Article content

(Bloomberg) — The US economy remained at a comfortable cruising speed in the final stretch of 2024, powered by healthy consumer spending and creating even more separation from its global counterparts.

The US economy remained at a comfortable cruising speed in the final stretch of 2024, powered by healthy consumer spending and creating even more separation from its global counterparts.

(Bloomberg) — The US economy remained at a comfortable cruising speed in the final stretch of 2024, powered by healthy consumer spending and creating even more separation from its global counterparts.

Article content

Article content

Economists surveyed by Bloomberg project the government’s initial estimate of fourth quarter gross domestic product — the sum of goods and services produced — to show an annualized 2.7% increase. That would follow back-to-back quarters of about 3% growth.

Advertisement 2

This advertisement has not loaded yet, but your article continues below.

THIS CONTENT IS RESERVED FOR SUBSCRIBERS ONLY

Subscribe now to read the latest news in your city and across Canada.

SUBSCRIBE TO UNLOCK MORE ARTICLES

Subscribe now to read the latest news in your city and across Canada.

REGISTER / SIGN IN TO UNLOCK MORE ARTICLES

Create an account or sign in to continue with your reading experience.

THIS ARTICLE IS FREE TO READ REGISTER TO UNLOCK.

Create an account or sign in to continue with your reading experience.

or

Article content

Thursday’s report on US economic activity surfaces a day after the conclusion of the first Federal Reserve policy meeting of 2025. Against a backdrop of healthy demand and stubborn inflation, officials are widely expected to hold borrowing costs steady. At their December confab, policymakers signaled just two interest-rate cuts this year.

The GDP data are projected to show personal consumption of goods and services exceeded a 3% annualized pace for a second straight quarter, fueled by a strong labor market. That helps to explain how the US continues to outperform advanced economies in Europe and around the world.

In contrast to the US, figures in the coming week are predicted to reveal that the French economy stagnated in the closing months of 2024, as well as a slight contraction in Germany. Data on GDP in the broader euro area, also set for release on Thursday, are seen showing scant growth — extending a multi-year trend of sluggishness.

Monthly US household spending figures on Friday will likely point to momentum heading into 2025. Economists also expect the personal income and spending report to show a slight pickup in the Fed’s preferred inflation gauge from a month earlier.

Advertisement 3

This advertisement has not loaded yet, but your article continues below.

Article content

What Bloomberg Economics Says:

“While loan-delinquency rates have been rising — especially for lower-income households — wealthier households that account for about 40% of consumer spending have benefited from the equity-market rally and asset appreciation. We’ve taken that signal onboard in our 2025 consumption forecast, and now expect spending to slow more gradually than we previously did.”

— Anna Wong, Stuart Paul, Eliza Winger, Estelle Ou and Chris G. Collins, economists. For full analysis, click here

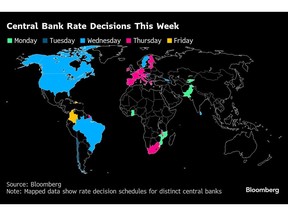

Looking north, the Bank of Canada is expected to cut rates by 25 basis points on Wednesday, a slowdown after two consecutive 50 basis-point cuts at a time US President Donald Trump’s tariffs threats are generating considerable uncertainty.

GDP data for November and a flash estimate for December will show the impact of the US election and Prime Minister Justin Trudeau’s sales tax holiday on the economy.

Elsewhere, rate cuts in the euro zone and Sweden and a 100 basis-point hike in Brazil are among the expected highlights. Several reports from Japan and a key speech by the UK chancellor will also keep investors occupied.

Top Stories

Get the latest headlines, breaking news and columns.

By signing up you consent to receive the above newsletter from Postmedia Network Inc.

Thanks for signing up!

A welcome email is on its way. If you don’t see it, please check your junk folder.

The next issue of Top Stories will soon be in your inbox.

We encountered an issue signing you up. Please try again

Article content

Advertisement 4

This advertisement has not loaded yet, but your article continues below.

Article content

Click here for what happened in the past week, and below is our wrap of what’s coming up in the global economy.

Asia

It’s a relatively quiet week in Asia, where much of the region — including China, Hong Kong and South Korea — will celebrate the Lunar New Year starting on Wednesday.

China on Monday releases manufacturing data for January as well as December industrial profits, which are set to show a decline for another month.

Japan is the exception to the quiet in the wake of its central bank decision on Friday to raise its rate to the highest in 17 years. A data deluge begins Tuesday with producer prices among services firms for December, expected to show another pickup. Consumer confidence is reported the following day.

Friday brings a look at the rest of Japan’s economy: The jobless rate in December likely held steady, while consumer prices in Tokyo — the largest city and a national proxy — may have picked up slightly in January. Meanwhile, retail sales are expected to be little changed in December from the prior month, and housing starts likely fell at a faster pace. Preliminary industrial production figures for December will also be reported.

Advertisement 5

This advertisement has not loaded yet, but your article continues below.

Article content

Australia releases several indicators, including December consumer prices, which are set to pick up from the prior year. Import and export prices for the fourth quarter are reported on Thursday and producer prices, also for the final three months of 2024, are out Friday.

On Thursday and Friday, New Zealand releases trade data as well as consumer and business confidence.

In the Philippines, numbers on Thursday are set to show that GDP expanded in the fourth quarter at a faster pace than the prior three months. Thailand caps the week on Friday with trade and manufacturing production figures.

Elsewhere across Asia, Pakistan’s central bank is expected to cut rates on Monday, and Sri Lanka officials announce their policy rate on Wednesday.

Europe, Middle East, Africa

A 25 basis-point rate cut from the European Central Bank is a near certainty on Thursday at the Governing Council’s first decision of the year.

With policymakers apprehensive about Trump’s possible tariffs and relatively sanguine about inflation risks, further reductions are likely. Investors will look for clues in President Christine Lagarde’s comments to reporters after the announcement.

Advertisement 6

This advertisement has not loaded yet, but your article continues below.

Article content

Aside from the closely-watched German Ifo business sentiment report on Monday, fourth-quarter GDP data are due just hours before the ECB outcome.

They may reveal that a contraction in Germany, stagnation in France and paltry expansion in Italy held back the wider region, which is anticipated to have notched up growth of just 0.1% overall.

Also informing officials will be a reading of inflation in Spain, expected to be unchanged at 2.8% in January. Other such reports will arrive on Friday, with Germany’s likely to be stuck at 2.8% and France seen showing a slight acceleration to 1.9%. Euro-zone numbers are due the following week.

In the UK, investors may focus on a major speech on growth by Chancellor Rachel Reeves on Wednesday, following a turbulent start to the year in financial markets and an avalanche of bad economic news. Bank of England Governor Andrew Bailey and colleagues will testify to lawmakers on Wednesday on financial stability matters.

Elsewhere in the wider region, South Africa and Nigeria will publish details on an overhaul of their inflation data. Both are changing their reference years to 2024 and reweighting certain indexes. Nigeria will also rebase its GDP numbers.

Advertisement 7

This advertisement has not loaded yet, but your article continues below.

Article content

Several monetary decisions are scheduled:

Advertisement 8

This advertisement has not loaded yet, but your article continues below.

Article content

Latin America

Chile’s central bank meets Tuesday after easing policy at 11 of its last 12 meetings. The economy has been losing momentum, but headline inflation actually rose in 2024 and pressures on energy prices, along with peso weakness, have analysts forecasting a hold at 5%.

Colombia’s central bank is more likely than not to cut its rate for a 10th straight meeting, to 9.25%. Policymakers slowed the pace of easing in December as jitters over Brazil’s fiscal imbalances sent shudders through the region’s markets.

Deteriorating inflation expectations since then may give policymakers reason to pause.

Mexico posts full-2024 trade results and December unemployment ahead of the flash reading on fourth-quarter output. Analysts have marked down their October-December estimates, with some seeing a negative print versus the previous three months.

Brazil puts up its lending and government budget balance reports along with its broadest measure of inflation, while the country’s central bank publishes its expectations survey.

Banco Central do Brasil also holds its first monetary policy meeting of the year, and has pledged to deliver a second straight 100 basis-point hike, taking the rate to 13.25%. Inflation is moving further above the 3% target, and expectations are unmoored.

—With assistance from Laura Dhillon Kane, Katia Dmitrieva, Monique Vanek, Robert Jameson, Ott Ummelas and Alexander Weber.

Article content

Share this article in your social network