Saudi Arabia faces the most precarious moment yet of its economic reinvention.

Author of the article:

Bloomberg News

Abeer Abu Omar

Published Jul 14, 2024 • 5 minute read

You can save this article by registering for free here. Or sign-in if you have an account.

b{virrqb}bz}9uhsb8o5a4(n_media_dl_1.pngBloomberg

Article content

(Bloomberg) — Saudi Arabia faces the most precarious moment yet of its economic reinvention.

Eight years after now-Crown Prince Mohammed bin Salman unveiled Vision 2030, his blueprint for a life after oil, delays and scalebacks with the multitrillion dollar makeover are laying bare the pressure on the kingdom’s finances.

With the budget in deficit for six straight quarters, Saudi Arabia has become the biggest issuer of international debt in emerging markets. And its decision to cut oil production with other OPEC+ members in 2023 has failed to raise export revenues substantially.

Advertisement 2

This advertisement has not loaded yet, but your article continues below.

THIS CONTENT IS RESERVED FOR SUBSCRIBERS ONLY

Subscribe now to read the latest news in your city and across Canada.

Exclusive articles from Barbara Shecter, Joe O’Connor, Gabriel Friedman, Victoria Wells and others.

Daily content from Financial Times, the world’s leading global business publication.

Unlimited online access to read articles from Financial Post, National Post and 15 news sites across Canada with one account.

National Post ePaper, an electronic replica of the print edition to view on any device, share and comment on.

Daily puzzles, including the New York Times Crossword.

SUBSCRIBE TO UNLOCK MORE ARTICLES

Subscribe now to read the latest news in your city and across Canada.

Exclusive articles from Barbara Shecter, Joe O’Connor, Gabriel Friedman, Victoria Wells and others.

Daily content from Financial Times, the world’s leading global business publication.

Unlimited online access to read articles from Financial Post, National Post and 15 news sites across Canada with one account.

National Post ePaper, an electronic replica of the print edition to view on any device, share and comment on.

Daily puzzles, including the New York Times Crossword.

REGISTER / SIGN IN TO UNLOCK MORE ARTICLES

Create an account or sign in to continue with your reading experience.

Access articles from across Canada with one account.

Share your thoughts and join the conversation in the comments.

Enjoy additional articles per month.

Get email updates from your favourite authors.

Sign In or Create an Account

or

Article content

Here is a look at the key stress points.

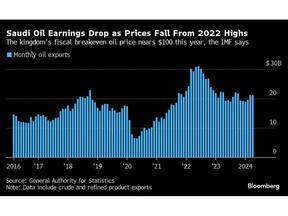

Petrodollar Reliance

The Gulf country’s oil earnings have dropped around one-third from 2022 levels, when Brent crude averaged nearly $100 a barrel thanks to Russia’s invasion of Ukraine. That’s weighing on the kingdom’s overall economic stability as it keeps spending on Prince Mohammed’s huge projects, which include everything from the new city of Neom to tourist resorts, football leagues and AI investments.

“The vision is facing a test of reality and there are adjustments being taken,” said Jean-Michel Saliba, Bank of America Corp.’s Middle East and North Africa economist. “It is a sign of maturity. I don’t think it’s a sign that the vision is being derailed.”

Goldman Sachs Group Inc. found that Saudi Arabia’s sovereign-risk score — a measure that takes into account financial and governance metrics — worsened the most after Israel among emerging markets during the first half of the year. A ranking by Morgan Stanley in June reached a similar conclusion, with the kingdom among “key laggards.”

High Spending

“My biggest concern is that the rise in expenditure leads to substantial deficits that are structural, rather than temporary or cyclical,” said Justin Alexander, director of Khalij Economics and an analyst for consultant GlobalSource Partners.

Top Stories

Get the latest headlines, breaking news and columns.

By signing up you consent to receive the above newsletter from Postmedia Network Inc.

Thanks for signing up!

A welcome email is on its way. If you don’t see it, please check your junk folder.

The next issue of Top Stories will soon be in your inbox.

We encountered an issue signing you up. Please try again

Article content

Advertisement 3

This advertisement has not loaded yet, but your article continues below.

Article content

Rising debt captures the changes in Saudi finances over the past decade. While still low by international standards, the share of government debt to economic output has risen from 1.5% in 2014 and is on track to exceed 31% toward the end of the decade, according to the International Monetary Fund.

Saudi Arabia could draw more scrutiny in the bond market and from credit rating companies if the ratio “creeps up more rapidly than forecast,” said Alexander.

Record Debt

The government and other Saudi entities, including banks, the wealth fund and oil giant Aramco, have raised over $46 billion in dollar and euro bonds so far this year. That’s meant that Saudi Arabia has displaced China as the most prolific developing-nation issuer in international bond markets, according to data compiled by Bloomberg.

“The fiscal deficits will have to continue being funded by both external issuance on the Eurobond front and domestic issuance,” said Carla Slim, an economist with Standard Chartered Plc.

Still, the government has the flexibility — as it’s already showing — to reduce or delay investments in its so-called giga-projects, according to Jim Krane, a fellow at Rice University’s Baker Institute for Public Policy in Houston.

Advertisement 4

This advertisement has not loaded yet, but your article continues below.

Article content

“Since there’s no organized political opposition, there is little harm in scaling back or even making a dramatic U-turn on your 10-year development plan,” said Krane.

Rising Liabilities

The country’s external financial position is under pressure as it ramps up imports. The current-account balance — the broadest measure of trade and investment — will drop to almost zero in 2024 and shift into deficit from next year, the IMF forecasts, after being in surplus to the tune of 13% of GDP in 2022.

One result is “an unprecedented increase” in the foreign liabilities of Saudi lenders, according to Barclays Plc, given their growing role of providing hard currency to help meet domestic financing needs.

Local liquidity for Saudi banks remains stretched, as measured by the interest rates they charge one another for loans. The three-month Saudi Interbank Offered Rate has averaged a record of more than 6% this year.

The IMF says the Saudi government needs Brent to be nearly $100 a barrel to balance its budget, about $15 more than current levels. Bloomberg Economics estimates the break-even price at $109 per barrel, once domestic spending by the Public Investment Fund — the sovereign wealth fund — is taken into account.

Advertisement 5

This advertisement has not loaded yet, but your article continues below.

Article content

Foreign Investment

Foreign direct investment has been slow to materialize outside the oil and gas sector, making it harder for the crown prince to make his ambitions a reality.

The government wants to attract $100 billion of FDI annually by 2030, a haul roughly three times bigger than it’s ever achieved. Inflows reached around $2.5 billion during the first quarter, according to government data, a fraction of this year’s goal.

FDI was just $12.3 billion in 2023, 60% less than neighboring United Arab Emirates, a much smaller economy, according to the United Nations Conference on Trade and Development.

Partly because of that, non-oil growth — a crucial gauge for the government — eased to the slowest pace since the coronavirus pandemic during the first quarter. That was one reason the IMF recently downgraded its forecast for Saudi Arabia’s overall economic expansion this year to 2.6%. In late 2023, it was forecasting 4%.

Officials expect fiscal expenditure at around $333 billion this year. That would be a decline from 2023, underscoring the government’s newfound caution.

Advertisement 6

This advertisement has not loaded yet, but your article continues below.

Article content

Even so, the kingdom’s budget will be in the red for years to come, meaning domestic institutions like the PIF and Armaco will remain on the hook for many of the giga-projects.

What Bloomberg Economics Says…

“The biggest obstacle facing Saudi Arabia continues to be its unwaning reliance on oil. Although the kingdom has tried to lift prices through OPEC+, supply coming from elsewhere hindered that effort. Authorities need to spend to keep the economy ticking and the population happy, but maintain enough restraint to contain the budget deficit.”

— Ziad Daoud, chief emerging-markets economist. Read more here.

For all the setbacks and pressures, the crown prince is determined to see his goals through, even if they take a different shape.

“The transformation is now institutionalized,” said Karen Young, a senior research scholar at Columbia University’s Center on Global Energy Policy. “The larger process of diversification is well underway, and I don’t see a large chance of backtracking.”