It was not the first time Lam, who has been investing on and off in Hong Kong stocks since the late 1990s, had seen it happen.

The index dropped below 15,000 points during SARS in 2003, the Global Financial Crisis in 2008, and zero-COVID lockdowns in 2022.

But while ebbs and flows are part of the investment game, Lam said watching the key measure of Hong Kong’s stock market tumble “back to square one” felt different this time.

“It seems I cannot see the future,” Lam told Al Jazeera by phone from Hong Kong.

The reason, Lam said, is China.

As Beijing increases its control over all aspects of life in Hong Kong, including the economy, and gloom persists about the state of China’s post-pandemic recovery, investors have been voting with their money and looking to other markets.

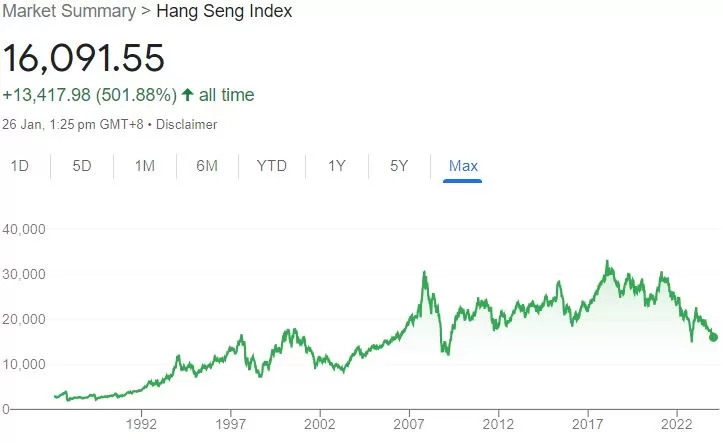

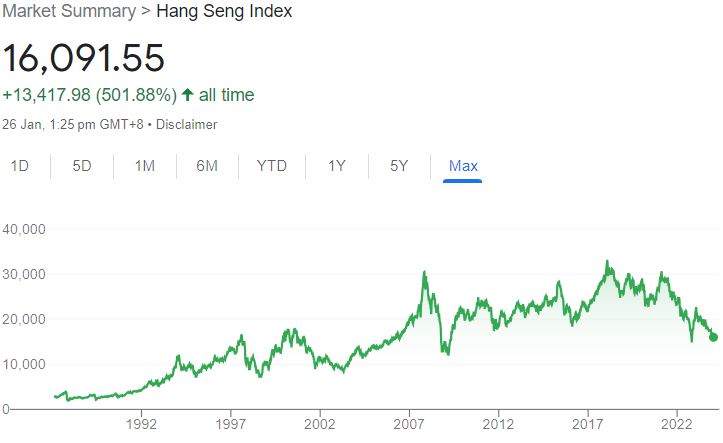

More than a quarter-century after Hong Kong’s return to China, the Hang Seng is more or less back to where it was during its final days as a British colony.

On Friday, the index hovered below 16,100 points – lower than it was on July 1, 1997, the day of the handover.

Over the same period, stocks in the United States, Japan and other popular markets have flourished.

Investors in the SP500, the most popular measure of the performance of the US market, have seen their money grow nearly 10-fold since 1997.

“If there’s any new announcement from the Chinese government about regulations or the control of some industry, then the market can fluctuate very seriously,” said Lam, whose investment portfolio includes blue chip stocks, fixed-term deposits and property.

“The relationship between Hong Kong and China is closer and closer, the control is tighter, so we cannot ignore what they are doing in China.”

Hong Kong has had a front-row seat to China’s crackdowns in recent years, from the imposition of a draconian national security law on the city to tightening regulation of corporate giants such as Alibaba and Tencent and raids on foreign companies on the Chinese mainland.

Many of China’s biggest companies are dual-listed in Hong Kong and China and make up a large portion of the Hang Seng Index along with Chinese banks and other tech companies.

At the same time, China’s economy has struggled to recover from the impact of COVID-19 and Beijing’s harsh pandemic restrictions, amid nagging structural issues including a shrinking population, high local government debt, and a slow-moving real estate crisis.

Gross domestic product officially grew 5.2 percent in 2023 – the weakest performance in decades, excluding the pandemic.

Despite Beijing’s insistence that China is open for business, foreign investors’ confidence is waning.

Last year, China recorded the first drop in foreign direct investment in 12 years, with inflows declining 8 percent to $157.1bn.

“When we look at broader business sentiment both for the financial sector and for the general economy – first and foremost, economic fundamentals both in Hong Kong and in China are not doing very well at the moment,” Chim Lee, a China analyst at the Economist Intelligence Unit, told Al Jazeera.

Lee said China hitting its economic growth target last year was “not particularly impressive” as Beijing set a relatively weak target.

Analysts estimate that some $6 trillion – the equivalent of over one-quarter of the entire output of the US economy – has been wiped off stock markets in China and Hong Kong since early 2021.

China’s CSI 300 Index, which measures the top 300 companies on the Shanghai and Shenzhen stock exchanges, has fallen more than 40 percent over the past three years, while the Hang Seng has fallen 50 percent over the same period, according to Bloomberg data.

Investors are instead flocking to other markets like Japan and the US where analysts predict a bullish 2024.

The Nikkei 255 Index, an index of the Tokyo Stock Exchange’s top companies, posted highs not seen in over 30 years last week, while the S&P 500 in New York closed at an all-time high for the sixth day in a row on Thursday.

“[Hong Kong’s] economy may now be no more than a large rounding error on China’s GDP but it still plays an important role in finance and capital market transactions for and with the Mainland. So it’s self-evident that bearish sentiment and beaten up stock price valuations in China proper wash over into [Hong Kong] too,” George Magnus, an associate at Oxford University’s China Centre and Research Associate at SOAS, London, told Al Jazeera.

Hong Kong’s declining rights and freedoms – which are supposed to be guaranteed until 2047 under an agreement known as “one country, two systems” – have added fuel to the crisis of confidence.

Since the passage of the national security law in 2020, the city’s political opposition and independent media have been all but wiped out and hundreds of people have been arrested for non-violent offences related to activism and speech.

Hundreds of thousands of Hong Kongers have left the city amid Beijing’s tightening control along with their money.

Lam said she decided last year to move her pension fund overseas and she plans to sell her remaining stock investments in Hong Kong at a loss.

“They say they want to do something, but we don’t see real action,” Lam said of the government’s policy on the economy.

In October, Hong Kong slashed stamp duty on property sales and stock transfers, but consumption and tourism have yet to recover to pre-pandemic levels.

Analysts say that reviving both Hong Kong and China’s economy will take much bolder action.

Beijing is considering a potential $278bn rescue plan for the stock market, Bloomberg reported this week, citing sources close to the matter, but many analysts argue broader structural reforms are needed to restore investor confidence.

A similar rescue plan deployed after a tumble in China’s stock market in 2015 produced mixed results – even though the government moved quickly and the overall economy was on a stronger footing.

Memories of that rescue plan and concerns that Beijing will not make difficult but necessary reforms are one reason why the rescue plan has been met with a lukewarm response, said Alicia Garcia Herrero, chief economist for Asia Pacific at Natixis.

“Here it’s really the market saying, I’m sorry you’re not growing. I don’t trust your numbers; your future looks gloomy – which wasn’t the case in 2015. It was perceived to be a temporary shock, so I think this is, to start, the difference,” Garcia Herrero told Al Jazeera.

Beijing arguably also has less room to manoeuvre this time thanks to its high levels of debt and limited scope of monetary easing.

“They’ve used so many bullets, the credibility of the next bullet is lower,” she said.