Hungary’s political landscape has undergone a major shift following the electoral defeat of Viktor Orbán’s Fidesz party after 16 years in power. The new governing Tisza party, led by Prime Minister Péter Magyar, is now reversing several institutions created under the previous administration, including the controversial Sovereignty Protection Office.

The office was established in 2023 under former Prime Minister Viktor Orbán to monitor what the government described as foreign political interference in domestic affairs.

What Happened

The Tisza party has submitted a bill to parliament proposing the abolition of the Sovereignty Protection Office (SPO), arguing that it has no genuine public function and was used for political purposes.

According to the bill, the agency was designed to pressure opposition figures, journalists, civil society organizations, and media outlets by labeling them as serving “foreign interests.”

The SPO did not immediately respond to requests for comment. During its operation, it published studies aligned with the former government’s positions on issues such as migration, Ukraine, and relations with the European Union.

Why the Office Is Controversial

Critics have long argued that the Sovereignty Protection Office functioned as a political tool rather than an independent watchdog. It was frequently accused of targeting government critics and reinforcing narratives favorable to the ruling party at the time.

The European Commission had also launched infringement proceedings against Hungary over the law that created the agency, raising concerns about its compatibility with EU standards on media freedom and democratic oversight.

Opponents compared the SPO to similar legislation in other countries that restrict foreign-funded organizations, warning that it risked undermining press freedom and civil society independence.

Political Shift After the Election

The proposed abolition comes after a major political transition in Hungary, where the Tisza party defeated Orbán’s Fidesz in parliamentary elections, ending more than a decade of uninterrupted rule.

The new government has signaled a broader effort to dismantle institutions seen as politically aligned with the previous administration and restore institutional neutrality in governance.

What Comes Next

The bill will now be debated in parliament, where the Tisza party holds a governing majority. If passed, it would formally dissolve the Sovereignty Protection Office and potentially roll back other measures introduced under Orbán’s leadership.

The move is likely to deepen political divisions in Hungary, where debates over media freedom, foreign influence, and relations with the European Union remain highly contentious.

Jaua defended the importance of national unity in the struggle to reclaim sovereignty. (Venezuelanalysis)

Elías Jaua is a Venezuelan intellectual, university professor, and politician who served as vice president under Hugo Chávez in addition to several ministerial roles in the Chávez and Maduro administrations. He currently heads the Center for the Study of Socialist Democracy (CEDES). In this exclusive interview, Jaua discusses Venezuela’s post-January 3 conjuncture, the anti-imperialist struggle to reclaim sovereignty, and the role to be played by Chavismo.

Venezuela’s reality changed on January 3 with the US strikes and kidnapping of President Maduro. How would you describe the current situation? And regarding the US, there is talk of “conditional sovereignty” and “tutelage,” while officials speak of a “cooperation agenda.” What is your take on this?

Sovereignty is a comprehensive concept. You either have it or you don’t. Sovereignty means not depending on anyone. It is the foundation of a republic. A republic means independence from others, something distinct from liberal, individual freedom. Venezuela today is a state under tutelage, overseen by the Donald Trump administration. This was officially declared by Trump and White House officials such as Secretary of State Marco Rubio.

This is also clearly reflected in oil production, which must be sold primarily to the US, and the proceeds from those exports do not enter directly into Venezuela’s coffers but instead into a US Treasury account. From there, the Venezuelan government will make requests and have certain amounts necessary for the country’s basic functioning disbursed. That is a complete loss of economic sovereignty. We have also seen how reforms to strategic laws, such as those governing hydrocarbons and mining, have been rushed through. Today, there is immense pressure on labor legislation, both from the Venezuelan business community and from transnational capital, which views labor laws as yet another obstacle to attracting investment.

And finally, we have seen that Venezuela’s foreign policy – which was openly supportive of Palestine, Iran, and Cuba – has been significantly toned down. This is another clear sign that Venezuela is no longer an independent state. Its status as a republic is entirely relative.

US forces recently ran a military exercise in Caracas, with aircraft flying over the city and landing at the embassy compound. (EFE)

In light of all this, how do you feel the government and other national political groups should respond?

I view the decision made on January 3 not to respond to the US military attack as a responsible one, because the enemy clearly had military superiority and the capability to control the entire airspace using high-tech means. A response would have resulted in significant destruction of the country’s infrastructure and armed forces, as well as the killing of thousands of civilians.

Now, four months later, the Venezuelan government and all political forces should clearly denounce to the international community the coercion to which we are being subjected. On the one hand, as a public denunciation, but also to have it formally recorded before international bodies such as the International Commission on Human Rights. What occurred in January were war crimes, a fact supported by United Nations rapporteurs. Next, a complaint should be filed with the International Court of Justice to restore control over national revenues to the Venezuelan state.

One might argue that this is ineffective at the moment, that international law is irrelevant and international organizations are incapable of acting – and that is true. But the country must establish a legal precedent because these institutions still exist, and as a result they are a source of rights. These complaints set precedents so that the country can, in the future, claim the rights that have been damaged by the occupying power.

Finally, it is important to reach out to the international community, and above all to the peoples of the world, so that they know there is a nation that refuses to be placed under tutelage and subjected to these conditions, in order to build international solidarity. An internal political stance must also be established, because this attempt to conceal the gravity of the coercion to which the country is being subjected numbs popular consciousness, undermines patriotic morale, and that is contrary to what is expected of the leadership – not only of the government, but of the entire political leadership of the nation.

But what if that triggers another US military attack?

I don’t think a repeat of the January 3 incident is imminent because it would have repercussions in the US domestic political landscape. The political cost for the Trump administration would no longer be zero, as it practically was on January 3, but there would be greater resistance, especially for attacking a country that has simply exercised its rights before international bodies to claim sovereignty over resources and political self-determination.

Put another way, the option of not denouncing this, of not activating available mechanisms, is to accept and normalize this situation of neocolonialism, and I believe that is a very dangerous path that could even lead to Venezuela’s annexation by the US. I believe there are moments when peoples, nations, and their leaders must take a firm stand for the sake of history. Here it is no longer a matter of defending a party or a political movement, but rather the existence of a nation that was born free. We have a historic responsibility to ensure it remains that way for future generations.

Jaua highlighted the importance of denouncing US neocolonial impositions and calling for international solidarity. (Unión Radio)

US officials repeat their “three-phase plan,” which ends with a political “transition,” on a daily basis, while the extremist opposition demands immediate elections to seize power at any cost. From your perspective, what is the path forward, and what should the priorities be?

The priority is to regain independence. If we hold elections, that is with candidates for what? For governor of the colony? Anyone who truly wants to hold the presidency of the Republic of Venezuela must first raise their voice in favor of the immediate restoration of the country’s sovereign rights over its resources and revenues and the assertion of political self-determination.

In any case, I argue that any eventual electoral process should be the result of a national agreement, renationalizing politics and not waiting for a call from the White House one day announcing that there will be elections in six months. That would be very shameful. I believe that Venezuelan political forces would be obligated, as part of that strategy to reclaim and demand the restoration of Venezuela’s sovereignty, to also commit to the international community and the Venezuelan people to seek a political, democratic, and electoral path forward.

In a recent article, you spoke of an inability to manage the internal political conflict, which paved the way for foreign intervention. Could you elaborate on this idea? How has that situation changed since January 3?

Foreign meddling began on the very first day of the Bolivarian Revolution, and there were agents that facilitated it. The first concrete example was the April 11, 2002 coup d’état, with the open participation of the US and Spanish governments, and from that point on, that interference never ceased. But there was always a degree of autonomy that allowed, especially after 2004, for the democratic resolution of the conflict through national agreements. For instance, the recall referendum that ultimately ratified Chávez’s mandate.

But starting in 2014, after the right-wing insurrectionary attempt known as “La Salida” and its failure, the US began to intervene directly by declaring Venezuela an “unusual and extraordinary threat,” and from that point on, the opposition lost any capacity to make decisions. I was a member of the dialogue delegation in the Dominican Republic in 2018 and saw how an agreement signed by everyone was overturned by a phone call from the US embassy.

I also believe that later, over the past five years, the Venezuelan government chose to engage in dialogue with the US and bet that the conflict would be resolved directly with Washington. Therefore, everyone put all their eggs in the White House’s basket, and the decision slipped completely out of the control of the country’s internal institutions until the game came to a standstill. And indeed, at the behest of the far-right opposition, Washington intervened and attacked on January 3. That is why I say that reclaiming internal political control in order to resolve the conflict would be an act of dignity and courage on the part of the entire Venezuelan political leadership. Conflict is not going to vanish, because today the calls for a conflict-free Venezuela come alongside a set of measures that deepen it. For example, labor deregulation, social disinvestment, political exclusion, etc.

“We’re socialists and anti-imperialists!” banner in a Chavista march. (Archive)

In recent years, you have analyzed and debated the direction of Chavismo amid sanctions and the implementation of orthodox macroeconomic adjustment policies. Since January 3, we have seen a drastic overhaul of key pillars of the Bolivarian project, such as the Hydrocarbons Law, and critical voices growing louder, including Mario Silva and Luis Britto García. What is the current state of Chavismo, in your opinion?

First of all, the revision and change of course regarding fundamental aspects of Chavismo’s historic program did not begin on January 3 but much earlier. It was formalized starting in 2018 with the Program for Economic Recovery, Growth, and Prosperity, aimed at halting the advance of the transition to socialism and restoring the private sector’s hegemony in managing the economy, with clear consequences for social rights and the fight against social inequality. This was also accompanied by increasingly undemocratic mechanisms, from the political leadership, to impose a change of course in economic and social policy.

However, a fundamental core of Chavismo’s programmatic unity – the struggle for independence and national sovereignty – remained intact, and that kept Chavismo cohesive despite major differences. Today, I believe Chavismo must be situated within different spheres. There is a Chavismo within the United Socialist Party (PSUV) – no one can dispute that – but I believe there is a broader, and much larger, Chavismo, with a cultural, political, and symbolic identity rooted in a metanarrative that exists outside the PSUV and the Great Patriotic Pole. That sector currently lacks clear leadership and organizational structure, but it retains its values. It may have circumstantial views of the situation, but essentially it continues to uphold the principles that launched this process: sovereignty, participatory and protagonist democracy, democratic pluralism, freedom, political ethics, debate, speaking the truth, and social equality. It also holds a vision of a multipolar world, in solidarity with international struggles. These were, in essence, the core tenets of Chavismo from its inception and remain relevant for a significant portion of the Venezuelan population that is Chavista or was once Chavista.

You have talked about building national unity at this juncture, but also about upholding Chávez and his legacy. Are these two paths compatible?

This is a difficult and painful reflection because the figure and the project of Hugo Chávez have been burdened with a series of deviations. Practices that run completely contrary to the principles and values he defended, and upon which he built the Chavista project. For example, the case of Víctor Hugo Quero and his mother is deeply outrageous (1). It is a truly shameful incident, yet international news outlets report, “Chavismo admits to the disappearance of a detainee,” “Mother of prisoner killed by Chavismo dies.” Is it Chavismo or just a few individuals responsible? What about the men and women who, for over 25 years, laboriously dreamed, built, and dedicated part of their lives to creating well-being and the common good in their communities, to building a national project called “Chavismo”? It is very unfair because Chavismo, as a movement, is being accused of things it did not do. Chavismo is not this or that leader; it is the men and women who gave up the only thing they had – their time, their effort – to build community, a national project, to plant crops, to learn to read and write or to teach others to read and write, to study, and so on.

I stand by Chavismo as the men and women who dreamed, who continue to dream, and who have given their all to build a more humane society. For me, that will continue to be Chavismo. And those of us who have held leadership posts in this process must assume their responsibilities for the good and the bad. But it is unethical to blame a popular movement, a popular ideal like Chavismo, for the mistakes, deviations, and vile acts that some leaders may have committed.

I believe that the call for national unity, to paraphrase [revolutionary communist leader Alfredo] Maneiro, will spring from the most authentic Chavismo, but will transcend it. It will converge with other currents of the left that were not Chavista, with social democratic sectors that broke away from the extremist opposition, and with people who never took a stance on the political conflict the country has experienced in recent decades. It will be the plurality of opinions, of people, of organizations, that will provide the foundation for a necessary movement, which I see as unstoppable and already feel in the streets, in this struggle to regain independence and sovereignty.

Jaua served as Chávez’s vice-president from 2010 to 2012. (Archive)

Note

(1) Victor Quero died in state custody in July 2025 but his family was not notified. His mother, Carmen Navas, continued to search for him until his death was publicly acknowledged in May 2026 after a judge denied an amnesty request. Navas passed away shortly afterward.

Washington has imposed a semi-colonial tutelage over Caracas. (Archive)

On January 3, the US bombed Venezuela’s capital region and kidnapped President Nicolás Maduro. The unprecedented attack represented the culmination of a quarter-century of imperialist hybrid war, including devastating unilateral sanctions, mercenary incursions, “color revolution”-style insurrections, media disinformation, and NGO infiltration.

The four months since have brought a flurry of developments, from renewed diplomatic ties with the US to an overhaul of key legislative pillars of the Bolivarian Revolution. Additionally, the Trump administration established semi-colonial control over Venezuelan oil revenues, with the amounts and timings of disbursements back to Caracas left entirely at US officials’ discretion. The arrangement is similar to the one Washington has forced on Iraq since the 2003 invasion.

This compromised sovereignty is a catalyst for other issues. On the one hand, it makes it tougher for the Venezuelan government to improve living standards without challenging business interests. On the other, the burden of Venezuela’s external debt might see Washington attempt to impose an IMF loan that will bury the country in debt and dependency for decades.

Venezuelan Acting President Delcy Rodríguez alongside US Energy Secretary Chris Wright at the presidential palace. (Credit: Presidential Press)

The holy grail of foreign investment

The acting Rodríguez government’s tenure has been marked by accelerated political and economic transformations. On the international front, Caracas has restored diplomatic ties with Washington and recently resumed dealings with the US-controlled International Monetary Fund (IMF) and World Bank.

Domestically, Rodríguez has changed key cabinet and military posts, while pushing through the National Assembly a number of reforms with the explicit goal of making the country more attractive for private sector investment, especially from Western multinationals.

Plans to reform pension, tax, housing, and the landmark 2012 labor law are in motion. Mining and hydrocarbons have already undergone pro-business overhauls, with slashed fiscal responsibilities, decreased oversight, and disputes subjected to international arbitration. In contrast to Chávez’s reassertion of oil sovereignty, which underpinned the massive sociopolitical achievements of the Bolivarian Revolution, the reformed energy law brings back the old concession model that puts operations and sales in the hands of private corporations.

In tandem, the Trump administration has issued licenses to pave the way for Western conglomerates to return to Venezuela, and several have already struck deals under the new highly favorable conditions. The licenses maintain and even double down on US sanctions by barring dealings with China, Cuba, Iran, North Korea, and Russia and mandating that all Venezuelan state revenues from oil and mining be deposited in US Treasury-run accounts.

The subordination to US impositions saw Venezuelan authorities extradite former diplomatic envoy and minister Alex Saab to face charges in the US with little to no explanation. The move was shocking but not out of context. In recent weeks, there has been a succession of ceremonies at Miraflores presidential palace where Trump officials get the red-carpet welcome and escort corporate executives to sign contracts under the new pro-business incentives. Far-right tech moguls, including Palantir founder Peter Thiel, are already taking advantage of Trump’s leverage to establish a lucrative foothold in the country. For his part, the US chargé d’affaires holds regular publicized meetings with Venezuelan cabinet ministers.

Caracas’ technocratic and pragmatic approach has dovetailed with a corresponding shift in discourse. On foreign policy, the anti-imperialist rhetoric has all but vanished. As Trump unleashes a savage war against Iran and threatens to “take over” Cuba, Venezuelan leaders have refrained from condemning the escalating imperialist aggression while emphasizing their desire to build good relations with Washington. At the same time, references to Maduro have drastically decreased, as documented in a recent investigation. Domestically, the central focus has become macroeconomic stability and attracting foreign investment. Both Acting President Rodríguez and her brother, National Assembly President Jorge Rodríguez, acknowledged receiving “recommendations” and “suggestions” from oil majors amid the recent hydrocarbon overhaul.

Rodríguez and the Bolivarian leadership, under ongoing US pressure, are betting that the pro-business opening will lead to accelerated economic growth that will trickle down into improved living conditions, thus allowing the government to rebuild social legitimacy and political prospects. However, this plan faces serious roadblocks.

US Chargé d’Affaires John Barrett meeting with Venezuelan Electricity Minister Rolando Alcalá. (Credit: @usembassyve)

Rising domestic pressure

The first issue is that the acting authorities may not have a lot of time to improve the living conditions of the Venezuelan people.

Over the previous seven years, with the economy asphyxiated by the US economic blockade, the Maduro government prioritized macroeconomic stability and reduced inflation first and foremost, through a strict monetarist policy package. While the approach, coupled with a modest oil industry recovery, did lead to slowed down inflation and modest economic growth, it came at a price of freezing wages, consumer credit, and public spending. The minimum wage, last raised in 2022, is now worth less than US $1 per month, with further increases replaced by non-wage bonuses that cheapen labor costs for employers.

Though these bonuses have increased periodically (the income floor is now $240/month for public sector workers), they are still far from covering living costs. On May 1, Rodríguez ignored growing calls for a minimum wage hike, the conversion of bonuses to wages, and the restoration of collective bargaining rights, instead doubling down on the bonus policy. With government officials announcing a labor reform soon, it is likely that the return of the minimum wage will come alongside a significant erosion of workers’ rights and employer responsibilities.

However, apart from its commitment to fiscal discipline, the Rodríguez acting government has little room to maneuver because of its lack of direct management over oil revenues. At the mercy of the Trump administration to return export earnings in the amount and timing of its choosing, Venezuelan authorities are unlikely to commit to anything that might unsettle the budget. Rodríguez herself warned that wage increases must be “responsible.”

There is a delicate balance to strike. To implement the current pro-business agenda, not to mention the US rapprochement, the government needs social peace, and only improved material conditions for the working-class majority can ensure that in the short term.

Venezuelan trade unions have mobilized to demand a restored minimum wage and labor rights. (Credit: La Izquierda Diario)

The specter of debt

It is not just the pressure for better living standards that looms large on Venezuela’s economic front. There is a growing expectation that creditors will soon reengage with Venezuelan authorities to collect on a sizable external debt: a combination of defaulted bonds, unpaid loans, and arbitration awards that, with interest accrued over years, may amount to as much as $170 billion. The Venezuelan government recently announced the launch of a debt restructuring process, while Washington issued a license allowing the hiring of financial and consulting services.

Given the recent overtures to foreign capital, Venezuelan leaders will be hard-pressed to honor whatever commitments necessary to render the country a favorable investment climate. Nevertheless, a major chunk of this debt is illegitimate.

On the one hand, debt ballooned in the mid-2010s as Venezuela’s credit rating was unjustifiably downgraded and borrowing costs went up, as Washington slapped its first rounds of sanctions on the Caribbean country. The Maduro government made a strategic choice to prioritize debt service as the economy reeled following a collapse of global oil prices, hoping that this “discipline” would stave off a scenario where the country was shut out of financial markets. It turned out differently.

Venezuela was gradually locked out of global finance after the Trump administration’s 2017 financial sanctions. Bonds defaulted one after another and have been accruing interest ever since. And the notoriously corrupt US-backed “interim government” also played its part in running up Venezuela’s liabilities and pilfering state assets abroad.

The diverse group of bondholders and corporations owed arbitration awards is sure to receive the backing of the White House, which holds the purse of Venezuela’s export proceeds. This mechanism could be utilized to directly transfer Venezuelan state income to creditors in what would effectively amount to international wage garnishing. Given how Venezuelan bonds have risen in recent months, investors are eagerly eyeing a significant windfall.

Venezuela’s unsustainable debt burden opens the door for further US imperial predations. Even if there is an agreement to pay 50 cents on the dollar for Venezuela’s $170 billion debt for a period of 15 years, that comes to $5.6 billion a year, roughly a quarter of the present budget. It is simply unpayable.

While Caracas may be able to settle with some creditors by privatizing Venezuelan state assets, it will not amount to much. Venezuelan leaders will stress that, with the recent reforms and US opening, the economy will grow tremendously, and they will be able to honor all commitments. But creditors are not willing to wait when they can cash in now, especially given Venezuela’s weak bargaining position. The government cannot maintain a functioning country in the short term with a huge debt burden. As a result, the US might take advantage of the crisis to impose a major loan from the IMF or some lending coalition.

Trump has pushed for the return of Western corporations to Venezuela at the expense of Russian, Chinese and other counterparts. (Credit: VCG)

Sovereignty under threat

An IMF or similar loan program is more than just an agreement to lend some amount under certain repayment conditions. It is an opportunity to impose neocolonial arrangements on Global South countries. In Venezuela’s case it is even more symbolic: it would mean exacting the proverbial pound of flesh for Chávez’s revolutionary audacity to challenge US hegemony in the Western hemisphere.

An eventual long-term credit program would surely come alongside a structural adjustment package of mass privatizations, gutted social expenditure, and all-around liberalization of the economy. Given the current leverage over Venezuela, US officials may attempt to further entrench the rollback of the Caribbean nation’s sovereignty.

Between the growing domestic demands for improved living conditions and the specter of debt renegotiation, the acting Rodríguez government will find it increasingly difficult to walk the tightrope of maintaining social peace while continuing to make one concession after another to monopoly capital and the Trump White House.

With the limits of US imperialism nakedly exposed in Iran, Trump needs a victory in Venezuela. But that victory does not entail a buoyant economic recovery with social justice, let alone the survival of a sovereign and revolutionary project. Victory for the US is a dependent country, mired in debt and underdevelopment, where Western corporations plunder natural resources and geopolitical rivals are kept at bay.

Ultimately, any long-term plan for sovereign development needs to start from the fact that US imperialism, to echo Che Guevara, is “not to be trusted even a little bit,” much less considered a “partner” in a “cooperation agenda.” It will undoubtedly be a major hill to climb. But thankfully, even if it means starting over, the Bolivarian Revolution is not starting from scratch.

Taiwanese President William Lai Ching-te said Sunday that Taiwan would not do anything to trigger conflict with China but vowed the island would never allow itself to be traded away, or give up sovereignty. File Photo by Ritchie B. Tongo/EPA-EPA

May 18 (UPI) — Taiwanese President William Lai Ching-te said Taiwan would not do anything to trigger confrontation with China but vowed the island would never allow itself to be traded away or give up sovereignty.

In an online post Sunday, Lai said that “as a responsible party in the region and across the Taiwan Strait, Taiwan will not provoke or escalate conflict,” but neither would it yield to pressure to relinquish its “national sovereignty and dignity, or its democratic and free way of life.”

Lai’s statement came after Beijing warned U.S. President Donald Trump to be “extra cautious” over Taiwan, which Beijing regards as a breakaway province, saying it could result in clashes and potential conflict that could place the entire Sino-U.S. relationship “in great jeopardy.”

Speaking aboard Air Force One on his way back to Washington from his summit with Chinese President Xi Jinping, Trump said he had “made no commitment” either way on the Taiwan question or an $11 billion deal to sell arms to the island that was sent to Congress for approval in December.

Trump said he and Xi had discussed the arms deal in depth and that he would make a determination on whether it would go through “over the next fairly short period of time.”

“I’m going to say I have to speak to the person that right now is, you know, you know who he is, that’s running Taiwan,” Lai’s name apparently having slipped his mind.

Trump also strictly adhered to Washington’s long-held position of strategic ambiguity by refusing to answer questions over whether the United States would come to Taiwan’s aid militarily, were it attacked.

Beijing wants reunification and has not ruled out retaking Taiwan by force, particularly if it declared independence.

Back in the United States, Trump appeared to urge caution over Taiwan independence, telling Fox News on Friday that while nothing in the United States’ policy on Taiwan had changed, he wasn’t “looking to have somebody go independent.”

“I’m not looking to have somebody go independent. And, you know, we’re supposed to travel 9,500 miles to fight a war. I’m not looking for that. I want them to cool down. I want China to cool down,” he said.

Although the United States switched diplomatic recognition from Taipei in favor of Beijing in 1979 and acknowledged there is only one China of which Taiwan is a part– the so-called “One China” policy it follows to this day — the Taiwan Relations Act requires it to treat any effort to alter Taiwan’s future by force as a threat to peace in the region and U.S. interests.

The legislation requires the United States to provide the island with arms to defend itself and for the United States to maintain its own capacity “to resist any resort to force or other forms of coercion that would jeopardize the security, or social or economic system, of the people of Taiwan.”

However, there is no guarantee of committing U.S. troops to help defend the island.

In his post, Lai expressed gratitude for the United States’ “continued support” for peace in the Taiwan Strait, as well as ongoing military assistance.

“Given China’s unwavering commitment to the use of force to annex Taiwan and its continued military expansion in an attempt to alter the regional and cross-strait status quo, the United States’ continued arms sales to Taiwan and its deepening of U.S.-Taiwan security cooperation, even to the point of necessity, are crucial elements in maintaining regional peace and stability,” wrote Lai.

Wreathes are seen amongst the statues at the Korean War Veterans Memorial during Memorial Day weekend in Washington on May 27, 2023. Memorial Day, which honors U.S. military personnel who died while in service, is held on the last Monday of May. Photo by Bonnie Cash/UPI | License Photo

Foreign Minister Yván Gil (left) and former UN Ambassador Samuel Moncada (right) reiterated Venezuela’s longstanding position on the Essequibo dispute. (Archive)

Caracas, May 8, 2026 (venezuelanalysis.com) – The Venezuelan government reasserted its sovereignty claim over the Essequibo Strip during an International Court of Justice (ICJ) hearing aimed at resolving the long-standing territorial dispute with Guyana.

Venezuelan representative Samuel Moncada, defended the country’s “inalienable right” over the 160,000 square kilometer resource-rich territory during his intervention on Wednesday.

The ICJ is holding a week of hearings in The Hague between the two South American nations over the controversy, which in recent years has raised fears of a possible military confrontation. Venezuela has repeatedly stated that it does not recognize the court’s jurisdiction over the matter. However, Guyana unilaterally brought the dispute before the ICJ in 2018.

In this context, Moncada argued that the only valid legal instrument governing the dispute is the 1966 Geneva Agreement, which calls for a practical and mutually satisfactory solution between Caracas and Georgetown.

“Venezuela is here today because it cannot remain silent in the face of a process in which Guyana seeks to use the Court to unilaterally redefine the nature of the controversy,” Moncada said. He added that Venezuelans rejected the ICJ’s jurisdiction over the issue in the December 2023 referendum.

For his part, Guyanese Foreign Minister Hugh Hilton Todd told the judges that the case has “existential importance for Guyana” because it affects more than 70 percent of the country’s territory.

“For Guyanese people, the very idea that our country could be dismembered is a true tragedy because we would lose the vast majority of our land and population. Guyana would cease to be Guyana without them,” Todd argued during Guyana’s hearing session on Monday.

Moncada responded by saying that Guyana’s position implied that decades of mediation efforts by United Nations officials and Good Offices processes were attempts to “dismember” Guyanese territory, when in reality they sought the negotiated settlement that Guyana is now attempting to avoid.

The Guyanese government intends to have the ICJ uphold an 1899 arbitration ruling that awarded the Essequibo to the United Kingdom. However, in 1962 Venezuela filed a complaint before the United Nations seeking to nullify the award after evidence emerged suggesting that the decision had been reached fraudulently.

As a result, in 1966, while Guyana was negotiating its independence from the United Kingdom, the parties signed the Geneva Agreement, establishing that the Essequibo region would remain administered by Guyana while its sovereignty claim by Venezuela remained unresolved until a mutually agreed settlement could be reached.

The accord effectively superseded the Paris ruling and established a four-year framework to resolve the dispute in a “practical, peaceful and satisfactory” manner for both sides. Although no final resolution has been achieved, the agreement is still considered to be in force.

Tensions between the two countries escalated significantly in 2015 after ExxonMobil discovered massive offshore oil reserves in the disputed area, giving Guyana access to one of the world’s highest per capita oil reserves. Though the Essequibo is under Guyanese administration, Venezuela includes the territory in its official map and recently established administrative structures for its eventual 24th state.

The court at The Hague is scheduled to hold four hearings in total, during which both countries will present their legal arguments.

Guyana presented its first round of arguments on Monday, May 4, while Venezuela did so on Wednesday, May 6. Guyana’s second round took place on Friday, May 8, and Venezuela is scheduled to respond again on Monday, May 11.

Although the hearings will conclude that day, a final ruling could take months or even years. While ICJ rulings are legally binding, the court has no direct mechanism to enforce compliance.

According to Venezuelan Foreign Minister Yván Gil, regardless of the judicial proceedings, “the inevitable outcome will be Guyana’s return to the negotiating table to definitively resolve the territorial controversy under the framework of the 1966 agreement.”

Venezuela has gone through many stages in its assertion of ownership over natural resources and relationship with foreign corporations. (Venezuelanalysis / AI-generated image)

Venezuela’s recent Hydrocarbon Law reform has sparked fierce debates about its short- and long-term implications. In this essay, Blas Regnault, an energy policy analyst and researcher, offers an in-depth analysis of the new legislative framework, from the significant changes to the state’s governance over its natural resources to his perspective on a sovereign recovery of the oil industry.

The recent hydrocarbon reform: an overview

It is important to distinguish between two closely connected but analytically separate developments: first, US oversight of Venezuelan oil revenues after Maduro’s kidnapping; and secondly, the new Hydrocarbon Law itself. The first is an externally imposed mechanism that conditions oil sales, revenue collection, transport, and the distribution of oil proceeds to US interests. The second is a domestic legal reform whose constitutionality and political legitimacy have been widely questioned.

It remains unclear whether the new law is fully operative in practice, or whether it is only being applied selectively while its fiscal substance is displaced by the US revenue-control mechanism. But the outcome is largely the same: a loss of fiscal automaticity and a form of fiscal sovereignty under tutelage in relation to Venezuelan oil income.

In other words, the crisis of governance in the Venezuelan oil sector, together with its chronic lack of transparency since 2017, now culminates in a profound loss of sovereign control over all three dimensions of the business: its rentier dimension, belonging to the nation; its fiscal dimension, belonging to the state; and its shareholder dimension, linked to the role of the state oil company PDVSA as principal participant in extraction and commercialisation.

Therefore, the new law is not simply a technical reform. It is not merely about updating contracts, modernising procedures, or making the sector more attractive to investors. The deeper issue is that the reform changes the way the nation is compensated for the use of the subsoil and therefore alters the very governance of the sector. What is at stake is the relationship between sovereignty, ownership of the subsoil, and public income.

It is true that, on paper, the law formally preserves state ownership over the resource. But the business models it opens weaken the practical substance of that ownership. And that is the crucial point. Ownership is not a decorative legal formula. Ownership means that the state, acting on behalf of the nation, has the right to decide whether the resource remains underground or is extracted; and if it is extracted, under what conditions, with what public charge, and for whose benefit. The recent reform softens the link between ownership and the nation’s participation as owner of the subsoil, turning something that was once grounded in a general rule into something negotiable, adjustable, and highly discretionary.

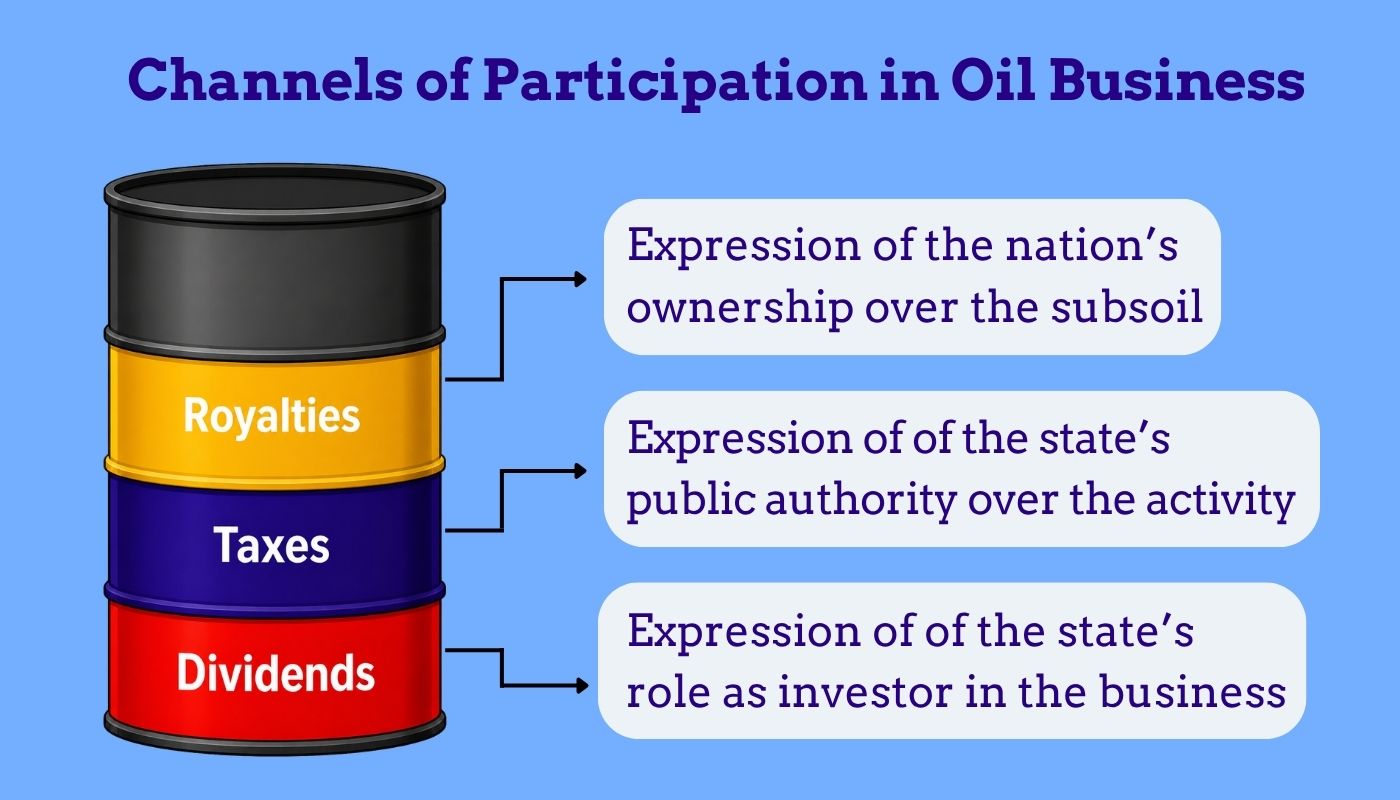

A useful way of understanding the economic and social significance of the reform is to distinguish the different streams of public income historically associated with oil in Venezuela. Under the former hydrocarbon law, the nation participated in the oil business through three distinct channels: as owner, as tax authority, and as shareholder. The first channel, corresponding to ownership, was royalty. The second was taxation, arising from the state’s fiscal authority over the activity. The third was dividends, arising when the state participated through PDVSA and therefore received income in its capacity as stakeholder rather than as landlord or tax authority.

This distinction matters because the oil business has historically involved different claimants competing over the fruits of extraction. In a sector marked by extraordinary profitability and strategic importance, the owner of the rent, the fiscal authority, and the capitalist operator all seek to maximize their share of the value generated. In the Venezuelan framework that prevailed before 2026, those three roles were clearly present: the nation as owner of the subsoil, the state as fiscal authority, and the operator as capitalist actor. The new law alters the balance between them.

Illustration of the different revenue streams in the Venezuelan oil industry. (Venezuelanalysis)

Royalty

The royalty is where the change is most revealing. As already noted, royalty is the clearest expression of ownership. It is paid upfront. It does not depend on profit. It is charged before taxes are assessed and before the remaining income covers the factors of production; that is, wages, interest, profits, and the other claimants on the project. In other words, royalty is not part of the production costs. If the oil price is 100 dollars per barrel and the agreed royalty rate is 30 per cent, the owner receives 30 dollars per barrel straight away. That is the proprietorial logic in its purest form.This has long been a battleground in the global oil industry. The dispute over rent has historically taken place between the operating companies, whether private national oil companies acting as operators, and the owner of the resource, that is, the landlord. Depending on the property-rights regime, that owner may be a private individual, as in parts of Texas, or the state, as in Venezuela and in most oil-exporting countries. Whether in Texas, Alaska, Saudi Arabia, Kuwait, Norway, the United Kingdom, Nigeria, or Venezuela, the property-rights regime has been the principal legal instrument through which the owner secures a share of the rent. It is a legitimate exercise of sovereignty, recognised by all parties involved in the global oil business.

Table 1: Effect of royalty rates on the nation’s per-barrel income using Merey 16 prices, Venezuela, January–March 2026

Month (oil price)

30% royalty

10% royalty

1% royalty

Jan 2026 ($43.21)

$12.96

$4.32

$0.43

Feb 2026 ($52.31)

$15.69

$5.23

$0.52

Mar 2026 ($86.00)

$25.80

$8.60

$0.86

Source: author’s calculations based on OPEC-MOMR January – March 2026 for Merey 16

And yet the new law, in practical terms, empties out that proprietorial logic by turning royalty into a negotiable variable within a range of zero to 30 per cent, something highly unusual in the global oil business. The potential scale of the loss becomes immediately clear once one thinks in terms of export volumes. At an oil price of 86 dollars per barrel, a 1 per cent royalty leaves the nation with less than one dollar per barrel, whereas a 30 per cent royalty yields 25.8 dollars. If Venezuela exports 800,000 barrels per day, that means roughly 688,000 dollars per day under a 1 per cent royalty, compared with 20.64 million dollars per day under a 30 per cent royalty. This is a dramatic compression of the owner’s income. It shows that a high oil price cannot compensate for the hollowing out of the royalty. Put simply, under the new law, higher oil prices will no longer automatically translate into greater income for the nation if royalties are arbitrarily lowered to the benefit of transnational capital. This is not a marginal fiscal concession; it is a radical compression of the nation’s proprietorial income.

Taxes

Turning to taxes, under the previous legal framework, the fiscal regime included not only taxes on profits, but also local and municipal taxes on oil activity, together with other parafiscal charges and special contributions linked to extraordinary profits. These different channels gave the public side several routes through which to capture value from extraction. Under the new law, much of that architecture is displaced and compressed into an integrated tax on gross income that will also be set in a discretionary fashion up to a fixed ceiling. According to supporters of the reform, this new framework is designed to ensure the project’s “economic equilibrium.” But the political significance of that shift is considerable. What was previously structured through several distinct legal claims can now be more easily absorbed into a flexible package, negotiated project by project. In that sense, this is not simply simplification; it is a substantial thinning of the fiscal claim. Once the fiscal architecture becomes thinner, the public claim over oil value becomes weaker, more flexible, and ultimately more negotiable.

Table 2 illustrates the magnitude of the change using the March 16, 2026, marker Merey 16 price. Under the previous regime, taxes and parafiscal charges alone could amount to about $31 per barrel, or 36 percent of the barrel price. Under the post-reform interim scenario, that could fall to about $17.6 per barrel, or 20.5 percent.

Table 2: Tax and parafiscal take per barrel before and after the reform

Fiscal Component

Former Law (reference model)

Post-reform scenario

Difference

Taxes and parafiscal charges per barrel (USD)

$31

$17.6

-$13.4

As share of barrel price (%)

36%

20.5%

-15.5%

Note: Figures are illustrative and based on the March 2026 Merey 16 price of US$86 per barrel, using the reference model for the former regime and the intermediate scenario for the post-reform regime. Source: Authors’ calculations based on the comparative fiscal scenarios and March 2026 Merey 16 price data.

Dividends

Finally, there are dividends arising from state equity participation, and these too must be distinguished from both royalty and taxation. Dividends are not paid because the nation owns the subsoil, nor are they collected because the state exercises fiscal authority over the activity. They arise because the state participates in the business as shareholder and therefore receives part of the profits in its capacity as investor. In other words, dividends represent the state’s participation in the profits of the business itself. But that income is not necessarily available for immediate public use in the same way as royalty or taxation. Part of it may be retained within the company, used for reinvestment, capital expenditure, debt service, or the wider financial needs of the enterprise. So, unlike royalty, which expresses ownership, or tax, which expresses fiscal authority, dividends are tied to the corporate logic of the business. Depending on the ownership structure, this channel of participation may range, illustratively, from zero to 60 per cent of distributable profits.

International jurisdiction of potential oil litigation

There is also an important jurisdictional dimension. By reducing the fiscal share captured by the state and by placing greater weight on contractual flexibility, the reform moves the sector towards a framework that is more exposed to international arbitration. At the same time, the sanctions and licensing regime has become part of a broader architecture of control over the oil business: control over access to the fields, control over marketing channels, and control over financial access to revenues. So, this is not merely a domestic fiscal reform. It is also part of a broader reordering of the legal and financial chain through which Venezuelan oil is governed.

Key takeaways

Supporters of the new law argue that it delivers increased flexibility, greater operability, improved investment prospects, and greater bankability. And that is not a trivial argument. In a country that has experienced production collapse, sanctions, institutional erosion, and a loss of market share, it is understandable that policymakers would seek a framework that appears more attractive to capital. In that sense, the reform may indeed reduce perceived risk and make projects easier to finance. It may also simplify part of the gross take and make negotiations easier. In that sense, the reform should not be caricatured. But it also entails the abandonment of each of the nation’s and the state’s historic roles in the sector, undermining the institutional fabric that once gave the oil economy a degree of stability and rationality.

For that reason, the disadvantages of the reform ultimately outweigh its potential benefits. What is lost is fiscal automaticity. That means the nation is no longer guaranteed a stable share by rule, but must now negotiate it, justify it, or recover it through more uncertain channels. Put differently, the reform replaces payment-by-rule with payment-by-negotiation on a case-by-case basis. In practical terms, each contract will generate its own conditions over each of the principal sources of public income arising from oil activity.

What is also lost is the clarity of a system in which the state charges because it owns the resource, not because the project happens to be commercially convenient. Once royalties become variable and fiscal terms are subordinated to the “economic equilibrium” of the project, the centre of gravity shifts. The guiding principle is no longer the nation as sovereign owner; it becomes the financial viability for the investor/operator. That is a profound political change presented as technical pragmatism.

In summary: the 2026 reform does not abolish formal ownership, but it hollows it out in practice. It replaces a more proprietorial fiscal logic with a more contractualized and discretionary one. That may attract investment, but it also weakens the automatic link between national ownership and national income. Whatever mechanism one chooses to emphasize, the result is much the same:

The nation no longer receives royalty by rule, but under externally conditioned arrangements. What is presented as flexibility is a retreat from ownership.

The state compresses its fiscal participation at every level.

The state oil company weakens its position as an investor.

Once that happens, the central question is no longer simply, “How much is the state collecting?” but rather “Who decides, under what rules, with what traceability, and with what accountability?”

Shell oil wells in Lake Maracaibo, Western Venezuela, in the 1950s. (Archivo Fotografía Urbana)

The historical context of Venezuela’s oil legislation

Venezuela’s oil history is not just a history of contracts or companies; it is a history of how the nation has tried to define its authority over the subsoil. Venezuela did not begin from the same position as many oil-exporting countries in West Asia or North Africa. It was already an independent republic when it developed its mining and hydrocarbons legislation. That matters, because it means Venezuela built a national jurisdictional framework around state ownership of mines and deposits, rather than inheriting a colonial concessionary order imposed from outside. That distinction is central.

From the early twentieth century onwards, successive legal frameworks progressively consolidated the republic’s sovereign claim over oil-bearing land. In other words, Venezuelan oil law was historically moving towards a more explicit assertion of the nation’s right to charge for the extraction of its natural wealth. This is one reason Venezuela mattered so much internationally: not only because it was a major producer, but because it became a reference point for fiscal regimes and sovereign oil governance, including later in the wider OPEC environment. In that sense, Venezuela’s experience was historically complete in a way that few other oil-producing countries were.

Nevertheless, there is a paradox surrounding the 1975-1976 nationalization of the oil industry. On paper, it ought to have marked the culmination of national control, but it did not deepen sovereignty. In practice, it helped produce a shift towards a more internationalized governance structure. The Ministry, as representative of the owner-nation, was gradually displaced by state oil company PDVSA, and PDVSA increasingly operated under a logic of global business rather than one of public sovereign rule. So instead of the owner-state speaking directly, the national oil company became the intermediary, and that had long-term consequences. Put differently, PDVSA, together with international oil capital, gained ground in the long struggle to reduce the landlord’s direct grip over rent.

This is where the historical relationship with Western transnational corporations becomes more nuanced than a simple story of foreign domination versus nationalist resistance. The issue is not merely the presence of Western companies, but the governance structures they operate under. Venezuela moved from a more classic proprietorial regime towards a more cessionary one, and later, especially in the late 1980s and 1990s, towards more liberal or non-proprietorial arrangements. The oil opening (“Apertura Petrolera”) of the 1990s is especially important here, because it reduced the fiscal burden and shifted the framework in a way that centralized the operator’s conditions. That was already a major break.

The Chávez years brought a partial reversal. The restoration of the property right was not merely ideological posturing; it was a restoration of a more classical fiscal logic, in which the sovereign character of the state take was reaffirmed. But that restoration took place amid other contradictions, including the politicization of PDVSA and the accumulation of debt. So even that phase did not resolve the deeper institutional tensions.

The 2026 reform, then, does not emerge from nowhere. It is a new chapter of a long historical movement: from national jurisdiction, to nationalization, to cessionary governance, to the oil opening, to partial reassertion, to crisis and collapse, and now to a new form of contractualization from a position of weakness. Venezuela’s oil history has been a struggle not simply over who owns the oil, but over who governs the terms on which ownership is exercised. The present reform is the latest chapter in that struggle, but it is a particularly radical one because it comes after institutional erosion and under a global order that is far more contractual, litigious, and externally structured than the one Venezuela faced in the mid-twentieth century.

Chevron, Eni, Repsol, and Shell are among the corporations to have struck contracts under the new and improved conditions. (Venezuelanalysis)

Oil in the present geopolitical battle

The current geopolitical context of the US-Israeli aggression against Iran should, in principle, strengthen Venezuela’s bargaining position. When West Asia becomes more unstable, supply security rises as a strategic concern, and oil regains immediate geopolitical urgency, countries with large reserves and an established production history become more valuable.

Venezuela has occupied that position before. Venezuelan oil played an important strategic role for the Allies during the Second World War, for example. Today, renewed disruption around Iran and the Strait of Hormuz has again tightened the market and raised the geopolitical value of accessible barrels.

That is precisely why the current outcome appears so paradoxical. If global conditions improve Venezuela’s leverage, one would expect the country to negotiate from a stronger position and to demand a larger participation. One would expect a legal framework that captures more rent, not less; that uses geopolitical scarcity to reinforce state take, not to dilute it. But the current reform, alongside the sequence of deals with foreign conglomerates, and combined with US control over revenues, seem to move in the opposite direction.

This leads to the second point: the geopolitical issue is not only price or supply. It is also about control. What is emerging is a form of sovereignty under tutelage. Venezuela may formally remain the owner of the resource, but effective control over commercialization, revenue channels, and external validation appears increasingly conditioned from outside. Whether one calls that tutelage, external supervision, or subordinated reintegration, the takeaway is the same: sovereignty over the resource is no longer identical to sovereignty over the business. Recent US licenses illustrate the point very clearly. Washington has opened the door to renewed oil transactions with PDVSA, but under Treasury oversight and with proceeds channelled into US-administered accounts. That is not normal sovereign control over national oil income.

This is where the distinction between the origin and the destination of rent becomes especially useful. Even before we ask what is done with oil income socially or politically, we first need to know how that income is generated: through what pricing, what discounts, what fiscal structure, and through which payment channels. If that first level is opaque, then both the origin and the destination of rent become politically indeterminate. In other words, the problem is not only that the country may receive less revenue. The problem is that the country may not even be able to clearly verify what it is owed, how, and why. That is a much deeper sovereignty problem.

As a result, a geopolitical context that would, in theory, favor Venezuela, sees the country re-entering global markets with weakened sovereignty, under a framework of greater flexibility for operators and less certainty for the nation. That is why the debate is no longer only about production volumes or export flows. The real debate is about the jurisdictional and political order that now governs Venezuelan oil: who authorizes, who commercializes, who arbitrates disputes, who tracks the proceeds, and who answers to the country.

Blas Regnault was a guest on the Venezuelanalysis Podcast.

What does a sovereign recovery look like?

Moving from critique to programme is difficult, and the first honest thing to say is that no one can predict the exact path ahead. Venezuela is emerging from collapse, sanctions, loss of market share, institutional erosion, and a deep social crisis. Any recovery scenario, therefore, is bound to be politically fraught. But one thing is clear: if the country does not rebuild the public intelligibility of oil income, then any so-called recovery may simply reproduce opacity, distrust, inequality, and social tension.

A sovereign recovery does not mean autarky. It does not mean excluding foreign firms, nor does it mean mechanically returning to an earlier model. It means something more precise: restoring the link between ownership, public rule, and accountable income capture. In other words, if the nation owns the resource, then the nation must be able to know, verify, and govern how value is extracted from it. That means transparency over net prices, discounts, taxes, royalties, exemptions, payment channels, and the destination of funds. Without that, there can be no recovery in any meaningful sovereign sense. It would simply be resumed extraction.

A sovereign recovery also requires stripping away some of the ideological confusion that usually surrounds debates on natural resources. As Bernard Mommer argued more than twenty years ago, the governance of natural resources is, in many ways, a more elementary question than the conventional left-right divide suggests. In the case of oil and minerals, the deeper divide is above versus below. It is the tension between those who live and work on the surface (the nation, society, the public realm) and those who make their living from the subsoil.

That is why the question of ownership comes before the question of distribution, that is, before the question of what is done with the income generated by oil activity. Only after establishing the governance over the resource and the rules over its extraction does the familiar left-right question properly arise: how that income is used, whether for social spending, public services, etc., or private accumulation.

The first step, then, is transparency. Not as a slogan, but as an institutional obligation. Who is selling? At what net price? Under what discounts? With what deductions? Paid where? Audited by whom? These are not minor administrative questions. They are the very mechanics of sovereignty in an extractive economy. If the country cannot answer them, then the state is no longer exercising full command over its principal source of income.

The second step is to move away from excessive discretion and back towards intelligible general rules. Contracts will always matter in oil. But there is a difference between contracts operating within a strong public framework and contracts effectively replacing public rule. Once everything becomes negotiable in the name of investment or “economic equilibrium,” the public realm shrinks and the executive realm expands. That is politically dangerous in any country, but especially in one where oil historically underpinned a broader social pact.

The third step is to reconnect oil income with social legitimacy. This is not an abstract issue. It is whether oil wealth translates to salaries, living standards, public services, social protection, and some minimum sense of collective benefit. If the country enters a new extractive cycle in which more oil is produced but public income remains narrow, opaque, or externally conditioned, then social tensions are likely to intensify rather than diminish. That is why a sovereign recovery cannot be measured by production figures alone. It must be judged by whether the nation regains an intelligible and legitimate claim over the income stream.

In simple terms, the average Venezuelan citizen is aware of fluctuations in crude prices because they know they affect the national budget. Oil income is widely and legitimately perceived as income belonging to the nation, and therefore as something that ought to support public services and collective welfare. Even when that income is later misused (through corruption, clientelism, or mismanagement) the underlying perception remains: oil revenue belongs to all Venezuelans.

That is also why the current situation can be described as one of sovereignty under tutelage. The country may still be sovereign in formal terms, yet it operates under external supervision in practical terms. Unless that gap is closed, the language of recovery will remain politically fragile.

Blas Regnault is an oil market analyst and researcher based in The Hague, whose work explores how oil prices move across time and what they tell us about the global economy. Drawing on years of experience in central banking, energy research, and international consulting, he brings together political economy, business cycles, production costs, and petroleum governance in a way that is both rigorous and accessible.

He has spent much of his career studying the deeper forces behind oil price trends and fluctuations, always with an eye on the institutional and geopolitical realities of the global petroleum market. Later this year, he will publish his book, Political Economy of Oil Prices: Trends and Business Cycles in the Global Petroleum Market, with Routledge.

The views expressed in this article are the author’s own and do not necessarily reflect those of the Venezuelanalysis editorial staff.

Venezuela’s January 2026 hydrocarbons law reform marks a major shift in the country’s oil sector. It establishes a more flexible fiscal regime in the name of “international competitiveness,” while expanding the private sector role in extraction, operations, and dispute resolution mechanisms.

The reform follows years of US sanctions on Venezuela’s oil industry and coincides with new US licenses allowing Western conglomerates to move into Venezuela’s energy sector.

Join Blas Regnault, energy policy analyst and consultant focused on oil geopolitics, alongside Venezuelanalysis editors Ricardo Vaz and Lucas Koerner, as they break down the reform, its economic and political context, and what it means for control over strategic resources and national sovereignty.