Just before a hotly contested US election considered a toss-up, options traders across markets appear to be reducing risk and bracing for more volatility.

Author of the article:

Bloomberg News

Natalia Kniazhevich, Vassilis Karamanis and Edward Bolingbroke

Published Nov 03, 2024 • 5 minute read

You can save this article by registering for free here. Or sign-in if you have an account.

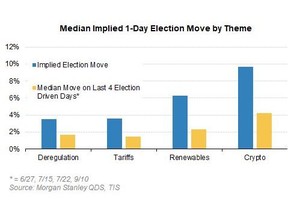

Implied election moves by sectorSource: Morgan Stanley

Article content

(Bloomberg) — Just before a hotly contested US election considered a toss-up, options traders across markets appear to be reducing risk and bracing for more volatility.

Equity options volatility climbed through most of October even as the market’s swings were muted, in anticipation of not just the upcoming election but also earnings season and a Federal Reserve interest-rate decision. The race between Kamala Harris and Donald Trump is too close to call in the final days before the vote.

Advertisement 2

This advertisement has not loaded yet, but your article continues below.

THIS CONTENT IS RESERVED FOR SUBSCRIBERS ONLY

Subscribe now to read the latest news in your city and across Canada.

Exclusive articles from Barbara Shecter, Joe O’Connor, Gabriel Friedman, and others.

Daily content from Financial Times, the world’s leading global business publication.

Unlimited online access to read articles from Financial Post, National Post and 15 news sites across Canada with one account.

National Post ePaper, an electronic replica of the print edition to view on any device, share and comment on.

Daily puzzles, including the New York Times Crossword.

SUBSCRIBE TO UNLOCK MORE ARTICLES

Subscribe now to read the latest news in your city and across Canada.

Exclusive articles from Barbara Shecter, Joe O’Connor, Gabriel Friedman and others.

Daily content from Financial Times, the world’s leading global business publication.

Unlimited online access to read articles from Financial Post, National Post and 15 news sites across Canada with one account.

National Post ePaper, an electronic replica of the print edition to view on any device, share and comment on.

Daily puzzles, including the New York Times Crossword.

REGISTER / SIGN IN TO UNLOCK MORE ARTICLES

Create an account or sign in to continue with your reading experience.

Access articles from across Canada with one account.

Share your thoughts and join the conversation in the comments.

Enjoy additional articles per month.

Get email updates from your favourite authors.

THIS ARTICLE IS FREE TO READ REGISTER TO UNLOCK.

Create an account or sign in to continue with your reading experience.

Access articles from across Canada with one account

Share your thoughts and join the conversation in the comments

Enjoy additional articles per month

Get email updates from your favourite authors

Sign In or Create an Account

or

Article content

Bond yields have been rising since the Fed cut rates in September, leading investors to pull back on some futures positions and add tail-risk hedges on higher rates. For the most part, currency traders are betting on wider swings, with volatility for the yuan, Mexican peso and euro increasing on uncertainty about trade and tariffs.

“Positioning is pretty clean” after some general de-risking the past few weeks into the election and Fed meeting, said Stuart Kaiser, a US equity trading strategist at Citigroup Global Markets Inc. “That is good for risk/reward post election depending on result of course. Bonds seem to be moving more than stocks.”

Here’s a look at how options traders are positioning across various asset classes, from equities to crypto:

Stocks

As expected, much of the hedging for the election has showed up at the last minute, as shorter-term options make it easier to position closer to an event. Implied volatility is running well above realized levels, with investors bracing for wider swings even as the S&P 500 Index went 29 sessions without a drop of more than 1%.

Top Stories

Get the latest headlines, breaking news and columns.

By signing up you consent to receive the above newsletter from Postmedia Network Inc.

Thanks for signing up!

A welcome email is on its way. If you don’t see it, please check your junk folder.

The next issue of Top Stories will soon be in your inbox.

We encountered an issue signing you up. Please try again

Article content

Advertisement 3

This advertisement has not loaded yet, but your article continues below.

Article content

“We continue to see an interest in trades around the election with a pick up in recent days,” said Daniel Kirsch, head of options at Piper Sandler & Co. “Clients who expect Donald Trump to win the election are adding exposure to financials and crypto stocks, those who are betting on a Harris win buy options on renewable-energy stocks. There’s also a pick up in hedging with traders piling into put options for the S&P 500 and QQQ ETF.”

Shorter-term S&P 500 implied volatility has been running hot relative to one-month levels, as the election and Fed bump percolates through the calculation of the shorter-term measure. The Cboe VVIX Index — which measures the volatility of the VIX — is also elevated.

“Currently, the options skew is steep and VIX is much higher than realized volatility,” said Zhiwei Ren, portfolio manager at Penn Mutual Asset Management. “These are signs that the market is well hedged at this point.”

While volatility has been elevated, it’s pointing to about a 1.7% move for the S&P 500 the day after the election — not an outrageous swing. The implied move has fallen steadily from a peak of around 2% in early October to be about in line with the long-term average for past elections, according to Stefano Pascale, head of US equity-derivatives strategy at Barclays Plc.

Advertisement 4

This advertisement has not loaded yet, but your article continues below.

Article content

Beyond the general indexes, some sectors, such as crypto and clean-energy stocks, are seeing a surge in volatility well above their medians. Crypto stocks are pricing almost 10% moves, Morgan Stanley’s trading desk said last week, and those for renewable firms around 6%. That’s playing out in positioning, where, for example, more than 20,000 November call spreads were bought last week in Sunrun Inc.

Once past the election, fundamental market flows are building up support for a rally into the end of the year, as hedges are taken off, mutual fund buying kicks in during November, companies repurchase shares and lower volatility draws in systemic buying and rehedging by option dealers.

“Assuming a smooth post-election period, we believe these hedges may unwind and we could see a sharp drop of VIX and flatter skew,” said Ren. “If both happen, it could force more buyers into the market and push the market higher.”

FX

Short-term currency options that are now pricing in risk around the election have seen an implied volatility jump in anticipation of wider swings after the US vote. One-week dollar-yuan swings hit a record high late last week as traders hedged against the possibility of higher US tariffs that Trump has threatened and a global trade war that could especially hurt China.

Advertisement 5

This advertisement has not loaded yet, but your article continues below.

Article content

Volatility in the euro — also vulnerable to any trade tariffs that a victory for Trump could entail — has risen the most since 2020, reaching its highest level since March 2023, while risk reversals remain bearish on the euro versus the dollar. One-week volatility on the peso has climbed to the highest in more than four years, and its premium to expected swings further out in time widened to the highest since Bloomberg began compiling data in 2007.

Rates

Positioning in the Treasuries market over the past couple of weeks has been focused toward traders de-leveraging positions in futures, skewed toward long liquidations amid rising expectations of a post-election boost to fiscal stimulus, swelling the supply of Treasuries. The result has seen open interest, or the amount of positions held by traders, drop sharply in 10-year note futures since the start of October as yields have climbed.

The de-risking, or traders taking chips off the table, has also been reflected in the cash market, where the latest survey from JPMorgan Chase & Co. shows clients reducing both long and short positions, as neutrals rise. In the options market for Treasuries, tail-risk hedges sit at higher yields and a bigger bond market selloff versus current levels. The 109.50 December 10-year put is notably populated, equivalent to a yield of approximately 4.5% and around 25 basis points higher than current levels.

Advertisement 6

This advertisement has not loaded yet, but your article continues below.

Article content

“Election volatility premium is most pronounced in the bond market on long-end rates, which we believe reflects concerns over higher fiscal risks on a sweep outcome,” said Tanvir Sandhu, Bloomberg Intelligence’s chief global derivatives strategist. “The skew suggests demand for hedges using payer swaptions against a selloff in long-end rates.”

Crypto

Crypto traders are diverging on the election result, with the options market turning from aggressively bullish to a more hedge-focused approach. The implied volatility for short-term contracts such as the 14-day puts has risen significantly while calls with the same expiration remain stable, according to data compiled by crypto liquidity provider B2C2.

While there is no clear directional bias with heightened volatility going into the election, increasing premium for calls across longer tenors and termed Bitcoin futures on CME point to a bullish outlook beyond the election, with more rate cuts and potential positive changes in crypto policies in sight next year.

Cross-Asset

Binary options — in which a payout is triggered if a pair of conditions are met, such as a currency and a stock reaching pre-determined levels — tend to be a popular way to hedge possible outcomes around major events. Such trades have picked up going in the election, according to Esmail Afsah, a derivatives strategist at JPMorgan.

“I suspect this is mainly because investors have firm views on how individual assets are likely to behave in the four key permeations of the US election,” Afsah said. “Using hybrid options and betting on the direction of two assets concurrently allows to increase leverage materially and thus improve odds, providing of course that assets do indeed behave as expected.”

—With assistance from David Pan, Christian Dass, Jessica Menton and Jan-Patrick Barnert.