A week before Federal Reserve officials gather to reflect on the appropriate tempo of interest-rates cuts, three high-profile reports are set to show underlying resilience in the US economy and a temporary hiccup in job growth.

Author of the article:

Bloomberg News

Vince Golle and Craig Stirling

Published Oct 26, 2024 • 6 minute read

You can save this article by registering for free here. Or sign-in if you have an account.

ie9t237z6l{79}{h88b[f{9g_media_dl_1.pngBloomberg

Article content

(Bloomberg) — A week before Federal Reserve officials gather to reflect on the appropriate tempo of interest-rates cuts, three high-profile reports are set to show underlying resilience in the US economy and a temporary hiccup in job growth.

Friday’s employment report, expected to show a modest 110,000 increase in payrolls — about half this year’s average gain of 200,000 — will reflect hits to the labor market from two hurricanes as well as a work stoppage at aircraft maker Boeing Co. The unemployment rate is forecast to hold at 4.1%.

Advertisement 2

This advertisement has not loaded yet, but your article continues below.

THIS CONTENT IS RESERVED FOR SUBSCRIBERS ONLY

Subscribe now to read the latest news in your city and across Canada.

Exclusive articles from Barbara Shecter, Joe O’Connor, Gabriel Friedman, and others.

Daily content from Financial Times, the world’s leading global business publication.

Unlimited online access to read articles from Financial Post, National Post and 15 news sites across Canada with one account.

National Post ePaper, an electronic replica of the print edition to view on any device, share and comment on.

Daily puzzles, including the New York Times Crossword.

SUBSCRIBE TO UNLOCK MORE ARTICLES

Subscribe now to read the latest news in your city and across Canada.

Exclusive articles from Barbara Shecter, Joe O’Connor, Gabriel Friedman and others.

Daily content from Financial Times, the world’s leading global business publication.

Unlimited online access to read articles from Financial Post, National Post and 15 news sites across Canada with one account.

National Post ePaper, an electronic replica of the print edition to view on any device, share and comment on.

Daily puzzles, including the New York Times Crossword.

REGISTER / SIGN IN TO UNLOCK MORE ARTICLES

Create an account or sign in to continue with your reading experience.

Access articles from across Canada with one account.

Share your thoughts and join the conversation in the comments.

Enjoy additional articles per month.

Get email updates from your favourite authors.

THIS ARTICLE IS FREE TO READ REGISTER TO UNLOCK.

Create an account or sign in to continue with your reading experience.

Access articles from across Canada with one account

Share your thoughts and join the conversation in the comments

Enjoy additional articles per month

Get email updates from your favourite authors

Sign In or Create an Account

or

Article content

Economists expect Fed policymakers to discount these temporary factors and lower rates a quarter percentage point at their Nov. 6-7 meeting. While officials are confident that price pressures are generally abating, a separate report is forecast to show the central bank’s preferred gauge of underlying inflation accelerated at the end of September.

The personal consumption expenditures price index, excluding volatile food and energy costs, is seen rising 0.3%, the most in five months. The report on Thursday is also expected to show consumer spending and personal income strengthened in September from a month earlier, indicating momentum in the largest part of the economy.

What Bloomberg Economics Says:

“We expect October’s US payrolls report to show the first negative jobs print since December 2020, well below the consensus forecast of 120k. Much of the weakness is due to weather-related disruptions, but we also see a slowdown in cyclical sectors.”

—Anna Wong, Stuart Paul, Eliza Winger, Estelle Ou & Chris G. Collins. For full analysis, click here

On Wednesday, the government will also issue its first estimate of third-quarter gross domestic product, and forecasts call for a solid 3% annualized pace that would match growth seen in the previous three months. In addition to robust consumer spending, GDP was likely bolstered by a pickup in business outlays for equipment.

Top Stories

Get the latest headlines, breaking news and columns.

By signing up you consent to receive the above newsletter from Postmedia Network Inc.

Thanks for signing up!

A welcome email is on its way. If you don’t see it, please check your junk folder.

The next issue of Top Stories will soon be in your inbox.

We encountered an issue signing you up. Please try again

Article content

Advertisement 3

This advertisement has not loaded yet, but your article continues below.

Article content

Other reports this week include September job openings, third-quarter employment costs and October consumer confidence. The Institute for Supply Management will also release its October manufacturing index.

For more, read Bloomberg Economics’ full Week Ahead for the US

In Canada, GDP data will show if the economy is on track to hit the Bank of Canada’s forecast of 1.5% annualized growth in the third quarter. Officials previously estimated 2.8% growth but revised that down as they cut rates by 50 basis points on Oct. 23. Among appearances, Bank of Canada Governor Tiff Macklem and his colleague Carolyn Rogers will speak to lawmakers about that decision.

Elsewhere, the UK’s closely watched budget announcement, euro-zone inflation and growth numbers, the Bank of Japan’s rate decision and purchasing manager indexes showing the health of China’s economy will be among the highlights.

Click here for what happened last week and below is our wrap of what is coming up in the global economy.

Asia

China’s PMIs loom large in the coming week, with policymakers, economists and investors keen to gauge the current strength of the underperforming economy.

Advertisement 4

This advertisement has not loaded yet, but your article continues below.

Article content

It’s probably too soon to see if recent stimulus measures are having any initial impact, but if services and construction activity joins the factory sector in declining, calls for more efforts from Beijing are likely to mount.

The BOJ meets Thursday and is widely expected to keep interest rates unchanged. With renewed weakness in the yen likely on the mind of policymakers, market players will be looking out for any hawkish signals that suggest that the next hike is in the pipeline for December or not.

Elsewhere, Australia reports on price growth on Wednesday, with prices expected to slow, but likely not by enough to reignite near-term rate cut talk.

Indonesia and Pakistan also release inflation figures, while Hong Kong and Taiwan report on GDP.

PMIs from around Asia out Friday will give an indication of how the region’s economy is performing beyond China, as will trade figures from Thailand, Hong Kong, and South Korea.

For more, read Bloomberg Economics’ full Week Ahead for Asia

Europe, Middle East, Africa

The first glimpses of hard data that the European Central Bank will use to tailor its next easing move in December will be released this week, at a time when investors have increasingly priced in the chance of a half-point rate reduction.

Advertisement 5

This advertisement has not loaded yet, but your article continues below.

Article content

While signs of weakening are emerging, third-quarter GDP numbers on Wednesday are anticipated to show the economy sustained a 0.2% pace of growth, after buoyancy in Spain and steady expansion in France and Italy made up for a German recession.

Euro-zone inflation on Thursday is predicted by economists to have quickened slightly to 1.9%, just below the ECB’s 2% target, with Germany’s outcome even exceeding the goal.

Such results would conform to policymakers’ forecasts of a temporary pickup before price growth then settles around the goal in the first half of next year.

Elsewhere in Europe, Swiss inflation is predicted to have stayed steady at 0.8%, well below the central bank’s ceiling. Economists forecast a further rate cut in December.

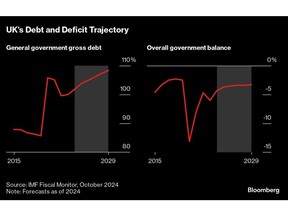

In the UK, Chancellor of the Exchequer Rachel Reeves will unveil the first budget of the newly elected Labour government on Wednesday, potentially one of Britain’s most significant fiscal announcements for years to come.

She faces a tight balancing act, with the International Monetary Fund advising a ramp-up in public investment, but also a push to repair its finances in the longer term.

Advertisement 6

This advertisement has not loaded yet, but your article continues below.

Article content

Reeves is poised to overhaul fiscal rules that could allow much more borrowing for capital spending, while she is also likely to target investors to raise the tax take.

South African Finance Minister Enoch Godongwana will present his own annual mid-term budget on Wednesday.

This will be the first since a multi-party government was formed with the centrist Democratic Alliance and eight other smaller rivals after the African National Congress lost its outright majority in May 29 elections.

Godongwana’s speech will be closely watched for news on efforts to rein in runaway state debt, new economic growth targets and how the government with back President Cyril Ramaphosa’s pledge to turn the country into a construction site — including details on a credit-guarantee facility to boost private sector involvement in the plan.

For more, read Bloomberg Economics’ full Week Ahead for EMEA

Latin America

The flash third-quarter economic output data from Mexico can be expected to show Latin America’s No. 2 economy is downshifting into year-end.

The consensus of analysts is that growth will slow for a third year in 2024 and likely yet again in 2025.

Advertisement 7

This advertisement has not loaded yet, but your article continues below.

Article content

Unemployment data for September will likely show a sixth straight rise. Even so, at just around 3%, joblessness is still well below its long-term average.

By contrast, September data should show Chile’s labor market is still operating with some degree of slack while copper output in the top-producing country will likely show that recovery from 20-year lows pushed ahead.

Peru watchers will be keen to see the core prints in October’s inflation report. Speaking after policymakers’ surprise Oct. 10 rate hold, central bank Chief Economist Adrian Armas cited core inflation, inflation expectations and economic growth as reasons to pause.

In Brazil, industrial output in September probably cooled from 2024’s torrid pace, the temperature of an already tight labor market ticked higher while budget figures headed deeper into the red.

Colombian policymakers on Thursday are all but certain to extend their current easing cycle to a longest-ever eighth straight meeting, trimming borrowing costs to as low as 9.5%. Analysts surveyed by the central bank don’t see a pause before 4Q 2025.

For more, read Bloomberg Economics’ full Week Ahead for Latin America

—With assistance from Paul Jackson, Robert Jameson, Monique Vanek, Laura Dhillon Kane, Tom Rees and Shiyin Chen.