US inflation figures in the coming week that are seen showing stubborn price pressures will reinforce the Federal Reserve’s cautionary posture toward future interest-rate cuts.

Author of the article:

Bloomberg News

Vince Golle and Craig Stirling

Published Nov 23, 2024 • 6 minute read

You can save this article by registering for free here. Or sign-in if you have an account.

7a3cyvn}0ny0hku({e9r3{j3_media_dl_1.pngChina’s National Bureau of Stati

Article content

(Bloomberg) — US inflation figures in the coming week that are seen showing stubborn price pressures will reinforce the Federal Reserve’s cautionary posture toward future interest-rate cuts.

The personal consumption expenditures price index excluding food and energy — the Fed’s preferred measure of underlying inflation — is projected to have risen by 0.3% in October from September, and by 2.8% from a year earlier, in what would be the largest advance since April.

Advertisement 2

This advertisement has not loaded yet, but your article continues below.

THIS CONTENT IS RESERVED FOR SUBSCRIBERS ONLY

Subscribe now to read the latest news in your city and across Canada.

Exclusive articles from Barbara Shecter, Joe O’Connor, Gabriel Friedman, and others.

Daily content from Financial Times, the world’s leading global business publication.

Unlimited online access to read articles from Financial Post, National Post and 15 news sites across Canada with one account.

National Post ePaper, an electronic replica of the print edition to view on any device, share and comment on.

Daily puzzles, including the New York Times Crossword.

SUBSCRIBE TO UNLOCK MORE ARTICLES

Subscribe now to read the latest news in your city and across Canada.

Exclusive articles from Barbara Shecter, Joe O’Connor, Gabriel Friedman and others.

Daily content from Financial Times, the world’s leading global business publication.

Unlimited online access to read articles from Financial Post, National Post and 15 news sites across Canada with one account.

National Post ePaper, an electronic replica of the print edition to view on any device, share and comment on.

Daily puzzles, including the New York Times Crossword.

REGISTER / SIGN IN TO UNLOCK MORE ARTICLES

Create an account or sign in to continue with your reading experience.

Access articles from across Canada with one account.

Share your thoughts and join the conversation in the comments.

Enjoy additional articles per month.

Get email updates from your favourite authors.

THIS ARTICLE IS FREE TO READ REGISTER TO UNLOCK.

Create an account or sign in to continue with your reading experience.

Access articles from across Canada with one account

Share your thoughts and join the conversation in the comments

Enjoy additional articles per month

Get email updates from your favourite authors

Sign In or Create an Account

or

Article content

The report is also expected to reveal resilient household spending and steady income growth at the start of the fourth quarter. Consumer outlays, unadjusted for price changes, are forecast to climb 0.4% after a 0.5% advance the previous month. Personal income is seen rising 0.3% for a second month, buoyed by healthy yet moderating job growth.

While Fed policymakers will receive another set of inflation data — the November consumer and producer price indexes — before their Dec. 17-18 meeting, they won’t see another PCE price gauge as they debate whether to lower rates.

What Bloomberg Economics Says:

“Several Fed officials discussing US economic conditions of late have echoed a theme recently introduced by Chair Jerome Powell — a December rate cut isn’t a done deal and the central bank can slow its easing pace given subsiding risks to the economy.”

— Anna Wong, Stuart Paul, Eliza Winger, Estelle Ou and Chris G. Collins. For full analysis, click here

The income and spending report packs the biggest punch for investors during a Wednesday data barrage ahead of the Thanksgiving Day holiday. The government that day will also release revised third-quarter gross domestic product, durable goods orders, jobless claims and merchandise trade deficit figures.

Top Stories

Get the latest headlines, breaking news and columns.

By signing up you consent to receive the above newsletter from Postmedia Network Inc.

Thanks for signing up!

A welcome email is on its way. If you don’t see it, please check your junk folder.

The next issue of Top Stories will soon be in your inbox.

We encountered an issue signing you up. Please try again

Article content

Advertisement 3

This advertisement has not loaded yet, but your article continues below.

Article content

On Tuesday, investors will parse minutes of the Fed’s early-November meeting for hints of policymakers’ appetite for a third straight rate cut next month. As of Friday, market participants assigned slightly better than even odds for another quarter-point reduction.

For more, read Bloomberg Economics’ full Week Ahead for the US

Turning north, Canada’s third-quarter gross domestic product on Friday may help officials decide between a second 50 basis-point rate cut or a more cautious 25 basis-point move in December. Output data pointed to 1% growth, but economists expect the expenditure-based figures to land closer to a central bank estimate of 1.5% annualized expansion, supporting the case for more gradual reductions.

Elsewhere, Chinese survey numbers, a likely pickup in euro-area inflation, and monetary decisions — including a possible large rate cut in New Zealand — are among the highlights.

Click here for what happened in the past week, and below is our wrap of what’s coming up in the global economy.

Asia

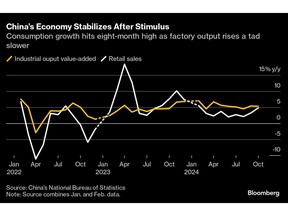

China’s economic health will stay in the spotlight, with purchasing managers’ indexes set for release at the end of the week.

Advertisement 4

This advertisement has not loaded yet, but your article continues below.

Article content

Policymakers and economists will look for further signs that Beijing’s recent stimulus is gaining early traction. Last month, both the factory and service sector PMIs showed resilient or expanding activity for the first time since April.

New Zealand’s central bank may consider a jumbo rate cut on Wednesday. The reduction is likely to be a half-percentage point rather than anything bigger as the Reserve Bank looks to balance caution over lingering inflation with the need to restart a stalled economy.

The Bank of Korea is expected to stand pat on Thursday as it monitors the impact of its pivot toward lower rates in October.

Reserve Bank of Australia chief Michele Bullock’s views on the policy outlook will be under the microscope when she speaks at an event a day after the latest monthly inflation figures are released.

Elsewhere, rate decisions are also due in Sri Lanka and Kazakhstan.

New Zealand, Hong Kong and Thailand will release trade figures in the coming week, Singapore has inflation numbers, and Japan will report on factory production, retail sales and the latest price growth data from Tokyo.

Advertisement 5

This advertisement has not loaded yet, but your article continues below.

Article content

For more, read Bloomberg Economics’ full Week Ahead for Asia

Europe, Middle East, Africa

Inflation will take center stage in the euro zone, where data releases will start on Thursday before a report for the region as a whole the following day.

Price growth is predicted by forecasters to have quickened in all four of the largest economies. Inflation in the euro area probably accelerated to 2.3% in November, the fastest reading for four months.

Investors will also watch for the European Central Bank’s survey of consumer-price expectations on Friday. Several appearances are scheduled over the course of the week by policymakers, including Chief Economist Philip Lane.

ECB officials have become increasingly sanguine on inflation prospects and will probably view the anticipated re-acceleration as a short-lived blip.

Germany’s Ifo index of business expectations on Monday — the first since Donald Trump’s re-election raised the prospect of new tariffs — will also be a highlight.

In the UK, the Bank of England is likely to draw attention. Governor Andrew Bailey will address business leaders on Monday, and the latest financial stability report will be published at the end of the week.

Advertisement 6

This advertisement has not loaded yet, but your article continues below.

Article content

Turning to Sweden, data on Friday may show the economy succumbed to a recession in the third quarter. Before that, two Riksbank officials are scheduled to speak.

For more, read Bloomberg Economics’ full Week Ahead for EMEA

Several monetary decisions are scheduled in the wider region:

On Monday, Israel’s central bank is likely to hold its base rate at 4.5% at a time when wars in Gaza and Lebanon are causing price pressures and slowing the economy.

On Tuesday, Nigerian officials may hike borrowing costs to cool price growth stoked by gasoline, currency weakness and floods. Governor Olayemi Cardoso has said the central bank wants a positive inflation-adjusted interest rate to attract investment and support the naira. The spread between inflation and the benchmark is now about 660 basis points.

Lesotho, whose currency is pegged to the rand and is experiencing slowing price growth, is expected to follow South Africa and cut by a quarter point.

In Mozambique on Wednesday, policymakers may keep their rate at 13.5%, concerned by the impact election unrest may have on inflation.

A day later, Gambian officials, encouraged by weakening price growth, may cut benchmark borrowing costs, currently set at 17%.

On Friday, Ghana is expected to leave its benchmark at 27% because of concerns about missing its year-end target for inflation at 18%.

Advertisement 7

This advertisement has not loaded yet, but your article continues below.

Article content

Latin America

In Mexico, the central bank’s quarterly inflation report and minutes of Banxico’s Nov. 14 decision to deliver a third straight rate reduction to 10.25% are keenly awaited.

Analysts have been trimming their 2024 and 2025 GDP forecasts while Banxico notably raised its fourth-quarter inflation projection to 4.7% from 4.3% at its November meeting.

Governor Victoria Rodríguez on Nov. 19 indicated that, given the progress in slowing consumer-price increases, more easing lies ahead.

Jobs data for October are also on tap in three of the region’s big economies. Brazil’s national unemployment may eclipse the previous low of 6.3% to set a new mark. In Colombia, the early consensus has the urban jobless rate falling to 8.9%, well below the average for the series. Chile’s current unemployment level of 8.7% points to the slack in the labor market and economy.

In addition to the jobs report, Chile also posts October retail sales, commercial activity, industrial production, manufacturing production and total copper output.

Budget figures and the Brazilian central bank’s weekly readout of market expectations bookend the mid-month inflation report, which is likely to show consumer prices taking another leg up, both above target and the top of its tolerance range.

Local economists have raised their year-end forecasts in 26 of the central bank’s last 28 weekly surveys.

For more, read Bloomberg Economics’ full Week Ahead for Latin America

—With assistance from Paul Jackson, Laura Dhillon Kane, Monique Vanek, Robert Jameson, Piotr Skolimowski and Paul Wallace.