Whether you’re speaking with Europe’s largest money manager, Australia’s giant pension funds, or a cash-rich insurer in Japan, there’s a resounding message you’ll hear when it comes to US Treasuries: They are still hard to beat.

Author of the article:

Published Jan 15, 2025 • 5 minute read

Article content

(Bloomberg) — Whether you’re speaking with Europe’s largest money manager, Australia’s giant pension funds, or a cash-rich insurer in Japan, there’s a resounding message you’ll hear when it comes to US Treasuries: They are still hard to beat.

Article content

Article content

Four months since incoming Vice President JD Vance said he was concerned Treasuries face a possible “death spiral” if bond vigilantes seek to drive up yields, firms including Legal & General Investment Management and Amundi SA say they are willing to give the new administration the benefit of the doubt.

Advertisement 2

Article content

There are plenty of reasons for global funds to buy even as Treasuries are mired in an historic bear market. The securities offer a huge yield premium over bonds in places such as Japan and Taiwan, while Australia’s rapidly growing pension industry is adding Treasuries every month because of the market’s depth and liquidity. The US also looks a safer bet than some European sovereign markets that are grappling with fiscal problems of their own.

Investors have also taken comfort in Trump’s nomination of hedge fund manager Scott Bessent to be his Treasury secretary, overseeing the government’s debt sales. Bessent, whose confirmation hearing before the Senate is scheduled for Thursday, aims to slash the deficit as a share of gross domestic product through tax cuts, spending restraint, deregulation and cheap energy.

“On the risk of a ‘death spiral,’ any bond market can become caught in a cycle of mutually reinforcing higher yields and higher debt projections,” said Chris Jeffery, head of macro strategy, asset management at Legal & General Investment, the UK’s biggest asset manager. But, “the incoming Treasury Secretary has talked about aiming for a 3% deficit in 2028. Bond investors have no reason to go on strike if the Federal government adopts such aspirations.”

Top Stories

Article content

Advertisement 3

Article content

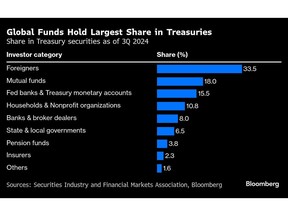

The stance of overseas investors toward Treasuries is more important than ever. Foreign funds held $7.33 trillion of long-term US debt at the end of October, about a third of the outstanding amount, and just below the record $7.43 trillion they owned in September, based on the latest US government data.

At the heart of the debate about whether to keep buying Treasuries is the largest US federal deficit outside of extreme periods such as the pandemic and the global financial crisis. There are a number of signs that investors are getting skittish. Benchmark US-year 10 yields have jumped more than a percentage point from September’s low, and are threatening to once again breach the key psychological level of 5%.

Yields on 10-year notes fell 14 basis points to 4.65% on Wednesday in response to benign US inflation data, the first drop in nine days.

Investors in Japan — the biggest overseas holders of Treasuries — are aware of the rising risks but remain eager buyers.

“The dominant view in markets is that the US Treasury market is too large and liquid and US seigniorage too deeply entrenched to undermine the central role of Treasuries in global central bank reserves,” said Naomi Fink, chief global strategist at Nikko Asset Management in Tokyo.

Advertisement 4

Article content

“In our central scenario, we anticipate the adjustment in US Treasury yields to proceed in an orderly fashion. However, the probability of a more disruptive adjustment, while still small, has increased in our view,” she said.

One reason Japanese investors favor Treasuries is that they provide exposure to the all-conquering dollar. Funds in the country would have reaped a return of 12% on their unhedged Treasury investments in 2024, with no less than 11.5% of that due to the greenback’s appreciation.

View From Europe

European funds are also largely optimistic, saying any spike up in Treasury yields is unlikely, especially as Trump appears aware of the need to keep global investors onside.

Markets are anticipating the new administration will mean higher US growth and inflation, which has caused the yield curve to steepen, but that’s actually making Treasuries more alluring, said Anne Beaudu, deputy head of global aggregate strategies at Amundi in Paris.

“US bonds appear more attractive at these levels, as rising yields will ultimately weigh on growth prospects or risky asset performance and the bar for hiking rates remains very high,” she said. “But the market will certainly remain cautious until we have more clarity on Trump’s agenda.”

Advertisement 5

Article content

At least some global funds are cautious on Treasuries as the US debt pile grows.

The budget deficit burgeoned to $1.83 trillion for the fiscal year ending September, according to the latest data published in October. The shortfall is forecast to swell further if Trump carries out his pledges to cut taxes and boost spending.

“The curve will remain very steep with a lot of new issuance coming to the market, and that again feeds negative into Treasuries,” said Kaspar Hense, senior portfolio manager at RBC Bluebay Asset Management in London. There’s at least some chance of spike in US yields, similar to that seen in the UK during the tenure of Prime Minister Liz Truss in 2022, he said.

The selloff in Treasuries in recent weeks though has convinced BlueBay to pare back some of its bets that 30-year year yields will underperform two-year ones, the company said this week.

‘No Better Place’

Investors in China, the second-biggest overseas holders of US debt, view the prospect of a Treasury meltdown as marginal.

“Even if concerns over higher borrowing costs and fiscal pressures in the US are legitimate, the chance for us to see a catastrophic collapse of the bond market is quite low,” said Ming Ming, chief economist in Beijing at Citic Securities Co., one of China’s biggest brokerages.

Advertisement 6

Article content

“If there is any unnecessary volatility in the US bond market, the Fed still has plenty of tools to stabilize it and manage liquidity. That will help ease pressures,” he said.

Investors in Taiwan are also continuing to put money into US debt.

“The momentum has not slowed despite expectations for slower or smaller rate hikes and chatter around the ‘death spiral,’ in fact, we’re seeing money continuing to pour in as yields rise,” said Julian Liu, chairman of Yuanta Securities Investment Trust, the island’s biggest local asset manager.

“For most Taiwan’s investors, the conclusion could likely be that there’s no better place to invest in.”

—With assistance from Jing Zhao, Masaki Kondo, Mia Glass, Alice Atkins, Betty Hou, Iris Ouyang, Chien-Hua Wan and Liz Capo McCormick.

Article content