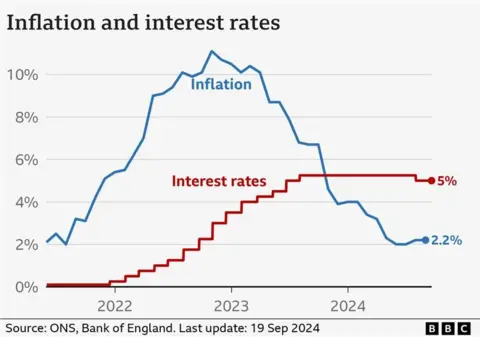

The Bank of England has said it should be able to cut interest rates “gradually over time” as it decided to hold borrowing costs at 5%.

The decision comes as prices continue to rise slightly faster than the Bank’s target, with inflation remaining at 2.2% last month.

Bank boss Andrew Bailey said it was “vital” that inflation remains low. “So we need to be careful not to cut too fast or by too much,” he said.

Experts are predicting the Bank will cut rates further in November.

The decision to hold interest rates, which was widely expected, follows a cut from 5.25% in August – the first reduction since the onset of the pandemic in 2020.

Just one member of the Bank’s nine-member rate-setting committee voted for a cut.

The base interest rate dictates the rates set by High Street banks and lenders.

The higher level has meant people are paying more to borrow money for things like mortgages and credit cards, but savers have also received better returns.

Higher interest rates push mortgage rates up. This can result in landlords raising their rent to cover higher repayments.

Rising rent forced us to move somewhere smaller

James and his wife Sofia are among those affected. They moved with their one-year-old son to Berkshire after their rent went up by £100 a month to £1,650 in May 2024.

They moved to a smaller terraced house where they are paying £1,400. They have a joint income of £54,000 and say they cannot save for a deposit to buy a house.

Sofia said: “When I went on maternity leave, I could only go off for about 10 weeks because we just couldn’t afford any more. Even that was a major stretch to the point where we had to put ourselves into a bit of debt.”

She said food banks helped them and sometimes her husband had to work from home as he did not have the money to fuel the car.

The Bank said the decision to hold this month was “guided by the need to squeeze persistent inflationary pressures” out of the UK economy.

It expects inflation to rise to around 2.5% towards the end of this year, but it also suggested the country’s economic picture was improving.

It said it had received reports of a “improving real incomes” and added mortgage approvals had increased to their highest level since September 2022 – the month of former Prime Minister Liz Truss’s infamous mini-Budget, which led to soaring mortgage rates.

While the impact of two giant global shocks – the pandemic and the Ukraine war – have died down, prices are still rising faster than the Bank’s 2% target.

And inflation is likely to tick up further over the course of the rest of the year.

The economic recovery is also muted. The strong growth in the first half of the year has slowed, with consumers holding back due to high prices.

The Bank warned while there was “improved sentiment and expectations” of increased economic growth, it expected weaker expansion of 0.3% between July and September, down from 0.4%.

The UK has had sluggish economic growth in recent years, something which the new Labour government has pledged it will change.