Why I’m Watching Costco Stock Closely Even if the Market Thinks It’s Overvalued

Costco is exceptional at delivering value for customers and shareholders.

Following a monstrous run over the last five years that saw the share price outperform the S&P 500, shares of Costco Wholesale (COST -0.89%) have cooled off in 2025. The stock is roughly flat year to date after surging to a 52-week high of $1,078 earlier this year.

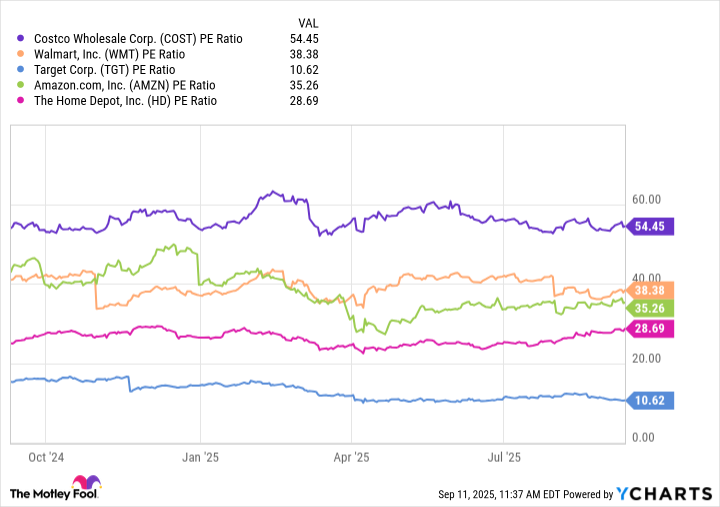

Costco shares have trailed the bull market rally in recent months. The only thing investors can blame is the stock’s high valuation. At a price-to-earnings (P/E) ratio of 50, the stock is the most expensive it’s been in 25 years. But sometimes stocks can trade for years at extended valuation levels. Costco’s exceptional operating performance and superb leadership certainly are deserving of a premium valuation.

While the stock could be in the process of settling at a lower P/E, there are two things about Costco’s business that make me interested in the stock even if it’s historically expensive.

Image source: Getty Images.

1. World-class operating efficiency

Costco has 81 million paying warehouse club members because it sells stuff in bulk cheaper than anyone else. Some investors might assume Costco prioritizes keeping its margins at a fixed level and reinvesting any cost savings in lower prices. While this is the basic strategy, Costco is still seeing its margins gradually rise.

Over the past 10 years, the company’s operating margin has improved from 3.1% to 3.8%. It has ticked up about 0.1% almost every year. This reflects several initiatives to improve operating efficiency, including automation, streamlining the checkout process, and continued growth in its private label brand Kirkland Signature, where sales continue to outpace Costco’s overall sales growth.

Costco capped off another solid year in terms of margin and operating profit growth. For fiscal 2025 (which ended in August), operating income grew 12% year over year, slightly above its past 10-year average annual increase of 11%. Earnings per share (EPS) grew 14% year over year excluding a tax benefit last year.

Consistency is a key element that can cause investors to award a premium valuation to a company. Next year, analysts expect Costco’s sales and adjusted earnings to grow 8% and 16%, respectively. The continued growth of Kirkland, which generates higher margins than other brands, and Costco’s culture of relentlessly squeezing every last ounce of inefficiency out of operations should maintain its recent trend of improving operating margin and earnings growth.

2. International opportunity

Perhaps the biggest factor that may cause the market to continue valuing Costco at a higher-than-average P/E is global expansion. Only 31% of Costco’s warehouse stores are outside the U.S., yet its discount operating model and global sourcing capabilities could pave the way for profitable international growth.

Costco currently has 914 warehouses worldwide, with 629 in the U.S. It plans to increase this base to 944 in fiscal 2026. Opening warehouses in foreign markets requires longer planning than in the U.S., but the company has a pipeline of openings it is pursuing internationally.

Current international stores are performing well. In the most recent quarter, its adjusted comparable-store sales in Canada grew 8.3% year over year, with other international markets up 7.2%. This was marginally higher than its U.S. comp-sales growth of 6%. Strong international growth prospects extend Costco’s ability to maintain consistent performance for many years.

But Costco is still finding plenty of room to expand on its home turf. Over the next year, two-thirds of its planned warehouse increase will be in the U.S. The combination of improving margins and growth opportunities at home and abroad justifies a high valuation.

Beyond numbers and growth opportunities, Costco’s corporate culture is just something you cannot pin to a specific P/E. The company’s consistent performance reflects a management team that is focused on one thing: delivering more value to customers. The fact it is succeeding on that mission while still improving margins makes Costco a highly valuable business.

Costco is one of a kind, and that’s why the stock still looks like a tempting buy even if it’s expensive.

John Ballard has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Costco Wholesale. The Motley Fool has a disclosure policy.