Chinese copper smelters are facing pressure to rein in an expansion that’s pounding the industry’s profitability. The viability of plants across the globe may be at stake.

Author of the article:

Bloomberg News

Bloomberg News

Published Nov 11, 2024 • 4 minute read

You can save this article by registering for free here. Or sign-in if you have an account.

e4amox52sa[yedb3wyhd{47s_media_dl_1.pngChina’s National Bureau of Stati

Article content

(Bloomberg) — Chinese copper smelters are facing pressure to rein in an expansion that’s pounding the industry’s profitability. The viability of plants across the globe may be at stake.

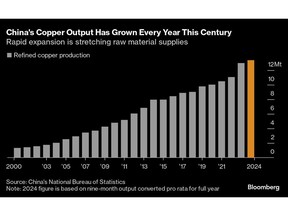

The top consumer of copper globally is on track to produce about half the world’s refined metal this year after a frenzy of smelter construction to secure supplies crucial to the energy transition. The boom in capacity has continued despite cutthroat competition for scarce raw materials that is crushing margins everywhere.

Advertisement 2

This advertisement has not loaded yet, but your article continues below.

THIS CONTENT IS RESERVED FOR SUBSCRIBERS ONLY

Subscribe now to read the latest news in your city and across Canada.

Exclusive articles from Barbara Shecter, Joe O’Connor, Gabriel Friedman, and others.

Daily content from Financial Times, the world’s leading global business publication.

Unlimited online access to read articles from Financial Post, National Post and 15 news sites across Canada with one account.

National Post ePaper, an electronic replica of the print edition to view on any device, share and comment on.

Daily puzzles, including the New York Times Crossword.

SUBSCRIBE TO UNLOCK MORE ARTICLES

Subscribe now to read the latest news in your city and across Canada.

Exclusive articles from Barbara Shecter, Joe O’Connor, Gabriel Friedman and others.

Daily content from Financial Times, the world’s leading global business publication.

Unlimited online access to read articles from Financial Post, National Post and 15 news sites across Canada with one account.

National Post ePaper, an electronic replica of the print edition to view on any device, share and comment on.

Daily puzzles, including the New York Times Crossword.

REGISTER / SIGN IN TO UNLOCK MORE ARTICLES

Create an account or sign in to continue with your reading experience.

Access articles from across Canada with one account.

Share your thoughts and join the conversation in the comments.

Enjoy additional articles per month.

Get email updates from your favourite authors.

THIS ARTICLE IS FREE TO READ REGISTER TO UNLOCK.

Create an account or sign in to continue with your reading experience.

Access articles from across Canada with one account

Share your thoughts and join the conversation in the comments

Enjoy additional articles per month

Get email updates from your favourite authors

Sign In or Create an Account

or

Article content

China’s excesses threaten the future of copper refining beyond its borders, said Grant Sporre, head of metals and mining research at Bloomberg Intelligence. Operations from Chile to Europe and India could be at risk, he said.

Mounting calls within the country to curb production and scale back the formidable pipeline of new plants have yet to be heeded. If the breakneck expansion continues — and forces curtailments elsewhere in the world — more output will be concentrated in China, even as western governments fret about its grip on strategic minerals.

The situation will come to a head at Asia’s biggest gathering of the copper industry in Shanghai this week, when smelters face crunch talks on the ore supply contracts that determine their margins. Miners have the whip hand at the annual negotiations because capacity is running so far ahead of global mine production.

The treatment and refining fees paid to smelters to convert ore into metal could drop to $40 a ton or less for next year, according to industry estimates, from $80 a ton in 2024. Such a settlement could lead to widespread losses. The previous low was $43 a ton in 2004, according to metals consultancy CRU Group, which has data going back to 1992.

Top Stories

Get the latest headlines, breaking news and columns.

By signing up you consent to receive the above newsletter from Postmedia Network Inc.

Thanks for signing up!

A welcome email is on its way. If you don’t see it, please check your junk folder.

The next issue of Top Stories will soon be in your inbox.

We encountered an issue signing you up. Please try again

Article content

Advertisement 3

This advertisement has not loaded yet, but your article continues below.

Article content

Demand from renewables, electric vehicles and grid infrastructure is poised to balloon in coming decades. That’s spurring more investment along the copper supply chain, but smelters are far quicker and cheaper to build than new mines.

The ore squeeze has been compounded by the construction of new plants in India, which is seeking to reduce its reliance on imports, and Indonesia, where the government plans to halt exports of ore that currently feed smelters throughout Asia.

That has intensified the need to impose restraint in China. Spot treatment fees made an unprecedented plunge below zero earlier in the year. But the industry’s push to cut output hasn’t had much impact. China’s production of refined copper has risen more than 5% so far in 2024. Last month, the country’s main metals association called for stronger government intervention to stem the “blind expansion.”

It’s a familiar refrain across Chinese industries, from steel to solar and EVs, which are grappling with the effects of overcapacity while at the same time attempting to protect jobs and targets for economic growth.

Advertisement 4

This advertisement has not loaded yet, but your article continues below.

Article content

China remains a net importer of copper, and doesn’t yet ship huge volumes overseas — unlike its steel and aluminum sectors, which are running up against increased protectionism from trade partners around the world. But that could change if it presses on with its expansion.

Top executives from key Chinese smelters have met in recent days to address the unfavorable market, according to people familiar with the talks. The meetings, which were attended by government representatives, included discussions about sticking more firmly to plans to cut production, said the people, who asked not to be identified as the information is private.

But there’s skepticism. Analysts believe Chinese producers can weather the conditions better than others because of their cost advantage. Most of the older, less efficient plants have already been retired, according to Bloomberg’s Sporre. And large, privately-owned smelters have been flushed out of the industry in recent years, leaving the sector dominated by state-owned firms more resilient to financial pressures.

“No one wants to cut first, but the ore tightness will be years-long and like running a marathon,” said Zhao Yongcheng, an analyst at Benchmark Mineral Intelligence Ltd. “Who can survive till the end will really be a test of everything from capital abundance to operations.”

Advertisement 5

This advertisement has not loaded yet, but your article continues below.

Article content

On the Wire

Climate negotiators secured a breakthrough on day one of the COP29 climate summit by agreeing on rules for a United Nations-administered global carbon market.

Gazprom is preparing to raise China gas flows to maximum contractual levels.

China’s credit expansion slowed more than expected in October, as a surge in government bond sales far exceeded growth in lending during a traditionally slow month for financing activity.

The Week’s Diary

(All times Beijing unless noted.)

Tuesday, Nov. 12:

Asia Copper Week in Shanghai, day 1

Wednesday, Nov. 13:

Asia Copper Week in Shanghai, day 2

CRU World Copper Conference Asia, day 1

CCTD’s weekly online briefing on Chinese coal, 15:00

Thursday, Nov. 14:

Asia Copper Week in Shanghai, day 3

CRU World Copper Conference Asia, day 2

CEO Summit and Asia Copper Dinner

Friday, Nov. 15:

China home prices for October, 09:30

China industrial output for October, including steel & aluminum; coal, gas & power generation; and crude oil & refining, 10:00