Coinbase may owe customers up to $400 million after hackers steal confidential data.

And with ByBit being duped for $1.5 billion in March, this marks the second major centralized exchange exploit in two months. As such, traders are fleeing to secure self-custody crypto wallets like Best Wallet.

Coinbase Hackers Steal Customer Data

According to a Coinbase tweet, “rogue overseas support agents” handed over customer data, including names, addresses, emails, and official government documents, to hackers.

Coinbase revealed that less than 1% of monthly active accounts were compromised, and that no passwords, private keys, or funds were exposed.

Cyber criminals bribed and recruited rogue overseas support agents to pull personal data on <1% of Coinbase MTUs. No passwords, private keys, or funds were exposed. Prime accounts are untouched. We will reimburse impacted customers. More here: https://t.co/SidVn59JCV

Its CEO CEO Brian Armstrong publicly addressed the situation on X, revealing that the hackers have demanded a $20 million ransom. Rather than folding, Coinbase announced a $20 million reward fund that will pay anyone for information that leads to the hackers’ arrest and conviction.

He underlined that the hackers aimed to use the data for phishing scams. That is, to impersonate Coinbase support agents and trick users into handing over their funds or more valuable account information.

Armstrong said that Coinbase will reimburse any users who lost funds resulting from the hack. He estimates this could cost the company up to $400 million.

Coinbase’s stock dropped by 7.2% after news broke.

However, some critics are concerned that the ramifications of this exploit run deeper. Operational security (OPSEC) is crucial in crypto, and people can be targeted in real life if they are known to hold large amounts of digital assets.

Reuters reported that Ledger co-founder David Balland was kidnapped in France in January and held for ransom until he was rescued in a police operation, for example.

OPSEC-aware crypto users are well aware of this danger, and so are concerned.

“The combination of data exposed here (real-life addresses, crypto addresses, and amount and real-life ID documents) is lethal,” wrote Lefteris Karapetsas on X.

Meanwhile, Nansen AI CEO Alex Svanevik called for US President Donald Trump to “dismantle the KYC/AML complex.”

It’s time for @realDonaldTrump to dismantle the KYC/AML complex.

All it does is compromise personal data for regular people – at an immense cost. Meanwhile practically no real criminals are caught.

Dismantling KYC regulations would mean exchanges could hold less customer data, helping protect their privacy.

However, users can already protect their privacy through KYC-free crypto wallets. And right now, Best Wallet appears as one of the most secure options.

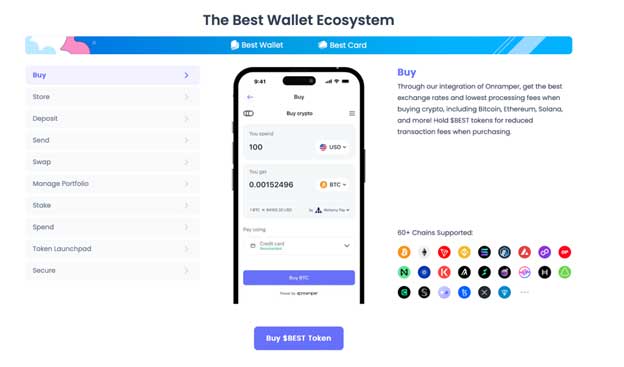

Best Wallet Brings Unmatched Security to the Wallet Space

Best Wallet is a KYC-free crypto wallet with a seamless user experience and market-leading security.

Being KYC-free means Best Wallet users retain complete privacy and hackers can’t steal their data.

But it doesn’t stop there. The wallet employs advanced fraud protection to help flag and block crypto scams. It also uses multi-level cryptographic technology for decentralized account recovery. This includes integrating support for Apple and Google accounts, so that users can easily retrieve access to their wallet, even without knowing their private keys.

When it comes to user experience, Best Wallet’s offerings go well beyond those of its peers. The wallet supports over 60 different blockchains, including Bitcoin, Ethereum, Solana, XRP, and Cardano. It also has a cross-chain DEX and even supports derivatives trading.

In addition, the wallet boasts features like a token launchpad, a crypto debit card, a staking aggregator, an NFT gallery, and more.

While making crypto much safer, Best Wallet also creates a seamless and frictionless user experience. It looks like it’s building the future of Web3.

$BEST Presale Soars Past $12M as Wallet Narrative Deepens

The Best Wallet Token offers ecosystem benefits, including trading fee discounts, higher staking yields, governance rights, and access to promotions on partner projects.

It’s currently available to buy via a token presale, which has raised $12.3 million so far.

Best Wallet Token’s presale strength signifies real market appeal, and the recent Coinbase incident will only amplify this in the months ahead.

Expert analyst Jacob Bury explored the Coinbase hack and suggested that Best Wallet Token could be a smart investment to capitalize on the current market outlook.

As such, traders seeking the most value for money should not wait to get involved.

This article is for informational purposes only and does not provide financial advice. Cryptocurrencies are highly volatile, and the market can be unpredictable. Always perform thorough research before making any cryptocurrency-related decisions.

One problem that promoters of cryptocurrencies have faced since the asset class first emerged is that its reputation stinks.

Crypto trading has become identified by regulators and in the public mind as a haven for scams, theft and other forms of sharp practice. The FBI, in its most recent annual report on cryptocurrency, found that crypto-related fraud has exploded. Criminality is “pervasive” in the field, the agency warned.

The elusive use case for crypto assets seemed to have been narrowed down to facilitating criminal fraud, ransomware attacks, drug and human trafficking.

Trump’s cryptocurrency ventures are nothing more than a fig leaf for pay offs from foreign nationals.

— Sen. Richard Blumenthal (D-Conn.)

Then came Donald Trump. During the presidential campaign and after his election, crypto promoters thought they were entering the nirvana of officially recognized legitimacy.

Trump signaled that he would end government regulatory initiatives on crypto, “in order to promote United States leadership in digital assets and financial technology while protecting economic liberty,” to quote the executive order he issued Jan. 23, effectively wiping out federal regulations on the class.

Newsletter

Get the latest from Michael Hiltzik

Commentary on economics and more from a Pulitzer Prize winner.

You may occasionally receive promotional content from the Los Angeles Times.

Things aren’t working out as they hoped. Since Trump returned to the presidency, his and his family’s involvement in crypto-related deals has critics charging that crypto has become an entirely new path for official corruption and conflicts of interest in the White House.

“Trump’s cryptocurrency ventures are nothing more than a fig leaf for payoffs from foreign nationals & foreign gov’ts,” Sen. Richard Blumenthal (D-Conn.) tweeted on May 7. Blumenthal’s target was the offer of a sit-down private dinner with Trump scheduled for May 22 at his Virginia golf club, and personal tours of the White House for the biggest buyers of $TRUMP, a “memecoin” assiduously promoted by Trump and his family.

The price of the coin soared to about $74 on Jan. 19, the day before Trump’s inauguration. It immediately fell in value, though its price has been propped up by the offer of the dinner and tours; the most recent quotes place it at about $13. The top 220 holders of the Trump coin, who are entitled to the dinner, spent nearly $148 million for the privilege, according to an estimate by Reuters.

More than half of the biggest holders appear to be foreign entities, according to an analysis by Bloomberg. That implies that the purchases might be designed to circumvent federal laws barring foreigners from making political contributions in the U.S.

Democratic Sens. Adam Schiff of California and Elizabeth Warren of Massachusetts demanded that the federal Office of Government Ethics, an independent executive branch agency, open an inquiry into the “severe risk that President Trump and other officials may be engaging in ‘pay to play’ corruption by selling presidential access to individuals or entities, to include foreign nationals and corporate actors with vested interests in federal action, while personally enriching the President and his family.”

DWF, a crypto firm based in the United Arab Emirates, announced last month that it had bought $25 million in coins issued by the Trump-affiliated firm World Liberty Financial, in part to “enhance regulatory engagement with U.S. policymakers.” Freight Technologies, a Houston logistics company, announced April 30 that it had borrowed $20 million to buy Trump coins, calling the transaction “an effective way to advocate for fair, balanced, and free trade between Mexico and the US.”

The unease has spread to Republicans on Capitol Hill, who fear that the Trumps’ crypto deals will undermine their efforts to enact crypto-friendly regulations.

“This gives me pause,” Sen. Cynthia Lummis (R-Wyo.), a leader in the legislative movement to pass a pro-crypto law, told NBC News. “Even what may appear to be ‘cringey’ with regard to meme coins, it’s legal, and what we need to do is have a regulatory framework that makes this more clear, so we don’t have this Wild West scenario.”

Trump’s activities already have derailed, if temporarily, the so-called GENIUS Act, which would regulate a form of cryptocurrency known as “stablecoins,” which are supposedly pegged to the value of underlying currencies such as dollars. Schiff and eight other Senate Democrats who had supported the measure have bailed on it, making passage in its current form virtually impossible.

Democrats in both chambers have introduced the “End Crypto Corruption Act,” which would bar the president, vice president, members of Congress and high-level executive branch appointees from issuing, sponsoring or endorsing any “cryptocurrency, meme coin, token, non-fungible token, stablecoin, or other digital asset that is sold for remuneration.”

Even some crypto promoters are no happier than the politicians. “They’re plumbing new depths of idiocy with the memecoin launch,” Nic Carter, a crypto investor and Trump supporter, told Politico.

As a crypto category, memecoins are disdained even by many participants in the field. They generally have even less utiilty or authenticity than mainstream cryptocurrencies, often originate as joke investments, and ride waves of pure hype. The Trump coin has no discernible value apart from its identification with Trump himself.

I asked the White House for comment on the accusations of corruption and received this reply from spokeswoman Karoline Leavitt: “President Trump is compliant with all conflict-of-interest rules, and only acts in the best interests of the American public.”

The memecoin isn’t Trump’s only venture into crypto, though some of his arrangements seem designed to give him plausible deniability if legal or ethics questions are raised. World Liberty Financial, which markets a crypto token designated $WLFI and a stablecoin designated USD1, is 60% owned by Trump and members of his family, who are entitled to up to 75% of the proceeds of sales of $WLFI.

The firm’s website features an image of Trump striking a heroic pose and says the WLFI token is “inspired by Donald J. Trump.” In the small print it asserts, however, that “any references to or quotes or imagery attributed to or associated with Donald J. Trump or his family members should not be construed as an endorsement or representation or warranty.”

Crypto investors really stepped up to the plate with political donations during the 2024 election cycle. Fairshake, the super PAC representing the class, spent nearly $41 million in contributions. That included $13 million to defeat two congressional candidates in Democratic primaries, Rep. Katie Porter (D-Irvine) and Rep. Jamaal Bowman (D-New York). Both were known to favor stricter regulation of the asset class, and both lost their races.

The biggest crypto firms spent lavishly in 2023 and 2024 to fatten Fairshake’s war chest, which collected more than $162 million in that time frame; Coinbase contributed $46.5 million, Ripple Labs, $45 million and Andreessen Horowitz, a major crypto investor, $44 million. Much of the total was funneled to two other crypto-related political action committees, according to federal election records.

After the election, many of the firms, like more traditional businesses, made contributions of $1 million or more to Trump’s inauguration fund.

One can hardly deny that the crypto camp has gotten its money’s worth from the Trump administration so far. The Securities and Exchange Commission has dropped or deferred more than a dozen enforcement cases against Ripple, Coinbase, Gemini, Kraken and other crypto promoters.

The largest victory arguably belongs to Coinbase, the biggest crypto trading platform in the U.S. The SEC in 2023 charged the firm with running an unlawful trading exchange and marketing unregistered securities. The case reflected the SEC’s position that what crypto firms are marketing are securities by a different name, and thus need to be registered as securities so buyers and sellers get the same legal protections as stock and bond investors.

Crenshaw noted that the deal was part and parcel of the SEC’s effective abandonment of crypto regulation. “This settlement, alongside the programmatic disassembly of the SEC’s crypto enforcement program, does a tremendous disservice to the investing public,” she wrote.

That won’t be the end of the deregulation drive. On April 7, Deputy Atty. Gen. Todd Blanche — who was Trump’s defense attorney in the New York criminal case that resulted in guilty verdicts on 34 felony counts of falsifying business records — ordered an end to Justice Department regulatory cases based on interpreting crypto assets as securities or commodities. That closed down the government’s principal regulatory initiative against crypto promoters.

Blanche directed the DOJ’s Market Integrity and Major Frauds Unit to “cease cryptocurrency enforcement,” and disbanded the National Cryptocurrency Enforcement Team, “effective immediately.”

There doesn’t seem to be any sign that Trump’s involvement with crypto will slow down even as he disembowels the government’s regulatory capacity over crypto ventures.

World Liberty Financial recently announced that Abu Dhabi would use its stablecoin to invest $2 billion in Binance, a multinational crypto firm that pleaded guilty and paid a $4.3-billion penalty in 2023 on charges of financial crimes including money laundering. Binance’s chief executive, Changpeng Zhao, also pleaded guilty and spent four months in U.S. prison.

On its investor advice webpage, the SEC used to post a warning on its website about crypto. “Trendy investments are especially ripe for fraudsters so be aware there is a real risk of fraud,” it said. “Cryptocurrencies may be today’s shiny, new opportunity but there are serious risks involved.”