Business activity in the euro area unexpectedly shrank this month, fueling concerns about the prospects for Europe’s economy and suggesting the European Central Bank will need to be more aggressive with interest-rate cuts.

Author of the article:

Bloomberg News

Vince Golle and Molly Smith

Published Nov 23, 2024 • 4 minute read

You can save this article by registering for free here. Or sign-in if you have an account.

g3xwqsh9fngoanqi84os7gpx_media_dl_1.pngBloomberg

Article content

(Bloomberg) — Business activity in the euro area unexpectedly shrank this month, fueling concerns about the prospects for Europe’s economy and suggesting the European Central Bank will need to be more aggressive with interest-rate cuts.

The euro fell to its lowest level since 2022 against the dollar after the purchasing managers gauge of service providers and manufacturers weakened. Political crises in Germany and France, as well as the threat of tariffs from a Donald Trump presidency in the US, also weighed on the currency.

Advertisement 2

This advertisement has not loaded yet, but your article continues below.

THIS CONTENT IS RESERVED FOR SUBSCRIBERS ONLY

Subscribe now to read the latest news in your city and across Canada.

Exclusive articles from Barbara Shecter, Joe O’Connor, Gabriel Friedman, and others.

Daily content from Financial Times, the world’s leading global business publication.

Unlimited online access to read articles from Financial Post, National Post and 15 news sites across Canada with one account.

National Post ePaper, an electronic replica of the print edition to view on any device, share and comment on.

Daily puzzles, including the New York Times Crossword.

SUBSCRIBE TO UNLOCK MORE ARTICLES

Subscribe now to read the latest news in your city and across Canada.

Exclusive articles from Barbara Shecter, Joe O’Connor, Gabriel Friedman and others.

Daily content from Financial Times, the world’s leading global business publication.

Unlimited online access to read articles from Financial Post, National Post and 15 news sites across Canada with one account.

National Post ePaper, an electronic replica of the print edition to view on any device, share and comment on.

Daily puzzles, including the New York Times Crossword.

REGISTER / SIGN IN TO UNLOCK MORE ARTICLES

Create an account or sign in to continue with your reading experience.

Access articles from across Canada with one account.

Share your thoughts and join the conversation in the comments.

Enjoy additional articles per month.

Get email updates from your favourite authors.

THIS ARTICLE IS FREE TO READ REGISTER TO UNLOCK.

Create an account or sign in to continue with your reading experience.

Access articles from across Canada with one account

Share your thoughts and join the conversation in the comments

Enjoy additional articles per month

Get email updates from your favourite authors

Sign In or Create an Account

or

Article content

Here are some of the charts that appeared on Bloomberg this week on the latest developments in the global economy, markets and geopolitics:

Europe

Euro-area business activity unexpectedly shrank in November, a sign of the damage being wrought by political chaos and heightened discord over trade. The euro fell to its weakest levels since 2022 against the dollar as traders priced in more interest-rate cuts from the European Central Bank. The chance of a 50 basis-point reduction in December rose to 50%, from about 15% at Thursday’s close.

UK inflation accelerated more than forecast in October to well above the Bank of England’s 2% target. Consumer-price inflation rose 2.3% from a year earlier after a jump in energy bills. Services inflation — which is being monitored closely by rate-setters for signs of domestic pressures — remained elevated at 5%.

A key gauge of euro-zone wages jumped by the most since the common currency was introduced in 1999 — complicating the ECB’s plans for interest-rate cuts as inflation eases. Third-quarter negotiated pay rose 5.4% from a year ago. That’s up from 3.5% in the previous three months and was largely driven by Germany.

Top Stories

Get the latest headlines, breaking news and columns.

By signing up you consent to receive the above newsletter from Postmedia Network Inc.

Thanks for signing up!

A welcome email is on its way. If you don’t see it, please check your junk folder.

The next issue of Top Stories will soon be in your inbox.

We encountered an issue signing you up. Please try again

Article content

Advertisement 3

This advertisement has not loaded yet, but your article continues below.

Article content

A dormant stock market, brittle currency, crisis-ridden political system, stagnant economy — so was the landscape in Europe even before Donald Trump won election in the US. Now, the continent faces new trade tariffs against its biggest companies and investment outflows as Trump’s plans to cut taxes and gut regulation make US stocks more attractive. Add to that the growing angst around Germany’s upcoming snap election and escalating Russia tensions and even the most optimistic investors are struggling to stay upbeat.

Asia

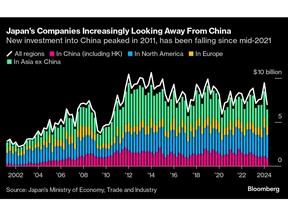

Japanese firms in China are becoming more pessimistic about the world’s second-biggest economy, with about two-thirds saying it’s getting worse and almost half scaling back or halting their investments. About 64% of Japanese companies said the Chinese economy is faring worse than last year, according to the latest survey from the Japanese Chamber of Commerce and Industry in China.

South Korea’s household debt grew the most in three years last quarter, highlighting a development that kept the central bank from pivoting on policy until last month. Mortgage loans, a major component of the credit, also rose by the most since the third quarter of 2021.

Advertisement 4

This advertisement has not loaded yet, but your article continues below.

Article content

US & Canada

Housing starts declined in October to the slowest pace in three months as hurricanes exacerbated an easing in construction activity more generally. Residential construction has struggled to gain traction this year against a backdrop of a growing number of new homes for sale and mortgage rates near 7%.

Trump’s vows to “frack, frack, frack” are about to collide with a global crude glut that’s set to, finally, temper record shale production.

Inflation in Canada rose by more than forecast and underlying price pressures reaccelerated, hiccups that may dissuade policymakers from a second straight 50 basis-point cut to interest rates next month. The first acceleration of headline inflation in five months may bolster a case for the Bank of Canada to reduce borrowing costs gradually, after officials stepped up the pace of easing in October.

Emerging Markets

Years of runaway inflation are testing the physical limits of Turkey’s cash-centric economy as its biggest banknotes become increasingly inadequate to cover even daily spending. The highest-denominated bill, for 200 liras ($5.80), now represents more than 80% of all cash in circulation, up from 16% in 2010, according to central bank data. After losing almost all its purchasing power, each note is worth enough to buy two filter coffees at Starbucks.

Advertisement 5

This advertisement has not loaded yet, but your article continues below.

Article content

Mexico’s inflation decelerated in early November while the economy continues to lose momentum, giving the central bank room to cut interest rates for a fourth straight meeting next month.

World

Ukrainian forces earlier this week carried out their first strike on a border region in Russia using Western-supplied missiles as President Vladimir Putin approved an updated nuclear doctrine expanding the conditions for using atomic weapons. The news sent investors scrambling into some of the world’s safest assets.

Iceland’s central bank accelerated its easing campaign, while South Africa also cut rates. Bank Indonesia warned there is less scope to lower them. Hungary, Angola, Paraguay and Egypt kept borrowing costs steady. Turkey also held while implying a cut could soon be justified due to slowing inflation.

—With assistance from Irina Anghel, Alice Atkins, Maya Averbuch, Taylan Bilgic, Kevin Crowley, Robert Jameson, Lucia Kassai, Sam Kim, Aliaksandr Kudrytski, James Mayger, Henry Meyer, Michael Msika, Tom Rees, Michael Sasso, Zoe Schneeweiss, Mark Schroers, Patrick Sykes, Randy Thanthong-Knight, Alex Vasquez and David Wethe.