California’s proposed billionaire tax gains majority support in new poll, with a partisan split on voter ID

SACRAMENTO — A new poll shows California voters are sharply divided over two brewing statewide ballot measures stirring up the nation’s partisan and economic divides: a one-time tax on billionaires to pay for mostly healthcare and a voter ID mandate that includes citizenship verification.

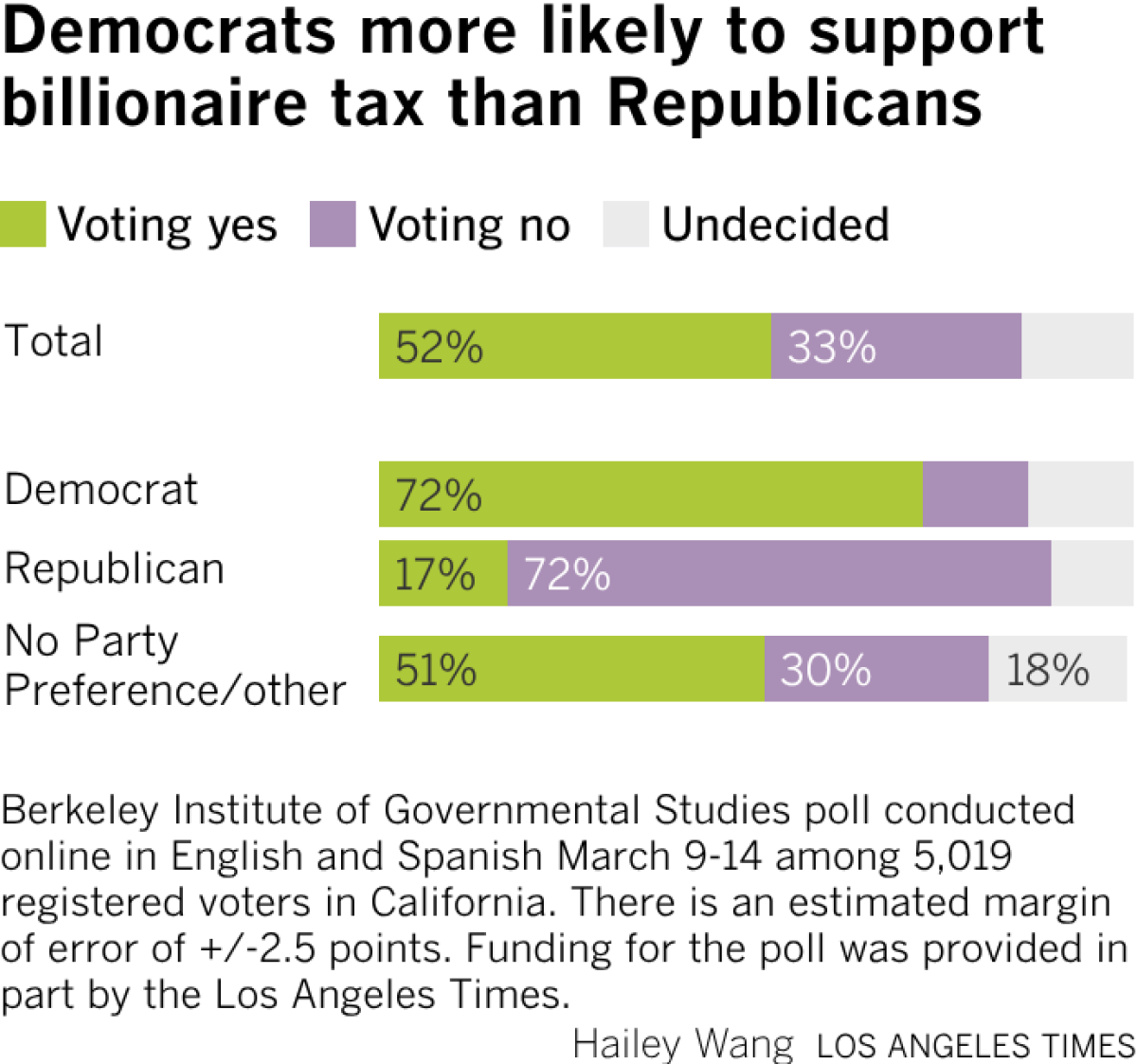

The survey conducted by UC Berkeley’s Institute of Governmental Studies and co-sponsored by The Times showed 52% of registered voters supported the billionaire’s tax, while 33% said they opposed it. Fifteen percent were undecided.

Support for the voter ID measure was more evenly split, with 44% of voters in support, 45% opposed and the remainder undecided.

The pair of statewide proposals, which have yet to qualify for California’s November ballot, emanated from opposite sides of California’s political spectrum. Organized labor and progressives are pushing hard for a new wealth tax in response to Republican cuts to federal healthcare programs, and the GOP-led call for additional voter restrictions comes in the wake of President Trump’s baseless claims that the 2020 election was stolen from him.

Poll director Mark DiCamillo said he “was a little surprised” by the results given how much attention each measure has already received.

“Just from reading the press accounts of these initiatives, I thought they would both be well ahead. There’s been a lot of discussion about them and advocates seem to be very confident in their chances of passage, but the polls seem to indicate otherwise,” he said.

The divisions over each measure fell largely along partisan and ideological lines.

On the billionaire’s tax initiative, 72% of Democratic voters said they would support the measure if the election were held today — and the same percentage of Republicans oppose it. A slim majority — 51% — of voters who are unaffiliated or registered with another party support the wealth tax, while 30% said they oppose it, with the remainder undecided.

Republican voters overwhelmingly support the voter ID initiative, with 91% saying they would vote for it. More than two-thirds of Democratic voters, 68%, said they would oppose the measure. No party preference voters appeared evenly split.

Neither ballot measure has officially qualified for the November ballot thus far, though proponents of the voter ID measure said this month that they turned in 1.3 million voter signatures to elections officials, well above the 875,000 required to qualify. Proponents of the new tax on billionaires have until June 24 to submit signatures to elections officials.

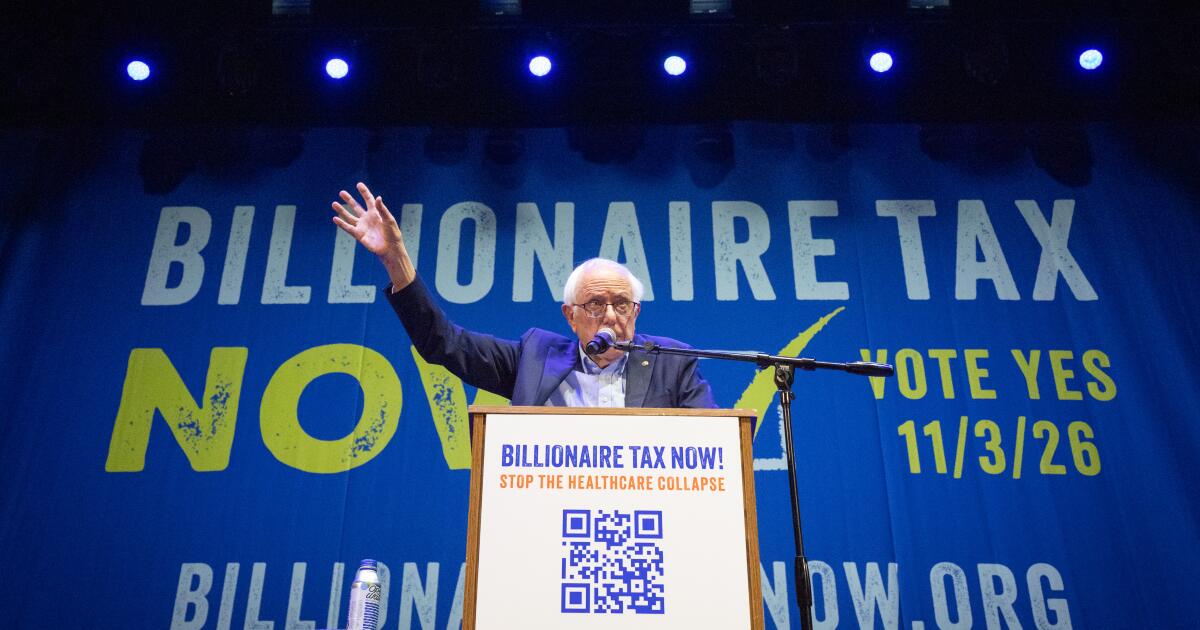

The billionaire tax has generated national news coverage and widespread debate over whether it would benefit low-income Californians or end up hurting the state’s tax base as billionaires move out of the state to avoid paying it.

The proposal is backed by the Service Employees International Union-United Healthcare Workers West, which represents 120,000 workers in California. Union leaders say that the tax would raise $100 billion to backfill steep cuts to federal healthcare programs under a sweeping tax and spending bill approved by the Republican-controlled Congress and signed in the summer by Trump.

The measure would impose a one-time 5% tax on the assets of California residents who are worth $1 billion or more, with options to pay it over multiple years.

According to SEIU-UHW, the new tax would apply to around 200 people in the state, though several wealthy tech leaders have made moves to change their residences and avoid paying the tax should it pass. In recent months, Meta Chief Executive Mark Zuckerberg, Google co-founders Larry Page and Sergey Brin and others have bought up lavish beachfront estates and new commercial office spaces in South Florida.

Some of those billionaires are also ponying up to defeat the measure. Brin, who according to Forbes is the world’s third-richest person, has contributed $45 million to a new ballot measure committee called Building a Better California, which is pushing an alternative statewide ballot measure that could scrap the billionaire’s tax.

Brandon Castillo, a veteran ballot measure campaign strategist who is not working on either of the two measures, said even though it’s currently polling above 50%, the billionaire’s tax is starting out “in a really shaky position.”

“This is not a very strong place to start,” he said. “That’s not to say they can’t keep this thing over 50%, but when you’re starting just barely above 50% and you have a tsunami of money and a huge campaign against you, it’s really hard to keep yourself at that level.”

Though previous public opinion polls at the state and national levels have shown broad support for requiring proof of citizenship to vote in elections, even among Democrats, the new Berkeley poll showed liberal voters are skeptical of the measure.

Proponents of voter ID contend that such laws prevent election fraud and, along with proof of citizenship mandates, prevent noncitizens from voting. Opponents say ID requirements threaten the fundamental constitutional rights of Americans who do not have the documentation readily available, and that the restrictions are unnecessary given that voting by noncitizens is rare and already outlawed in the U.S.

Under current law, Californians are not required to show or provide identification when casting a ballot in person or by mail. They are required to provide identification when registering to vote, and must swear under penalty of perjury, a felony, that they are eligible to vote and a U.S. citizen.

The poll showed that slim majorities of predominantly Spanish-speaking voters, voters who were born in another country and first-generation immigrants support the voter ID measure. A plurality of Latino voters also favor it, with 44% in support and 41% opposed.

But DiCamillo cautioned against reading too much into those numbers, noting that awareness of the measure is still relatively low.

“I’ve always seen in my history of measuring Latino voters’ support that they are relatively late deciders on most ballot measures,” he said. “How they break will be critical. I would say we’ll have to look at how they feel when we do our final preelection poll.”

Voter ID laws are also a top priority of Trump, who has pressured the Senate into taking up the SAVE Act, which would impose nationwide requirements for proof of citizenship to vote and already has passed the House of Representatives.

Castillo said Trump’s support could sway Democratic and liberal-leaning independents to vote against the measure.

Both DiCamillo and Castillo noted that with the November election still seven months away, voters are not paying much attention and those on either side of each ballot measure have not launched major campaigns yet.

“I suspect by the time election day comes around, these awareness numbers on the billionaire’s tax certainly are going to be much higher,” Castillo said. “You’re going to see 80-90% of voters familiar with it, just because they’re going to be inundated with advertising and earned media between now and November.”

The Berkeley IGS/Times poll surveyed 5,019 registered California voters online in English and Spanish from March 9 to 14. The results are estimated to have a margin of error of 2.5 percentage points in either direction in the overall sample, and larger numbers for subgroups.