Valeriy Shevchenko was getting ready to move into a new three-room apartment in Berlin’s upscale Prenzlauer Berg district before disaster struck. More than a year later, it’s still unfolding as part of the turmoil in German housing.

Author of the article:

Bloomberg News

Libby Cherry and Laura Malsch

Published Sep 21, 2024 • 5 minute read

You can save this article by registering for free here. Or sign-in if you have an account.

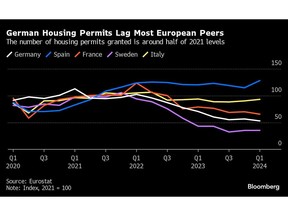

30ay7b0tbnqekq3es1tajgf7_media_dl_1.pngEurostat

Article content

(Bloomberg) — Valeriy Shevchenko was getting ready to move into a new three-room apartment in Berlin’s upscale Prenzlauer Berg district before disaster struck. More than a year later, it’s still unfolding as part of the turmoil in German housing.

Project Immobilien-Gruppe, the developer of the multi-family residential building where Shevchenko had bought a unit, went bankrupt, leading to a halt in construction just a few months before the family of three was supposed to move in.

Advertisement 2

This advertisement has not loaded yet, but your article continues below.

THIS CONTENT IS RESERVED FOR SUBSCRIBERS ONLY

Subscribe now to read the latest news in your city and across Canada.

Exclusive articles from Barbara Shecter, Joe O’Connor, Gabriel Friedman, and others.

Daily content from Financial Times, the world’s leading global business publication.

Unlimited online access to read articles from Financial Post, National Post and 15 news sites across Canada with one account.

National Post ePaper, an electronic replica of the print edition to view on any device, share and comment on.

Daily puzzles, including the New York Times Crossword.

SUBSCRIBE TO UNLOCK MORE ARTICLES

Subscribe now to read the latest news in your city and across Canada.

Exclusive articles from Barbara Shecter, Joe O’Connor, Gabriel Friedman and others.

Daily content from Financial Times, the world’s leading global business publication.

Unlimited online access to read articles from Financial Post, National Post and 15 news sites across Canada with one account.

National Post ePaper, an electronic replica of the print edition to view on any device, share and comment on.

Daily puzzles, including the New York Times Crossword.

REGISTER / SIGN IN TO UNLOCK MORE ARTICLES

Create an account or sign in to continue with your reading experience.

Access articles from across Canada with one account.

Share your thoughts and join the conversation in the comments.

Enjoy additional articles per month.

Get email updates from your favourite authors.

Sign In or Create an Account

or

Article content

The site still sat abandoned a year later, leaving the Shevchenkos in limbo. Not only are they stuck in their rental indefinitely, but their €250,000 ($278,340) initial payment — about half of the apartment’s total cost — is tied up in the insolvency process. Now, on top of their rent, they’re covering interest on the loan they took out to finance the down payment.

“It was a depressing few days after we got the news,” said Shevchenko, a 34-year-old software engineer who moved to Berlin from Russia in 2017. He feels let down not only by the developer, but also by politicians, who he thinks should better protect homebuyers. “I didn’t think something like this was possible in Germany,” he said.

Half-finished shells of would-be homes have become a regular sight across the country. More than 1,000 companies involved in real estate activities have collapsed since 2022 as part of the fallout from surging construction costs and the rapid interest-rate hikes undertaken by central banks.

While those dynamics are widespread, the impact in Germany has been particularly severe because of the amount of capital that was invested in a market long considered one of the safest in Europe. Yield-hungry pension funds and major landlords piled in to finance developments and purchase residential portfolios, driving up housing prices.

Top Stories

Get the latest headlines, breaking news and columns.

By signing up you consent to receive the above newsletter from Postmedia Network Inc.

Thanks for signing up!

A welcome email is on its way. If you don’t see it, please check your junk folder.

The next issue of Top Stories will soon be in your inbox.

We encountered an issue signing you up. Please try again

Article content

Advertisement 3

This advertisement has not loaded yet, but your article continues below.

Article content

Ambitious acquisitions at high prices were fueled by plentiful cheap debt from both bond markets and banks. Unlike most other European countries, German developments could be undertaken with “little or (almost) no equity,” according to a presentation from PwC. This high leverage meant they were particularly vulnerable when construction costs surged and financing dried up.

“We’ve seen a lot of situations where people had basically borrowed against the land from banks to get planning but haven’t done anything,” said Zach Vaughan, chief investment officer of real estate at Arrow Global, an investor in distressed assets. “Banks are sitting on a large loan and you can’t even pre-sell the apartments because the development company is essentially gone.”

The lack of affordable living space has fueled frustration, which has spilled over into anti-immigrant sentiment as migrants are blamed by many voters for worsening the housing crunch. On Sunday, the far-right Alternative for Germany is projected to win the state election in Brandenburg, the state that surrounds Berlin, while governing parties are likely to slump. It would be the party’s second victory in a regional election after Thuringia earlier this month.

Advertisement 4

This advertisement has not loaded yet, but your article continues below.

Article content

Stalled building sites are a totem of the difficulties faced by Germany’s government to promote new construction in a market that’s not keeping up with demand. Chancellor Olaf Scholz’s coalition has fallen far short on its promise to build at least 400,000 homes a year. Deutsche Bank economists forecast that just 260,000 units will be completed in 2024 and 265,000 in 2025.

“The crisis in residential construction will drag on for a long time,” said Klaus Wohlrabe, a senior economist at Germany’s Ifo Institute, whose monthly surveys show sentiment in the sector near record-low levels. “Companies are still looking for signs of hope.”

Construction saw the biggest decline of any sector in terms of gross value added to the economy last quarter, and the slowdown is adding headwinds to Germany’s already beleaguered economy. Ripple effects are also showing up in associated industries, from furniture makers to chemicals producers.

Smaller construction firms will be hit especially hard by the recent drop in new orders, according to René Hagemann, deputy managing director of German construction association HDB, noting that decreasing interest rates alone will not be enough to revive the sector. “Above all, investors need long-term stability and that is not the case at the moment,” he added.

Advertisement 5

This advertisement has not loaded yet, but your article continues below.

Article content

“Germany will continue to be one of the laggards across European real estate,” said Christian Fladeland, co-chief executive officer of Heimstaden Bostad, a Sweden-based landlord that own buildings from the UK to Poland, including nearly 30,000 homes in Germany. “It’s become more expensive to build new construction and the significant imbalances in the residential market are accelerating.”

The pain is especially acute for people like the Shevchenkos, who signed purchase contracts in good faith but have little recourse other than to wait and hope. The insolvency process is set up to pay off creditors as quickly as possible and is ill-suited for restructuring building projects, which require hefty investment before any money can be earned.

“Families who bought the apartment to live there — perhaps they even had to move out of their old apartment – it’s a lot of personal stress if it’s not possible to finish these projects,” said Volker Böhm at law firm Schultze & Braun, who is acting as insolvency administrator for Project Immobilien.

While many administrators like Böhm aim to finish the projects, making it work is a challenge. Securing fresh funds to pay contractors and buy materials can be expensive and existing creditors are often unwilling to put in good money after bad. Sometimes the burden can even fall on the prospective homebuyers themselves to stump up additional funds.

Advertisement 6

This advertisement has not loaded yet, but your article continues below.

Article content

For some investors, these half-built sites can pose an attractive opportunity to pick up projects relatively cheaply and benefit from a tight market in the future. Arrow Global, for instance, bought property developer Interboden out of insolvency in June with the intention to not only finish its pipeline of projects but also to take on other sites in need of fresh cash.

“What we’ve been seeing is numerous stranded projects — fundamentally good projects at various stages — with some partially or nearly complete where the developers had just run out of financing,” said Arrow’s Vaughan.

It’s not only developments that are in need of fresh investment. Much of Germany’s existing housing stock was built in the 1970s or earlier and needs upgrades. Many landlords have scaled back on capital expenditures to conserve cash, but improvements are increasingly unavoidable, particularly with regulations for energy efficiency.

“A lot of German housing stock is quite dated and needs significant investment to get energy ratings from abysmal to acceptable,” said Ben Bianchi, head of Europe for Oaktree Capital Management’s real estate group, who is looking to buy up residential portfolios from cash-strapped landlords for renovation.

In the meantime, the market continues to tighten. With few incentives for kicking off new housing developments, the gap between the price of new and existing homes is widening, one indicator of intensifying scarcity of new builds.

That means little prospect for relief for would-be home buyers like the Shevchenkos. Their project was picked up by a new contractor in spring, but construction didn’t restart this summer as hoped.

“I’m really worried that they will drop out too as soon as they realize that finishing this isn’t as profitable as they want it to be,” Shevchenko said.