Smaller enterprises look to boost value-added per worker. Global Finance names the winners of its third annual World’s Best SME Banks.

When it comes to productivity, bigger is usually better. Small and midsize enterprises (SMEs) and micro, small, and midsize enterprises (MSMEs) face a significant gap in value-added per worker compared to their larger peers.

Small-business productivity is half that of larger firms, according to a 2024 study by the McKinsey Global Institute (MGI). In emerging markets, the average is 29%, or a 71% gap. Kenya has the widest gap of the 16 emerging economies studied, at 94%, while Brazil has the narrowest, at 46%. In advanced economies, the average productivity gap is 40%, with Poland showing a 50% gap and the UK 16%.

These differences in value-added represent serious money left on the table, considering that MSMEs represent 90% of businesses globally: approximately half of the private-sector value-added and nearly two-thirds of business employment. According to MGI, the actual productivity ratio versus the top quartile level averages 5% and 10% of GDP for advanced and emerging economies, respectively.

“It ranges from 2% in Israel and the UK, to 10% in Japan among advanced economies, and from 3% in Brazil to 15% in Indonesia and Kenya among the emerging economies,” the authors reported. “On a per business worker basis, the amount is meaningful, ranging from about $3,000 in Israel to $12,900 in Japan among advanced economies and from $3,200 in Mexico to $8,800 in Indonesia among emerging economies (all in purchasing power parity terms).”

Lack of access to finance drives much, but not all, of the productivity gap. A World Bank study estimates that MSMEs face $5.2 trillion in unmet finance needs, or 50% more than the current lending market for such businesses.

Narrowing the gap

When MSMEs seek help to improve productivity, they can turn to governments, business partners, and financial institutions, each providing unique offerings.

Governments can assist with public financing programs and fund core infrastructure development, but poor management and oversight have often blunted their success.

“For decades, governments in emerging market and developing economies have implemented programs to improve SME access to finance, often at a large budget cost. Yet, the SME financing gap remains large, especially in the least developed countries, and public budgets are tight,”

Jean Pesme, global director of the World Bank’s Finance, Competitiveness, and Innovation Global Practice

He suggests governments adopt “a more evidence-driven approach for the design and implementation of support to ensure it reaches the SMEs facing the most critical financial constraints.”

On the other hand, the productivity gap can be bridged in part by creating an economic fabric in which larger and smaller companies work together, argues Olivia White, a senior partner at McKinsey and director of MGI. “That, in fact, boosts productivity both of the smaller firms and the larger ones,” she says.

The MGI study cited DuPont leveraging a banking relationship to secure working capital credit for its MSME suppliers in rural areas, strengthening its supply chain and increasing sales.

But not all help needs to be financial. The MGI report cites automotive MSMEs, which have “gained operational proficiency through systematic interactions with productive original equipment manufacturers, and small software developers [that] have benefited from talent and capital ecosystems seeded by larger companies.”

Financial institutions have historically been a two-edged sword for MSMEs, but that is changing. Banks fund MSMEs, but since the latter have less capital and security than larger players, they face more rigid credit-scoring models that slow account opening and lending.

Banks have adopted innovative underwriting approaches, however, that incorporate additional alternative credit data to deliver affordable credit. MSMEs have responded positively to these new offerings. An Experian survey found that 70% of small businesses are willing to furnish such data if it means a better chance to obtain credit or reduce their borrowing rate. Banks are also investigating how they might act as matchmakers between their MSME and larger clients.

“Financial institutions often own the most important connective links between smaller and larger firms, the payment rails,” says MGI’s White. “One of the major ways that small and large firms interact is one does something for the other, and there needs to be a payment. By maintaining those rails, banks make it easier for the smaller and larger firms to interact.”

Nevertheless, it is early days for providing such services, she adds. More financial institutions are talking about being matchmakers, and many are experimenting with platform mechanisms that could facilitate client-to-client connections. But there is more development work to be done before these platforms can scale. “I suspect it’s just going to depend a lot on the market and who sees that business opportunity,” says White.

Methodology

With input from industry analysts, corporate executives, and technology experts, the editors of Global Finance selected the World’s Best SME Banks 2025 winners based on objective and subjective factors. The editors consulted entries submitted by the banks as well as the results of independent research. Entries were not required.

Judges considered performance from April 1, 2024, to March 31, 2025. Global Finance then applied a proprietary algorithm to shorten the list of contenders and arrive at a numerical score of up to 100. The algorithm weights a range of criteria for relative importance, including knowledge of SME markets and their needs, breadth of products and services, market standing and innovation.

Once the judges narrowed the field, they applied the final criteria, including scope of global, regional, and local coverage, size and experience of staff, customer service, risk management, range of products and services, execution skills, and use of technology. In the case of a tie, the judges assign somewhat greater weight to local providers rather than global institutions. The panel also tends to favor private-sector banks over government-owned institutions. The winners are those banks and providers that best serve SMEs’ specialized needs.

BTG Pactual Empresas retains its ranking as the world’s best bank for small and mediumsized enterprises (SMEs). Its tremendous growth in the SME sector justifies this ranking.

SME lending has increased 28% year over year, with lending to this sector totaling R$28.3 billion (about $5.2 billion). SME loans now account for roughly 12% of the bank’s total credit book. And more than 30,000 SMEs opened new accounts with the bank in the first quarter of 2025 alone. Its NPL ratio is just 0.66%.

BTG Pactual offers a laundry list of general and sector-specific products for Brazilian SMEs. Consider its work in the agricultural arena. The bank reports that Brazil’s agricultural sector remains a vital pillar of the national economy. Accounting for approximately 25% of the country’s GDP, it is a key driver of productivity, employment and foreign trade. In addition to traditional banking services, BTG Pactual offers farmers flexible financing for essential products, such as fertilizers and seeds, as well as machinery financing and infrastructure loans for silos, warehouses, and logistics depots. Additional SME services include a B2B advisory network and an SME Insights portal, providing news and insights on entrepreneurship, management, and innovation.

Digital advances have done much to both attract new SME clients and retain existing ones. BTG Pactual’s digital capabilities in the field of same-day lending is one example: 96% of approved SME customers working with the bank’s digital lending platform have funds dispersed in less than 10 minutes.

Latin America Regional Awards

For more information on the BTG Pactual Empresas’ significant digital transformation efforts.

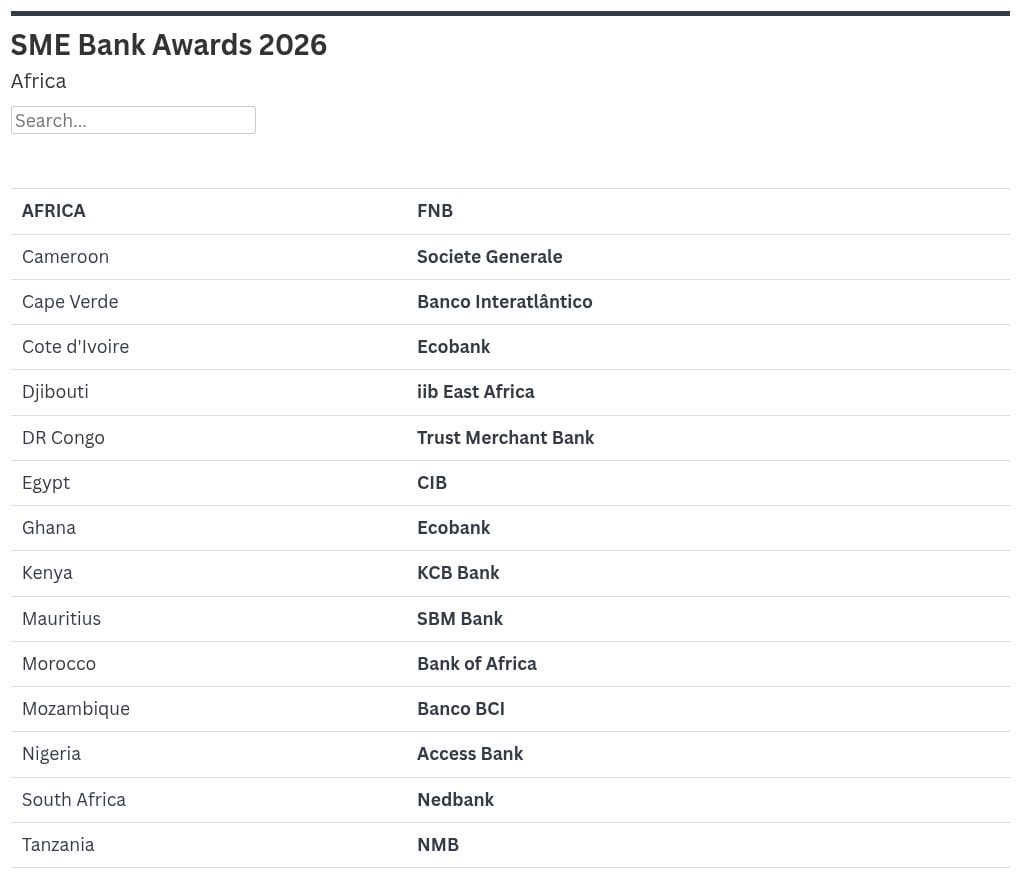

Small and midsize enterprises (SMEs) across Africa are driving innovation and inclusion despite persistent financing and productivity challenges.

Regional Winner | FNB

First National Bank (FNB) takes pride in being the largest bank for small and midsize enterprises (SMEs) in South Africa. The bank’s dominance in the field is rooted in a culture of walking with SMEs along their growth journey.

Last year, FNB’s loan book totaled $6.7 billion, with advances to SMEs accounting for approximately a third. With a formidable 1.3 million SME clients and 34% overall market share, FNB commands strong leadership in most aspects.

Cases in point are asset finance and revolving credit facility arrangements: The bank commands 51% and 42% market share in these, respectively. Growth in the commercial segment, which encompasses SMEs, remains steady, expanding by 6% year-overyear through June 2025.

FNB views its market dominance as a reflection of the real impact it has on SMEs, driven by innovation, digitalization, and a deep understanding of its customers. This is exemplified by some of its solutions, such as grant funding for catalytic projects and patient growth capital, which emphasizes sustained growth over short-term profits with flexible repayment terms.

The bank also prioritizes inclusive finance for Black-owned SMEs, a market that continues to struggle to access finance. For this segment, FNB goes even further to provide both equity and debt funding through its Vumela Enterprise Development Fund, which currently manages $38.9 million in assets.

By addressing structural barriers and enabling scalable growth, FNB ensures that SMEs continue to thrive. The ripple effect is inclusive economic transformation and job creation.

FNB is determined to replicate its home-market success across seven other African countries where it has a presence. Plans are also underway to expand the footprint into new markets, such as Ghana and Kenya.