A WOMAN has revealed that she instantly fell in love with her step-brother after he moved in to the family home, and ended up pregnant with his baby.

Tookie and Krys first met as teenagers, when Krys moved back in with his mother, after years of separation.

2

Tookie and Kris are step-siblingsCredit: YouTube

2

They share a daughter named BlueCredit: YouTube

Tookie was already living with Krys’ mum, and was being raised as her step-daughter.

“When I first saw her I thought she was too good for me”, Krys told Love Don’t Judge.

“I didn’t talk to her because I was too nervous”.

However, Tookie was instantly attracted to Krys, describing his “nerdy” look as “sexy”.

Read more real life stories

The duo, who were 15 and 17 at the time soon grew close, and after Tookie initiated things, they began sleeping together.

“One thing led to another, and we made a baby”, Krys said.

The couple were able to keep their relationship under wraps until Tookie became pregnant.

Jamie, Krys’ mum, found out about the pregnancy after receiving a phone call from Tookie’s mum.

“I expected Tookie and Krys to behave to eachother like brother and sister”, Jamie said.

Krys had only just got back in contact with his mother when he got Tookie pregnant, and was worried their bond would become fractured again.

Ex On The Beach stars reveal they’re ENGAGED after four kids and cheating scandal – and the wedding is just weeks away

Jamie said she was hurt and disappointed by the actions of the pair, but still loves Tookie as a daughter.

The couple now share a daughter named Blu, who is 20 months old.

Despite his young age, Tookie said that Krys was a great help following her birth, and she didn’t have to lift a finger.

“I love the way he is, you’re a good father”, Tookie said to Krys.

Here’s why I love being a young mum

Tracy Kiss, who fell pregnant at 19, has revealed what she believes are the pros of being a young mother.

The personal trainer and blogger, from Buckinghamshire, believes women who give birth in their teens make BETTER mothers than those in their 30s.

She claims young mums snap back into shape quicker, have more energy and relate more easily to their children, meaning they’re better behaved and happier.

Tracy told Fabulous: “Women who become first-time mums in their teens make better parents than those in their 30s or 40s.

“I believe if I’d been 10 or so years older before becoming a mother then I wouldn’t have the relationship I have with my children now.

“For a start, being older I would have had less energy and therefore less patience.

“I wouldn’t be as enthusiastic to speak to people after months of sleepless nights as I was in my teens.

“My body snapped back to its pre-pregnancy size through fitness post-birth, which in turn gave me the confidence to date and find love again. I’ve never been happier than I am now at the age of 30 with two children.

“If I’d have been alone at 40 with a newborn baby I’d be more tired, less happy with my body, less energetic and far more stressed from the shock of living my life for myself instead of putting others first. Sometimes age and the innocence of ignorance is a good thing.

“As a teen mum I just got on with it, found my feet and became responsible and capable because at the time I didn’t know any different.”

The couple get lots of hate online for their unique relationship, but don’t let trolls get them down.

“If you’re still judging, then honestly, you’re miserable”, Krys said.

A BELOVED car garage with hundreds of thousands of fans has been forced to close its doors.

The garage is shutting down after nearly six years, after its famous owner battled with “rising costs”.

3

An iconic garage is sadly closing its doors after six yearsCredit: facebook/BerrowMotors

3

Joe Betty runs the popular Shifting Motors YouTube channelCredit: instagram/shifting_metal

Joe Betty first set up his famous garage Berrow Motors in 2020, in the sleepy town of Burnham-on-Sea.

During that time, he slowly built up his customer base and started posting videos about motors online – quickly racking up millions of views.

His YouTube channel Shifting Metal takes viewers behind the scenes of his high-flying lifestyle, as he buys and trades luxury vehicles including Porsches, BMWs and Jaguars.

However, after becoming one of the most famous motor influencers in Britain, Joe has been forced to close the garage which helped launch his career.

The petrolhead and influencer says that rising costs are to blame for the sudden closure of Berrow Motors.

He said: “We’ve had nearly six fantastic years here.

“We’ve won awards, gained over 100,000 YouTube subscribers and raised over £30,000 for local causes — but have decided now is the time to move on.”

“The cost of running a business is constantly rising and has certainly played a part in my decision, but I also wish to focus more time on fundraising and other business ventures.”

He added: “I want to thank all of our wonderful customers for their business over the last few years and of course the team members who made Berrow Motors what it was.

“I really hope another motor trader takes over the site and makes a success of it – you couldn’t ask for better landlords than the Welland family.”

Fans flooded the comments section on Shifting Metal’s social media, as Joe broke the news.

One wrote: “sorry to hear that the business is closing down. I wish you and your family all the very best for the future”

Others said they would miss Joe’s hilarious challenges that he would set himself on YouTube.

In one video, he flipped a coin to set the price of a luxury land rover and, in another, he bought and sold a Mercedes C63 for an eyewatering £35,000.

After letting go of the garage, Joe says that he is going to be focusing on producing even more “car-centric” content online.

The news comes as even major car brands struggle to stay afloat.

Nissan has been forced to accelerate the closure of two of its factories in Mexico, as it slashes its number of global factories from 17 to 10.

The crisis-hit brand has been battling rising debt, which it is hoping to remedy through its Re:Nissan plan.

The decision means lowermortgagepayments for homeowners but often leads to smaller returns for savers.

That’s because the base rate impacts theinterest ratesbanks offer on savings accounts and loans, including mortgages.

The Co-operative Bank has wasted no time, announcing that interest rates on dozens of accounts will be reduced starting on August 14 and October 22.

On August 14, the Base Rate Tracker accounts will see reductions, with interest rates dropping from 4% to 3.75% and from 3.75% to 3.5%.

For example, if you had £1,000 deposited for 12 months, the interest earned at 4% would have been £40.

After the rate drops to 3.75%, you would earn £37.50 – a difference of £2.50.

Similarly, with the rate falling from 3.75% to 3.5%, the interest earned would decrease from £37.50 to £35, meaning £2.50 less over the year.

From October 22, various other accounts will experience cuts, including the Future Fund, which will see its rate fall from 1.53% to 1.46%, and the Online Saver, dropping from 2.12% to 2.06%.

Other affected accounts include the Smart Saver, Select Access Saver 5, and Privilege Premier Savings, with reductions ranging from 4.15% to 3.9% and 3.53% to 3.4%.

Switch bank accounts for free perks

Cash ISA holders will also be impacted, with Cash ISA 2 rates falling from 3.25% to 3%.

Fortunately, several savings providers still offer returns of up to 5%.

With the average bank customer holding around £10,000 in savings, according to Raisin, switching could be a smart move.

To help you get the best returns, we’ve listed the top savings rates for each account type below.

What types of savings accounts are available?

THERE are four types of savings accounts: fixed, notice, easy access, and regular savers.

Separately, there are ISAs or individual savings accounts which allow individuals to save up to £20,000 a year tax-free.

But we’ve rounded up the main types of conventional savings accounts below.

FIXED-RATE

A fixed-rate savings account or fixed-rate bond offers some of the highest interest rates but comes at the cost of being unable to withdraw your cash within the agreed term.

This means that your money is locked in, so even if interest rates increase you are unable to move your money and switch to a better account.

Some providers give the option to withdraw, but it comes with a hefty fee.

NOTICE

Notice accounts offer slightly lower rates in exchange for more flexibility when accessing your cash.

These accounts don’t lock your cash away for as long as a typical fixed bond account.

You’ll need to give advance notice to your bank – up to 180 days in some cases – before you can make a withdrawal or you’ll lose the interest.

EASY-ACCESS

An easy-access account does what it says on the tin and usually allows unlimited cash withdrawals.

These accounts tend to offer lower returns, but they are a good option if you want the freedom to move your money without being charged a penalty fee.

REGULAR SAVER

These accounts pay some of the best returns as long as you pay in a set amount each month.

You’ll usually need to hold a current account with providers to access the best rates.

However, if you have a lot of money to save, these accounts often come with monthly deposit limits.

What’s on offer?

If you’re looking for a savings account without withdrawal limitations, then you’ll want to opt for an easy-access saver.

These do what they say on the tin and usually allow for unlimited cash withdrawals.

The best easy access savings account available is from Cahoot, which pays 5% – and you only need to pay a minimum of £1 to set it up.

This means that if you were to save £1,000 in this account, you would earn £50 a year in interest.

Meanwhile, West Brom Building Society’s easy access account offers customers 4.55% back on savings worth £1 or more.

If you’re okay with being less flexible about withdrawals, a top notice account could be a great option.

These accounts offer better rates than easy-access accounts but still let you access your money more flexibly than a a fixed-bond.

RCI Bank UK’s 95 day notice account offers savers 4.7% back with a minimum £1,000 deposit, for example.

This means that if you were to save £1,000 in this account, you would earn £47 a year in interest.

Meanwhile, GB Bank’s 120-day notice account offers 4.58%, requiring a minimum deposit of £1,000.

If you want to lock your money away and keep the same savings rate for a set time, a fixed bond is a good choice.

The best fixed rate currently offered is Vanquis Bank’s one-year fixed bond, which pays 4.44%, requiring a minimum deposit of £1,000.

Meanwhile, Atom Bank’s one-year fixed bond offers 4.42% back on a deposit of £50 or more.

This means that if you were to save £1,000 in this account, you would earn £44.20 a year in interest.

If you want to build a habit of saving a set amount of money each month, a regular savings account could pay you dividends.

Principality Building Society’s Six Month Regular Saver offers 7.5% interest on savings.

It allows customers to save between £1 and £200 a month.

Save in the maximum, and you’ll earn £25.81 in interest.

While regular savings accounts look attractive due to the high interest rates on offer, they are not right for all savers.

You can’t use a regular savings account to earn interest on a lump sum.

The amount you can save into the account each month will be limited, typically to somewhere between £200 and £500.

Therefore, if you have more to save, it would be wise to consider one of the other accounts mentioned above.

How can I find the best savings rates?

WITH your current savings rates in mind, don’t waste time looking at individual banking sites to compare rates – it’ll take you an eternity.

Research price comparison websites such as Compare the Market, Go.Compare and MoneySupermarket.

These will help you save you time and show you the best rates available.

They also let you tailor your searches to an account type that suits you.

As a benchmark, you’ll want to consider any account that currently pays more interest than the current level of inflation – 3.4%.

It’s always wise to have some money stashed inside an easy-access savings account to ensure you have quick access to cash to deal with any emergencies like a boiler repair, for example.

If you’re saving for a long-term goal, then consider locking some of your savings inside a fixed bond, as these usually come with the highest savings rates.

LYING in bed at night 68-year-old Melanie O’Reilly lay awake worrying about how she couldn’t afford to quit her £23,500 a year, 37.5-hour a week job working in a call centre.

She was £13,000 in debt and knew she couldn’t afford to pay the £500 a month repayments to the bank – but she was desperately unhappy in her job.

1

Melanie O’Reilly, 68, thought she’d never retire due to debt

Her days were spent fielding angry calls from Hounslow residents complaining about council tax and housing benefit.

She had moved from South Africa to England in September 2019 with no savings but found a job quickly due to her past career in office furniture sales.

However, the pandemic hit and in October 2020 she was made redundant before struggling to find a job at a call centre in the local council in Hounslow, West London in February 2022.

“I couldn’t stand it anymore. I was sitting there most days in full-blown migraine feeling like I had sandpaper in my eyes, until I couldn’t see the screen anymore,” Melanie, now 69, said.

“I had been very good at my job in South Africa, and I was excellent at sales.”

“Suddenly I was being micromanaged by a 26-year-old, who would count how many times I went to the toilet in a day, and tell me off if I took 31 seconds on a call instead of 30 seconds.

“The staff turnover was ridiculously high and it started to affect my physical and mental health.”

Melanie, who had previously worked as an insurance PA in London before the move to South Africa, was utterly fed up, and knew she had to retire – but had no idea how she could do so with her mounting debt.

She had lent her son and daughter-in-law, who had also moved to the UK, money for a deposit on a home in Colne, Lancashire – but then disaster struck.

Suddenly her daughter-in-law was made redundant shortly after they had their first child, meaning they couldn’t pay Melanie back as quickly as they’d planned.

Melanie was also dealing with the financial fall out of splitting from her partner and she took out a £15,000 personal loan and she had mounting credit card debt of £3,000.

Worryingly one in three people approaching retirement now have debt, with the average over-65 borrower owing £17,000, according to Money Wellness.

Financial anxiety among the 65 to 74 age group has more than doubled since 2021.

“I had the personal loan, but I was not behind in my payments and I just knew, ‘I’ve got to leave. I have to retire.

“If I don’t, I am going to have a breakdown’,” Melanie said.

“I decided to retire and I did, in April 2024. I called up Lloyds Bank and I said, ‘I’ve got this personal loan with you and I know that a few months from now I’m going to end up not being able to pay you.’

“I knew I had to take preventative measures before I got behind in any of my payments.

“I was hugely concerned about how to get Lloyds Bank to agree to a reduced monthly payment.

“I knew I couldn’t pay them back £500 a month, and I knew they wouldn’t negotiate a new loan with me because I was unemployed, as I was now retired with no real income.”

Lloyds put Melanie in touch with Money Wellness, one of the largest providers of debt advice and debt solutions in the UK.

Money Wellness provides free, confidential support to anyone struggling with money or debt, with support available online 24/7 or over the phone, so people can get help in the way that suits them best.

Melanie still owed £13,000 of the £15,000 personal loan. She called Money Wellness, and they asked her to draw up an income and expense statement.

Advisors went through her statement in detail, making allowances for everything from clothing to haircuts, and calculating how much she could afford to pay back each month to help Melanie put a debt management plan in place.

“They were so empathetic and professional,” Melanie explains.

“We revised the budget down to a manageable figure that I could pay Lloyds Bank back and by the end of it, it felt like this was too good to be true.

“They took the burden of negotiations off my shoulders and it was all done seamlessly for me without me having to worry about anything.”

The adviser told Melanie that they would negotiate the figure she had to pay back directly with Lloyds Bank, to the extent of setting up a debit order.

“After the call, I sat back and wept,” Melanie remembers.

“I was hugely concerned because when I was working at the council, I had people calling me up saying, ‘I’ve got the bailiffs at my door. They’re bashing my door down. What do I do?’

“I did not want to be in that position, and I knew that that is a reality that can and does happen.

“I did not want to go anywhere near being that person who’s got the bailiff bashing at your door. That is why I nipped it in the bud before it became a problem.”

From paying £500 a month back, Melanie now pays back £134 a month, with no added interest.

She lives in a HMO in Burnley so she doesn’t pay utility bills or council tax and receives housing benefits and pension credit.

Her repayments come from a small state pension, pension credit and housing benefits.

She receives £456.64 state pension, £451.56 pension credit and £368.20 housing benefit every four weeks.

She’d had to spend her small private pension on replacing her car after a car accident, and buying essentials like furniture.

Money Wellness reviews her plan annually, adjusting the amount if her income changes.

Melanie feels positive about the future and says the debt advice she received from Money Wellness is “the best decision I ever took”.

“For so long, I’d sat with this worrisome burden, thinking ‘I need to retire but I’ve got this debt. What do I do?’ Then these angels from heaven stepped up and helped me,” she adds.

“I feel as though a mountain had been lifted off my shoulders.”

How to cut the cost of your debt

IF you’re in large amounts of debt it can be really worrying. Here are some tips from Citizens Advice on how you can take action.

Check your bank balance on a regular basis – knowing your spending patterns is the first step to managing your money

Work out your budget – by writing down your income and taking away your essential bills such as food and transport If you have money left over, plan in advance what else you’ll spend or save. If you don’t, look at ways to cut your costs

Pay off more than the minimum – If you’ve got credit card debts aim to pay off more than the minimum amount on your credit card each month to bring down your bill quicker

Pay your most expensive credit card sooner – If you have more than one credit card and can’t pay them off in full each month, prioritise the most expensive card (the one with the highest interest rate)

Prioritise your debts – If you’ve got several debts and you can’t afford to pay them all it’s important to prioritise them

Your rent, mortgage, council tax and energy bills should be paid first because the consequences can be more serious if you don’t pay

Get advice – If you’re struggling to pay your debts month after month it’s important you get advice as soon as possible, before they build up even further

Groups like Citizens Advice and National Debtline can help you prioritise and negotiate with your creditors to offer you more affordable repayment plans.

Locals also are required to pay £8 per day for parking, if they have the annual £5 permit.

This has triggered outrage, a notable drop in visitors according to residents.

One local business owner, Beck Gordon who owns a cafe and fishmonger’s, said: “In terms of day-trippers, if you talk about more local people, they definitely don’t come any more.”

Beck added: “It’s quieter generally.

“The parking’s definitely an issue.”

She pointed to the “absolutely ridiculous” fact that it is cheaper to get a weekly parking ticket that costs £25 or £50 than pay the car park fees, which would add up to £70.

Another cafe manager in the area revealed spending £120 of her earnings just on parking.

Salcombe was recently dubbed the most expensive seaside town in the UK, with average house prices of around £1.2 million in 2022.

Lloyds, however, revealed they did tumble by 22 per cent in the Devon hotspot to £970,657 in 2022.

Discovering UK’s Most Picturesque Towns

It is known for its high concentration of second homes, which constitute 60 per cent of its housing stock, which are being hit by double council tax.

Despite having some of the UK’s best seafood, and being a small fishing village, it receives hardly any tourists anymore.

Councillor Julian Brazil, who is in charge of community services at the local council, stated: “We’d like to do everything to help the tourism trade and we have kept our car parking charges as competitive as possible.

“Residents of the South Hams can benefit from our discounted resident parking scheme.”

“Many workers in Salcombe have benefited from our competitive parking permits, which offer significantly lower long-term parking compared to our pay-on-the-day rates.”

He added: “Be under no illusion, we don’t want to increase prices, but this is the best choice for us under the circumstances we find ourselves in.”

According to Brazil, the prices have been frozen for four years, and visitors are just being asked to contribute to public services.

Anti-tourist measures have been seen to be sweeping hotspots across the UK and Europe.

Earlier in the year, the GreaterManchesterMayor suggested that an existing optional fee in someManchester citycentrehotelsshould be replaced with a compulsory charge for visitors.

A COCKTAIL chain has fallen into administration, with four sites shutting their doors for good.

Simmons has appointed advisory firm Kroll to oversee the administration, company filings show.

1

Simmons Bars has fallen into administration and will close four sites for goodCredit: Alamy

In its most recent audited account the company posted a loss of £749,000 for the year to end March 2024, reversing a profit of just under £2million the previous year.

Last week Simmons revealed plans to close at least four sites to focus on its best performing venues.

The chain has venues across London and one in Manchester and offers cocktails, brunches and karaoke at its 21 locations.

Last week Nick Campbell, who founded the company in 2021, said the move would “streamline its portfolio and strengthen its financial position”.

He said: “As part of the process, we’ve taken the tough decision to exit four leases, allowing management to focus resources on our strongest performing venues.

“Alongside this, we’ve secured additional investment to support future expansion and operational improvements across the estate.”

Tough times for UK pubs

Many of Britain’s pub and bar chains are feeling the impact of the pandemic and cost of living crisis.

The hike in costs of every day goods has meant that punters have less money to part with at the till.

Meanwhile, hikes to employers’ National Insurance Contributions that were introduced in April have piled further pressure onto businesses that are already struggling.

Last month The Coconut Tree announced that it would be wound down after defaulting on its Company Voluntary Agreement (CVA).

The Sri Lankan restaurant group entered into the agreement last July, according to a report in Restaurant Online.

As a result, the group was required to initially repay £27,000 a month for the first three months.

Meanwhile, Oakman Inns & Restaurants fell into administration, with six sites shutting their doors for good.

It will see a total of 19 sites either sold or closed for good.

Do you have a money problem that needs sorting? Get in touch by emailing [email protected].

THE SKINT celebrities that are struggling to make ends meet – from Dawn O’Porter to Mischa Barton.

Even if you have made lots of money, it doesn’t always mean you’re not going to run into money problems as these celebrities have found out.

Mischa Barton

8

Mischa Barton even sued her mother over moneyCredit: Rex Features

The OC actress Mischa, 39, has had a widely-publicised battle with her former momager, Nuala Barton, over her money.

In July 2015, she even sued her mother, alleging that she lied about how much Mischa was being paid for a film role and pocketed the rest of the cash herself.

She’s also struggled to make mortgage payments on her home in the past, at one point falling five months behind.

Though she eventually sold the Beverly Hills mansion in summer 2016 for $7.05 million reports The BBC.

The television presenter, 46, who has been married to Bridesmaids actor Chris O’Dowd since 2012, has opened up about her money woes.

She expressed to MailOnline: “I work pay cheque to pay cheque. I’m always broke. My card got declined last week. I’m like, what the f*** is happening? When will this end?”

The Scottish writer and director has had a varied career, presenting several documentaries and shows including BBC’s Super Slim Me and How To Look Good Naked on Channel 4.

Meanwhile, Chris, 45, has starred in some of Hollywood’s biggest productions, including This Is 40, Thor: The Dark World, Gulliver’s Travels and St. Vincent.

The couple have two children, sons Art, 11, and Valentine, who is eight years old.

Wife of Hollywood actor claims she’s ‘always broke’ and ‘lives pay cheque to pay cheque’

Lindsay Lohan

8

Lindsay Lohan had her bank accounts seized in 2012Credit: Getty

The Parent Trap’s Lindsay Lohan had her bank accounts seized in 2012, for reportedly owing $234,000 in tax.

Lindsay apparently sent her 18-year-old sister to haggle with second hand stores to make some emergency cash from her old clothes.

Ali Lohan went to the vintage clothing store Wasteland to flog the singer’s most valuable designer gear.

Ali was seen arriving at the Los Angeles store with bags bursting with shoes, clothes and accessories.

But she was reportedly shocked when she was offered a lot less than she was expecting.

She went through items including a pair of Chanel pumps and a Balenciaga handbag, saying: “These have to be worth more, Lindsay was photographed wearing them, that has to add value.”

But the manager would not be swayed, and Ali had to settle much lower than she had planned.

Her Scary Movie 5 co-star, Charlie Sheen, gave her $100,000 towards the bill and Lindsay now appears to have her finances under control.

50 Cent

8

50 Cent declared himself bankrupt in 2015Credit: Getty

50 Cent declared himself bankrupt in 2015, but said the move was a ‘strategic’ one, and not because he’d spent all of his money.

He made the decision after he was sued for leaking a sex tape of Lastonia Leviston, who has a child with his rap rival Rick Ross, and didn’t want other people to follow suit.

He told US talk show host Larry King in 2015L “It’s a move that was necessary for me to make at this point.

“So I didn’t allow myself to create that big red and white bulls eye on my back, where I become the person that people consistently come to.”

He still had to pay off debts of more than $22 million, though, with $6 million going to Lastonia for invasion of privacy.

Shane Richie

8

Shane Richie had to borrow from friends and familyCredit: BBC/Jack Barnes/Kieron McCarron

Back in 2020, the EastEnders legend said the coronavirus pandemic hit him hard and left him begging friends and family for loans.

Shane revealed how the pandemic and years of daft spending had left him “literally skint.”

At the time he was relying on loans from friends and family, and government help to pay his mortgage.

He told the Mirror at the time: “I was going on tour, doing a TV series and panto but it all got cancelled in March. Now I am literally skint!

“You save for a rainy day but you don’t expect the rainy day to last eight months. Thankfully, I’ve been able to borrow money from mates, my family and the bank.”

He added: “I got rid of my car but only cos I lease a car for my wife for the school run. I can get around on a moped.

“I am alright, I have had a career and if it all finishes tomorrow, so be it. If the worst comes to the worst, I’ll do stand-up or resurrect a musical.”

Shane also revealed that he blew thousands on the strangest things, in particular Planet of the Apes memorabilia.

He said: “It was my favourite show as a boy, I couldn’t resist. It harks back to Christmases when mum and dad couldn’t afford much.”

In April 2014, Courtney was hit with a $320,000 tax bill, as well as being ordered to pay $96,000 to a fashion designer she defamed on Twitter.

Later that year, the singer told the Sunday Times, “I lost about $27 million.

“I know that’s a lifetime of money to most people, but I’m a big girl, it’s rock ‘n roll, it’s Nirvana money, I had to let it go.

“I make enough to live on, I’m financially solvent, I focus on what I make now.”

And back in 2021 according to official tax records, theHole lead singerhad five outstanding tax debts that have accumulated from 2017 to 2021.

The iconic artist was hit with three outstanding Internal Revenue Service liens, totaling $1.9 million, while the rest of the debt was owed to the State of California.

The Grammy nominee explained that she was living with her parents for a while in Las Vegas before the situation became unfavourable.

She eventually moved back to Los Angeles after her manager suggested she move in with him for a bit.

But the home was too small so Dawn ultimately resided in a hotel for eight months before deciding to research “car life.”

Following her search, the singer began living in her car in 2022 and said that she “felt free.”

She added: “I felt free. I felt like I was on a camping trip. It just felt like it was the right thing to do.

“I didn’t regret it. You know, a lot of celebrities have lived in their cars.”

The singer admitted that though the experience is sometimes “scary” she’s learned “what to do in my car and how to do it, like, how to cover my windows and you don’t talk to certain people.”

She explained: “You’re careful of telling people that you’re alone, as a woman especially.”

Cat Power had to cancel her European TourCredit: Getty

Charlyn Marie “Chan” Marshall, better known by her stage name Cat Power, is an American singer-songwriter.

She spent a lot of her own money on recording 2012 album, Sun.

Then, when it came time to tour Sun, she took to Instagram to share some bad news with fans.

She wrote: “I may have to cancel my European tour due to bankruptcy & my health struggle with angioedema.

“I have not thrown in any towel, I am trying to figure out what best I can do.”

The tour was indeed postponed, with Chan later adding: “The American tour has been wonderful and amazing, and with me being unable to afford to bring my show with full production (which i helped create), to Europe.

“Financially, really dumped a huge additional amount of stress on me as I was and still am fighting trying to get tour support.”

THOUSANDS on Universal Credit and 11 other benefits can expect early payments this month.

Benefits are paid into your bank or building society account earlier if your usual payment date falls on a bank holiday or the weekend.

1

Universal Credit and 11 other benefits are being paid early this month to some claimantsCredit: Alamy

The nextbank holiday is on Monday, August 25, meaning if you’re expecting a payment on this date it will be made on August 22.

So, if you check your statement on August 22 and notice a surprise amount of money, it will likely be your benefit being issued earlier.

If you are paid earlier than usual this month, make sure the money stretches further as you will have to wait longer than normal to get your next payment.

Universal Credit and 11 other benefits are paid on the first working day before a bank holiday. The full list is:

Anyone paid one of the above 12 benefits on August 22 instead of August 23, 24 or 25, should receive the same amount as usual.

The only reason the payment amount might change is if you have had a change in your circumstances.

For example, if you are on Universal Credit and your earnings have increased, your payment might go down.

If you are expecting a payment on August 22 and don’t receive it, contact the DWP.

You can also submit a complaint to the Government department to get a problem sorted if your payment is wrong.

How does work affect Universal Credit?

After August, there are two more bank holidays before the end of the year which could impact when you receive your benefits.

Entitledto’s free calculator determines whether you qualify for various benefits, tax credit and Universal Credit.

MoneySavingExpert.com and charity StepChange both have benefits tools powered by Entitledto’s data.

You can use Policy in Practice’s calculator to determine which benefits you could receive and how much cash you’ll have left over each month after paying for housing costs.

Your exact entitlement will only be clear when you make a claim, but calculators can indicate what you might be eligible for.

The new plans mean that anyone up to the age of 22 will not be able to claim the health element.

That means people claiming the health element of Universal Credit and new claimants with the most severe conditions will see their incomes protected in real terms.

The Government had put forward that people would need to score four points in one task such as washing and dressing to qualify for support.

Currently they can qualify with eight points across multiple activities.

The Government initially partially u-turned, saying the changes would come into effect in November 2026, but anyone claiming the benefit before this date would not be impacted.

A MAJOR high street bank has become the latest British lender to quit the Net Zero Banking Alliance, the bank said on Friday.

Barclays argued that the departure of several global lenders has left it no longer fit to support the bank’s green transition.

1

Barclays has become the latest British lender to quit the Net Zero Banking Alliance

Barclays’ decision to quit the foremost banking alliance focused on tackling climate change follows on from HSBC and several major US banks.

It also raises questions about the ability of the group to influence change in the sector going forward.

The bank said in a statement on its website: “After consideration, we have decided to withdraw from the Net Zero Banking Alliance.”

It added that its commitment to be net zero by 2050 remained unchanged and that it still saw a commercial opportunity for itself and its clients in the energy transition.

Earlier this week Barclays published the first update on its sustainability strategy in several years.

It said the bank made £500 million in revenue from sustainable and low-carbon transition finance in 2024.

Jeanne Martin, co-director of corporate engagement at responsible investment NGO ShareAction called the decision to leave the Net Zero Banking Alliance “incredibly disappointing and a step in the wrong direction at a time when the dangers of climate change are rapidly mounting.”

Barclays said the alliance was no longer fit for its purpose: “With the departure of most of the global banks, the organisation no longer has the membership to support our transition.”

The Net Zero Banking Alliance, a global initiative launched by the United Nations Environment Programme Finance Initiative, lists more than 100 members on its website – including leading international financial institutions.

A spokesperson for the alliance said it remains focused on “supporting its members to lead on climate by addressing the barriers preventing their clients from investing in the net-zero transition.”

In February, the rate dropped to 4.87%, followed by another cut in April to 4.61%.

In February, the bank reduced the rate to 4.87%, followed by another cut in April to 4.61%.

Now, just months later, rates are set to drop again, leaving savers questioning whether to stick with the account or explore better options elsewhere.

How Barclay Card Changes Could Affect You

ANALYSIS by Consumer Reporter, James Flanders:

Barclaycard’s change to its credit card repayment structure sounds great if you don’t dig into the details.

After all, Barclaycard says it’s “making the changes to give you greater flexibility each month”.

In practice, it means that if you can’t afford to pay off your balance in full at the end of each statement period, you can repay much less under the minimum repayment option than you have done previously.

If you only pay the minimum amounts on occasion, this is super useful.

But if you rely on this type of repayment plan in the long term, it could will cost you hundreds of pounds extra in interest.

It could also negatively affect your credit file as it’ll take you much longer to clear your debt.

More interest will be applied to your outstanding balance, too, as less is paid down each month.

For example, if you have a balance of £5,000 on a Barclaycard at 24% interest, where you only make the minimum payments and don’t spend on the card.

Under the old “2.5% of the balance plus the interest charged” rule, it would take around 14 years to clear the balance.

In total, you’d expect to pay about £3,500 in interest.

But with the new “1% of the balance plus the interest charged” calculation, it will take over 30 years to clear the same balance.

You’d then end up paying a whopping £8,500 in interest.

Before taking out a new credit card or increasing the amount you borrow, it’s vital to consider the consequences.

You should only borrow money if you can afford to pay it back.

It’s always vital to ask yourself if you actually need to borrow before committing to a new credit card, personal loan or overdraft.

If you use a credit card, I’d recommend that you always pay off your balance in full at the end of each statement period.

Lenders have a responsibility to help customers who are in debt.

If you’re in a debt crisis, your first point of call should be your lender.

They might help you out by offering you a reduced interest rate or a temporary payment holiday – so check in with your lender if you’re struggling.

LONDONERS have seen a 75 per cent rise in the “Sadiq Khan stealth tax” during the mayor’s time in office, we can reveal.

The levy — officially known as the mayoral precept — is added to council tax bills in all 32 city boroughs and has risen steadily since the Labour politician’s 2016 election.

For a Band D home, it has jumped from £280.02 in 2017 to £490.38 today.

City Hall Conservative Group leader Susan Hall said: “Sadiq Khan has taxed the life out of our city. Where has it all gone? Crime is out of control, traffic is at a standstill, nightlife is dead, house building’s virtually stopped and the green belt is at risk.

“To paraphrase the president of the USA, he’s a terrible mayor.”

A spokesman for the mayor said a record £1.16billion had been invested in policing this year, providing 935 neighbourhood cops.

He added: “Keeping Londoners safe is Sadiq’s top priority.”

Awkward moment Trump blasts ‘nasty’ Sadiq Khan for ‘terrible job’… before Starmer interrupts: ‘He’s a friend of mine!’

1

Londoners have seen a 75 per cent rise in the ‘Sadiq Khan stealth tax’ during the mayor’s time in office, we can revealCredit: AP

HOMEWARE giant Wayfair has slashed its UK workforce by more than half in just two years, as it grapples with tumbling sales and a sharp drop in profit.

The US-based furniture retailer, which operates across Britain, cut staff numbers from 847 in 2022 to just 405 by the end of 2024, according to fresh filings with Companies House.

2

Retail experts say changing consumer habits, rising costs and weaker demand are continuing to batter the home and furniture sector

The dramatic reduction follows a tough period for the business, with UK turnover plunging from £83.4million in 2022 to just £59.4million last year.

Profits also took a hit, with pre-tax earnings slipping from £2.6million to £2.2million over the same period.

Wayfair said it had made a 17 per cent cut to administrative expenses and was now focused on “driving cost efficiency” and “nailing the basics” as it tried to steady the ship.

Despite the ongoing slowdown, bosses remain upbeat about the retailer’s long-term prospects and said the group is working towards maintaining profitability and generating positive free cash flow.

The wider company reported a net revenue of $11.9billion (£8.8billion) globally last year – down $152million (£112million) on the year before.

International sales fell to $1.5billion (£1.1billion), while revenue in its core US market dropped to $10.4billion (£7.7billion).

Wayfair recorded a net loss of $492million (£363million) despite raking in $3.6billion (£2.7billion) in gross profits.

There was some relief in early 2025, as first-quarter results showed a $1billion (£740million) rise in total revenue, thanks to a modest recovery in US sales.

However, international takings continued to fall, dipping by $37million (£27million) to $301million (£223million).

Iconic department store follows Macy’s and reveals it’s ‘forced’ to close down in weeks after ‘more than a century’

Wayfair isn’t the only retailer feeling the pinch on the high street. Furniture favourite MADE.com collapsed into administration in 2022 after failing to find a buyer, leading to hundreds of job losses.

Habitat also shut down all standalone stores in 2021, moving exclusively online after years of underperformance.

Even major players have been forced to adapt.

Wilko closed its doors for good in 2023 after nearly a century in business, with more than 400 stores shutting and 12,000 staff affected.

Argos has continued to reduce its physical footprint, shutting dozens of standalone shops and moving into parent company Sainsbury’s stores to save costs.

Retail experts say changing consumer habits, rising costs and weaker demand are continuing to batter the home and furniture sector.

Many shoppers have tightened their belts amid soaring bills and higher interest rates, with big-ticket items like sofas and beds often the first to be cut from household budgets.

Wayfair bosses said the company remains “resilient” in the face of economic uncertainty and is pressing ahead with its long-term strategy to streamline operations and stay competitive.

RETAIL PAIN IN 2025

The British Retail Consortium has predicted that the Treasury’s hike to employer NICs will cost the retail sector £2.3billion.

Research by the British Chambers of Commerce shows that more than half of companies plan to raise prices by early April.

A survey of more than 4,800 firms found that 55% expect prices to increase in the next three months, up from 39% in a similar poll conducted in the latter half of 2024.

Three-quarters of companies cited the cost of employing people as their primary financial pressure.

The Centre for Retail Research (CRR) has also warned that around 17,350 retail sites are expected to shut down this year.

It comes on the back of a tough 2024 when 13,000 shops closed their doors for good, already a 28% increase on the previous year.

Professor Joshua Bamfield, director of the CRR said: “The results for 2024 show that although the outcomes for store closures overall were not as poor as in either 2020 or 2022, they are still disconcerting, with worse set to come in 2025.”

Professor Bamfield has also warned of a bleak outlook for 2025, predicting that as many as 202,000 jobs could be lost in the sector.

“By increasing both the costs of running stores and the costs on each consumer’s household it is highly likely that we will see retail job losses eclipse the height of the pandemic in 2020.”

2

Profits also took a hit, with pre-tax earnings slipping from £2.6million to £2.2million over the same period

State Pension (including Graduated Retirement Benefit)

Severe Disablement Allowance (transitionally protected)

Unemployability Supplement or Allowance (paid under Industrial Injuries or War Pensions schemes)

War Disablement Pension at State Pension age

War Widow’s Pension

Widowed Mother’s Allowance

Widowed Parent’s Allowance

Widow’s Pension

If you’re part of a married couple, in a civil partnership or live together, you’ll both get the cash bonus – as long as you both are eligible.

If you or your partner do not get one of the above qualifying benefits, then they could still get the bonus if they are over the state pension age by the end of the qualifying week.

Winter Fuel payment

The Winter Fuel Payment is made every year to help cover the cost of energy over the colder months.

It has been changed in recent months so that fewer can claim.

However, the cash boost, worth up to £300, is still valuable for those who quality – particularly those on Pension Credit.

The cash is usually paid in November and December, with some made up until the end of January the following year.

If you haven’t got your payment by then, you need to call the office that pays your benefits.

Households eligible for the payment are usually told via a letter sent in October or November each year.

If you think you meet the criteria, but don’t automatically get the winter fuel payment, you will have to apply on the government’s website.

The Child Winter Heating Assistance

If you’re based in Scotland, you could receive a child winter heating assistance payment of £255.80.

You get child winter heating payment for a child or young person under 19 who lives in Scotland and who is entitled to:

the highest rate of the care component of child disability payment (CDP) or disability living allowance (DLA), or

the enhanced rate of the daily living component of adult disability payment (ADP) or personal independence payment (PIP).

They must be entitled to the relevant disability benefit during the ‘qualifying week’, which is the week beginning on the third Monday in September (w/c Septmber 15 in 2025).

You do not have to make a claim for the payment, but it should be paid by Social Security Scotland, usually in November.

If you think you’re entitled but have not received payment by the end of December, you should contact Social Security Scotland on 0800 182 2222.

Warm Home Discount

The Warm Home Discount is an automatic £150 discount off energy bills.

As the money is a discount, there is no money paid to you, but you’ll get the payment automatically if your electricity supplier is part of the scheme and you qualify.

You’ll have to be in receipt of one of the following benefits to qualify for one of the payments:

If you don’t claim any of the above benefits, you won’t be eligible for the payment.

Cold Weather payment

Cold weather payments are dished out when temperatures are recorded as, or forecast to be, zero degrees or below, on average, for seven consecutive days between November 1 and March 31.

Eligible Brits are then given extra money to help heat their homes.

You get £25 for each seven-day period where the weather is below zero Celsius on average during this time frame.

You can check if your area has had a cold weather payment by popping your postcode into the government’s tool on its website.

You’ll need to be on certain benefits to qualify, which are:

Student maintenance loans are paid to university students to help cover living costs such as rent.

They are usually paid at the start of each new term, so you typically receive three payments a year.

Maintenance Loans are paid straight into your student bank account in three (almost) equal instalments throughout the year.

The amount you will receive depends on where in the UK you’re from, whether you’ll be living at home or not, your household income and how long you’re studying for.

The average Maintenance Loan is approximately £6,116 a year.

Are you missing out on benefits?

YOU can use a benefits calculator to help check that you are not missing out on money you are entitled to

Entitledto’s free calculator determines whether you qualify for various benefits, tax credit and Universal Credit.

MoneySavingExpert.com and charity StepChange both have benefits tools powered by Entitledto’s data.

You can use Policy in Practice’s calculator to determine which benefits you could receive and how much cash you’ll have left over each month after paying for housing costs.

Your exact entitlement will only be clear when you make a claim, but calculators can indicate what you might be eligible for.

A DRAGON’S Den winner and former Team GB gold medallist fraudulently used Covid loans to buy himself a £1.8million mansion.

Rick Beardsell illegally pocketed £100,000 worth of taxpayers cash to purchase his home – despite receiving a £75,000 investment during his stint on the BBC show.

6

Beardsell received £75,000 in investments after appearing on Dragon’s DenCredit: Cavendish

6

The British world sprinting champion illegally pocketed two Covid Bounce Back business loans to buy himself a £1.8m mansionCredit: Cavendish

6

Beardsell was only entitled to apply for one loan worth £50,000, but fraudulently applied for twoCredit: Cavendish

The 46-year-old fiddled two Covid Bounce Back loans to buy himself five-bed Holly House in the exclusive village of Prestbury, Cheshire.

Dad-of-two Beardsell was only entitled to apply for one loan worth £50,000, but fraudulently applied for two and greatly exaggerated his annual turnover by up to 23 times.

It came after the world champion sprinter had successfully secured investments from TV Dragons Tej Lalvani andDeborah Meadenfor his successful protein shake bottle business, ShakeSphere.

Chester Crown Court heard he applied for the loan to prop up his other company, Sports Creative Ltd, but none of the money went towards the sportswear business.

Prosecutor Geoff Whealan told the court Beardsell made the fraudulent applications to HSBC in December 2020 and then to NatWest in January 2021.

He said: ”The defendant stated on the HSBC form that the turnover of Sports Creative was £485,000 and on the NatWest form said it was £320,000.

“But unaudited financial statements showed turnover for the year end February 2020 was £20,622.

”The turnover was clearly exaggerated to secure the maximum bounce back loan.

“Subsequent transactions showed the bounce back loan funds were not being used for the economic benefit or business purposes of Sports Creative at this time.”

The money arrived in Sports Creative’s account in January 2021, but then almost £400,000 was transferred to Beardsell’s personal Santander account in the space of six months.

Then £431,160.80, including the remaining bounce back loan funds, was transferred to a firm of solicitors for the purchase of Holly House he bought with his wife Ezster.

Mr Whelan added: ”In effect the bounce back loan funds had been used for this purchase.

Shocking moment Dragons’ Den winner Ross Mendham smashes £100k Ferrari after ploughing into bike racks in city centre

“It can be inferred from the defendant’s conduct that it was his intention to use the bounce back loans for this purpose at the time he made the application for it.”

Beardsell, who won two World Records for sprinting, faced three years in jail after he admitted two charges of fraud.

In October 2024, he attended an interview under caution at the Insolvency Services offices.

In a statement he said: ”The guidance pertaining to Bounce Back Loans indicated that the proceeds of such loans may be utilised for any purpose that yields a direct benefit to the company.

”At that juncture, I sought professional advice and was advised that such purposes include, but are not limited to, the coverage of overhead expenses or outstanding liabilities, as well as the investment in company assets or property.

“The funds that were transferred to my personal account constituted a director’s loan and other economical overheads for the business.”

Mitigating, his counsel Nichola Cafferkey explained that the loans had been repaid in full to the banks.

She said: ”The loss of his good character is of some significance in respect of a man who has dedicated his life to his family, his professional entities and also his sporting endeavours.

“These offences were out of character and were committed four years ago.

“He has taken responsibility and repaid the money back. He knows that it’s his own fault.

“He has brought shame on his family and brought shame on himself.

”His wife is also his business partner and concerns that they have had about the ability to provide financially for their young children have been significant.”

The court also heard that Beardsell had suffered a series of medical issues both before and after securing the loans.

Ms Cafferkey continued: “A year prior to the submission of the first loan application, the defendant was diagnosed with an aggressive form of testicular cancer and required surgery and extensive chemotherapy.

“The chemotherapy was successful but led to some significant side effects.

”One of those being vertigo, of which he had a severe episode which required hospitalisation and thereafter there are ongoing long-term issues as a result of that.

6

Beardsell was sentenced to 18 months in prison, suspended for two yearsCredit: Cavendish

6

Hundreds of thousands of pounds were transferred to a firm of solicitors for the purchase of Holly HouseCredit: Cavendish

“The investigations brought on by the defendant’s own actions has had an impact on his family which has led to a situation where he has been experiencing significant stress over the past few years.

“On top of that there are ongoing knee pains associated with his athletic success at national and international level.

“He has been running a business for many years without issue and it is plain he is extremely remorseful and regretful for his actions.

“The impact on his wife’s physical health in terms of stress and strain has been significant. There has been significant weight loss and insomnia.

“This will be the only time that Richard Beardsell appears before the court.”

Beardsell was sentenced to 18 months in prison, suspended for two years.

He was also ordered to complete 250 hours of unpaid work and pay costs of £11,142.70.

Judge Simon Berkson told Beardsell: “You fraudulently lied and lied again in your applications for these loans.

“They were supposed to be for use in keeping your business running but the money was used for your own personal needs and the needs of your family.

“This is not a victimless crime. The government was trying to help struggling businesses at the time of national crisis.

“People were in lock down, people were dying and people were very ill at the time when people required their public services.

“You used fraudulently obtained public funds for your own use, depriving honest people of the scheme’s funds when the country was in crisis.

“You are a generally successful man both in business and in sports, particularly your involvement with athletics.

“You continue to run your business and it was on the TV programme Dragons’ Den.

“You are a married person with two children and they are young children. You have survived an aggressive form of cancer.

“I have concluded that an immediate custodial sentence would have a significant harmful impact on your wife and children.”

6

He was ordered to complete 250 hours of unpaid work and pay costs of £11,142.70Credit: Cavendish

Cropped shot of a woman holding a basket while shopping at a grocery storeCredit: Getty

But there are ways to drive down the cost of your weekly shop, starting with help through the Household Support Fund (HSF).

The £742million fund has been shared between councils in England who then decide how to allocate their share.

Some are directing cash payments to residents in need while others are distributing supermarket vouchers to cover the summerholidays.

We’ve rounded up what some local authorities are offering below.

We won’t have covered all the councils offering help, so if your local authority isn’t included it’s worth checking with it to see what you are eligible for.

Most councils have pages on their websites dedicated to the Household Support Fund where you’ll find details on who is eligible and what you’re in line for.

You can find what local council area you fall under by visiting www.gov.uk/find-local-council.

That said, below are some of the councils offering qualifying households supermarket vouchers.

Bracknell Forest Council

Schools in Bracknell are automatically distributing supermarket vouchers to children registered for free school meals.

These vouchers have been paid for through Bracknell Forest Council’s allotment of the Household Support Fund.

Families can get FREE washing machines, fridges and kids’ beds or £200 payments this summer – and you can apply now

The council has not confirmed how much the vouchers are worth.

Wakefield Metropolitan District Counci

Wakefield Metropolitan District Council is issuing supermarket vouchers worth £50 to families receiving council tax support.

The vouchers are being issued via letters on July 21 and take up to seven days to arrive.

Full instructions on how to redeem the vouchers will be included in the letters.

Once the voucher has been redeemed, it doesn’t have to be used all at once and can be used several times until it is spent.

Nottingham City Council

Nottingham City Council is distributing £75 supermarket vouchers to households each month until March 2026.

There is a limit on the number of vouchers being shared each month meaning you have to act fast to claim one.

Applications for this month’s vouchers opened on July 7 so may all have been allocated for July.

Nottingham City Council has said the dates applications for vouchers will open between August and next March will be confirmed “later in July”.

The vouchers are worth £90 per child meaning you could get £180 if you have two kids.

You don’t need to apply for the vouchers as they are being sent automatically to emails or as letters.

The council’s partner, Blackhawk, is issuing a 16-digit personalised code and instructions on how to redeem the vouchers on the Blackhawk website – ealingcouncil.select-your-reward.co.uk.

Devon County Council

Devon County Council has issued supermarket vouchers worth more than £90 to 22,000 families with children on free school meals.

The £90 is equivalent to £15 per week for the six week school holiday.

The council has said the vouchers can be redeemed in major supermarkets but hasn’t said which ones.

Portsmouth City Council

Portsmouth City Council is issuing £50 supermarket vouchers to children on benefits-related free school meals.

You might also be eligible if your child is not on free school meals and you’re on a low income, and can apply for the vouchers from the end of the school term.

You can also forward your email address to the council and will be contacted when the application window opens.

More details can be found via www.portsmouth.gov.uk/services/benefits-and-money-advice/help-and-support/money-advice/household-support-fund.

Bournemouth, Christchurch and Poole (BCP) Council

Families on free school meals are eligible for supermarket food vouchers being distributed by schools in the area.

You do not need to apply as they are being issued automatically.

Food vouchers may also be available for children under five years if certain criteria is met.

To receive a voucher, children must be living in Bournemouth, Christchurch, or Poole and meet one of the following criteria:

currently claiming 2 year old early education funding at an early years setting in Bournemouth, Christchurch or Poole during the term

currently claiming Early Years Pupil Premium funding for 3 and 4 year olds at an early years setting in Bournemouth, Christchurch or Poole during the term (this is different to the early education funding available to all 3 and 4 year olds)

currently have an open case with a social worker or Early Help family support worker and are of pre-school age

Food vouchers for this group of families have to be applied for, with more details on the BCP Council website.

Household Support Fund explained

Sun Savers EditorLana Clementsexplains what you need to know about the Household Support Fund.

Sun Savers Editor Lana Clements explains what you need to know about the Household Support Fund.

If you’re battling to afford energy and water bills, food or other essential items and services, the Household Support Fund can act as a vital lifeline.

The financial support is a little-known way for struggling families to get extra help with the cost of living.

Every council in England has been given a share of £421million cash by the government to distribute to local low income households.

Each local authority chooses how to pass on the support. Some offer vouchers whereas others give direct cash payments.

In many instances, the value of support is worth hundreds of pounds to individual families.

Just as the support varies between councils, so does the criteria for qualifying.

Many councils offer the help to households on selected benefits or they may base help on the level of household income.

The key is to get in touch with your local authority to see exactly what support is on offer.

The last round ran until the end of March 2025, but was extended.

The most current round is running between April 2025 and March 2026.

Do you have a money problem that needs sorting? Get in touch by emailing [email protected].

MOST UK supermarkets have loyalty schemes so customers can build up points and save money while they shop.

Here we round up what saving programmes you’ll find at the big brands.

Iceland: Unlike other stores, you don’t collect points with the Iceland Bonus Card. Instead, you load it up with money and Iceland will give you £1 for every £20 you save.

Lidl Plus: Lidl customers don’t collect points when they shop, and are instead rewarded with personalised vouchers that gives them money off at the till.

Morrisons: The My Morrisons: Make Good Things Happen replaces the More Card and rewards customers with personalised money off vouchers via the app.

Sainsbury’s: While Sainsbury’s doesn’t have a personal scheme, it does own the Nectar card which can also be used in Argos, eBay and other shops. You need 200 Nectar points to save up £1 to spend on your card. You need to spend at least £1 to get one Nectar point.

Tesco: Tesco Clubcard has over 17million members in the UK alone. You use it each time you shop and build up points that can be turned into vouchers – 150 points gets you a £1.50 voucher. Here you need to spend £1 in Tesco to get one point.

Waitrose: myWaitrose also doesn’t allow you to collect points but instead you’ll get access to free hot drinks, and discounts off certain brands in store.

2

One shopper was so ecstatic she posted a receipt of her purchase online to prove her savingsCredit: Facebook/@Extreme Couponing and Bargains UK group

BLACK Sabbath fans were left stunned by sky-high prices at Villa Park – with a pint setting punters back up to £8 during the legendary band’s final hometown gig.

The Back to the Beginning supershow, held at Aston Villa’s stadium in Birmingham, marks Ozzy Osbourne’s last ever live performance – and the first time the full band have played together in two decades.

5

Bill Ward, Ozzy Osbourne, Terry Butler and Tony Iommi of Black Sabbath

5

Black Sabbath fans arrived at Villa Park, queuing in long lines to enter the stadium – but for many, the bar and food prices were nearly as jaw-dropping as the music itself

5

Inside the venue, a pint of Poretti lager was going for £8, with a half pint at £4. A pint of Somersby cider wasn’t far behind at £7, or £3.50 for a half

But for many fans, the bar and food prices were almost as jaw-dropping as the music.

Inside the venue, a pint of Poretti lager was going for £8, with a half pint at £4.

A pint of Somersby cider wasn’t far behind at £7, or £3.50 for a half.

Cocktail fans after something stronger had to fork out £13 for a draught Rum Punch – while even a bottle of water cost £3.50.

In the Doug Ellis stand, the prices were just as steep – with a Carlsberg Pilsner priced at £6.50, a glass of wine for £7, and both a gin and tonic and a vodka lemonade costing £7.50 each.

And it wasn’t just the drinks that had fans digging deep.

Food options were limited and pricey too – with a sausage roll setting you back £5, a steaky pasty £6.50, and Yardbirds chicken and chips costing a whopping £15.

Even the basics weren’t cheap – a can of Coke was £3.50, a bar of chocolate £2.50, and a bag of Walkers crisps £2.20.

Fancy a hot drink? That’s £3.95 for a tea and £4.50 for an espresso.

Fans weren’t impressed.

Some took to social media to vent their frustration, saying the prices were “festival-level rip-offs” and that it “left a bad taste before the music even started”.

One gig-goer told us: “I knew it’d be expensive but £8 for a pint and £7 for chips? That’s taking the Mick.”

Another said: “You expect a bit of markup, but this is madness.

Ozzy’s not the only one going out with a bang – so is my bank account.”

The backlash over food and drink prices follows recent criticism surrounding the cost of VIP meet-and-greet packages with Ozzy Osbourne, set to take place during his upcoming appearance at Comic Con Midlands.

Fans are being charged £666 for the ‘Ultimate Sin’ VIP package – which includes a group photo with Ozzy, Sharon, Kelly, and Jack. But only two people are allowed per photo (except under-5s).

Want an autograph? That’ll cost extra.

Ozzy will sign a book for £225, or a poster, album or toy for £375. And if you want him to sign your guitar or mic?

That’ll be £750 – bringing the total package cost to £1,416.

Fan backlash has been fierce. One wrote: “Laughable prices, genuinely laughable.”

Another joked: “Time to start selling me kidney.”

While fans might be fuming over costs, the buzz inside Villa Park is electric.

This is a historic night – the last time Birmingham’s own heavy metal gods will share the stage in their hometown.

Ozzy, who’s battled serious health issues in recent years, admitted he won’t be performing a full set.

He said: “We’re only playing a couple of songs each.

“I don’t want people thinking ‘we’re getting ripped off’, because it’s just going to be … what’s the word? … a sample.”

He added: “I’ll be there, and I’ll do the best I can. So all I can do is turn up.”

The Back to the Beginning festival line-up is packed with legends, including Metallica, Slayer and Pantera – all joining in to celebrate Black Sabbath’s final bow.

Fans from across the UK – and some flying in from overseas – have packed out the stadium to say one last goodbye to the band that helped invent heavy metal.

5

Inside the venue, a pint of Poretti lager was going for £8, with a half pint at £4. A pint of Somersby cider wasn’t far behind at £7, or £3.50 for a half

5

Backlash over pricey pints comes after criticism of Ozzy’s £666 VIP packages

M&S has made a huge change at all cafes and shoppers will be fuming.

Prices at the Percy Pig makers in-store cafes have risen by up to 20%, with the cost of a Gastro Fish & Chips meal increasing by £2.

1

M&S has raised prices across its in-store cafesCredit: Alamy

It’s beer battered fish, served with chips, petit pois and tartar sauce used to cost £9.95 in August 2024.

But its most updated menu for June 2025 shows the cost of the beloved British dish has risen to £11.95 across sites.

The price of a single portion of chips at the cafe has also increased by 50p, now costing £2.50.

And fans of its brekkie are forking out more too.

M&S’s All Day Big Breakfast, served with sausages, bacon, soft poached eggs, tomatoes, potato rosti, baked beans and toast, used to cost £9.50.

But punters are now paying an extra 45p for the hefty morning meal.

Elsewhere, toast with jam and butter now costs £3.75 up from £3.50 and a breakfast ciabatta’s was £4.95 but now costs £5.25.

The posh retailer has also shaken up what is served on menus, axing its nutty granola bowl priced at £4.25.

This has been replaced with a Berry Bliss granola bowl that costs 70p more.

An M&S spokesperson told The Sun: ” We’re committed to providing trusted value for our customers by mitigating and offsetting as much of the current food inflation as we can.

Shoppers race to M&S as one of their best selling items which is a mum-essential viral are scanning for just 63 PENCE

“We are working hard to ensure we offer a wide range of price points and options for our customers, never compromising on the M&S quality they expect.”

It is not uncommon for restaurants, cafés and grocery stores to raise prices due to increased operational costs, including hikes to National Insurance contributions and wages.

Shoppers were outraged after it was discovered a 170g of the iconic sweet treat had been hiked by 10p, now costing £2.

The bestselling sweets have undergone a 33% price hike since 2017 when a packet cost just £1.50.

MORE PRICE RISES

M&S is not the only retailer hiking costs for customers.

Earlier this year, Morrisons also increased the cost of a number popular menu items in its cafés.

The Full Breakfast was hiked by 25p to £7, while its sweet Stacked Pancakes have risen by £4.25 to £4.50.

The price of a Ultimate Fish, Chips & Mushy Peas has increased by £7.75 to £8.50.

Meanwhile, battered sausages, chips and mushy peas increased from £6 to £6.50.

Greggs increased the price of a sausage roll to £1.30 nationally at the start of the year.

The rise means that the Brit favourite jumped by more than a third since it cost £1 in 2022.

At some travel locations, such as London Bridge, the price of a sausage roll has increased from £1.50 to £1.55.

Elsewhere, Costa Coffee has hiked the price of a brew across its hospital concessions.

An audit by our investigators found that a small latte or cappuccino costs £3.90 and a medium £4.10 at Medivest’s Royal Victoria Infirmary’s Costa Coffee outlet in Newcastle.

CHEAP Chinese firms could soon be cut out from government contracts under new rules championing British industry, The Sun can reveal.

Ministers want to prioritise UK-based firms in critical sectors like steel, energy, and cyber, putting them at the front of the queue.

The shake-up would allow the public sector to sidestep foreign tender bids, giving homegrown heroes a bigger slice of Whitehall’s £400bn procurement pot.

Currently, foreign suppliers can undercut British businesses with cheap labour and rock-bottom prices.

But in a push to bolster national security and create jobs across the UK, the likes of British Steel would be prioritised.

Under the new blueprint, now up for consultation, Whitehall departments would also favour British Steel for the £725bn of infrastructure spending earmarked for the next decade.

Meanwhile, firms slow to pay small and medium businesses will be kicked out of the procurement race.

Chancellor of the Duchy of Lancaster, Pat McFadden, said: “Strong industry is essential to our national security.

“The new rules being considered will give us the power to protect our national industries, ensuring more money goes to them as we buy goods and services in government.

“Our reforms will boost growth and ensure British industry is supported to deliver national security and our Plan for Change.”

Gareth Stace, UK Steel boss, hailed the move as a game-changer, saying: “The publication of this guidance for steel procurement and the launch of the consultation are unequivocally positive news for the UK steel industry.

“These changes rightly recognise the strategic importance of steelmaking to national security and the vital role of resilient domestic supply chains.”

MPs urgently recalled to Parliament over national crisis as emergency law must be passed TODAY to save major UK industry

1

Cheap Chinese firms could soon be cut out from government contracts under new rules championing British industries such as steelCredit: Getty

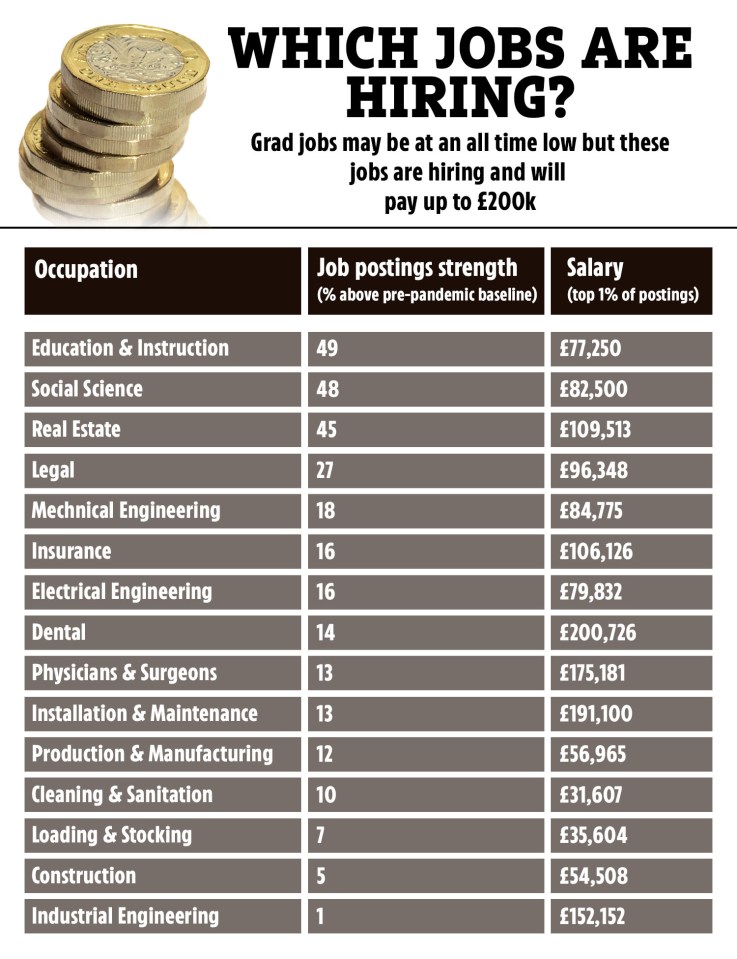

GRADUATES are facing the toughest jobs market in eight years but some industries are bucking the trend and paying big.

New data from the Indeed Hiring Lab reveals graduate job ads are down 12% compared to last year and even worse than during the pandemic.

2

Research shows there are sectors hiring which offer some seriously high wages

In fact, grad roles are now at their lowest point since at least 2018, as employers hold onto staff and cut back on new hires.

But it’s not all doom and gloom. Indeed’s mid-year labour market update shows there are sectors hiring and they’re paying some seriously high wages, with top jobs offering up to £200,000 a year.

Expert Jack Kennedy, senior economist at Indeed, said: “The UK labour market started 2025 with serious headwinds but rather than crash, it’s seen a gradual softening.

“While hiring appetite is weak, job losses have remained modest. The big challenge now is for new entrants like graduates, who are finding it tough to get a foot in the door.

“But sectors like education and real estate are still hiring in big numbers and roles offering flexibility, like hybrid or remote jobs, are holding up too.”

Here, we reveal the fastest-growing job sectors in the UK right now and the top salaries workers could earn.

2

Education & instruction – up 49%

The education sector has seen the biggest increase in job postings, with demand up by 49% compared to pre-pandemic levels. Top earners in this field can make up to £77,250.

This surge is largely due to a national shortage of teachers, particularly in subjects like science, maths and special education.

With government initiatives encouraging more people to enter teaching, there are more opportunities than ever, not just for qualified teachers but also for teaching assistants and support staff.

Entry-level roles such as teaching assistants, cover supervisors, and graduate trainee teachers are also in high demand,

Sam Thompson’s huge new job revealed – and there’s an Ant and Dec link

Social science – up 48%

Closely following education, social science roles have grown by 48%. The top 1% of salaries reach £82,500, with many positions available in areas like policy research, community development, psychology, and criminology.

Graduates with degrees in sociology, psychology, and public policy are finding more roles in local government, charities and think tanks.

Real estate – up 45%

The real estate sector has posted a 45% rise in job listings. It’s a lucrative industry too, with top earners bringing in £109,513.

The UK property market remains resilient, with growth in both commercial and residential lettings.

Many graduates can break into the industry through roles like lettings negotiators, property administrators, and junior estate agents, where commissions can quickly boost take-home pay.

Legal – up 27%

Legal roles have seen a 27% increase in demand, with the best-paid positions offering up to £96,348.

This growth is being driven by a backlog of court cases and rising demand for legal advice in areas such as employment, family law, and corporate compliance.

Law graduates, paralegals and legal support staff are in demand across both private firms and public sector bodies.

The legal sector has also seen growth in remote roles, making it more accessible for early-career professionals.

Mechanical engineering – up 18%

Mechanical engineering continues to be a growth area, with a hiring increase of 18%. Top salaries in this field can reach £84,775.

As the UK focuses more on infrastructure, robotics, and renewable energy projects, mechanical engineers are needed in sectors ranging from automotive to aerospace and manufacturing.

Those at the start of their careers might look at field service technician roles, control panel engineering, or graduate engineer positions, especially as the UK invests in EV infrastructure and smart grids.

Insurance – up 16%