Energy prices may take ‘months’ to normalise, despite ceasefire: Analysts | US-Israel war on Iran News

Even though a fragile ceasefire between Iran and the United States and Israel has been announced, it’s going to be a long time before prices of oil and gas come back to pre-war levels, experts say.

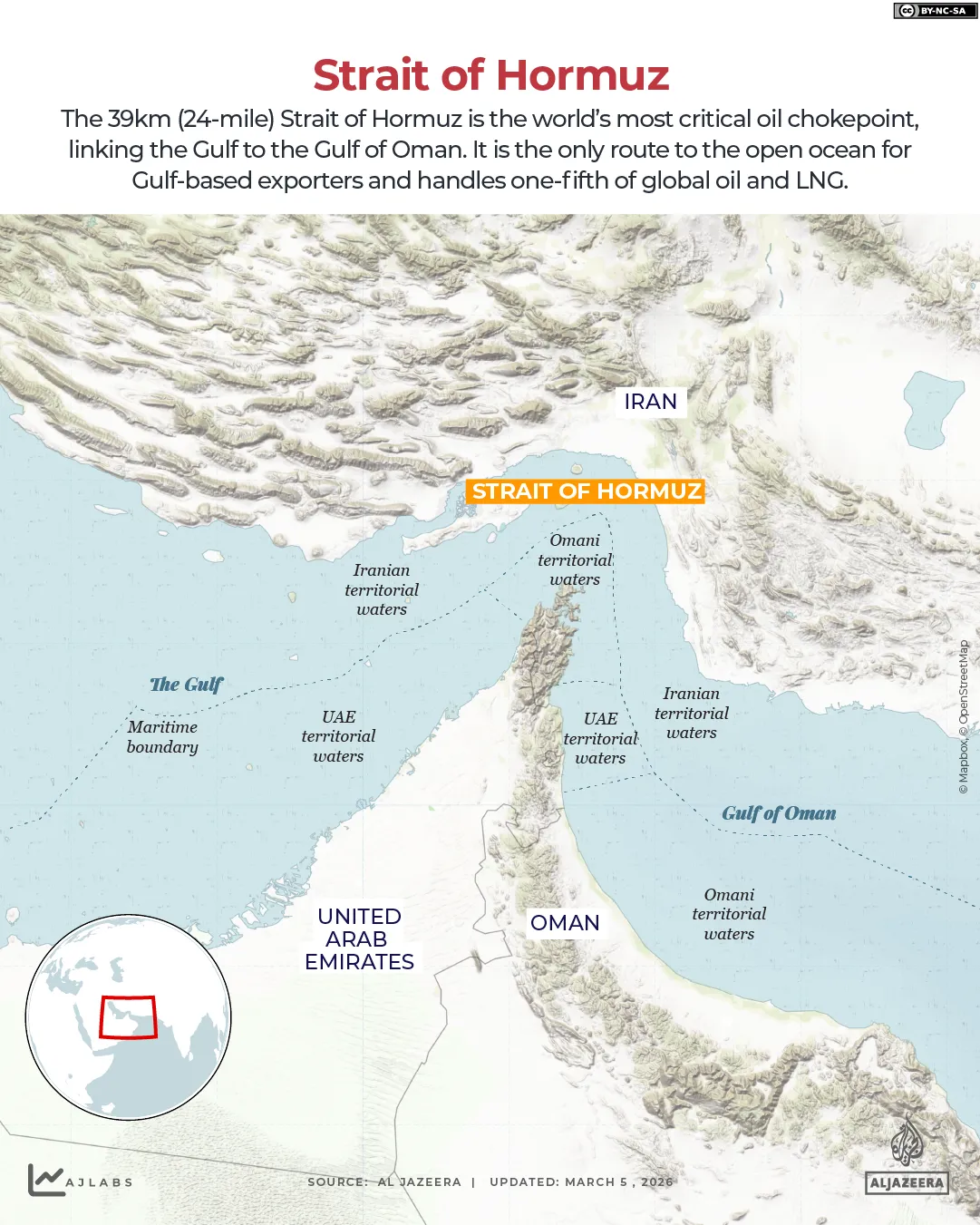

In response to the US-Israeli attacks, Iran choked off the Strait of Hormuz, the narrow channel linking the Gulf to the Gulf of Oman, through which roughly 20 percent of the world’s oil and gas exports pass from the Middle East, mainly to Asia and also to Europe.

Recommended Stories

list of 4 itemsend of list

It also attacked energy infrastructure in several Gulf countries, leading to soaring prices of not just energy but also of byproducts like helium, used in a range of products like tiles used in homes and semiconductor equipment. Fertilisers that rely on some of these inputs were hit too, impacting sowing seasons.

As a result, consumers the world over, but particularly in developing countries of Asia and Africa, have felt the brunt of those shortages and soaring prices. The question on many minds: Now that there is a ceasefire in place, how quickly will prices normalise?

“Anyone who tells you they know the answer to that question is lying,” said Rockford Weitz, professor of practice in maritime studies at The Fletcher School at Tufts University. “It’s too early to tell when we return to normal.”

There needs to be a predictable and stable flow of cargo through the strait before markets can stabilise, experts say.

“What we’re seeing is the biggest disruption in the history of global oil markets,” said Weitz.

Before this conflict, approximately 120-140 ships passed through the Strait of Hormuz every day. On Wednesday, only five vessels crossed the strait, while seven passed through the waterway on Thursday.

That shows why “to get back to normal is going to be a while”, Weitz told Al Jazeera. “And it’s too complicated to know at this stage when that will happen, as it requires collaboration with the great powers [US, China and Russia], but also regional powers [UAE, Saudi Arabia, India and Pakistan]. It’s hard to say when it will end, as there are so many parties who can make it not happen.”

There is also some concern that developments, like Iran charging a toll fee to allow ships to pass through and skyrocketing insurance fees, will keep oil prices high.

“There are reports that Iran is charging fees to tankers going through the Hormuz Strait,” US President Donald Trump wrote on TruthSocial Thursday.

“They better not be and, if they are, they better stop now.”

But experts agree that those fees, rumoured to be about $2m per vessel, are not enough to move the needle on oil prices.

“What is causing oil prices to rise is not insurance. It’s about getting tankers through. Tolls won’t be the cost driver,” said Weitz.

‘Signs of strain’

Some of that reality was on display with the reopening of the strait, showing “signs of strain just hours after the ceasefire was announced”, said Usha Haley, W Frank Barton Distinguished Chair in international business at Wichita State University.

Compounding that problem was the fact that some countries, including Iraq, had shut down production because of limited storage capacity, further taking oil supplies offline.

“That will take weeks and months to reopen,” Haley added.

“It’s going to be a contested reopening … LNG [liquefied natural gas] will take months to rebalance because of the hits to infrastructure, and can take three to six months to normalise if everything else remains normal. And it’s not.”

Slower growth

On Thursday, International Monetary Fund managing director Kristalina Georgieva warned that the fund will downgrade its forecast for the world economy next week from the current expectation of 3.3 percent. “Growth will be slower – even if the new peace is durable,’’ Georgieva said.

While the war has hit most economies, “it hasn’t really affected the two primary [US] targets – Russia and China. Russia, in fact, has benefitted enormously, and Chinese ships have been allowed to go through,” said Haley.

The US has hit Russia with multiple sanctions for its war on Ukraine, including capping sales of Russian oil to undercut its income stream. Similarly, the first Trump administration put tariffs on China and curbed US exports of certain high-end technology, measures that were held up under the administration of former US President Joe Biden and further ratcheted up by Trump last year with his tariffs blitz.

But amid the war on Iran and the effective closure of the Strait of Hormuz, the US temporarily eased some sanctions on Russian oil, and countries desperate for crude have since paid far higher prices to Moscow than the subsidised energy that President Vladimir Putin’s government was previously offering them.

“We [the US] really need to decide what we want to do long-term, who our targets are. There’s got to be some coherence to what we want to do.”

For now, “an overhang of greater risk premium of supplies out of the Gulf means oil prices will remain higher than what they were before the attack started”, said Rachel Ziemba, adjunct senior fellow at the Center for a New American Security.

While it’s possible that some of the blocked oil and oil products could be released soon, providing a short boost of supplies in the coming days and weeks, “that would be a temporary support” and is still conditional on the ceasefire holding and converting to a broader deal, said Ziemba.

For now, she’s keeping an eye on Iraq to see if it strikes a side deal with Iran. Iraq, long a proxy battleground between the US and Iran, can produce at least 3.5 million barrels of oil per day, production that it had shut off because of limited storage capacity, said Ziemba.

Should that come back online, it will help oil flows and, eventually, prices. But the uncertainty of the truce and the history of attacks on Iraq mean that the future of the country’s oil production remains unclear. “In that environment, who wants to invest in scaling up production?” Ziemba wondered.