token Offering (STO) platform under the Financial Services Commission’s regulatory sandbox.

It is now building a blockchain-based system that integrates issuance, investment, payment, and settlement—supported by partnerships with SK Telecom, Hana Financial Group, and a working group of 23 global service providers.

Mirae Asset 3.0: A Group-Wide Re-Targeting

Mirae Asset Group—which includes Mirae Asset Securities—is taking another bold leap forward following two earlier eras: 1.0, marked by its founding and the pioneering of mutual funds, and 2.0, defined by global expansion and ETF leadership. In October 2025, the Group declared the beginning of a new 3.0 era, advancing toward a future in which traditional and digital assets converge, powered by innovation in Web3 and digital assets.

While innovation inherently involves risk, Mirae Asset Group continues to move forward with unwavering conviction, guided by the long-term global strategy and leadership of its Founder & Global Strategy Officer (GSO).

Anchored by this vision, the Group surpassed KRW 1,000 trillion in client assets in just 28 years since its founding (as of July 2025).

In a global market where many institutions speak of innovation, Mirae Asset Group demonstrates what true innovation looks like—bold, disciplined, and relentlessly future-focused.

As a permanent innovator, the Group—and Mirae Asset Securities—will continue to evolve in ways that draw heightened attention from the world of global private banking.

Austrian MEP Thomas Waitz (The Greens) told Euronews that the European Commission should rethink its budget plans in order to shield EU farmers from the impact of the Mercosur agreement, which could be adopted this week.

Under the Commission’s proposal for the 2028–2034 budget, funding for the Common Agricultural Policy would fall by 20%. Critics of the Mercosur deal argue it would expose EU farmers to unfair competition, as imports from South American countries could be more competitive on the European market.

“You cannot cut the funds by 20% literally and by 40% if you include inflation and sacrifice the farmers just for the profit of a few national companies or European industry,” Waitz told Euronews.

He said large agribusinesses stand to gain from the agreement, while small and medium-sized farmers would bear the costs.

EU farmers protest deal

The coming days are decisive for the trade pact, concluded in 2024 between the European Commission and Mercosur countries – Argentina, Brazil, Paraguay, and Uruguay – to establish a transatlantic free trade zone.

The European Parliament remains sharply divided over the deal. Tuesday will see lawmakers vote on a Commission-backed safeguard clause to monitor potential market disruptions from Mercosur imports, while EU member states are also expected to take a position at the Council in the coming days.

Commission President Ursula von der Leyen hopes to travel to Latin America on Saturday to sign the agreement in Foz do Iguaçu, on the Argentina–Paraguay border,Euronews has learned.

EU farmers are set to protest on Thursday as national leaders gather for a European summit.

If no agreement is reached beforehand, the issue will be pushed to the top of the summit agenda, with tense negotiations expected.

Ireland and the Netherlands, previously critical of the deal, have yet to clarify their positions. Italian farmers are also voicing opposition, putting pressure on Prime Minister Giorgia Meloni to declare her stance.

“If we lose them, we lose the rural areas and the ability to supply our population independently with food,” Waitz added.

Italy’s silence on the Mercosur trade pact is deafening – and potentially decisive. Rome could become the kingmaker between supporters of the deal and countries seeking to block it.

European Commission President Ursula von der Leyen plans to fly to Brazil on December 20 to sign off the agreement. France, facing farmer anger over fears of unfair competition from Latin America, opposes the deal and wants to postpone the EU member states vote scheduled this week to allow the signature.

The trade pact with Mercosur countries – Argentina, Brazil, Paraguay, and Uruguay – aims to create a free-trade area for 700 million people across the Atlantic. Its adoption requires a qualified majority of EU member states. A blocking minority of four countries representing 35% of the EU population could derail ratification.

By the numbers, Italy’s stance is pivotal. France, Hungary, Poland and Austria oppose the deal. Ireland and the Netherlands, despite past opposition, have not officially declared their position. Belgium will abstain.

That leaves Italy in the spotlight. A diplomat told Euronews the country is feeling expose but that may not be a bad position to be in if it plays its cards rights to get concessions.

Coldiretti remains firmly opposed to the agreement

Rome’s agriculture minister had previously demanded guarantees for farmers.

Since then, the Commission has proposed a safeguard to monitor potential EU market disruptions from Mercosur imports. The measure, backed by member states, will be voted on Tuesday by EU lawmakers at plenary session in the European Parliament in Strasbourg.

Italy’s largest farmers’ association, Coldiretti, remains firmly opposed.

“It’s going to take too long to activate this safeguard clause if the EU market is hit by a surge of Mercosur’s imports,” a Coldiretti representative told Euronews.

On the other side, Prime Minister Giorgia Meloni faces a delicate balancing act between farmers and Confindustria, the industry lobby, while Italy remains the EU’s second-largest exporter to Mercosur countries.

This was also made clear by Agriculture Minister Francesco Lollobrigida a few days ago in Brussels. “Many industrial sectors and parts of the agricultural sector, such as the wine and cheese producers, would have a clear and tangible benefit [from the deal]. Others could be penalized,”he said.

This is why Italy has not taken a clear stance up to now. “Since 2024, we tried to protect everybody”, Lollobrigida argued, while remaining ambiguous on the country’s position.

Supporters of the deal are wooing Meloni, seeing her as the path to get the agreement done and open new markets amid global trade obstacles, including nationalist policies in the US and China.

“As long as the Commission president is preparing to go to Brazil to the Mercosur summit, we need to do what’s necessary for that to happen,” an EU senior diplomat from a pro-deal country said.

Yet uncertainty lingers. No one wants to schedule a vote that might fail, and Italy’s prolonged silence is rattling backers, sources told Euronews.

One diplomat familiar with the matter speaking to Euronews conceded “it’s hard, looks difficult”.

The global banking industry is currently in the midst of a profound digital transformation, propelled by the accelerating pace of technological advancements and the continuously evolving expectations of modern consumers and clients.

At the vanguard of this monumental shift are the World’s Best Digital Banks 2025, institutions that are not merely adapting to change but actively demonstrating how innovative digital strategies can fundamentally reshape and redefine the landscape of financial services.

These leading digital banks excel by integrating strategic vision, a customer-centric approach, and robust technology such as AI, blockchain, and the cloud. This combination offers tailored solutions both for individual consumers through personalized experiences and for businesses via sophisticated digital platforms, creating new financial interaction paradigms for the 21st century.

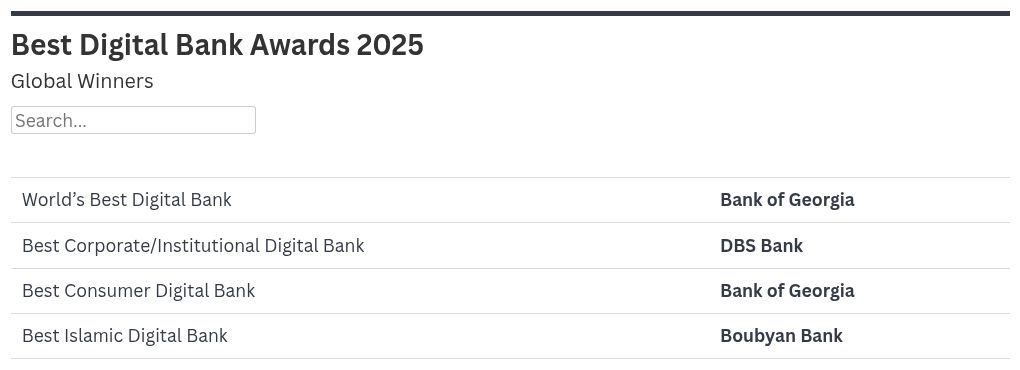

World’s Best Digital BankandBest Consumer Digital Bank

Bank of Georgia

For the second consecutive year, Global Finance has named Bank of Georgia (BOG) the World’s Best Digital Bank and Best Consumer Digital Bank. This achievement highlights BOG’s commitment and leadership in digital banking, stemming from a strategic vision, customer focus, and in-house technological innovation.

At the core of BOG’s strategy is CEO Archil Gachechiladze’s “customer obsession.” This principle drives the bank to deliver intuitive, inclusive, and customer-centric banking. BOG achieves this by consistently understanding and adapting to the evolving demands of its diverse customer base.

A 700-strong, in-house IT team powers BOG’s digital agility. This team develops the bank’s core banking system, digital channels, and payment platforms. This self-reliance provides a competitive advantage, fostering rapid iteration and feature delivery. Minimizing third-party dependencies gives BOG control over its technological road map, allowing swift responses to market changes. The bank’s microservices-based architecture has accelerated application development and transaction processing, boosting efficiency.

The bank has established itself as a leading innovator by developing an open-banking API marketplace—a catalog of APIs available to third parties, enabling integration of BOG’s services into third-party platforms—facilitating an ecosystem with hundreds of partners. This initiative significantly enhances the customer experience through a comprehensive mobile application that functions as a “financial super app,” says Gachechiladze. Going beyond traditional banking, the app integrates BOG’s Personal Finance Management tool for budgeting and spending analysis. It also proactively identifies and presents personalized loan and credit opportunities, including buy now, pay later options. The “super app” extends its utility beyond finance, incorporating services such as in-app stock trading; digital gift card purchases; and diverse payment solutions for transportation, covering car-related expenses including fines and parking, as well as public transport passes.

Customer convenience is central to BOG’s digital strategy. The bank offers 24/7 digital onboarding, allowing new customers to open accounts and receive digital debit cards instantly. This is supported by continuous, multichannel customer support via text, phone, or video chat.

BOG’s digital transformation includes innovative payment solutions. These involve using smartphones as payment terminals for small businesses and individuals. The bank has also pioneered face-recognition technology for payments. Furthermore, BOG developed a dedicated mobile application for businesses, streamlining operations and transactions.

Best Corporate/Institutional Digital Bank

DBS Bank

DBS Bank’s status as a leading digital bank is the result of a comprehensive digital-transformation strategy launched in 2014 with the goal of making banking effortless and seamless. This success is built upon several critical pillars.

The first of these foundational pillars is DBS’ commitment to tangible value from its technology, beginning with rigorous quantification of AI investments, attributing substantial financial gains to these initiatives. These gains are projected to reach 750 million Singapore dollars (about US$577 million) in 2024 and surpass SG$1 billion in 2025, a tangible demonstration of value that distinguishes the bank from its competitors.

Building on this strategic investment, DBS has industrialized its AI strategy, deploying over 1,500 AI and machine learning models across more than 370 use cases. These encompass internal operations, such as AI-driven audits for enhanced risk management; and a generative-AI (Gen AI) platform, DBS-GPT, that supports over 90% of staff, saving thousands of employee-days annually. Customer service is further enhanced by Gen AI–powered assistants that efficiently transcribe and summarize queries, while personalized nudges provide proactive financial guidance to clients.

Beyond consumer and internal applications, DBS prioritizes the customer journey for institutions and for small and midsize enterprises (SMEs) through the bank’s Managing through Journeys program. Digital innovations have led to a significant 30% reduction in time to open corporate accounts for SMEs in Singapore and halved the time required for implementing payment and collection API mandates. The bank’s digital lending platform for SMEs provides faster financing with improved credit risk assessment, resulting in a double-digit reduction in time-to-cash (the time it takes for a business to receive financing).

Complementing DBS’ internal strategy, an extensive ecosystem and API strategy that boasts over 400 partners empowers the bank to acquire new business without incurring traditional customer acquisition costs. DBS has also pioneered institutional blockchain services, facilitating instant multicurrency transaction settlements.

Finally, DBS’ success is deeply rooted in a fundamental cultural shift toward an agile, innovation-driven environment, mirroring a technology startup. This decade-long journey has been guided by a clear vision to “make banking joyful” through seamless digital experiences, a commitment now extended to corporate and institutional clients who can enjoy the same seamless and “joyful” banking experience as consumers.

Best Islamic Digital Bank

Boubyan Bank

For the past decade, Boubyan Bank has consistently been recognized by Global Finance as the World’s Best Islamic Digital Bank. This achievement is a testament to its strategic vision, which seamlessly integrates digital innovation with Islamic principles through a sustainable and focused approach.

Boubyan has successfully forged a “digital-first” Islamic identity, demonstrating that Islamic banking can be modern, digital, and highly appealing to a tech-savvy audience, particularly younger generations. The bank’s strategy is built on prioritizing customer satisfaction, driving revenue growth, and achieving cost reduction through innovative digital solutions.

As a pioneer in the Kuwaiti market, Boubyan offers “first-in-Kuwait” products that simplify banking and deliver unique value to both retail and business customers. Key innovations include Msa3ed, or Musaed, an AI-powered conversational banking assistant that provides instant support in both Arabic and English, further enhanced by Gen AI for more-intelligent interactions. Another significant milestone is the launch of Nomo: a UK-based, sharia-compliant, digital bank enabling Middle Eastern customers with international lifestyles to swiftly open UK accounts, offering multicurrency payments, international transfers, and sharia-compliant investment opportunities. Additionally, Boubyan provides a comprehensive suite of digital solutions for SMEs, such as ePay for collections and eRent for real estate management.

Customer experience is paramount to Boubyan’s digital strategy, meticulously guided by human-centered design. The bank consistently achieves high customer-satisfaction ratings, with an impressive 99% of financial transactions conducted through its mobile app. The bank’s numerous awards for customer service further underscore that Boubyan’s digital convenience is seamlessly supported by a robust service ethos.

Boubyan’s Digital Innovation Center facilitates rapid product launches unencumbered by legacy systems. The bank actively collaborates with global and regional fintech partners to integrate cutting-edge technologies, such as Snowdrop Solutions for data enrichment.

Internally, Boubyan harnesses AI for operational excellence. This is exemplified by the automation of corporate risk assessment, which has dramatically reduced processing time from weeks to mere hours. AI is also deployed to optimize call centers and enhance internal workflows, showcasing a comprehensive commitment to efficiency that extends beyond customer-facing tools.