MILLIONS of households could slash their water bills by up to hundreds of pounds a year.

But many Brits aren’t aware of the discounts they could be entitled to.

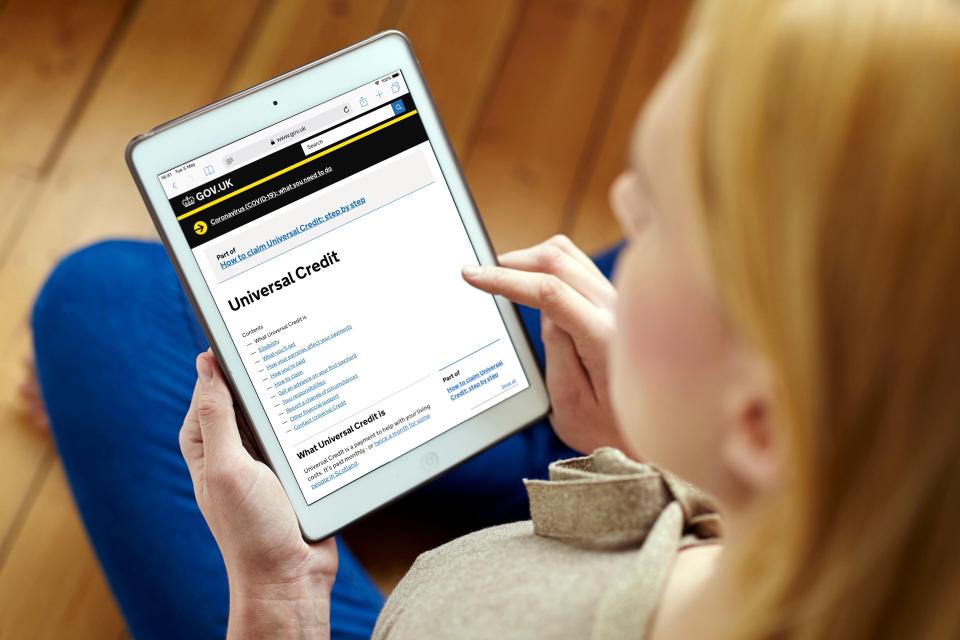

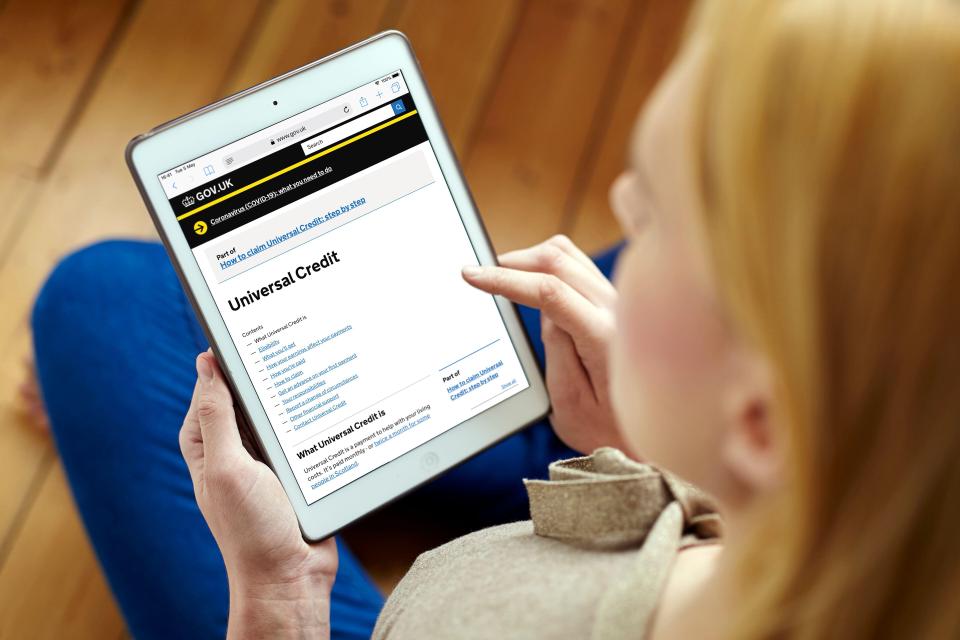

1

Millions of Brits could qualify for help with their billsCredit: Getty

All water companies in England and Wales now offer social tariffs to help lower-income customers.

But because each company sets its own rules, the support varies wildly depending on where you live.

Despite the growing cost of living and rising utility prices, millions of eligible people still aren’t claiming the discounts available.

Last year, consumer watchdog CCW said more than two million households had received help with their water bills, but millions more could be saving and aren’t.

Some of the biggest discounts are available through schemes like WaterHelp, run by Thames Water, which offers a 50% reduction.

The reduction is for households earning under £21,749 a year (not including disability benefits), or where bills account for more than 5% of net income.

There’s alsoWaterSure, a national scheme available to water meter customers on means-tested benefits.

If you have a medical condition that needs extra water or you have three or more children under 19 living at home, you could get your bill capped at the average annual charge.

With Thames Water, for example, that cap is currently £423 a year.

The average annual water and sewerage bill for a Thames Water customer is currently around £864.

Doubling Compensation for Water Issues: Government’s Big Move

So that means if you qualify for WaterHelp, you get 50% off your bill and would therefore save £432 a year.

What’s available at other providers?

Other providers offer even bigger savings.

Southern Water gives customers up to 90% off bills through its Essentials Tariff if they earn under £22,010 and have less than £16,000 in savings.

Wessex Water, South West Water, and Bournemouth Water also offer generous reductions, in some cases 85% or more, depending on your circumstances.

Meanwhile, Anglian Water, Essex & Suffolk Water, and Northumbrian Water offer discounts of up to 50% for households earning less than £23,933 or receiving Pension Credit.

In many cases, discounts kick in if your water bill makes up more than 3% of your income after housing costs.

To find out if you’re eligible, check your supplier’s website or give them a call.

Some schemes ask for proof of income or benefits, while others carry out a short financial assessment.

If you’re unsure who supplies your water, you can find out using this tool.

On top of that, many water firms also offer emergency grants to help with arrears, and free water-saving gadgets like tap aerators and shower timers to help cut your usage.

SANTANDER is slashing interest rates for two of its savings accounts from today – and customers should check if they’re affected.

The major bank is cutting savings rates from June 3 (today) on its Good for Life ISA and Rate for Life accounts.

1

Santander is slashing interest rates for two of its savings accountsCredit: Getty

The interest rate on the Good for Life ISA account will drop from 4.5% to 4.25%, while the rate for the Rate for Life account will drop from 4.75% to 4.5%.

Those who have saved less than £1,000 in the Rate for Life account will still continue to earn the same rate (1%) on these balances.

It comes after the Bank of England (BoE) cut the base rate from 4.5% to 4.25% last month – the fourth cut since 2020.

The base rate is used by banks to determine the interest rates offered to customers on savings and borrowing costs.

Read more on bank accounts

While a rate cut is good news for borrowers, it’s usually bad news for savers, who will usually see savings rates fall when the base rate is cut.

This means they will earn less on their cash.

For example, the average easy access savings rate was 2.78% on May 8, when the base rate was cut.

Now it has dropped to 2.72%, according to comparison site Moneyfacts.

Santander is not the only bank cutting rates on savings accounts. HSBC has also cut rates on eight of its savings accounts today.

Nationwide Building Society cut savings rates on 63 of its accounts on Sunday, from easy-access ISAs to children’s accounts.

Santander’s £130 Million Recovery: What You Need to Know

NatWest cut savings rates on four of its accounts last Friday.

Meanwhile, rates on three of its savings accounts and a kids’ current account will be slashed from July 15.

How to get the best savings rate

As savings rates tumble, now is a good time to check what the interest rate is on your existing account.

Around £280billion is sitting in accounts paying zero interest, according to latest data from the BoE.

If you have an interest rate below the rate of inflation – which is currently 3.5% – then consider moving your money elsewhere, otherwise the spending power of your savings is eaten away.

The best easy access savings rate (based on a balance of £1,000) is offered by Atom Bank at 4.5 per cent.

Experts are predicting that more cuts to the base rate this year are likely, so it may be worth considering locking up your money in a fixed rate savings account if you can afford to do so.

The best one year fixed rate savings account is offered by Hampshire Trust Bank at 4.45%.

However, be aware that you usually can’t make withdrawals out of fixed term savings accounts, even in an emergency.

Anne Bowes from The Private Office said: “Review your savings accounts and switch if you are being paid an uncompetitive rate.

“Double check the terms and conditions of any account you are looking to open – or indeed close – as some accounts may have very short-term bonuses or restricted access.

“That means you might not earn as much interest as you hoped, or get hold of the money in as timely a manner as you were expecting.”

How to switch banks

For customers not happy with the latest shake-up, you may want to consider switching banks.

Switching bank accounts is a simple process and can usually be done through the Current Account Switch Service (CASS).

Dozens of high street banks and building societies are signed up – there’s a full list on CASS’ website.

Under the switching service, swapping banks should take seven working days.

You don’t have to remember to move direct debits across when moving, as this is done for you.

All you have to do is apply for the new account you want, and the new bank will tell your existing one you’re moving.

There are a few things you can do before switching though, including choosing your switch date and transferring any old bank statements to your new account.

You should get in touch with your existing bank for any old statements.

When switching current accounts, consider what other perks might come with joining a specific bank or building society.

Some banks offer 0% overdrafts up to a certain limit, and others might offer better rates on savings accounts.

And some banks offer free travel or mobile phone insurance with their current accounts – but these accounts might come with a monthly fee.

Where to find the best savings rates

Many savings accounts offer miserly rates meaning that money is generating little or no return.

However, there are ways to get your cash working hard. Sun Savers Editor Lana Clements explains how to make sure you money is getting the best interest rate.

Easy access savings accounts offer flexibility for customers, meaning they can dip in and out of cash when needed. However, the caveat is that rates can change at any time.

If you’re keeping your money in an easy access account, you’ll need to keep checking whether it’s the best paying account for your circumstances and move if not.

Check in at least once a month to see what is happening in the market.

Check what is offered by your bank – sometimes the best rates are for customers only.

But do search the wider market as often top savings accounts are offered by lesser known providers.

Comparison sites are a good place to check for the top rates. Try Moneyfactscompare.co.uk or Moneysupermarket.

You can search by different account type. You’ll usually get a better interest rate if you can lock your money away for a fixed amount of time, but it’s always a good idea to keep some money in an easy access account in case of emergencies.

Don’t overlook regular savings accounts often pay some of the best rates, but you’ll need to commit to monthly payments. This can be a great way to get into a savings habit while earning top rates at the same time.

DRIVERS looking to buy an affordable but reliable older motor should consider one of these top 10 picks from the Which? annual car survey.

The consumer group has revealed a list of cars it recommends with five-star reliability ratings between 10-15 years old, some for less than £3,000.

From nippy city cars to big family SUVs, there are options for all drivers hunting for a bargain buy that doesn’t scrimp on quality.

Michael Passingham, senior researcher at Which?, told thisismoney that hybrid cars have come to dominate the list of most reliable, older vehicles.

He said: “Why do these cars perform so well? One reason could be that the hardest part of a car’s life – starting and pulling away – are mostly handled by the small electric motor.

“These motors have fewer moving parts than combustion engines and, along with sturdy main battery packs, really don’t have to work all that hard.

“The downside is that our data shows a much higher failure rate of the 12V battery (the small battery all cars have) on full hybrids; this component is worked hard so it pays to buy a quality one and get it replaced every five years or so.”

In good news for consumers, so called ‘full’ hybrids’ have been removed from the 2030 ban on sales of new petrol and diesel cars planned by the government.

Micheal warned against opting for a plug-in hybrid, saying that this type of car has “one of the least reliable engine types according to our data”.

Here is the full list of the 10 best buys for the most reliable older cars…

10. Toyota Auris (2012-2019)

Average used price: £4,650

10

The Toyota Auris is a great option for those wanting a green car that boasts impressive reliability especially for the priceCredit: Alamy

Faults: 28% Breakdowns: 7% Days off the road: 5.3

The predecessor to the Toyota Corolla, the Auris served as the brands family hatchback offering for almost two decades until it was replaced in 2019.

The second generation Auris, sold between 2012-2019, boasts impressive reliability with less than three in ten owners reporting faults in the last year, and only seven per cent saying their vehicle broke down.

The average price of £4,650 makes this a competitive option when looking for a family, and environment, friendly hatchback.

The only caveat is that the Auris took an average of 5.3 days to get back on the road after a breakdown, which is higher than other cars on this list.

Princess Andre hits back at money-shaming trolls who claim ‘Peter and Katie Price bought her £10k motor as first car’

9. Suzuki Alto (2009-2014)

Average used price: £2,800

10

The Suzuki Alto is a small city-friendly car that is simple enough to get repaired cheaply and get back on the road quicklyCredit: Alamy

Faults: 25% Breakdowns: 1% Days off the road: 2.6

The Suzuki Alto, released in 2009, is still living up to its promise of being a cheap, compact and reliable supermini.

It was first offered for £6,000-£7,000 and now can be snapped up for less than three grand, the cheapest buy on this list.

The simplicity of the Alto makes it a particularly reliable option, with just 1 per cent reporting breakdowns in the last 12 months, and a quarter saying they had to deal with faults.

If it does need a repair, the Alto’s simplicity means it gets back to you in an average of only 2.6 days.

8. Toyota Yaris (2011-2020)

Average used price: £3,100

10

The Toyota Yaris has a great track record of reliability, making it one of the most popular hatchbacks of the last 25 yearsCredit: Handout

Faults: 23% Breakdowns: 6% Days off the road: 3.1

The go-to small, dependable car for many in the last 25 years, the Yaris, is still making recommendation lists for its affordability and reliability.

With less than a quarter reporting faults and only 6 per cent dealing with a breakdown in the last 12 months, the Yaris still holds up remarkably well after all this time.

This is the 2011-2020 model with a hybrid drivetrain, an addition which makes it economical to drive as well as to buy, averaging just over £3,000.

7. Suzuki Swift (2010-2016)

Average used price: £3,500

10

Suzuki Swift is considered by some an overlooked gem of the supermini classCredit: Getty

Faults: 27% Breakdowns: 8% Days off the road: 1.4

Suzuki appears again on this list with the 2010-2016 Swift supermini, a compact, simple vehicle at a compelling price.

Received positively upon release, the Swift was praised for being fun to drive with a competitive blend of efficiency and performance.

Now on sale for only around three and a half grand, this might be a great option for those looking for a small but fiery little motor.

Although it scores a little worse on breakdowns, with 8 per cent being the highest on this list, it does only spend a brief 1.4 days in the shop when things do go wrong.

Couple this with a good score of 27 per cent reporting faults, and this characterful car is still a good buy in 2025.

6. BMW X1 (2009-2015)

Average used price: £5,200

10

The BMW X1 is surprisingly reliable for a big luxury SUVCredit: handout

Faults: 35% Breakdowns: 7% Days off the road: 2.1

In a shock entry to this list, the BMW X1 is an outlier for luxury SUVs, which are often unreliable and costly to repair.

On the contrary, the X1 competes with other, much smaller, simpler cars with a respectable record of just 7 per cent reporting breakdowns last year and only 2.1 days taken to fix on average.

Consumers may be able to take advantage of typically low SUV resale prices, generally due to reliability and repair cost concerns, to pick up this hidden gem for a very reasonable price of around £5,000.

That said, the X1 does rank low on this list in terms of faults, with over a third experiencing issues in the last 12 months.

5. Skoda CitiGo (2009-2019)

Average used price: £4,500

10

The Skoda Citigo is mechanically identical to the popular VW Up! making it a great choice for a small car on a budget that also boasts good reliabilityCredit: Getty

Faults: 22% Breakdowns: 5% Days off the road: 2.8

Mechanically identical to the VW Up!, the Skoda CitiGo was meant for squeezing into tight parking spaces and down narrow streets while keeping your fuel costs and insurance premiums to a minimum.

After being discontinued five years ago, the CitiGo now makes for a tempting prospect on the second-hand market.

It was initially praised for being surprisingly roomy for being so small, and for being the cheaper alternative to the Up! while essentially being the same car.

It boasts impressive reliability, with only 22 per cent reporting faults and 5 per cent experiencing a break down.

The CitiGo is fairly quick to repair as well, only spending 2.8 days at the garage before being ready for more.

4. Honda Jazz (2008-2015)

Average used price: £3,800

10

The Honda Jazz is popular among older drivers, but this doesn’t mean it’s not a great option for a convenient and reliable motorCredit: handout

Faults: 25% Breakdowns: 4% Days off the road: 2.7

Almost exclusively driven by those of a certain age, the Honda Jazz is popular amongst the older demographic for a reason: its convenient, reliable and easy to drive.

These attributes might get Grandma excited, but they should also make the Jazz an attractive option for anyone looking for a solid vehicle at a bargain price.

One in four owners reported a fault with their cars and the average time in the garage was 2.7 days being fixed by mechanics.

Your Jazz shouldn’t be seeing the inside of a garage too often though, with only 4 per cent breaking down in the last year.

3. Lexus RX 450h (2009-2015)

Average used price: £6,400

10

The Lexus RX 450h is a very reliable option for a big family motor, breakdowns are very rare according to Which?Credit: Handout

Faults: 16% Breakdowns: 0% Days off the road: 2

This chunky SUV was voted the most satisfying car to own in 2024 in a Which? survey.

A glance at the cars record quickly confirms that one of the factors that make it so popular must be its excellent reliability.

Looking at the hybrid-powered models here, only 16 per cent reported a fault in the last year and none had their RX break down on them.

For the times that the RX was sent into the garage, it only spent 2 days on average being worked on.

The price is a little higher than some others on this list, but buyers are getting both space, comfort and relatively good fuel efficiency.

2. Mazda MX-5 (2005-2015)

Average used price: £3,800

10

The Mazda MX5 Roadster Coupe is a British icon, and could be yours for less than £4,000 if you opt for an older modelCredit: Getty

Faults: 26% Breakdowns: 0% Days off the road: 1.7

The iconic MX-5 speeds into the number two spot for good reason, bucking the trend of unreliable sports car to still deliver thrilling driving with solid build quality at a good price.

Hailing originally from the late 1980’s, this example of the world’s best selling roadster is the third generation MX-5, it debuted in 2005 and still holds up today.

The record from Which?’s data is flawless when it comes to breakdowns, and shows that this classic is quick to fix only spending 1.7 days in the shop.

Just over a quarter reported faults, but that’s not a huge figure when it comes to second-hand sports cars.

1. Lexus CT 200h (2011-2020)

Average used price: £7,300

10

The Lexus CT 200h is the number one car according to the Which? car survey for reliabilityCredit: PR handout

Faults: 13% Breakdowns: 0% Days off the road: 1.2

Topping the list as the most reliable 10 to 15 year-old car comes the Lexus CT 200h, a full hybrid hatchback which served as the brands answer to the Ford Focus and VW Golf until 2020.

CT 200h owners surveyed by Which? delivered glowing reviews, reporting zero breakdowns and only 13 per cent experiencing a fault with their car.

Drivers praised the vehicles comfort and, of course, reliability, only pointing to a small boot and clunky infotainment system as critiques, as reported by thisismoney.

The car sells for around £7,000, the priciest offering so far, but its near spotless record should mean your investment pays off with a dependable motor that is good for years to come.

The ones to steer clear of

Which? puts the diesel powered Vauxhall Zafira (2005-2014) and Nissan Qashqai (2007-20013) as two of the least reliable vehicles that consumers should steer well clear of if dependability is their aim.

The Zafira has become known for catching fires in recent years due to issues with its heater blower motor and regulator. This usually happens when owners replace parts with cheaper, aftermarket components.

It is hardly a wonder that drivers are turning to cut-price alternatives when the Zafira breaks down on three in ten owners, with more than half reporting faults in the last year.

The car also takes a whopping 14 days on average for repairs to be made.

The first generation Nissan Qashqai also from suffers reliability issues, and needs almost a week in the garage on average before it is road-ready after a malfunction.

Both these cars use diesel fuel, and Which? has found that this is by far the worst fuel type for reliability, with an average fault rate of 48 per cent, compared to 39 per cent for petrol and 23 per cent for hybrids.

She showed that the coupons include a free Lidl tote bag, a bakery item, and fresh fruit.

Chloe said: “So go to Lidl and get a pastry and some fruit, or you could even get stuff to make avocado on toast. There’s loads of options.”

She added: “You’ve got a free breakfast and a bag to carry it home in.”

In the caption section, Chloe also explained that there’s “no minimum spend so you can get these freebies without buying anything else.”

Five Lidl rosés you need this summer, according to a wine expert – a £6.99 buy is as light & crispy as £22 Whispering Angel

The video received 78.5 views and 74 comments after four days of being shared on her account.

Many wanted to share their excitement after hearing the news.

One wrote: “Got mine. Thank you for sharing.”

A second added: “Free strawberries! I’m going to get everyone in my house to download it!”

Whilst a third said: “It’s true, I had also downloaded the Lidl app, from which I also got this shopping bag, muffins and many other things.”

4

There are specific steps to take when downloading the app

Why do Aldi and Lidl have such fast checkouts

IF you’ve ever shopped in Aldi or Lidl then you’ll probably have experienced its ultra-fast checkout staff.

Aldi’s speedy reputation is no mistake, in fact, the supermarket claims that its tills are 40 per cent quicker than rivals.

It’s all part of Aldi’s plan to be as efficient as possible – and this, the budget shop claims, helps keep costs low for shoppers.

Efficient barcodes on packaging means staff are able to scan items as quickly as possible, with the majority of products having multiple barcodes to speed up the process.

It also uses “shelf-ready” packaging which keeps costs low when it comes to replenishing stock.

IF your child’s birthday is coming up and the thought of splashing the cash on a lavish cake sends shivers down your spine, fear not, you’ve come to the right place.

A mother has revealed that rather than forking out hundreds of pounds for a personalised cake for her daughter’s birthday, she DIY-ed a supermarket buyCredit: TikTok/@mummyandmylaa

3

For less than £20, Amy was able to celebrate her child’s birthday in styleCredit: TikTok/@mummyandmylaa

3

Amy nabbed the Pretty in Pink Lambeth Cake from WaitroseCredit: Waitrose

But in a bid to save cash, one savvy mum took matters into her own hands and was able to cut costs by DIY-ing her little darling’s birthday dessert.

Posting on social media, a mother named Amy shared a step-by-step tutorial of how she DIY-ed her daughter Myla’s pink birthday cake – and it cost her less than £20.

So if you’re on a budget and your purse is feeling tighter than ever before, then you’ll need to listen up.

The pink coloured golden sponge cake, which is filled with raspberry jam and topped and decorated with pale pink and dark pink buttercream, cost Amy just £18.

Then, using some pink icing and ribbons she already had, she was able to personalise the cake – and we think it looks incredibly professional.

Alongside a short clip shared online, the influencer penned: “Making my daughter’s first birthday cake, saving £100s!”

Showing off the box-fresh vintage-style cake, which is decorated with whirls and swirls of piping, Amy beamed: “Come with me to DIY my daughter’s first birthday cake for only £18!”

Amy confirmed that she used letter cutters to cut out “Myla is one” in pink icing, which she placed on top of the cake.

Following this, she attached pretty pink bows, which she already had from Shein, and was able to stick these to the cake with cocktail sticks.

The simple chocolate cake recipe using only TWO ingredients – it’s sweet and you won’t even need to put it in the oven

We think Amy’s DIY cake looks brilliant and is a great way for those strapped for cash to save money, without having to scrimp on the celebrations.

The TikTok clip, which was posted under the username @mummyandmylaa, has clearly left many open-mouthed, as it has quickly racked up 178,600 views.

Not only this, but it’s also amassed 2,782 likes, 31 comments and 780 saves.

Social media users were impressed with the jaw-dropping cake and many eagerly raced to the comments to express this.

Time-saving mum hacks

Morning Routine

Nighttime Preparation: Set out clothes for yourself and the kids, pack lunches, and organise backpacks before bed.

Effortless Breakfasts: Keep simple, healthy breakfast options on hand, such as overnight oats, smoothie packs, or pre-made breakfast burritos.

Meal Planning

Weekly Meal Prep: Dedicate time each week to plan your meals to eliminate daily decision-making.

Bulk Cooking: Prepare larger quantities and freeze portions for future use.

Hands-Off Cooking: Make use of slow cookers or Instant Pots for easy, unattended meal prep.

Ready-to-Use Veggies: Purchase pre-chopped vegetables or chop them all at once to save time during the week.

Household Chores

Daily Laundry: Do a load of laundry every day to prevent a buildup of dirty clothes.

Continuous Cleaning: Encourage kids to clean up after themselves and perform small cleaning tasks throughout the day.

Efficient Multitasking: Fold laundry while watching TV or listen to audiobooks/podcasts while cleaning.

Organisation

Family Command Centre: Set up a central hub with a calendar, to-do lists, and important documents.

Daily Decluttering: Spend a few minutes each day decluttering to maintain an organised home.

Organised Storage: Use bins and baskets to keep items neat and easy to locate.

Kid Management

Prepared Activity Bags: Have bags packed with essentials for various activities (e.g., swimming, sports).

Routine Visuals: Implement visual charts to help kids follow their routines independently.

Task Delegation: Assign age-appropriate chores to children to foster responsibility and reduce your workload.

One person said: “Love that. Wish I hadn’t already ordered a cake almost the exact same.”

Another added: “This is genius!”

A third commented: “Super cute!”

Not only this, but another parent beamed: “Omg that cake is adorable, I wish I knew about it before!”

This is genius!

TikTok user

At the same time, one user wondered: “What it nice? I worry that supermarket cakes can be dry inside as they are sat on the aisle for a while.”

To this, the content creator replied and confirmed: “Not dry at all!!!

“Honestly, it tasted AMAZING, no regrets!!!”

Unlock even more award-winning articles as The Sun launches brand new membership programme – Sun Club

HAVING family over soon but stuck for ideas as well as cash?

You could jazz up dishes, for added wow factor, just by using leftover uncooked veg to knock up some pickle or relish. Here’s some ideas . . .

RECYCLE OLD JARS: You will need jars to put your pickle or relish in, and could get a 12-pack of 300ml ones at Hobbycraft for £9, but the cheapest way to get started is to reuse empty jam or sauce jars.

Give them a good wash, or pop in the dishwasher then use boiling water to rinse.

TANGY TREAT: Pickled red onions are easy. Finely slice the onion, pop in a jar, cover with white wine vinegar, £2 at Sainsbury’s, and add a pinch of salt and of sugar.

Put the lid on and shake, leave for 20 minutes before trying — adding more vinegar, salt or sugar as you think best.

Pop in the fridge and use on everything from tacos to sarnies.

SPICE OF LIFE: Slice up any spare chilli peppers and pop in a jar.

Then put 100ml of water in a pan and heat on the stove with a few teaspoons of sugar and one of salt, plus you could add mustard seeds or bay leaves from your spice rack. Bring to the boil then pour the liquid into the jar.

Carefully put the lid on the jar and leave to cool. Once at room temperature, store in the fridge and the chillis should keep for a few months.

CRUNCHY RELISH: Use up any mini- cucumbers or radishes to make a tasty relish.

Slice your veg and keep it crunchy by adding to a sieve with ice cubes for ten to 20 minutes before pickling.

I’ve figured out how to make the perfect fried eggs – it’s so simple, works every time and you don’t even need any oil

Make a brine following the same instructions as before, leave to cool and add to the jar with your veg.

You can also add onion, and herbs such as dill, for extra flavour.

PASS THE CARROTS: The key for great pickled carrots is to cut them up into very fine matchsticks or use a peeler to create shavings.

Follow the same brine instructions as above, but add some rice wine vinegar if you have it, as well as a dash of fish sauce.

Once cooled and refrigerated, you can use these on Asian dishes such as dumplings or stir fries.

All prices on page correct at time of going to press. Deals and offers subject to availability.

8

Combine leftover vegetables and empty jars for easy storageCredit: Getty

Deal of the day

8

This Graco Myavo Stroller is currently reduced to £99.99Credit: Supplied

PICK up the Graco Myavo Stroller in midnight black at smythstoys.com – usually £124.99, now £99.99 as part of the baby goods sale.

SAVE: £25

Cheap treat

8

Iceland is selling Curry pot noodles at a 53p discountCredit: Supplied

TUCK into a Curry Pot Noodle from Iceland. They were £1.20 each, now down to 67p.

SAVE: 53p

What’s new

8

Pandora currently has a 40 per cent sale, making it the ideal time to buy a giftCredit: Supplied

CHARM your way into a loved one’s heart with a gift from Pandora.

The summer sale is now on, with up to 40 per cent off the popular charms and jewellery.

Top swap

8

The Diorshow brow styler costs £24.95Credit: Supplied

8

The budget e.l.f. Instant Lift brow pencil is just £3 at BootsCredit: Supplied

GIVE brows a makeover using the Diorshow brow styler, above, £24.95, or try the budget e.l.f. Instant Lift brow pencil, below, £3, both Boots.

SAVE: £21.95

Little helper

PLANNING a BBQ?

Co-op members can get two meat packs for £5.50 (£6.50 non-members).

Minted lamb kebabs are usually £4.70, so it’s a £3.90 saving with the deal.

Shop and save

8

Dunelm has a discount on this stylish storage trunkCredit: Supplied

HIDE clutter in a stylish storage trunk. This Remy basket was £25 and is now down to £20 at Dunelm.

SAVE: £5

Hot right now

STOCK up on your favourite beers at Morrisons with an offer of three packs for £30, saving around £9.

Includes ten-packs of Estrella and Doom Bar.

PLAY NOW TO WIN £200

8

Join thousands of readers taking part in The Sun Raffle

JOIN thousands of readers taking part in The Sun Raffle.

Every month we’re giving away £100 to 250 lucky readers – whether you’re saving up or just in need of some extra cash, The Sun could have you covered.

Every Sun Savers code entered equals one Raffle ticket.

The more codes you enter, the more tickets you’ll earn and the more chance you will have of winning!

AS KING Canute found over a thousand years ago, it is quite difficult to stand on a beach and order the tide to recede.

Today, it is equally difficult to make the argument that giving families cash is not always the best way of lifting them out of poverty.

2

David Blunkett grew up on just bread and dropping at home – but he is warning that lifting the 2 child benefit cap is not the best way to tackle povertyCredit: Alamy

This is especially true when one particular measure becomes the symbol of whether or not you’re on the right side of the debate about child poverty.

But as someone who now can afford the comforts of life, I constantly remind myself of my childhood.

The grinding poverty that I experienced when my father was killed in a work accident when I was 12 – leaving my mother, who had serious health problems, to fight a long battle for minimal compensation.

Having only bread and dripping in the house was, by anyone’s standards, a hallmark of absolute poverty.

Why on earth would I question, therefore, the morality of reversing a Tory policy introduced eight years ago?

This restricts the additional supplement to universal credit – worth over £3,000 a child per year – to just two children.

I should know, my friends tell me, that the easiest and quickest way of overcoming the growth in child poverty is to restore the £3.5 billion pounds it would cost to give this additional money for all the children in every family entitled to the credit.

It is true that the policy, introduced in 2017, failed its first test.

Women did not stop having more than two children even when they were strapped for cash. It is still unclear why.

After all, many people have to make a calculation as to how many children they can afford.

2

Keir Starmer is under massive pressure form Labour backbench MPs to lift the 2 child benefit cap and go on a new welfare spending spreeCredit: AP

But one thing must be certain: namely, that if you give parents a relatively substantial additional amount of money for every child they have whilst entitled to benefits, they are likely to have more children.

Nigel Farage, leader of Reform UK, said as much last week. His argument for restoring the benefit to the third and subsequent children was precisely that we needed to persuade low- income families to have more children.

Surely having children that you cannot afford to feed is the legacy of a bygone era?

All those earning below £60,000 are entitled to the basic child benefit, so the argument is about just over £60 a week extra per child.

One difficulty in having a sensible debate about what really works in overcoming intergenerational poverty is the lack of reliable statistics.

Some people have claimed, over recent days, that over 50 per cent of children in Manchester and Birmingham live in poverty.

I fear that such claims should be treated with scepticism.

Those struggling to make ends meet – sometimes having not just one but two jobs – who pay their taxes and national insurance and plan their lives around what can be afforded, have the right to question where their hard-earned wages go.

The simple and obvious truth is that child poverty springs from the lack of income of the adults who care for them.

Transforming their lives impacts directly on the children in their family.

There is a limit to how much money taxpayers are willing to hand over to pay for another family’s children.

Helping them to help themselves is a different matter.

So, what would I do?

Firstly, I would ensure that families with a disabled youngster automatically have the entitlement restored.

This would self-evidently apply also to multiple births.

In both cases, life is not only more difficult, it is also harder to get and keep a job.

I would come down like a ton of bricks on absent parents.

My mum was a single parent because she was widowed; many others are single in the sense that the other partner has walked away.

The Child Maintenance Service should step up efforts to identify and pursue absent parents who do not pay their fair share towards their child.

We, the community, have a clear duty to support and assist those in need.

To help those where a helping hand will restore them to independence and self-reliance.

But there is an obligation on individuals as well as the State, and mutual help starts with individuals taking some responsibility for themselves.

Finally, if (and this is where I am in full agreement with colleagues campaigning to dramatically reduce child poverty) we make substantial sums of money available to overcome hardship, then a comprehensive approach to supporting the families must surely be the best way to achieve this.

As ever in politics there is a trade off. What you spend on handing over cash is not available to invest in public services: that is the reality.

Help from the moment a child is born, not just with childcare but with nurturing and child development.

Dedicated backing to gain skills and employment and to taper the withdrawal of help so that it genuinely becomes worthwhile having and keeping a job.

A contract between the taxpayer and the individual or household. Government is about difficult choices, that is why Keir Starmer and his colleagues are agonising over what to do next.

Angela Rayner says lifting 2-child benefit cap not ‘silver bullet’ for ending poverty after demanding cuts for millions

THOUSANDS of struggling households are eligible for free cash worth £100 to cover the cost of living.

The help comes via the Household Support Fund, a £742million pot of money that has been shared between English councils.

1

Households in Hartlepool are eligible for free money via the Household Support FundCredit: Getty

Local authorities then have to decide how to distribute their share of the fund before March 31, 2026.

Hartlepool Borough Council has been given £1.75million to share between hard-up households.

The local authority is giving £40,000 to Hartlepool Food Bank to distribute food parcels across the borough and £90,000 to Citizens Advice to help residents struggling with their energybills.

But, it is also distributing £100 food vouchers to all children eligible for free school meals aged between two and 19.

Meanwhile, £100 bank payments or food vouchers will be shared between pensioners on council tax support.

Details on how either of the £100 payments will be distributed are yet to be revealed.

However, if you meet the criteria, you will likely be contacted by Hartlepool Council about when to expect them or any nextsteps.

We have also contacted Hartlepool Council to find out when families with children on free school meals and eligible pensioners will receive the payments and will update this story when we have heard back.

Councillor Brenda Harrison, leader of Hartlepool Borough Council, said: “We know that a lot of households across the borough are struggling financially, and we hope that these measures will help to bring them some much-needed relief and ease the pressure they are currently under.

“This demonstrates the Council’s on-going commitment and determination to tackle financial hardship and to improve the lives of Hartlepool residents.”

Three key benefits that YOU could be missing out on, and one even gives you a free TV Licence

Can I get help if I live outside Hartlepool?

Put simply, yes. However, it will depend on your circumstances and where you live.

The Household Support Fund was set up to help households cover essentials such as energy or water bills and food costs.

But, each council can set its own eligibility criteria meaning whether you qualify for help is a postcode lottery.

That said, funding is aimed at anyone who’s vulnerable or struggling to pay for essentials.

So, if you are financially hard-up or on benefits, it is likely you will be able to get help.

It’s worth bearing in mind, any help you receive via the Household Support Fund won’t affect your benefit payments.

The type of help on offer varies from supermarket vouchers to direct cash payments into your bank account.

Some councils are allocating their share of the fund to community groups and charities who you have to get in touch with.

Household Support Fund explained

Sun Savers Editor Lana Clements explains what you need to know about the Household Support Fund.

If you’re battling to afford energy and water bills, food or other essential items and services, the Household Support Fund can act as a vital lifeline.

The financial support is a little-known way for struggling families to get extra help with the cost of living.

Every council in England has been given a share of £742million cash by the government to distribute to local low income households.

Each local authority chooses how to pass on the support. Some offer vouchers whereas others give direct cash payments.

In many instances, the value of support is worth hundreds of pounds to individual families.

Just as the support varies between councils, so does the criteria for qualifying.

Many councils offer the help to households on selected benefits or they may base help on the level of household income.

The key is to get in touch with your local authority to see exactly what support is on offer.

The current round runs until the end of March 2026.

If you’re on benefits, have limited savings, or are struggling to cover food and energy bills, it’s worth seeing if you’re eligible for help.

Contact your local council and see if you have to apply or whether support is being distributed automatically.

You can find what council area you fall under by using the government’s council locator tool – www.gov.uk/find-local-council.

Other help if you’re on a low income

It’s not just the Household Support Fund you can lean on if you’re struggling to cover the cost of essentials like energy bills or food.

You might be able to get free money covering the cost of food if you’re on benefits through the Healthy Start scheme.

The scheme is open to pregnant women and families with young children on low incomes.

You get a prepaid card which you top up and can use to buy healthy foods for your kids at the supermarket.

You can get £8.50 per week for newborns up to one-year-olds – worth £442 a year. Find out more via healthystart.nhs.uk.

Meanwhile, several energy firms offer grants to households who are struggling to pay their energy bills worth up to £2,000.

It’s also worth checking if you’re eligible for benefits if you haven’t already – billions of pounds worth is going unclaimed, according to Policy in Practice.

You can use one of the below calculators to find out if you could be eligible for help:

Do you have a money problem that needs sorting? Get in touch by emailing [email protected].

The base rate is the rate charged by the BoE to smaller high street banks on loans, with any fall usually mirrored in savings rates.

Newcastle Building Society is reducing rates on the 37 personal savings accounts by 0.25 percentage points.

The Double Access Saver/ISA (Issue 4) will drop from 4.05% to 3.80%, for customers eligible for a bonus interest rate.

Meanwhile, the Newcastle Cash Lifetime ISA (Issue 3) will fall from 2.70% to 2.45%.

The Newcastle Junior Cash ISA will be cut from 3.75% to 3.50% and the Regular Saver Plus from 2.50% to 2.25% for anyone receiving the bonus interest rate.

Customers with fixed-rate savings accounts won’t see interest rates fall from June 5.

Interest rates on two variable rate savings accounts – the Loyalty Saver (Issue 1) and Quadruple Access Saver/ISA (Issue 1) – will also not change as they have only been available to customers since April 24.

You can view the table above to find out how the interest rate on your savings account has changed.

Or, you can visit www.newcastle.co.uk/savings/manage-your-savings-account/interest-rates and click on “Current and Closed Issue Variable Savings Interest Rates”.

What is the Bank of England base rate and how does it affect me?

The Sun asked Newcastle Building Society to comment.

MAJOR BANKS CUTTING RATES

A host of banks are reducing interest rates on savings accounts as the BoE continues to cut its base rate.

It comes after the BoE cut its base rate from 4.50% to 4.25% on May 8.

The central bank raises its base rate to discourage people from spending and encourage them to save, which in turn is designed to make inflation fall.

It lowers its base rate when inflation is under control, meaning people are encouraged to spend and pump money into the economy.

A lower base rate signals good news for those with mortgages who see the interest rates charged on them fall.

However, it’s usually bad news for those with savings accounts as banks slash interest rates.

If you’ve got a savings account with an interest rate set to drop, it might be worth shopping around for a better deal now.

Check out comparison sites like moneysavingexpert.com and moneyfactscompare.co.uk to browse the best out there.

According to Moneyfacts, Chip is offering the best rate on an easy access savings account, with a rate of 4.77%.

Meanwhile, the best easy access cash ISA is also with Chip and offering a rate of 4.99%.

Always look beyond just the headline interest rate on any savings account though.

Some offer additional perks which can make them more cost-effective and suited to you, based on your circumstances.

For example, some offer you access to free TV subscriptions or cheaper or free cinema tickets.

Different types of accounts pay out interest at different times too while others will offer a bonus interest rate which falls after a set period.

Some savings accounts penalise you for making withdrawals over a certain limit.

Meanwhile, ISAs can be effective for saving cash as any interest earned on them is tax-free.

Read more below about the different types of savings accounts and what they offer.

SAVING ACCOUNT TYPES

THERE are four types of savings accounts fixed, notice, easy access, and regular savers.

Separately, there are ISAs or individual savings accounts which allow individuals to save up to £20,000 a year tax-free.

But we’ve rounded up the main types of conventional savings accounts below.

FIXED-RATE

A fixed-rate savings account or fixed-rate bond offers some of the highest interest rates but comes at the cost of being unable to withdraw your cash within the agreed term.

This means that your money is locked in, so even if interest rates increase you are unable to move your money and switch to a better account.

Some providers give the option to withdraw, but it comes with a hefty fee.

NOTICE

Notice accounts offer slightly lower rates in exchange for more flexibility when accessing your cash.

These accounts don’t lock your cash away for as long as a typical fixed bond account.

You’ll need to give advance notice to your bank – up to 180 days in some cases – before you can make a withdrawal or you’ll lose the interest.

EASY-ACCESS

An easy-access account does what it says on the tin and usually allows unlimited cash withdrawals.

These accounts tend to offer lower returns, but they are a good option if you want the freedom to move your money without being charged a penalty fee.

REGULAR SAVER

These accounts pay some of the best returns as long as you pay in a set amount each month.

You’ll usually need to hold a current account with providers to access the best rates.

However, if you have a lot of money to save, these accounts often come with monthly deposit limits.

Do you have a money problem that needs sorting? Get in touch by emailing [email protected].

I PUSHED the order button on my phone and then 10 minutes later my groceries were at my door.

I often find I’m missing an ingredient for a recipe and with two kids at home it’s easier to get the items delivered.

5

Trial of supermarket deliveries with Lana Clements, photographed by Oliver Dixon for Sun Features – 12 May 2025.Photo shows Sainsburys and COOPCredit: Oliver Dixon

But how much extra am I paying?

Sun Savers Editor Lana Clements puts 60-minute delivery services to the test.

Selecting the cheapest, pint of semi-skimmed milk, six-pack of eggs, punnet of strawberries, three-pack of Solero ice creams, loaf of white bread and two-pack of burgers.

TESCO WHOOSH

MIN SPEND: No minimum spend but baskets under £15 incur an extra £2 charge.

BASKET COST: £16.55

FEES: £2.99

TOTAL COST: £19.54

5

My order arrived in 12 minutes, which was pretty speedyCredit: Oliver Dixon

Tesco claims deliveries come in 20 minutes to 70 per cent of the UK from 1,500 stores.

The choice of products was good and I was able to order everything I needed and keep costs relatively low.

For example, I was offered three different packs of strawberries to choose from.

This means the basket cost was lower than rival Tesco, however, the fees were more than £2 higher and included a carrier bag fee making it more expensive overall.

The order came exactly 10 minutes after placing it making it the fastest in the test.

And I can’t complain about the food which was all in great condition.

You can also order Sainsbury’s through Uber Eats and Deliveroo but you can earn Nectar points when ordering through Chop Chop.

This was the quickest delivery and there was a great choice of food but the fee was at the higher end of the scale.

RATING: 4/5

MORRISONS VIA AMAZON

MIN SPEND: £15 for Amazon Prime members, £40 for non-members

BASKET COST: £15.48 ( plus the extra sausages)

FEES: Orders over £60 are free for Prime members, £2 for between £40 and £60, and £4 under £40. For non-members, fees are £3 for orders over £60 and £5 between £40 and £60.

TOTAL COST: £19.48

Same-day deliveries within two-hour timeslots.

When I logged on at 9.30am in the morning, I had the choice of three slots available with the earliest being 2-4pm, the next 4-6pm and then 6-8pm.

I picked the later slot to make sure I didn’t miss the delivery while on the school run.

The choice of products was fantastic and the cheapest prices.

I needed to meet a minimum spend of £15, as I’m an Amazon Prime member. I added on a pack of sausages to bring the total order up to £15.48.

By 8pm nothing had arrived.

Then at 8.09pm I received a text message to say the order had been cancelled and that I would be refunded.

There was no reason given for the cancellation.

Luckily we didn’t go hungry as the other orders were arriving – but I was not impressed.

The fees and minimum spends are offputting too.

RATING: 0/5

WAITROSE VIA UBER EATS

MIN SPEND: No min spend over £15, but under £15 it’s £3.

BASKET COST: £13.11 (after discounts)

FEES: £3.93 Made of three parts: *Service fee (10% of your subtotal capped at £2.99) £1.64 for my order *Delivery fee (depends on variables including location and availability of drivers) £1.79 for my order. *Bag fee (depends on retailer) 50p for my order

TOTAL COST: £17.64

5

The selection from Waitrose was great and my order arrived within 26 minutes.Credit: Oliver Dixon

On Uber Eats I can get Sainsbury’s and Co-op delivered as well as Waitrose.

The selection from Waitrose was great and my order arrived within 26 minutes.

I also got 50 per cent off selected fruit and veg as there was an offer running, which knocked off £2.69 off my total bill.

The fees seem excessive as you’re charged for service, delivery and bags separately.

My order was also split into two bags, pushing up the cost.

Good choice of food and it arrived in reasonable time and condition.

RATING 3/5

CO-OP VIA DELIVEROO

MIN SPEND: No min spend

BASKET COST: £13.55 (no eggs) changed to £8.10 after substitutions (no eggs, no strawberries)

The order arrived in a reasonable 17 minutesCredit: Oliver Dixon

Through Deliveroo I can get Waitrose and Sainsbury’s delivered but I tested Co-Op.

Unfortunately, it was not long after the supermarket suffered from cyber attacks impacting its stock levels and product availability.

However, I was still able to order burgers, milk, bread and ice lollies – and raspberries instead of strawberries. But there were no eggs at all.

The original order total came to £15.50.

However, the raspberries were out of stock when it came to packing and my one pint of milk was changed to a two-pint carton, while the lollies were changed to Co-Op own brand.

The order arrived in a reasonable 17 minutes.

Unlike all the other deliveries, my Co-Op shopping arrived in a green compostable bag.

This didn’t seem to offer the food as much protection as the brown paper bags from the other supermarkets.

As a result, I wasn’t too happy with my loaf of bread which arrived seriously squished.

Fees are split in a similar way to Uber Eats and made up of three parts.

The order arrived in good time but I wasn’t happy with my squashed bread and the choice also let down the experience but this seemed like bad timing.

RATING: 2/5

OTHER SUPERMARKETS

Asda and Ocado both offer speedy grocery deliveries.

Asda offers between an hour and four hours from 330 stores.

My closest branch is five miles away but I couldn’t get it delivered.

There’s no minimum spend and fees are £8.50 to £8.99.

Ocado’s Zoom delivery is between 6am and 10pm.

It currently only covers parts of West and East London.

Minimum spend is £15 and fees start from £1.49.

THE HIDDEN COST OF SPEEDY DELIVERY

IT’S not just the delivery fees that make ordering same-day delivery a pricey option.

There is a stealth cost that makes these services more expensive than standard online delivery – or if you just popped into the shop.

The vast majority of food items had been given a markup compared to the price for standard online delivery.

This markup varied between shops but made the basket almost £3 more expensive in some cases, than if you’d bought the items yourself at the shop or through online delivery.

Sainsbury’s: £15.20 versus £12.74 = £2.46 more expensive

Tesco: £16.44 versus £14.50 = £1.94 more expensive

Morrisons: £15.48 versus £14.73 = 75p more expensive

Waitrose: £13.11 versus £12.40 = 71p more expensive

The savings will still provide relief to millions, as over 22million households on standard variable tariffs are directly affected by the price cap, which is updated every three months.

Experts at Cornwall Insight had rightly predicted the energy price cap would drop to £1,720 in July.

Currently, the price cap sets annual energy costs at around £1,849.

However, many households may still pay more than Ofgem‘s headline figure.

This is because the price cap doesn’t cap total bills but limits the maximum cost per kilowatt-hour (kWh) of gas and electricity, along with daily standing charges.

Ofgem’s headline figure is based on the assumption that a typical household consumes 2,700 kWh of electricity and 11,500 kWh of gas annually.

So if you use more than a typical households expect to pay more.

What is the energy price cap?

However, energy experts say that households could make significant savings by switching to a fixed-rate energy deal now.

By choosing a fixed deal, customers can lock in consistent rates for a set period, potentially avoiding fluctuations in energy prices.

Of course, opting for a fixed energy deal carries the risk that, if energy prices drop further, you might end up paying more than you would on a variable tariff.

However, analysts have long said that households should not anticipate any significant drops in prices this year.

In response, National Energy Action Chief Executive Adam Scorer said: “Any fall in the price of energy is always welcome news, but this is a short fall from a great height. Bills remain punishingly high for low-income households.

“Four years of extraordinarily high energy bills has taken its toll. We hear heart-breaking cases every day.

“The likely expansion in eligibility for the Winter Fuel Payment will be a relief for some, but National Energy Action is calling for deeper energy bill support and a real focus to support households out of debt.”

How do I calculate my energy bill?

BELOW we reveal how you can calculate your own energy bill.

To calculate how much you pay for your energy bill, you must find out your unit rate for gas and electricity and the standing charge for each fuel type.

The unit rate will usually be shown on your bill in p/kWh.The standing charge is a daily charge that is paid 365 days of the year – irrespective of whether or not you use any gas or electricity.

You will then need to note down your own annual energy usage from a previous bill.

Once you have these details, you can work out your gas and electricity costs separately.

Multiply your usage in kWh by the unit rate cost in p/kWh for the corresponding fuel type – this will give you your usage costs.

You’ll then need to multiply each standing charge by 365 and add this figure to the totals for your usage – this will then give you your annual costs.

Divide this figure by 12, and you’ll be able to determine how much you should expect to pay each month from April 1.

How can I find the cheapest fixed deals?

To find the best fixed energy deals, start by visiting price comparison websites, which aggregate various offers from different energy suppliers.

The best sites include Uswitch.com and MoneySavingExpert’s Cheap Energy Club.

Enter your postcode and current energy usage details to receive a list of available deals tailored to your needs – it’ll take you less than five minutes.

You’ll then be able to compare the rates, contract lengths, and any additional features or benefits offered by each deal.

Next, visit the websites of individual energy suppliers to check if they have exclusive deals that are not listed on comparison sites.

Sometimes, suppliers offer special promotions or discounts directly to customers.

Compare these offers with those on the comparison websites to ensure you get the best possible rate.

Finally, consider customer service reviews and the overall reputation of the suppliers.

Once you have identified the best deal, follow the instructions to switch your energy provider.

What energy bill help is available?

There’s a number of different ways to get help paying your energy bills if you’re struggling to get by.

If you fall into debt, you can always approach your supplier to see if they can put you on a repayment plan before putting you on a prepayment meter.

This involves paying off what you owe in instalments over a set period.

If your supplier offers you a repayment plan you don’t think you can afford, speak to them again to see if you can negotiate a better deal.

SHOPPING experts have revealed when is the ideal time to stock up on major garden essentials to make huge savings.

Three of the key items should be bought this month in order to make the biggest savings.

3

Gazebos are a must-have for the unpredictable British summerCredit: Getty

Boffins at comparison site Idealo have done the hard work for us and worked out that shoppers could save £183.84 if they purchase a gazebo this month, rather than in November, when they are at its worst price.

One shopper recently bragged about picking up a “huge” gazebo from her local Morrisons for just £20.

May is also your month for hedge trimmer shopping and you could save £12.80 as opposed to buying in August as their most expensive month.

As most parents will know, tearing kids away from screens can sometimes be a challenge, making garden toys a lifeline in the summer months.

read more on garden bargains

If you’re after something that will keep your little ones entertained for hours, what about the trusty pogo stick?

May is the best month to pick one up, creating a saving of £1.24 rather than in December.

For your other green-fingered needs, June has been officially crowned as the cheapest month of the year to buygarden bitsin the UK, with the greatestdealson offer.

While June is ideal, buying garden goodies any time between the end of May and August is also promised to save you cash.

Idealo found that savings of up to £649 can be made by buying each item at the right time.

Katy Phillips, senior brand and communications manager at idealo tells The Sun: “Our data shows that a little patience can go a long way when it comes to saving money on garden essentials this year.

“Holding off until the right month could save shoppers hundreds of pounds on big-ticket items like sun loungers, tables and fire pits.

“We’d always recommend comparing prices across multiple retailers before committing to a purchase. With a bit of planning, and by using apps with tools like price alerts, you can enjoy your garden for less and make your money stretch further this summer.”

3

The best time to buy a hedge trimmer is MayCredit: Getty

How to save money on garden furniture

Opting to buy your new garden furniture or items on sale could save you a lot of money.

Most retailers start discounting garden items after summer and will run promotions over the winter, but be aware stock can be far more limited during this time.

Retailers will start reintroducing more to their garden ranges during spring and may run limited promotions over bank holidays, for example.

You are unlikely to get a great deal just before or in the height of summer, but some retailers offer mid-summer clearance sales to get rid of old stock, so keep an eye out.

Remember to always shop around when making a big purchase, as even if one store has a sale on, you may be able to get a better deal elsewhere.

You can use websites like Price Spy to compare the prices of items across multiple retailers and see how the prices have changed over time.

Remember, you may not need to buy you furniture – you could save a fortune by up-cycling old items instead.

Giving dirty pieces a good wash and a lick of fresh paint can make them look brand new.

You can also pick up perfectly good items second-hand.

Try platforms like Facebook Marketplace or eBay to see if anyone near you is getting rid of old items – you may even be able to pick them up for free.

3

May is an excellent month to score the best deals on garden toolsCredit: Getty

Check below to see how much more you’ll get each monthCredit: Alamy

It’s important to note that, although the new rates are now in effect, most people won’t see an increase in their payments until later this month or in June.

This is because those on Universal Credit have to wait a bit longer to receive the uprating because of how the benefit is assessed.

It means that the date you’ll receive the pay boost will depend on when your last assessment period was.

Universal Credit is paid monthly and is based on your circumstances each month.

This is called your “assessment period”, and it starts the day you make your claim.

The new Universal Credit rates will not come into effect until after the first full one-month assessment period, which starts on or after April 7.

Those whose assessment periods started after April 7 saw their benefits rise as early as May 13.

However, those whose assessment periods started before this date could be waiting until June 12 to receive the payment boost.

Here’s how your previous assessment period affects when you’ll get the payment boost:

March 17 to April 16 – increase applied in May, you’ll get it in your payment on May 21

March 18 to April 17 – increase applied in May, you’ll get it in your payment on May 22

March 19 to April 18 – increase applied in May, you’ll get it in your payment on May 23

March 20 to April 19 – increase applied in May, you’ll get it in your payment on May 24

March 21 to April 20 – increase applied in May, you’ll get it in your payment on May 25

March 22 to April 21 – increase applied in May, you’ll get it in your payment on May 26

March 23 to April 22 – increase applied in May, you’ll get it in your payment on May 27

March 24 to April 23 – increase applied in May, you’ll get it in your payment on May 28

March 25 to April 24 – increase applied in May, you’ll get it in your payment on May 29

March 26 to April 25 – increase applied in May, you’ll get it in your payment on May 30

March 27 to April 26 – increase applied in May, you’ll get it in your payment on May 31

March 28 to April 27 – increase applied in June, you’ll get it in your payment on June 1

March 29 to April 28 – increase applied in June, you’ll get it in your payment on June 2

March 30 to April 29 – increase applied in June, you’ll get it in your payment on June 5

March 31 to April 30 – increase applied in June, you’ll get it in your payment on June 6

April 1 to April 31 – increase applied in June, you’ll get it in your payment on June 7

April 2 to May 1 – increase applied in June, you’ll get it in your payment on June 8

April 3 to May 2 – increase applied in June, you’ll get it in your payment on June 9

April 4 to May 3 – increase applied in June, you’ll get it in your payment on June 10

April 5 to May 4 – increase applied in June, you’ll get it in your payment on June 11

April 6 to May 5 – increase applied in June, you’ll get it in your payment on June 12

How does work affect Universal Credit?

Are you missing out on benefits?

YOU can use a benefits calculator to help check that you are not missing out on money you are entitled to

Entitledto’s free calculator determines whether you qualify for various benefits, tax credit and Universal Credit.

MoneySavingExpert.com and charity StepChange both have benefits tools powered by Entitledto’s data.

You can use Policy in Practice’s calculator to determine which benefits you could receive and how much cash you’ll have left over each month after paying for housing costs.

Your exact entitlement will only be clear when you make a claim, but calculators can indicate what you might be eligible for.

Here’s a full list of the new benefit rates for 2025-26 so you can check how much extra you might get.

Universal Credit

Universal Credit standard allowance (monthly)

Single, under 25: £316.98 (up from £311.68)

Single, 25 or over: £400.14 (up from £393.45)

Joint claimants both under 25: £497.55 (up from £489.23)

Joint claimants, one or both 25+: £628.10 (up from £617.60)

Extra amounts for children

First child (born before April 6, 2017): £339 (up from £333.33)

Child born after April 6, 2017 or subsequent children: £292.81 (up from £287.92)

Disabled child (lower rate): £158.76 (up from £156.11)

Disabled child (higher rate): £495.87 (up from £487.58)

Extra for limited capability for work

Limited capability: £158.76 (up from £156.11)

Work-related activity: £423.27 (up from £416.19)

Carer’s element

Caring for a severely disabled person at least 35 hours a week: £201.68 (up from £198.31)

Work allowance increases

Higher work allowance (no housing): £684 (up from £673)

Lower work allowance (with housing): £411 (up from £404)

Everything you need to know about Universal Credit

HUGE changes to Buy Now Pay Later rules that will help protect customers have been confirmed by the government.

The new Labour government has published its response to a consultation on proposals to tighten up rules in the Buy Now, Pay Later (BNPL) sector.

1

The government has confirmed huge changes to the Buy Now Pay Later rules,Credit: Getty

BNPL is a type of credit scheme that allows shoppers to purchase items and spread the payments over a set period and is used by 10million Brits.

While the schemes are popular, they have remained largely unregulated, which has raised concerns about people falling into debt.

The government has now said that from next year BNPL firms will need to follow “consistent standards,” so shoppers know exactly what they’re signing up for.

This means firms will have to be clear and transparent about any late fees or if they could affect customers’ credit ratings and how.

They should also signpost customers towards debt help in any correspondence.

For consumers, that could look like upfront credit checks to make sure people can repay what they borrow.

Also, customers will have quicker access to refunds and the right to complain to the Financial Ombudsman.

The plans will bring the products under FCA regulation while ensuring they also adhere to a large proportion of the Consumer Credit Act and Section 75, which give shoppers various rights.

Lisa Webb, Which? Consumer Law Expert, said that research shows that many users “do not realise they are taking on debt or consider the prospect of missing payments.”

She added: “It’s good to see the government taking action to regulate BNPL firms and introducing affordability checks.

Five key changes to PIP & Universal Credit as Labour’s benefits crackdown unveiled

“The government also needs to ensure this includes greater marketing transparency and information about the risks of missed payments and credit checks.”

Proposals to regulate BNPL products were first touted in 2021 but faced repeated delays.

Last year, The Sun revealedthe previous Conservative government had paused the plans over fears that it would drive BNPL firms out of the market during atough cost of livingcrisis.

Then in October, the Treasury Tulip Siddiqexclusively told The Sun that the government had finalised its “bespoke” plans and intended to pass the legislation “as soon as possible” in early 2025.

The legislation bringing BNPL into regulation is set to be laid in Parliament today, May 19.

A consultation on the findings is set to take place with the rules expected to come into force next year.

How can I use BNPL without losing out?

The hope is that this new regulation will prevent people from being able to take on more than they can realistically afford to pay back.

But when used correctly, BNPL plans can be a useful way of managing your finances.

The products work in a similar way to other types of credit. The main difference is that they don’t charge interest.

You usually have to make payments by set deadlines over a period of time.

If you meet these repayment deadlines, you shouldn’t be charged any extra fees.

How to cut the cost of your debt

IF you’re in large amounts of debt it can be really worrying. Here are some tips from Citizens Advice on how you can take action.

Check your bank balance on a regular basis – knowing your spending patterns is the first step to managing your money

Work out your budget – by writing down your income and taking away your essential bills such as food and transport If you have money left over, plan in advance what else you’ll spend or save. If you don’t, look at ways to cut your costs

Pay off more than the minimum – If you’ve got credit card debts aim to pay off more than the minimum amount on your credit card each month to bring down your bill quicker

Pay your most expensive credit card sooner – If you have more than one credit card and can’t pay them off in full each month, prioritise the most expensive card (the one with the highest interest rate)

Prioritise your debts – If you’ve got several debts and you can’t afford to pay them all it’s important to prioritise them

Your rent, mortgage, council tax and energy bills should be paid first because the consequences can be more serious if you don’t pay

Get advice – If you’re struggling to pay your debts month after month it’s important you get advice as soon as possible, before they build up even further

Groups like Citizens Advice and National Debtline can help you prioritise and negotiate with your creditors to offer you more affordable repayment plans.

YOU may use price comparison sites to get the best deals for your broadband or car insurance – but probably don’t do the same when shopping.

Whether you’re looking for great buys for your home and garden, a good deal on a new summer outfit or simply to drive down the cost of your weekly shop, there are online tools that can help you get the best price.

FANCY FEATURES: For homeware, tech, clothes and more, compare prices using sites like PriceRunner, Idealo, Google Shopping and PriceSpy.

Check across different sites to make sure you get the best deal.

They all have clever features to help you make the savviest shopping choices.

Idealo is one that allows you to scan barcodes in store to check if a product is cheaper online

READ MORE MONEY SAVING TIPS

With the PriceRunner on the Klarna app, you can access an AI assistant who will interpret what you’re looking for and help you find the right item.

PAST PRICES: The sites’ price-tracking tools also help you to check if deals are as good as they look.

They show price history, so you can see how the cost of an item has gone up and down.

That way you can judge whether you might get a better deal by waiting.

If you’re shopping via Amazon, then CamelCamelCamel will show you how much items have previously sold for.

Use the tool to check out the offers during Amazon’s Everyday Essentials Week, starting on Wednesday.

Cut car insurance costs and save money

FOOD FOR THOUGHT: For grocery shopping, download the Trolley app or log on to trolley.co.uk.

You can search for any item you’d find in the big supermarkets, including own brands, to see the best prices.

On the app, you can scan barcodes, create shopping lists and get price alerts when an item changes price.

It shows Heinz Tomato Ketchup, 1.35kg, is currently £4.92 at Asda or £6 at Morrisons.

Prices on page correct at time of going to press. Deals and offers subject to availability

7

Three savvy ways to use price comparison sites for your shoppingCredit: Getty

Deal of the day

7

Save £50 the Vileda Sun Rise rotary washing line

SWAP using a costly tumble dryer for drying your clothes outside on the Vileda Sun Rise rotary washing line, down from £167.99 to £117.99 at vileda.co.uk.

SAVE: £50

Cheap treat

7

Save £1.75 on Cadbury Dairy Milk Buttons ice cream with a ClubcardCredit: Supplied

TREAT the family to Cadbury Dairy Milk Buttons ice cream, £4.50 for a pack of four from Tesco, or £2.75 with a Clubcard.

SAVE: £1.75

What’s new?

IF you missed the sell-out metal striped chair from Asda last summer, there’s now another chance to buy it.

The garden lounger is £39, while stocks last.

Top swap

7

This white linen blend short-sleeved shirt is £18 from MatalanCredit: Supplied

7

Or try the linen blend shirt just £7.99 from LidlCredit: Supplied

FELLAS can update their wardrobe with the white linen blend short-sleeved shirt, £18 from Matalan, or they can try the linen blend shirt, £7.99 from Lidl.

SAVE: £10.01

Little helper

LAY on a tasty spread with three sharing plates for £8 at Sainsbury’s with Nectar, saving up to £5.50. Includes bacon-wrapped halloumi sticks and goat’s cheese and caramelised onion quiches.

Shop & save

7

Save £3.90 on a pack of The Best fresh pasta, sauce and garlic bread from a selection at MorrisonsCredit: Supplied

PICK up a pack of The Best fresh pasta, sauce and garlic bread from a selection at Morrisons for £6, to make a tasty Italian meal for two.

SAVE: £3.90

Hot right now

SEARCH “kids eat free megathread” now at hotukdeals.com for a list of restaurants, cafes and supermarkets with “kids eat free” deals.

PLAY NOW TO WIN £200

7

Join thousands of readers taking part in The Sun Raffle

JOIN thousands of readers taking part in The Sun Raffle.

Every month we’re giving away £100 to 250 lucky readers – whether you’re saving up or just in need of some extra cash, The Sun could have you covered.

Every Sun Savers code entered equals one Raffle ticket.

The more codes you enter, the more tickets you’ll earn and the more chance you will have of winning!

Fresh figures from the Energy Ombudsman reveal that British Gas came out worst out of all energy companies in the UK.

The firm received 48 complaints per 100,000 domestic customers between October and December 2024 – the worst rate in the country.

With an estimated 7.5 million UK households on its books, that’s around 3,600 complaints officially accepted by the Ombudsman in just three months.

The stats reveal how many cases were accepted per 100,000 customers – giving a clearer picture of which firms are falling short.

Here’s how the rest stack up:

Scottish Power – 27.8 complaints per 100K (approx. 1,390 cases, based on 5 million customers)

EDF Energy – 26.6 per 100K (1,463 cases, 5.5 million customers)

OVO Energy – 26.4 per 100K (1,056 cases, 4 million customers)

Octopus Energy – 22.5 per 100K (1,643 cases, 7.3 million customers)

E.ON Next – 21.2 per 100K (1,060 cases, 5 million customers)

Utility Warehouse – 18.7 per 100K (187 cases, 1 million customers)

Utilita – 11.1 per 100K (approx. 89 cases, 800,000 customers)

Utilita and Utility Warehouse were the best of the bunch, with the lowest complaint rates – while Octopus Energy continued its strong customer service record with a below-average rate.

These figures show how many complaints were accepted by the ombudsman after customers failed to get a resolution directly from their supplier.

All energy firms have been contacted for comment.

OVERALL COMPLAINTS FALL – BUT THOUSANDS STILL STRUGGLING

Across the board, the number of energy disputes accepted by the Energy Ombudsman fell by 24% in 2024, down to 92,938 cases from 122,829 the year before.

That’s a positive step – but complaints are still a third higher than in 2021, showing many customers are still getting a raw deal.

From TV to energy… tips to save you money on 7 bills that are going up in April

The most common problem? Billing issues, which made up 58% of all cases.

Top gripes included:

Disputed gas or electricity usage

Incorrect account balances