Four wins to go. How can your team reach the final and win the World Cup 2026? Click here to find out.

Who: Brazil vs Norway What: FIFA World Cup 2026 – Round of 16 Where: New York New Jersey Stadium, East Rutherford, New Jersey, US When: Sunday, July 5, at 4pm (20:00 GMT) How to follow: We will have all the build-up on Al Jazeera Sport from 17:00 GMT before our live text commentary stream.

Recommended Stories

list of 3 itemsend of list

Two of the world’s most exciting forwards, Vinicius Jr and Erling Haaland, will light up Sunday evening in New Jersey when Brazil face Norway in a blockbuster round of 16 clash.

For all their dominance on the world stage, Brazil have historically struggled to find a way past Norway, and after four failed attempts, the Selecao will hope the fifth time is the charm.

Carlo Ancelotti’s talented side has its fair share of flaws, and having narrowly escaped elimination in the last 32 against Japan, they need an improved performance against Norway – one of the dark horses at this tournament.

Spearheaded by Haaland and Martin Odegaard, Norway arrive with bragging rights – they are one of only three countries Brazil have faced at a World Cup without registering at least one victory.

How did Brazil and Norway reach the round of 16?

Brazil finished at the top of Group C, with wins over Scotland and Haiti, and a draw with Morocco. They fought from a goal down to beat Japan 2-1 in stoppage time in the last 32.

Norway came second in Group I, winning against Iraq and Senegal and falling to France. They sealed a late 2-1 victory over Ivory Coast in the last 32 – the Scandinavian nation’s first World Cup knockout victory after previous exits to Italy in 1938 and 1998.

Can Haaland extend Norway’s dream run?

Be it for club or country, towering forward Haaland’s impact cannot be understated.

Of the 10 goals Norway have scored at the tournament, Haaland is responsible for half – numbers that are remarkable for a 25-year-old making his World Cup debut.

Come Sunday, Norway will need their 1.95-metre- (6.4ft)-tall, pony-tailed talisman to strike again if they are to reach the quarterfinals for the first time.

Brazil will be wary of Norway’s lethal striker Erling Haaland [Paul Ellis/AFP]

Norway could take inspiration from their 1998 World Cup side, which famously beat Brazil 2-1 in a group game. And they need not look further than their coach Stale Solbakken – a midfielder in that Norwegian squad – for words of advice.

“Brazil are favourites, of course they are, but we are hopeful that we will give them a match, and we are not playing the game for fun – we are playing to win the game and to reach the quarterfinals,” said Solbakken. “It’s possible, but it’s very difficult.”

The Norwegians will be wary of Brazil’s very own trump card Vinicius, whose four goals at the tournament have made him the team’s leading scorer and most influential player. Vinicius became the first Brazilian since Ronaldo and Rivaldo in 2002 to score in all three group stage matches at a World Cup. That was the last time Brazil lifted the trophy.

Brazil vs Norway prediction

The Opta supercomputer gives Brazil a 53.6 percent likelihood of winning in regulation time, while Norway’s chances of winning are 22.4 percent.

The model estimates a 24 percent probability of the game going to extra time.

Brazil vs Norway: Kickoff time, TV channel

Brazil: SBT, CazeTV (4pm, Brasilia Standard Time)

Norway: TV2, NRK (9pm, Central European Summer Time)

United Kingdom: ITV1, ITVX, STV, STV Player (8pm, British Summer Time)

United States: FOX, FOX One, Telemundo App, Telemundo Network, Peacock (4pm, Eastern Daylight Time)

To check the TV listings for your country, head to FIFA’s TV listing schedule here.

Norway fans do the traditional rowing celebration in the stands [Dylan Martinez/Reuters]

Who will the winner face in the quarterfinals?

The winner of the Brazil vs Norway match will face either Mexico or England in the quarterfinals in Miami on Saturday, July 11.

Brazil vs Norway: Head-to-head

Norway hold the rare distinction of never having lost to Brazil, with two wins and two draws from their four previous meetings, including a memorable 2-1 victory over Brazil in the group stage of the 1998 World Cup.

Brazil and Norway last met in a friendly in 2006, which ended 1-1.

More worryingly for Ancelotti, Brazil have been eliminated from each of their last six World Cup knockout ties against European opponents since beating Germany in the 2002 final.

Brazil vs Norway: Team news

Brazil’s Lucas Paqueta picked up a hamstring injury in the last game, while Raphinha, who also picked up the same issue in the second game, has resumed individual training and could make the bench.

Norway’s Julian Ryerson is out with a thigh injury.

Brazil’s Bruno Guimaraes has four assists at the World Cup – only Pele recorded more (six) for the five-time world champions at a World Cup [Annegret Hilse/Reuters]

How can your team reach the final and win the World Cup 2026? Click here to find out.

Who: France vs Paraguay What: FIFA World Cup 2026 – Round of 16 Where: Philadelphia Stadium, US When: Saturday, July 4, at 5pm (21:00 GMT) How to follow: We will have all the build-up on Al Jazeera Sport from 18:00 GMT before our live text commentary stream.

Recommended Stories

list of 4 itemsend of list

Kylian Mbappe’s France have been the outstanding team so far at this World Cup and will be expected to get the better of Paraguay on Saturday and extend their run to the quarterfinals.

France look a very good bet to win their third World Cup, and they are certainly expected to overcome a Paraguay team ranked 41st in the world.

After winning the trophy in 2018 and losing the 2022 final on penalties, France are hoping to become only the third team in World Cup history to reach three consecutive finals, after West Germany and Brazil.

That remains a long way off but their performances so far suggest they will take some beating.

Tuesday’s 3-0 defeat of Sweden in the last 32, in which Mbappe scored twice and Bradley Barcola once, made it four wins in four matches with 13 goals scored.

But the Paraguayans head to Philadelphia with their confidence sky-high after their victory on penalties against Germany – which led to a national holiday being declared back home.

What happened in France’s last-32 game?

Mbappe scored twice, and Michael Olise was in scintillating form as France beat Sweden 3-0.

The Real Madrid striker finished a superb move to break the deadlock just before half-time. Olise set up Paris Saint-Germain winger Barcola for the second goal on 53 minutes, and then delivered a delightful pass for Mbappe to complete a convincing victory.

Mbappe’s strikes saw him move level with Lionel Messi on six goals in the all-star golden boot race at this World Cup.

The France captain now has 18 World Cup goals in total, meaning he is just one behind Messi’s overall record of 19, a mark 27-year-old Mbappe will keep chasing.

Olise in action against Sweden [AFP]

What happened in Paraguay’s last-32 game?

The Germans trailed 1-0 at half-time to Julio Enciso’s 42nd-minute header from Matias Galarza’s cross on Monday.

It was a limp display by the four-time winners in the first period, but they drew level in the second half, when Kai Havertz scored eight minutes after the restart with a glancing header from Florian Wirtz’s ball in from the flank.

Germany then had a Jonathan Tah goal from a corner ruled out after a VAR review for a foul on Paraguay’s keeper, and with no further goal, the game went to spot kicks after extra time.

Havertz, who helped Arsenal end a 22-year wait to win the English Premier League title this season, missed the opening kick of the shootout. The forward’s side would miss three kicks in total, as Paraguay, who themselves missed two kicks, eventually prevailed 4-3.

Deschamps releases the handbrake

France have enjoyed plenty of success during Didier Deschamps’s 14 years in charge, but for a long time there was a sense that a pragmatic coach was not allowing his team to maximise their attacking potential.

Now at his last tournament before stepping down, that appears to have changed. Mbappe, Barcola, Ousmane Dembele and the brilliant Michael Olise seem unstoppable.

“There is an excellent rapport between the attacking players. They speak the same footballing language,” said Deschamps after the Sweden game.

But France’s coach says his side will not take Paraguay lightly.

“They are not here by chance. Germany are a top side, and they have that South American DNA, which means they get stuck in,” Deschamps said.

“And they have good players too. You can’t just qualify for the last 16 of the World Cup like that by chance.”

Mbappe in action against Sweden during the Round of 32 [Vincent Carchietta/Reuters]

‘We also have our own strengths’

One Paraguayan player well-known in France is Julio Enciso of Strasbourg, who scored against Germany.

He recognises that few people will expect Paraguay to win as they aim to reach the quarterfinals of the World Cup for just the second time.

“We also have our own strengths, and with our style of play, we’re going to try to make things difficult for any opponent,” said Enciso.

Enciso celebrates scoring against Germany in the last 32 [AFP]

Extreme heat warnings

One potential opponent for both teams is the weather, with temperatures in Philadelphia set to reach 37 degrees Celsius (98 Fahrenheit) on Saturday.

This match will take place in the city where the American Declaration of Independence was signed 250 years ago, but celebrations for the occasion are at risk of being affected by storms.

France have already played in Philadelphia in this World Cup, and their 3-0 win over Iraq during the group stage was interrupted for two hours because of rain and thunder.

Coping with the conditions could be a challenge, and both sides will want to avoid the draining prospect of extra time and penalties.

The last meeting of the countries at a World Cup featured extra time and turned out to be one of the most pivotal moments in the modern history of the French national team.

On their way to winning the trophy for the first time on home soil in 1998, Les Bleus – with Deschamps as captain – edged Paraguay 1-0.

France vs Paraguay: Kickoff time, TV channel

France: Bein Sports 1 (11pm, Central European Time)

United Kingdom: BBC, ITV (10pm, British Summer Time)

United States: FOX, Telemundo (5pm, Eastern Daylight Time)

To check the TV listings for your country, head to FIFA’s TV listing schedule here.

France vs Paraguay prediction

The Opta supercomputer gives France a 78.8 percent chance of winning in regulation time, while Paraguay are at 7.6 percent.

The model estimates a 13.7 percent probability that the game will go to extra time.

Head-to-head

The two countries have faced each other five times, with France winning three of the games and two ending as draws.

France beat Paraguay 5-0 in their most recent encounter – a friendly in 2017 – in which Olivier Giroud scored a hat-trick.

June 02, 2017: France 5-0 Paraguay (friendly)

June 01, 2014: France 1-1 Paraguay (friendly)

May 31, 2008: France 0-0 Paraguay (friendly)

June 28, 1998: France 1-0 Paraguay (World Cup last 16)

June 08, 1958: France 7-3 Paraguay (World Cup group stage)

Team news

Neither side has any suspensions or reported injury concerns.

Four wins to go. How can your team reach the final and win the World Cup 2026? Click here to find out.

Who: Canada vs Morocco What: FIFA World Cup 2026 – Round of 16 Where: Houston Stadium, Texas, US When: Saturday, July 4, at noon (17:00 GMT) How to follow: We will have all the build-up on Al Jazeera Sport from 14:00 GMT before our live text commentary stream.

Recommended Stories

list of 3 itemsend of list

The Round of 16 gets under way on Saturday with World Cup cohosts Canada taking on Morocco in Houston, Texas.

It marks a historic day for Canadian football, with the men’s team set to play in the last-16 for the first time in their history, thanks to a dramatic late victory over South Africa.

But in their bid to extend a dream run, Canada face a daunting challenge against Morocco, who stunned the Netherlands on penalties to punch their ticket to this round.

The African champions, semifinalists of the last edition, are unbeaten at this year’s tournament and have grown stronger with every game.

Al Jazeera tells you everything about Canada vs Morocco:

How did Canada and Morocco reach the Round of 16?

Canada came second in Group B with four points, securing a win over Qatar and a draw with Bosnia and Herzegovina. They lost to Switzerland in the final group game. The Canadians beat South Africa 1-0 in the round of 32.

Morocco were second in Group C with seven points, winning against Scotland and Haiti, and holding Brazil to a draw. In the Round of 32, they scored a late equaliser to force the game to extra time before beating the Netherlands 3-2 in a thrilling shootout.

Can Canada pass the Moroccan test to extend dream run?

Canada are the underdogs in this last-16 game, sitting 24 places below world number six Morocco in the FIFA rankings. But after breaking numerous records at the tournament – including earning their first World Cup point and winning their first game – their campaign is nothing less than a success.

“Preparing for Morocco is like a gory, horrible nightmare,” coach Jesse Marsch said. “[But] we want to be here and we expect to be here. So we know that everybody’s going to write us off, and in that is an opportunity.”

For Morocco, the game against Canada is just another hurdle in the deep run they are hoping for this summer in North America. Four years on from stunning Spain and Portugal to become the first Arab and African nation to reach the semifinals, Morocco have arrived with bigger ambitions and increased expectations.

“If we get things wrong, we’ll go home,” Morocco manager Mohamed Ouahbi said. “We need to ensure that we have all the tools and we’re using the tools in our arsenal to go as far as we can.”

Canada will be wary of Morocco’s talismanic forward Ismael Saibari, their top scorer with three goals and the newly signed Bayern Munich player who also scored the winning spot-kick to send them to the round of 16.

Canada vs Morocco prediction

The Opta supercomputer gives Morocco a 52.7 percent likelihood of winning in regulation time, while Canada is at 21.7 percent.

The model estimates a 25.6 percent probability of the game going to extra time.

To check the TV listings for your country, head to FIFA’s TV listing schedule here.

Fans of Canada pose for a photograph inside the stadium before their last-32 match against South Africa in Inglewood, California [Alex Grimm/Getty Images/AFP]

Who will the winner face in the quarterfinals?

The winner of the Canada vs Morocco match will face either France or Paraguay in the quarterfinals in Boston on Thursday.

Canada vs Morocco: Head-to-head

The two teams have met four times, with Morocco winning on three occasions, while one game ended in a draw.

Canada are winless against Morocco, who won 2-1 in their last meeting, a group game at the 2022 World Cup in Qatar.

Canada vs Morocco: Team news

Ismael Kone is out with a broken ankle. Alphonso Davies played his first minutes at the tournament in the last game as a 75th-minute substitute and could start against Morocco.

No injuries have been reported in the Morocco camp.

On Sunday, Mexico will take on England at Mexico City’s famed Estadio Azteca for a round of 16 World Cup match in one of the most hotly anticipated contests of the tournament so far.

But days before anything goes down on the pitch, Mexico and England fans have already started bickering with each other online — from cheeky jabs to heated debates about which country does beans on toast better.

Joining in on the soccer smack talk are two of the biggest rock stars from the countries — Liam Gallagher of Oasis fame and Maná frontman Fher Olvera.

The “Wonderwall” singer’s prediction was so audacious that Olvera took it upon himself to publicly respond with an Instagram video Wednesday evening.

“The singer of Oasis said that Mexico will lose to England 5-0,” Olvera said in Spanish with a giant grin on his face while draped in a Mexican flag. “No way! Check yourself dude! 5 to 0? Calm down! We’ll see you Sunday to see how it goes, dude. Don’t play with me.”

By Thursday morning Gallagher amended his prediction for the match.

“[L]et me just clear someting up I was obv kidding when I said England will beat Mexico 5-0,” the English rocker wrote in an X post. “I reckon it’ll be more like 3-0 to England.”

Maná already made its mark on this year’s World Cup when it played its 1992 hit “Oye Mi Amor” at the tournament’s opening ceremony in Mexico City ahead of the Mexico-South Africa match on June 11.

Sunday’s contest between England and Mexico also marks the first time the English side will play at Estadio Azteca since the 1986 World Cup when they lost to eventual-champions Argentina in a quarterfinal game infamous for Diego Maradona‘s “Hand of God” goal.

The last time Mexico and England squared off in a World Cup setting was during the 1966 World Cup in England where the Three Lions beat El Tri 2-0 in a group stage match at Wembley Stadium.

Five wins to go. How can your team reach the final and win World Cup 2026? Click here.

Who: Brazil vs Japan What: FIFA World Cup 2026 – round of 32 Where: Houston Stadium, Houston, United States When: Monday, June 29, at 12pm (17:00 GMT) How to follow: We will have all the build-up on Al Jazeera Sport from 14:00 GMT ahead of our live text commentary stream.

Recommended Stories

list of 4 itemsend of list

Carlo Ancelotti faces his first major test as the Brazil coach when the record five-time world champions take on Japan, arguably the best Asian team at the tournament, in the round of 32.

Monday’s meeting in Houston offers Brazil the chance to exact revenge for their friendly defeat to Japan late last year, as the South American giants lock in on their target of a deep run in North America.

The odds are heavily in Brazil’s favour, but after Japan came out of a tricky group with flying colours, it would be foolish to write them off.

There is also a mutual respect and camaraderie between the nations, given the overwhelming Brazilian influence on professional football in Japan.

Al Jazeera tells you everything about the second game of the round of 32:

Of all the seven goals Brazil registered across three games, Real Madrid star forward Vinicius Jr scored four of them, while Matheus Cunha netted three. Bruno Guimaraes bagged the most assists (three).

Brazil’s forwards Matheus Cunha, left, and Vinicius Jr are spearheading Brazil’s attack at the World Cup [Roberto Schmidt/AFP]

Ancelotti in relaxed mood ahead of Japan clash

Since their low-key display in the first game, Brazil appear to be growing into the tournament, showing glimpses of their all-round potential, with some of the Selecao stars finding their rhythm.

Ancelotti knows Japan will be no pushovers, describing the record four-time Asian champions as “one of the best teams” in the world.

During Sunday’s pre-match press conference, the Italian was relaxed and betrayed no signs of feeling the pressure, despite Brazil being cast as the clear favourites for the knockout tie.

“We need a lot of things: A strong mind, a strong heart, a clear mind,” he told the media. “I think we have to be ready for anything that might take place in a knockout match, and a lot can happen in a knockout match.

“I think the team is ready. They’re motivated, they’re confident,” added Ancelotti, who is leading Brazil’s charge for a record-extending sixth world title.

How did Japan reach the round of 32?

Japan started their campaign by holding the Netherlands to a 2-2 draw before thrashing Tunisia 4-0 in the second game. They wrapped up the first round with a 1-1 draw with Sweden, which saw them finish with five points, confirming a second spot in Group F.

Ayase Ueda and Daichi Kamada are the joint top scorers for Japan so far, with two strikes each, while Keito Nakamura, Junya Ito and Daizen Maeda have also scored one each.

Japan’s Junya Ito, right, has scored once in the tournament, while Ayase Ueda, left, and Daichi Kamada, centre, have two goals each [Daniel Becerril/Reuters]

Dark horses Japan are ‘united’, says Moriyasu

Japan have lived up to their billing as the “dark horses” at the tournament, holding two formidable European sides – the Netherlands and Sweden – to draws.

After beating Germany and Spain en route to a round of 16 run at the 2022 World Cup, Japan have shown the world they are capable of pulling off upsets, especially on the sport’s biggest stage.

Japan coach Hajime Moriyasu said his side’s collective spirit can fire them into the last 16 again.

“All the players will do what they can for the team and contribute,” Moriyasu said on Sunday. “The team is united, and that feeling is getting even stronger now.”

Japan’s best finish at the World Cup has been reaching the round of 16 on four occasions: 2002, 2010, 2018 and 2022. They have never won a World Cup knockout game.

Brazil vs Japan: master vs the apprentice

Launched in 1993, Japan’s top-flight, the J-League, took much of its inspiration from Brazil and also employed plenty of their players.

Zico, the creative lynchpin of Brazil’s fabled 1982 World Cup team, was enticed out of retirement to join Kashima Antlers, while internationals Bismarck and Elivelton started a run of Brazil national team players making the move to Japan.

By the late 1990s, seven of the Brazil team that won the 1994 World Cup, including captain Dunga, had played or were playing for Japanese clubs and, by extension, lent their influence to a rapidly developing scene.

Brazil vs Japan predictions

Opta’s supercomputer has calculated a 58.3 percent probability of Brazil winning this fixture in regulation time, while Japan is assessed an 18.1 percent chance of victory.

The probability of going to extra time – or potentially penalties – is 23.6 percent.

Who will the winner face in the round of 16?

The winner of Brazil vs Japan will face either Norway or the Ivory Coast in the round of 16.

Brazil vs Japan: Kickoff time, TV channel

Brazil: CazeTV, TV Globo, GETV, Globoplay, sportv (2pm, Brasilia Time)

Japan: NHKBS1, DAZN, Fuji TV (2am on Tuesday, Japan Standard Time)

United Kingdom: ITVX, ITV1, STV Player, STV (6pm, British Summer Time)

To check the TV listings for your country, head to FIFA’s TV listing schedule here.

Brazil vs Japan: head-to-head

In the all-time head-to-head record, Brazil have only lost once to Japan (W11 D2 L1). In their only World Cup contest 20 years ago at Germany 2006, Brazil won 4-1.

Significantly, Japan’s sole victory over Brazil came in their most recent clash, a 3-2 victory in a friendly in October 2025 in which Brazil let a two-goal lead slip in Tokyo, with Ueda scoring the hosts’ winner.

Brazil vs Japan: Team news

Raphinha remains sidelined for Brazil due to a hamstring injury, while Japan’s Takefusa Kubo is out with a sprained knee.

Neymar, who made his first appearance for Brazil since October 2023 when he came off the bench in the last game, will be available to play more minutes against Japan. The star forward is working his way back to full fitness after dealing with a lingering calf injury.

The 2026 World Cup will have 13 different kickoff times. You can use the Al Jazeera Sport widget to find out exactly when your team is playing in your local time.

Who: Colombia vs Portugal What: FIFA World Cup 2026 Group K match Where: Hard Rock Stadium, Miami When: Saturday, 7:30pm local time (23:30 GMT) How to follow: We’ll have all the build-up on Al Jazeera Sport from 20:30 GMT ahead of our live text commentary stream.

Recommended Stories

list of 4 itemsend of list

One of the biggest group games of the 2026 World Cup takes place in Miami on Saturday when Colombia face Portugal in a battle of Group K’s top two.

Colombia, powered by Luis Diaz and Daniel Munoz, have already booked their ticket to the round of 32 as the current table-toppers, while Cristiano Ronaldo-led Portugal, who are second, are also assured of a knockout berth.

Those standings could change after Saturday’s fixture at Hard Rock Stadium, where a capacity crowd is expected after tickets reportedly sold for thousands of dollars.

Al Jazeera tells you everything you need to know about Colombia vs Portugal:

Portugal expect ‘away’ atmosphere in Miami

Spearheaded by the larger-than-life presence of superstar Ronaldo, Portugal are a huge and popular draw globally – but for this match, Colombia will hold the spectator edge at Hard Rock Stadium.

With hundreds of thousands of Colombian Americans living in the Miami metropolitan area, the Colombian team has a partisan crowd behind them. In the lead-up, Portugal coach Roberto Martinez remarked that his side would be playing “away from home” while acknowledging the enormous hype around the final matchday for both teams.

Colombia vs Portugal is the most in-demand fixture of all 72 group-stage games, according to The Athletic, with five million ticket requests made in the first 24 hours of the Random Selection Draw in December.

“It means I had to buy tickets for my family in November,” Martinez quipped when asked about the fan dedication. “That’s what it means, because I knew it was going to be difficult to get tickets.”

“I think it’s fascinating. The passion of the game in a difficult moment in the world. Football still brings unity, it brings passion, it brings inspiration for the kids … So I hope football wins and inspiration of anyone that watches the game.”

While Colombia have reached the knockout stages with six points from two games, Portugal sit second on four points and are all but through. Finishing second could give them a tougher path in the knockout stage, with England or Croatia potential opponents.

Portugal train ahead of their game against Colombia, where they’ll be aiming to earn the top spot [Leonardo Fernandez/Getty Images via AFP]

Colombia coach warns team against Ronaldo, Vitinha

Colombia coach Nestor Lorenzo said his team will need “special tactical discipline” against Portugal, whom he considers one of the favourites to win the tournament. The Colombians need to avoid defeat to advance as group winners, but Lorenzo was taking nothing for granted against the No 5 side in the FIFA world rankings.

“We’ll try to maintain our style and our footballing identity,” he said.

“But without a doubt, we have to pay attention to the other characteristics and strengths [that Portugal] has. It’s a very well-coached team. They have a coach and players who are at the elite level of world football … and that shows in their game.”

Lorenzo also said Colombia will be wary of the threat posed by Ronaldo, who scored twice in the last match, and Vitinha, the defensive midfielder known for his ball control, work rate and playmaking abilities.

“Both Vitinha and Ronaldo are decisive players. One in the organisation of the game and the quality of his playmaking, and the other in finishing,” he added. “So we absolutely cannot leave them alone or neglect them. Hopefully, the team collective will be well-oiled.”

Colombia are set to feature in the World Cup knockouts for the first time since 2018, having failed to qualify for the 2022 World Cup in Qatar.

Wing-back Daniel Munoz has been a standout player in the Colombia squad, with two goals in two games [Ulises Ruiz/AFP]

Colombia vs Portugal prediction

Opta’s supercomputer has calculated a 48.9 percent probability of Portugal winning this fixture, while Colombia is assessed a 26 percent chance of victory. There is a 25.1 percent probability of the game ending in a draw.

Overall, Colombia are favourites to finish on top of Group G, with a 53.32 percent probability, according to Opta.

Colombia vs Portugal: Kickoff time, TV channel

Colombia: DSPORTS, RCN TELEVISION SA, CARACOL, DGO (6:30pm Colombia Standard Time)

Portugal: RTP 1, RTP Play, LiveModeTV, SPORT.TV5 (00:30am on Sunday, Western European Summer Time)

United Kingdom: BBC iPlayer, BBC One, Red Button 1 (00:30 am on Sunday, British Summer Time)

To check the TV listings for your country, head to FIFA’s TV listing schedule here.

What’s the scenario in Group K?

Colombia (six points) and Portugal (four points) are assured of a round of 32 berth each as the top two teams. The Democratic Republic of the Congo are third with one point, and Uzbekistan bottom with zero.

The top two teams from each of the 12 groups, along with the eight best third-placed teams, will proceed to the round of 32.

DR Congo have to beat Uzbekistan to stand a chance of advancing via the third-place team route.

Can Portugal finish on top of Group K?

Yes, Portugal can topple Colombia from first place in Group K if they beat the South Americans. Currently, they have a two-point difference.

If Portugal draw with Colombia or lose to them, Ronaldo’s side will remain second.

What’s the benefit of winning a group?

Group winners start their knockout campaign against a third-placed team from another group.

In this case, the Group G winner will face a third-placed team from Group D, E, I, J or L in the round of 32 in Kansas City on July 3.

Form guide

(Last five games, latest first)

Colombia: W-W-W-W-L

Portugal: W-D-W-W-W

Both teams have a solid record over the last five matches, with Portugal edging Colombia with an unbeaten streak over that period.

Portugal thrashed Uzbekistan 5-0 and were held to a 1-1 draw by DR Congo in the first game of the World Cup. They defeated Nigeria and Chile in pre-World Cup friendlies and beat the USA in a March friendly.

Colombia defeated DR Congo 1-0 and Uzbekistan 3-1 at the tournament. Before that, they beat Jordan and Costa Rica in June friendlies but lost to France in a March exhibition fixture.

Portugal have scored six goals across two matches at the tournament, including a double from Cristiano Ronaldo [Ronaldo Schemidt/AFP]

Colombia vs Portugal: Team news

No injuries have been reported by either Colombia or Portugal.

Meta CEO Mark Zuckerberg has given the green light to develop a prediction market app, according to the New York Times, as Meta moves to capitalise on one of the fastest-growing sectors in tech and finance.

ADVERTISEMENT

ADVERTISEMENT

The app is currently being referred to as Arena internally and would let users earn points for correctly predicting the outcomes of events such as sports results, political developments and stock market moves but without any real money changing hands, at least initially.

It would operate independently of Meta’s existing social platforms, though those could funnel users towards it, according to the reporting.

What is a prediction market?

A prediction market is essentially a financial exchange where people buy and sell contracts or bets tied to the outcome of real-world events.

Each contract is a simple yes-or-no question, such as whether a certain candidate will win an election, a team will come out first in a championship or if a major political figure will pass by a certain date.

On Polymarket and Kalshi, the two most popular prediction market platforms, users buy contracts that pay out $1 if they are right and nothing if they are wrong.

As more people trade those contracts, the price reflects the market’s probability of the event occurring. If a bet is worth 40 cents, there’s a 40% chance of it happening, according to the people who have placed bets.

Fans of prediction markets argue the mechanism produces more accurate forecasts than polls or political analysts because participants have real money on the line.

Polymarket and Kalshi

The two dominant platforms in the space are Polymarket and Kalshi, which together generated around 85–90% of the roughly $44 billion (€40bn) in total trading volume recorded in 2025.

Polymarket, founded in 2020 by New York University dropout Shayne Coplan, operates globally on the blockchain. In October 2025, the New York Stock Exchange’s parent company invested $2 billion (€1.8bn) in the platform, in a major sign that Wall Street was taking the sector seriously.

Kalshi, founded in 2018 by two MIT graduates, spent years winning regulatory approval before launching as the first prediction market sanctioned by the US Commodity Futures Trading Commission (CFTC).

The turning point came in October 2024, when a US court ruled Kalshi could legally offer election contracts 32 days before the presidential election. Monthly trading volume has since surged from less than $5 billion (€4.6bn) in September 2025 to around $24 billion (€21.8bn) in April 2026, overtaking the roughly $14 billion (€12.7bn) wagered monthly through legal or traditional US sportsbooks.

Donald Trump Jr. becoming an investor in Polymarket and a paid adviser to Kalshi, while federal regulators adopted a more permissive stance, also helped fuel the boom.

The risks

The boom has not come without controversy and legal cases have mounted, with a former special forces soldier getting arrested over allegations he used insider knowledge of a US operation to capture Venezuelan president Nicolás Maduro to place a winning trade on Polymarket worth around $400,000 (€365,000).

Some US states have begun suing the platforms, arguing they are running illegal gambling operations without proper licences. The Trump administration has responded by suing the states that have moved to ban prediction markets, creating a messy legal standoff between federal and state authority.

A New York Times review found that Polymarket published hundreds of false and misleading social media posts, while Politico uncovered a campaign to pay influencers to praise the platform’s supposed accuracy.

Whether Meta’s gamified, cashless version of the concept can avoid those pitfalls or will simply serve as a gateway to them remains unclear.

The 2026 World Cup will have 13 different kickoff times. You can use the Al Jazeera Sport widget to find out exactly when your team is playing in your local time.

Who: Brazil vs Haiti What: FIFA World Cup 2026 Group C match Where: Lincoln Financial Field, Philadelphia When: Friday, 6:30pm local time (00:30 GMT Saturday) How to follow: We’ll have all the build-up on Al Jazeera Sport from 21:00 GMT in advance of our live text commentary stream.

Recommended Stories

list of 3 itemsend of list

Brazil’s draw with Morocco in their opening match left fans with more doubts than belief, with millions wondering if the record five-time champions are still among the world’s best teams.

Having slipped to third in a group that they were expected to dominate, Brazil now face minnows Haiti in their second group game, needing a World Cup reset.

Head coach Carlo Ancelotti will need to address several shortcomings with his team if he wants to avoid another disappointing performance during the group stage.

Here is all to know before Brazil vs Haiti kicks off:

No need to panic yet, suggests Brazil

While Brazil’s weak showing in the first game has raised questions about the team’s odds of a deep run, Ancelotti believes it is no cause for concern just yet.

Against Morocco, Brazil showed signs of nerves during the early stages and struggled to cope with the AFCON champions’ attack. Some players also struggled to cope with the intensity of the encounter.

The Italian coach, who has been in charge for just over a year, said the upcoming match with Haiti offers his side an opportunity to address their weak points.

“You don’t win the World Cup in the first match,” Ancelotti told reporters in Philadelphia on Thursday.

“The players’ self-criticism was very positive. I think we’ll sort out the problems; I remain confident that we’ll be competitive.”

Critics have argued that Brazil lacks an identity under Ancelotti, but the 67-year-old – nicknamed “Don Carlo” – believes adapting his tactics according to gametime situations is more important.

“I don’t want a single identity,” he said. “I want my team to have multiple identities.”

Former Real Madrid coach Carlo Ancelotti took over the team in May 2025 [Caean Couto/Imagn Images via Reuters]

Haiti want to make their people proud

It took Haiti more than half a century to return to the World Cup, and the Caribbean underdogs have somewhat of a cruel challenge at hand, being grouped alongside world-class Brazil, African giants Morocco, and Scotland.

While their 1-0 defeat to Scotland in the opening game did not dampen their spirit, Haiti know they face a far more difficult task against Brazil, who have no shortage of talent in their squad.

The odds are stacked against Haiti, but in a tournament where upsets have not been uncommon, their fans are daring to dream.

“Tomorrow [Friday], we’ve got everything to gain in a match like this. It’s been 52 years since we last featured in a World Cup, and now we’re up against Brazil – we’ve got to live up to our fans’ expectations,” coach Sebastien Migne said.

“It’s a privilege to be here, and I hope we can make the Haitian people proud of us.

“It would be absolute madness in Haiti if we won this match,” he added.

World No 85 Haiti, still looking for their first goal of this World Cup campaign, enter the match 80 spots below Brazil on the FIFA rankings.

Haiti coach Sebastien Migne gives instructions to his players during a hydration break [Brian Snyder/Reuters]

Brazil vs Haiti prediction

Stats provider Opta’s supercomputer has handed Brazil a whopping 87.3 percent probability of winning against Haiti, who have a mere 4.3 percent chance of winning. There is an 8.4 percent probability of a draw.

Overall, Brazil are seventh in the list of title favourites – with a 5.2 percent probability – behind a bunch of teams including France, Argentina and England, who make up the top three.

Haiti: TNH, Tele Haiti (8:30 pm Eastern Daylight Time)

United Kingdom: STV, STV Player ITV1, ITVX (01:30 Saturday, British Summer Time)

United States: FOX, FOX One, Telemundo App, Telemundo Network, Peacock (7:30pm Eastern Daylight Time)

To check the TV listings for your country, head to FIFA’s TV listing schedule here.

How does the group stage work?

Brazil, Haiti, Morocco and Scotland are in Group C.

Scotland lead the group with three points, followed by Morocco in second spot with one point. Brazil is in third place, also on a point, while Haiti is at the bottom with no points so far.

The top two teams from each of the 12 groups – along with the eight best third-placed teams – proceed to the next phase, the round of 32, which has been introduced at the World Cup for the first time.

(Al Jazeera)

Form guide

(Last five games, latest first)

Brazil: D-W-W-W-L

Haiti: L-L-W-D-L

Brazil have performed significantly better than Haiti in their last five matches.

They started their campaign in North America with a 1-1 draw with Morocco. Before the World Cup, Brazil registered victories over Egypt and Panama in friendlies and beat Croatia in March. But they lost to France in March.

Haiti suffered a defeat to Scotland in their opening World Cup game. They lost to Peru and beat New Zealand in pre-World Cup friendlies earlier this month, while they drew with Iceland and lost to Tunisia in friendlies in March.

Brazil vs Haiti: Head-to-head

Brazil have faced Haiti three times, winning on all occasions. Their last meeting dates back to a 2016 Copa America group game, in which Brazil thrashed Haiti 7-1.

Friday’s meeting between Brazil and Haiti will be their first at a World Cup.

Brazil vs Haiti: Team news

Just as in their opening match, Brazil’s oft-injured star Neymar Jr has been ruled out of the Haiti game.

A lingering calf strain will keep the veteran forward – Brazil’s all-time leading scorer with 79 goals – sidelined with the team hoping he recovers in time to feature in their final group game on June 24 against Scotland. He has not played for Brazil since October 2023.

Neymar was diagnosed in late May with the injury and has featured in just half of the games for his club side Santos this year due to various fitness issues.

For Haiti, striker Nazon – who was on the bench last time – is doubtful.

Neymar has not travelled with the rest of the Brazil team for their second World Cup game [Caean Couto/Imagn Images via Reuters]

Brazil predicted XI

Ancelotti is expected to make changes following criticism over his decision to start striker Igor Thiago and right-back Roger Ibanez against Morocco. Danilo and Cunha are widely tipped to replace them in the lineup against Haiti.

The World Cup group stage continues on Monday, with four more matches taking place across the United States.

Spain begin their campaign against World Cup newcomers Cape Verde, Belgium face Egypt in what could be one of the day’s closest games, Saudi Arabia take on Uruguay in Miami, and Iran meet New Zealand in Los Angeles.

Recommended Stories

list of 4 itemsend of list

Away from the football, Uruguay’s disrupted travel plans, divisions within Los Angeles’s Iranian American community before Iran’s opener, and Haiti’s inspiring return to the World Cup are all drawing attention beyond the pitch.

Belgium face Egypt at Seattle Stadium in Seattle at the same time, with the Group G rivals also getting under way at 12pm local time (19:00 GMT).

Later, Saudi Arabia meet Uruguay at Miami Stadium in Miami Gardens, Florida. That match starts at 6pm local time (22:00 GMT).

The day’s final fixture sees Iran face New Zealand at Los Angeles Stadium in Inglewood, California. Kickoff is at 6pm local time (01:00 GMT on June 16).

What do the predictions say for Spain vs Cape Verde?

Spain are the clear favourites to win, but Cape Verde have already made history by reaching the World Cup for the first time.

The teams have never played each other. Spain’s last two World Cup matches against African opponents came against Morocco, drawing 2-2 in 2018 before losing on penalties after a 0-0 draw in the 2022 quarterfinals.

Opta’s predictions strongly favour Spain. After running 25,000 simulations, the statistics company gave Spain an 87.2 percent chance of winning the Group H opener. A draw was predicted in 8.1 percent of the outcomes, while Cape Verde were given a 4.8 percent chance of causing an upset.

Only one African team has ever beaten Spain at a World Cup: Nigeria, who won 3-2 in the group stage in 1998.

Spain vs Cape Verde

What do the predictions say for Belgium vs Egypt?

This one could be much closer than many people expect.

Opta’s predictions suggest there is very little separating the sides. In 25,000 match simulations, Belgium won 37.2 percent of the time, while Egypt came out on top in 35.5 percent. A draw happened in 27.3 percent of the simulations.

Belgium are slight favourites. It could end up being one of the closest games of the day, with a single goal potentially making the difference.

Belgium face pressure to avoid repeating their performance in 2022 in Qatar, when they did not advance beyond the group stage. The Belgians finished third in 2018 in Russia.

Belgium vs Egypt – World Cup

What do the predictions say for Saudi Arabia vs Uruguay?

Saudi Arabia and Uruguay have met only once before at a World Cup. Uruguay won that match 1-0 in 2018.

The teams have also faced each other in a friendly match. That game, played in Saudi Arabia in 2014, ended in a 1-1 draw.

The predictions favour Uruguay. In 25,000 simulations run by Opta, Uruguay won 64.7 percent of the time. Saudi Arabia won 13.9 percent of the simulations, while 21.4 percent ended in a draw.

Saudi Arabia vs Uruguay – World Cup

What do the predictions say for Iran vs New Zealand?

Iran and New Zealand have only played each other twice before, and this will be their first meeting in a competitive match.

Their first game ended in a 0-0 draw in New Zealand in 1973. Thirty years later, Iran won 3-0 in Tehran, with Ali Karimi scoring twice before Hossein Kaebi added a third goal.

The predictions give Iran the edge. In 25,000 simulations run by Opta, Iran won 53.8 percent of the time. New Zealand won 20.4 percent of the simulations, while 25.8 percent ended in a draw.

Iran vs New Zealand – World Cup

What else is shaping the World Cup?

Uruguay’s travel plans hit by delays before World Cup opener

Uruguay’s preparations for their World Cup opener have been disrupted after travel problems delayed the team’s arrival in the US.

The squad had been due to fly from Cancun, Mexico, before Monday’s Group D match against Saudi Arabia in Miami. However, reports in Uruguay said the charter flight was not cleared to enter the US, forcing the team to make alternative arrangements.

The Uruguayan Football Association (AUF) said the delay was outside its control. A replacement plane was eventually organised, with the team expected to reach South Florida only about a day before kickoff.

“Due to problems beyond the control of the AUF, the departure from Mexico has been delayed,” the association said in a statement. “The squad is resting at the hotel. The new departure time set by FIFA is 4:15pm [21:15 GMT].”

Japan fans continue World Cup cleanup tradition after Netherlands draw

The blue bags Japanese fans waved while celebrating their team’s goals, and then stayed behind for something else after the match ended.

Following Japan’s 2-2 draw with the Netherlands, supporters stayed behind to collect rubbish from the stands before leaving the stadium, continuing a tradition that has become a familiar part of the World Cup.

The cleanup effort first caught global attention at the 1998 tournament in France, and Japanese fans have kept it going at every World Cup since.

Iranian Americans divided over Team Melli

As Iran prepare to begin their World Cup campaign in Los Angeles, members of the Iranian American community in Westwood, or “Tehrangeles”, remain split over how to respond.

While some opposition activists plan protests against the team, others are setting politics aside to support the football. Business owner Roozbeh Farahanipour told Al Jazeera’s reporter Ali Harb that “the community is divided” and there is no consensus on whether to boo the national team or back the US-Israel war against Iran.

Trudeau defends attending US match instead of Canada’s opener

Former Canadian Prime Minister Justin Trudeau attended the US World Cup opener against Paraguay in California instead of Canada’s game against Bosnia and Herzegovina in Toronto.

Trudeau said he chose to be at the game in Inglewood because his girlfriend, singer Katy Perry, was performing in the pre-match show at SoFi Stadium.

“Sometimes supportive boyfriend duties call. But you know who I’m rooting for to take the Cup,” he wrote on X.

Canada’s opener in Toronto and the US match in Los Angeles were played just hours apart, prompting some fans to question why the former prime minister was not supporting the home team.

Trudeau served as Canada’s prime minister from 2015 to 2025.

After returning to the World Cup for the first time since 1974, Haiti’s campaign has given people a rare reason to celebrate.

For Olivier Woodensky Pierre, the World Cup is a dream come true. He is the only player in Haiti’s squad who still lives in the country. Born in Cite Soleil, one of the poorest areas in the capital, Port-au-Prince, Pierre hopes the team’s achievement will inspire young people back home.

“Every player always wishes to play in the World Cup. That was my dream. That’s why I’m fighting to be here. I got the chance to be selected to play in the World Cup. I am advising the youth not to be discouraged. Keep fighting, work, and be disciplined,” Pierre told Al Jazeera’s Teresa Bo.

Haiti’s qualification has brought a sense of hope to a country going through one of the most difficult periods in its recent history. Gangs control large parts of the capital, violence has displaced hundreds of thousands of people, and many Haitians have taken to the streets to demand peace while also celebrating the team’s return to football’s biggest stage.

The journey to the World Cup was far from straightforward. Because of the ongoing political crisis, Haiti had to play its home qualifiers abroad. There was also a lack of funding.

“It was really difficult before because there were no sponsors to finance the team. You know, since we qualified for the World Cup, FIFA provided money for preparation, and the government provided $4m that were crucial to help us prepare,” Thecieux Jeanty of the Haitian Football Federation told Al Jazeera.

Pastor Winston Noel also voiced disappointment over US visa restrictions affecting Haitians.

“FIFA must talk to the Trump administration to tell them that this cannot be the case because it is the World Cup. All countries that qualify must have their fans to come and support their teams,” he said.

“The World Cup is something special for us Haitians. Many children here in Haiti will participate in the World Cup, even though this generation doesn’t know the names of all the players. But we are very happy because it’s a great achievement for us,” Noel said.

Haiti eventually opened their World Cup campaign with a 2-0 defeat to Scotland, but for many supporters the tournament is about more than results. It remains a rare moment of pride, unity and hope for a country that has endured years of hardship.

The World Cup continues on Saturday, with Brazil beginning their campaign and three more group-stage matches taking place across North America.

Brazil take on Morocco in the day’s biggest match, while Qatar face Switzerland, Haiti meet Scotland and Australia play Turkiye as more teams get their tournaments under way.

Recommended Stories

list of 4 itemsend of list

Away from the football, there has been plenty to talk about. Donald Trump skipped the United States’ opener, former Canadian Prime Minister Justin Trudeau was at the US game instead of Canada’s, and Ghana midfielder Thomas Partey will miss his team’s first match after Canada denied his visa application.

In Peru, police made headlines after carrying out a drug raid dressed as World Cup mascots.

Here is what to know:

What’s the World Cup schedule on June 13?

Qatar take on Switzerland at BC Place in Vancouver, with kickoff scheduled for 12pm local time (19:00 GMT).

The day’s action concludes with Haiti meeting Scotland at AT&T Stadium in Arlington, Texas. Kickoff is set for 8pm local time (01:00 GMT on June 14).

Australia and Turkiye then get Group D under way at Lumen Field in Seattle, with kickoff at 9pm local time (04:00 GMT on June 14).

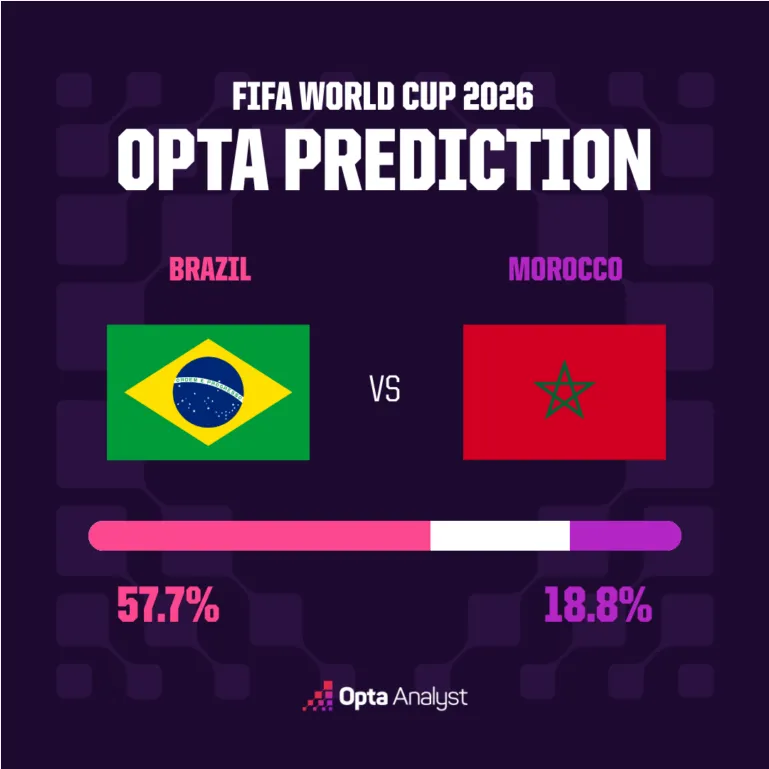

What do the predictions say for Brazil vs Morocco?

Brazil and Morocco have only faced each other once before at a World Cup, with Brazil winning their 1998 group-stage meeting. Morocco got their revenge in a 2-1 friendly win in 2023.

Brazil have won seven of their eight World Cup matches against African opponents, with their only defeat coming against Cameroon in 2022.

The five-time champions have not lifted the trophy since 2002. Since then, they have usually exited in the quarterfinals, apart from their run to the 2014 semifinals.

Opta’s 25,000 simulations give Brazil a 57.7 percent chance of winning. A draw happened in 23.5 percent of the projections, while Morocco won in 18.8 percent.

The winner could put themselves in a strong position to top Group C.

What do the predictions say for Qatar vs Switzerland?

Qatar and Switzerland have met only once before, with Qatar claiming a 1-0 friendly win in 2018 thanks to a late goal from Akram Afif. Afif is among nine players from that squad still in Qatar’s 2026 World Cup team, while Switzerland have seven survivors from that defeat, including Granit Xhaka and Remo Freuler.

Opta’s 25,000 simulations make Switzerland the clear favourites in this Group B clash, giving them a 76.0 percent chance of victory. Qatar won just 9.1 percent of the projections, while 14.9 percent ended in a draw.

A point would likely be considered a positive result for the Gulf side.

What do the predictions say for Australia vs Turkiye?

Australia and Turkiye have met only twice before, with Turkiye winning both friendlies in 2004. Turkiye have also won all four of their previous World Cup matches against Asian opponents.

Opta’s 10,000 simulations give Turkiye a 55.3 percent chance of victory, compared with 20.5 percent for Australia and 24.1 percent for a draw.

Neither side has a strong record in World Cup openers, however. Turkiye have lost both of their previous first matches, while Australia have lost five of their six opening games.

What do the predictions say for Haiti vs Scotland?

Haiti and Scotland have never faced each other before, making this one of several first-time matchups at the expanded 48-team World Cup. It will also be Haiti’s first-ever game against a team from the British Isles.

Opta’s 25,000 simulations make Scotland clear favourites, giving them a 59.0 percent chance of victory. Haiti won 19.2 percent of the projections, while 21.8 percent ended in a draw.

Haiti vs Scotland

What else is shaping the World Cup?

The football has only just started, but the World Cup is already making headlines away from the pitch, too.

Trump did not attend the US World Cup opener

The US president did not attend the US men’s national team’s World Cup opener against Paraguay in Los Angeles.

His absence drew attention because Trump has recently attended several high-profile sporting events, including Game 3 of the NBA Finals earlier this week. He is also expected to host a UFC event at the White House on Sunday.

A White House official said Trump instead plans to attend the World Cup final on July 19 at MetLife Stadium in East Rutherford, New Jersey.

The US president called into a USMNT team meeting with some words of support via Andrew Giuliani, the White House’s World Cup task force CEO.

Partey denied entry into Canada

Ghana midfielder Thomas Partey will miss his country’s World Cup opener against Panama after Canada denied his visa application while he awaits trial in the United Kingdom on multiple rape charges, which he denies.

FIFA confirmed on Friday that the 32-year-old would not be permitted to travel from Ghana’s base camp in Smithfield, Rhode Island, to Toronto for Wednesday’s match.

“His visa application has been refused by the Canadian government,” FIFA said in a statement.

“FIFA is not involved in the immigration processes of host countries, including the adjudication of visas. As with previous FIFA events, the host government ultimately determines who receives a visa and is admitted into the country.”

Trudeau attends the US’s World Cup

As Canada and the US kicked off their World Cup campaigns on the same day, former Canadian Prime Minister Justin Trudeau was in California rather than Toronto.

The 54-year-old did not attend Canada’s 1-1 draw with Bosnia and Herzegovina at BMO Field. Instead, he was at SoFi Stadium in Inglewood alongside pop singer Katy Perry, who performed during the pre-match opening ceremony before the US faced Paraguay.

Peruvian officers use World Cup mascot costumes in Lima drug bust

Peruvian police have gone viral after carrying out a drug raid in Lima dressed as World Cup mascots.

Video shared by police showed officers dressed as World Cup mascots breaking through a metal gate with a battering ram before entering the property.

Once inside, they arrested a suspected drug dealer and recovered weapons and bags of what authorities believe were narcotics.

The World Cup may be decided on the pitch, but another competition is already under way off it: Which host city has the best food?

In a report for Al Jazeera, Lou Browne travelled across North America to find out what fans can expect beyond the stadiums.

In Mexico City, taco vendors are hoping the tournament brings more customers. “Well, now the World Cup is coming, and we hope we’ll get customers,” a tortilla cook at El Califa de Leon told Al Jazeera. “I imagine there will be a lot of people, foreigners or locals.”

Philadelphia is proudly backing its famous Philly cheesesteak. Locals say visitors should learn how to order properly. “You want to tell them what kind of cheese you want,” Anthony Rossi, a cook at Geno’s Steaks, explained. “And you say if you want onions, which is ‘wit’ or ‘wit-out’ … Keep it simple.”

Across the border, Toronto is making the case for poutine, the Canadian dish of fries topped with gravy and cheese curds. “Poutine is the … not the best … dish, but poutine is from Canada,” said Lisa Deni, a French tourist.

In Kansas City, barbecue is a point of pride. “This is really good,” diner Camilla Thomas said. “We’ve been enjoying coming here. and bringing people from out of town here and giving them a little taste of Kansas City.”

And in Miami, locals insist the Cuban sandwich is a must-try. “The Cuban sandwich, croquetas, and cafecito are really the way to go,” said Daniel Figueredo, cofounder of Sanguich. “The Cuban sandwich really is the thing you have to have when you come to Miami.”

For fans travelling across North America this summer, the hardest choice may not be picking the World Cup winner, but deciding which host city serves the best food.

Love Island fans were left fuming after the latest episode and took aim at two islanders they called ‘shady’ after their sneaky move

Samraj, Aidan, Lorenzo, Sean, Sam on Love Island(Image: ITV)

Love Island fans were fuming at a “shady” duo. Viewers were less than impressed after Lorenzo and Priya snuck away to the hideaway for a flirt and a kiss.

But, while the name of the game is to find your perfect match, many viewers criticised the pair for their sneaky moves. On X (formerly Twitter), one user complained: “Priya and Lorenzo are both shady af.”

Another wrote: “Lorenzo is actually finished. Jasmine is gonna COOK him.” And a third said: “Very embarrassing fumble by Priya and Lorenzo, they will be evicted from my villa.”

It follows the introduction of the two new bombshells to the group. They were quick at work, selecting the two boys they wanted to share an intimate date with.

But as per Love Island’s unwritten rules, there was a twist. The girls in the villa sat back and watched as events unfolded.

Ope, whose comments to the boys raised eyebrows among the girls, sat down to enjoy a date with Victoria and quickly made his move by kissing her hand.

Despite appearing to be building on things with Angelista, his comments about coupling up in the villa didn’t go down well. Explaining that things have been progressing at a slower pace than he’s used to.

“So you still haven’t had your first kiss?” Victoria asks. “No, are you going to be my first kiss?” Ope responds cheekily.

It left the girls fuming, with Angelista ending up in tears in the bedroom. Sam’s date went much better, though, as he appeared respectful toward the girls in the villa.

But the reaction from the girls watching on the big screen left a lot to be desired. With Cocktail Night drawing to a close, the boys made their way back to the Villa with Namibia and Victoria, but they were met with a frosty welcome back.

They seemed unsure why until Aidan spotted the big screen and realised what had happened. He told the boys, “Oh no, they watched it.”

And that left Ope very nervous. As he attempted to pull Angelista for a conversation, she abruptly shut down his request. Providing a frank assessment of what she saw, Jasmine tells one Islander: “A bunch of you acted like boys, and a bunch of you acted like men.”

Just before the episode aired, George Knight spoke about his sudden exit from the ITV2 show for the first time since his departure. The bombshell decided to quit the villa just days after entering.

He said in an Instagram video: “Hello, everyone. Just wanted to take a moment and come on and say a massive, massive thank you to every single person who has reached out over the past two days, wishing me their love, their support, and all their well wishes.

“It has been completely overwhelming, and I am trying to get back to every message, which is pretty, pretty much impossible. But thank you so much.”

He continued: “And I think moments like this give you a massive kind of perspective on the bigger picture, and as fun and as great my six days in the villa were, it’s obviously important for me to be here with my family, so thank you so much.

“It’s been, as I said, completely overwhelming, and a massive thank you to all of ITV’s welfare team and the execs who have been amazing. Hopefully it’s not the last you see of me, and looking forward to the year ahead, and yeah, thanks again, guys.”

Love Island continues tomorrow at 9pm on ITV2 and ITVX

Sen. Ted Cruz, R-Texas, speaks Wednesday at a Senate subcommittee hearing focused on the recent surge in popularity of sports betting and betting by minor. Photo by Erika Tulfo/Medill News Service

WASHINGTON, May 20 (UPI) — As sports betting and prediction market platforms like Kalshi and Polymarket grow in popularity, U.S. senators on Wednesday weighed the need to regulate use of the platforms by minors.

One main issue senators raised during a hearing by the Senate Commerce Subcommittee on Consumer Protection, Technology and Data Privacy was how prediction markets use social media to advertise their platforms to underage users, putting them at risk of a gambling addiction.

“Young people are being inundated with advertisements on social media. Their favorite influencers and sports figures are introducing minors to betting,” said Sen. Marsha Blackburn, R-Tenn., who chaired the hearing.

“This is not safe. It needs to stop, and advertising to minors is disgusting,” Blackburn said.

The “No Sure Bets: Protecting Sports Integrity in America” hearing was intended to discuss the prevalence of sports betting and its impact on the integrity of matches.

It followed a unanimous Senate vote last month to ban its members and their staffs from trading on prediction market platforms, and the senators seemed determined to do more. Issues surrounding gaming continue to be a hot topic in Congress, where more than 10 active bills are related to prediction markets.

Some recent high-profile scandals surrounding prediction market platforms have also drawn attention to the industry, including the arrest of U.S. Army soldier Gannon Van Dyke last month. He was charged with using classified information to profit from a Polymarket wager related to the capture of Venezuelan president Nicolás Maduro in January.

In the same month, Kalshi fined and suspended from its platform three congressional candidates for betting on the outcomes of their own elections.

In the hearing, Sen. John Hickenlooper, D-Colo., criticized prediction markets like Kalshi for hiring social media influencers to promote their platforms to adolescent users.

“I think it’s specifically dangerous for minors to get into sports betting, and especially on prediction markets. That’s why almost all the states say [the legal betting age] is 21, not 18,” Hickenlooper said.

“Prediction markets let users as young as 18 bet on sports, but they also market their products to younger, more vulnerable audiences who are in many cases adept at getting around the platform precautions.”

A study released in January by Common Sense Media found that more than one-third of adolescent boys aged 11 to 17 admitted to engaging in gambling over the past year. Almost 60% of those who have been gambling said that they were exposed to gambling content through social media.

Kalshi, in an email, denied advertising to minors and pointed to recently implemented consumer protection measures, including requesting a selfie from the user to supplement documents verifying their age.

Hickenlooper grilled Patrick McHenry, a former U.S. representative now acting as senior adviser to the Coalition for Prediction Markets, on the guardrails to ensure underage users could not access their platforms.

McHenry pointed to the Commodity Futures Trading Commission, which oversees prediction markets and regulates them as a form of financial derivative rather than an avenue for gambling.

“The CFTC is a cop on the beat. It has the capacity to oversee this market, just as they’ve done with a broader commodities marketplace that has been around and well-versed for decades,” he said.

The Commodity Futures Trading Commission’s jurisdiction over prediction markets has been a contentious topic, since users can trade event contracts related to sports, weather, politics and more.

The Prediction Markets Are Gambling Act, which Sen. Adam Schiff, D-Calif., introduced in March, seeks to ban prediction markets from listing contracts that resemble sports bets, arguing that such contracts are considered gambling and should be subject to state regulation.

The agency argues that sports event contracts were treated as “swaps,” a term used to describe events that have potential economic consequences.

But Sen. Ted Cruz, R-Texas, pushed back against the classification of sports contracts on prediction markets as financial derivatives.

“What is the economic consequence of whether a pitcher throws a ball or strike?” he asked.

Another bill specifically targeting digital gambling advertisements to minors was introduced Monday. Sens. Richard Blumenthal D‑Conn., and Katie Britt, R‑Ala., are advocating the Gaming Advertisement to Minors Enforcement Act, which would implement a federal ban on sports betting ads on social media platforms for minors.

Dogecoin is trading near $0.116 in May 2026, with a market cap of around $17.9 billion and a 24-hour volume of over $2.37 billion.

The latest Dogecoin price prediction data shows room for a move toward the $0.13 to $0.25 range in 2026, but DOGE still needs stronger meme coin demand before a larger rally becomes realistic.

For traders looking beyond older meme coins, Meme Punch and Poly Truth add two newer presale stories through P2E gaming and prediction market data.

This article breaks down DOGE’s 2026 outlook, the main rally drivers, and how $MEPU and $PTRUE compare with Dogecoin’s meme coin setup.

How Dogecoin Is Performing in May 2026

Dogecoin still has one of the strongest brands in crypto. It ranks inside the top 10 by market value, and CoinGecko shows DOGE up 22.2% over 30 days, which keeps it active on trader watchlists.

Daily volume also supports the short-term case. DOGE’s 24-hour trading volume was about $2.37 billion, which shows a recent rise in market activity and gives traders enough liquidity for short-term moves.

However, DOGE is no longer a small coin. A market cap near $18 billion means each major price move needs real buying pressure, not only social media noise.

Dogecoin Price Prediction for 2026

CoinCodex gives DOGE a short-term target of $0.1302 for one month and $0.1491 for three months. Its near-term table also shows a 5-day target around $0.1142, which keeps DOGE close to its current range before any stronger move develops.

Changelly gives a wider full-year 2026 range. Its analysis places DOGE between $0.0957 and $0.142, with an average price near $0.119. For May 2026, Changelly estimates a range between $0.108 and $0.131, with an average near $0.120.

Binance’s prediction page takes a different approach because its figures are based on user input and shown on an “as is” basis. The page also states that the data does not represent Binance’s own view or advice, which makes it useful as crowd input rather than a firm forecast.

Can DOGE Stay a Top Meme Coin in 2026?

Dogecoin still has the main ingredients that keep meme coins alive. It has deep liquidity, wide exchange access, a long trading history, and a community that can bring quick attention during bullish periods.

The harder part is growth from here. DOGE already has a large market cap, so a 2x or 3x move requires much more capital than it would for a smaller meme coin or early-stage presale.

The $0.13 to $0.15 zone is the first area to watch because CoinCodex’s one-month and three-month targets sit near that range. A cleaner move above those levels would make the 2026 outlook stronger.

What Could Push Dogecoin Higher?

Dogecoin’s next rally needs more than past fame. DOGE can still move sharply, but only if volume, social demand, and wider market strength return together.

The strongest DOGE drivers are easy to track.

Bitcoin strength can bring traders back into higher-risk crypto.

Meme coin rotation can lift DOGE, SHIB, PEPE, and other large meme assets.

Higher daily volume can confirm that buyers are returning.

Social attention can turn DOGE into a retail-led trade again.

Clean breakouts above near-term resistance can make short-term targets more realistic.

If those signals line up, DOGE can stay one of the main meme coins to watch in 2026. Without them, the price may stay close to the current forecast range.

Why New Meme Coin Presales Are Getting More Attention

Dogecoin gives traders liquidity and recognition, but newer presales can move on smaller starting bases. They also have more room to shape a fresh story before wider market exposure.

Meme Punch and Poly Truth show two different directions for presale demand. Meme Punch builds around meme coin gaming, while Poly Truth focuses on prediction market intelligence.

Meme Punch ($MEPU)

Meme Punch turns meme coin culture into a medieval P2E battle arena. Players choose meme-inspired knights, fight rivals, climb the leaderboard, and earn $MEPU rewards.

The game loop is easy to scan.

Players choose from meme fighters such as Pepe, Doge, Floki, Brett, and Pudgy Penguin.

Arena battles decide leaderboard progress.

Winners earn $MEPU rewards.

$MEPU can be used for weapons, skins, and special powers.

Staking adds another token use inside the project.

$MEPU has a total supply of 10 billion tokens.

Presale: 40%

DEX/CEX liquidity: 12%

Marketing: 16.5%

Game rewards: 9.5%

Staking: 14.5%

Project funds: 7.5%

Poly Truth ($PTRUE)

Poly Truth gives the presale market a data-led angle through prediction market intelligence. The project uses AI-powered analysis to help users read active events across crypto, sports, politics, and other markets.

Its system has three parts.

The Runners collect data from active prediction events across the internet.

The Starlet compares sources, finds patterns, and calculates probability scores.

The Presenter turns the analysis into event reports that show which outcome has stronger data support.

$PTRUE has a total supply of 11.5 billion tokens.

Presale: 40%

Liquidity pool: 17%

Development: 13%

Team: 10%

Staking rewards: 10%

Marketing: 8%

Community and airdrops: 2%

DOGE vs. $MEPU and $PTRUE

Dogecoin is still the established meme coin in this group. It has the liquidity and name recognition that smaller tokens usually need years to build.

Meme Punch offers a more active meme coin angle because $MEPU is tied to gameplay, battle rewards, upgrades, and staking. Poly Truth moves away from meme culture and gives traders a presale tied to data, prediction markets, and event analysis.

The comparison is simple.

DOGE gives traders an established meme coin with deep liquidity.

$MEPU adds P2E gaming to meme coin demand.

$PTRUE adds prediction market data to the presale market.

DOGE may stay the safer meme coin benchmark because it already trades across major markets. $MEPU and $PTRUE offer earlier-stage exposure to newer stories that are still building attention.

Is DOGE Still One of the Best Meme Coins to Buy Now?

The Dogecoin price prediction for 2026 still supports a measured bullish case, but it does not point to an easy return to old highs.

CoinCodex’s one-month and three-month targets keep DOGE in the $0.13 to $0.15 area, while Changelly’s full-year range stays between $0.0957 and $0.142.

DOGE still has the liquidity, brand power, and community needed to lead another meme coin move. The stronger rally case needs rising volume, better market sentiment, and a broader meme coin rotation.

For traders comparing old and new meme coin stories, Dogecoin still holds the benchmark spot. Meme Punch brings a playable meme coin model through $MEPU, while Poly Truth adds a different presale route through $PTRUE and prediction market intelligence.

Disclaimer: This article is for informational purposes only and does not constitute financial or investment advice. ModernDiplomacy.eu is not a licensed crypto-asset service provider under EU regulation (MiCA). Cryptocurrencies are highly volatile and involve significant risk. Always conduct your own research and consult a licensed advisor before making any investment decisions.

As he reaches 100, broadcaster and naturalist Sir David Attenborough has spoken of the changes he has seen in his lifetime – and the horrifying consequences of climate change in the years to come

Sir David has issued a dire warning about humanity’s future(Image: Dave Benett, Dave Benett/Getty Images)

Legendary broadcaster Sir David Attenborough made a worrying prediction for 2030 – and predicted the state of the planet is likely to get worse after that. The iconic naturalist celebrates his 100th birthday on Friday (May 8) and he has long been heralded as the natural world’s biggest champion.

He has also been vocal about the threats facing the Earth. In 2020, as the world was in lockdown as a precaution against Covid-19, Sir David made what he called a “personal witness statement” about the threat of climate change. Many of the dire predictions he made about the world are beginning to come true.

Back in 2020 he warned that 10 years from that date, with much of the Amazon rainforest becoming a dry desert and the polar icecaps shrinking, the effects of climate change will become truly irreversible – and threaten the extinction of humanity.

As he released his Netflix documentary, A Life on Our Planet, Sir David made a personal appeal to world leaders. He said: “There are short-term problems and long-term problems. Politicians are tempted to deal with short-term problems all the time and neglect long-term problems.

“{Climate change] is not only a long-term problem, it is the biggest problem humanity has ever faced. Please examine it, and please respond.”

The prognosis for the rest of the century looks pretty bleak if Sir David’s predictions are to be believed. He said that if he had been born in 2020, instead of 1926, he would be witness to the full range of climate collapse: “In the 2030s, The Amazon Rainforest, cut down until it can no longer produce enough moisture, degrades into a dry savannah, bringing catastrophic species loss… and altering the global water cycle.

“At the same time, the Arctic becomes ice-free in the summer. Without the white ice cap, less of the sun’s energy is reflected back out to space. And the speed of global warming increases.”

By the 2040s, just 14 years from today, Sir David predicts: “Throughout the north, frozen soils thaw, releasing methane, a greenhouse gas many times more potent than carbon dioxide, accelerating the rate of climate change dramatically.”

Through the 2050s, as today’s schoolchildren reach middle age, the world’s seas will become a sterile desert: “As the ocean continues to heat and becomes more acidic, coral reefs around the world die. Fish populations crash.”

Into the 2080s, mankind truly becomes an endangered species: “Global food production enters a crisis as soils become exhausted by overuse. Pollinating insects disappear… and the weather is more and more unpredictable.”

The stable climate that has endured longer than human civilisation will be lost forever by 2100, Sir David says.

“Our planet becomes four degrees Celsius warmer,” he adds, “Large parts of the earth are uninhabitable. Millions of people rendered homeless. A sixth mass extinction event… is well underway.”

He describes these various tipping-points as “a series of one-way doors,” with each bringing irreversible change.”

As he muses on his long life, Sir David warren that someone born today who lives as long as he has will see almost unimaginable change: “Within the span of the next lifetime, the security and stability of the Holocene, our Garden of Eden… will be lost.”

Average global temperatures have risen by more than 1C since the 1850s. Since 2015, every successive year has brought record high temperatures – causing heatwaves, floods, droughts, and fires as well as irrevocable habitat loss for many species.

Sir David thinks that humanity is the species most under threat. He said: “I used to think this was about saving the planet, and now I realise it’s not …nature will always look after itself. It’s about saving us.”