Asian stocks were poised for a mixed opening on Monday as traders grappled with continued political upheaval in South Korea and awaited signs of fresh stimulus from Beijing. Oil was steady after the Syrian government was toppled.

Author of the article:

Published Dec 08, 2024 • Last updated 22 minutes ago • 4 minute read

Article content

(Bloomberg) — Asian stocks were poised for a mixed opening on Monday as traders grappled with continued political upheaval in South Korea and awaited signs of fresh stimulus from Beijing. Oil was steady after the Syrian government was toppled.

Article content

Article content

Australian stocks and equity futures in Hong Kong fell while those in Japan and mainland China climbed. US contracts were little changed after the S&P 500 advanced on Friday following a jobs report indicating the labor market is cooling enough to allow the Federal Reserve to cut interest rates this month. The dollar was steady against major peers in early trading.

Advertisement 2

Article content

Investors are readying themselves this week for a final flurry of central bank decisions across four continents, a key meeting of Chinese officials and US inflation data in an effort to pad returns for the year and help guide positions into 2025. A gauge of global stocks has returned more than 20% this year, on track for a second straight outsized return, according to data compiled by Bloomberg.

“It will be a lively week ahead with event risk all over the shop,” Chris Weston, head of research at Pepperstone Group Ltd. in Melbourne wrote in a note to clients. “A hot US CPI print may not necessarily derail a cut at next week’s FOMC meeting” but it may effect the outlook for further easing and move the dollar.

In Asia, South Korean assets may move as some lawmakers push for President Yoon Suk Yeol to resign amid mounting public anger of the brief imposition of martial law last week. Opposition lawmakers said they would push for another impeachment vote on Yoon after the first one failed.

Meanwhile, the People’s Bank of China’s daily fixing of the yuan will be parsed after the central bank signaled support for the currency through a series of strong fixings last week. That comes ahead of consumer and producer price data that may point to sluggish demand in the world’s second largest economy and add to expectations of more fiscal support from the Central Economic Work Conference which is due to start on Wednesday.

Top Stories

Article content

Advertisement 3

Article content

“There is a reasonable case to be made that China may have been keeping its powder dry pending US trade policy changes from January,” Barclays strategists led by Themistoklis Fiotakis write in a note to clients. Given there’s scope for some dollar easing, “yuan depreciation pressures should also ease temporarily given PBOC resistance at about 7.30” per dollar.

Middle-East

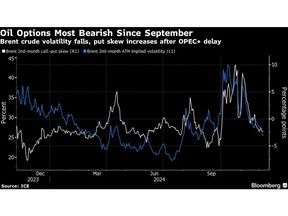

Crude was little changed after Saudi Arabia cut prices for buyers in Asia by more than expected after OPEC+ further delayed a lift to production. Moves could be tempered as markets assess the fallout from the toppling of Syrian President Bashar al-Assad’s government by opposition groups, a major blow to key backers Russia and Iran which may reshape the region as conflicts persist.

Treasuries extended their recent rebound on Friday, with investors getting a reprieve from a selloff that crested in November as Donald Trump’s presidential victory raised inflation risks. Since then, however, yields have drifted lower on speculation the Fed will ease policy again at this month’s gathering, its last before Trump takes office, as it tries to steer the economy to a soft landing.

Advertisement 4

Article content

In response to possible tensions between the incoming administration and the US central bank, Trump told NBC’s Meet the Press on Sunday that he has no plans to replace Fed Chair Jerome Powell once he returns to the White House. Markets are now pricing a roughly 80% chance the Fed cuts at its December meeting, though officials have cautioned on the pace of further cuts.

The Fed’s projections already offer a gradual pace of easing “yet even slower cuts and potentially a pause could be warranted,” Societe Generale economists including Klaus Baader wrote in a note to clients. “We expect a 25 basis-point rate cut at the December FOMC meeting but even that is dependent on upcoming CPI.”

Elsewhere this week, Australia’s central bank will likely keep its key interest rate on hold amid indications the nation’s economy is beginning to soften. The European Central Bank, Bank of Canada and Swiss National Bank are all expected to ease policy, while the Brazilian central bank may hike to arrest inflation pressures.

In other commodities, gold edged higher in early trading on Monday after China’s central bank expanded its gold reserves in November, ending a six-month pause in purchases.

Advertisement 5

Article content

Key events this week:

- Japan GDP, current account, Monday

- China PPI, CPI, Monday

- Mexico CPI, Monday

- Australia rate decision, Tuesday

- Germany CPI, Tuesday

- Brazil CPI, Tuesday

- Japan PPI, Wednesday

- Chinese leaders expected to hold annual Central Economic Work Conference, beginning Wednesday through Dec. 12

- RBA Deputy Governor Andrew Hauser speaks, Wednesday

- US CPI, Wednesday

- Canada rate decision, Wednesday

- Brazil rate decision, Wednesday

- Australia unemployment, Thursday

- India CPI, Thursday

- Eurozone ECB rate decision, Thursday

- Switzerland rate decision, Thursday

- France CPI, Friday

- Eurozone industrial production, Friday

Some of the main moves in markets:

Stocks

- S&P 500 futures were little changed as of 8:16 a.m. Tokyo time

- Hang Seng futures fell 0.6%

- Australia’s S&P/ASX 200 fell 0.4%

Currencies

- The Bloomberg Dollar Spot Index rose 0.2%

- The euro was little changed at $1.0566

- The Japanese yen was little changed at 149.94 per dollar

- The offshore yuan was little changed at 7.2800 per dollar

- The Australian dollar rose 0.1% to $0.6400

Cryptocurrencies

- Bitcoin rose 0.4% to $100,443.18

- Ether rose 0.1% to $3,998.83

Bonds

- Australia’s 10-year yield declined one basis point to 4.21%

Commodities

- West Texas Intermediate crude was little changed

- Spot gold rose 0.3% to $2,641.65 an ounce

This story was produced with the assistance of Bloomberg Automation.

Article content