It’s wrong to expect that a cycle of interest-rate cuts from the Federal Reserve will suddenly revive the green transition, according to Barry Norris, the founder and chief investment officer of UK hedge fund Argonaut Capital Partners.

Author of the article:

Bloomberg News

Sheryl Tian Tong Lee

Published Sep 29, 2024 • 4 minute read

You can save this article by registering for free here. Or sign-in if you have an account.

6l06pj5dluo3tpv8gpudy1s{_media_dl_1.pngBloomberg

Article content

(Bloomberg) — It’s wrong to expect that a cycle of interest-rate cuts from the Federal Reserve will suddenly revive the green transition, according to Barry Norris, the founder and chief investment officer of UK hedge fund Argonaut Capital Partners.

“For the last few years, energy-transition insiders believed that the problems in the industry stemmed purely from high interest rates,” Norris said in an interview. “Interest rates are now falling, so logically sentiment in this part of the market should be better. Instead, the insiders are going back to governments asking for more subsidies.”

Advertisement 2

This advertisement has not loaded yet, but your article continues below.

THIS CONTENT IS RESERVED FOR SUBSCRIBERS ONLY

Subscribe now to read the latest news in your city and across Canada.

Exclusive articles from Barbara Shecter, Joe O’Connor, Gabriel Friedman, and others.

Daily content from Financial Times, the world’s leading global business publication.

Unlimited online access to read articles from Financial Post, National Post and 15 news sites across Canada with one account.

National Post ePaper, an electronic replica of the print edition to view on any device, share and comment on.

Daily puzzles, including the New York Times Crossword.

SUBSCRIBE TO UNLOCK MORE ARTICLES

Subscribe now to read the latest news in your city and across Canada.

Exclusive articles from Barbara Shecter, Joe O’Connor, Gabriel Friedman and others.

Daily content from Financial Times, the world’s leading global business publication.

Unlimited online access to read articles from Financial Post, National Post and 15 news sites across Canada with one account.

National Post ePaper, an electronic replica of the print edition to view on any device, share and comment on.

Daily puzzles, including the New York Times Crossword.

REGISTER / SIGN IN TO UNLOCK MORE ARTICLES

Create an account or sign in to continue with your reading experience.

Access articles from across Canada with one account.

Share your thoughts and join the conversation in the comments.

Enjoy additional articles per month.

Get email updates from your favourite authors.

Sign In or Create an Account

or

Article content

It’s a view that flies in the face of the conventional wisdom currently making the rounds across much of Wall Street, with analysts at Citigroup Inc. and Goldman Sachs Group Inc. among those declaring that a turning point has been reached for green stocks. They point to examples like wind-farm operator Orsted A/S, up 20% this year, and Siemens Energy AG, which has gained an eye-popping 174%.

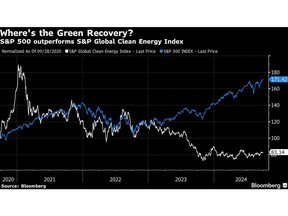

But there are also plenty of green stocks that continue to struggle. Vestas Wind Systems A/S is down 30% this year, after higher costs from servicing installed turbines ate into profits. Meanwhile, Vestas and other European turbine manufacturers are losing ground in India’s growing wind market, according to BloombergNEF. And the S&P Global Clean Energy Index has lost roughly 6% since the end of December, compared with a more than 20% gain in the S&P 500.

Find Out More: Merryn Talks Money With Barry Norris: ‘Moral Case’ For Fossil Fuels (Podcast)

Despite recent gains in some green stocks, the overall sector remains far off the heights reached during the pandemic, when environmental, social and governance investing was all the rage amid an energy crisis and emergency interest rate cuts. From a peak reached at the start of 2021, S&P’s index of clean-energy stocks has since lost more than half its value.

Top Stories

Get the latest headlines, breaking news and columns.

By signing up you consent to receive the above newsletter from Postmedia Network Inc.

Thanks for signing up!

A welcome email is on its way. If you don’t see it, please check your junk folder.

The next issue of Top Stories will soon be in your inbox.

We encountered an issue signing you up. Please try again

Article content

Advertisement 3

This advertisement has not loaded yet, but your article continues below.

Article content

Norris says he’s fundamentally skeptical toward the basic premise of the green transition and posits that if capitalism had been left to its own devices, most green companies would never have been born.

It’s a view that feeds into a wider shift in rhetoric among the titans of private finance, as pandemic-era enthusiasm for the green transition is replaced by language keenly focused on generating profits.

Meanwhile, there’s also been a tendency toward slippage in definitions for green concepts such as “transition,” with some financial professionals now choosing to add coal assets to the mix.

Norris points to Europe as proof that policies forcing the private sector to embrace the green transition come at an economic cost, with companies in the region consistently seeing lower valuations than their US peers. The Stoxx Europe 600 has gained only half as much as the S&P 500 this year. And over the past five years, European stock valuations have grown roughly a third as much as their US counterparts.

“Look at what’s going on in the European car industry at the moment,” Norris said. “It will end in the hollowing out of the European industrial base.”

Advertisement 4

This advertisement has not loaded yet, but your article continues below.

Article content

He rejects the notion that ratcheting up subsidies to help compete with China would make green investments more palatable in the West.

“If the energy transition created better, more useful products,” then there wouldn’t be any need for subsidies, Norris said.

In the US, the Biden administration’s landmark climate bill — the 2022 Inflation Reduction Act — may unleash as much as $3.3 trillion in spending, analysts at Goldman Sachs have estimated. The European Union has also pledged to pour money into the green transition, including a plan to raise €1 trillion ($1.1 trillion) from public and private sources.

That’s still less than the subsidies funneled into the global fossil-fuel industry, with International Monetary Fund figures showing that oil, gas and coal received $7 trillion in global subsidies as recently as 2022, with $1.3 trillion of that in the form of direct government support.

Meanwhile, there’s growing evidence that unless more private finance is channeled into the green economy, humans will fail to rein in greenhouse gas emissions, pushing global warming beyond the critical threshold of 1.5C. And while asset owners such as pension funds and insurers are stepping up efforts to align their portfolios with global climate goals, there’s little evidence that the rest of the global finance industry is doing the same.

Advertisement 5

This advertisement has not loaded yet, but your article continues below.

Article content

Norris says his key concern is that green companies only appear to be viable when they don’t have to contend with normal startup costs.

“Everywhere and always the energy transition requires zero cost of capital, government subsidies and coercion of better products to survive,” he said. “This results in anemic economic growth because so much national resource is being misallocated to activities which are economically backward.”

He warns that continued funneling of resources into the green transition will backfire, leading voters to eject politicians backing policies that favor renewable energy.

In Norris’s view, “the energy transition is failing and will fail.”

If the green transition weren’t so reliant on subsidies, Norris says “hedge funds would be more enthusiastic.”