Treasury Secretary Bessent confirms steps for a Donald Trump $250 bill

ATLANTA — Treasury Secretary Scott Bessent said Thursday that his department has prepared the design for a $250 bill featuring President Trump, anticipating the passage of stalled legislation in Congress to put the president on a new denomination of legal tender.

Bessent said at the White House that authorizing the currency will be up to lawmakers on Capitol Hill, but that “we’ve created the bill” because “we have to be prepared.”

The secretary downplayed the idea that the administration is pushing the matter, despite Trump’s penchant for infusing his name and likeness across the nation’s capital and into the observances of the 250th anniversary of the Declaration of Independence. Bessent also insisted there is nothing inappropriate about Trump’s visage being part of the seminal national celebration.

“The president doesn’t do it; the House and the Senate have to do it,” Bessent said at the White House, referring to legislation, introduced by Rep. Joe Wilson (R-S.C.), that would direct the Treasury Department’s Bureau of Engraving and Printing to put Trump’s face on the new bill to mark the 250th anniversary of the nation’s founding.

A Treasury Department spokeswoman said the agency carried out “appropriate planning and due diligence” to implement a potential congressional mandate “to produce a $250 commemorative note which will appropriately recognize the 250th Anniversary of our great nation.” The spokeswoman did not mention Trump.

If passed and signed into law by Trump, Wilson’s bill would mark an extraordinary recognition for a sitting U.S. leader and comes as Trump has sought to place himself at the center of Independence Day commemorations. The Department’s preparation for the languishing legislation suggests some enthusiasm for the idea on the part of the Trump administration.

Report: Trump ally has pushed to expedite new currency

The agency’s explanation follows a Washington Post report stating that U.S. Treasurer Brandon Beach, a Trump appointee, has been pushing the Bureau of Engraving and Printing to expedite the process for a new currency note. The paper also reported that the former BEP chief, Patricia Solimene, was reassigned after pushing back.

The Treasury spokesperson declined to comment on Solimene’s status but confirmed that Michael Brown, a top Beach aide, became acting director of engraving and printing May 18.

Beach did not respond to an Associated Press request for comment.

Wilson’s legislation, which so far has languished in Congress, is intended to create an exception to existing law that bars any living person from appearing on U.S. currency; the bill would allow current and former presidents to be featured.

Bessent confirmed the measure is designed for one person.

“Donald J. Trump,” he said emphatically, repeating the full name that the president himself often uses in the third person.

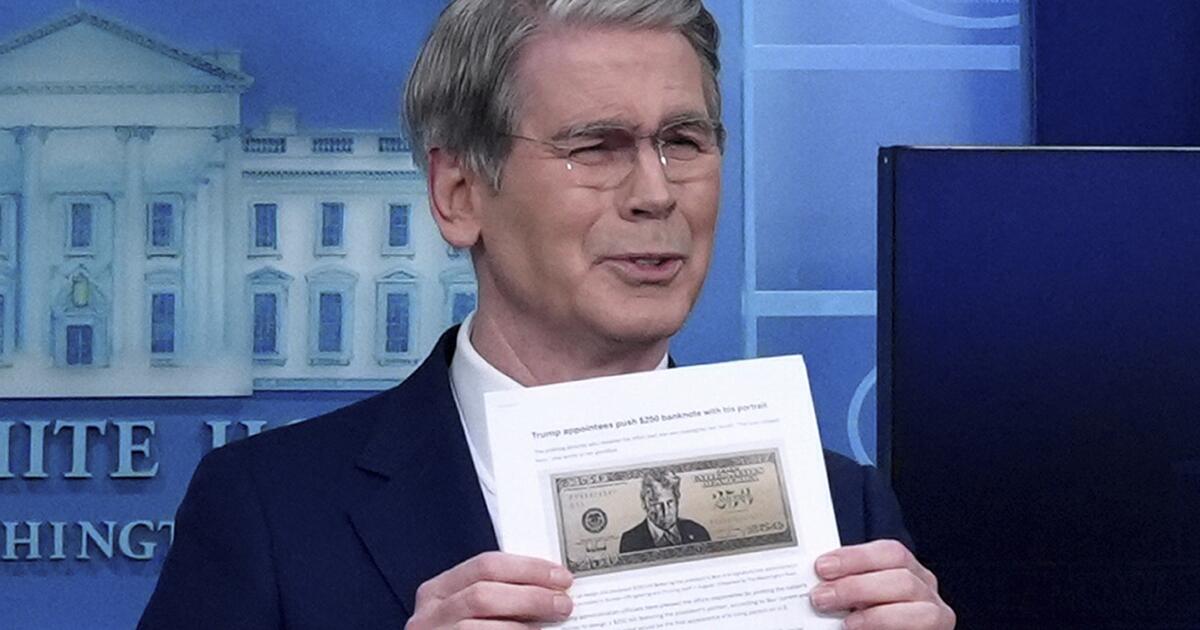

According to the Post report, Beach last fall provided the Bureau of Engraving and Printing with the design for the new bill. It featured Trump’s portrait — the same one that adorns banners hanging on some federal buildings in Washington — and a 250th anniversary logo. Trump’s signature also was included, a design element that would differ from other paper money.

British artist Iain Alexander told the Post he designed the bill and said he’d discussed it with the president. Alexander did not respond to an AP request for comment.

The newspaper also reported that Solimene resisted pressure from Beach and Brown and stressed to them the lengthy legal and procedural process required to issue new currency. Solimene was reassigned against her will, the Post reported, paving the way for Brown to oversee the bureau.

Trump has aggressively spread his name and likeness

A new currency note would be the latest example of Trump expanding his personal brand in his official capacity since returning to the White House last year.

Beach and Bessent already streamlined approval of a commemorative 250th anniversary coin featuring Trump. The Treasury Department has asserted that those special coins fall outside the prohibition on living presidents appearing on money. In 1926, the nation’s 150th anniversary, then-President Calvin Coolidge appeared on a commemorative half-dollar coin that was official legal tender.

The Trump administration has had banners featuring his portrait hung on the Department of Justice and other federal buildings. And his slate of appointees to the Kennedy Center governing board added his name to the national performing arts facility that Congress originally designated as a memorial to assassinated President John F. Kennedy. That renaming is being challenged in court because of the federal law establishing the center as the official memorial to the 35th president.

Bessent noted that unless Wilson’s exception passes, current law sets just two conditions for him to consider on currency: that “In God We Trust” is printed somewhere on it, and that only deceased individuals be depicted, with their names described below their portraits.

“It’s all up to Capitol Hill,” Bessent said. “We will stick to the law.”

Barrow writes for the Associated Press.