Germany’s strict borrowing rules, long championed by conservative politicians and fiscally hawkish economists, could soon be in for an overhaul that a growing chorus of critics argues is long overdue.

Author of the article:

Bloomberg News

Jana Randow and Mark Schroers

Published Nov 21, 2024 • 6 minute read

You can save this article by registering for free here. Or sign-in if you have an account.

(Bloomberg) — Germany’s strict borrowing rules, long championed by conservative politicians and fiscally hawkish economists, could soon be in for an overhaul that a growing chorus of critics argues is long overdue.

Debate around loosening the framework that’s helped keep Germany’s budget deficit in check since 2009 has intensified as the country heads toward February’s snap election. Even Friedrich Merz, the Christian Democrat chancellor candidate who is leading in opinion polls, has acknowledged the need for more flexibility to help fund the massive investments required in areas like infrastructure, energy and defense.

Advertisement 2

This advertisement has not loaded yet, but your article continues below.

THIS CONTENT IS RESERVED FOR SUBSCRIBERS ONLY

Subscribe now to read the latest news in your city and across Canada.

Exclusive articles from Barbara Shecter, Joe O’Connor, Gabriel Friedman, and others.

Daily content from Financial Times, the world’s leading global business publication.

Unlimited online access to read articles from Financial Post, National Post and 15 news sites across Canada with one account.

National Post ePaper, an electronic replica of the print edition to view on any device, share and comment on.

Daily puzzles, including the New York Times Crossword.

SUBSCRIBE TO UNLOCK MORE ARTICLES

Subscribe now to read the latest news in your city and across Canada.

Exclusive articles from Barbara Shecter, Joe O’Connor, Gabriel Friedman and others.

Daily content from Financial Times, the world’s leading global business publication.

Unlimited online access to read articles from Financial Post, National Post and 15 news sites across Canada with one account.

National Post ePaper, an electronic replica of the print edition to view on any device, share and comment on.

Daily puzzles, including the New York Times Crossword.

REGISTER / SIGN IN TO UNLOCK MORE ARTICLES

Create an account or sign in to continue with your reading experience.

Access articles from across Canada with one account.

Share your thoughts and join the conversation in the comments.

Enjoy additional articles per month.

Get email updates from your favourite authors.

THIS ARTICLE IS FREE TO READ REGISTER TO UNLOCK.

Create an account or sign in to continue with your reading experience.

Access articles from across Canada with one account

Share your thoughts and join the conversation in the comments

Enjoy additional articles per month

Get email updates from your favourite authors

Sign In or Create an Account

or

Article content

Merz last week signaled a new openness to tweaking the mechanism known as the debt brake to give the government additional wiggle room. That marked a surprising departure from his party’s long-held stance that the limit on net new borrowing, enshrined in the country’s basic law and introduced by an earlier conservative government, is sacrosanct.

Merz knows that if his CDU/CSU bloc wins the election, he will almost certainly need to form a coalition with at least one other party to secure a Bundestag majority. His likely alliance partners, the Social Democrats and Greens, are proponents of increased borrowing and disagreement on the issue with the Free Democrats prompted the breakup of Chancellor Olaf Scholz’s ruling alliance this month.

“It’s very likely that the debt brake won’t survive the next coalition negotiations in its current form,” said Holger Schmieding, chief economist at Berenberg. “After their experiences in the current coalition, the Social Democrats or Greens would be out of their minds to enter into another coalition without reforming the debt brake — and the CDU knows this.”

Top Stories

Get the latest headlines, breaking news and columns.

By signing up you consent to receive the above newsletter from Postmedia Network Inc.

Thanks for signing up!

A welcome email is on its way. If you don’t see it, please check your junk folder.

The next issue of Top Stories will soon be in your inbox.

We encountered an issue signing you up. Please try again

Article content

Advertisement 3

This advertisement has not loaded yet, but your article continues below.

Article content

The debt brake limits structural budget deficits to 0.35% of gross domestic product. And while it allows for exceptions during national emergencies or recessions, it’s increasingly seen as unfit for purpose given the country’s vast investment needs.

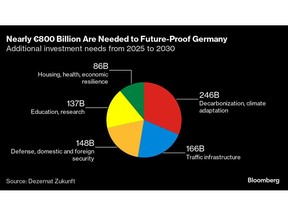

According to estimates by Dezernat Zukunft, a Berlin-based think tank, some €800 billion ($844 billion) in additional spending is needed between 2025 and 2030 to update Germany’s infrastructure, bolster its defense and increase growth potential. Nearly half of those investments fall within the responsibilities of regional and municipal administrations, who aren’t allowed to run deficits at all.

What Bloomberg Economics Says…

“Raising public spending to tackle Germany’s economic challenges will remain a hot potato for the next government. It’s mainly what toppled the ruling coalition. But the path to relaxing the nation’s strict borrowing limits is far from straightforward, no matter who prevails in the Feb. 23 snap election.”

—Antonio Barroso and Martin Ademmer. For full note, click here

Proposals on how to reform the debt brake, initially introduced after costly bank bailouts following the global financial crisis, have accumulated in recent years. They include linking borrowing limits to debt levels, expanding the use of special off-budget funds, so-called golden rules for certain kinds of spending, more room for regional governments and flexibility in interpreting the current rules.

Advertisement 4

This advertisement has not loaded yet, but your article continues below.

Article content

Many of these would require changes to Germany’s constitution, which needs the backing of a two-thirds majority in parliament.

Part of the discussion is about how much fiscal leeway Germany actually has.

Some economists argue there’s already plenty. The country’s debt-to-GDP ratio is around 64%, only slightly above the 60% reference value enshrined in the European Union’s fiscal rules and much lower than Italy’s 140% or France’s 110%.

“The strong fiscal position of the German government would, in principle, allow an aggressive fiscal expansion,” said Dirk Schumacher, head of European macro research at Natixis.

Friedrich Heinemann, an economist at the Mannheim-based research institute ZEW, agrees that Germany’s comparatively small debt load is a sign of strength.

But he also warns of financial liabilities that are larger than official statistics suggest. That’s partly because the country’s share of EU debt doesn’t appear in national data, and partly due to the unfunded pension entitlements of a rapidly aging population.

Such reservations suggest that Germany may continue to embrace fiscal conservatism even after reforming or loosening some of the rules. Here’s a look at the options being discussed:

Advertisement 5

This advertisement has not loaded yet, but your article continues below.

Article content

Linking Borrowing Limits to Debt Levels

EU rules allow governments to run structural deficits as high as 0.5% if their debt load is above 60% — and twice as much if debt is below that threshold.

The Bundesbank suggested as early as 2022 that Germany should adopt the more flexible EU rules. The country’s council of economic experts made a similar proposal this year that included a 0.35% cap on net new borrowing if debt levels climb above 90%.

Special Funds

Germany created a €100 billion off-budget fund to upgrade its military after Russia’s invasion of Ukraine and that could serve as a blueprint for similarly earmarked investments that wouldn’t count toward deficit rules.

But this approach has also raised some legal doubts, with some critics saying such “shadow budgets” are designed to circumvent the debt brake and threaten Germany’s fiscal stability.

Golden Rules

So-called golden rules exempting certain kinds of spending are another way to raise cash without running afoul of the debt brake. Some have suggested using the space between Germany’s 0.35% of GDP deficit cap and the EU’s 0.5% to support infrastructure projects. Prior to 2009, Germany had a version of such a rule in its constitution.

Advertisement 6

This advertisement has not loaded yet, but your article continues below.

Article content

More Freedom for Regions

While the federal government is allowed to run a small deficit, Germany’s 16 federal states are required to balance their budgets. That rule is increasingly drawing criticism from regional leaders, who argue that a significant share of the country’s investment needs falls within their remit and they should be subject to the same fiscal rules as the government in Berlin.

“If states were allowed to act in the same way as the federal government, it would be possible for Germany to double its borrowing,” said Roland Koch, who served as Hesse state premier for Merz’s CDU party in the decade through 2010. “Pressure will come from this direction.”

Cyclical Adjustment and Transition Phases

Some tweaks to existing rules are possible without changing the constitution, though the fiscal space they’d open up is limited.

They include a gradual phasing in of existing rules after years when the debt brake was suspended as long as there are no slippages. Experts have also proposed ways of improving the process of factoring divergences of actual growth and tax revenue from projections into fiscal plans.

Advertisement 7

This advertisement has not loaded yet, but your article continues below.

Article content

Political Reservations

Merz has argued that his willingness to reform Germany’s debt brake hinges on where the extra money will be spent.

“If the result is that we spend even more money on consumption and social policy, then the answer is no,” he said last week. “If the result is that it is important for investment, it is important for progress, it is important for the livelihoods of our children, then the answer may be different.”

Merz could face resistance from within his own conservative alliance. Markus Soeder, who leads the CDU’s smaller Bavarian sister party, the CSU, has a long list of demands to be met before he’d be willing to consider changing the rules.

Some economists have argued that politicians are wasting valuable time and urged them to push ahead with reform before the Feb. 23 election.

“Then a government could get started right away,” said Sebastian Dullien, director of the IMK economic research institute. “Without such a reform, the new government risks failing because of the same obstacle as the old one — because of the debt brake, which is not appropriate for today’s times.”

—With assistance from Michael Nienaber and Kamil Kowalcze.